Whether you want to become an estate agent, buy your first investment property, or start flipping houses, the UK real estate market in 2026 offers genuine opportunity — but also more complexity than the property influencer community typically acknowledges. This guide separates the realistic from the wishful and gives you a concrete framework for entering the market, whatever your starting point.

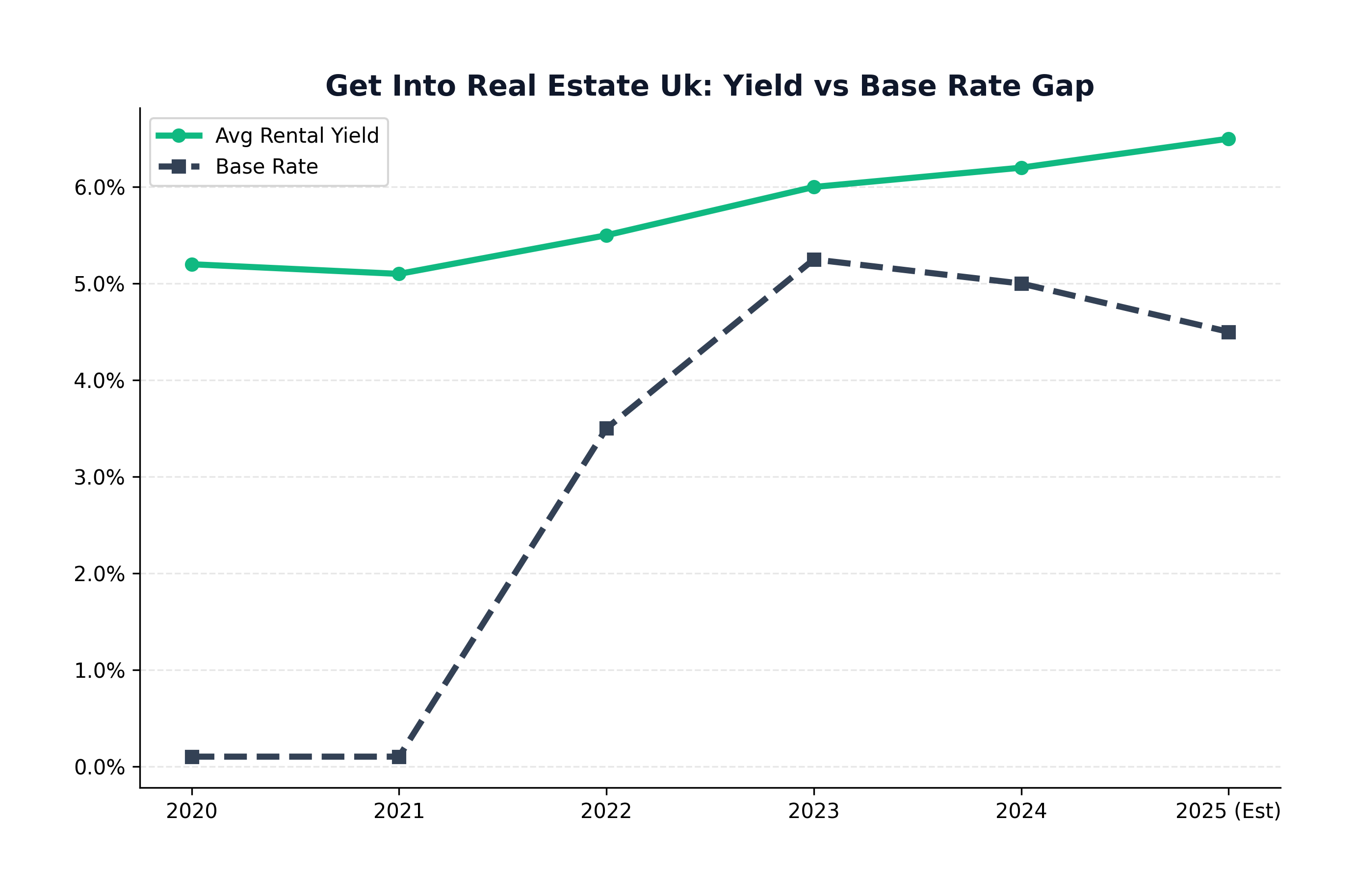

Figure: Yield vs Interest Rates

Figure: Yield vs Interest Rates

Career vs Investment: Choosing Your Path

The first distinction to make is whether you want to work in real estate (as a career) or invest in it (as a capital allocation strategy). These paths are fundamentally different in terms of skills required, capital needed, and income profile. Many people conflate them because the same vocabulary — properties, valuations, transactions — applies to both. But an estate agent is primarily a salesperson; a property investor is primarily a capital allocator. Recognising which appeals to you will save you considerable time and money.

