The UK property market has long been the cornerstone of domestic wealth creation. However, the traditional barrier to entry—a hefty deposit, stamp duty surcharges, and the ability to secure a mortgage—has increasingly marginalized ambitious but cash-light professionals. In 2026, the landscape is shifting rapidly.

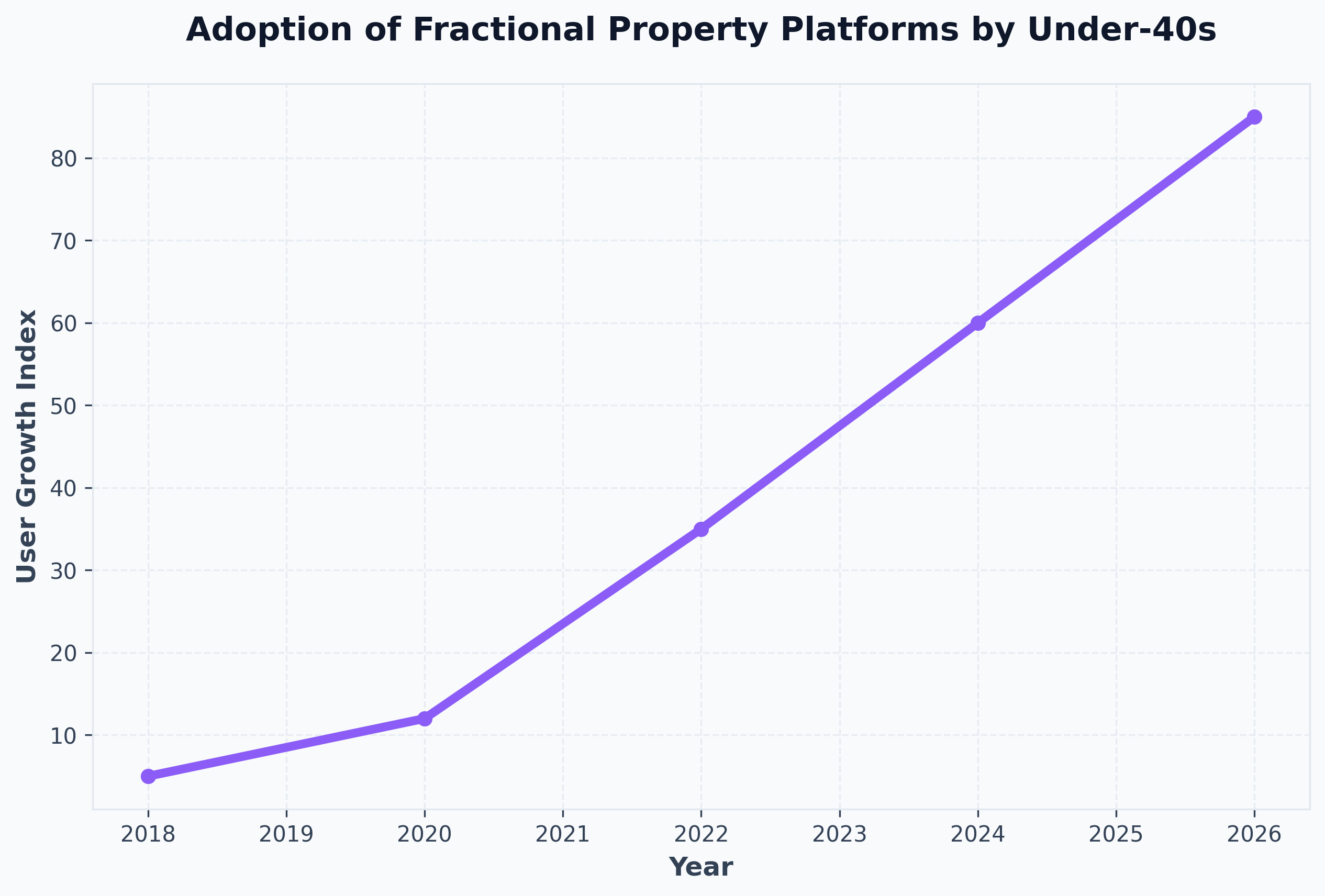

If you want the returns of real estate without the six-figure upfront capital, fractional property investment UK and other pooled structures offer a revolutionary alternative.

This comprehensive guide breaks down exactly what these models are, how pooling money to buy real estate works in practice, and why a pooled property investment might be the smartest addition to your 2026 portfolio.

What is a Pooled Investment Fund?

At its core, what is a pooled investment fund? It is a mechanism where multiple individuals combine their financial resources to purchase an asset—in this case, real estate—that they could not afford (or do not want to buy) individually.

Instead of one person buying a £500,000 apartment in Manchester, 100 people might each invest £5,000. True pooled real estate investment means you own a proportionate share of the underlying asset or the debt secured against it, entitling you to a corresponding share of the rental income and eventual capital appreciation.

