Why Off-Plan Is Dominating the UK New-Build Market

Over a third of all new-build homes in England and Wales are now sold off-plan. That statistic alone should tell you something: developers are not offering these deals out of generosity. They need pre-sales to secure financing, and smart investors are leveraging that desperation to lock in discounts of 10–15% below projected market value before a single brick is laid.

But here is the uncomfortable truth that most property blogs skip over. Off-plan is not a "hack." It is a calculated bet — one that can deliver exceptional returns when executed correctly, or leave you holding a depreciating asset in a half-finished development if you get lazy with your due diligence.

This guide strips away the glossy CGI images and developer promises. We are going to walk through the exact mechanics, risks, tax implications, and regional strategies that separate profitable off-plan investors from the ones who end up on property forums asking how to exit their contracts.

How Off-Plan Property Actually Works (The Mechanics Most Guides Skip)

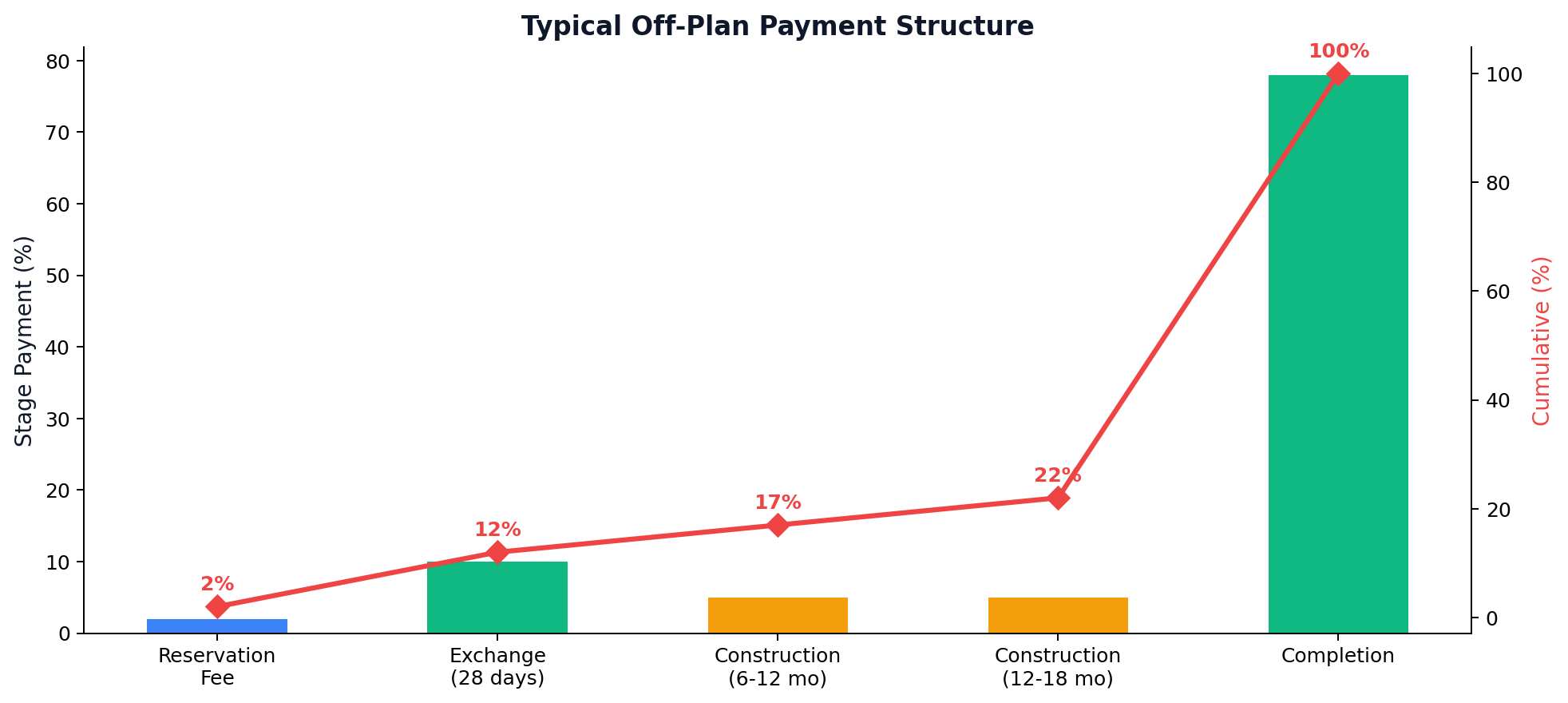

The Payment Structure

Off-plan purchases in the UK follow a staged payment model, and understanding this structure is critical because it defines your cash flow exposure.

