Executive Summary In 2026, the question is no longer if you can get financing for a property flip, but at what cost. With the Bank of England base rate settled at a "new normal" of 3.8-4.2%, the landscape of bridging loans, development finance, and private joint ventures has become highly sophisticated. This guide breaks down the four primary pillars of financing a "Buy, Refurbish, Sell" project, helping you maximize leverage without sacrificing your exit margin.

The Four Pillars of 2026 Property Flipping Finance

Successful investors in 2026 do not rely on a single source of capital. They "stack" their financing based on the project's risk profile and speed requirements.

1. Bridging Finance (The Speed Play)

Bridging loans remain the "gold standard" for flippers who need to move quickly, especially at auctions or for distressed assets that are currently "unmortgageable" due to missing kitchens, bathrooms, or structural issues.

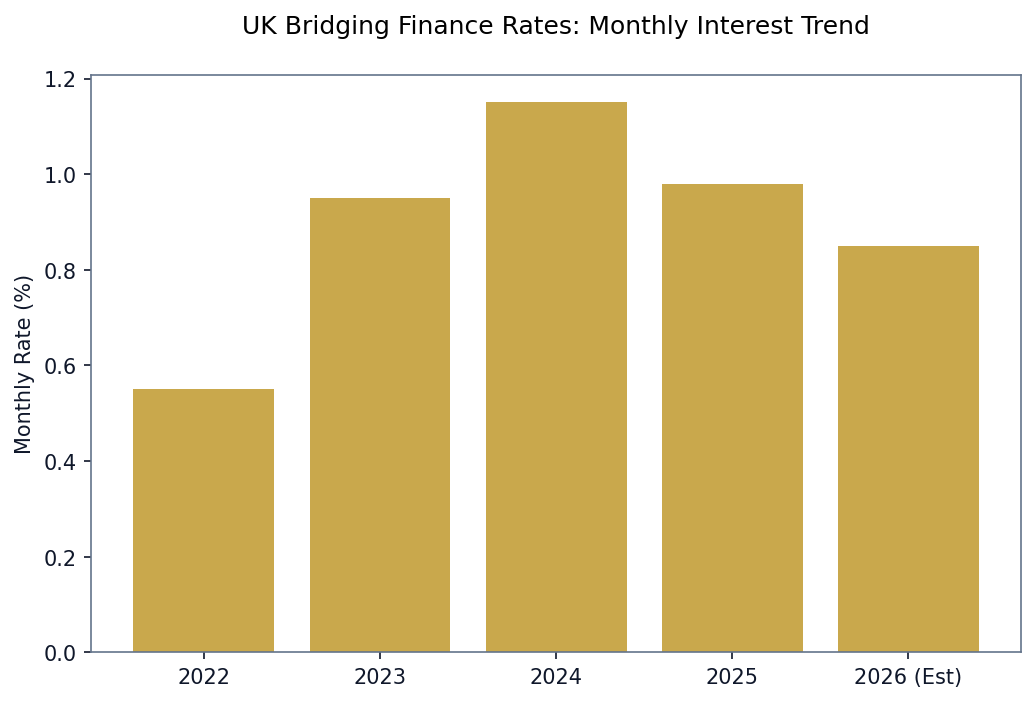

- 2026 Rates: 0.75% to 1.1% per month.

- Best for: "Light Refurb" projects with a 4-8 month duration.

- Key Advantage: Allows you to secure the asset without wait times for a traditional mortgage.