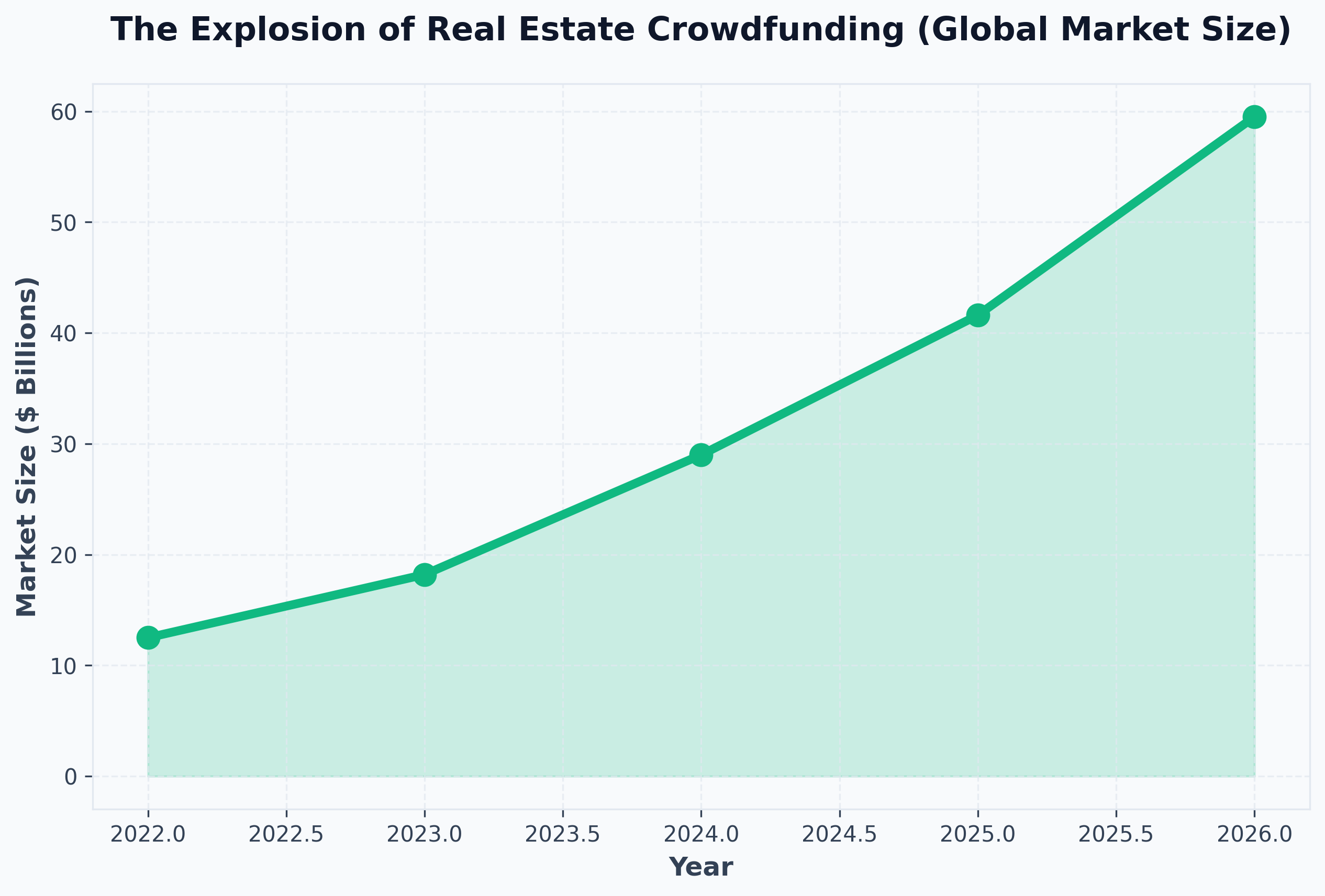

Why The Surge in Popularity?

In 2026, with interest rates stabilizing but the cost of living still tight, investors are looking for yield without leverage. By leveraging pooled property investment, you bypass the need for a mortgage entirely. You also sidestep the operational nightmares of being a landlord—no boiler repairs, no tenant referencing, and no EPC compliance headaches. It is the ultimate hands-off yielding asset.

