UK property investment isn't dead. But the era of easy money — where you could buy almost anything in the right postcode and watch it appreciate — is firmly over.

What replaced it is something more demanding, and more rewarding for those who approach it correctly: a market where strategy, structure, and location matter enormously, and where the investors who did their homework in 2024 and 2026 are quietly building serious portfolios while others wait on the sidelines.

This guide covers everything you need to know about how to invest in property in the UK — from understanding what property investment actually means, to choosing the right strategy for your capital, to the tax structures that separate profitable investors from frustrated ones.

If you're looking for motivational fluff, you won't find it here. What you will find is the honest picture: the numbers, the risks, the structures, and the gaps that most competitors won't show you.

What Is Investing in Property? (And Is It Still Worth It?)

Property investment means deploying capital into real estate with the expectation of a return — either through rental income, capital appreciation, or both.

In the UK context, this has traditionally meant buying a residential property, letting it to tenants, and collecting rent. But the strategy landscape has expanded considerably. Today, investing in property in the UK can mean anything from owning a single terraced house in Liverpool to holding shares in a managed investment syndicate, acquiring commercial space for residential conversion, or co-investing fractionally through a platform.

Is it still worth it?

This is genuinely contested — particularly on Reddit, where r/UKPersonalFinance has spent years debating whether buy-to-let still beats the S&P 500 after tax, fees, and effort.

Here's the honest answer: it depends on your capital, your tax bracket, your time, and your strategy.

For a basic-rate taxpayer with £250,000 in cash and the right structure, a portfolio of buy-to-lets in the North can absolutely outperform index funds on a risk-adjusted basis over ten years. For a 40% taxpayer with £50,000 in savings and no appetite for hands-on management, direct buy-to-let is probably not the right starting point — but that doesn't mean property is closed off.

The key shift in 2026: property investment rewards structure and strategy far more than it did even five years ago. The investors doing well are those who have chosen wisely — not just "bought property."

How Much Money Do You Need to Invest in Property in the UK?

One of the most common questions — and one most articles answer too vaguely.

Here is a practical framework based on your starting capital:

| Capital Available | Recommended Entry Point | Expected Gross Yield |

|---|---|---|

| Under £5,000 | Property crowdfunding, REITs via ISA | 4–7% (variable) |

| £10,000–£25,000 | Managed syndication / fractional investment | 7–10%+ (managed) |

| £25,000–£50,000 | Small buy-to-let (North England, Midlands) | 5–8% gross |

| £50,000–£100,000 | HMO, larger BTL, off-plan with developer | 6–10% gross |

| £100,000+ | BRRR portfolio, commercial conversion, multiple units | 8–12%+ (deal-dependent) |

A few things worth noting:

- The 25% deposit rule. For a standard buy-to-let mortgage, you'll need a minimum 25% deposit. On a £150,000 property, that's £37,500 — before legal fees, stamp duty, and any refurbishment costs. Always model the full acquisition cost, not just the deposit.

- You don't need £100k to invest in property. Managed syndication and fractional investment platforms have opened the door to serious property exposure at lower entry points — with genuinely hands-off management. More on this below.

- Your capital tier dictates your strategy. This is not a one-size-fits-all market. The single biggest mistake new investors make is trying to force a strategy that doesn't match their resources.

7 Ways to Invest in Property in the UK (Compared)

There is no universally "best" strategy. There is only the strategy that fits your circumstances. Here's an honest comparison of the main options available to UK investors in 2026.

Strategy Comparison Table

| Strategy | Min. Capital | Avg. Gross Yield | Effort Required | Risk Level |

|---|---|---|---|---|

| Buy-to-Let (BTL) | £35,000+ | 5–8% | Medium | Medium |

| HMO | £50,000+ | 8–12% | High | Medium-High |

| BRRR | £40,000+ | 8–14% (post-refi) | High | High |

| Off-Plan | £25,000+ | 6–9% | Low | Medium |

| Managed Syndication | £10,000+ | 7–10% | Very Low | Medium |

| REITs | £100+ | 4–6% | Very Low | Low-Medium |

| Commercial Conversion | £75,000+ | 10–18% | High | High |

1. Buy-to-Let (BTL)

The foundational UK property strategy. You purchase a residential property, let it to one household, and collect rent.

