The UK buy-to-let market has undergone a historic transformation, shifting from a casual wealth-building strategy into a highly regulated, tax-heavy institutional environment. At the absolute center of this shift are the 2026 rules regarding stamp duty on buy to let properties.

If you are a landlord looking to expand your portfolio this year, understanding the exact thresholds, surcharges, and legal structuring required to mitigate Stamp Duty Land Tax (SDLT) is paramount. A miscalculation here doesn't just reduce your yield; it can entirely wipe out your first year's profits before you've even handed over the keys.

This comprehensive guide breaks down exactly how the 5% surcharge works, how non-resident penalties compound, and the legal structures savvy landlords are using to maintain robust net yields in 2026.

The 2026 Reality: The 5% Buy-to-Let Surcharge

The most critical factor dictating property acquisition strategies this year is the additional residential property surcharge. Any individual or corporate entity purchasing a residential property that is not their sole, primary residence is subject to this higher tier of taxation.

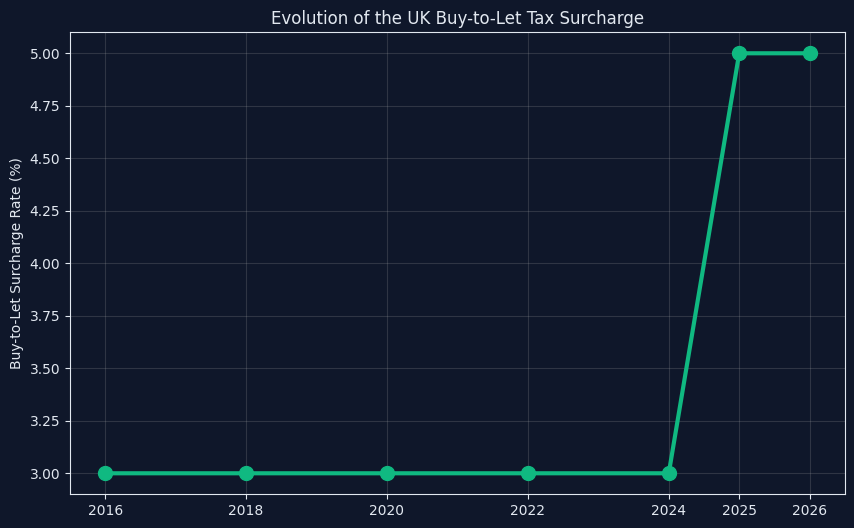

Previously set at 3%, the surcharge on any buy to let stamp duty uk acquisition was increased to a punitive 5%. This means that when calculating your purchase costs, you must add a flat 5% to every single standard SDLT tax band.

The Standard vs. Surcharge Thresholds

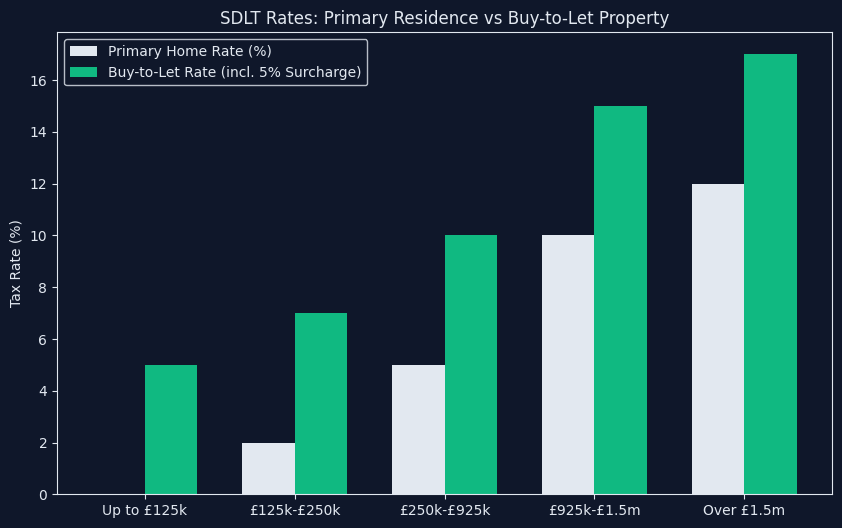

The standard nil-rate band (the amount you can spend before paying any standard SDLT) currently sits at £125,000. However, for a buy-to-let property, the 5% surcharge kicks in immediately on the entire purchase price if the property is valued at over £40,000.

