The Angel Investment Landscape in UK Property

The UK's angel investment market is the second largest in the world, behind only the United States. With over 18,000 active angel investors across the country, there is more private capital available for property ventures than most entrepreneurs realise. The problem is not supply — it is positioning.

Most property investors who fail to raise angel capital make the same fundamental mistake: they pitch a deal instead of pitching a business. Angels are not lenders. They are experienced business professionals who deploy capital alongside their expertise, networks, and strategic thinking. If you approach them with "I need £200k for a refurb in Salford," you have already lost. If you approach them with "I have a scalable model that generates 15% net returns on student HMOs across the North West, and I need capital to acquire the next three units," you are speaking their language.

This guide is built from analysing how successful property entrepreneurs in the UK actually raise angel investment — not the theory, but the operational reality of legal structures, expected returns, pitch mechanics, and the regulatory framework that determines what you can and cannot do.

Understanding What Angels Actually Want

The Return Expectations

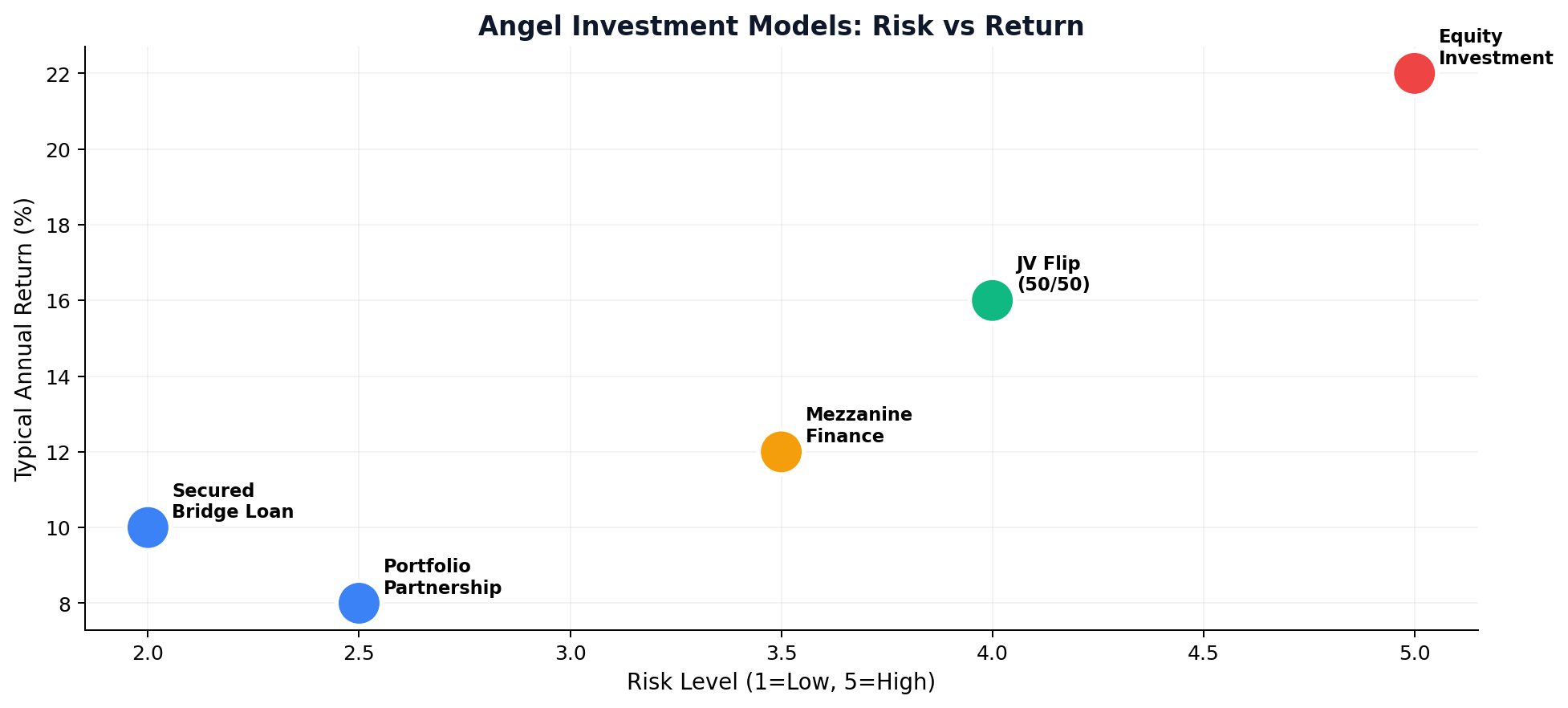

Angel investors in UK property typically expect returns in one of two structures:

Fixed-Return Lending (Most Common) The majority of property angel deals are structured as secured loans rather than equity investments. This is important because it fundamentally changes the legal and regulatory position. A typical structure:

- Interest Rate: 8–12% per annum, paid monthly or rolled up

- Security: First or second charge on the property

- Term: 12–24 months (aligned with refurb/flip timeline)

- Exit: Refinance onto a long-term mortgage or sale of the property

This structure is attractive to angels because the return is predictable, the capital is secured against a tangible asset, and the downside is protected by the property value.

Equity Joint Ventures (Higher Risk, Higher Reward) In a JV structure, the angel invests capital in exchange for a share of the profits (typically 40–60% to the angel, with the operator retaining the remainder). The appeal for the angel is the potential for significantly higher returns — a successful flip or HMO conversion might deliver 20–30% annualised returns on their capital. The risk is that their return is directly tied to the operator's competence.

Beyond Money: What Angels Bring to the Table

A good angel investor contributes far more than cash. Experienced property angels typically offer:

- Deal flow access — connections to off-market opportunities through their existing networks

- Development experience — particularly valuable for investors transitioning from single lets to HMOs or small developments

- Professional introductions — solicitors, accountants, planning consultants, and mortgage brokers who understand property investment structures

- Strategic challenge — a sounding board who will stress-test your numbers and assumptions before you commit

This is why the "angel" label matters. A passive lender gives you money. An angel gives you an unfair advantage.

Where to Find Property Angel Investors in the UK

Angel Networks and Platforms

Several established networks connect property entrepreneurs with private investors:

Angel Investment Network (angelinvestmentnetwork.co.uk) The UK's largest angel network, listing property investment opportunities from startups to established portfolios. Investors can browse opportunities across residential, commercial, and development categories. The platform charges a listing fee but provides access to a verified investor base.

Property Angels Club (propertyangelsclub.com) A members-only network specifically focused on property. This club brings together high-net-worth individuals, sophisticated investors, and property professionals to facilitate deal flow and networking. Membership provides access to curated deals and networking events.

The Angels Network (propertyangels.life) Designed for high-net-worth and sophisticated investors, this network focuses on non-equity lending opportunities — secured loans to UK property developers. Investors must self-certify as high-net-worth (annual income above £100,000 or net assets above £250,000 excluding primary residence) or as sophisticated investors.

Property Networking Events

The most effective route to angel capital is still face-to-face networking. The UK property networking scene is extensive:

- Property Investor Network (PIN) — monthly meetings in over 40 UK cities

- Progressive Property events — workshops and masterminds with active investors

- Local REIA (Real Estate Investors Association) groups — smaller, relationship-focused meetings

- Property development expos — annual events in London, Manchester, and Birmingham

The strategy is not to pitch at these events. It is to build relationships over 3–6 months, demonstrate your knowledge and track record, and let investment conversations develop organically. Angels invest in people first, deals second.

Professional Referrals

Accountants and solicitors who specialise in property investment maintain networks of active investors. A warm introduction from a shared professional adviser carries significantly more weight than a cold approach through a platform.