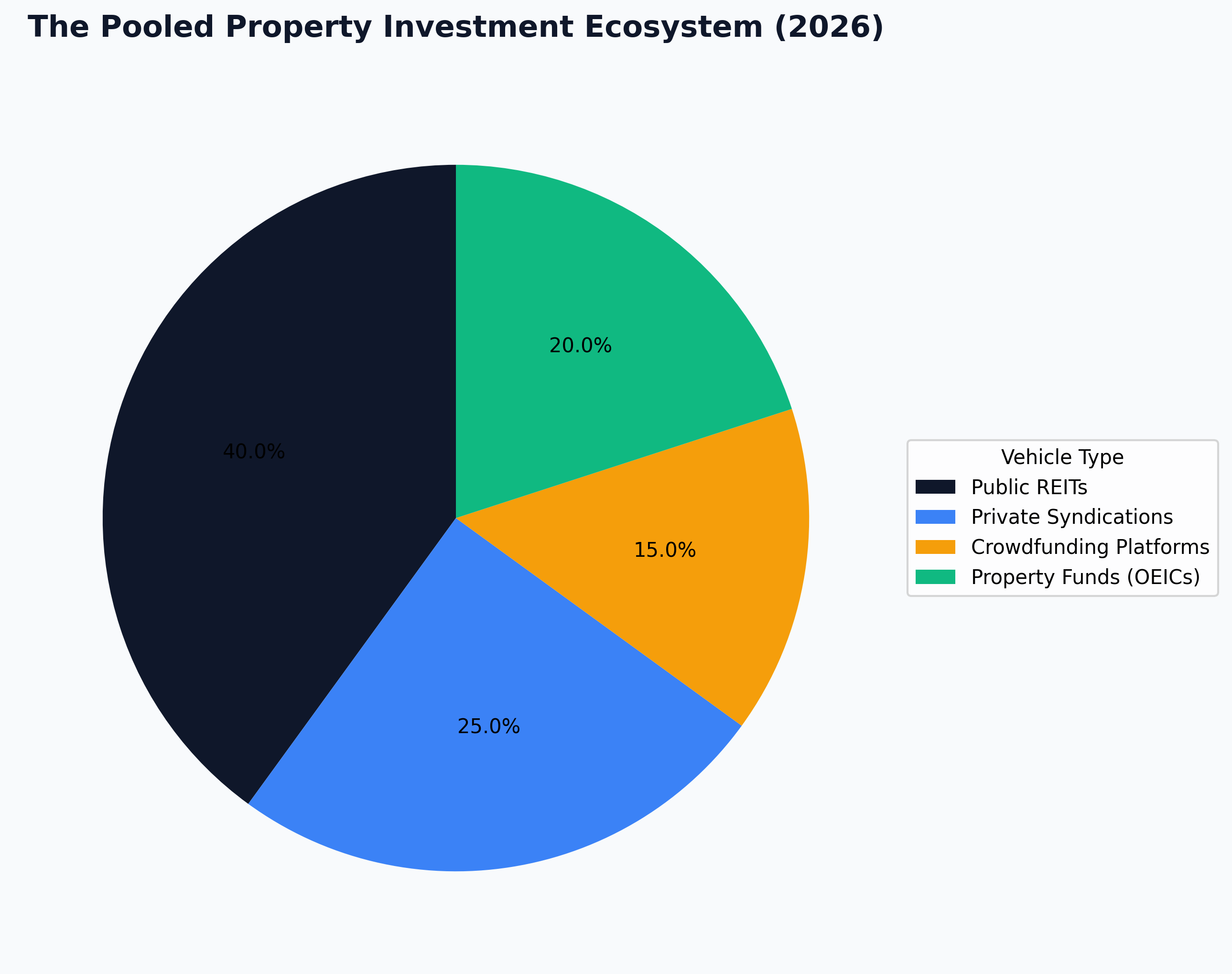

4 Ways to Execute Fractional Ownership UK

"Fractional ownership" is an umbrella term. Underneath it sits a highly diverse ecosystem of investment vehicles. Here are the four dominant ways to execute fractional ownership UK in 2026.

1. Real Estate Crowdfunding Platforms

This is the most direct, digital-first method. Dedicated online platforms source, vet, and list commercial or residential properties. Investors can buy shares in a Special Purpose Vehicle (SPV) that owns the specific property.