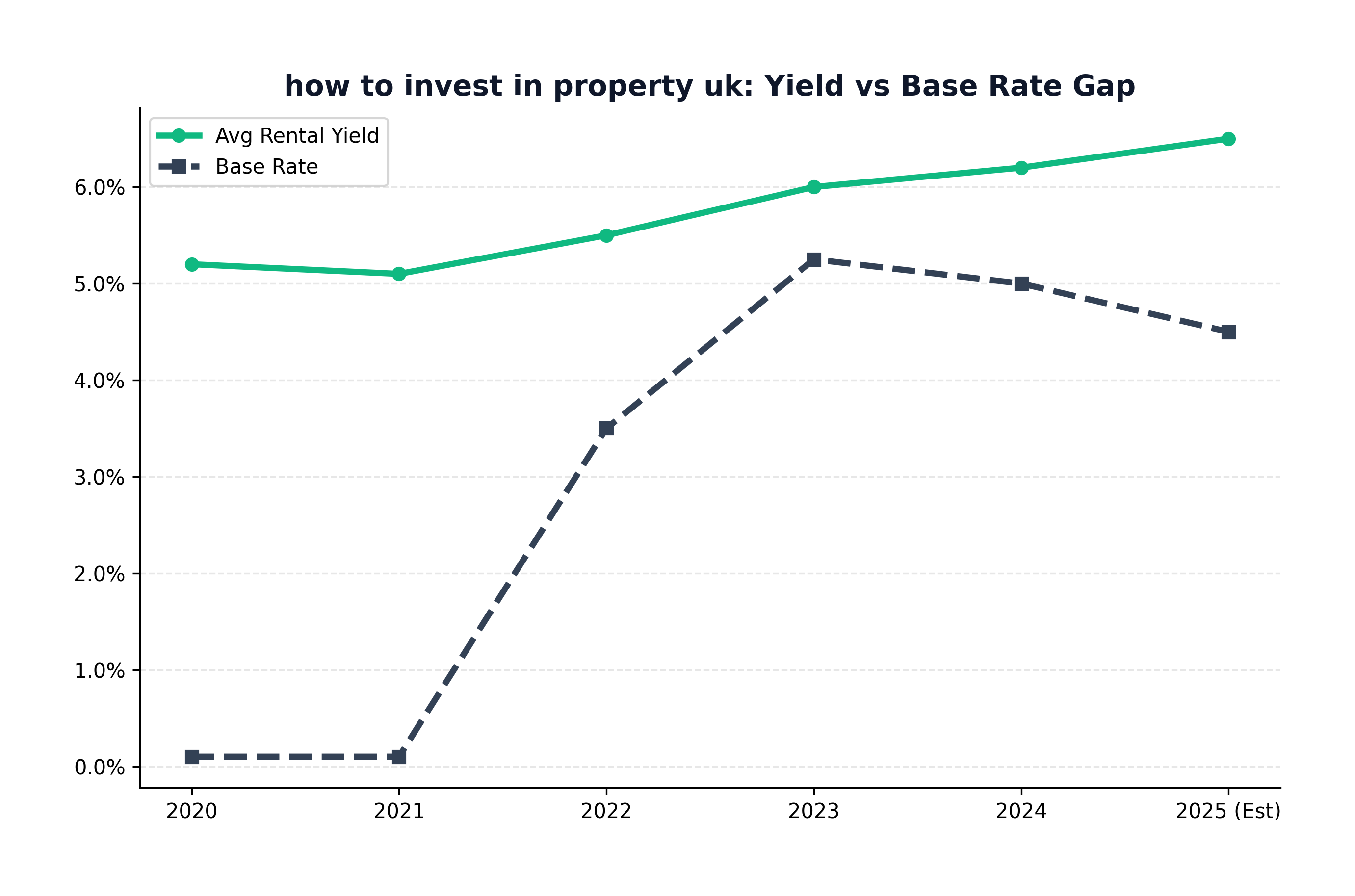

Buy-to-let is still viable — but Section 24 tax changes (limiting mortgage interest relief for individual landlords) and the October 2024 stamp duty surcharge increase to 5% on additional properties have materially changed the numbers. Run them before you commit.

What works now: Single lets in the North and Midlands, particularly in high-employment cities with strong tenant demand. A gross yield of 6%+ is the minimum worth pursuing; 7%+ is a serious target.

What doesn't: Leveraged BTL in London for most investors — the numbers rarely work once you factor in acquisition costs, void periods, and the Section 24 adjustment.

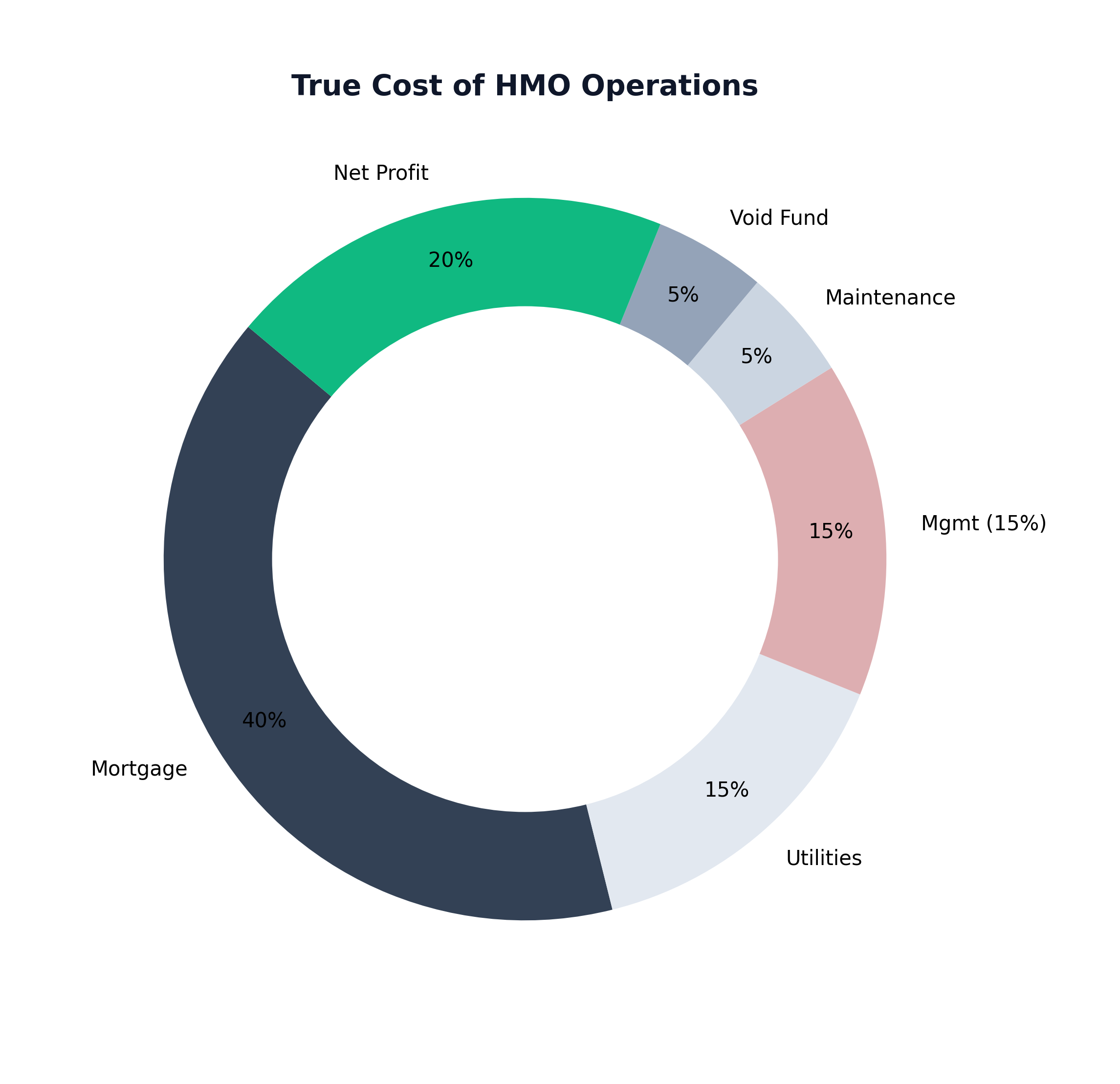

2. Houses of Multiple Occupation (HMOs)

An HMO is a property let to three or more tenants from more than one household, sharing common areas. The higher tenant count typically means higher gross rental income.