Here is how the combined 2026 SDLT bands function for buy-to-let landlords:

- Up to £125,000: 5% (0% standard + 5% surcharge)

- £125,001 to £250,000: 7% (2% standard + 5% surcharge)

- £250,001 to £925,000: 10% (5% standard + 5% surcharge)

- £925,001 to £1.5 million: 15% (10% standard + 5% surcharge)

- Above £1.5 million: 17% (12% standard + 5% surcharge)

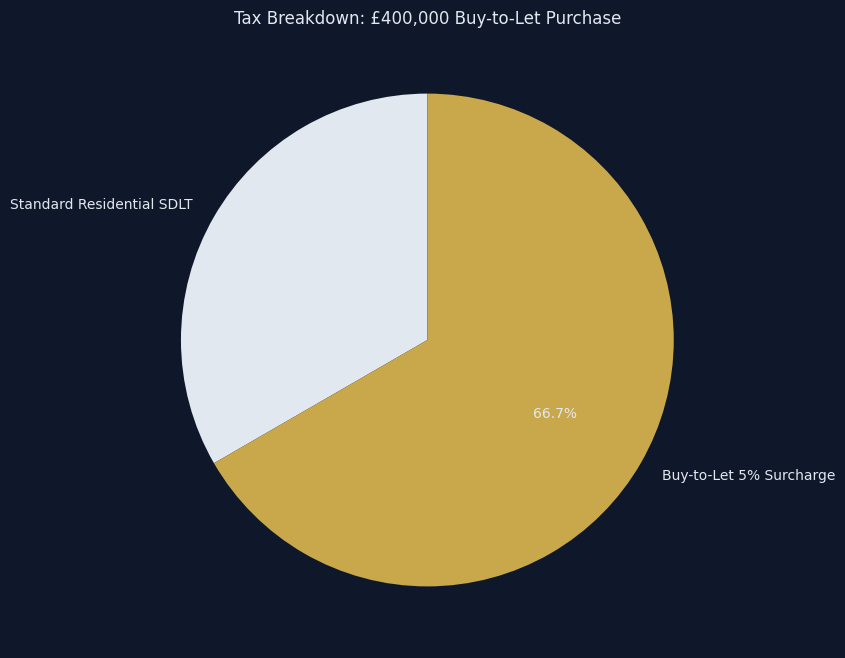

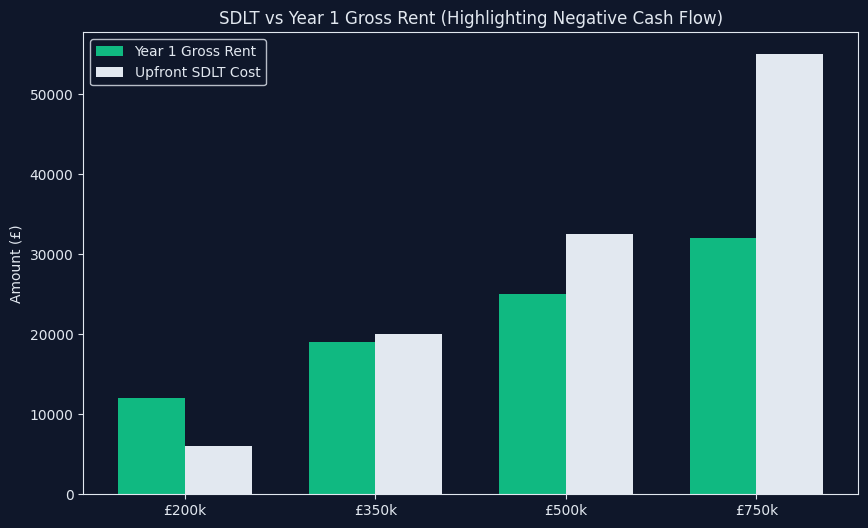

Consider a landlord purchasing a £400,000 semi-detached house. Under the standard residential rates, the SDLT would be £10,000. However, as it is a buy-to-let, the 5% surcharge adds an additional £20,000 to the bill. To complete the transaction, the landlord must produce £30,000 in liquid capital just to clear HMRC—a massive drag on initial return on investment (ROI).