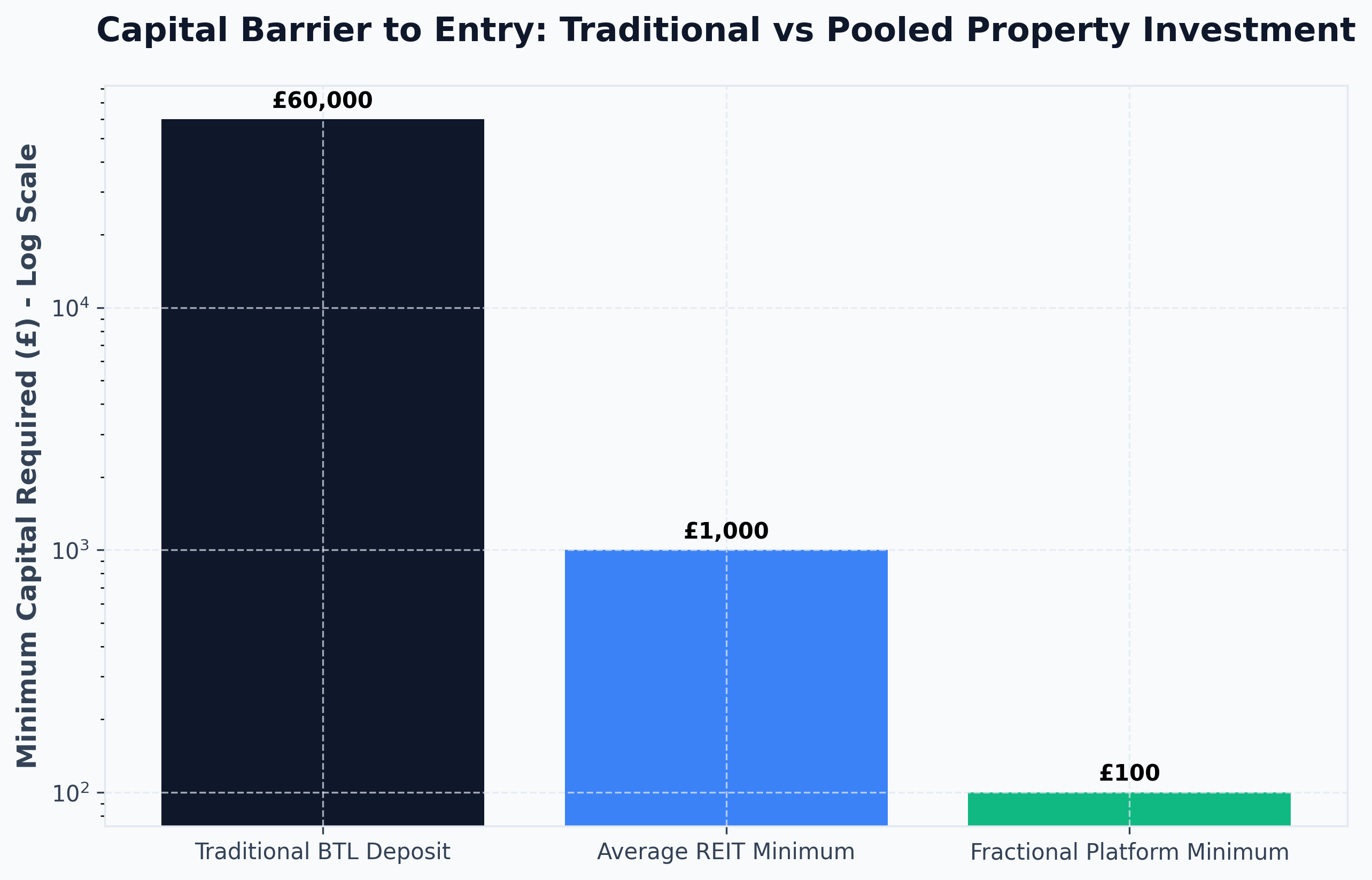

- The Pros: Incredibly low barrier to entry (often as little as £100). High transparency (you pick the exact building you want to invest in).