- Reservation Fee: Typically £500–£5,000 to take the unit off the market. This is usually non-refundable but deducted from the purchase price.

- Exchange Deposit: 10–20% of the purchase price, payable when contracts are exchanged (usually 28 days after reservation).

- Staged Payments: Some developers request further payments at construction milestones — slab completion, roof on, fit-out. These are more common in larger developments.

- Completion Payment: The balance, usually funded by your mortgage, payable on legal completion.

The critical insight here is the time gap between exchange and completion. On a typical off-plan purchase, this can be 12–36 months. During that window, you have significant capital committed but no income, no asset to refinance against, and no guarantee that the market will cooperate.

The Legal Framework

Every off-plan buyer in England and Wales is protected by the Consumer Code for Home Builders, which requires developers to provide clear information about the property, a right to cancel within a cooling-off period, and an independent dispute resolution process. The NHBC Buildmark warranty (or equivalent from LABC or Premier Guarantee) covers structural defects for 10 years post-completion.

However — and this is a knowledge gap most guides miss entirely — the warranty does not cover cosmetic defects after the first two years, nor does it protect you if the developer changes specifications mid-build. Your contract's specification schedule is your only protection, and most buyers never read it.

The Financial Case: When Off-Plan Beats Resale

Capital Appreciation During Construction

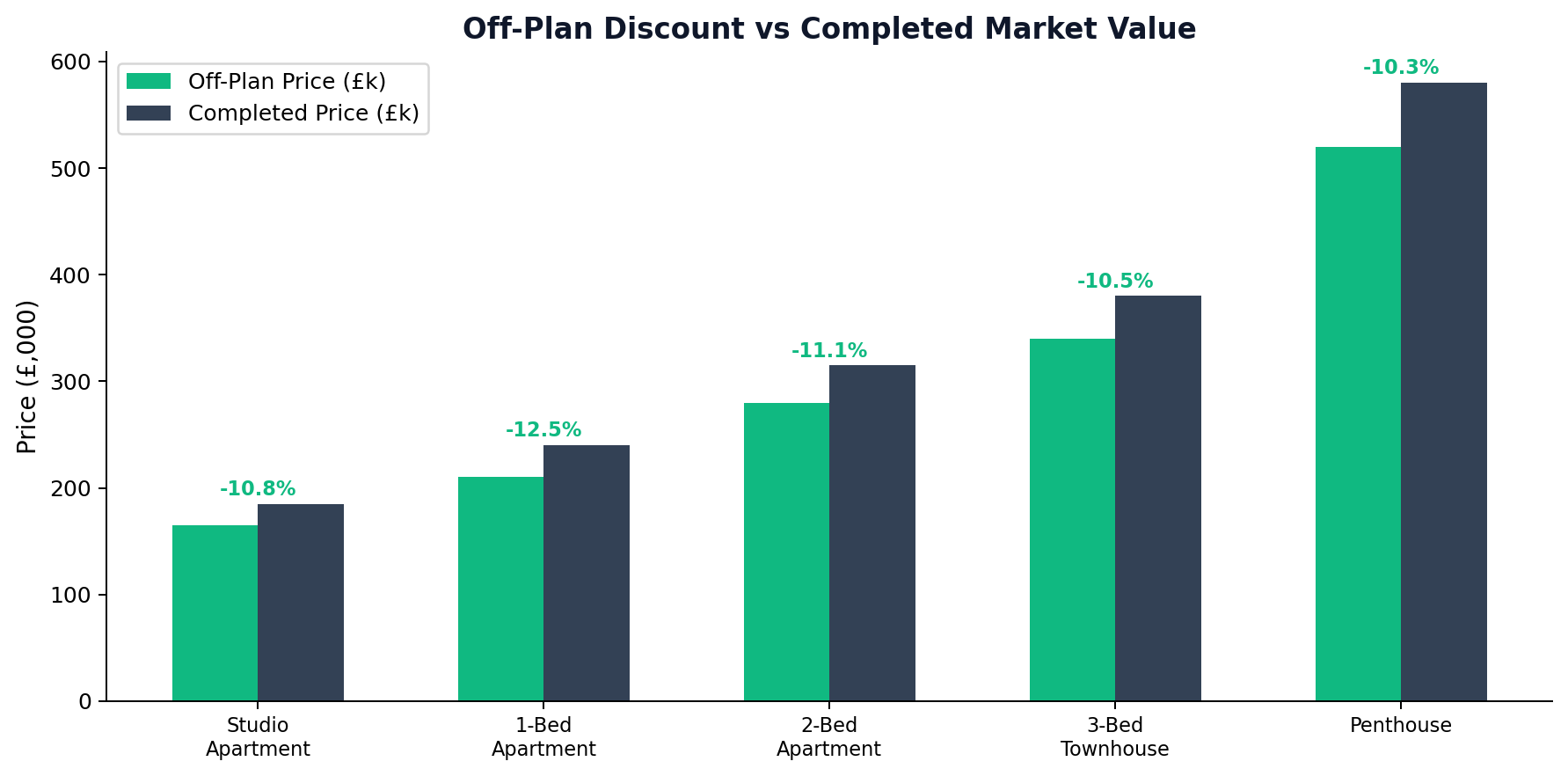

The core investment thesis is straightforward: you lock in today's price and benefit from price growth during the construction period. In a rising market, this can deliver leveraged returns that outperform any other property strategy.