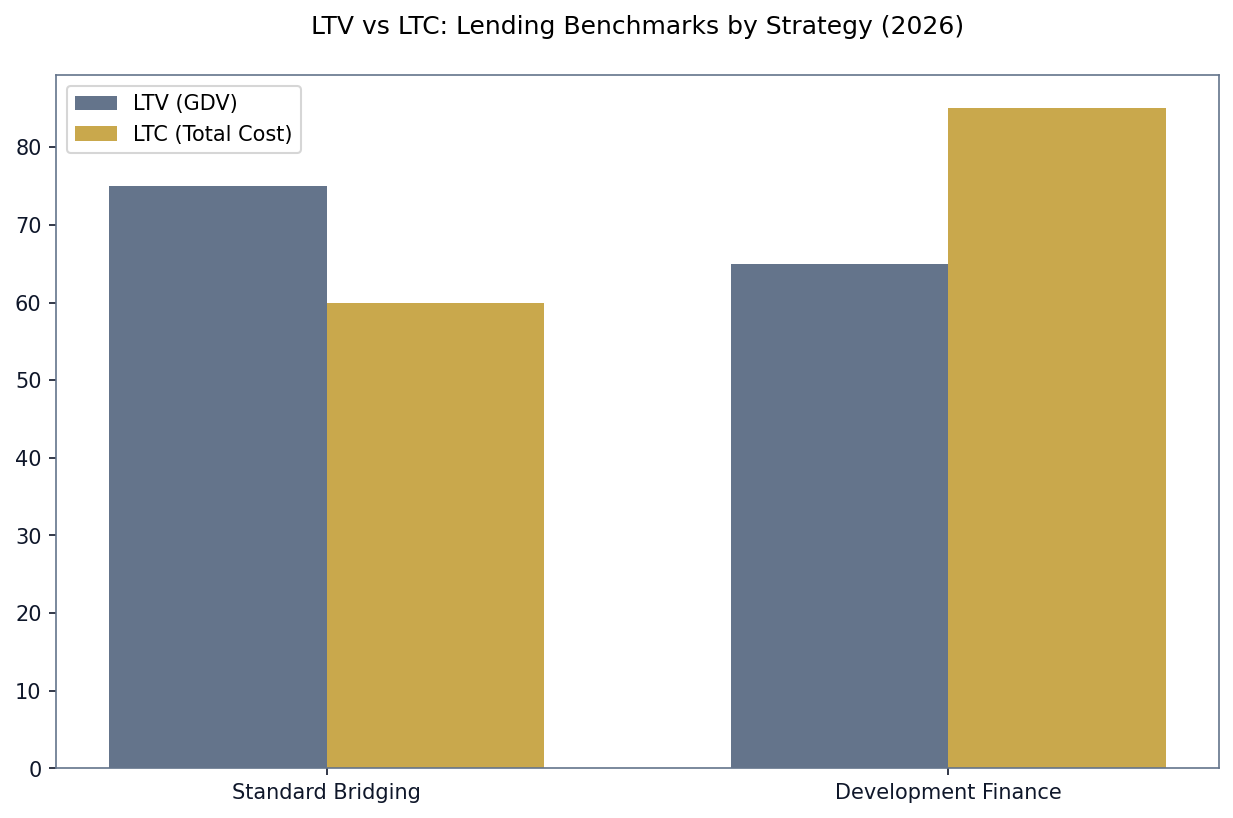

2. Development Finance (The Structural Play)

If your strategy involves "Heavy Refurbishment" (extensions, loft conversions, or converting a house into an HMO), development finance is the correct vehicle.

- 2026 Structure: Interest is often "rolled up" (no monthly payments), and the lender funds both the acquisition and 100% of the build costs.

- Best for: Projects with a 12-18 month timeline.

3. Personal Cash & "High-Street" Mortgages

While rarely used for the buy phase of a flip due to the "6-month rule" (where most lenders won't let you sell or refinance for 6 months), some specialist lenders in 2026 have removed this restriction for professional developers.

- Internal Link Opportunity: To see if your numbers stack up using traditional debt, use our Buy Refurbish Sell Yield Calculator UK.

