The property ladder is broken. Maybe you just need a boost.

With the average deposit now exceeding £60,000, saving for a home solo feels impossible for most under-35s. But "property" doesn't have to be a solo sport.

Whether you want to invest £1,000 for a 10% return without owning bricks and mortar, or pool resources with three friends to buy a mansion, sharing is the new owning.

This guide breaks down the two main ways to share property in 2026: the "Digital Way" (Fractional Investment) and the "Manual Way" (Co-Living). Both have massive upside, and both can ruin you if you don't read the fine print.

Method 1: The "Digital Way" (Fractional Investment)

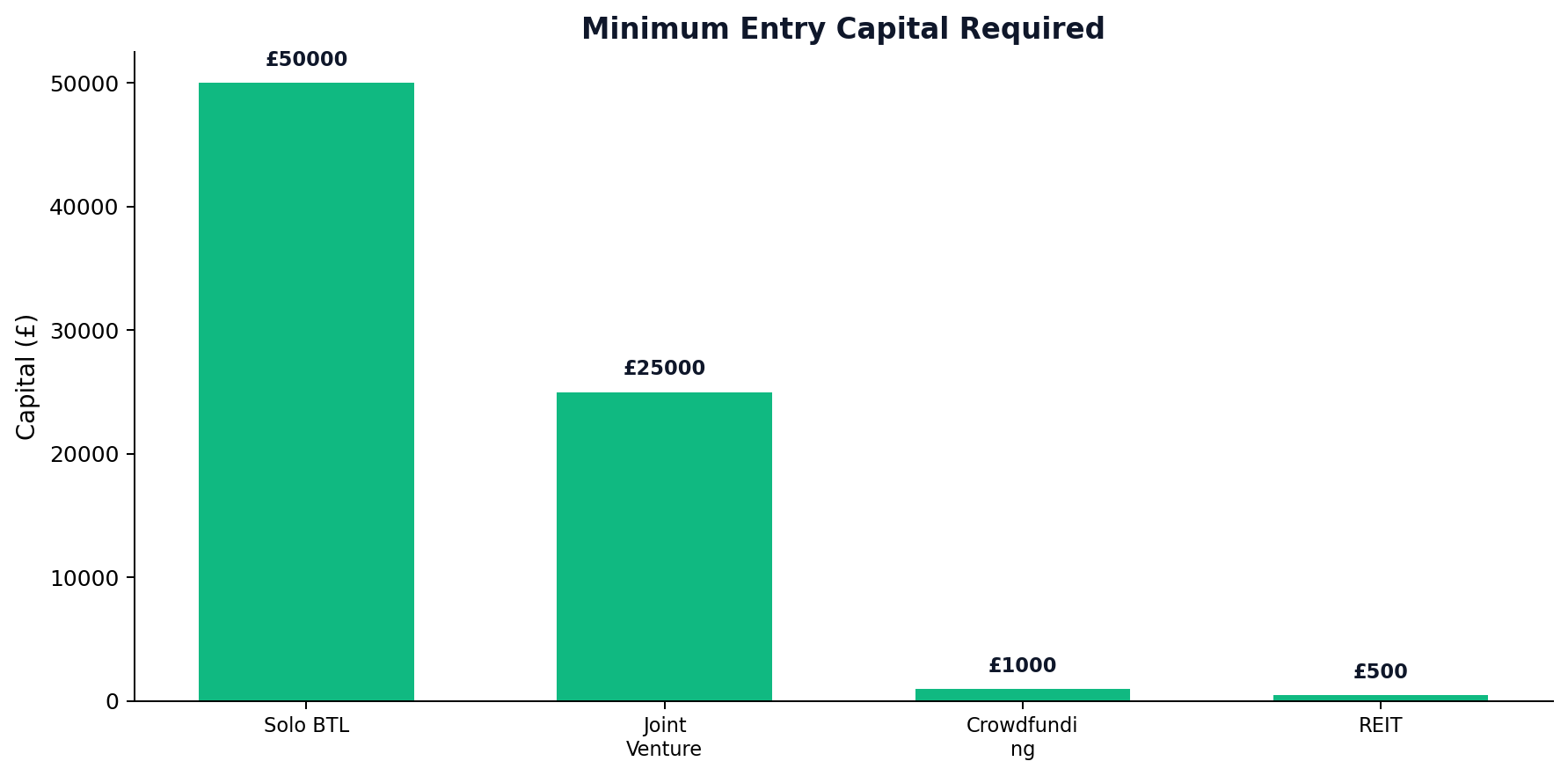

Don't want to fix toilets? Don't have £50k? This is for you. Fractional investment platforms allow you to own a "slice" of a property project for as little as £1,000.

