PGIM Real Estate — the property investment arm of Prudential Financial, the US insurance and asset management giant — has built one of the most distinctive UK real estate strategies of any global manager, with a specific focus on Single-Family Rental (SFR) and affordable housing. With over £310 million committed to UK affordable housing and a growing portfolio of energy-efficient family homes across England, PGIM's UK platform offers institutional investors a rare combination of financial returns, inflation protection, and measurable social impact.

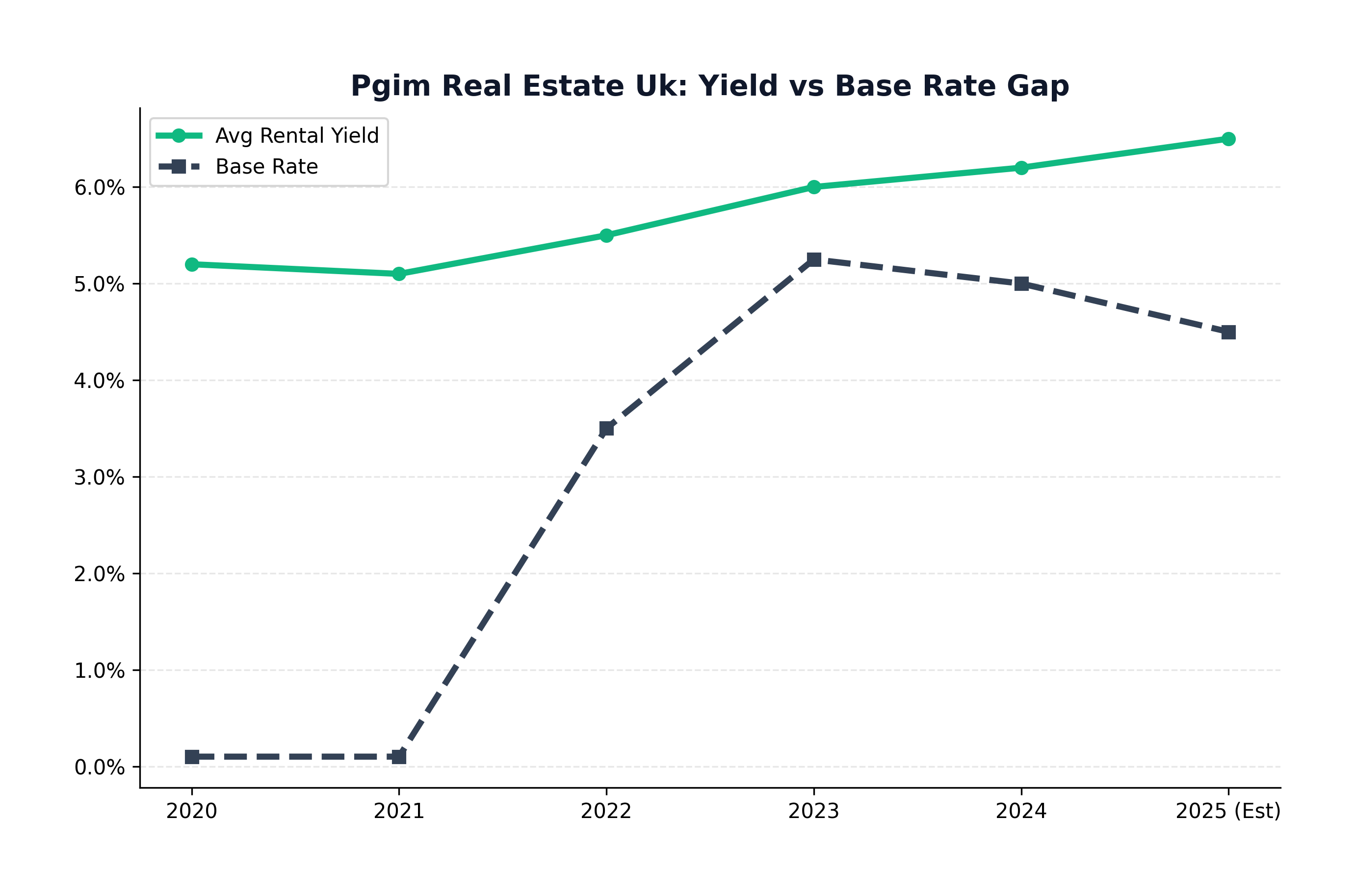

Figure: Yield vs Interest Rates

Figure: Yield vs Interest Rates

PGIM Real Estate: The Prudential Connection

PGIM (Prudential Global Investment Management) manages over $1.3 trillion in assets across all asset classes, with real estate representing a significant component — approximately $200 billion in property equity and debt globally. The UK real estate team operates as part of PGIM's European platform, combining local expertise in housing markets, planning, and development with the capital base and institutional credibility of a Tier 1 global manager.