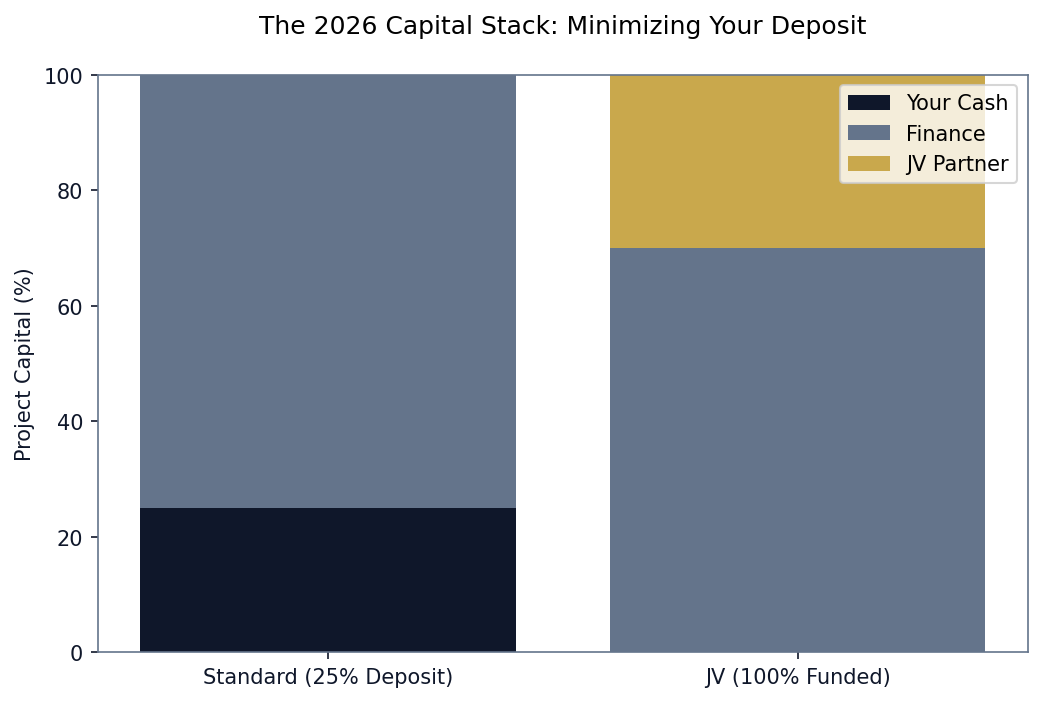

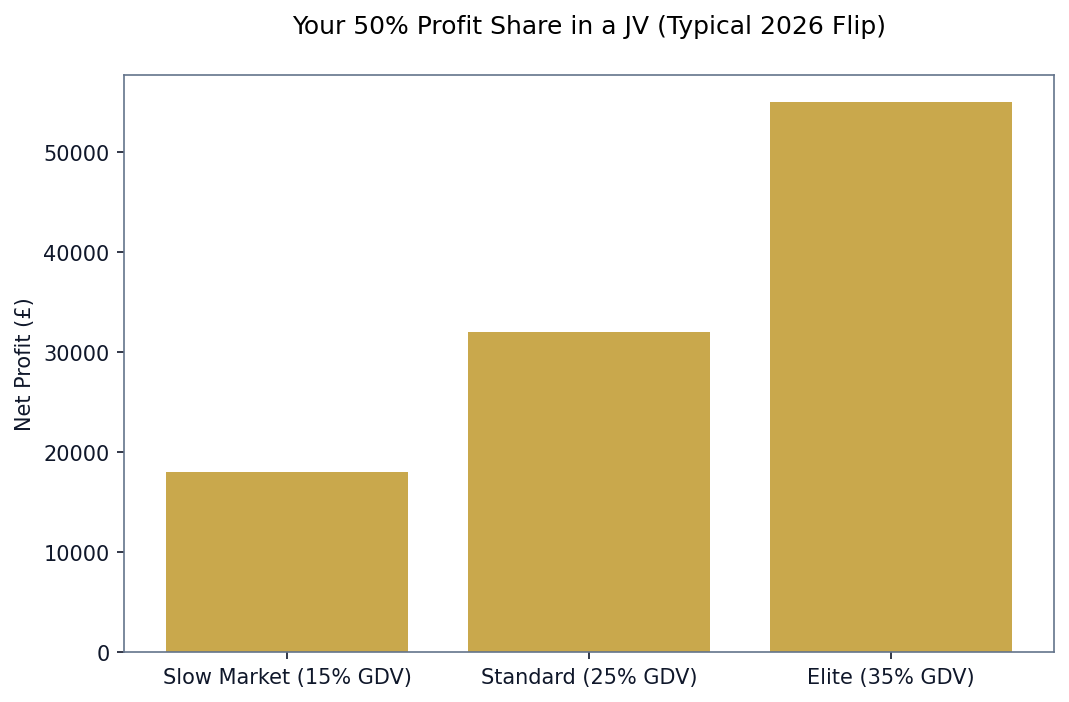

The "100% Funding" Secret: Joint Ventures (JV)

In a 2026 market characterized by tighter lending criteria, many professional flippers are using Joint Venture (JV) agreements to fund the "gap" between their bridging loan and the total project cost.