A well-run three-bedroom HMO in a university city or commuter town can return 8–12% gross — materially above standard BTL. The trade-off: licensing requirements (mandatory HMO licence for five or more occupants), higher management costs, and stricter compliance obligations under housing health and safety regulations.

HMOs reward experienced operators. For a first investment, the compliance burden can be significant. For a second or third property where you understand the management demands, they are one of the highest-yield strategies available.

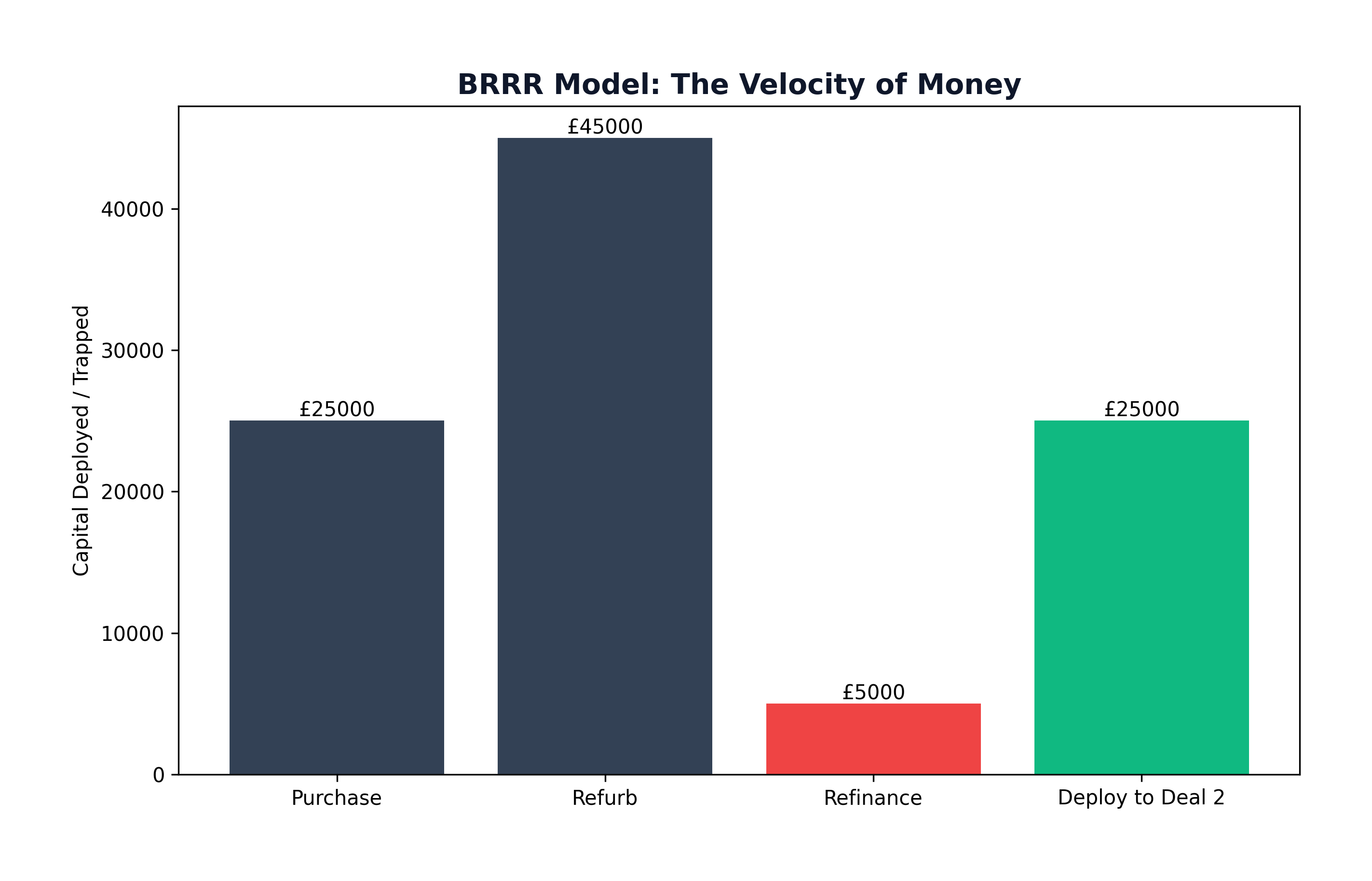

3. Buy, Refurbish, Refinance, Rent (BRRR)

BRRR is a capital recycling strategy: buy an undervalued property, renovate it to increase its value, refinance at the new higher value (releasing equity), then rent it out. The goal is to recover most or all of your initial capital within the deal.

Here's a real example from the 2024 UK market that circulated widely in property investment circles:

- Purchase: Studio flat in South Wales, £120,000

- Refurbishment: £6,000 (new kitchen, bathroom, flooring, decoration)

- Refinanced value: £170,000

- Capital released in refi: £42,500 (at 75% LTV on new value)

- Net capital left in deal: approximately £30,000

This isn't magic. It requires deal sourcing skill, the ability to manage a renovation on time and budget, and access to a buy-to-let mortgage lender willing to refinance quickly. Refurbishments consistently overrun on both time and cost for investors who haven't done one before. Factor in a 20% contingency as standard.

BRRR has diminished somewhat from its 2015–2020 golden era — higher interest rates have compressed the refi margins — but deals still exist for disciplined operators.

4. Off-Plan Property Investment

Buying a property before it's built. Developers often offer early-bird discounts of 5–15% to investors who commit during the planning or construction phase, in exchange for the risk that the finished product may differ slightly from expectations.

In cities undergoing significant regeneration — Manchester, Birmingham, Liverpool — off-plan has consistently delivered strong returns, particularly when the purchase price locks in below what the completed unit would fetch on the open market.

Key risk: developer failure. Always conduct due diligence on the developer's track record, solicit an independent valuation, and understand the completion timeline before exchanging.

