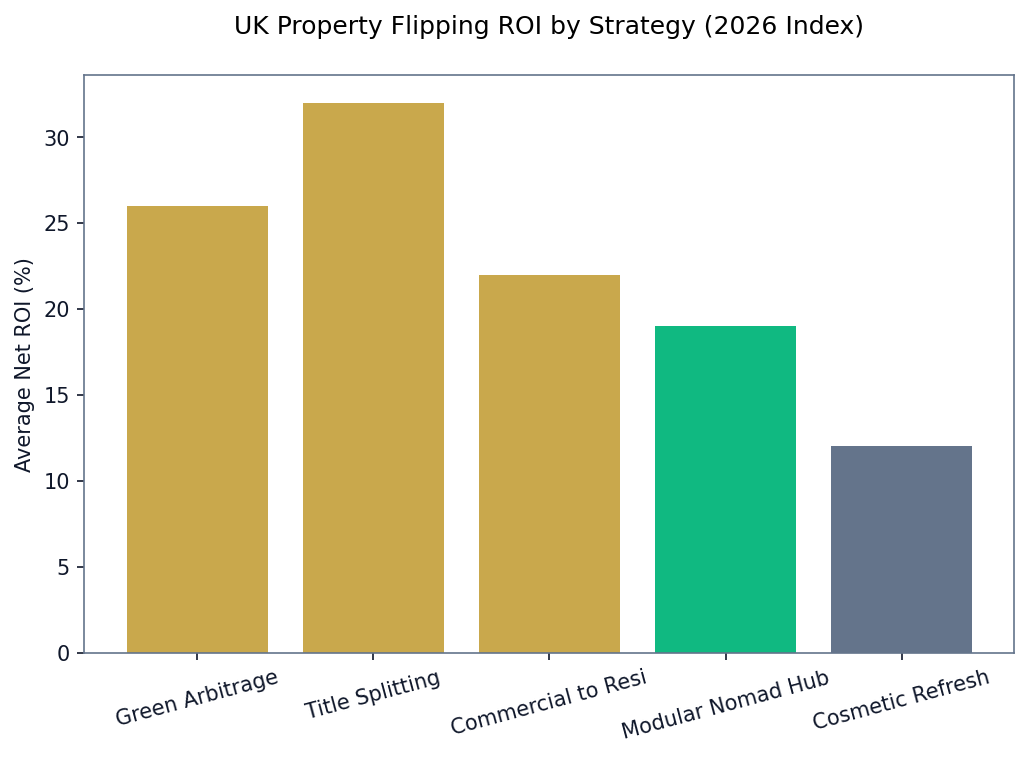

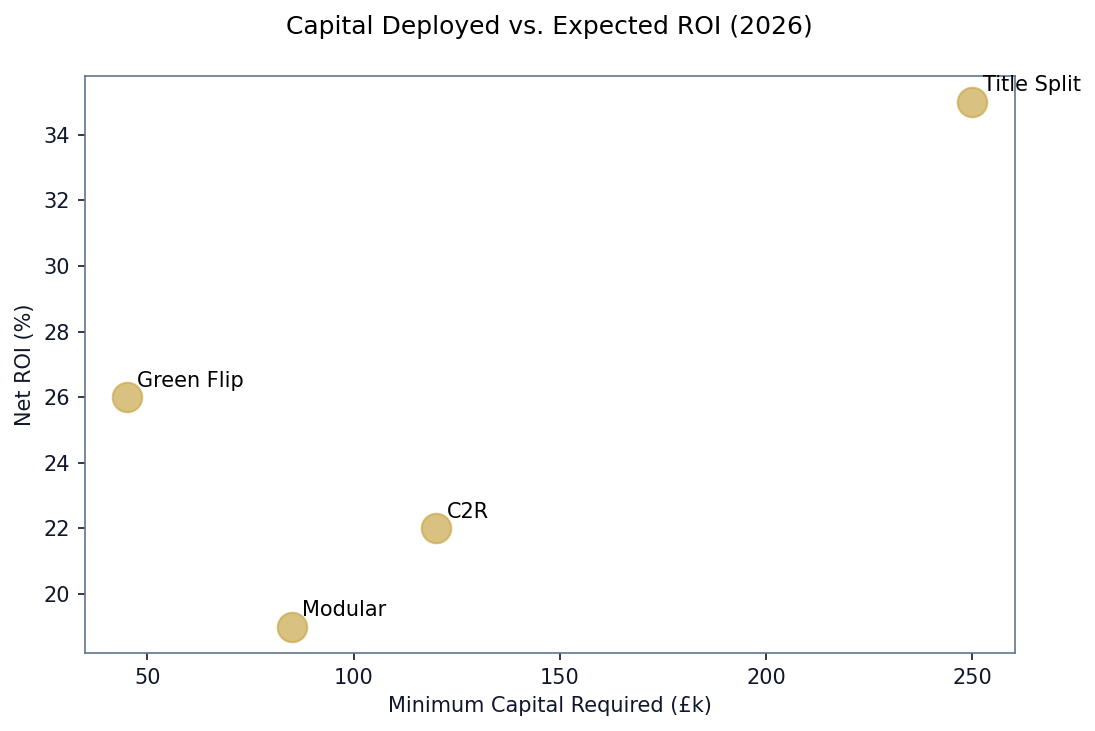

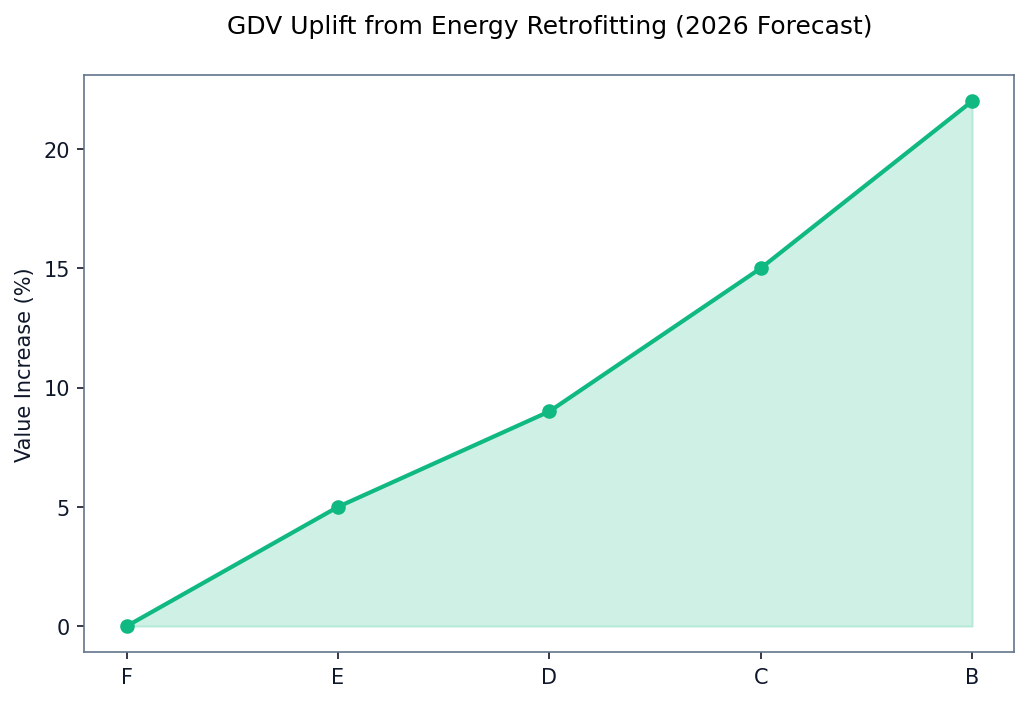

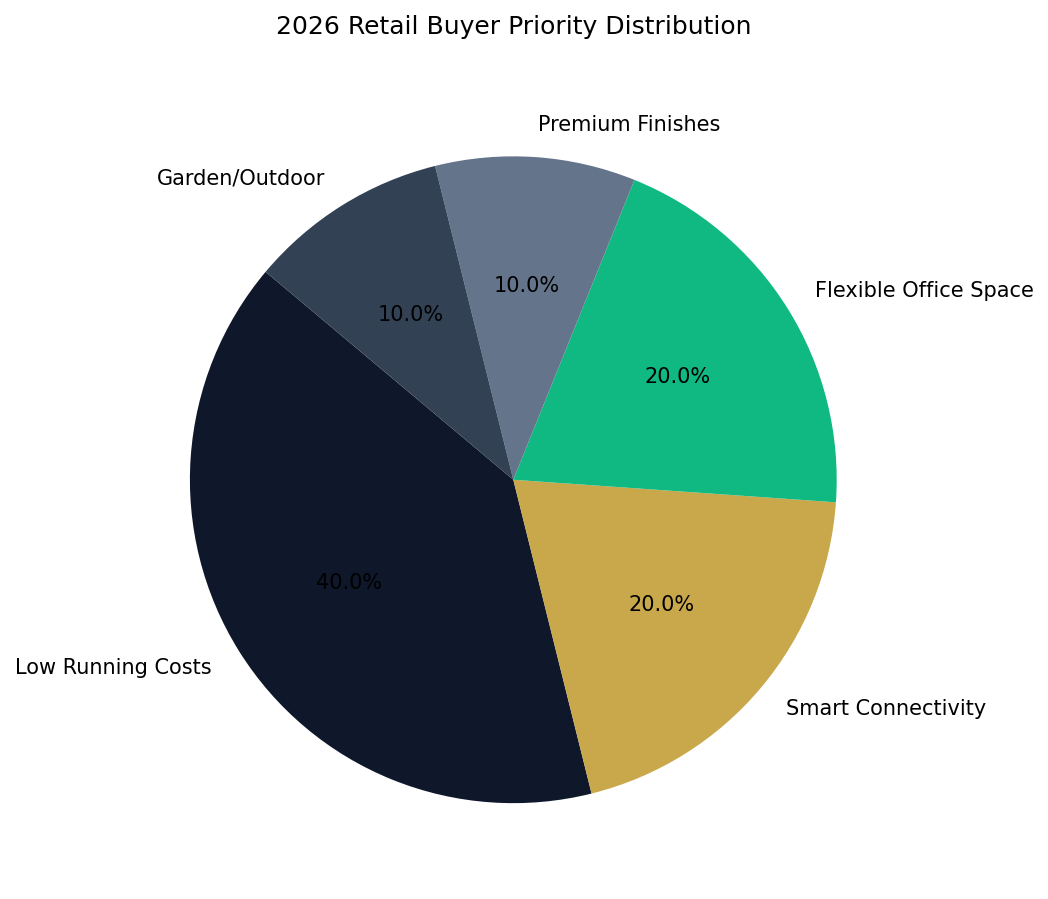

Executive Summary

The reality of house flipping in the UK is starkly different from the glamorous portrayals on daytime television. It is not an interior design hobby; it is a ruthless, high-stakes spreadsheet exercise. In a market characterised by elevated borrowing costs, stringent lender requirements, and cautious buyers, the margin for error has evaporated. A successful flip requires military-grade precision, from the initial market analysis to the final staging.

This guide distils the 15 most critical house-flipping tips required to navigate the 2026 UK property market and avoid a catastrophic financial flop. We have structured these insights chronologically, moving from pre-purchase due diligence through to project execution and the final exit strategy. By adhering to these professional standards—and acknowledging the hidden traps like the '6-Month Rule' and compounding bridging finance interest—investors can consistently extract maximum margin from their projects.

Phase 1: Pre-Purchase Precision (Tips 1-5)

The profitability of a flip is almost entirely determined before you even exchange contracts. Mistakes made during the acquisition phase cannot be renovated away.

1. Know Your Market and Ceiling Prices

Never buy a property without intimately understanding the 'ceiling price' of that specific street. Analyse sold data on Rightmove and Zoopla for recently renovated, comparable properties. Your target demographic dictates your renovation standard; a high-end finish in a first-time buyer market will not yield a return on investment (ROI), while a budget finish in a premium postcode will render the property unsellable.

