The UK new build sector has undergone a radical transformation. Gone are the days of blind speculation, where retail investors threw 20% deposits at obscure developers and waited for unearned capital appreciation to bail them out of bad mathematics.

In 2026, the cost of commercial debt, stringent RICS surveyor guidelines, and inflated construction costs have created a hyper-segmented market. If you execute a flawed new build strategy today, you will face catastrophic valuation gaps, soaring service charges, and unviable yields.

However, for sophisticated investors who understand staging leverage, localized regeneration premiums, and institutional block pricing, the new build sector remains one of the most mechanically profitable asset classes in Europe.

In this 3,000-word audit, we will dismantle and rebuild the best new build property investment strategies 2026. We will cover how to extract 50%+ ROCE before a building even completes, how to weaponize the zero-CapEx nature of modern apartments, and how to execute the exact block-arbitrage models utilized by Shaded Canvas.

The Core Thesis: Why Buy New Build at a Premium?

The most common criticism of new build property is the "New Build Premium." Developers typically price unbuilt units 10% to 15% higher than equivalent secondary stock (older Victorian or 1990s housing) in the exact same postcode.

Why pay a premium when you could buy cheaper secondary stock?

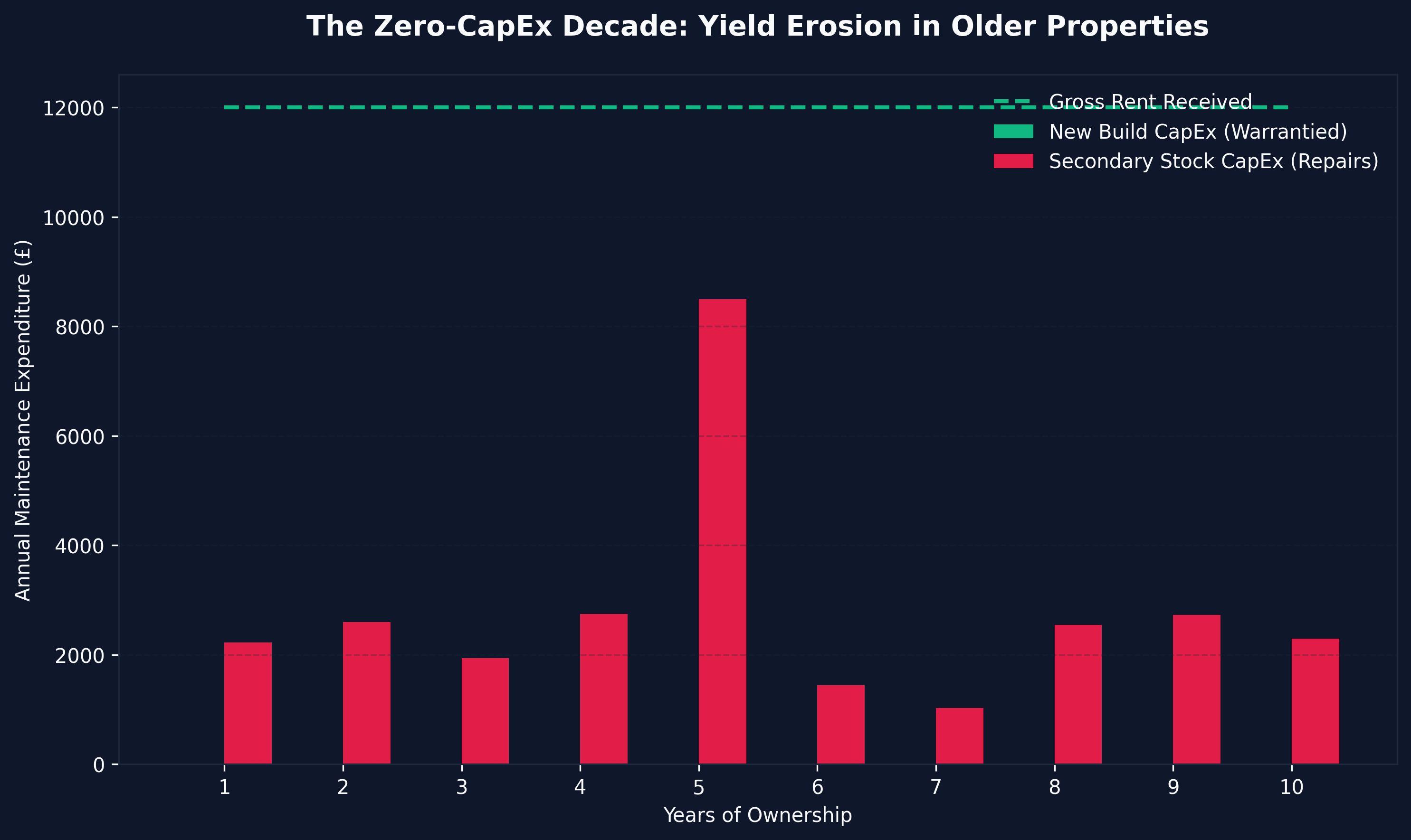

1. The Zero-CapEx Decade

The profit model of how to invest in property uk is constantly threatened by Capital Expenditure (CapEx). When a 30-year-old boiler fails, or a Victorian roof begins to sag, a £4,000 repair bill instantly annihilates an entire year of net rental profit.