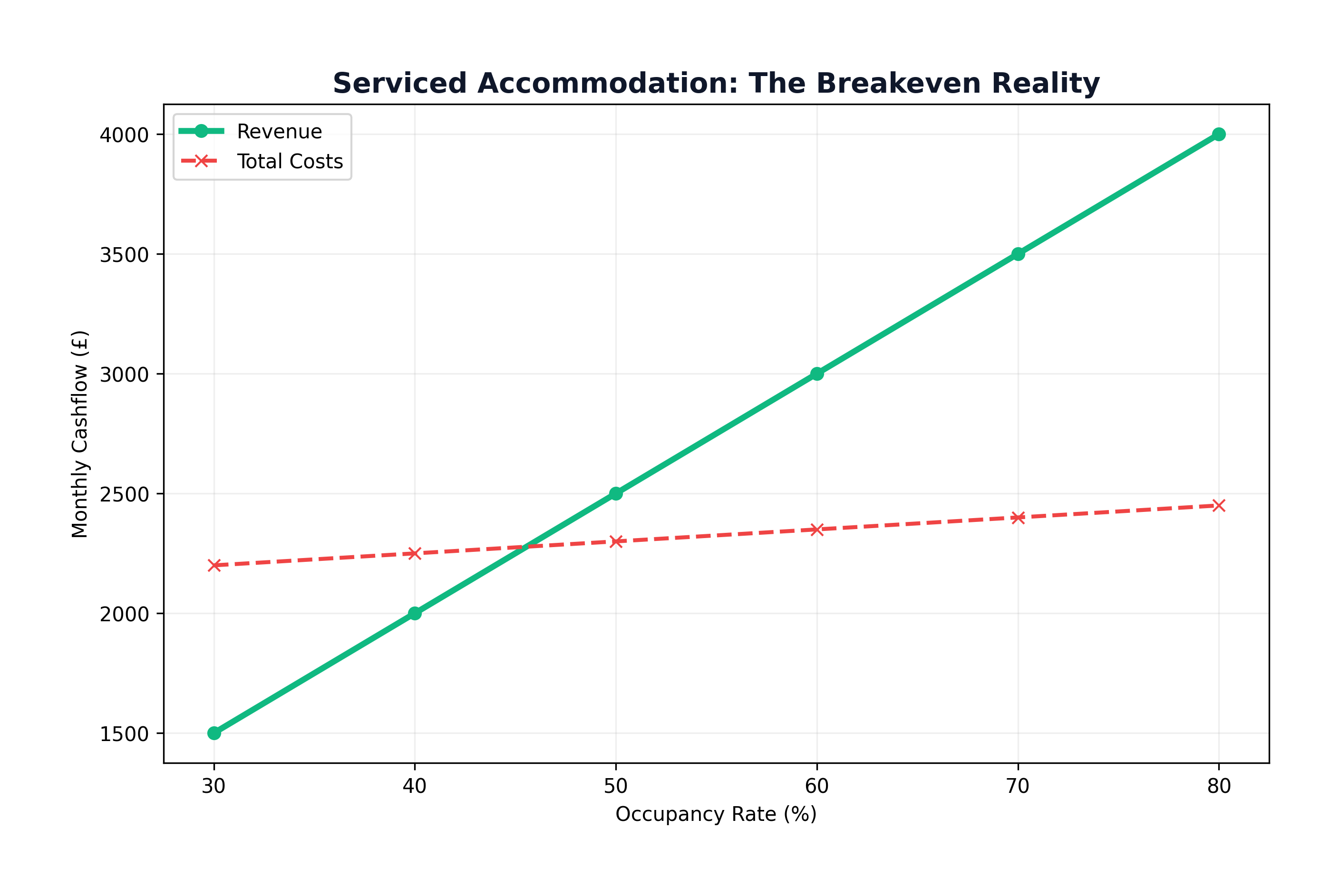

5. Managed Syndication / Fractional Investment

This is the strategy most competitors fail to cover — and it represents one of the most significant shifts in UK property investment accessibility over the past five years.

Managed syndication involves co-investing alongside other investors in a property (or portfolio of properties) managed by a professional operator. Investors own equity proportionate to their stake, receive a share of rental income, and benefit from capital appreciation — without any landlord responsibilities.

Why it matters in 2026:

- Entry from £10,000–£25,000 in some structures, rather than the £40,000+ required for a solo BTL

- Fully managed: no tenants, no maintenance calls, no compliance headache

- Access to larger, higher-quality assets (commercial, purpose-built HMOs, multi-unit buildings) that individual investors couldn't access alone

- Diversification: spread capital across multiple deals and locations

What to watch: Management fees and platform charges significantly affect net returns. Model the total cost of ownership — setup fees, annual management, re-letting charges, and maintenance mark-ups — before committing. Liquidity can also be limited; many syndication structures require a medium-to-long holding period.

At Shaded Canvas, this is the model we operate within: managed, transparent, and designed for investors who want serious property exposure without the operational burden that erodes both returns and quality of life.

6. Real Estate Investment Trusts (REITs)

REITs are companies that own and operate income-producing real estate. In the UK, you can invest in listed REITs through a Stocks and Shares ISA — making them the most tax-efficient and liquid property investment vehicle available.

Gross yields tend to be lower (4–6% for diversified UK REITs), but the simplicity, liquidity, and ISA tax wrapper are genuinely compelling for investors with smaller capital or those who want zero management involvement.

Reddit's advice here is worth noting: for lower-rate taxpayers with under £20,000 to invest, a diversified REIT or UK property fund in an ISA often matches or exceeds levered direct ownership after tax and costs. It's not exciting, but that's not always a bad thing.