2. Location Dictates the Renovation

Focus on fundamentals: proximity to transport links, good schools, and local amenities. A perfectly renovated house on a highly undesirable street will always struggle to sell. You can change the floorplan, but you cannot change the postcode.

3. Calculate Every Hidden Cost

Amateur flippers focus solely on the purchase price and the build cost. Professionals meticulously calculate Stamp Duty Land Tax (SDLT)—including the mandatory 3% surcharge for second homes—legal fees, valuation fees, estate agent commissions, and the punitive monthly interest of bridging finance. If the numbers do not align with the 70% Rule (Total Costs < 70% of After Repair Value), walk away.

4. Secure Funding Before Viewing

In the current market, cash is king, and bridging finance is the next best thing. Secure an agreement in principle from a commercial finance broker before you start viewing properties. Vendors of distressed assets favour buyers who can move rapidly. If you cannot prove your funding, you will lose the best deals to professional sourcers.

5. Mandate a Level 3 Structural Survey

Never, under any circumstances, bypass a comprehensive Level 3 RICS structural survey. The discovery of Japanese Knotweed, severe subsidence, or non-compliant spray foam insulation in the loft after completion will instantly turn a viable flip into an unmortgageable liability.

Phase 2: Budgeting and The Power Team (Tips 6-10)

Execution relies entirely on the people you employ and the capital you hold in reserve.

6. Build Your 'Power Team'

Your Power Team—consisting of a commercial finance broker, a 'flip-friendly' conveyancing solicitor, an architect, and a lead contractor—is your most valuable asset. As the community on r/UKProperty frequently notes: a bad builder will bankrupt a good deal, but a phenomenal builder can save a mediocre one.

7. Always Hold a 15-20% Contingency Fund

No renovation has ever gone exactly to plan or precisely to budget. When opening up walls in period UK properties, you will inevitably discover unforeseen issues. A 15% to 20% contingency fund is not an option; it is a mandatory requirement to prevent the project from stalling due to a lack of capital.

8. Separate Emotion from ROI

The most common mistake first-time flippers make is falling in love with the property. You are not living there. Do not install bespoke, high-end fixtures simply because you like them. Every pound spent must be justified by a corresponding increase in the final valuation. Stick to neutral, broadly appealing, and cost-effective designs.

9. Order Materials Prior to Completion

Time is your biggest enemy when utilising short-term finance. Do not wait until you have the keys to start ordering kitchens, bathrooms, or structural steel. Given current supply chain lead times, order your primary materials as soon as contracts are exchanged to ensure your tradespeople can start on day one.

10. Secure Comprehensive Renovation Insurance

Standard home insurance does not cover a property undergoing significant structural renovation or one that is unoccupied for an extended period. You must secure specialist Unoccupied Property and Works in Progress insurance to protect your capital against theft, fire, or liability claims during the build.

Phase 3: Execution and Timelines (Tips 11-13)

Once the build commences, the focus shifts to speed and compliance.

11. Create a Rigid Timeline and Penalise Delays

A detailed Gantt chart or project schedule is essential. Your lead contractor must agree to this timeline. Every week the project overruns is a week of compounding bridging loan interest eating into your profit. Consider incentivising early completion and heavily penalising unjustified delays.

12. Pay Attention to Detail

While you should not overcapitalise, the quality of the finish matters immensely. Buyers are hyper-critical. Poorly cut skirting boards, messy silicone sealant, or misaligned tiling will immediately signal a 'cheap flip' and result in lower offers. Quality finishes sell homes quickly.

13. Don't Forget Planning and Building Control

Attempting to bypass Building Control to save time or money is a fatal error. When it comes time to sell, the buyer's solicitor will demand completion certificates for all structural work, electrical installations, and gas plumbing. Without these, the sale will collapse. Ensure all work is legal and properly signed off.

Phase 4: The Exit Strategy (Tips 14-15)

The project is not complete until the cash is back in your bank account.

14. Sell at the Right Time

Understand local market cycles. Launching a property to market in the second week of December is generally a poor strategy compared to the traditional 'Spring Bounce'. However, you must balance market timing against the cost of holding the property empty.