The Legal Framework: What You Must Get Right

FCA Regulation and the Collective Investment Scheme Trap

This is where most inexperienced property entrepreneurs get into trouble — and where the consequences can be severe.

Under the Financial Services and Markets Act 2000, arranging or managing a collective investment scheme (CIS) without FCA authorisation is a criminal offence. A CIS exists when:

- Multiple investors pool capital

- The investment is managed by a single operator

- Investors do not have day-to-day control over the scheme

If you raise money from two or more investors and manage it collectively — even informally — you may be operating an unregulated CIS. The maximum penalty is two years imprisonment and an unlimited fine.

How to Stay Legal:

- Individual deals only. Structure each investment as a separate bilateral agreement between you and one angel. Do not pool capital from multiple angels into a single fund.

- Joint venture agreements. A properly drafted JV agreement between two parties (you + one angel) is generally not a CIS, provided both parties have genuine input into decision-making.

- Secured lending. Simple loans secured against property are generally outside FCA jurisdiction. However, if you are arranging or advising on these loans as a business, you may still need FCA permissions.

- Legal advice is non-negotiable. Budget £2,000–£5,000 for a solicitor who specialises in property JV agreements and understands the FCA perimeter.

Tax Implications for Angels

How the investment is structured determines the tax treatment for both parties:

For the Angel (Lender):

- Interest income is taxed as Income Tax at their marginal rate (20%, 40%, or 45%)

- Interest must be declared on their Self Assessment tax return

- No Capital Gains Tax relief applies to interest income

For the Angel (JV Partner):

- Profit share is taxed based on the holding structure

- If the JV is a partnership, profits are taxed as Income Tax at the angel's marginal rate

- If the JV is a limited company (SPV), the angel can receive returns as dividends (taxed more favourably) or director's salary

For the Operator:

- Interest paid on angel loans is deductible against rental income if the property is held in a limited company

- If held personally, Section 24 restricts mortgage interest (and by extension, angel loan interest) relief to a 20% tax credit

SSAS and SIPP Investment

A niche but growing area: angels investing through their Self-Invested Personal Pension (SIPP) or Small Self-Administered Scheme (SSAS). These pension wrappers can invest in commercial property and, under certain conditions, lend to property ventures. The returns compound tax-free within the pension.

However, strict rules apply:

- SIPPs cannot directly own residential property (severe tax penalty if breached)

- SSAS schemes can lend money but at arm's-length terms

- Connected party transactions require independent valuation

This is specialist territory. Any angel proposing to invest through a pension should be working with a qualified pension administrator.