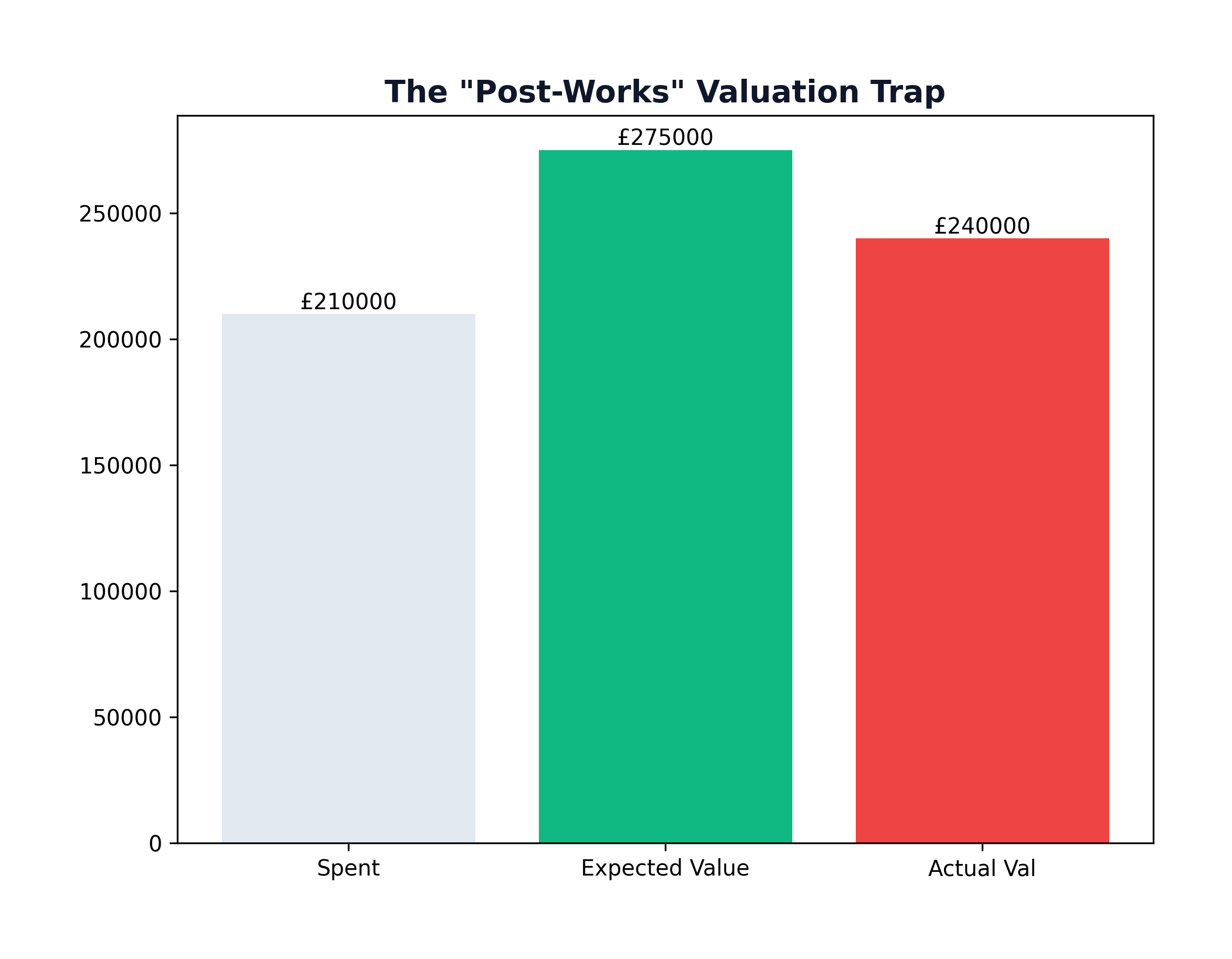

7. Commercial-to-Residential Conversions

2024 saw an expansion of Permitted Development Rights that made it meaningfully easier to convert certain commercial buildings — offices, retail units, some light industrial — into residential accommodation without full planning permission.

The appeal: commercial properties often trade at a significant discount to equivalent residential square footage. The conversion can therefore create built-in equity on day one.

This is not a beginner strategy. It requires a robust understanding of planning regulations, building control requirements, financing costs (bridging loans are typically required), and end-market demand in the conversion location. Done well, gross returns of 10–18% are achievable. Done poorly, costs spiral and the project stalls.

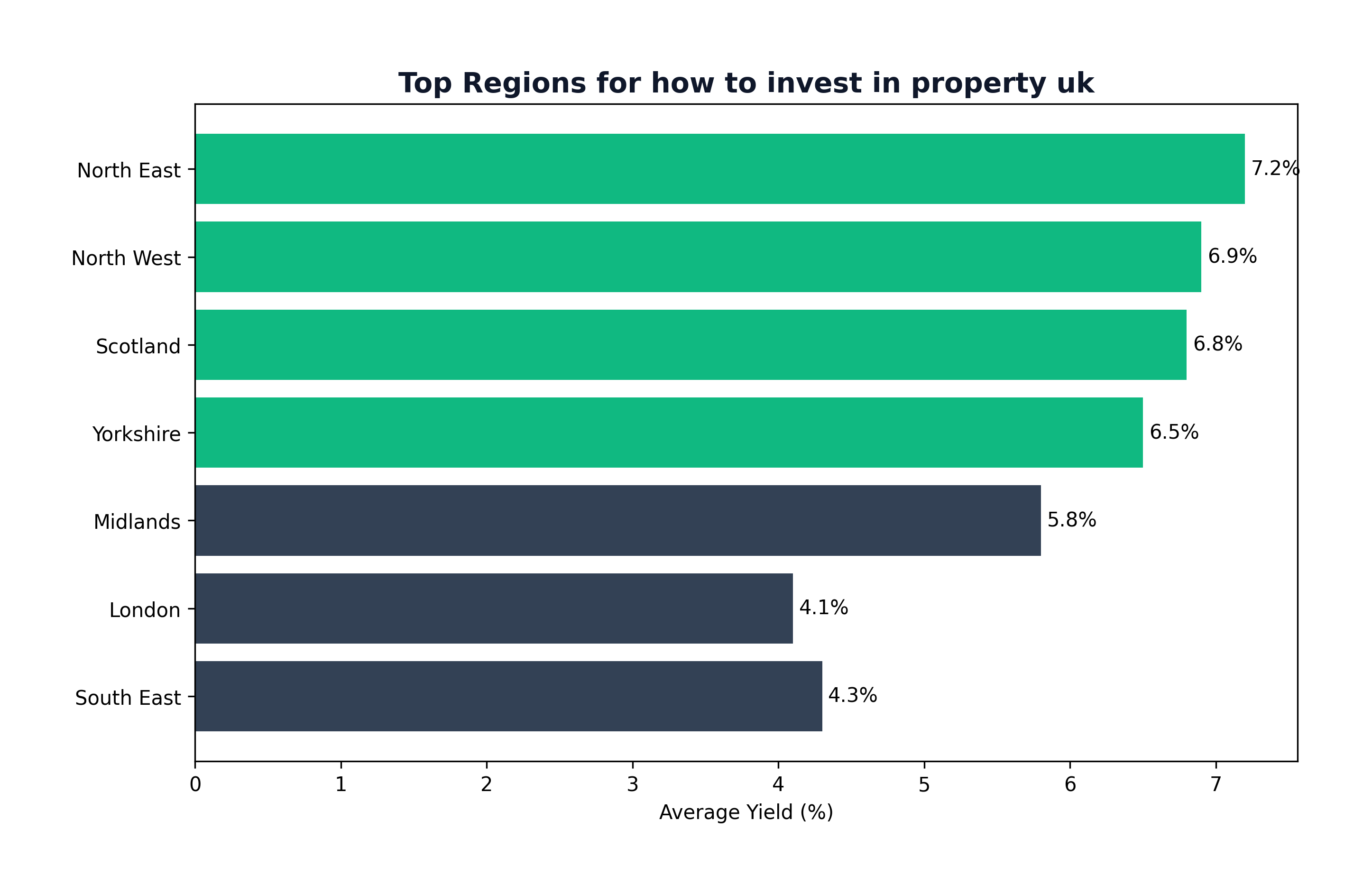

The Best UK Locations to Invest in Property (2026 Data)