15. Be Patient and Stick to Your Numbers

Desperation breeds poor decisions. Do not rush into a bad deal simply because you have the capital ready to deploy. Similarly, if your finished property receives a lowball offer in the first week, hold your nerve. Trust your initial ARV calculations and your estate agent's guidance.

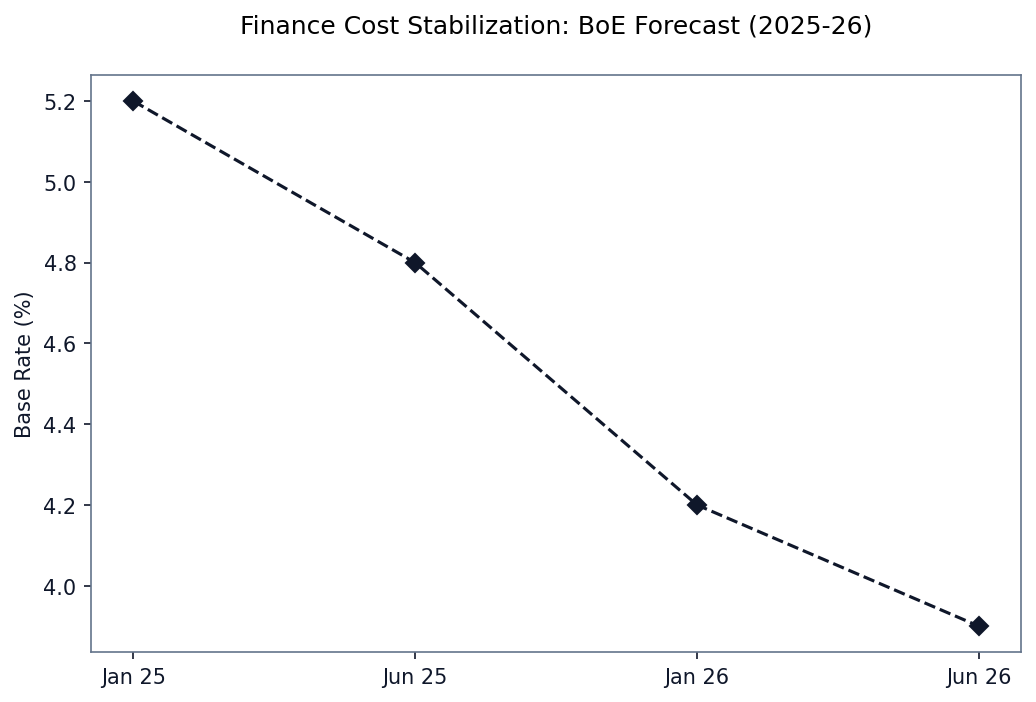

The 6-Month Rule and Bridging Finance Traps

A critical UK-specific hurdle that often blindsides new flippers is the '6-Month Rule'. Many high-street mortgage lenders (including major banks like Santander and HSBC) operate a policy where they will refuse to lend to a buyer if the vendor (you) has owned the property for less than six months.

This is an anti-fraud measure, but it severely impacts the flipping model. If you complete a rapid eight-week renovation and immediately list the property, your buyer pool is restricted to cash buyers or those using specialist lenders. If you must wait for the six-month mark to pass before a standard buyer can complete, you must factor an additional four months of bridging finance interest into your initial spreadsheet.

Actionable Next Steps

To transition from reading to executing, ensure your legal and financial structures are optimized for property trading.

HMRC views flipping as a trading activity, not an investment. Therefore, profits are subject to Income Tax rather than Capital Gains Tax (CGT). To mitigate this, the vast majority of professional flippers operate through a Limited Company (Special Purpose Vehicle - SPV), allowing them to pay the lower Corporation Tax rate.

Before you start viewing properties, establish your SPV and connect with a specialist commercial finance broker to understand your precise borrowing capacity. Only then should you begin hunting for your first flip.

Stop being a landlord. Start being an investor.

Shaded Canvas introduces serious capital to vetted UK property opportunities — targeting 12–16% net returns.

Start Investing →