The Yield Landscape in 2026

The UK's average gross rental yield sits at approximately 5.8% — a number that is simultaneously encouraging and utterly meaningless. National averages obscure a property market that is fundamentally fragmented. A terraced house in Sunderland and a one-bed flat in Kensington exist in the same country but operate in entirely different financial universes.

For investors who prioritise cash flow over capital appreciation — and in a 5% base rate environment, that should be most of you — the question is not "is property still a good investment?" It is "where exactly do I need to buy, and what do I need to buy, to achieve a yield that actually works after all costs?"

This analysis is built from current rental data, regional pricing trends, and the operational reality of managing high-yield assets. We are going to move past the generic "best places to invest" lists and get into the specifics that determine whether a property will generate real income or just look good on a spreadsheet.

Gross Yield vs Net Yield: The Number That Actually Matters

Before we examine locations, we need to establish a common language. The property industry has a persistent credibility problem with yield figures, and it starts with the difference between gross and net.

Gross Yield = (Annual Rental Income ÷ Property Purchase Price) × 100

Net Yield = ((Annual Rental Income − Annual Operating Costs) ÷ (Property Purchase Price + Acquisition Costs)) × 100

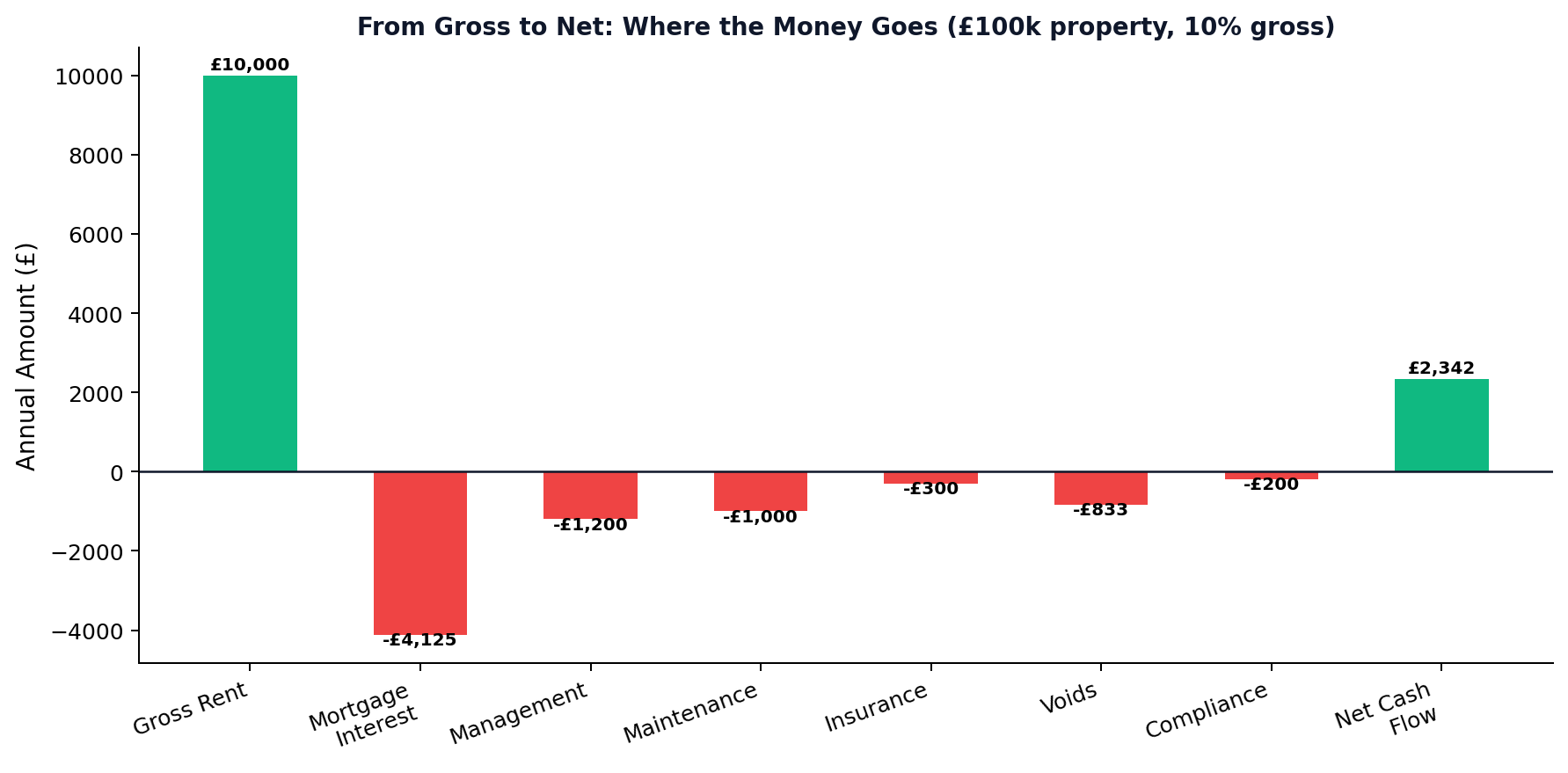

A property advertised at a 10% gross yield might deliver a 5% net yield once you factor in:

| Cost Category | Typical Annual Amount | Impact on £100k Property at 10% Gross |

|---|---|---|

| Mortgage interest (75% LTV at 5.5%) | £4,125 | -4.1% |

| Management fees (12% of rent) | £1,200 | -1.2% |

| Maintenance & repairs | £1,000 | -1.0% |

| Insurance (landlord) | £300 | -0.3% |

| Void periods (1 month) | £833 | -0.8% |

| Regulatory compliance | £200 | -0.2% |

| Total Operating Costs | £7,658 | -7.6% |

| Net Yield (pre-tax) | 2.4% |

That £10,000 gross rent just became £2,342 in actual cash flow. And we have not yet accounted for income tax, Section 24 restrictions, or capital expenditure.

The lesson: Never make an investment decision based on gross yield alone. A property that achieves 7% gross in a well-managed area will almost always outperform an 11% gross property in a high-maintenance, high-void area.