Building Your Angel-Ready Pitch

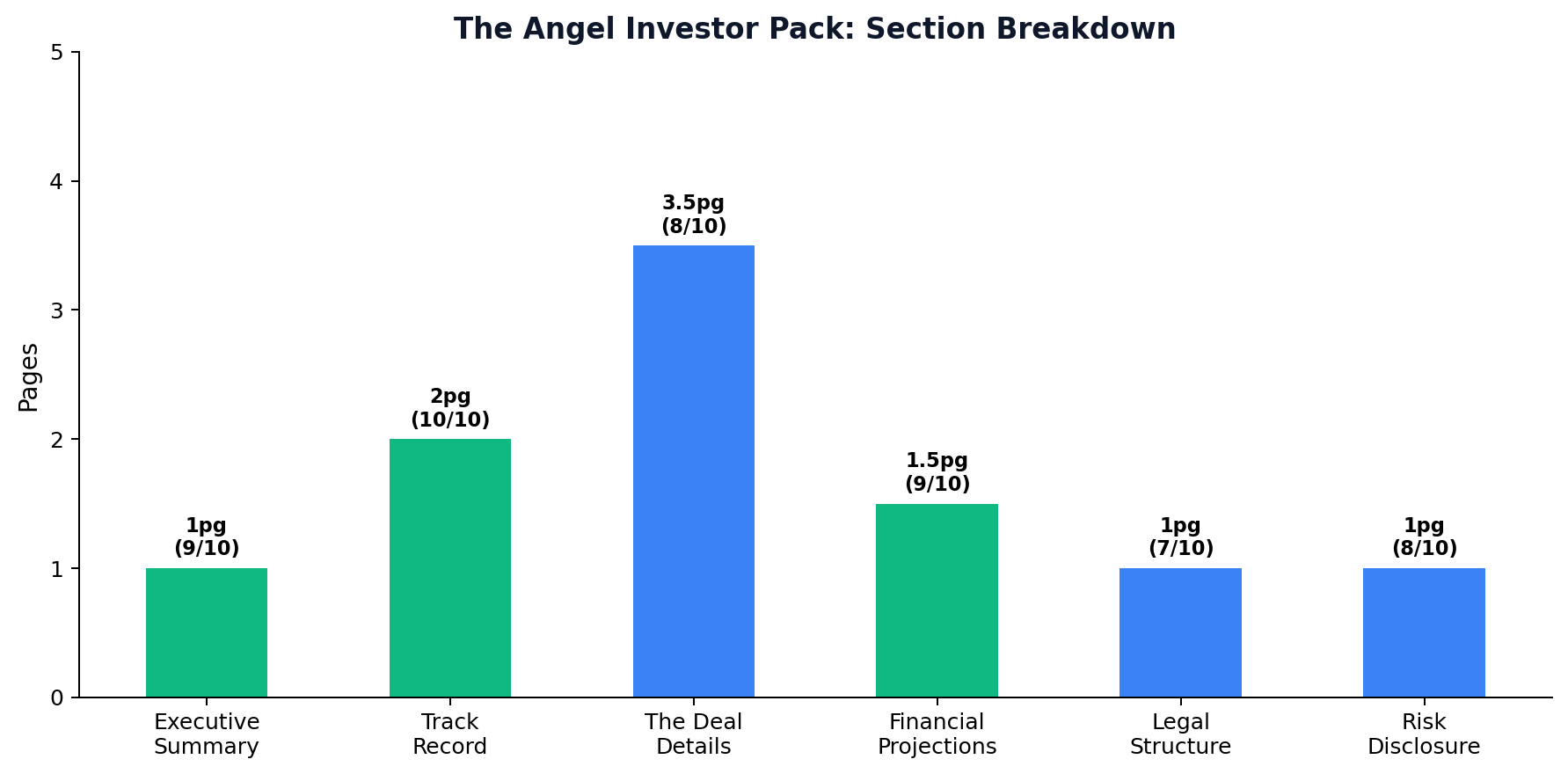

The Investor Pack

An investor pack is not a PowerPoint deck — it is a document that demonstrates you think like a business owner, not a property enthusiast. The essential components:

1. Executive Summary (1 page) Your thesis in 200 words. What you do, what returns you deliver, and what you need.

2. Track Record (2 pages) Before-and-after case studies of completed deals with actual numbers — purchase price, refurbishment cost, end value, rental income, and ROI. If you do not have a track record, be honest about this and compensate with a more detailed market analysis.

3. The Deal (3–4 pages)

- Property details and comparables

- Refurbishment scope with itemised budget

- Exit strategy (refinance or sell) with conservative projections

- Worst-case scenario and how your capital is protected

4. Financial Projections (1–2 pages) Three-year cash flow projection showing:

- Gross rental income

- Operating costs (management, maintenance, insurance, voids)

- Mortgage/loan interest

- Net profit before and after tax

- Return on angel's capital (ROI, IRR if applicable)

5. Legal Structure (1 page) How the investment will be structured — loan agreement, JV agreement, or SPV — and the security offered.

6. Risk Disclosure (1 page) Property values can fall. Projects can overrun. Tenants can default. An honest risk disclosure builds more credibility than a "guaranteed returns" promise, which is both misleading and potentially illegal.

The Pitch Meeting

Angels make investment decisions based on the person as much as the opportunity. In the meeting:

- Lead with credibility. Your opening should establish why you are capable of delivering on this plan.