The First-Time Buyer Landlord: A Cautionary Tale

A frequent strategy discussed among younger investors is attempting to use first-time buyer privileges to bypass the higher taxes. If you have never owned a property anywhere in the world, can you buy a rental property without the extra tax?

The rules here are nuanced. If you are a genuine first-time buyer and your very first purchase is a buy-to-let, you do not pay the 5% additional property surcharge, because you are not purchasing an additional property.

However, you cannot claim First-Time Buyer Relief (which eliminates standard SDLT on properties up to £300,000). First-Time Buyer Relief strict stipulates that the property must be intended as your only or main residence.

Therefore, a first-time buyer purchasing a £350,000 buy-to-let will pay the standard residential rates (£7,500), avoiding the hefty £17,500 surcharge, but forfeiting their right to claim first-time buyer relief on any future primary residence they acquire.

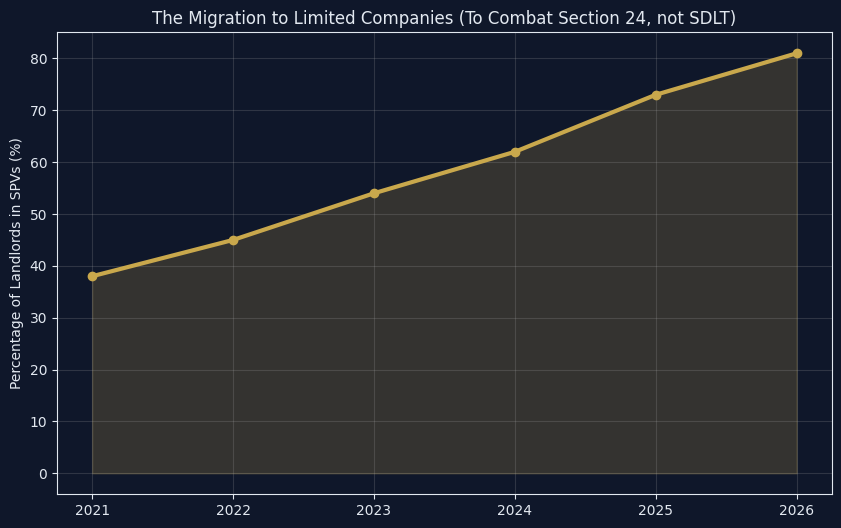

Incorporating: Does a Limited Company Save SDLT?

With the sting of Section 24 stripping away mortgage interest tax relief for higher-rate taxpayers, a massive proportion of UK landlords have transitioned to purchasing through a Limited Company (Special Purpose Vehicle, or SPV).

While an SPV is highly advantageous for income tax efficiency and portfolio scaling, it offers zero protection against the buy-to-let stamp duty surcharge.

HMRC rules state that any corporate body purchasing a residential property is automatically subject to the 5% additional property surcharge from day one, even if it is the company's very first acquisition. Furthermore, if a non-natural person (like a company) buys a residential property over £500,000 and does not intend to rent it out commercially, they face a flat 15% super-tax. Fortunately, acting as a genuine property rental business provides relief from this 15% rate, dropping you back down into the standard bands plus the 5% surcharge.

The Overseas Investor: Compounding the Tax Burden

If you are an expat landlord or a foreign national investing in the UK rental market, the mathematics require even tighter scrutiny.

The UK government levies a 2% non-UK resident surcharge on residential property acquisitions. A non-UK resident is defined strictly for SDLT purposes: if you have not spent at least 183 days in the UK during the 365 days leading up to the transaction, you are a non-resident.

Crucially, this 2% is stacked on top of the 5% buy-to-let surcharge. This means an overseas investor purchasing an additional property in the UK faces an automatic 7% tax rate on the first £125,000 of the property, escalating rapidly to 12%, 17%, and higher.

How Savvy Landlords are Adapting in 2026

The reality of the 2026 tax framework is that purchasing standard, single-let residential homes is mathematically challenging unless the property is heavily undervalued or located in a radical capital-growth hotspot.

