The UK property market in 2026 presents a unique paradox. While base rates have begun a slow descent, bringing mortgage affordability back into focus, the regulatory landscape has never been stricter. In this environment, acquiring assets at retail prices often yields underwhelming returns. The true margin lies in below market value property sourcing. However, finding the deal is only half the battle; knowing how to finance finding below market value property is what separates active investors from passive observers.

This comprehensive guide breaks down the financial architecture required to secure BMV deals in 2026, analyzing bridging loans, specialist mortgages, cash strategies, and the sweeping legislative changes you must navigate.

The 2026 BMV Landscape: Why Speed is Capital

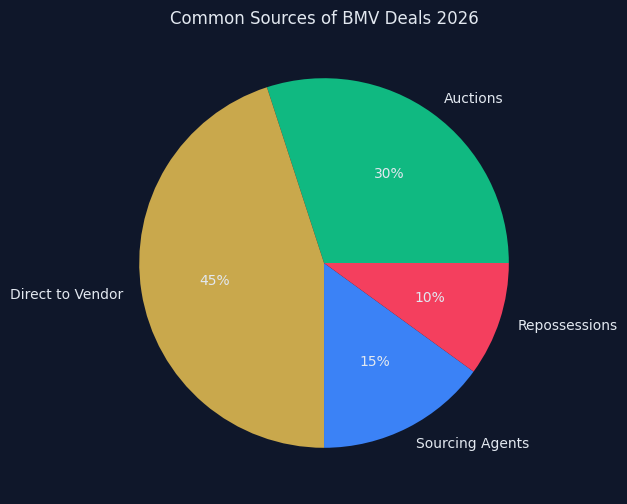

To understand how to finance finding below market value property, one must understand why these properties are below market value in the first place. These are rarely listed on Rightmove in prime condition. They are often "distressed" properties—whether due to physical degradation (unmortgageable), legal complications (short leases), or seller circumstances (probate, risk of repossession).

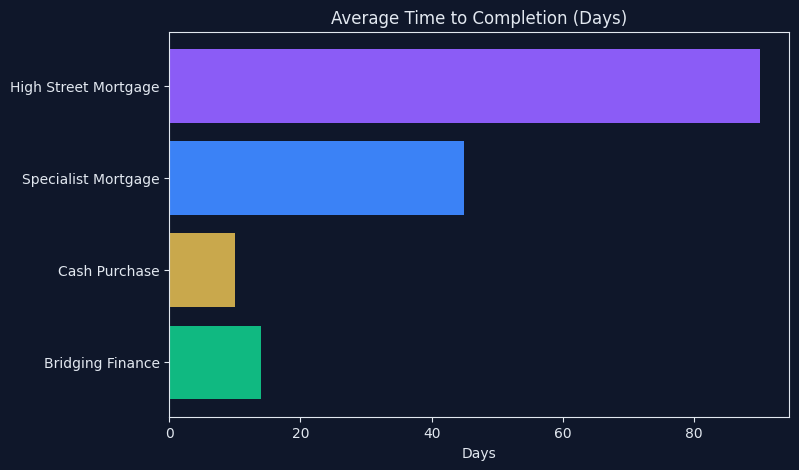

Because these deals are distressed, traditional High Street mortgages are usually unsuitable. They take too long to arrange (often 8 to 12 weeks), and traditional lenders will automatically reject properties lacking a functioning kitchen or bathroom. Therefore, financing these deals requires capital that can deploy rapidly.

Strategy 1: Bridging Finance BMV Deals

Bridging finance is the cornerstone of acquiring BMV property. It is short-term, secured lending designed to "bridge" the gap between the immediate purchase of a property and a longer-term financial exit (such as refinancing onto a BTL mortgage or selling).

Why Bridging Works for BMV

When you learn how to finance finding below market value property, bridging is often the first tool you use.

- Speed: A bridging loan can be arranged in a matter of weeks, sometimes days, allowing you to act as a quasi-cash buyer.

- Condition Agnostic: Bridging lenders are less concerned with the current condition of the property and more focused on the Gross Development Value (GDV)—what the property will be worth once you have refurbished it.

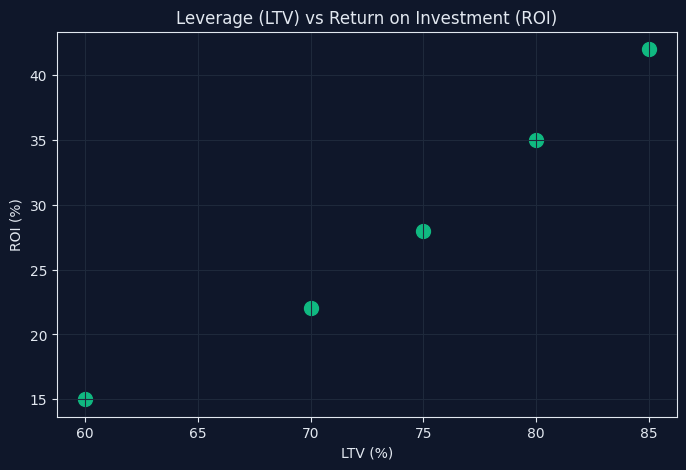

- Leverage on Value, Not Purchase Price: Crucially, some bridging lenders will lend based on the Open Market Value (OMV) rather than the purchase price. If you buy a property worth £100,000 for £70,000, some lenders will calculate their Loan-to-Value (LTV) against the £100,000, significantly reducing the cash deposit you need to contribute.