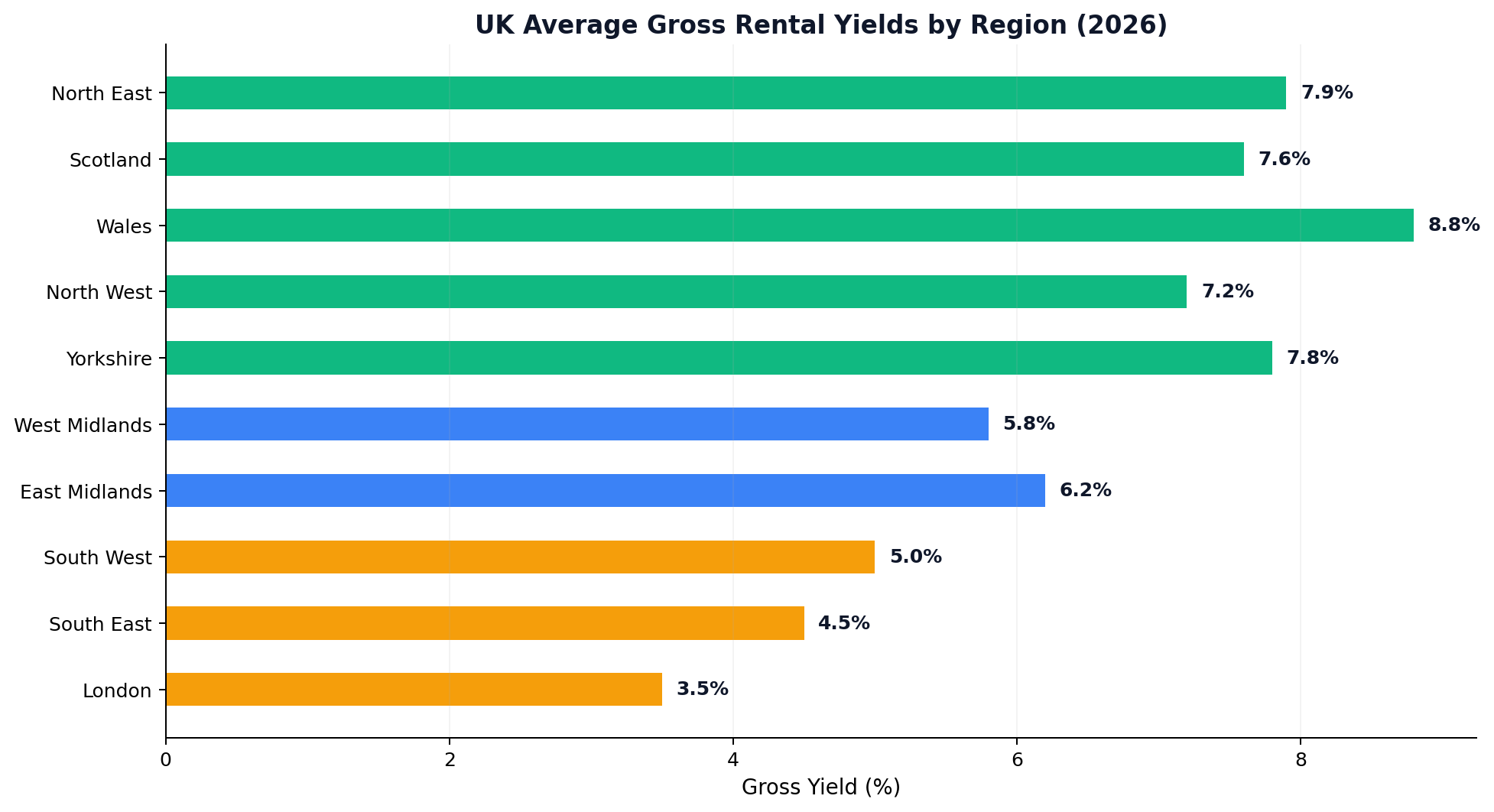

The Regional Yield Map: Where the Numbers Work

Tier 1: The 8%+ Gross Zone

North East England — Average Gross Yield: 7.9%

The North East consistently delivers the UK's highest rental yields, driven by a simple formula: average property prices of £114,098 combined with average monthly rents of £748. The region's economy has historically been dependent on manufacturing and public sector employment, but significant investment in technology, healthcare, and the service sector is diversifying the tenant base.