Location is the variable that separates a 4% gross yield from an 8% one — often on properties of similar quality. Here's where the numbers are compelling in 2026:

| City / Region | Avg. Property Price | Avg. Gross Yield | 5-Year Capital Growth Forecast | Demand Level |

|---|---|---|---|---|

| Sunderland | ~£140,000 | 8–9% | Moderate | High (rental) |

| Glasgow | ~£175,000 | 6–7.5% | Strong | Very High |

| Liverpool | ~£185,000 | 6–7% | Strong | Very High |

| Manchester | ~£230,000 | 5.5–7% | Very Strong | Very High |

| Leeds | ~£215,000 | 5.5–6.5% | Strong | High |

| Birmingham | ~£230,000 | 5.5–6.5% | Strong | High |

| London | £500,000+ | 3–4.5% | Moderate | Very High |

| Sheffield | ~£185,000 | 5.5–7% | Moderate-Strong | High |

The Northern Powerhouse narrative is not hype. Sunderland averaging 8%+ gross yields, Glasgow and Liverpool consistently delivering 6–7%, and Manchester's continued regeneration projects are all creating genuine returns for disciplined investors.

London remains a capital appreciation play for investors with deep pockets and long time horizons. As a yield market for most investors, the numbers rarely justify the acquisition cost.

How to Finance a UK Investment Property

Buy-to-Let Mortgages

The standard financing route. Key parameters to understand:

- Minimum deposit: 25% (some lenders require 40% for the best rates)

- Rental coverage: Lenders typically require expected monthly rent to cover at least 125% of the monthly interest payment (some require 145% for higher-rate taxpayers)

- Rate premium: BTL mortgage rates run 0.5–2% above equivalent residential rates — factor this into your yield calculations

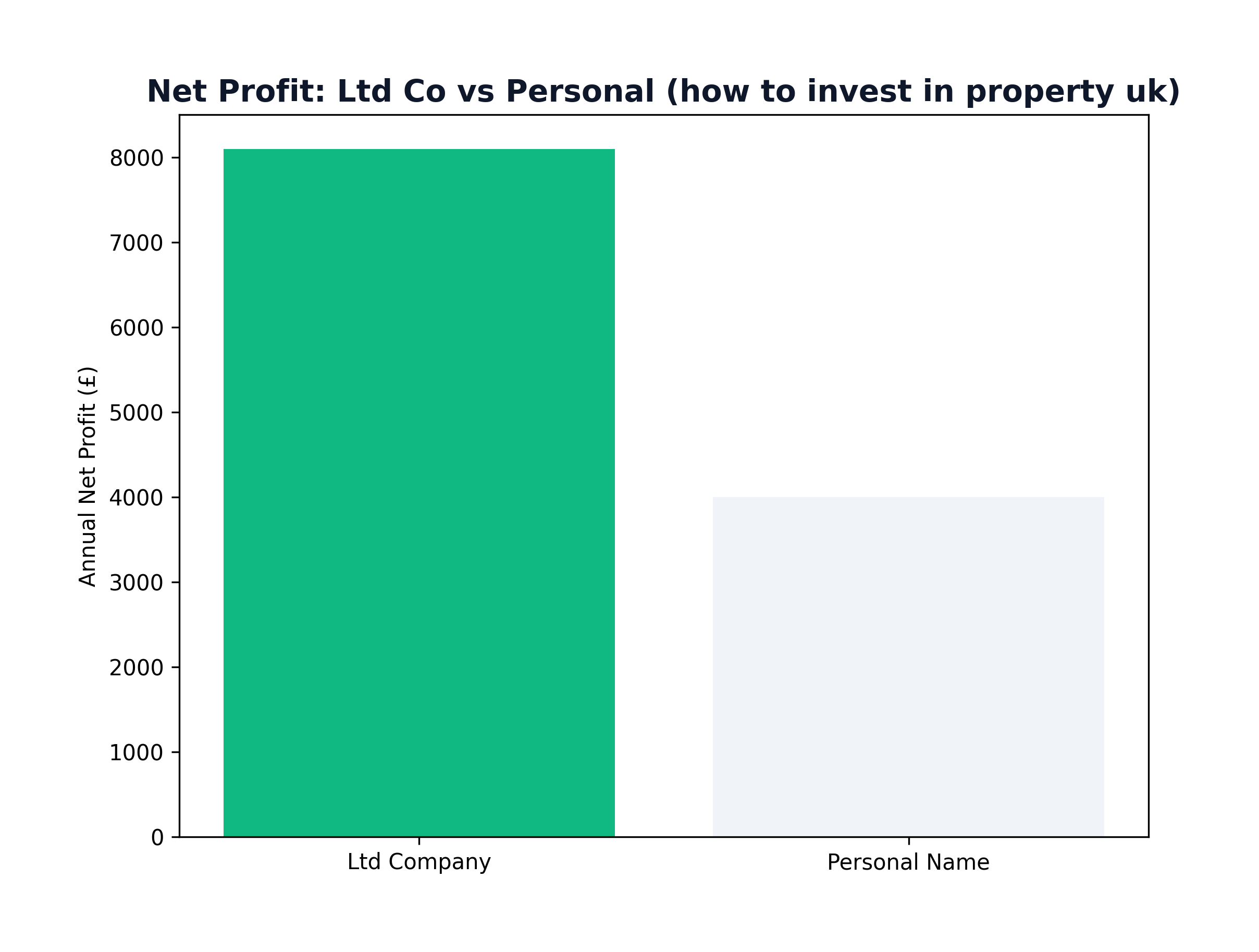

SPV / Limited Company Structure

This is consistently the most important structural decision for anyone investing in UK property at scale or in a higher tax bracket.