The connection to Prudential Financial — one of the US's largest insurance and annuity providers — creates a natural alignment with the affordable housing strategy's income profile. Long-term, inflation-linked rental income precisely matches the liability structure of annuity providers: predictable, growing, long-duration cash flows. PGIM's own principal capital has been deployed into the strategy alongside third-party investor capital — a powerful signal of conviction.

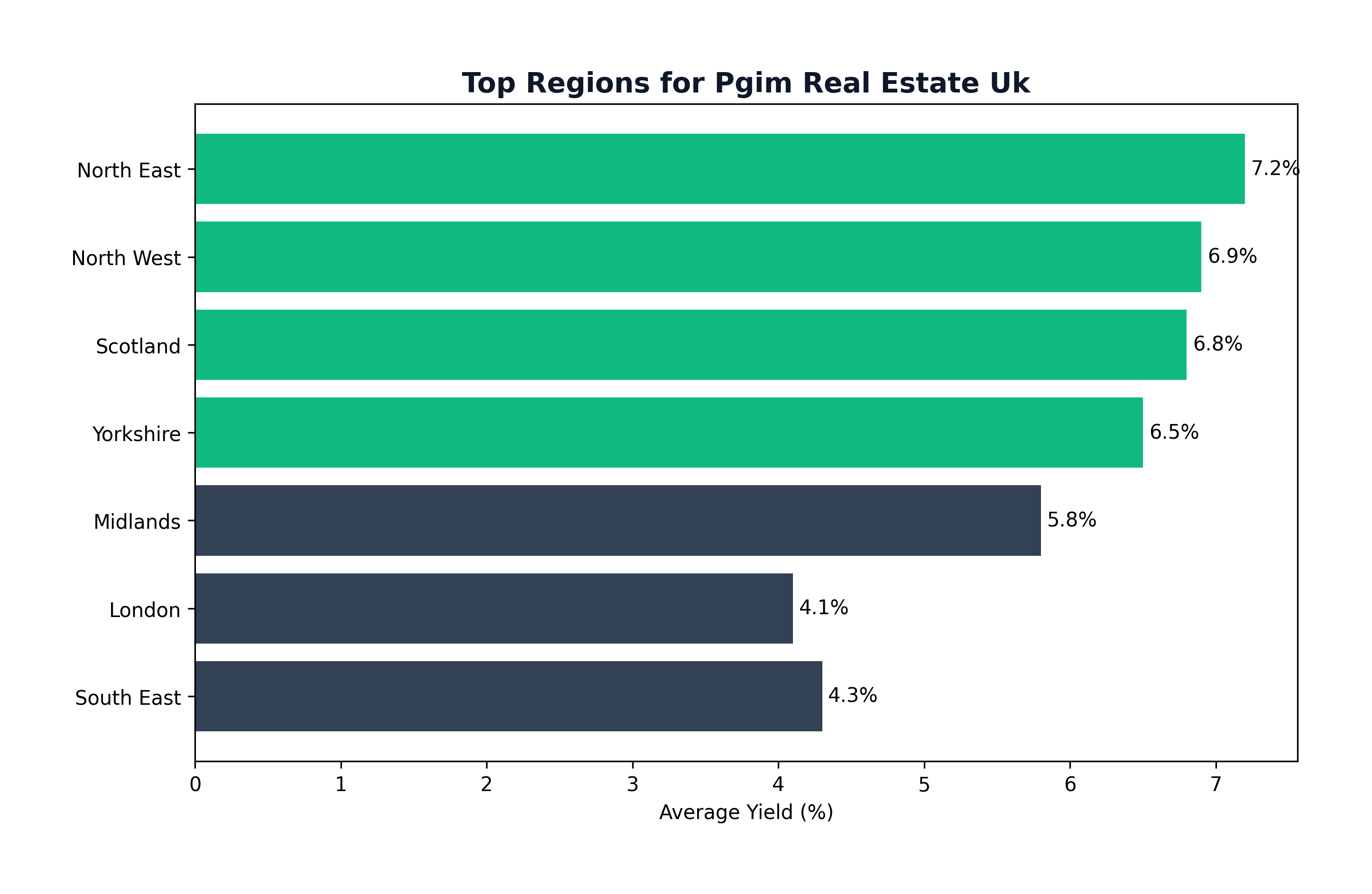

Figure: Regional Yield Heatmap

Figure: Regional Yield Heatmap

The Affordable Housing Strategy: Why SFR is Booming

Single-Family Rental — the institutional ownership and management of individual houses (as opposed to apartment blocks) for private rental — is an established asset class in the United States that is at an earlier stage of development in the UK. The structural drivers in the UK are compelling: homeownership rates have fallen from 70.9% in 2003 to approximately 63% in 2023, driven by affordability constraints, tighter mortgage criteria, and the life-stage preferences of younger households. These former or would-be homeowners become renters — and they prefer the space, garden, and school catchment area of a house over a flat.

PGIM's affordable housing strategy targets working families and co-renters — households earning 60–100% of median income who cannot access market-rate homeownership but cannot qualify for social housing. This 'missing middle' cohort represents the UK's largest undersupplied housing demographic and the target for the government's affordable housing delivery programmes. Rental levels are set at 70–80% of market rent, providing genuine affordability for tenants while generating sustainable yields for investors.