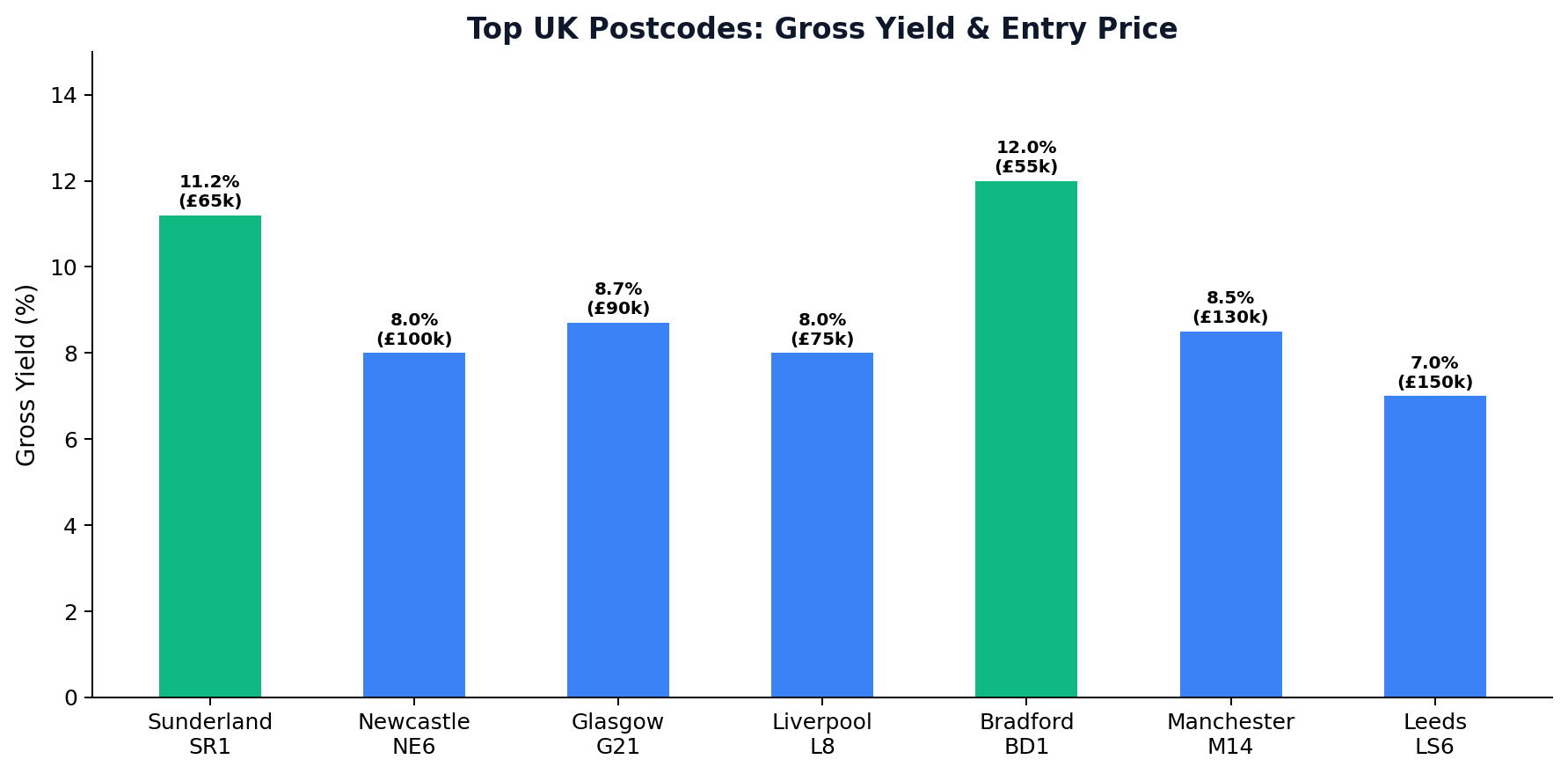

Sunderland (SR1): The standout postcode, delivering gross yields of up to 11.2%. Entry prices for terrace houses start at £55,000–£75,000. Rental demand is driven by the University of Sunderland (15,000+ students) and the Nissan manufacturing plant (6,000+ employees). However, capital appreciation has been flat or modest — this is a pure cash flow play.

Newcastle (NE4, NE6): More balanced proposition combining yields of 7–8.5% with genuine capital growth potential. The £350m Stephenson Quarter regeneration and the expanding tech corridor around Science Central are driving both tenant demand and property values. Entry prices: £80,000–£130,000 for yielding assets.

Scotland — Average Gross Yield: 7.6%

Scotland operates under different legislation (the Private Residential Tenancy replaces ASTs), different tax treatment (Land and Buildings Transaction Tax rather than SDLT), and — critically for high-yield investors — different licensing requirements for HMOs.

Glasgow: The strongest performing city in the UK by some metrics, delivering average yields of 7.25–9.3% depending on the data source and methodology. Glasgow's combination of four major universities, a growing financial services sector, and average property prices significantly below the UK average creates an almost uniquely favourable yield environment. Entry prices: £80,000–£150,000 for yielding flats.

Belfast: Matching Glasgow's top yields at 9.3% in recent assessments, with the UK's lowest price-to-earnings ratio. The city benefits from a young, growing population and significant tech investment (including operations from PwC, Deloitte, and Citi). Northern Ireland also has its own property tax regime, which can be more favourable for investors.

Wales — Average Gross Yield: 8.83% (Q4 2026)

Wales recorded the UK's strongest annual rental growth in Q4 2026, driven by limited housing supply and growing demand in cities like Swansea (7.0% gross yield) and Cardiff. The Renting Homes (Wales) Act 2019 introduced a distinct regulatory framework that investors must understand — it offers enhanced tenant protections but also clearer landlord obligations.

