Why Overseas Investors Keep Choosing UK Property

There is no legal restriction preventing non-UK residents from buying property in England, Wales, Scotland, or Northern Ireland. None. No visa requirement, no residency threshold, no nationality bar. The UK is one of the most open property markets in the world — and that openness, combined with a transparent legal system, strong rule of law, and deep liquidity, is precisely why international capital continues to flow into British bricks.

But openness does not mean simplicity. Overseas investors face a distinct set of challenges that domestic buyers never encounter: a 2% SDLT surcharge, enhanced anti-money laundering scrutiny, specialist mortgage requirements, complex cross-border tax obligations, and the operational reality of managing an asset from thousands of miles away.

This guide is built for the overseas investor who has decided that UK property belongs in their portfolio and now needs to understand exactly how to execute — from finding the right property to structuring the purchase tax-efficiently, managing it remotely, and planning an exit strategy that does not hand half the profit to HMRC.

The Tax Landscape: Every Levy You Will Face

Tax is the single biggest friction point for overseas property investors, and it is the area where the most costly mistakes are made. The UK government has progressively tightened the tax treatment of non-resident property investors over the past decade, and the changes announced in the October 2024 Autumn Budget added further complexity.

Stamp Duty Land Tax (SDLT) — England and Northern Ireland

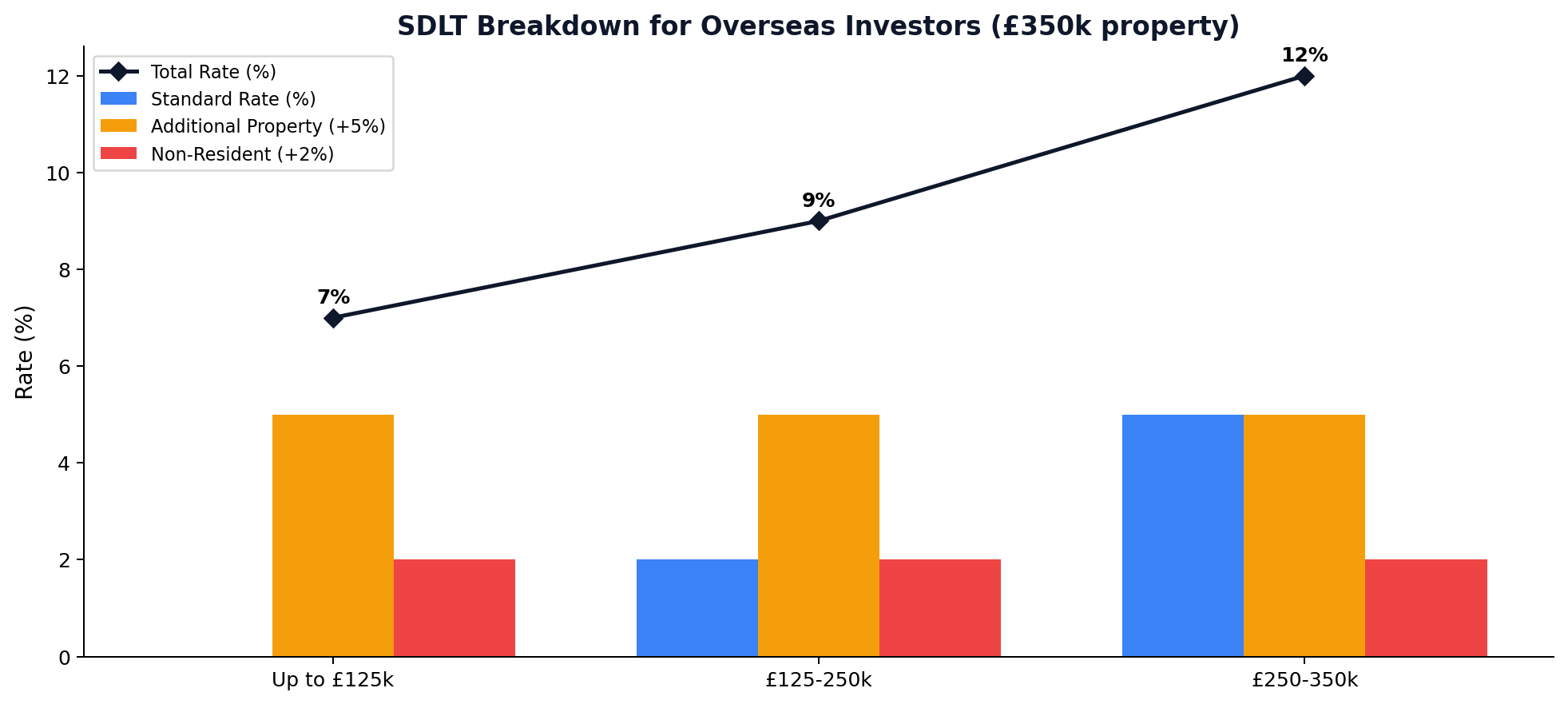

Non-UK residents pay a 2% surcharge on top of all standard SDLT rates for residential property valued at £40,000 or more. If you are purchasing an additional property (as most overseas investors are), you also pay the 5% higher-rate surcharge (increased from 3% in October 2024).