- Present conservative numbers. If the deal works at pessimistic assumptions, the angel knows it works.

- Have your exit strategy ready. "What happens to my money if things go wrong?" is the first question every angel asks. Have a clear, documented answer.

- Be transparent about fees. If you are taking a sourcing fee, management fee, or performance bonus, disclose it upfront.

- Offer flexible terms. Some angels want monthly interest payments. Others prefer rolled-up interest or profit share at exit. Demonstrating flexibility shows commercial maturity.

Deal Structures That Work: Three Proven Models

Model 1: The Secured Bridge

Scenario: You find a below-market-value property requiring light refurbishment.

- Angel lends £150,000 secured by first charge on property

- Interest rate: 10% per annum, rolled up

- Term: 12 months

- You purchase at £120k, refurb £20k, end value £175k

- Exit: refinance onto BTL mortgage at 75% LTV (£131,250), repay angel with interest (£165,000)

- Your profit: £10,000 cash plus equity in the property

- Angel's return: £15,000 (10%) on a secured investment

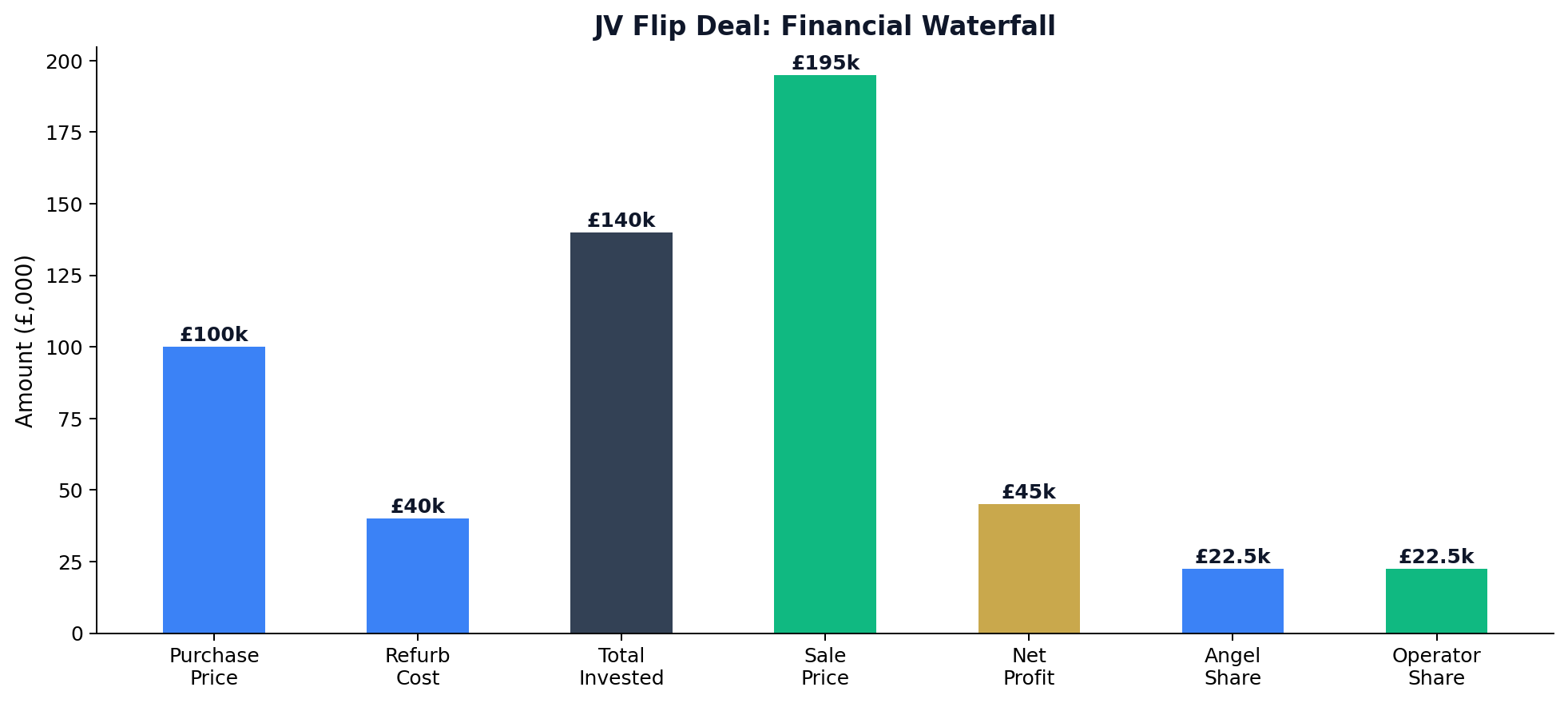

Model 2: The JV Flip

Scenario: You source a property requiring significant refurbishment and manage the project.

- Angel provides 100% of capital (purchase + refurb)

- You provide time, expertise, and project management

- Profit split: 50/50 after all costs

- Purchase: £100k, Refurb: £40k, Total: £140k

- Sale price: £195k, Net profit after costs: £45k

- Angel receives: £22,500 (profit share) + £140k (capital return)

- Your fee: £22,500 for zero capital outlay

Model 3: The Portfolio Partnership

Scenario: You operate a buy-to-hold portfolio and need growth capital.

- Angel invests £200,000 as a loan to your SPV (limited company)

- Interest rate: 8% per annum, paid monthly (£1,333/month)

- Security: Second charge across your existing portfolio (£600k+ value)

- Term: 36 months with option to extend

- You acquire and refurbish two properties, adding them to your rental portfolio

- At year 3: refinance both properties, repay angel, and retain the assets and cash flow

Common Mistakes That Kill Angel Deals

Overvaluing your contribution. If the angel is providing all the capital and you are providing "sweat equity," a 50/50 split is ambitious. Many first-time operators should accept 30–40% until they have a proven track record.