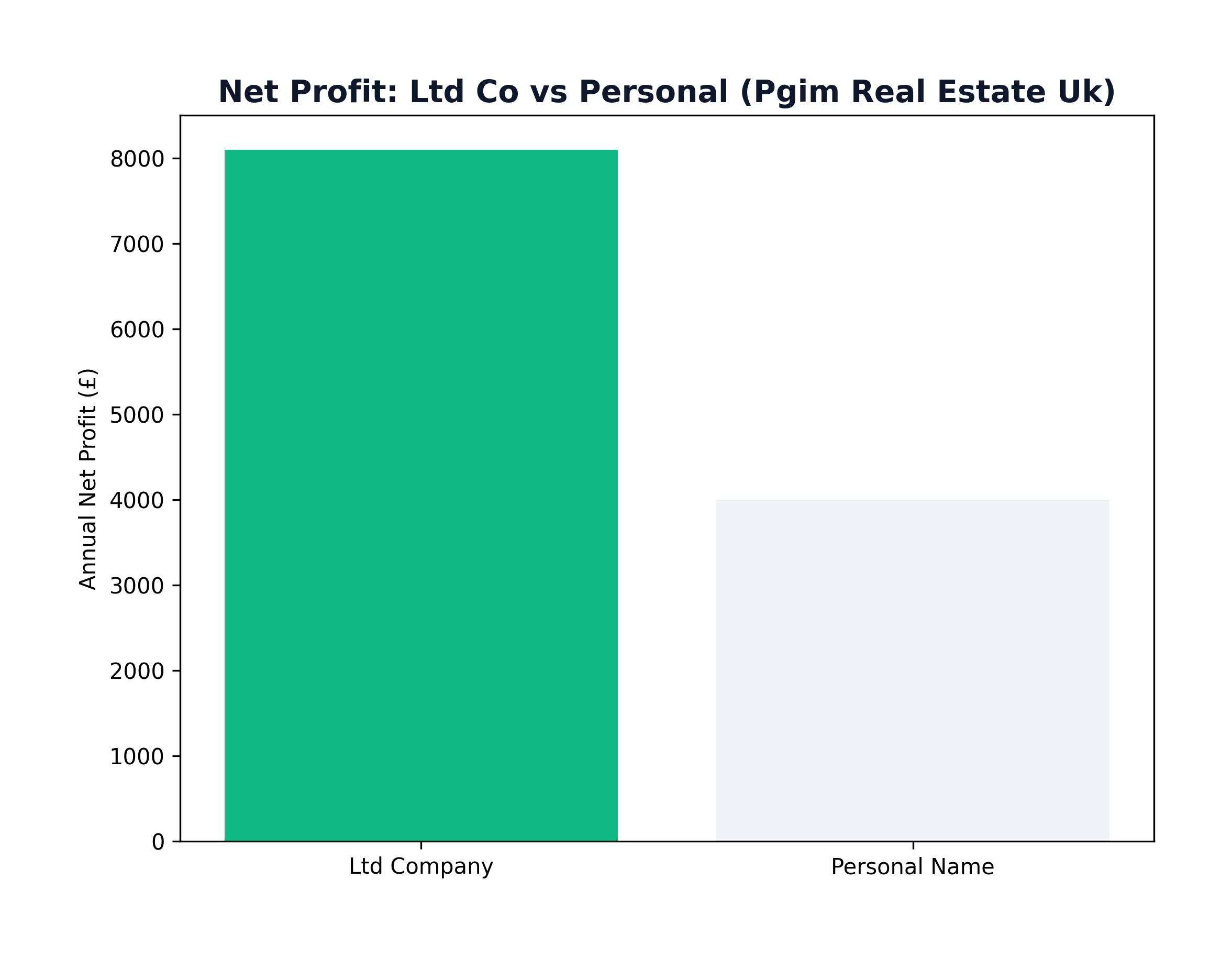

Figure: Tax Trap: Personal vs Ltd

Figure: Tax Trap: Personal vs Ltd

Portfolio Highlights: Projects and Principles

PGIM's UK portfolio includes developments in Exeter, Littlehampton, and several other English towns and cities where planning consent, land availability, and local authority partnership support new affordable housing delivery. The development approach emphasises energy efficiency — all homes in the portfolio are targeting EPC Band A or B, with solar photovoltaic panels, heat pump heating systems, and EV charging points as standard specifications. This is not just an ESG checkbox: energy-efficient homes attract and retain tenants more effectively, suffer lower void periods, and carry lower embodied carbon — all of which improve the investment case as well as the impact case.

Long-term stable cash flows are the hallmark of the strategy. Leases with registered housing associations and local authority partners are typically structured at 25 years, with annual RPI/CPI-linked rent reviews. This creates a bond-like income stream with equity-like upside from asset appreciation — a hybrid return profile that is genuinely scarce in the current market.