Real example from the current cycle: A two-bedroom apartment in Manchester's Northern Quarter, reserved off-plan in March 2024 at £245,000, completed in September 2026 and valued at £278,000 — a 13.5% uplift in 18 months. The investor's cash commitment during that period was just the 10% deposit (£24,500), meaning their return on capital deployed was effectively 134%.

But this is not a guaranteed outcome. Between 2022 and 2023, several London off-plan developments completed into a falling market, with investors receiving valuations below their purchase price. The developer discount was real, but the market moved against them.

Developer Incentives Worth Negotiating

Beyond the headline discount, developers routinely offer incentives that directly impact your yield and cash flow:

- Stamp Duty contributions — Some developers will cover part or all of your SDLT liability. On a £300,000 property, that is a saving of up to £2,500 for first-time buyers or £5,000 for additional property purchasers.

- Furniture packages — Fully furnished units typically command 8–12% higher rents and let faster, particularly in city-centre locations targeting young professionals.

- Rental guarantees — Proceed with extreme caution here. A 6% "guaranteed yield" for two years sounds attractive until you discover the guarantee is priced into a higher purchase price. Always compare the guaranteed rent against the open market rate for the area.

- Deposit boosts — Some developers will match your 5% deposit with an additional 5%, giving you a 10% exchange deposit but only requiring half the cash. These are genuinely useful for investors seeking to preserve capital across multiple reservations.