Tier 2: The 6–8% Sweet Spot

North West England — Average Gross Yield: 6.8–7.8%

The North West combines strong yields with genuine capital growth — a combination that is increasingly rare in the UK market.

Manchester (M14 — Fallowfield/Rusholme): The UK's highest-yielding urban postcode at 12% gross, driven by a student population exceeding 100,000 across the University of Manchester and Manchester Metropolitan. However, this headline figure masks operational complexity — student lets have higher void periods (summer months), turnover costs, and management requirements.

Liverpool: Postcodes in the L1, L3, and L8 areas consistently deliver 7–8.5% yields with entry prices from £65,000 for studio and one-bed flats. The Liverpool Waters regeneration (£5.5 billion over 30 years) is the largest single development in UK history and is expected to add significant upward pressure on both rents and values.

Yorkshire and the Humber — Average Gross Yield: 7–8.6%

Bradford (BD1): Delivering up to 12% gross yield with entry prices among the UK's lowest (terraces from £50,000). Bradford's massive city-centre regeneration programme and its designation as a UNESCO City of Film are slowly improving the area's reputation, but investors must be prepared for higher management costs and more challenging tenant demographics.

Leeds (LS3, LS6): Yields of 6.5–8% in areas close to the universities and city centre, with stronger capital growth fundamentals than Bradford. Leeds' financial and legal sectors provide a professional tenant base that reduces void risk.

Tier 3: The 4–6% Growth Zone

South East and London — Average Gross Yield: 3.5–5.5%

These regions are capital appreciation plays, not yield investments. However, specific micro-markets buck the trend:

- Barking, London (IG11): 7.2% gross yield — the highest in London — with entry prices of £250,000–£300,000 for two-bed flats.

- Thamesmead (SE28): 6.4% with the additional upside of Peabody's 30-year regeneration masterplan.

- East Ham (E6): 6% yield combined with 22% price growth over five years.

Property Types: What Yields the Most

Houses in Multiple Occupation (HMOs)

Average UK HMO yield: 8.61% (Q4 2026) North East HMO yield: up to 15.1%

HMOs are the highest-yielding mainstream property strategy in the UK because they generate multiple rental streams from a single asset. A four-bed terrace that might achieve £750/month as a single let can generate £1,600–£2,400/month as a four-room HMO.

However, the operational burden is significant:

- Mandatory licensing in all local authorities for properties with 5+ tenants forming 2+ households. Many councils now require additional licensing for smaller HMOs. Licence fees range from £500–£1,500 per property, renewable every five years.

- Article 4 directions in many urban areas now require planning permission to convert a C3 dwelling to a C4 HMO (use class change). Cities including Leeds, Manchester, Nottingham, and Bristol have implemented Article 4, restricting supply and driving up existing HMO values.

- Management intensity is three to five times higher than a single let. Communal areas require cleaning, utility bills are the landlord's responsibility, and tenant turnover is higher.

- Fire safety requirements include interlinked smoke/heat detectors, fire doors to all rooms and kitchens, emergency lighting, fire blankets, and clear escape routes. Non-compliance is a criminal offence.

The verdict: HMOs are not passive investments. They are a business. If you are willing to operate them (or pay 15–18% management fees for specialist HMO management), the returns justify the effort. If you want passive income, look elsewhere.

Student Lets

Student accommodation lets are a subset of HMOs that benefit from predictable annual demand cycles (September intake), guaranteed income (often underwritten by parental guarantors), and location premiums near university campuses.

The risk is concentration: if a university reduces its intake, merges departments, or shifts to online delivery, your demand base evaporates. Always target properties within walking distance of multiple universities or colleges, not just one.

Terraced Houses and Flats

For non-HMO investors, terraced houses consistently deliver the strongest yields across England and Wales, followed by flats. Detached houses have the lowest rental yields due to their higher purchase prices relative to achievable rents. The sweet spot for single-let yield is a two-bed terrace in a Northern city — affordable to purchase, easy to let, and low maintenance.