SDLT Calculation for Non-Resident Buying Additional Property (£350,000 purchase):

| Band | Rate | Tax |

|---|---|---|

| Up to £125,000 | 0% + 5% + 2% = 7% | £8,750 |

| £125,001–£250,000 | 2% + 5% + 2% = 9% | £11,250 |

| £250,001–£350,000 | 5% + 5% + 2% = 12% | £12,000 |

| Total SDLT | £32,000 |

That is 9.1% of the purchase price consumed by SDLT before you even receive the keys. This upfront cost must be factored into your yield calculations from day one.

Scotland and Wales have their own transaction taxes (Land and Buildings Transaction Tax and Land Transaction Tax respectively), with different rates and band thresholds. Scotland does not currently apply an overseas buyer surcharge, making it potentially more tax-efficient for non-resident investors.

Income Tax on Rental Income

Rental income from UK property is subject to UK Income Tax regardless of where you live. As a non-resident landlord, you fall under the Non-Resident Landlord (NRL) Scheme, which requires your letting agent or tenant to deduct 20% withholding tax from your gross rent and remit it directly to HMRC.

You can apply to HMRC to receive your rental income gross (without the 20% deduction) by completing the NRL1 form. Approval is typically granted if you have a good compliance history or can demonstrate that your UK tax affairs are up to date. You will still need to file a UK Self Assessment tax return each year to declare your rental income and claim allowable expenses.

Allowable deductions against rental income include:

- Mortgage interest (if held in a limited company — see Section 24 below)

- Letting agent fees

- Property management costs

- Insurance premiums

- Maintenance and repairs

- Ground rent and service charges

- Travel expenses for property inspections (within reason)

- Professional fees (accountant, solicitor)

