London has weathered recessions, Brexit shocks, and global pandemics — and still commands premium pricing from international buyers. For overseas investors evaluating where to place capital in 2026, London remains the top-ranked city for cross-border real estate investment in Europe, drawing buyers from Hong Kong, the Middle East, the United States, and Singapore in significant volumes. This guide explains the macro case, the best areas, the tax reality, and the step-by-step process for non-resident buyers.

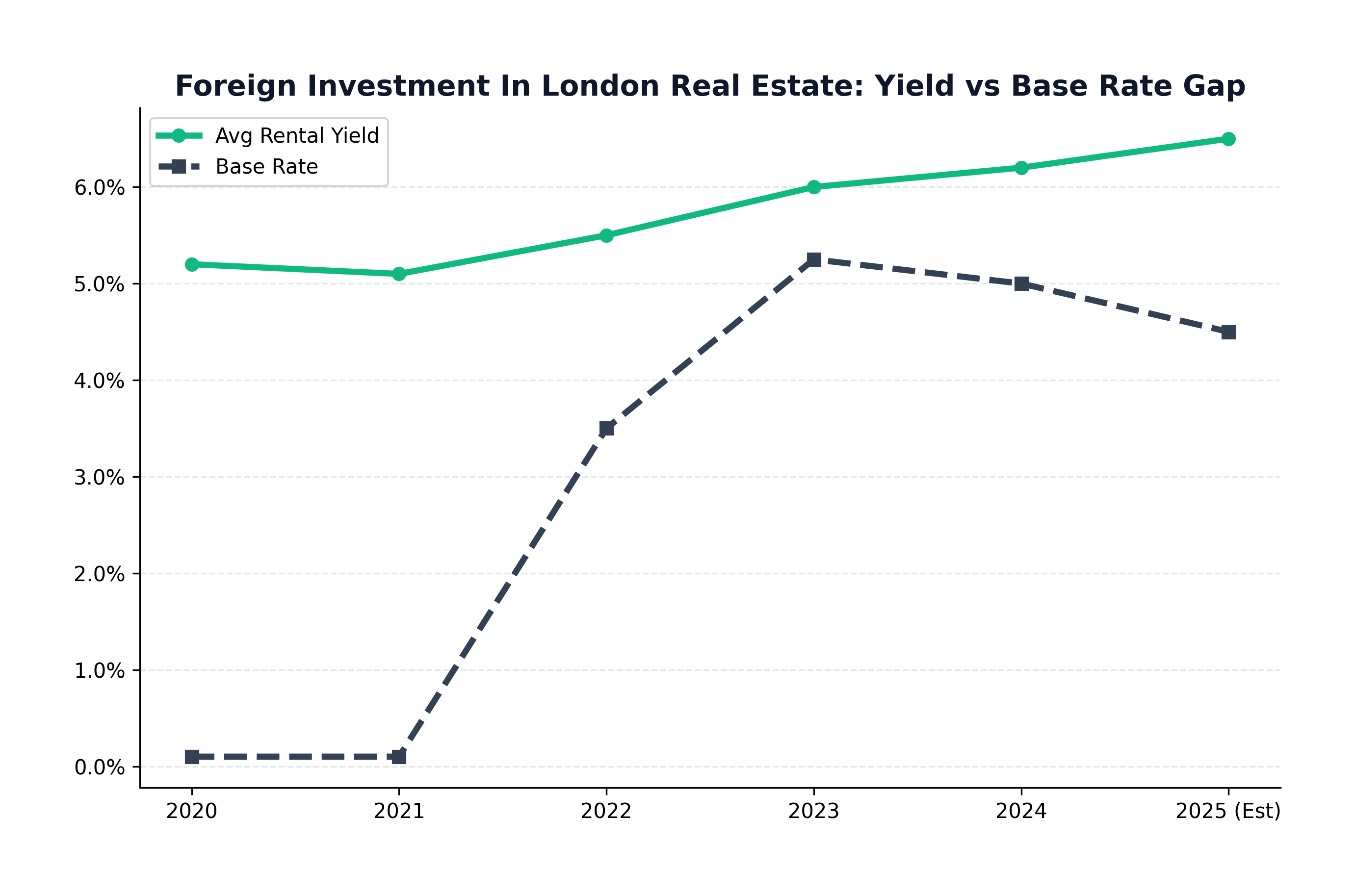

Figure: Yield vs Interest Rates

Figure: Yield vs Interest Rates

Why London? The Macro Case for Foreign Buyers

London's safe-haven status is not marketing language — it is embedded in the city's structural advantages. The rule of law underpins everything: English contract law is the global standard, property rights are transparent and enforceable, and disputes can be resolved through a court system that foreign investors trust implicitly. This legal certainty is genuinely rare on a global stage and commands a premium that most overseas buyers are willing to pay.