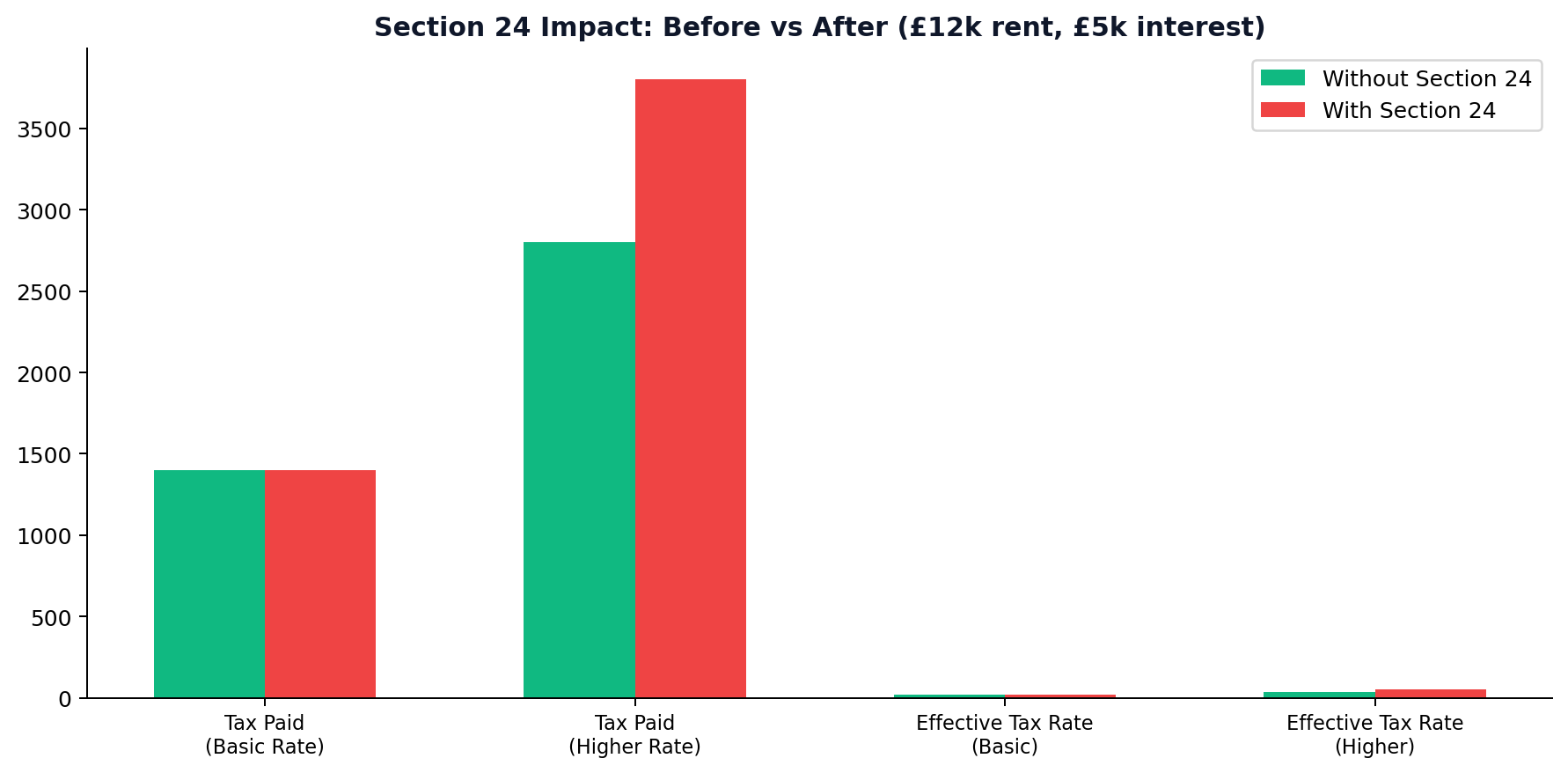

The Section 24 Reality Check

No analysis of UK rental yields is complete without addressing Section 24 — the tax change that has fundamentally reshaped the economics of buy-to-let.