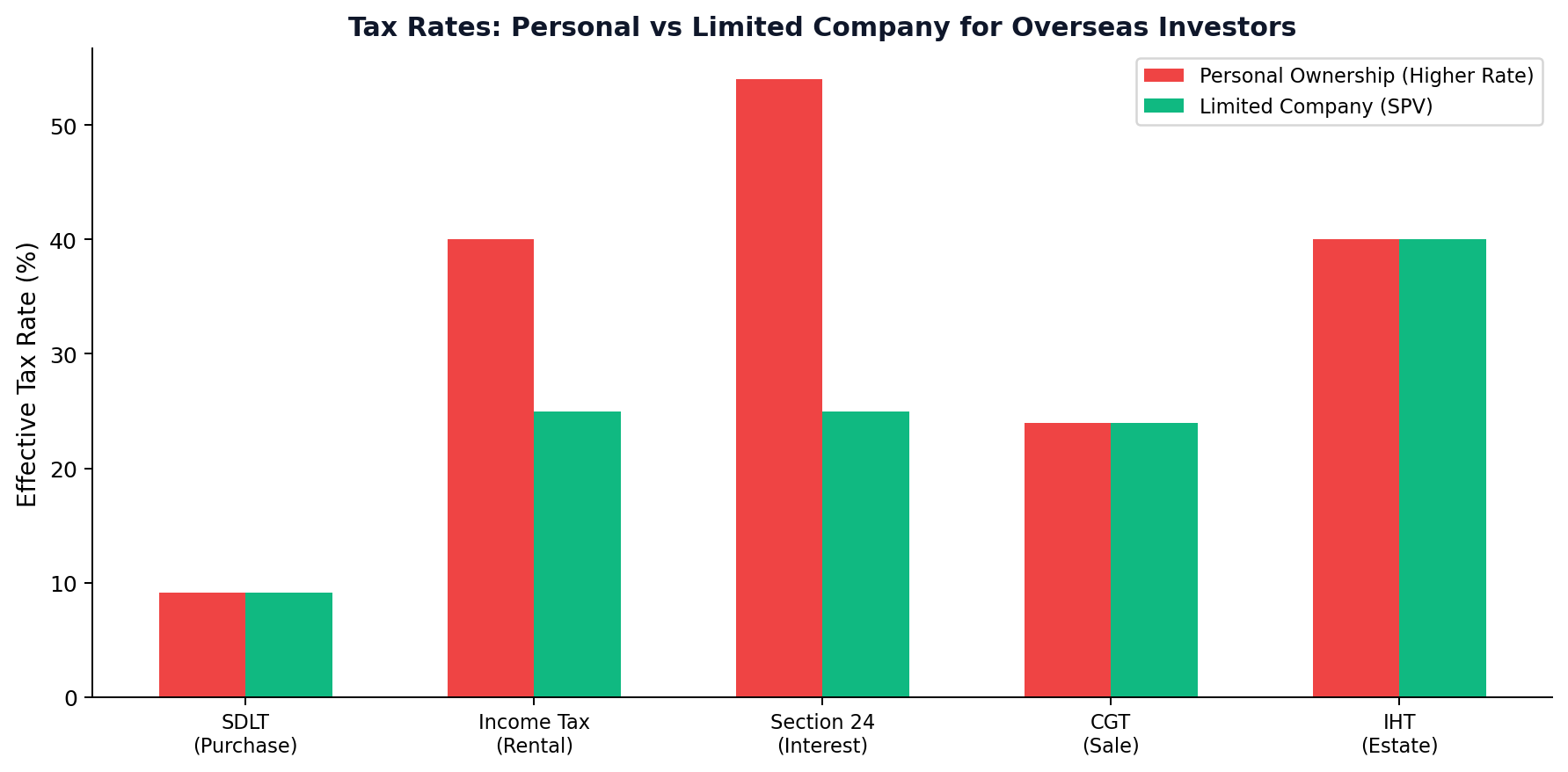

Section 24: The Mortgage Interest Restriction

If you hold your UK property personally (not in a company), the Section 24 restriction applies: you cannot deduct mortgage interest from your rental income for tax purposes. Instead, you receive a 20% tax credit on the interest paid.

For overseas investors who are higher-rate taxpayers in the UK (income above £50,270), this creates a phantom profit — you are taxed on rental income that has already been consumed by mortgage payments.

Solution: Most overseas investors now purchase through a UK limited company (SPV). The company pays Corporation Tax at 25% on profits (or 19% on profits up to £50,000), and mortgage interest remains fully deductible. The annual filing costs (approximately £500–£1,500 for accountancy and company secretarial services) are a worthwhile trade-off.

Capital Gains Tax (CGT)

Since April 2015, non-UK residents have been liable for UK Capital Gains Tax on the disposal of UK residential property. The current rates are:

- 18% for gains within the basic rate band

- 24% for gains above the basic rate band

You must file a CGT return with HMRC within 60 days of the property sale completing. This is a strict deadline — miss it, and you face automatic penalties even if no tax is due.

Important: You may be able to offset the UK CGT liability against tax payable in your country of residence under a Double Taxation Agreement (DTA). The UK has DTAs with over 130 countries. However, the interaction between UK and overseas tax obligations is complex and requires specialist cross-border tax advice.

Inheritance Tax (IHT) — The Hidden Trap

This is the tax that catches most overseas investors by surprise. UK residential property is within the scope of UK Inheritance Tax regardless of the owner's residency or domicile status. IHT is charged at 40% on the value of UK property above the £325,000 nil-rate band (unless the property is left to a spouse, civil partner, or charity).