The city's time zone sits at the intersection of Asian and American trading hours, making it the natural headquarters for multinationals. That corporate demand creates sustained rental pressure from relocated executives, financial services professionals, and tech workers — the tenant cohort that keeps Prime Central London (PCL) voids low and rents stable. Proximity to world-ranked universities — Imperial College, UCL, LSE — adds another layer: a permanent pipeline of high-earning graduates who extend demand into zones 2 and 3.

Currency is the current entry point. Sterling's relative weakness against the US dollar, Hong Kong dollar, and UAE dirham since 2016 has created a structural discount for dollar-denominated buyers. A buyer purchasing in USD is effectively acquiring London property at a 20–25% discount versus the pre-referendum exchange rate. This FX tailwind does not last indefinitely, but it is a meaningful accelerant for overseas demand in 2026.

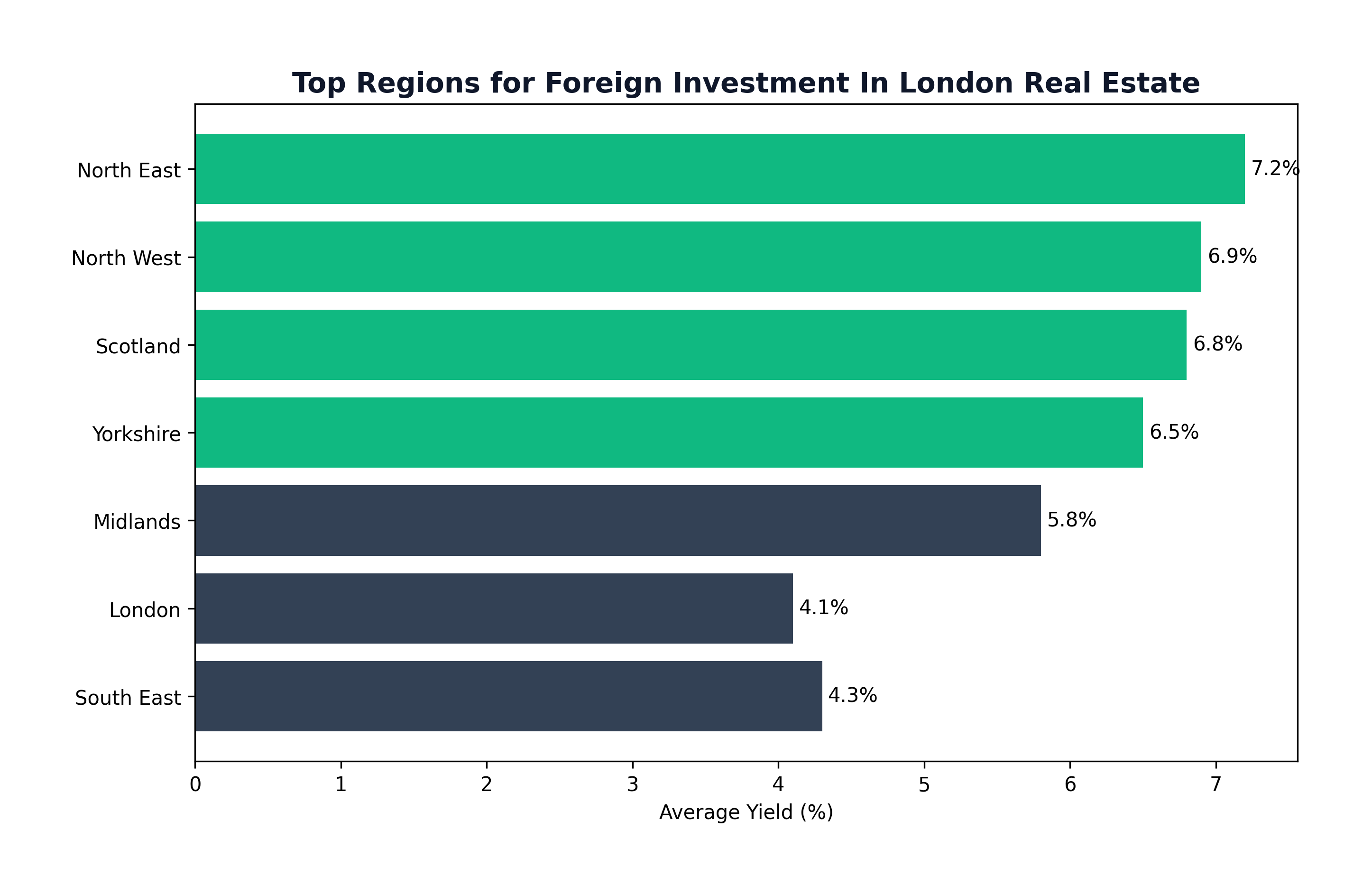

Figure: Regional Yield Heatmap

Figure: Regional Yield Heatmap

The 'Flight to Quality' in Prime Central London

PCL — loosely defined as Mayfair, Knightsbridge, Belgravia, Chelsea, and Kensington — has seen a bifurcation from the wider London market. While mid-range zones have experienced price stagnation, trophy assets in PCL have held value or appreciated modestly. The reason is straightforward: supply is permanently constrained (you cannot build more Georgian townhouses in Mayfair) and the buyer pool is globally diverse. When Chinese buyers pull back, Middle Eastern buyers fill the gap; when Americans hesitate, European capital steps in.

This dynamic insulates PCL from the domestic mortgage cycle that drives pricing in zones 3–6. Foreign buyers are frequently cash purchasers or use private banking facilities rather than conventional mortgages, removing rate sensitivity from their decisions. This makes PCL a genuinely different asset class to 'London property' as a whole.