Since April 2020, landlords holding property personally can no longer deduct mortgage interest from their rental income. Instead, they receive a 20% tax credit on the interest paid. For basic rate taxpayers, this is largely neutral. For higher and additional rate taxpayers, it creates a phantom profit — you pay tax on income you never received.

Example: Section 24 Impact on a High-Yield Property

| Metric | Without Section 24 | With Section 24 |

|---|---|---|

| Annual Rent | £12,000 | £12,000 |

| Mortgage Interest | £5,000 | £5,000 |

| Taxable Income | £7,000 | £12,000 |

| Tax at 40% | £2,800 | £4,800 |

| Tax Credit (20% of £5k) | – | (£1,000) |

| Actual Tax Paid | £2,800 | £3,800 |

| Effective Tax Rate on Net Income | 40% | 54% |

The solution for most portfolio landlords is to hold properties in a limited company (SPV), which pays Corporation Tax at 19–25% and can deduct mortgage interest in full. In Q4 2024, approximately 75% of new BTL purchases were made through limited companies. The trade-off: corporate mortgage rates are typically 0.5–1% higher, and extracting profits from the company triggers additional dividend tax.

Building a High-Yield Portfolio: The Strategic Framework

Step 1: Define Your Yield Target

Work backwards from your required net income:

- Determine your target monthly cash flow (e.g., £500/property/month)

- Add operating costs (management, maintenance, voids, insurance)

- Add mortgage costs at current rates

- The total gives you the gross yield threshold your target market must achieve

For most leveraged investors in the current rate environment, properties need to achieve 7%+ gross yield to deliver meaningful monthly cash flow.

Step 2: Choose Your Market

Based on the data above, the optimal markets for high-yield investment in 2026 are:

- North East England — highest yields, lowest entry prices, improving economic fundamentals