How it Works:

- The Developer (You): Provides the expertise, the sourcing (using Property Sourcing Companies UK), and the project management.

- The Investor: Provides the deposit and refurb capital.

- The Split: Typically a 50/50 profit share upon sale.

This strategy allows you to Build a UK Property Portfolio in 2026 with zero of your own capital left in the deal.

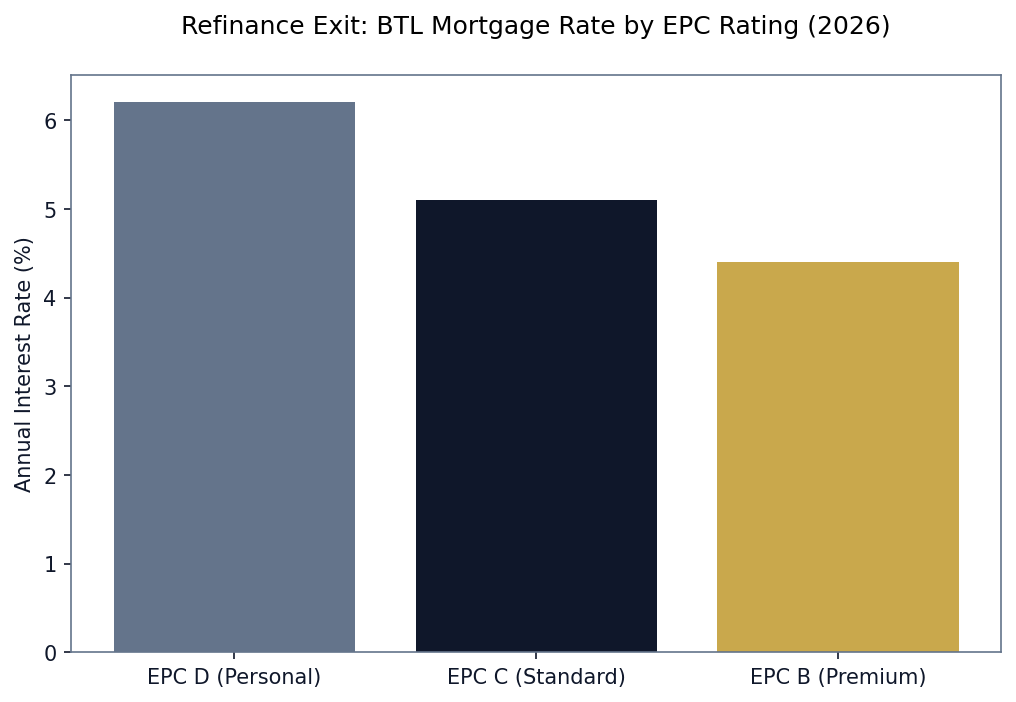

Navigating the "Refinance" Exit in 2026

If you decide not to sell but to "Rent and Refinance" (the BRRRR model), your finance strategy must account for the "End Value Appraisal."

2026 Refinancing Checklist:

- The 75% LTV Benchmark: Most BTL (Buy-to-Let) lenders will lend up to 75% of the new valuation.

- EPC Requirements: In 2026, you cannot refinance onto a competitive long-term rate unless the property is rated EPC 'C' or above.

- Speed to Market: The faster you finish the refurb, the lower your total interest cost on the bridging loan.

Internal Link Opportunity: For a deep dive into whether this model is actually profitable after interest costs, see Is Flipping Houses Worth It UK.