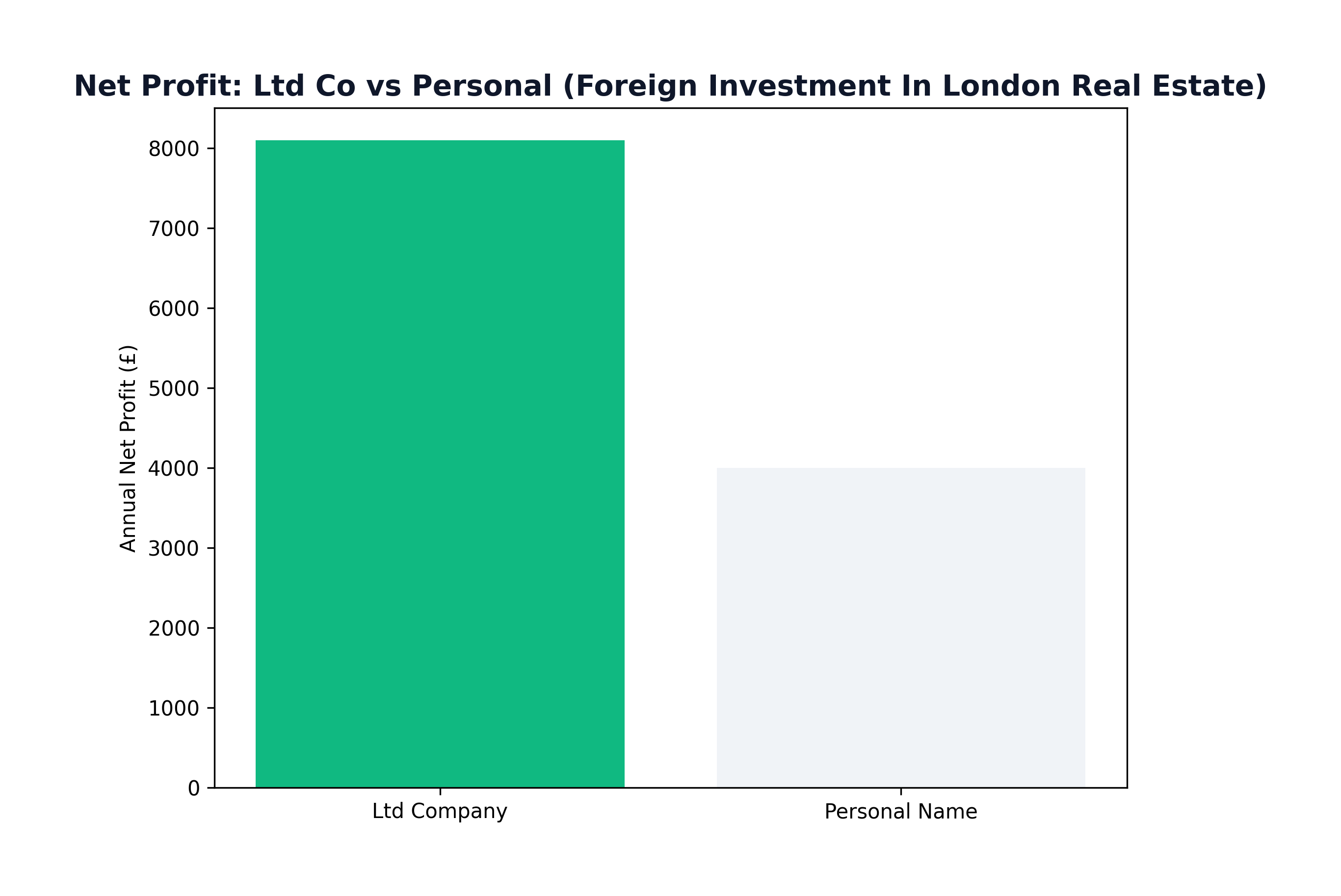

Figure: Tax Trap: Personal vs Ltd

Figure: Tax Trap: Personal vs Ltd

Top Areas for Foreign Buyers in 2026

Mayfair & Knightsbridge — The Classics

Average pricing: £2,000–£5,000+ per square foot. These boroughs continue to attract ultra-high-net-worth (UHNW) buyers seeking trophy assets, embassy-zone rentals, and storage of wealth in bricks. Rental yields are modest at 2.5–3.5%, but capital preservation and potential appreciation are the primary draw. The Grosvenor Estate's ongoing stewardship ensures area quality is protected.

King's Cross & Nine Elms — Regeneration Growth

King's Cross has transformed into one of London's most vibrant live-work destinations, anchored by Google's European HQ. Nine Elms (home to the US Embassy and extensive new-build stock) appeals to investors seeking higher yields (3.5–4.5%) and modernisation-era growth. Both areas have benefitted from significant public infrastructure investment and attract young professionals as tenants — the exact cohort that international investors prefer.

Canary Wharf — Yield Focus

Canary Wharf delivers the highest rental yields in Inner London at 4.5–5.5%, driven by financial services tenants and proximity to Crossrail. New waterfront developments including Wood Wharf offer contemporary stock with service charges factored into pricing. The area is best suited to investors prioritising income over capital appreciation, as the Wharf's long-term growth story is more contested than central zones.