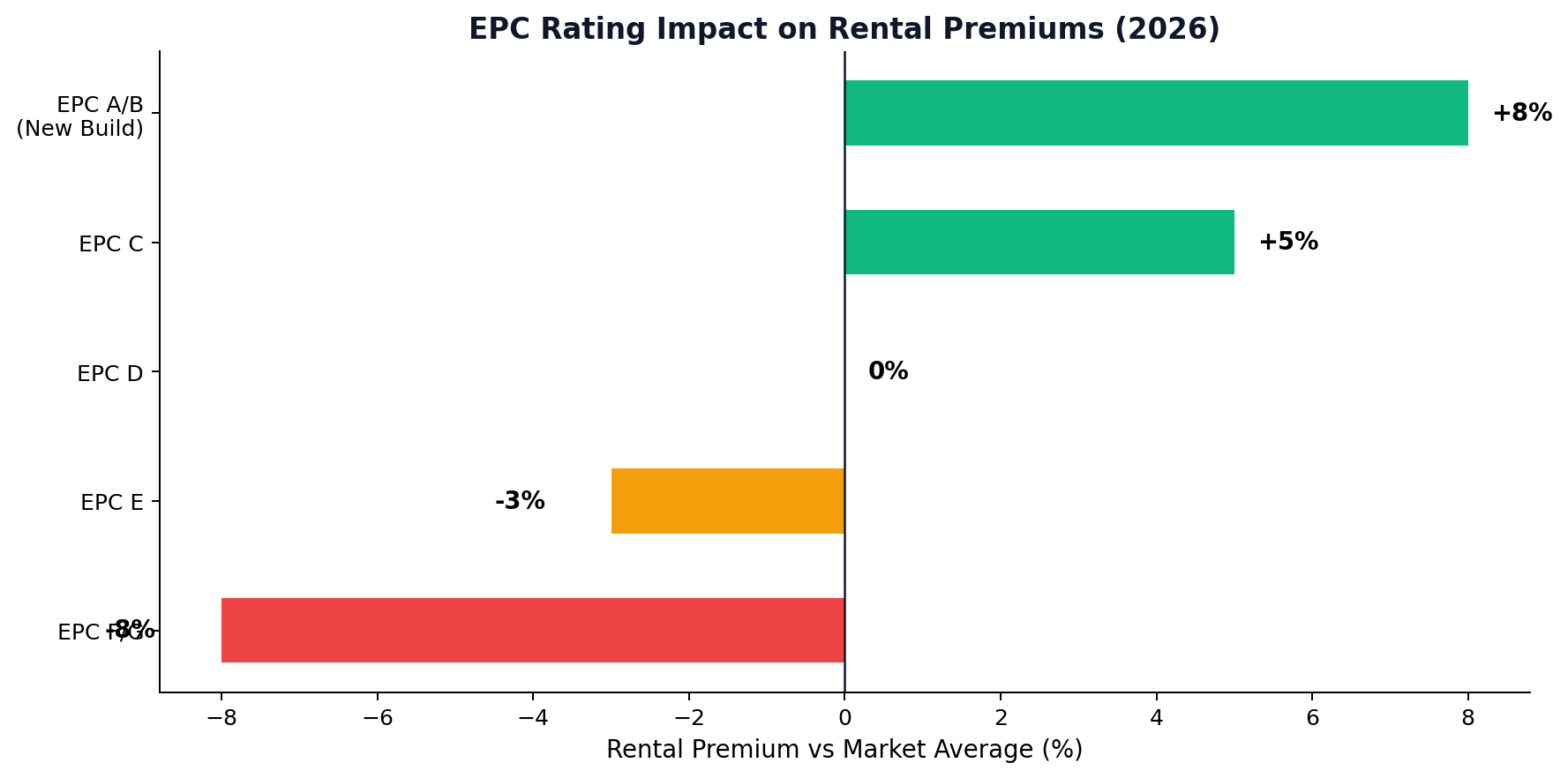

Energy Efficiency: The Hidden Yield Booster

New-build off-plan properties are constructed to current Building Regulations, which means they typically achieve an EPC rating of A or B. This is not just a marketing point — it has direct financial implications.

From April 2026, the Minimum Energy Efficiency Standard (MEES) requires all rental properties to hold a minimum EPC rating of C. Older stock failing this threshold will require costly retrofitting (typically £5,000–£15,000 per property). Off-plan buyers sidestep this entirely, and their tenants benefit from energy bills that are £500–£1,000 per year lower than comparable older properties, making new-builds easier to let and justifying premium rents.

The Risk Register: What Can Actually Go Wrong

1. Developer Insolvency

Between 2022 and 2024, over 4,500 UK construction firms entered insolvency proceedings. If your developer goes under mid-build, your deposit is at risk unless it is protected by an NHBC-backed deposit protection scheme or held in a solicitor's escrow account. Before exchanging, verify:

- Is the developer NHBC-registered?