To circumvent the brutal drag of the 5% surcharge, intelligent capital is migrating toward two distinct strategies:

1. High-Density Assets (HMOs and Co-living)

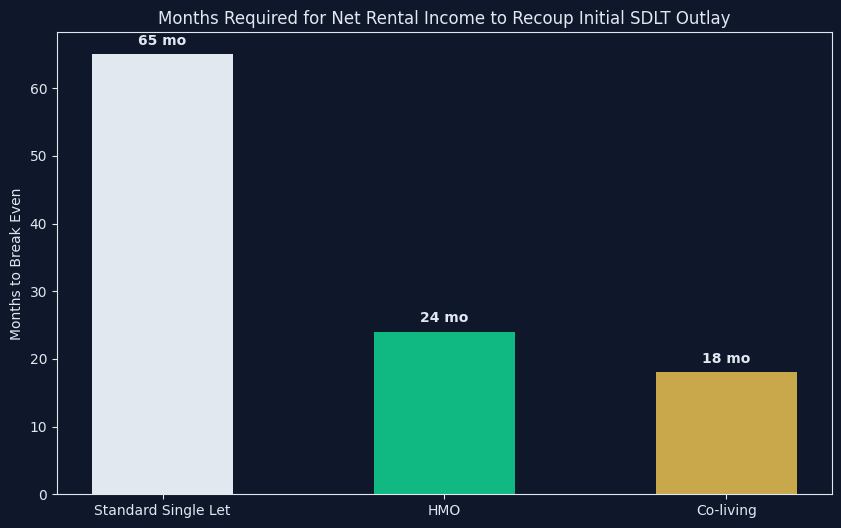

If you cannot escape the high entry tax, you must aggressively engineer the monthly cash flow to absorb it. Houses in Multiple Occupation (HMOs) transform a standard residential dwelling into a micro-apartment complex. While the acquisition still attracts the 5% buy-to-let surcharge, the gross yields—often hitting 9-12% in the North—allow landlords to recoup the SDLT outlay within the first 18-24 months, rather than the 5-7 years it takes with a standard single-let.

2. Commercial and Mixed-Use Evasion

The most potent defense against the buy-to-let stamp duty surcharge is to stop buying purely residential property altogether.

Non-residential property (commercial units, retail spaces, agricultural land) is entirely exempt from the 5% surcharge and enjoys vastly superior standard SDLT rates (topping out at 5% for properties over £250,000).