The Cost of Bridging in 2026

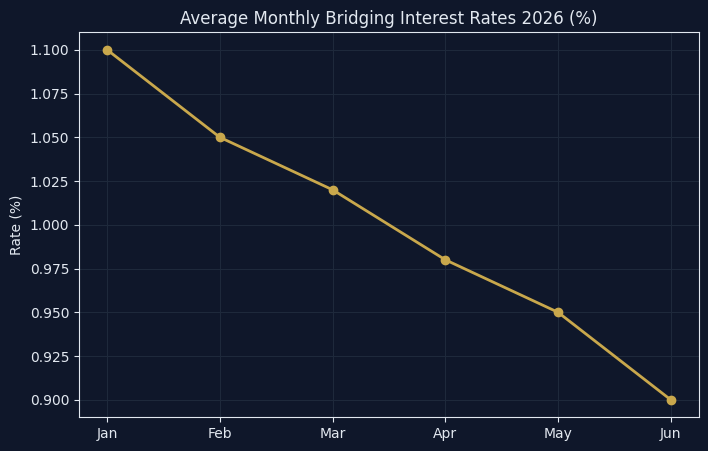

Interest rates for bridging finance BMV deals in 2026 typically range between 0.75% and 1.2% per month. While this sounds expensive annualized, the loan is only held for a short period (typically 6 to 9 months). You must factor arrangement fees (usually 1% to 2% of the loan amount), exit fees, and valuation costs into your deal analyzer.

Strategy 2: Specialist Mortgages for Below Market Value

While high street lenders shy away from BMV, specialist commercial and buy-to-let lenders offer tailored products.

The "Day One Remortgage" Myth

In previous decades, investors could buy a property for cash, refurbish it over a weekend, and remortgage it on Monday at the higher value to pull all their cash out. Today, the "Six-Month Rule" (where lenders require you to own the property for six months before remortgaging) is standard practice, though specialist lenders offer exceptions.

Specialist mortgages for below market value often involve "light refurbishment" products. The lender provides the initial purchase funds (based on the lower purchase price) and holds back a portion of funds to cover the refurbishment. Once the work is complete and a reinspection occurs, the lender releases the final funds, and the product automatically transitions into a standard term mortgage.

Strategy 3: Cash Purchases for Distressed Property

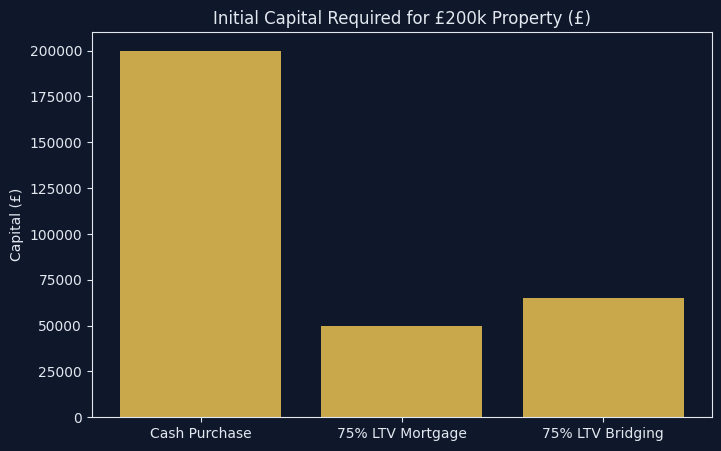

Cash remains the absolute king when negotiating below market value. A seller facing repossession does not care about your mortgage offer in principle; they care about guaranteed completion in 14 days.

Raising Cash

If you do not have the liquid capital, raising it becomes part of the sourcing process:

- Private Investors: Offering fixed returns (e.g., 8-10% per annum) to high-net-worth individuals in exchange for a first charge on the property.

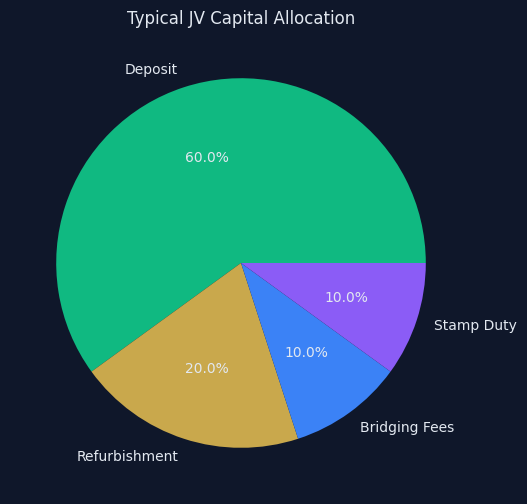

- Joint Ventures (JVs): Partnering with a cash-rich, time-poor investor. You find the BMV deal and manage the project; they provide the capital. Profits are typically split 50/50.