- Is the deposit protection scheme backed by an insurer (not just the developer's own reserves)?

- Does the developer have a track record? Check Companies House for filed accounts, director history, and any county court judgements.

2. Completion Delays

The average off-plan completion delay in the UK is currently 4–6 months beyond the contracted date. This creates several cascading problems:

- Mortgage offer expiry. Standard mortgage offers are valid for 6 months. If your completion is delayed, you may need to reapply, potentially at a higher interest rate. Some lenders (Halifax, Nationwide) now offer 9-month validity specifically for off-plan purchases — insist on this.

- Bridging finance. If your existing property sale is timed to your off-plan completion, a delay can force you into expensive bridging finance at 0.5–1.5% per month.

- Longstop dates. Your contract should include a longstop date — the absolute final deadline for completion. If the developer misses this, you can rescind the contract and recover your deposit in full. Many buyers do not even know this clause exists.

3. Specification Changes

Developers retain the right to make "minor variations" to specifications — and their definition of "minor" can be surprisingly broad. Flooring downgrades, appliance substitutions, and layout modifications are all common. The defence is simple: ensure your solicitor includes a specification schedule as a contractual appendix, not merely a marketing document.

4. Valuation Shortfalls

At completion, your mortgage lender will send a surveyor to value the property. If the valuation comes in below your purchase price, you must fund the shortfall from cash. This is more common than you might think — particularly in developments where all units are sold off-plan and there are no comparable sales data for the surveyor to reference.

Mitigation: Always hold a cash reserve of 5–10% above your deposit to cover potential shortfalls.