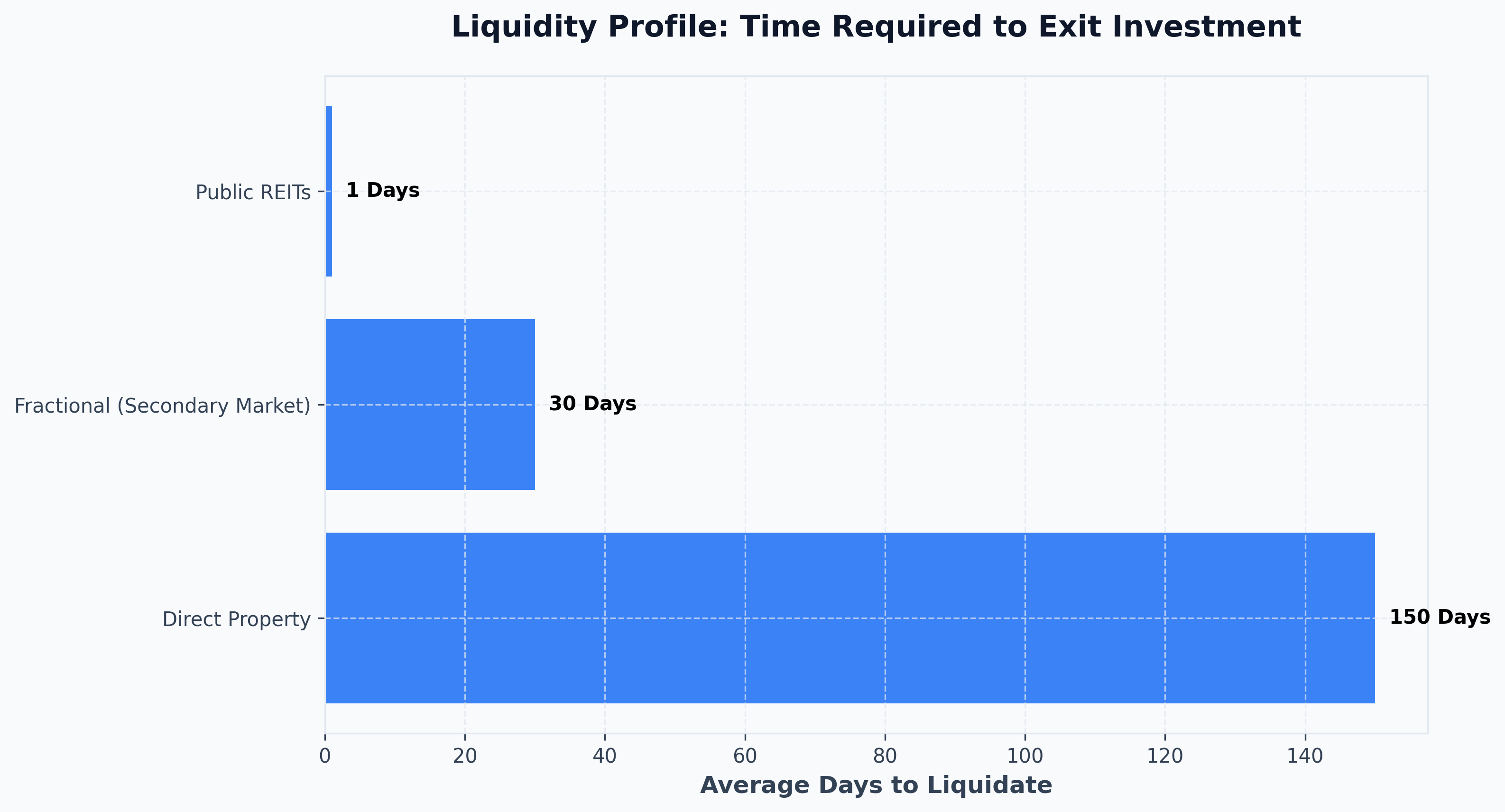

- The Cons: Secondary markets for selling your shares can sometimes be illiquid if the platform does not have high trading volume.