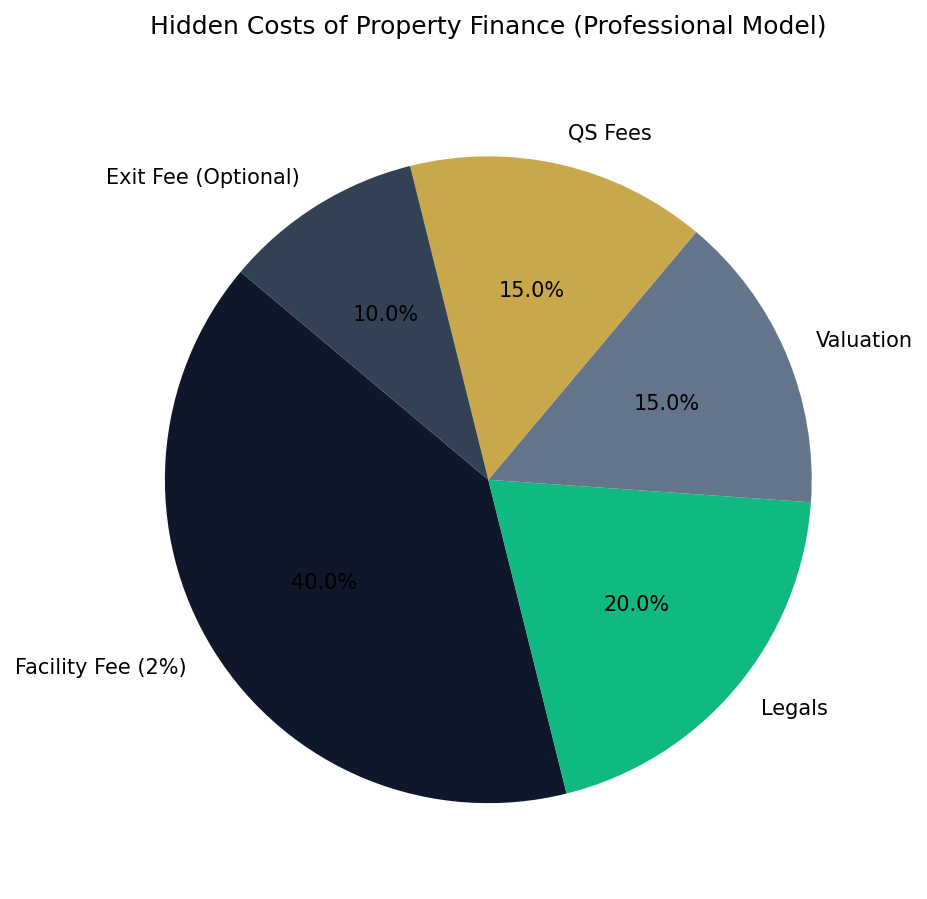

Hidden Costs of Flipping Finance: What to Watch Out For

- Facility Fees: Typically 2% of the loan amount, paid upfront.

- Exit Fees: Some lenders charge 1% of the total loan amount when you repay. Avoid these if possible.

- Valuation & Legal Fees: You often pay for both your solicitor and the lender's solicitor. Budget at least £3,000-£5,000 for these "soft costs."

- Quantity Surveyor (QS) Fees: For heavy refurbs, lenders will require a QS to sign off on "drawdowns" of funds.

Conclusion: Mastering the Capital Stack

Financing a buy, refurbish, sell project in 2026 requires a blend of speed, leverage, and risk management. By understanding the "Capital Stack"—using bridging for speed, JV cash for the deposit, and high-spec refurbs to secure a high exit valuation—you can scale your flipping business regardless of the Bank of England's base rate.

To start building your own data-driven finance model, begin with our comprehensive guide on How to Invest in Property UK.

Disclaimer: Financing involves significant financial risk. The rates provided are estimates based on 2026 UK lending benchmarks. Always consult a FCA-regulated mortgage broker before making financial decisions.

Stop being a landlord. Start being an investor.

Shaded Canvas introduces serious capital to vetted UK property opportunities — targeting 12–16% net returns.

Start Investing →