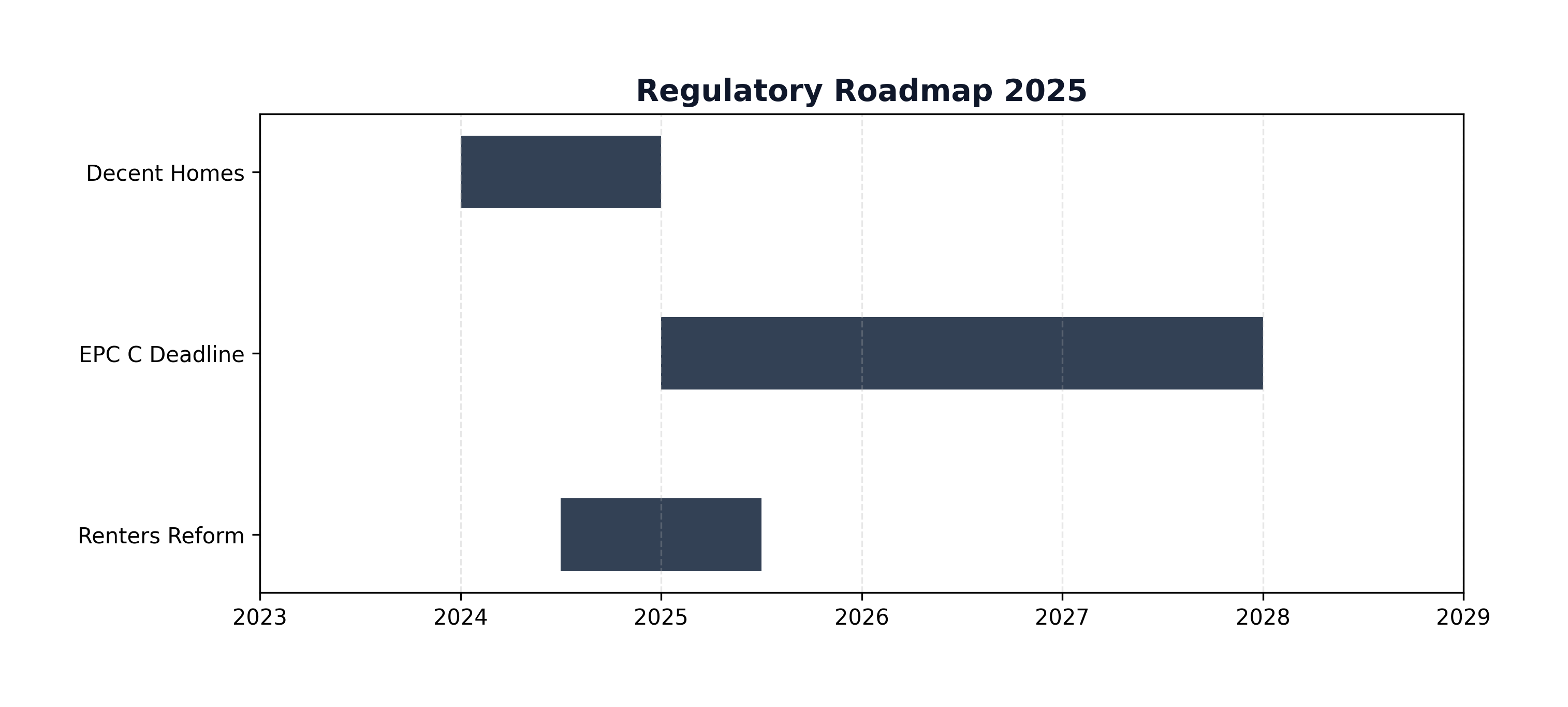

Figure: Regulatory Roadmap

Figure: Regulatory Roadmap

The Tax Reality for Overseas Buyers

Overseas buyers face a 2% SDLT (Stamp Duty Land Tax) surcharge on top of standard residential rates — applied since April 2021 and showing no sign of reversal under the current government. On a £2 million property, this adds £40,000 to acquisition costs. On top of this, the existing 3% additional property surcharge (for buyers who already own any residential property anywhere in the world) applies, meaning total SDLT for many foreign buyers can reach 17% on the portion above £1.5m.

For high-value properties held in corporate structures, the Annual Tax on Enveloped Dwellings (ATED) is a critical consideration. Properties worth over £500,000 held by companies are subject to annual ATED charges ranging from £4,150 to £269,450 depending on value. Relief is available for genuine lettings, but the compliance burden is real. Inheritance Tax (IHT) exposure for non-domiciled individuals has been significantly tightened — post-April 2026 reforms mean that UK residential property held through offshore structures is now firmly within the IHT net for long-term UK residents, requiring careful structuring advice before purchase.