Ignoring the legal structure. Handshake deals and informal agreements are recipes for litigation. Budget for proper legal documentation from day one.

Promising guaranteed returns. It is illegal to guarantee returns on an investment (unless guaranteed by a regulated entity). Even implying guaranteed returns in your pitch materials can trigger FCA scrutiny.

Not understanding Section 24. If the property is held personally and the angel's interest payments are significant, Section 24 can create a phantom tax liability that makes the deal unviable. Always model the tax position before committing.

Rushing the relationship. Angels who invest after a single meeting are either reckless or desperate — neither is a good partner. Expect the process to take 2–4 months from first contact to capital deployment.

Conclusion: Building Your Investment Ecosystem

Property angel investment is not a transaction — it is a relationship. The most successful property entrepreneurs in the UK are not those who close one deal with one angel. They are the ones who build an ecosystem of investors, advisers, and professionals who grow together over multiple deals.

Start small. Demonstrate returns. Reinvest in the relationship. The first angel deal is always the hardest. The second is easier. By the third, your angels are introducing their friends.

Next Steps:

- Build your investor pack with actual numbers from your last deal (or a detailed market analysis if you are starting out).

- Attend three property networking events this month and focus on relationship-building, not pitching.

- Engage a solicitor who specialises in property JV agreements to draft your standard investment terms — budget £2,000–£5,000 for this foundational document.

📚 Related Reading

- Off Plan Property for Sale UK: The 2026 Investor's Playbook

- Investing in UK Property from Overseas: The Complete 2026 Framework

- Best Type of Property to Invest in UK: A No-Nonsense Breakdown of Every Strategy in 2026

- How Environment Affects Business Success

- How I save nearly £2,000 a Year on Groceries for a Family of 4

Stop being a landlord. Start being an investor.

Shaded Canvas introduces serious capital to vetted UK property opportunities — targeting 12–16% net returns.

Start Investing →