Loan-Based Crowdfunding (Peer-to-Peer)

- The Concept: You act as the bank. You lend money to a property developer who builds homes. They pay you interest when the homes sell.

- The Platforms: CrowdProperty & Sourced Capital.

- Returns: Typically 8-10% per annum.

- Risk: The developer could go bust. Your capital is at risk. (Check if the platform has a "First Charge" security over the land—this is crucial).

Equity-Based Crowdfunding

- The Concept: You own shares in a specific rental property. You get a % of the rent and a % of the capital growth when it's sold.

- The Platforms: Property Partner (London House Exchange) & Shojin (often junior equity).

- Returns: 4-6% yield + Capital Growth.

- Risk: Values can go down. And critically, liquidity. You cannot just "sell" your shares instantly. You often have to wait for the platform to sell the entire building, which can take 5 years.

Method 2: The "Manual Way" (Buying with Friends)

This is the biggest trend of the decade. Why rent a shoebox when you and two mates can buy a 4-bed house?

The Legal Structure: Tenants in Common

If you are buying with friends, never buy as "Joint Tenants."

- Joint Tenants: You all own 100% of the property effectively. If you die, the others get your share automatically. (Great for married couples, terrible for friends).

- Tenants in Common: You own specific shares (e.g., You own 50%, Friend A owns 25%, Friend B owns 25%). If you die, you can leave your 50% to your mum/partner/dog.

The "Exit Strategy": The Deed of Trust

Living with friends is fun. Living with friends who owe you £100,000 is stressful. What happens if:

- Mike wants to move in with his girlfriend?

- Sarah loses her job and can't pay the mortgage?

- You all hate each other after 2 years?

You need a Deed of Trust. This is a legal document that sets the rules before you buy.

- The Clause: "If one person wants to sell, the others have 3 months to buy them out. If they can't, the whole house is sold on the open market." without this, one stubborn friend can trap your money in the house forever.

The Mortgage: Joint Borrower Sole Proprietor (JBSP)

Bank of Mum and Dad tapping out? Some lenders offer JBSP mortgages where up to 4 incomes can be used to calculate affordability, but only 2 people are on the title deeds (avoiding higher stamp duty for parents).

- Why use it? Boost your borrowing power to buy a bigger/better asset.

Risks: The Things Nobody Tells You

1. The "Nominee" Risk (Crowdfunding)

When you invest in a platform, you don't usually own the house directly. A "nominee company" owns it on your behalf. If the platform goes bust, extracting your asset can be a legal nightmare. Always check the platform's "Wind-Down Plan."

2. The Relationship Risk (Co-Buying)

Money changes friendships. If your friend stops paying the mortgage, the bank will come after you for the full amount (Joint and Several Liability). Ensure you trust your co-buyers with your life (and your credit score).

3. Illiquidity

Property is not Bitcoin. You cannot sell in 5 minutes. Whether it's a crowdfunding share or a physical house, assume your money is locked away for at least 3-5 years.