Regional Strategy: Where to Buy Off-Plan in 2026

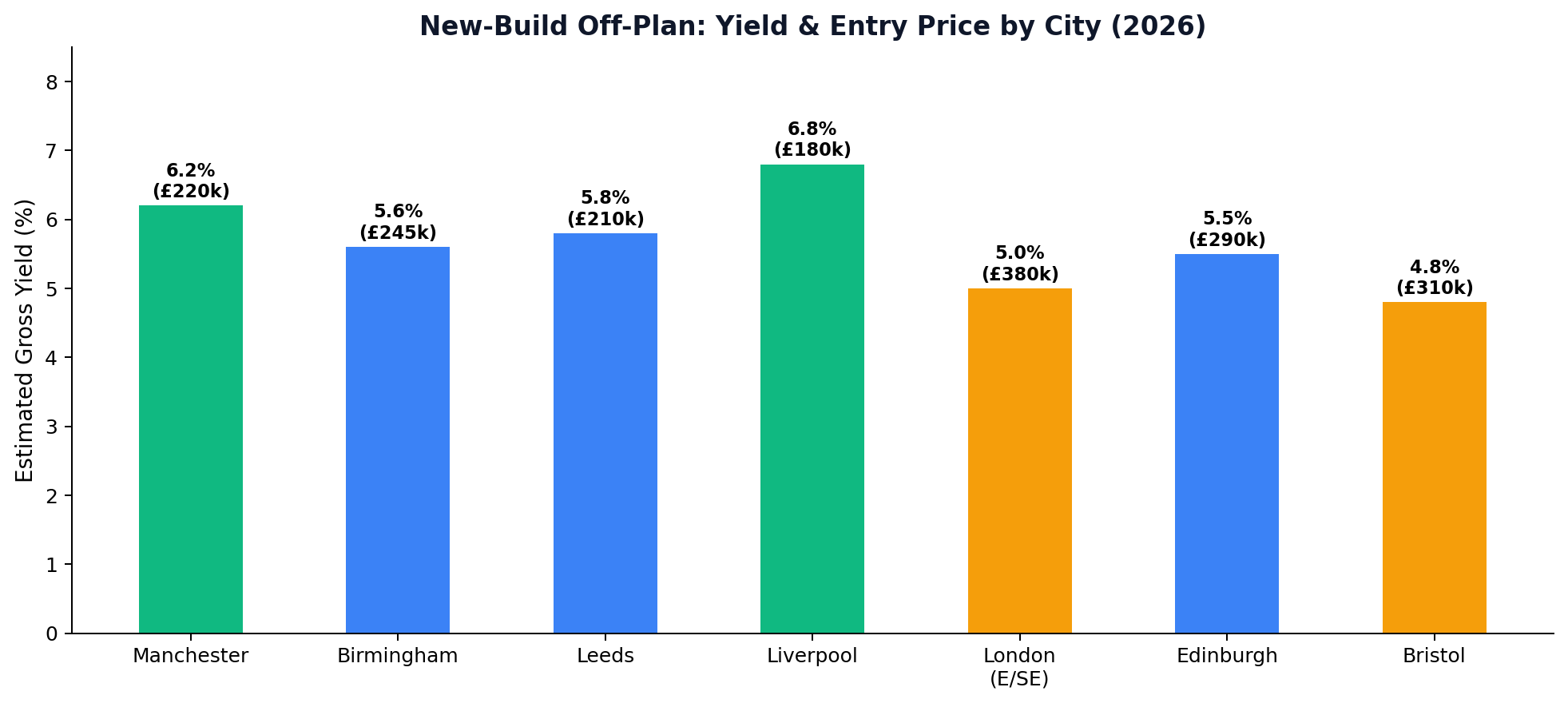

Northern England: The Yield Play

The cities delivering the strongest off-plan returns are concentrated in the North and Midlands, where the combination of affordable entry prices and strong rental demand creates a favourable yield dynamic.

- Manchester: The UK's strongest regional rental market. Off-plan two-beds in areas like Ancoats, New Islington, and Salford Quays are entering the market at £230,000–£290,000 with projected yields of 6–7%. The city's population is projected to grow by 100,000 by 2030.

- Liverpool: Lower entry prices (off-plan one-beds from £130,000) and yields consistently above 7% in the Baltic Triangle, Knowledge Quarter, and L1 postcode. The £5.5 billion Liverpool Waters regeneration is driving long-term capital growth expectations.

- Birmingham: The Big City Plan and HS2 (despite delays) continue to support demand. Digbeth and Eastside developments are achieving off-plan sales at £200,000–£260,000 for two-beds with projected yields of 5.5–6.5%.

- Leeds: The city's financial and legal sectors are expanding, driving professional rental demand. Off-plan in the city centre from £180,000 with yields around 6%.

London: The Capital Growth Play

London off-plan is a fundamentally different proposition. Yields are lower (3.5–5% in most zones), but capital appreciation potential remains strongest in areas benefiting from infrastructure investment.

- East London is the current hotspot. The Elizabeth Line has already driven price increases of 18% in Abbey Wood and 22% in East Ham over five years. Off-plan developments in Barking (IG11) are entering at £280,000–£350,000 with yields of 6–7% — the best blend of yield and growth in the capital.

- Thamesmead (SE28) is the long-term speculation play. Peabody's masterplan for 11,500 new homes over 30 years could make this London's largest regeneration project. Off-plan entry prices remain below £300,000 for two-beds.

- Battersea and Nine Elms offer premium off-plan with yields around 4.5–5% but strong capital growth driven by the Northern Line Extension and the Power Station redevelopment.

Scotland: The Regulatory Advantage

Scotland's distinct legal system (including the Land and Buildings Transaction Tax rather than SDLT) and strong rental market (average gross yields of 7.6% nationally) make it an underserved market for off-plan investors. Glasgow in particular is delivering yields of 7.25–9.3% with entry prices significantly below English cities.