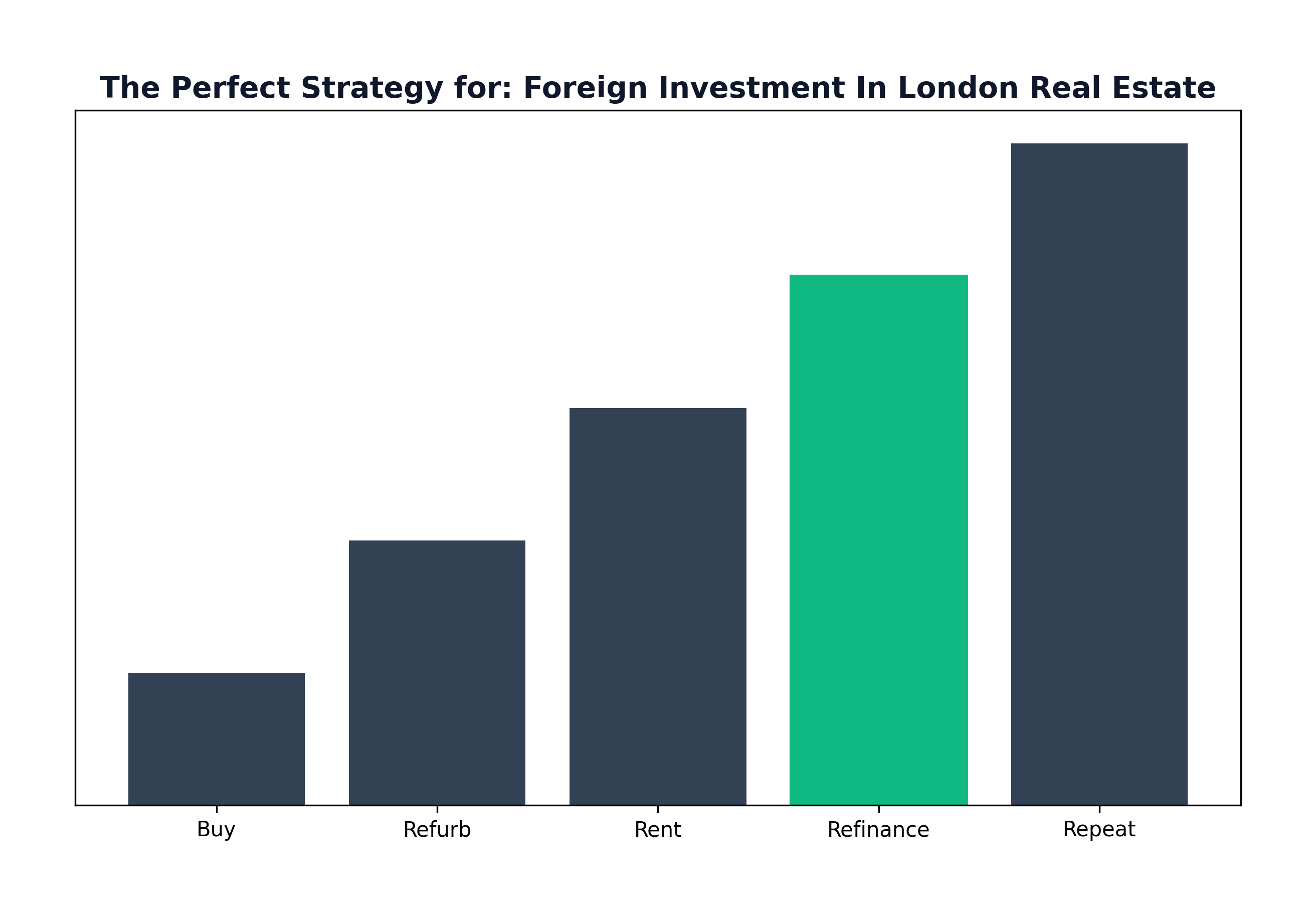

Figure: Strategy Cycle

Figure: Strategy Cycle

Buying Process: A Step-by-Step Guide for Non-Residents

The biggest friction point for foreign buyers is KYC/AML compliance — Know Your Customer and Anti-Money Laundering checks required by estate agents, solicitors, and lenders. Buyers must demonstrate a clean, documented source of funds. This typically requires bank statements going back 12–24 months, evidence of the transaction that generated the capital (sale of business, inheritance, salary history), and in some cases a letter from an accountant or lawyer in the country of origin. The process is bureaucratic but navigable with preparation.

Using an international broker versus going direct to an estate agent has measurable advantages. International brokers maintain relationships with developers, off-market sellers, and private offices — access that a buyer approaching an estate agent cold will not receive. A dedicated buying agent adds a further layer: they negotiate on your behalf, identify structural or leasehold issues early, and ensure the price is defensible against comparable sales data. Their fee (typically 1–2% of purchase price) frequently pays for itself in negotiated discounts.