Since Section 24 phased out full mortgage interest deduction for individual landlords, higher-rate taxpayers who own BTL properties in their personal name face a significantly higher effective tax rate on rental income. A Special Purpose Vehicle (SPV) limited company, by contrast, continues to deduct mortgage interest as a business expense against corporation tax (currently 25% for profits over £250,000).

Honest caveats: Setting up an SPV has costs (formation, accountancy, filing), limited companies cannot access all BTL mortgage products (though the market has expanded), and extracting profits from the company creates a further tax event. Always model the numbers with your accountant before choosing the structure.

For investors planning to own more than two or three properties, or for higher-rate taxpayers, the SPV direction is increasingly hard to argue against.

Joint Ventures

For investors with time and deal-finding skills but limited capital, joint ventures — partnering with a capital provider — represent a genuine route into property investment. The deal-finder sources and manages the property; the capital partner funds the acquisition. Returns are split according to the agreed structure.

JVs require trust, legal documentation, and aligned expectations. They work best when both parties bring something the other cannot provide.

Bridging Finance

Short-term, higher-rate finance used for BRRR and conversion projects where speed is essential and a standard mortgage isn't available (e.g., uninhabitable property). Rates typically run at 0.75–1.5% per month. Bridging should always have a clear exit — usually a refinance onto a long-term product.

Tax on UK Property Investment — The Numbers You Need to Know

Tax is where most UK property investment articles go vague. Here's the actual picture:

Stamp Duty Land Tax (SDLT)

From October 2024, investors purchasing additional residential properties pay a 5% surcharge on top of standard SDLT rates. For a £200,000 property, this adds £10,000 to your acquisition cost. Model it from the start.

Non-UK residents face an additional 2% surcharge on top.

Income Tax on Rental Income

Rental income is taxable at your marginal rate. Section 24 means individual landlords receive only a basic-rate (20%) tax credit on mortgage interest — not a full deduction. For 40% and 45% taxpayers, the effective tax rate on rental income has increased materially.

This is the single biggest tax reason to consider an SPV structure before buying.

Capital Gains Tax (CGT)

When you sell an investment property, any profit above your annual CGT allowance (£3,000 in 2024/25) is taxable. UK residential investment properties attract CGT at:

- 18% for basic-rate taxpayers

- 24% for higher and additional-rate taxpayers

There is no CGT within an ISA-held REIT — another reason REITs deserve consideration for smaller portfolios.

Limited Company vs. Personal Ownership: The Tax Comparison

| Scenario | Individual (40% taxpayer) | Limited Company (SPV) |

|---|---|---|

| Rental income (annual) | £18,000 | £18,000 |

| Mortgage interest | £9,000 | £9,000 (deducted at source) |

| Taxable profit | £18,000 (no full deduction) | £9,000 |

| Tax rate | 40% (after 20% credit) | 25% corporation tax |

| Approx. tax liability | £5,400 | £2,250 |

Numbers are illustrative. Consult an accountant for your specific position.

Inheritance Tax

Investment properties held personally are included in your estate at 40% above the nil-rate band (£325,000, or £500,000 with the residence nil-rate band if applicable). SPV structures offer more flexibility for estate planning, though they don't eliminate IHT exposure automatically.

10 Mistakes UK Property Investors Make

This section doesn't exist in most competitor articles. It should.

1. Ignoring the full cost of acquisition. Stamp duty, legal fees, survey costs, mortgage broker fees, refurbishment, and landlord insurance add 8–12% to the purchase price. Many investors model yield on the purchase price alone. Model it on the total cost of ownership.

2. Choosing a property because you like it. You're not living there. Emotional property selection — buying a pretty Victorian terrace because it appeals to you rather than to tenants — is one of the most expensive mistakes in property investment.

3. Skipping the SPV structure. Higher-rate taxpayers who buy in personal name without accounting for Section 24 often find their numbers collapse within two to three years as the tax reality hits.

4. Over-leveraging on BRRR. Renovation projects have a near-universal tendency to overrun. Enter a BRRR with no contingency and you'll fund the overrun from personal savings or stall the project entirely.

5. Defining "cheap" as "good yield." A £60,000 terraced house in a low-demand area with high void periods and antisocial tenancy risk does not produce better returns than a £180,000 property in Liverpool with consistent 6.5% yield. The numbers tell the whole story — not the headline price.

6. Buying a property guru course. Reddit is unambiguous on this and they're right. The investors who have built serious UK property portfolios have learned through books, mentors, and doing — not through £5,000 weekend courses that primarily enrich the course provider.

7. Setting rent based on aspiration, not market. Too high and you sit empty. Too low and you erode your margin for years. Use Rightmove, Zoopla, and local agents to sense-check your rental expectation before you complete.