2. Private Joint Ventures (JVs) & Syndications

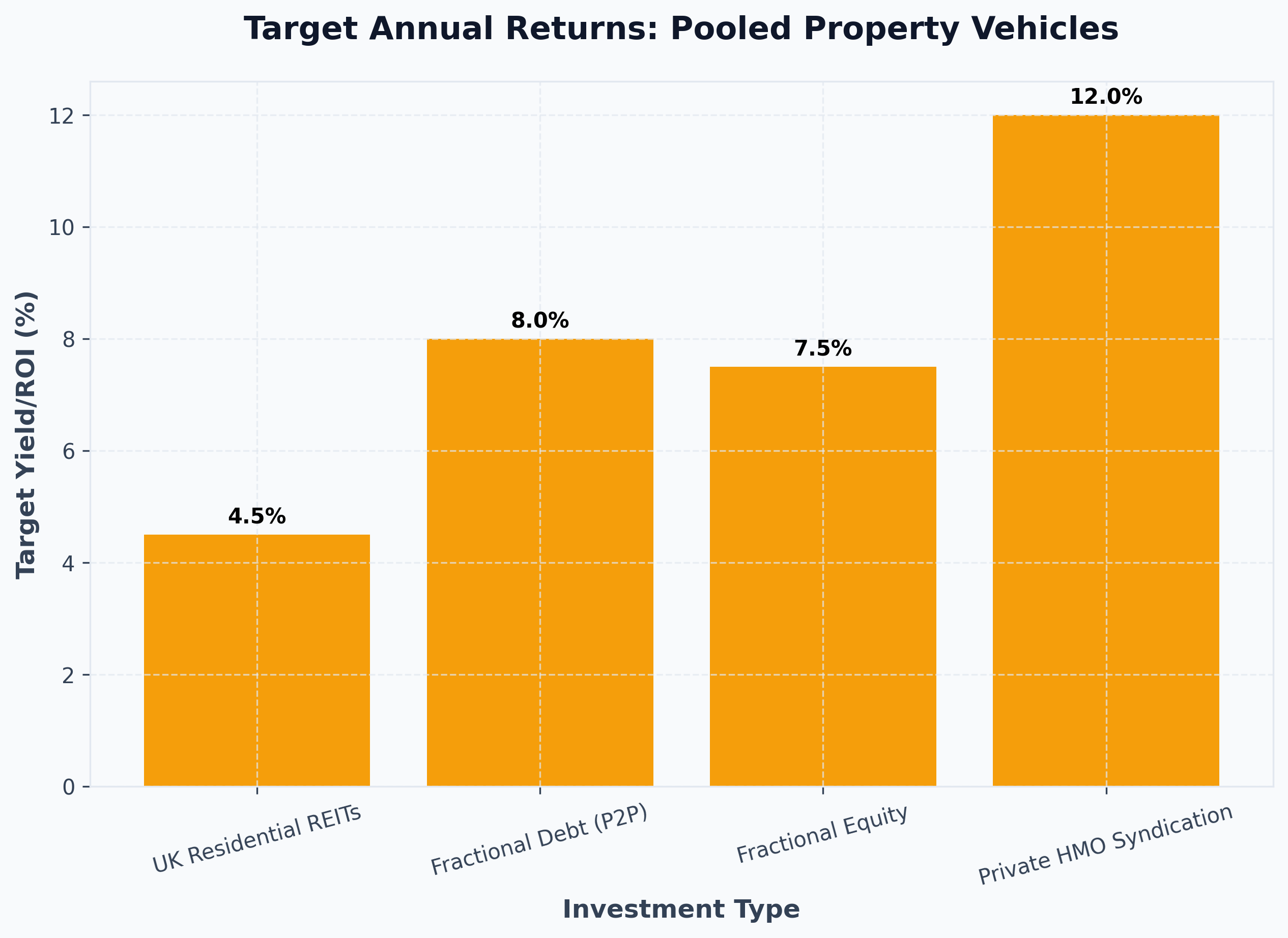

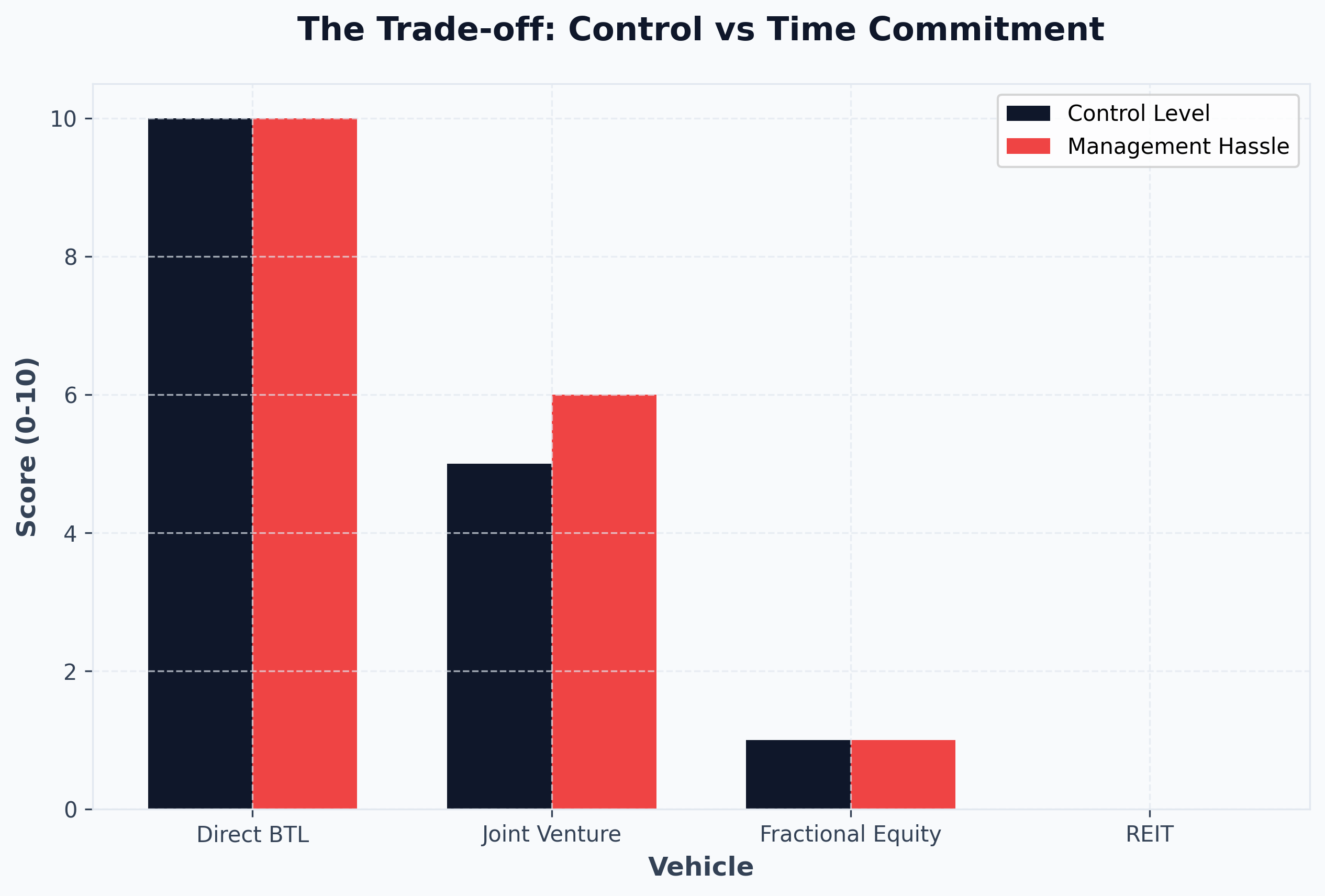

If you are asking how to start a property portfolio UK with a small group of trusted peers, a private JV or syndication is the answer. This is the traditional method of pooling money to buy real estate. A lead investor (the sponsor) finds an off-market deal, perhaps a high-yielding HMO (House in Multiple Occupation) in the Midlands, and raises capital from 3-5 private investors to fund the deposit and refurbishment.

- The Pros: Higher potential returns (often 10-15% ROI) as there are fewer corporate overheads, and you are adding value through refurbishment.

- The Cons: Requires high trust among partners, complex legal structuring (Shareholder Agreements), and typically a higher minimum investment (£20k+).