New builds eliminate this variable. Regulated by the NHBC (National House-Building Council) 10-year structural warranty and a 2-year developer defect warranty, a new build investor effectively models exactly £0 in capital expenditure for the first decade of ownership.

2. Hyper-Leveraged Staging

You cannot buy a £250,000 Victorian terrace with £12,500. You must complete the purchase in 8 weeks via a 25% deposit (£62,500) and a mortgage.

With new builds (off-plan), developers in 2026 frequently accept a 5% exchange deposit (£12,500). That £12,500 legally controls a £250,000 asset for two years. If the asset grows by 5% annually during the build cycle, the total GDV reaches £275,625. Your £12,500 deposit generated £25,625 in underlying equity—a 205% Return on Capital, purely via mechanical staging leverage.

3. The Energy Performance (EPC) Mandate

The legislative landscape in 2026 heavily penalizes energy-inefficient properties. Secondary stock (EPC ratings of D, E, or F) requires vast retrofitting capital (insulation, heat pumps) to remain legally lettable under the Minimum Energy Efficiency Standards (MEES). New builds guarantee EPC A or B ratings out of the box, future-proofing your portfolio against green compliance fines.

With the foundational advantages established, we must explore the specific strategies required to exploit them.

Strategy 1: The Pre-Completion Flip (Contract Reassignment)

The Pre-Completion Flip is the most aggressive, highest-yielding, and highest-risk strategy in the new build playbook. It involves buying off-plan, riding the localized capital growth curve during the two-year construction phase, and selling the contract before you actually have to buy the apartment.

The Mechanics of the Flip

- The Exchange: You reserve a £300,000 apartment in a Phase 1 release of a massive regeneration zone (e.g., Ancoats in Manchester or Digbeth in Birmingham). You put down a 10% deposit (£30,000).

- The Growth Cycle: Over the next 24 months, the developer completes the building. Alongside inflation, the completion of local infrastructure (tram stops, commercial hubs) drives organic capital growth.

- The Reassignment: Six months before the building is finished, the current market value (GDV) of the apartment is £340,000. Under the "reassignment clause" in your contract, you sell your rights to purchase the unit to a hands-off investor for £340,000.

The Mathematics

- Initial Capital Deployed: £30,000

- Sale Price (Reassignment): £340,000

- Original Contract Liability: £270,000 (Owed to the developer)

- Net Gross Profit: £40,000

- Return on Capital Employed (ROCE): 133%

You extracted a 133% return from real estate without ever securing a mortgage, paying stamp duty (SDLT is paid at physical completion), or dealing with a tenant.

The Critical Risks

This strategy is highly precarious in 2026. If the market stagnates and the property does not grow from £300,000, you will not find a buyer willing to pay a premium. You are now legally required to complete the £300,000 purchase.

If you do not have the financial liquidity to secure a 75% commercial mortgage and bridge the remaining 15% balance, you will default. You will lose your £30,000 deposit and the developer will pursue you for breach of contract.

To understand exactly how bridging loans can save a failing reassignment strategy, you must review our comprehensive audit on how to finance new build property investment.

Strategy 2: The High-Yield Holding Strategy (Yield Stripping)

For investors seeking passive liquidity rather than speculative equity gains, the High-Yield Hold is the definitive 2026 off-plan strategy.

This involves retaining the asset at practical completion and utilizing the unique characteristics of new developments to maximize the Net Operating Income (NOI).

The CapEx Delta

If a traditional BTL yields 6% gross, and a new build yields 5.5% gross, retail investors often mistakenly choose the traditional BTL.

However, older stock requires roughly 1% to 1.5% of the property’s value in annualized maintenance. A £250,000 older terraced house will consume ~£3,000 per year in structural repairs, void periods (during repairs), and compliance updates.

The new build (under its NHBC 10-year warranty) consumes £0.