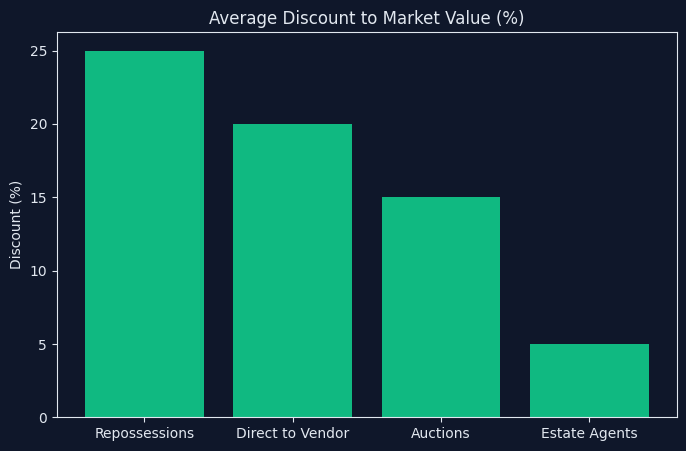

Cash purchases for distressed property allow you to secure discounts of 20% to 35%, refurbish the asset, and then refinance it at its true market value to recycle your capital (the BRRR strategy).

The 2026 Compliance and Tax Reality

Financing is deeply intertwined with compliance. The 2026 regulatory landscape dictates how profitability is calculated.

Renters Rights Act 2025 Impact

Fully implemented by May 2026, the Renters Rights Act 2025 impact is profound. With the abolition of Section 21 "no-fault" evictions and the shift to periodic tenancies, lenders are stress-testing mortgages more rigorously. They view the inability to easily remove tenants as a heightened risk profile. This means Interest Coverage Ratios (ICRs) are stricter, often requiring a rental income that is 145% of the mortgage interest calculated at a stressed rate of 5.5%.

Making Tax Digital for Landlords 2026

As of April 2026, Making Tax Digital for landlords 2026 is mandatory for those with property and self-employment income over £50,000. This requires digital record-keeping and quarterly submissions to HMRC. When raising finance, lenders now expect pristine digital accounting records to prove serviceability.

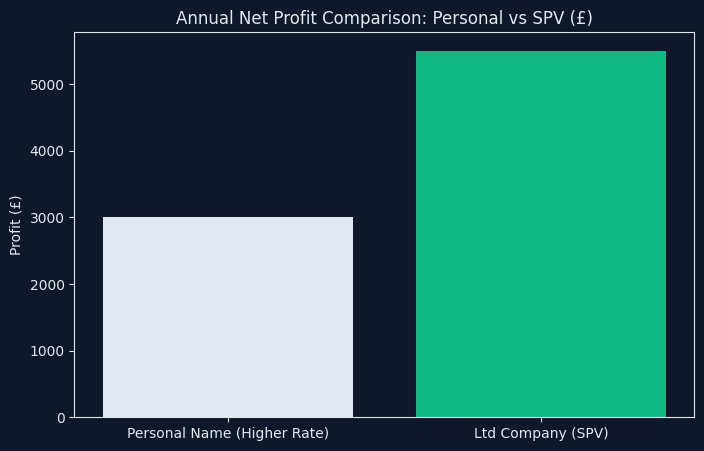

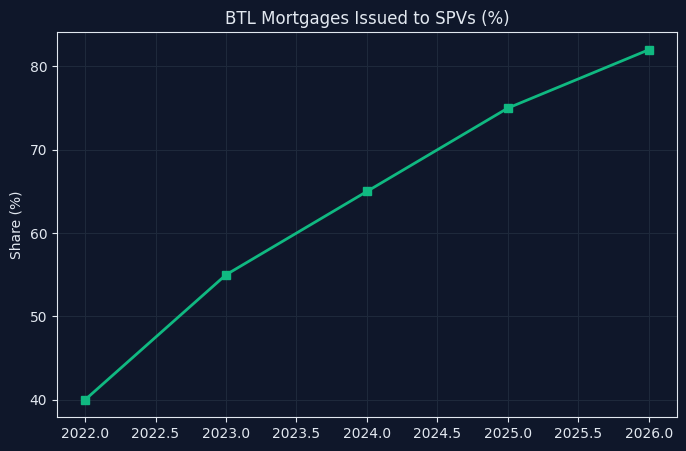

Furthermore, the restriction on mortgage interest relief (Section 24) remains, meaning holding BMV properties in a personal name is highly tax-inefficient for higher-rate taxpayers. Consequently, 2026 sees the vast majority of BMV finance being deployed through Special Purpose Vehicles (Limited Companies).

Conclusion: Executing the Strategy

Understanding how to finance finding below market value property requires a multi-faceted approach. You must build relationships with specialist bridging brokers, understand the legal structures required for Joint Ventures, and meticulously factor in the heavy compliance burdens of 2026. By mastering these financial tools, you unlock the ability to acquire distressed assets, force appreciation, and build a robust, high-yielding portfolio.

Stop being a landlord. Start being an investor.

Shaded Canvas introduces serious capital to vetted UK property opportunities — targeting 12–16% net returns.

Start Investing →