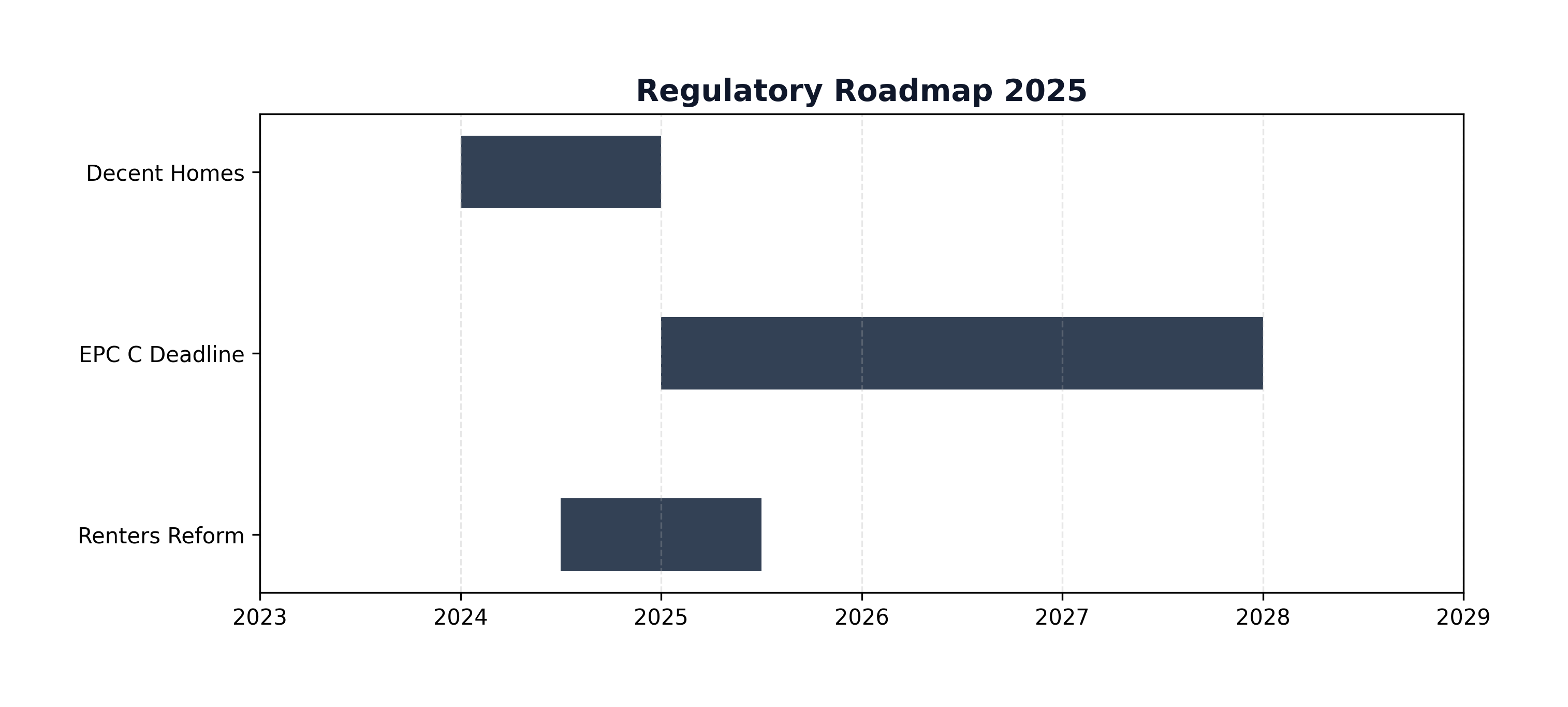

Figure: Regulatory Roadmap

Figure: Regulatory Roadmap

Market Outlook: PGIM's 2026 European Real Estate View

PGIM Real Estate's European real estate outlook for 2026 identifies residential — both market-rate multifamily and affordable single-family — as the sector best positioned for return improvement. Office markets are expected to continue bifurcating between Grade A (recovering) and secondary (challenged), with the repricing of secondary office assets still incomplete in several markets. Apartment and residential sectors are expected to see yield compression as interest rates normalise and institutional capital committed to residential assets globally seeks deployment.

Liquidity improvements across European commercial property markets are expected as the transaction volume freeze of 2023–2024 thaws. For PGIM's residential strategy, improved market liquidity supports both exit optionality (the ability to sell individual homes or portfolios if required) and continued acquisition (more motivated sellers, more transparent pricing). The affordable housing sub-sector specifically is insulated from the general commercial market liquidity cycle because its income stream is contractual and government-supported rather than market-dependent.

Figure: Strategy Cycle

Figure: Strategy Cycle

Why Invest? The Triple Mandate

Diversification

UK affordable housing has demonstrated very low correlation with traditional commercial real estate and listed equities. During the 2022 commercial property repricing, affordable housing assets retained value because their income streams were contractual and their occupancy was guaranteed — unlike offices or retail, where both rent and occupancy came under pressure simultaneously. This diversification benefit makes affordable housing a portfolio stabiliser rather than a return maximiser.

Social Impact (S in ESG)