- Older Stock Net Yield: 6% Gross - 1.5% CapEx = 4.5% True Net Yield

- New Build Net Yield: 5.5% Gross - 0% CapEx = 5.5% True Net Yield

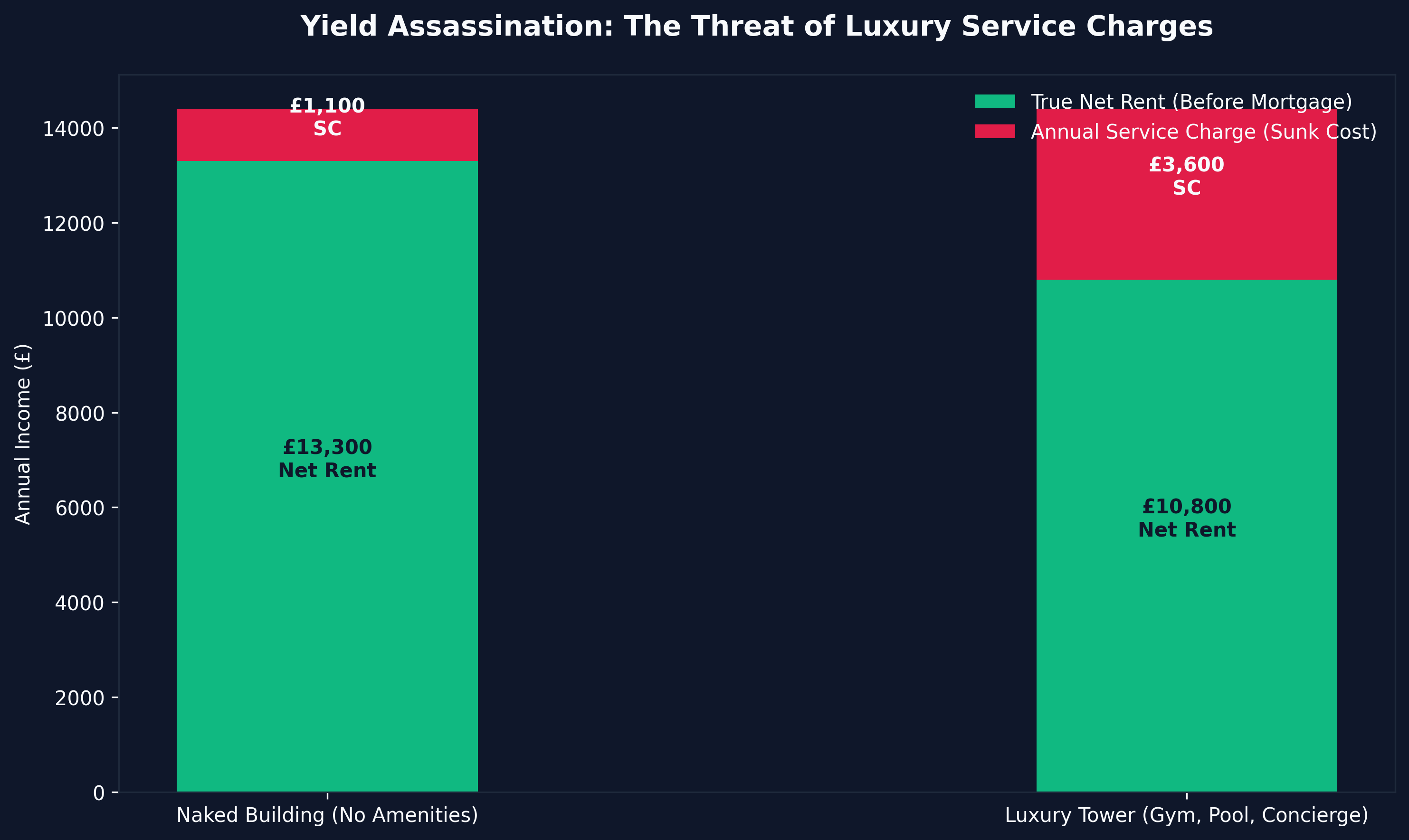

The "Service Charge" Threat

The holding strategy is frequently assassinated by escalating service charges. High-rise new builds equipped with concierges, gyms, pools, and cinema rooms carry exorbitant monthly management fees. A £300-per-month service charge (£3,600 annualized) will utterly destroy your rental yield.

The best holding strategy in 2026 requires targeting "naked buildings"—boutique new builds containing 20 to 50 units with zero luxury amenities. No gym. No pool. No 24-hour concierge. Only a secure entry system and a lift. This keeps the service charge beneath £1,200 annually, preserving your gross-to-net yield conversion.

To model your exact net yield and stress-test these service charges, utilize our free off plan property investment yield calculator uk.