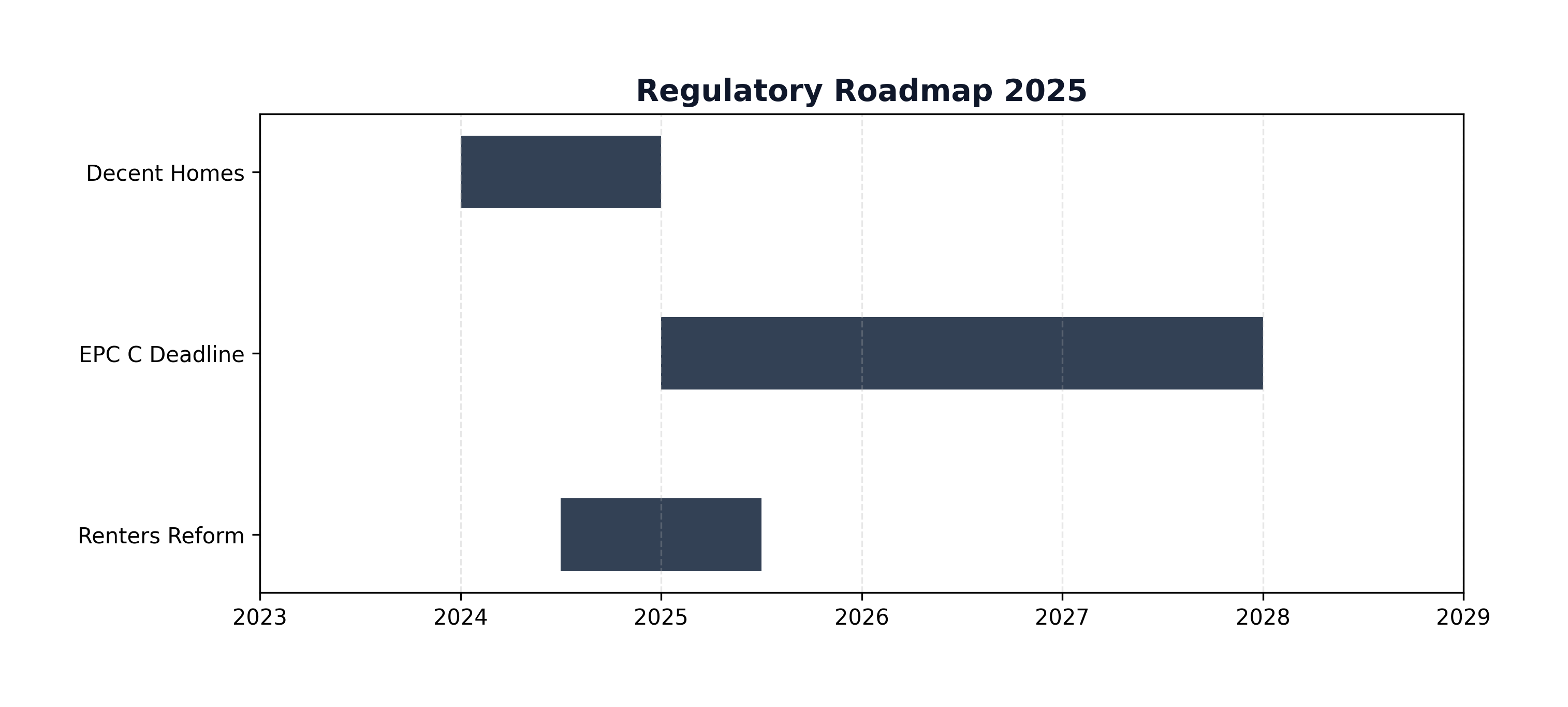

8. Failing compliance basics. A property without a valid EPC (minimum E rating required from April 2026 and likely to tighten further), gas safety certificate, and electrical safety report exposes you to civil penalties, inability to serve notice, and in some cases criminal liability. These are not optional.

9. Waiting for perfect conditions. The investors who made money in 2020 didn't have the benefit of hindsight. They had a clear strategy, a good deal, and the discipline to execute. Persistent market-timers consistently miss the window.

10. Having no exit strategy. When will you sell? Under what conditions? To whom? If you can't answer these questions before you buy, you haven't finished planning your investment.

Step-by-Step: How to Start Investing in Property in the UK

Here's a structured process for investors who are serious about execution:

Step 1: Define your objective. Income now, capital growth later, or a balance of both? Your answer shapes every subsequent decision — strategy, location, leverage, and hold period.

Step 2: Assess your capital realistically. Not just what you have in savings, but what you can deploy without creating personal financial risk. Include acquisition costs in your capital model.

Step 3: Choose your strategy. Use the capital tier framework and strategy table above. Match strategy to capital, time, and tax position.

Step 4: Build your professional team. You need, at minimum: a specialist buy-to-let mortgage broker, a conveyancer experienced in investment property, a property-literate accountant, and a letting agent who operates in your target area. Don't try to do this without them.

Step 5: Research your target location. Look at: average rents on Rightmove and Zoopla (not what landlords ask — what comparable properties actually let for), void rate estimates from local agents, regeneration plans, and employment anchors in the area.

Step 6: Run the full numbers. Use this yield calculation as a starting point:

Gross yield = (Annual rent / Total purchase cost) × 100

Net yield = (Annual rent – Annual costs) / Total purchase cost × 100

Costs include: mortgage interest, letting agent fees (8–15% of rent), maintenance reserve (typically 10% of rent), insurance, and your management time if relevant.

Step 7: Negotiate and complete. Unlike residential buyers, investment purchases are driven by numbers, not emotion. Make offers based on your yield targets, not comparables. Be prepared to walk away from anything that doesn't work on paper.

Step 8: Let and manage (or delegate entirely). Decide before you complete whether you will self-manage or use a letting agent. Self-management saves money and costs time; professional management costs money and saves time. For investors with multiple properties or demanding careers, professional management almost always makes sense mathematically when quality of life is included.

Is Property Investment Right for You? An Honest Assessment

Property investment is likely right for you if:

- You have at least £25,000 in capital available (or £10,000 for managed/syndicated routes)

- You have a long-term mindset (5–10 years minimum horizon)

- You are willing to invest time in understanding the tax and legal landscape

- Your financial position can absorb a 3–6 month void period without stress

It may not be the right starting point if:

- Your entire available capital is below £10,000 (explore REITs or property funds in an ISA first)

- You need immediate liquidity — investment property is illiquid

- You are a higher-rate taxpayer who hasn't modelled the Section 24 impact yet

The honest alternative: For investors who genuinely cannot or don't want to manage the operational demands of direct property ownership, a diversified global equity index fund in a Stocks and Shares ISA will, over a 20-year compounding horizon, outperform leveraged buy-to-let for many individuals. This isn't defeatism — it's intellectual honesty. Know what you're getting into.

How Shaded Canvas Approaches Property Investment

At Shaded Canvas, we operate a managed syndication model designed for investors who want serious property exposure without the landlord burden.

What that looks like in practice:

- Hands-off, fully managed — we handle everything: acquisition, tenancy, compliance, maintenance, reporting

- Lower entry point — access to larger, institutional-quality assets from a fraction of what direct ownership requires

- Transparent returns — clear reporting, no hidden management mark-ups

- Designed for working professionals and experienced investors who want their capital working harder without their time being consumed

If you're considering how to invest in property in the UK and want to explore whether our model fits your situation, start with a discovery call. We'll give you the honest picture — including whether our approach is right for you.

Final Thoughts

Property investment in the UK works in 2026. But it works best for investors who have done the preparation — who understand the strategy, the structure, the tax, and the location — before they deploy a single pound.

The era of set-it-and-forget-it BTL is behind us. What's in front of us is a market that rewards discipline, punishes laziness, and continues to generate serious long-term wealth for the investors who approach it correctly.

Do the numbers. Choose the right structure. Pick a strategy that fits your capital. And if you're not sure where to start — talk to someone who's already operating in the market, not someone selling you a course about it.

Stop being a landlord. Start being an investor.

Shaded Canvas introduces serious capital to vetted UK property opportunities — targeting 12–16% net returns.

Start Investing →