Few institutional investments can demonstrate social impact as directly and measurably as affordable housing. Every home built or acquired by PGIM's strategy houses a family at a rent they can afford — reducing housing stress, improving educational outcomes for children, and reducing healthcare costs associated with poor-quality housing. For pension fund investors whose beneficiaries are drawn from exactly the same working-family demographic, this impact alignment is meaningful and increasingly reportable under mandatory ESG disclosure frameworks.

Inflation Hedging

RPI/CPI-linked rent reviews provide genuine inflation protection over the long term. In periods of elevated inflation (as experienced in 2022–2024), annual rent uplifts of 8–10% dramatically improve real returns relative to fixed-income alternatives. For investors with inflation-linked liabilities — final salary pension schemes, RPI-linked annuities — this characteristic is of specific and significant value that is difficult to replicate through other real assets.

Figure: HMO Expense Breakdown

Figure: HMO Expense Breakdown

Accessing PGIM's UK Affordable Housing Strategy

The strategy is accessible to institutional investors through PGIM's European real estate platform, with minimum commitments starting at £25 million for commingled fund participation. Separately Managed Accounts are available for larger allocations (£100 million+), allowing bespoke portfolio construction within the affordable housing universe. UK defined benefit pension schemes, insurance companies, and large family offices represent the primary investor base. Prospective investors should engage PGIM's UK business development team directly for access and to review the current fund terms and pipeline.

Stop being a landlord. Start being an investor.

Shaded Canvas introduces serious capital to vetted UK property opportunities — targeting 12–16% net returns.

Start Investing →