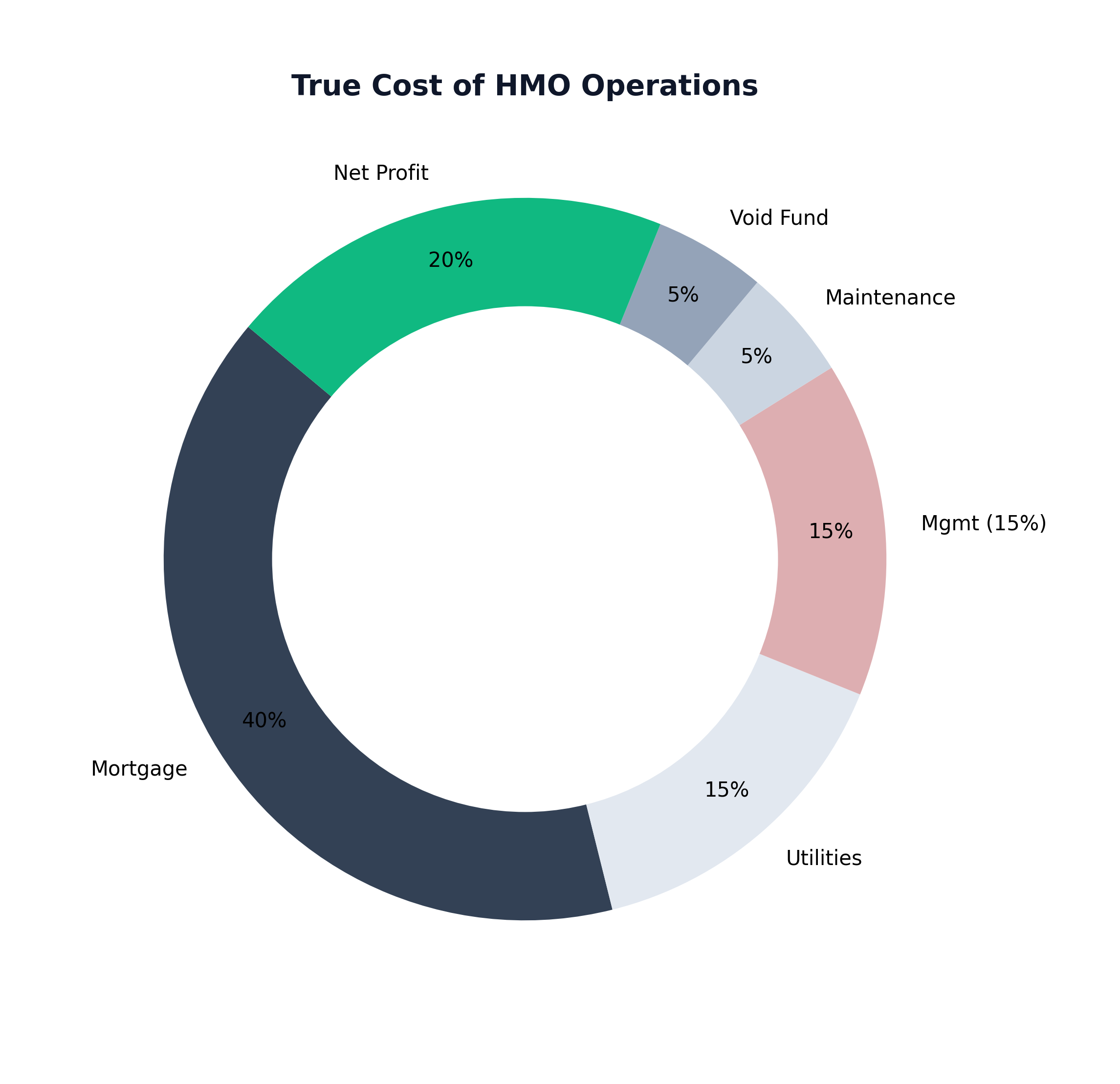

Figure: HMO Expense Breakdown

Figure: HMO Expense Breakdown

Financing & Mortgages for Overseas Buyers

The overseas buyer mortgage market is specialist but active. Lenders including HSBC Expat, Barclays International, and several private banks offer mortgages to non-UK residents based on foreign income — though maximum LTVs are typically 65–75% rather than the 90%+ available to residents. Interest-only products are widely available to HNWIs (typically requiring £300k+ income or £3m+ in assets), reducing monthly outflows and preserving capital for further investment.

Many sophisticated overseas buyers structure their purchase via a UK Special Purpose Vehicle (SPV) — a limited company incorporated for the purpose of holding the property. This can offer corporation tax advantages on rental profits (25% vs up to 45% for personal ownership), though the mortgage rates are typically 0.5–1% higher for limited company borrowers, and SPV mortgages are assessed purely on rental income coverage ratios. Legal advice on the appropriate structure is essential before exchange of contracts.

Stop being a landlord. Start being an investor.

Shaded Canvas introduces serious capital to vetted UK property opportunities — targeting 12–16% net returns.

Start Investing →