Critically, holding the property through an overseas company does not protect you. Since April 2017, shares in overseas companies that derive their value from UK residential property are treated as UK assets for IHT purposes.

The primary mitigation strategies are:

- Life insurance — a term policy covering the potential IHT liability

- Gifting — transferring property more than 7 years before death removes it from the estate

- Trust structures — complex and expensive, but can be effective with proper professional advice

Non-Dom Regime Abolition (From April 6, 2026)

The UK's "non-domiciled" (non-dom) tax regime — which historically allowed non-UK domiciled individuals to shelter overseas income and gains from UK tax — has been abolished from April 6, 2026. It has been replaced with a new residence-based test for foreign income and gains.

This change primarily affects overseas investors who also spend significant time in the UK (more than 183 days per year or meeting the "sufficient ties" test). If you are a pure overseas investor with no UK residence, the non-dom reform is less directly relevant — but it signals the UK government's direction of travel toward broader taxation of international wealth.

The Purchase Process: Step by Step

Step 1: Define Your Investment Strategy and Budget

Before engaging with agents or developers, determine:

- Investment objective: Rental yield, capital appreciation, or a combination

- Budget: Including SDLT, legal fees (budget £2,000–£5,000), survey costs, and mortgage arrangement fees

- Holding structure: Personal name, UK limited company, or overseas entity

- Management approach: Self-managed (impractical for most overseas investors) or professional property management (10–15% of rent)

Step 2: Secure Financing (If Needed)

Obtaining a UK mortgage as a non-resident is possible but more restrictive than for domestic buyers:

- Specialist lenders cater to this market — mainstream high-street banks generally do not offer mortgages to non-residents

- Deposit requirements are typically 25–35% of the purchase price (vs. 20–25% for UK residents)

- Interest rates are usually 1–2% higher than equivalent UK resident products

- Evidence requirements are more stringent — expect to provide certified translations of foreign income documents, bank statements (typically 6–12 months), and proof of overseas tax status

- Currency risk: If your income is in a non-GBP currency, lenders may apply additional stress testing to account for exchange rate fluctuations

A specialist mortgage broker with experience in overseas buyer mortgages is essential. Budget £500–£1,000 for broker fees, recoverable if you proceed with their recommended product.

Step 3: Find the Property

Overseas investors have several sourcing channels:

- Online portals: Rightmove, Zoopla, and OnTheMarket list virtually all properties for sale in the UK. Most offer detailed photographs, floor plans, and EPC ratings. Many developers now provide virtual tours that allow you to assess a property without travelling.

- Estate agents: For the secondary market, a local estate agent can provide market insight, negotiate on your behalf, and coordinate viewings (including video viewings for remote buyers).

- Developers: For off-plan or new-build purchases, buying directly from the developer eliminates the estate agent layer and may provide access to early-release pricing and incentives.

- Property auctions: An advanced strategy requiring pre-auction legal review and immediate exchange on the fall of the hammer. Not recommended for first-time overseas buyers.

Step 4: Appoint a UK Solicitor

A UK-based solicitor or licensed conveyancer is mandatory for property purchases in England and Wales (in Scotland, a solicitor handles the entire transaction including the offer process).

Your solicitor will conduct:

- Title checks — confirming the seller has the legal right to sell

- Local authority searches — planning applications, environmental issues, highway schemes

- Anti-money laundering (AML) due diligence — enhanced for non-resident buyers

AML documentation you will need:

- Certified copy of passport (certified by a notary, solicitor, or embassy in your country)

- Certified proof of address (utility bill or bank statement, less than 3 months old)

- Source of funds documentation — bank statements, sale proceeds, gift letters, or business accounts demonstrating where the purchase funds originate

- Source of wealth documentation — for higher-value purchases, evidence of how you accumulated your overall wealth

These requirements are non-negotiable and reflect the UK's obligations under the Money Laundering Regulations 2017 (as amended). Allow 2–4 weeks for the AML process if your documents need to be certified internationally.

Step 5: Make an Offer and Exchange

In England and Wales, making an offer is not legally binding until contracts are exchanged (signed by both parties). Between offer acceptance and exchange, either party can withdraw without penalty — a process known as "gazumping" (if the seller accepts a higher offer) or "gazundering" (if the buyer reduces their offer).