- Glasgow/Belfast — strong yields with distinct regulatory environments

- North West England — best combination of yield and capital growth

- Yorkshire — Bradford for pure yield, Leeds for balanced returns

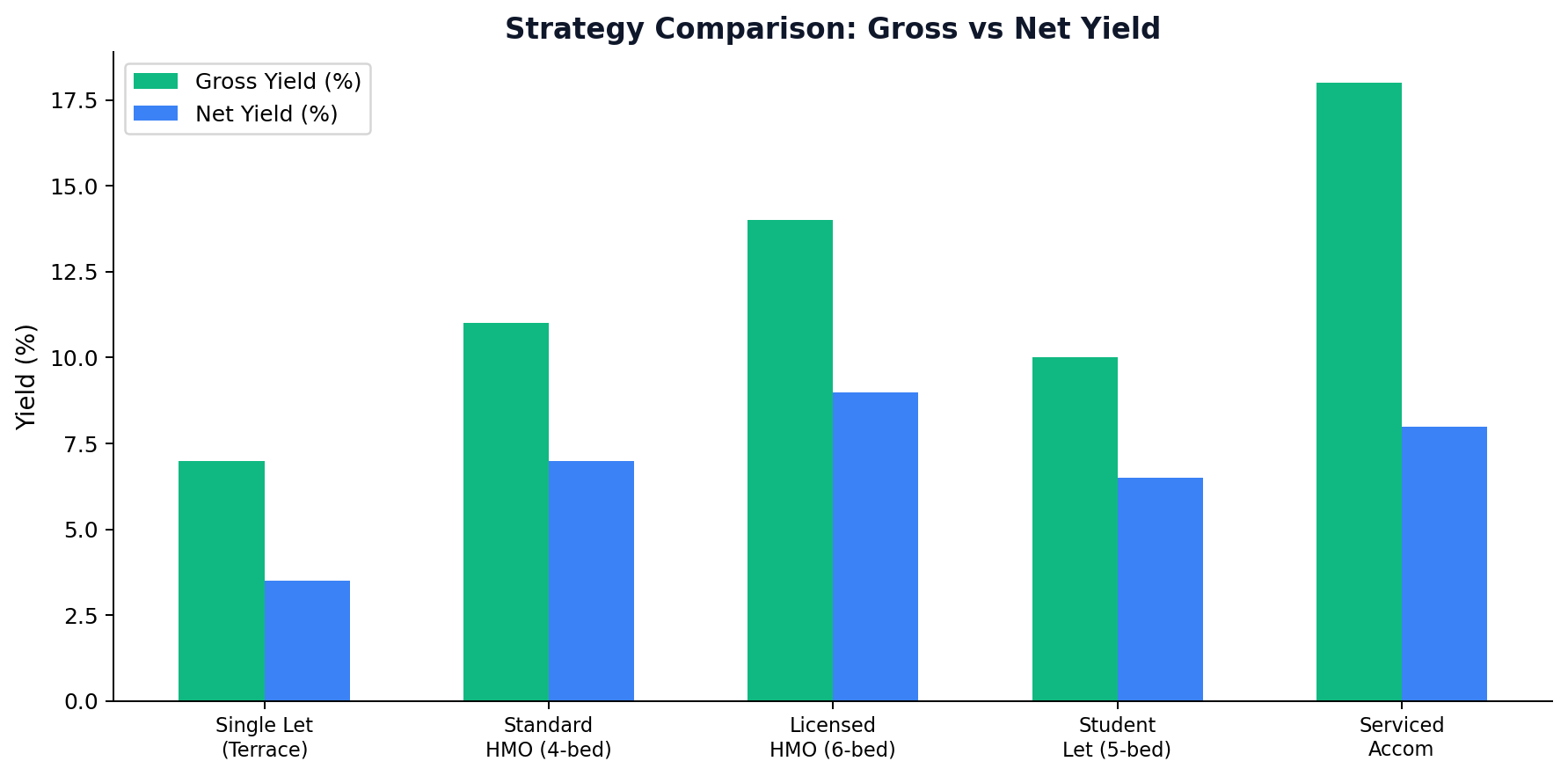

Step 3: Choose Your Strategy

| Strategy | Typical Gross Yield | Management Intensity | Capital Required | Best For |

|---|---|---|---|---|

| Single Let (Terrace) | 6–8% | Low | £50–130k | Passive investors |

| HMO (Licensed) | 10–15% | High | £100–200k | Active operators |

| Student Let | 8–12% | Medium | £80–150k | Experienced landlords |

| Serviced Accommodation | 15–25% gross | Very High | £100–200k | Full-time operators |

Step 4: Model Conservatively

Use a 6% mortgage rate for stress testing (even if current rates are lower), assume one month void per year, and budget 10% of annual rent for maintenance. If the numbers still work under these assumptions, the investment has genuine resilience.

Conclusion: Yield Is Not the Whole Story

The highest-yielding property in the UK is meaningless if it sits empty for three months, attracts unreliable tenants, or requires constant maintenance. Yield must be assessed alongside tenant quality, void risk, capital appreciation potential, and management practicality.

The smartest investors in 2026 are not chasing the highest number on a spreadsheet. They are building portfolios that blend high-yield Northern assets (for cash flow) with growth-oriented Southern or urban assets (for long-term wealth). This barbell approach delivers income today and capital tomorrow.

Next Steps:

- Calculate the net yield threshold you need based on your current mortgage rates and tax position.

- Research specific postcodes in the North East and North West using Rightmove rental data to verify achievable rents.

- Decide whether your management capacity supports HMO or single-let strategies before committing capital.

📚 Related Reading

- Off Plan Property for Sale UK: The 2026 Investor's Playbook

- Investing in UK Property from Overseas: The Complete 2026 Framework

- Best Type of Property to Invest in UK: A No-Nonsense Breakdown of Every Strategy in 2026

- How Environment Affects Business Success

- How I save nearly £2,000 a Year on Groceries for a Family of 4

Stop being a landlord. Start being an investor.

Shaded Canvas introduces serious capital to vetted UK property opportunities — targeting 12–16% net returns.

Start Investing →