The Estate Agency Route

Entry-level negotiator roles at estate agencies pay between £18,000 and £25,000 base salary, with OTE (on-target earnings) reaching £30,000–£40,000 once commission is included. There is no mandatory qualification to work as an estate agent in the UK — though Propertymark qualifications (the industry body's certifications) are increasingly expected by reputable agencies. The career ceiling for a top-performing agent or branch manager can comfortably exceed £70,000–£100,000 in high-value markets like London and the Home Counties. The real skill is negotiation, relationship management, and local market knowledge — not property expertise per se.

The Investor Route

Investing in property requires capital. Despite the 'no money down' strategies sold by online courses, the reality for most investors is a minimum 25% deposit for a buy-to-let mortgage, plus legal fees (circa £2,000–£3,000), survey costs (£500–£1,500), and Stamp Duty Land Tax — which on a £100,000 property as an additional dwelling stands at £3,000. A realistic minimum entry point for a conventional BTL in a Northern city is £18,000–£25,000. In London or the South East, you are looking at £60,000+ for a property that meets lender income coverage ratios.

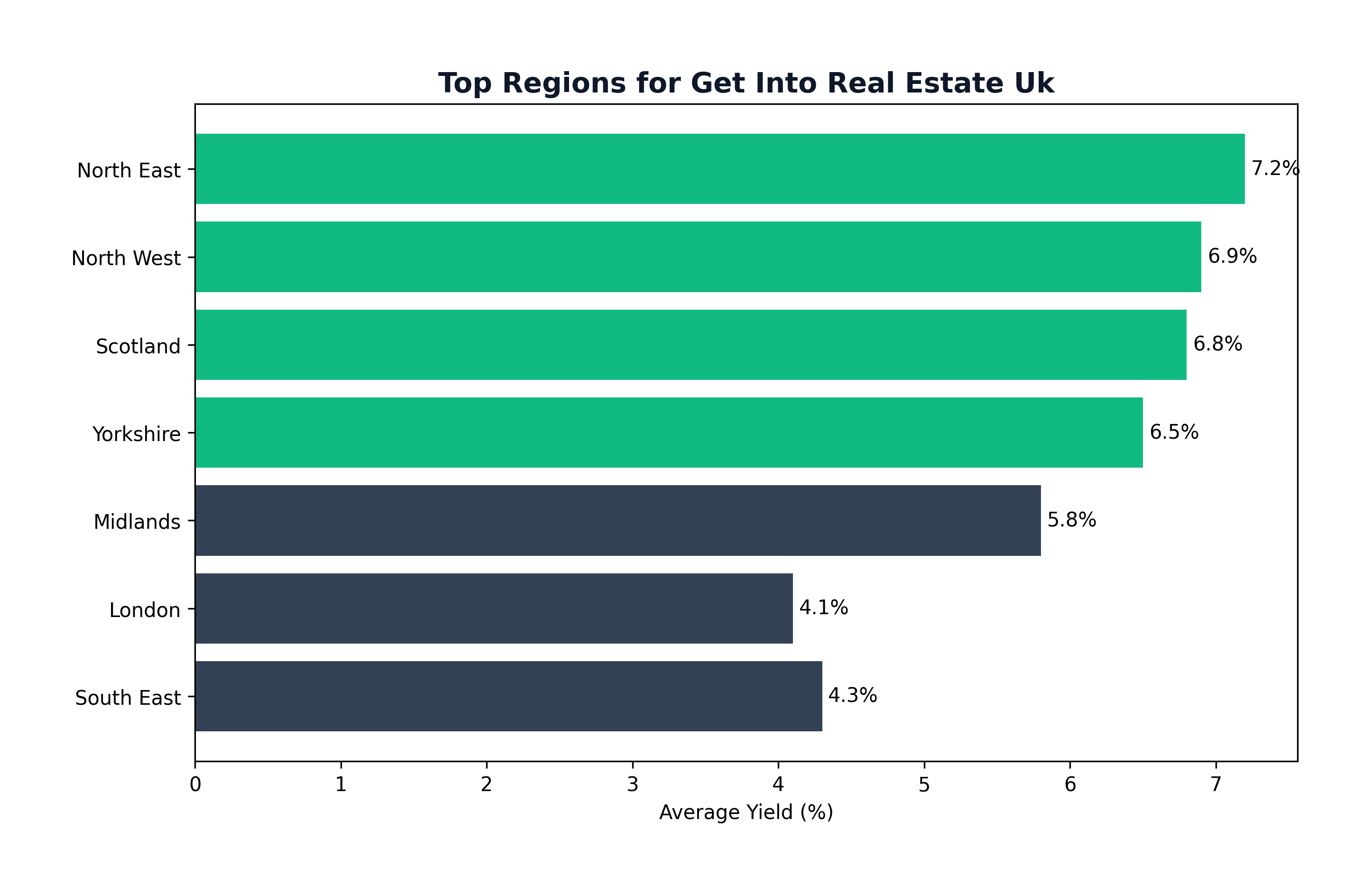

Figure: Regional Yield Heatmap

Figure: Regional Yield Heatmap

The Investment Landscape: Strategies Compared

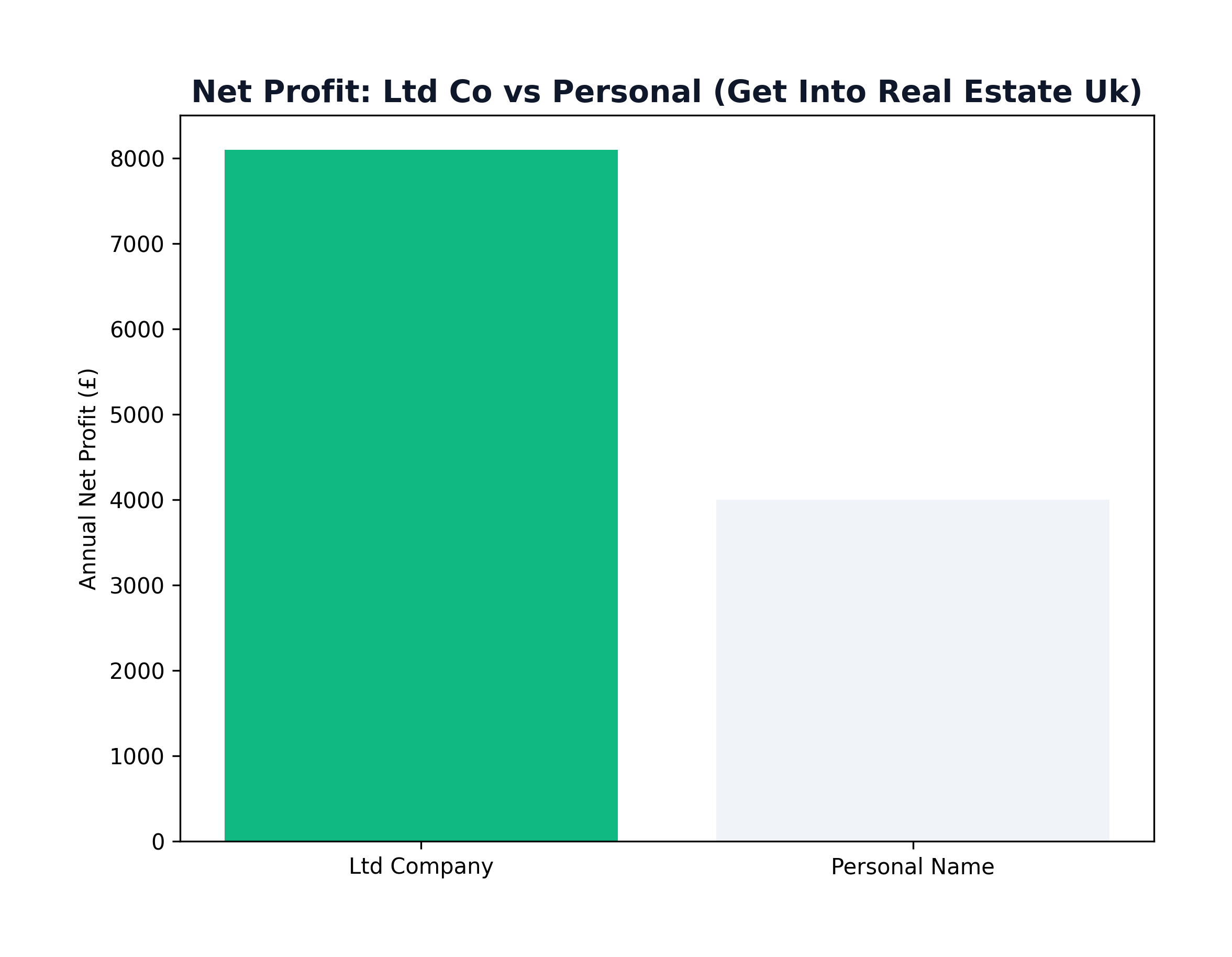

Standard Buy-to-Let remains the most common entry point for new investors — a straightforward purchase of a residential property let to a single household. However, the tax environment has deteriorated significantly for higher-rate taxpayers since Section 24 removed mortgage interest relief in 2020. This has driven almost all sophisticated investors into purchasing through a limited company (SPV), where mortgage interest remains fully deductible as a business cost.

Houses in Multiple Occupation (HMOs) — properties let room by room — deliver substantially higher yields but carry proportionally higher operational complexity. Mandatory licensing applies to larger HMOs (5+ occupants, 2+ storeys), local councils can impose Additional Licensing in designated areas, and the management overhead is significant. Many first-time investors overestimate the yield premium and underestimate the friction.

Figure: Tax Trap: Personal vs Ltd

Figure: Tax Trap: Personal vs Ltd

Financial Barriers to Entry — The Real Numbers

A common misconception is that low-income investors cannot access the BTL mortgage market. This is incorrect. While some lenders require minimum personal incomes of £25,000–£30,000, several specialist lenders have no minimum income requirement — they assess the loan purely on the rental income coverage ratio (typically 125–145% of the monthly mortgage payment at a stressed rate of 5–6%). This means the property must be capable of generating sufficient rental income, regardless of the buyer's salary. In areas where yields are 8–10%, this criterion is easily met.

Stamp Duty Land Tax is the cost that catches new investors out most often. On a £150,000 investment property (typical in Northern cities), an investor who already owns their home pays a 3% surcharge across the purchase — £4,500 — before standard rates apply. First-time buyers purchasing an investment property lose their FTB relief. Always model SDLT into your acquisition costs before making an offer.