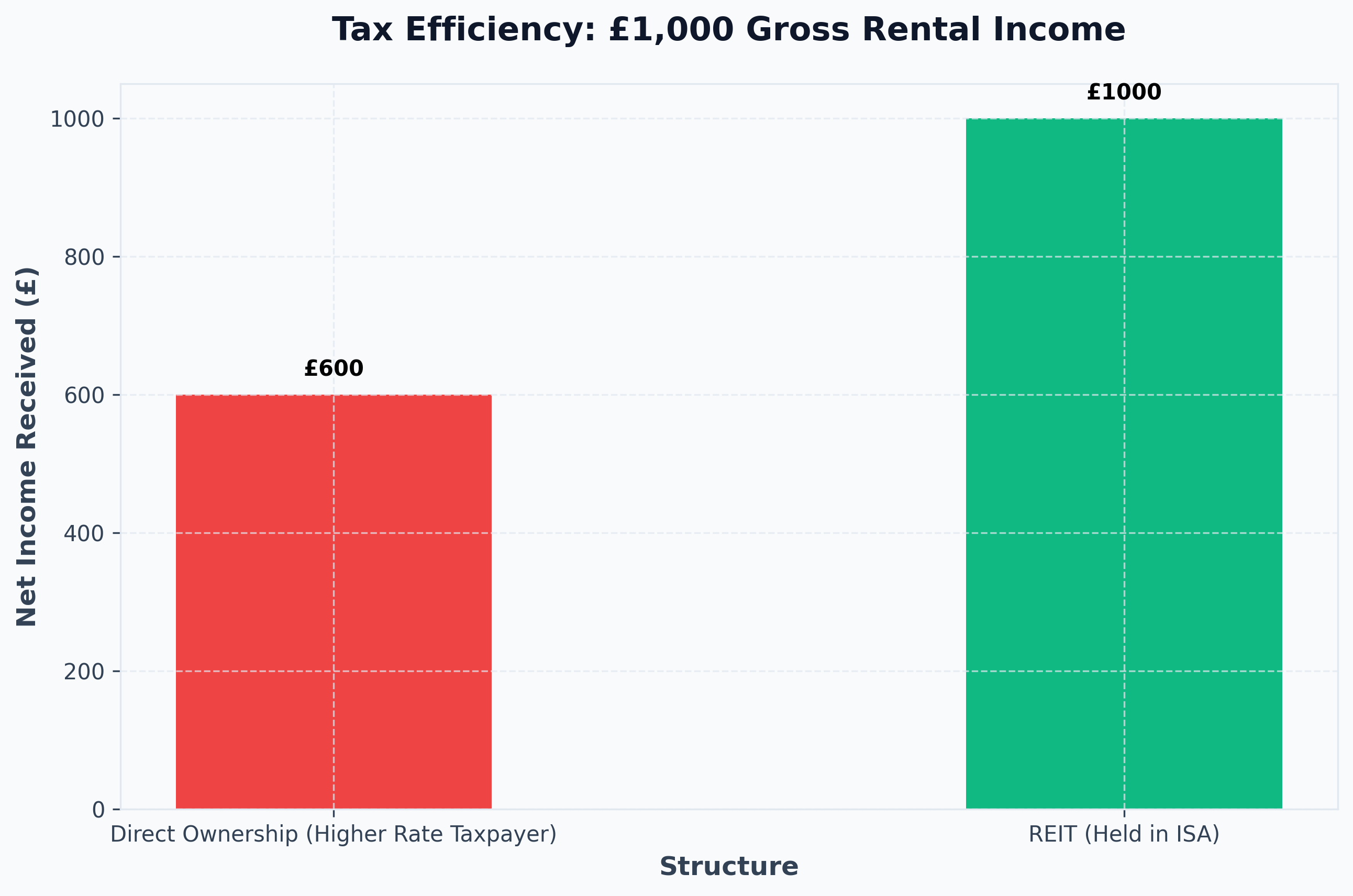

3. Real Estate Investment Trusts (REITs)

A REIT is a publicly-traded company that owns, operates, or finances income-generating real estate. Buying shares in a REIT on the London Stock Exchange is the most liquid form of pooled real estate investment.

- The Pros: Instant liquidity (you can sell your shares in seconds). Tax efficiency (REIT dividends can be held within a Stocks & Shares ISA, rendering your rental income effectively tax-free).

- The Cons: Performance is correlated with the wider stock market, not just the underlying property value. You have zero control over the specific assets acquired.

4. Property Unit Trusts (PAIFs)

Property Authorised Investment Funds are open-ended funds regulated by the FCA. They pool investor money to buy sweeping portfolios of commercial real estate—logistics hubs, supermarkets, and office buildings. They offer deep institutional diversification that is impossible to achieve individually.

The Benefits of Fractional Property Investment UK

Why are busy professionals turning to these models instead of traditional Buy-to-Let?