Stamp Duty and Tax: The Numbers That Actually Matter

Stamp Duty Land Tax (SDLT) — England and Northern Ireland

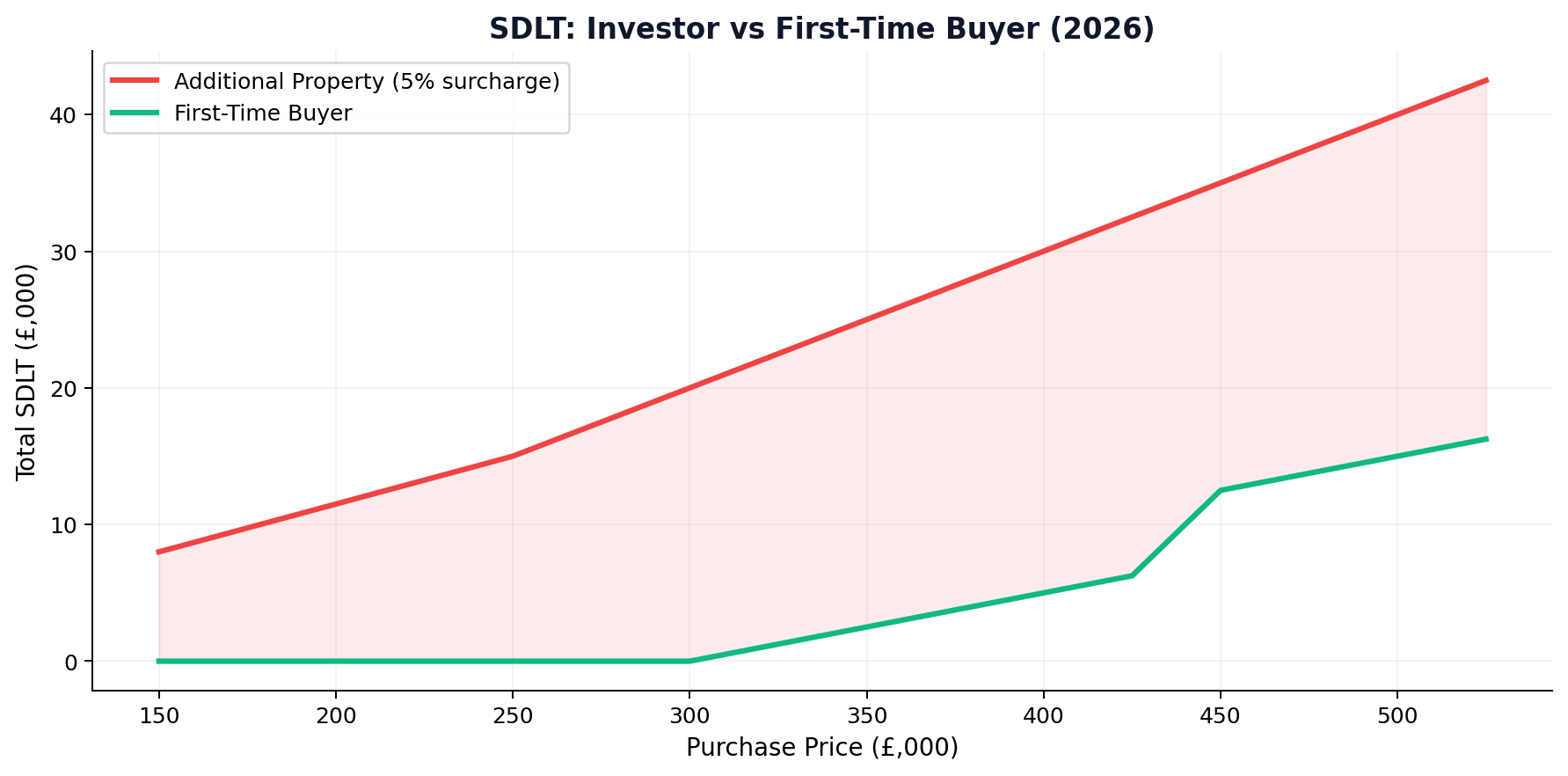

Off-plan properties attract SDLT on the contracted purchase price, not the projected completion value. This is a genuine advantage — you are taxed on today's lower price even if the property appreciates during construction.

Current SDLT Rates (as of April 2026):

| Purchase Price Band | Standard Rate | Additional Property Surcharge |

|---|---|---|

| Up to £125,000 | 0% | 5% |

| £125,001–£250,000 | 2% | 7% |

| £250,001–£925,000 | 5% | 10% |

| £925,001–£1,500,000 | 10% | 15% |

| Above £1,500,000 | 12% | 17% |

First-time buyers benefit from relief on properties up to £425,000 in England, paying 0% on the first £425,000. This makes off-plan particularly attractive for first-time buyer-investors, though you must intend to occupy the property as your main residence to qualify.