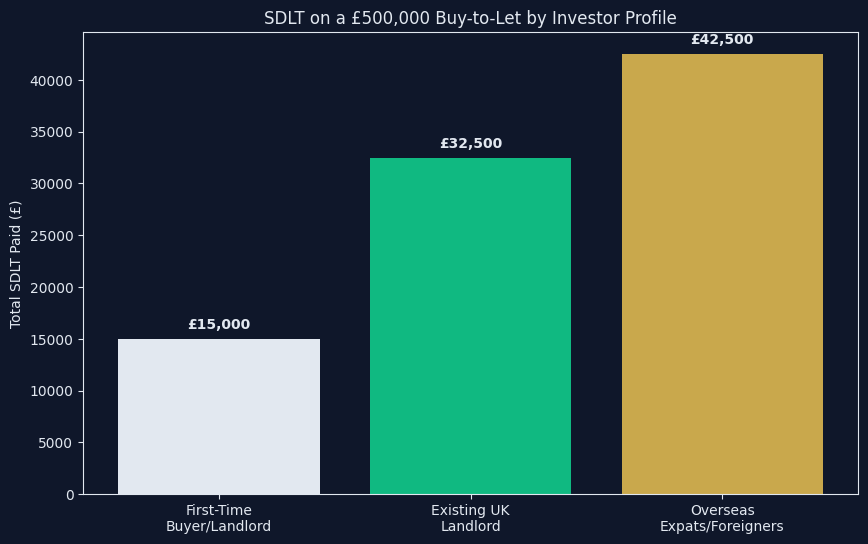

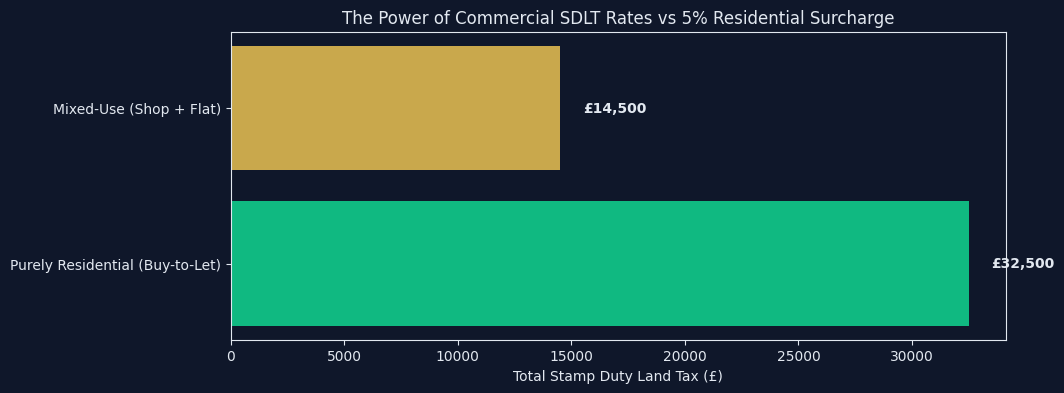

Furthermore, mixed-use property—a single transaction comprising both residential and non-residential elements, such as a high-street shop with a rental flat upstairs—is taxed completely under commercial SDLT rules. Buying a £500,000 residential buy-to-let costs £32,500 in SDLT. Buying a £500,000 mixed-use property costs £14,500. This £18,000 immediate capital saving is why mixed-use portfolios are accelerating rapidly through 2026.

The Rule of Six (Bulk Purchasing)

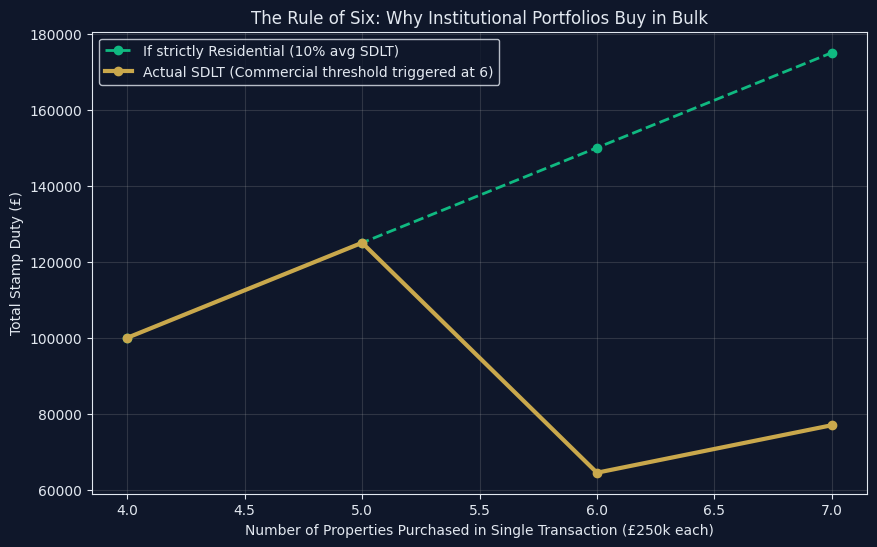

While Multiple Dwellings Relief (MDR) was controversially abolished, preventing landlords from averaging out the cost of a block of flats to lower their tax bracket, the "Rule of Six" remains intact.

If a landlord purchases six or more residential units in a single, unified transaction from the same seller, the entire acquisition is forcibly reclassified as a commercial transaction by HMRC. This strips away the 5% residential surcharge and caps the SDLT at a maximum of 5% across the entire portfolio value. For high-net-worth landlords, bulk acquiring new-build blocks off-plan is the ultimate efficiency play.

Conclusion: Strategic Financial Modeling

Surviving as a landlord in 2026 requires more than just finding a property with "good bones" in a nice area. It requires institutional-level financial modeling. The buy to let stamp duty uk surcharge is a fixed cost that permanently alters your yield curve.

Always consult a specialized property tax advisor and run exhaustive scenarios through an updated SDLT calculator before submitting an offer. By understanding exactly how these taxes interface with ownership structures, residency status, and property types, you can engineer a portfolio that generates formidable, sustainable wealth despite the hostile regulatory environment.

Stop being a landlord. Start being an investor.

Shaded Canvas introduces serious capital to vetted UK property opportunities — targeting 12–16% net returns.

Start Investing →