Figure: Minimum Entry Capital Required

Figure: Minimum Entry Capital Required

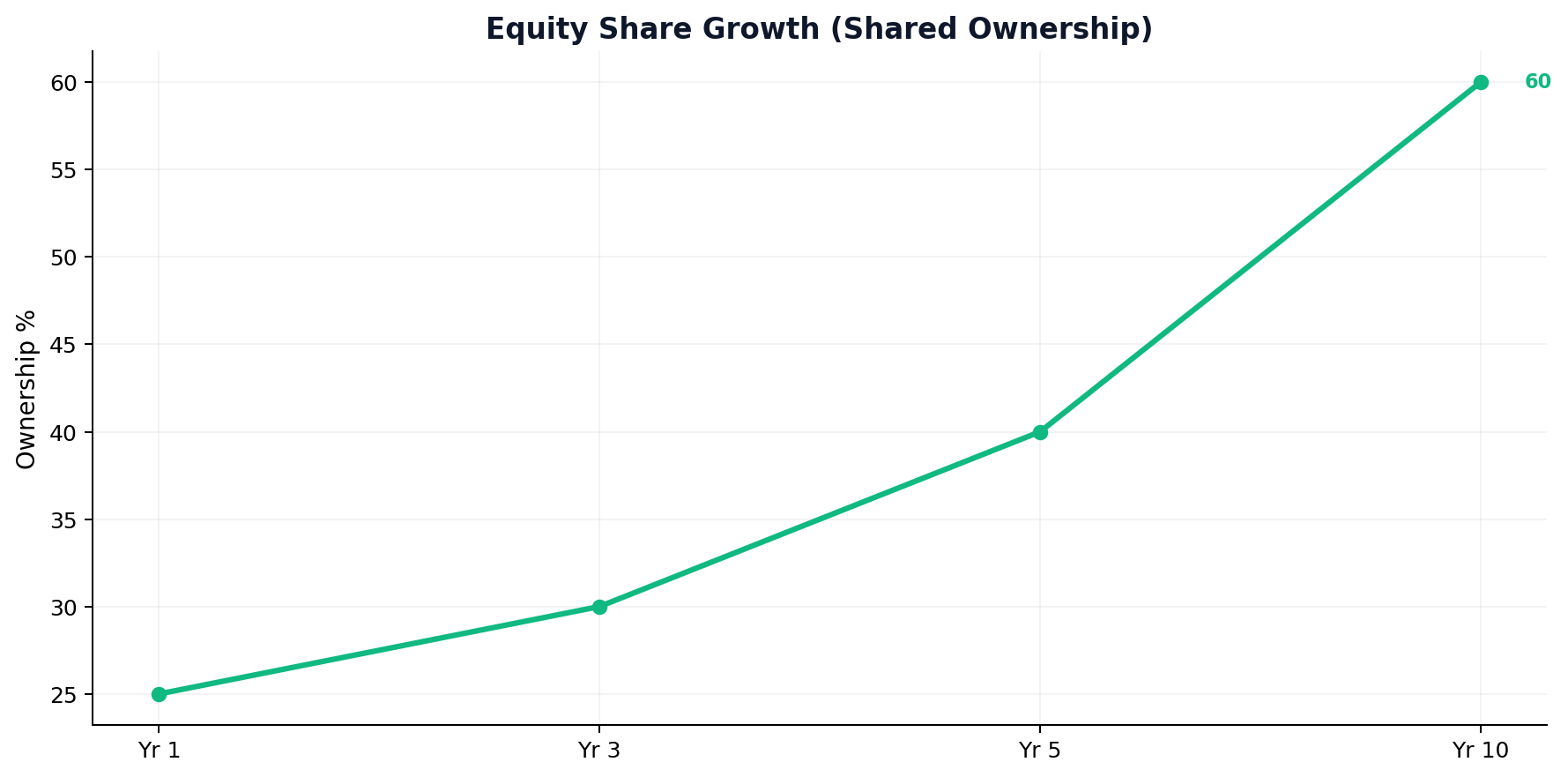

Figure: Equity Share Growth

Figure: Equity Share Growth

Conclusion: Which is right for you?

- If you have £1,000 - £10,000: Go Digital. Use a platform like CrowdProperty. It's hands-off, high-return, and you don't need a mortgage.

- If you have £30,000+: Go Manual. Club together with a trusted friend, get a Deed of Trust, and buy a physical asset. The leverage (mortgage) will make you far richer in the long run than any crowdfunding platform.

Stop being a landlord. Start being an investor.

Shaded Canvas introduces serious capital to vetted UK property opportunities — targeting 12–16% net returns.

Start Investing →