1. Extreme Diversification

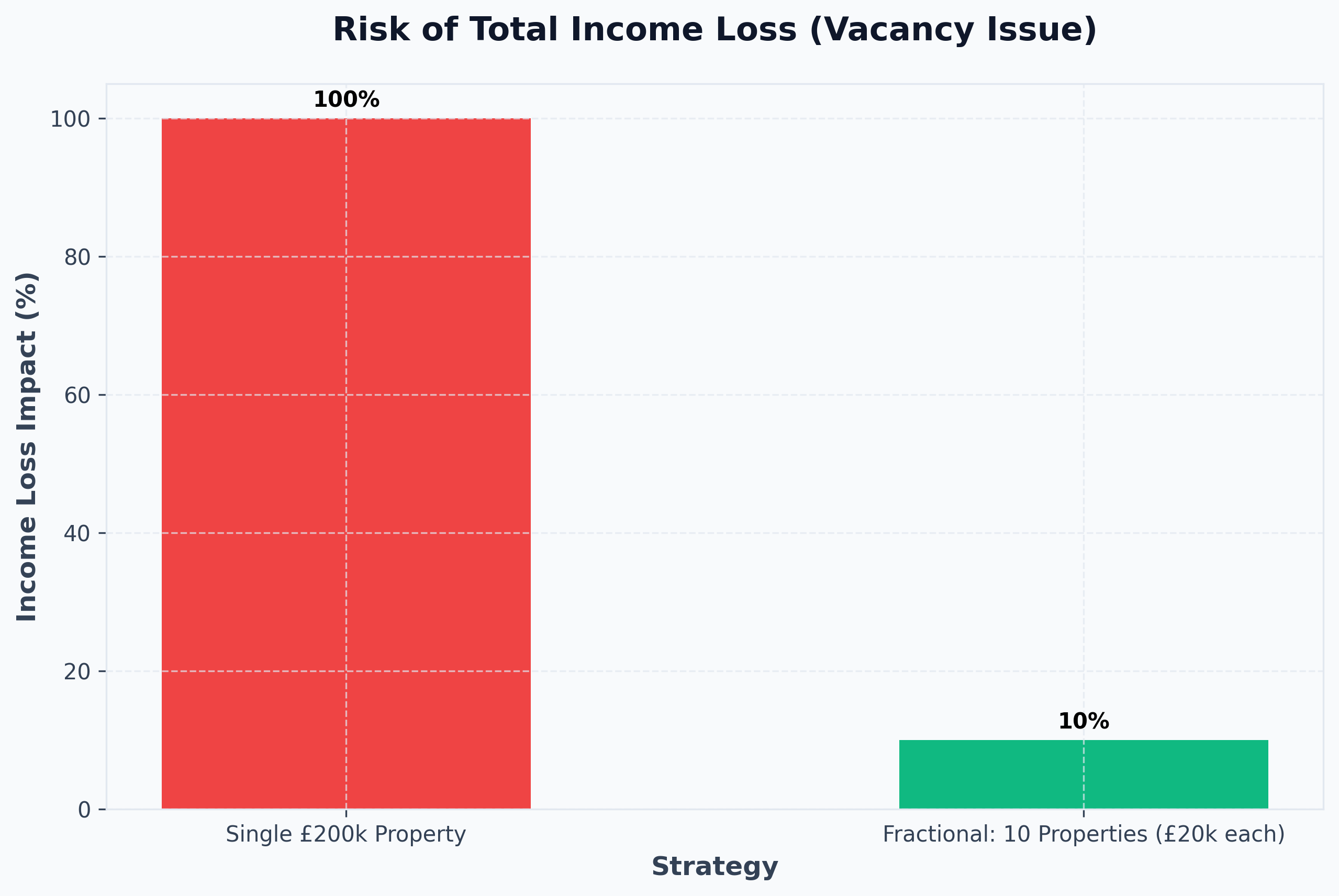

If you have £50,000 to invest, buying a single traditional BTL ties 100% of your capital to one geographic postcode and one tenant. If that tenant stops paying, your yield drops to 0%. By utilizing fractional property investment UK, you could deploy £5,000 across ten different properties in ten different cities. This dilutes void risk almost entirely.

2. Access to Commercial & Premium Assets

A single investor rarely has the £5 million required to buy a thriving logistics warehouse on the M1 corridor or a premium PBSA (Purpose-Built Student Accommodation) block. Pooled property investment democratizes access to these high-yielding, institutional-grade commercial assets.

3. Total Passivity

Traditional property investment is an active second job. Fractional ownership requires nothing more than an annual review of your portfolio dashboard. The platforms, fund managers, or lead syndicators handle all tenant management, maintenance, and legal compliance.

Is Pooled Real Estate Investment Safe?

No investment is without risk, and pooled real estate investment is no exception. In 2026, the FCA has tightened regulations on crowdfunding platforms and alternative investment funds, providing better protection for retail investors. However, key risks remain:

- Platform Risk: What happens if the crowdfunding platform goes bust? (Ensure they use a bankruptcy-remote SPV structure).

- Liquidity Risk: Unlike a REIT, selling your shares in a private syndication or a specific crowdfunded property can take months if there isn't a willing buyer on the secondary market.

- Management Competency: Your returns are entirely dependent on the skill of the fund manager or the lead JV partner executing the strategy.

Conclusion: A Modern Strategy for a Modern Market

For the modern professional, wealth creation needs to be scalable, diversified, and entirely hands-off.

Whether you opt for the instant liquidity of a REIT, the granular control of an online crowdfunding platform, or the high-yield potential of a private syndication, fractional property investment UK has firmly established itself as a mainstream wealth-building tool in 2026.

By strategically pooling money to buy real estate, you can bypass the traditional hurdles of the housing market, unlocking professional-grade yields from the comfort of your laptop.

Stop being a landlord. Start being an investor.

Shaded Canvas introduces serious capital to vetted UK property opportunities — targeting 12–16% net returns.

Start Investing →