Non-UK resident surcharge: An additional 2% on top of all rates above.

Ground Rent: The Leasehold Reform Win

The Leasehold Reform (Ground Rent) Act 2022 caps ground rent at a peppercorn (effectively zero) for all new residential leases granted from 30th June 2022. This is a significant win for off-plan buyers of flats and apartments, eliminating the "doubling ground rent" clauses that plagued earlier developments. If you are buying off-plan in 2026, your ground rent should be zero. If it is not, walk away.

The Professional Snagging Process

Completion day is not the end of your due diligence — it is the beginning. A professional snagging survey (typically £300–£500) will identify defects that the developer is legally obligated to fix under the NHBC warranty.

Common defects found in off-plan completions include:

- Poorly sealed window frames (leading to draughts and condensation)

- Uneven plasterwork and paint finish

- Incorrectly fitted kitchen units and appliances

- Drainage issues in bathrooms

- External brickwork defects

You have a two-year defect liability period from completion during which the developer must remedy all reported issues at their own cost. After two years, only structural defects are covered under the NHBC warranty (years 3–10). Document everything with photographs, submit your snagging list in writing, and set clear deadlines for remediation.

The Due Diligence Checklist: 10 Non-Negotiable Steps

Before committing to any off-plan purchase, work through this checklist:

- Developer track record — Check Companies House for filed accounts, director history, and previous developments. Visit completed schemes if possible.

- Planning permission status — Is full planning granted, or only outline? Outline planning carries significantly more risk.

- NHBC or equivalent registration — Confirm the development is registered with a recognised warranty provider.

- Deposit protection — Verify your deposit is held in an escrow account or protected by an insured scheme.

- Specification schedule — Ensure it is annexed to the contract, not just referenced in marketing materials.

- Longstop date — Confirm there is a contractual deadline for completion with your right to rescind if breached.

- Ground rent structure — Must be peppercorn for new leases. Zero exceptions.

- Service charge estimate — In apartment blocks, service charges of £2,000–£4,000 per year are common and directly impact your net yield.

- Local rental market analysis — Do not rely on the developer's "projected yield." Check Rightmove, Zoopla, and SpareRoom for actual achieved rents in the postcode.

- Mortgage in principle — Secure an off-plan mortgage agreement before exchanging. Some lenders will not lend on certain developments or developers.

Conclusion: The Off-Plan Edge in 2026

Off-plan property remains one of the most powerful tools in a UK property investor's arsenal — but only for those who treat it as a surgical operation rather than a speculative punt.

The investors who are winning right now share three characteristics: they buy in high-demand regeneration zones where rental growth outpaces the rest of the market, they negotiate every available incentive from the developer, and they maintain a cash reserve large enough to absorb the unexpected — because in off-plan, the unexpected is the only certainty.

The market is currently offering a rare window. Developers are under pressure to sell, which means discounts and incentives are at their most generous. But this window will close as interest rates ease and buyer confidence returns. If you have done the research, run the numbers, and identified the right development — the time to act is now.

Next Steps:

- Run a stress test on your target property at a 6% mortgage rate to confirm the yield still works.

- Verify the developer's track record through Companies House and NHBC before engaging a solicitor.

- Secure a mortgage in principle from a lender that offers 9-month validity for off-plan purchases.

📚 Related Reading

- Best Capital Growth Property UK: Where Property Prices Are Actually Heading in 2026 and Beyond

- Passive Income Property UK: How to Build a Rental Portfolio That Actually Pays You in 2026

- Property Investments Manchester: The Definitive Investor's Guide to the UK's Most Dynamic City in 2026

- Buy dirt

- Hobbies That Make Money: Real "Cheat Codes" for Turning Your Passion Into Profit

Stop being a landlord. Start being an investor.

Shaded Canvas introduces serious capital to vetted UK property opportunities — targeting 12–16% net returns.

Start Investing →