At exchange, you pay the deposit (typically 10% of the purchase price) and become legally committed to the purchase. Completion follows, usually 2–4 weeks later, when the balance is paid and legal ownership transfers.

In Scotland, the system is different — the offer process is conducted through solicitors, and an accepted formal offer creates a legally binding contract immediately.

Remote Property Management

Professional Management Is Not Optional

For overseas investors, professional property management is a necessity, not a luxury. A reputable management company will handle:

- Tenant finding, referencing, and onboarding

- Rent collection and arrears management

- Maintenance coordination and emergency repairs

- Regulatory compliance (gas safety, electrical safety, EPC, deposit protection)

- Section 8/Section 21 notices and possession proceedings (if needed)

- Periodic property inspections (typically quarterly)

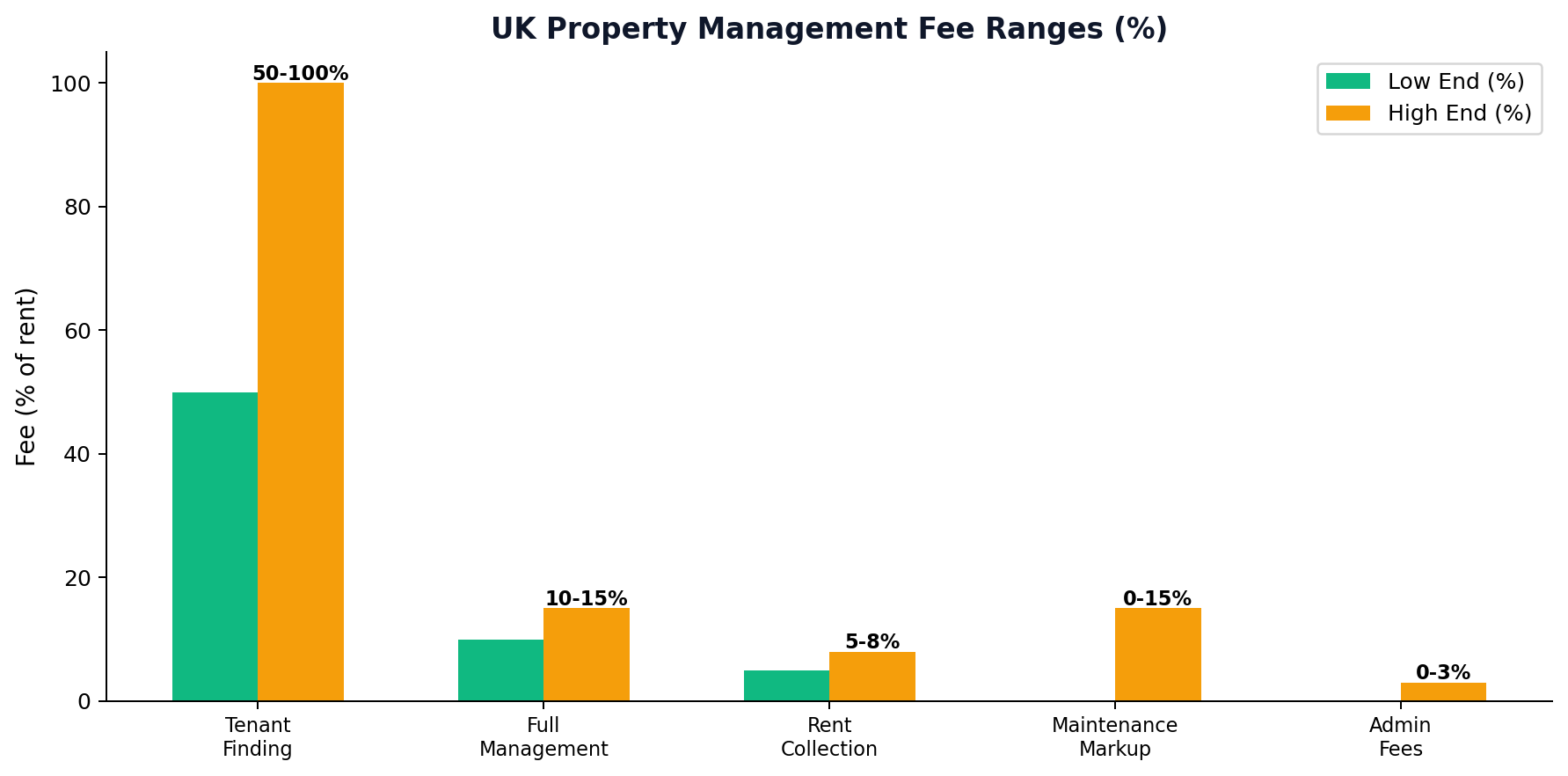

Fees: Expect to pay 10–15% of monthly rent for full management, plus 50–100% of one month's rent as a tenant finding fee for new tenancies. Some companies offer fixed monthly fees rather than percentage-based pricing.

Choosing the Right Management Company

Not all property management companies are equal, and overseas investors are particularly vulnerable to underperformance because they cannot easily inspect the property or interview the manager in person.

Due diligence checklist:

- Are they a member of ARLA Propertymark (the industry body for letting agents)?

- Do they hold client money protection insurance (legally required since April 2019)?

- Can they provide references from other overseas landlord clients?

- What is their average void rate across their managed portfolio?

- Do they provide an online portal with real-time financial reporting and maintenance updates?