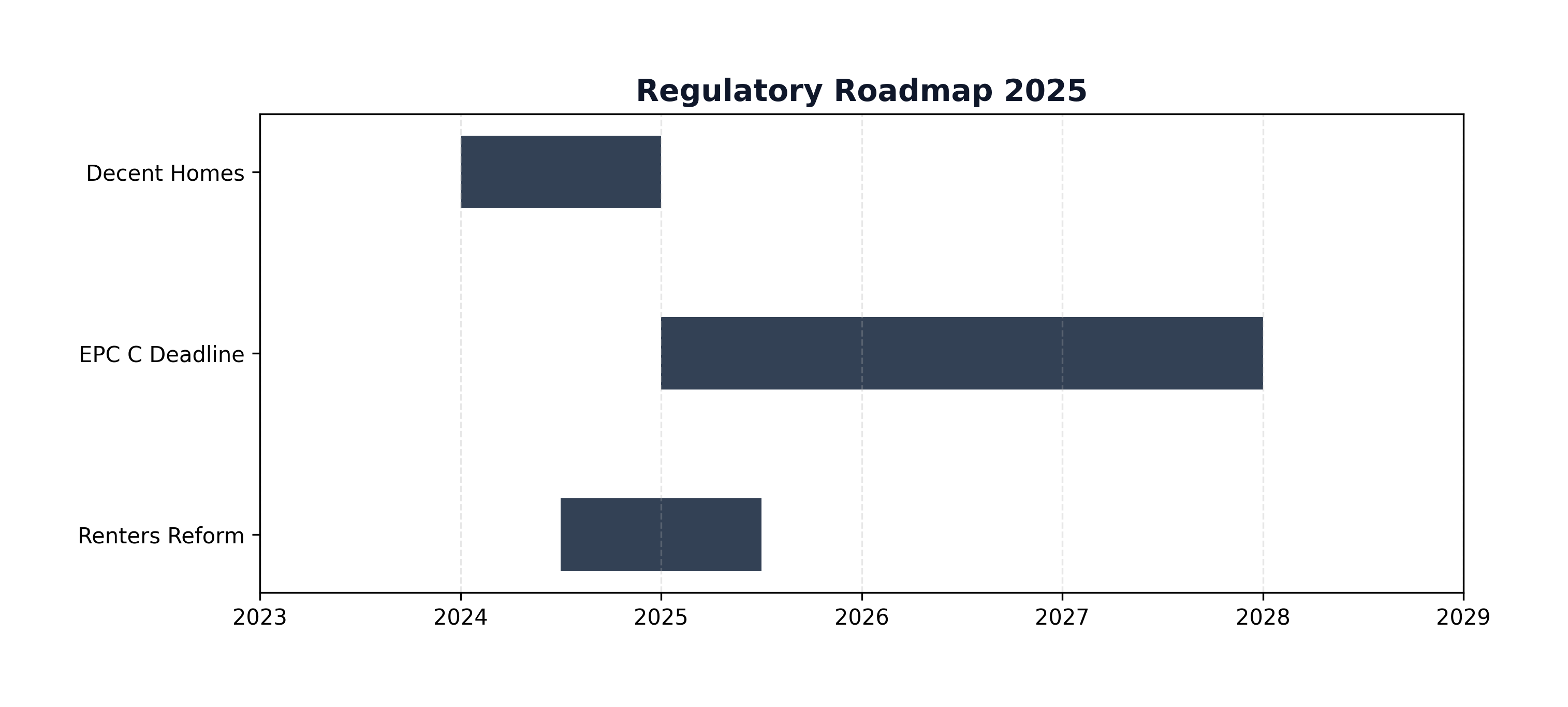

Figure: Regulatory Roadmap

Figure: Regulatory Roadmap

Education and Networking — Avoiding the £5,000 Guru Trap

The UK property education market is saturated with high-ticket 'mentorship programmes' and weekend seminars costing £3,000–£10,000. The honest assessment is that the foundational knowledge — how mortgages work, how to evaluate deals, how to manage tenants — is freely available through the podcasts Property Hub, Inside Property Investing, and the BiggerPockets UK content, as well as through PIN (Property Investor Network) meetings, which are free to attend in most cities.

What paid communities can genuinely offer is accountability, deal flow, and access to experienced investors willing to answer questions. If you are evaluating a paid programme, the test is simple: does the trainer generate the majority of their income from property investing, or from selling education? The former is a credible operator; the latter is a red flag regardless of the marketing language.

Building a 'power team' is more valuable than any course: a specialist BTL mortgage broker (essential), a conveyancing solicitor experienced in investment purchases, and a reliable local builder. These relationships compound in value over time and are not sold at any seminar.

Figure: Strategy Cycle

Figure: Strategy Cycle

Your 90-Day Action Plan

Days 1–30: Establish your financial baseline. Understand your credit score, how much deposit you can access (including equity in any existing property), and what your maximum mortgage borrowing looks like. Get an Agreement in Principle from a BTL broker — not a high street bank.

Days 31–60: Target a strategy and geography. Research rental yields using Rightmove rental data versus sold prices on Zoopla. Identify two or three areas where gross yields exceed 7%. Visit the area on a weekday to assess demand, regeneration signals, and local lettings agent quality.

Days 61–90: View properties actively, with a pre-built deal analysis spreadsheet. Model every deal at 7% mortgage rate (stress test), 10% management fees, 10% void allowance, and £500/year maintenance reserve. If the numbers work after all deductions — proceed to solicitors.

Stop being a landlord. Start being an investor.

Shaded Canvas introduces serious capital to vetted UK property opportunities — targeting 12–16% net returns.

Start Investing →