Where to Invest: Location Strategy for Overseas Buyers

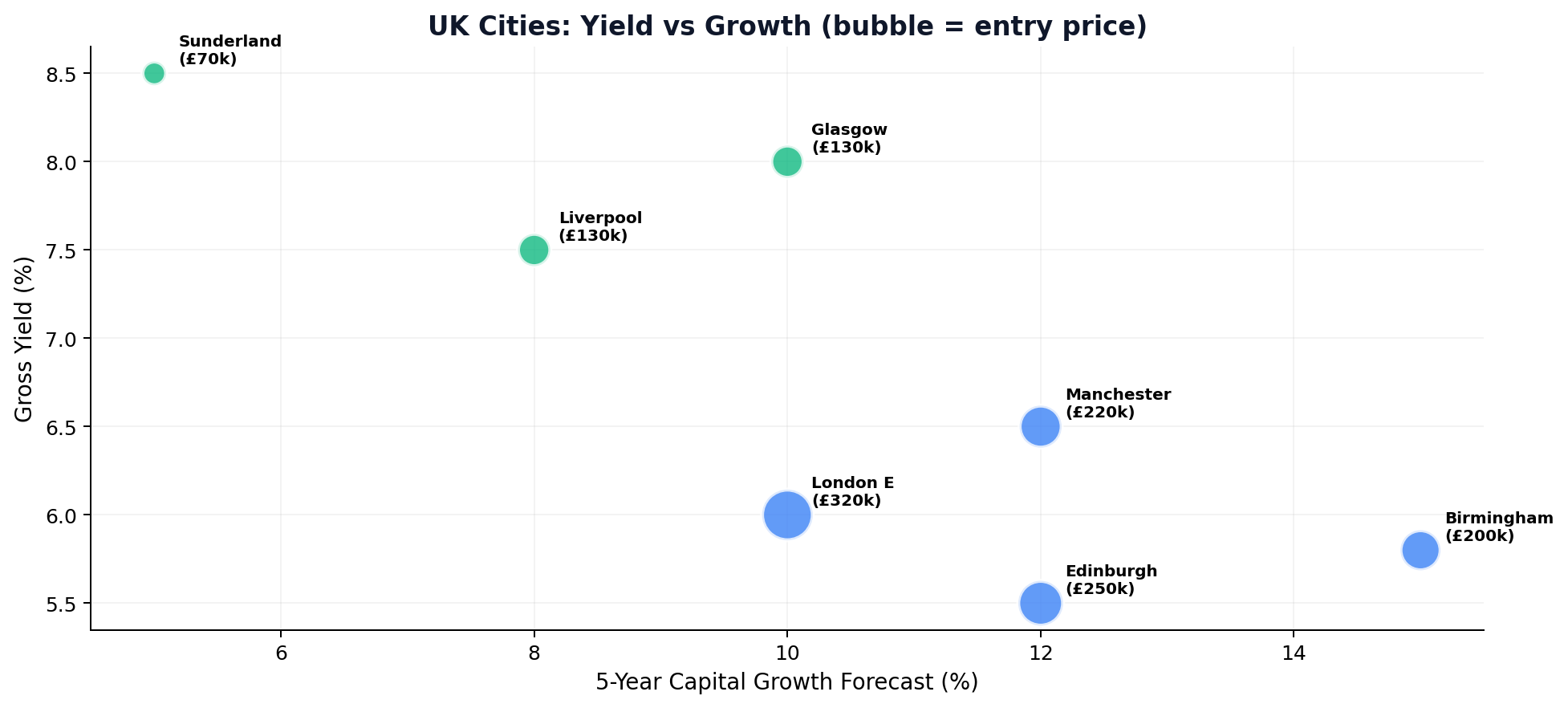

For Maximum Yield

- North East England: Sunderland, Newcastle — yields of 7–9%, entry prices from £55,000–£130,000

- North West England: Liverpool, Manchester — yields of 6–8%, entry prices from £130,000–£290,000

- Scotland: Glasgow, Edinburgh suburbs — yields of 7–9%, lower transaction taxes

For Capital Growth

- London (East): Barking, Stratford, Canning Town — blend of yield (5.5–7%) and infrastructure-driven growth

- Manchester: Strong rental demand and consistent capital appreciation (40% over 5 years)

- Birmingham: HS2 and Big City Plan driving long-term growth fundamentals

For Hands-Off Simplicity

- New-build apartments in managed developments offer the lowest maintenance burden, integrated property management, and NHBC warranty protection. Ideal for overseas investors who want to minimise complexity.

Currency Risk and Repatriation

Currency fluctuations can significantly impact your returns. A property that delivers 6% yield in GBP may deliver more or less when converted to your home currency. Consider:

- Forward contracts: Lock in an exchange rate for future rental income repatriation

- Multi-currency accounts: Services like Wise, Currencycloud, or OFX offer significantly better exchange rates than high-street banks

- GBP retention: If you do not need the income immediately, retaining it in a UK bank account avoids conversion costs and allows you to compound returns in sterling

Opening a UK bank account as a non-resident can be challenging. Some banks (Barclays, HSBC) offer international accounts, but the onboarding process is lengthy. A UK limited company can open a business bank account more easily, which is another advantage of the SPV structure.

Critical Clarification: Property ≠ Residency

Buying property in the UK does not grant any residency or immigration rights. You cannot live in the UK simply because you own property there. If you intend to spend more than 6 months per year in the UK, you will need a visa — and property ownership is not a qualifying criterion for any UK visa category.

This is a common misconception among overseas investors from jurisdictions where property purchase grants residency (e.g., Portugal's Golden Visa, formerly). The UK has no equivalent programme.

Conclusion: The Overseas Investor's Edge

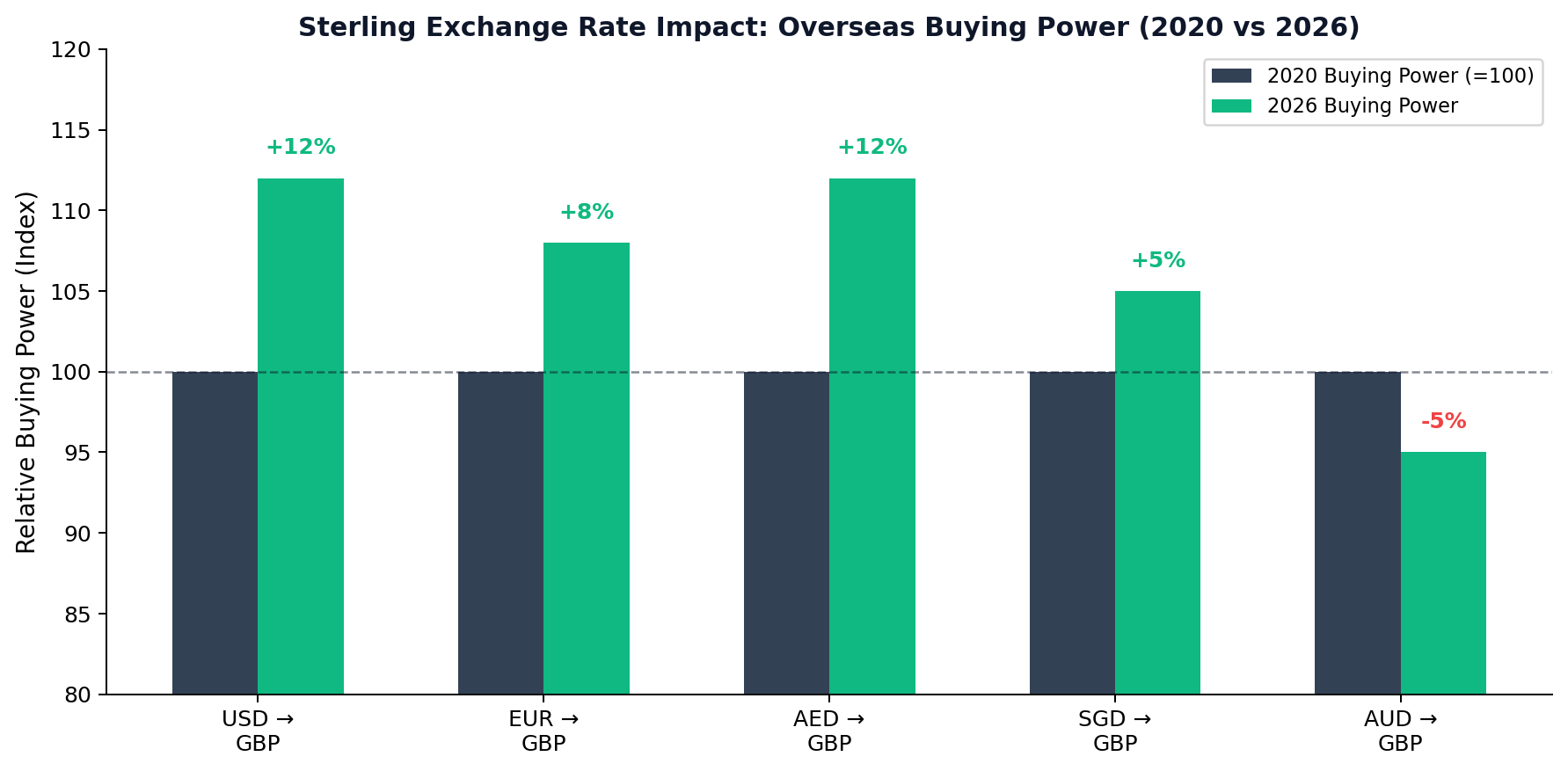

Despite the additional tax burden and operational complexity, overseas investment in UK property remains fundamentally attractive. The market is liquid — you can sell. The legal system is transparent — your rights are protected. The rental market is deep — tenants are plentiful. And sterling's current valuation means that investors holding USD, EUR, AED, or SGD are buying at a structural discount compared to a decade ago.

The investors who succeed from overseas share three characteristics: they structure correctly (limited company, specialist mortgage, professional management), they engage locally (UK solicitor, UK accountant, UK management company), and they hold for the long term — because UK property rewards patience above all else.

Next Steps:

- Engage a UK tax adviser with cross-border expertise to model the tax implications specific to your country of residence.

- Obtain a mortgage agreement in principle from a specialist overseas buyer lender before searching for property.

- Appoint a UK solicitor and begin the AML documentation process — this takes longer than you expect, so start early.

📚 Related Reading

- Best Capital Growth Property UK: Where Property Prices Are Actually Heading in 2026 and Beyond

- Passive Income Property UK: How to Build a Rental Portfolio That Actually Pays You in 2026

- Property Investments Manchester: The Definitive Investor's Guide to the UK's Most Dynamic City in 2026

- Buy dirt

- Hobbies That Make Money: Real "Cheat Codes" for Turning Your Passion Into Profit

Stop being a landlord. Start being an investor.

Shaded Canvas introduces serious capital to vetted UK property opportunities — targeting 12–16% net returns.

Start Investing →