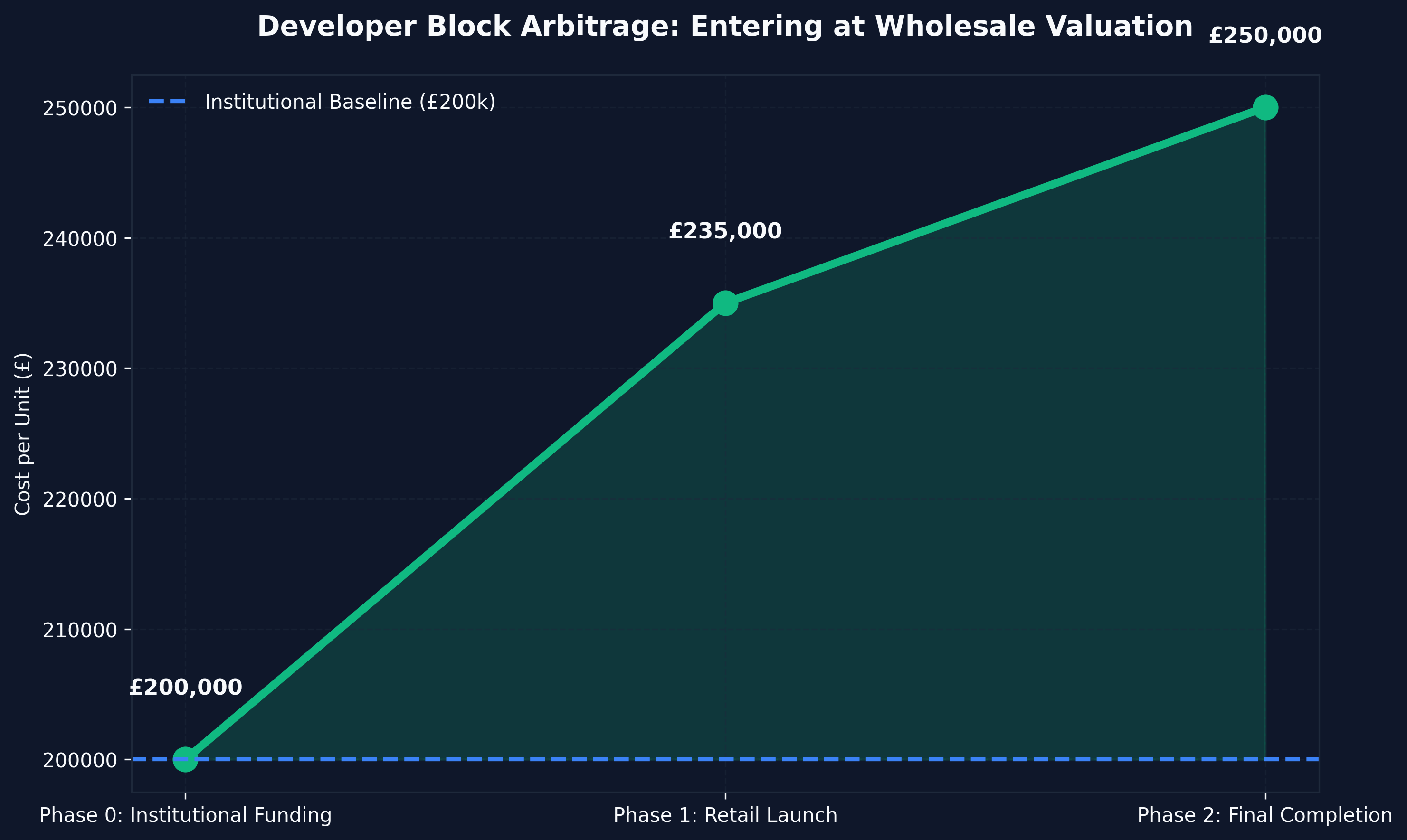

Strategy 3: Developer Block Arbitrage (The Institutional Model)

Retail investors buy single units. Institutional investors (and syndicated wealth structures) buy entire blocks. This is the Block Arbitrage Strategy.

When a developer plans a 100-unit tower, they possess massive exposure. Constructing the tower requires a £15M commercial development loan. To secure that loan, the bank requires the developer to prove "demonstrable demand" by pre-selling 30% of the units off-plan.

The developer is desperate for early liquidity to satisfy the bank.

The Arbitrage Mechanics

An institutional fund approaches the developer at "Phase 0" (before any marketing brochures are printed).

The fund offers to buy 20 units in a single transaction, instantly satisfying the bank's pre-sale criteria. In exchange for de-risking the entire £15M project, the developer gives the institutional fund a 20% wholesale discount.

- Retail Unit Price (Phase 2 Launch): £250,000

- Institutional Block Deal Price: £200,000

The institution holds a massive £50,000 equity buffer from Day 1.

How Retail Investors Access Block Arbitrage

Historically, retail investors with £20,000 in savings were locked out of block arbitrage. You cannot command a 20% developer discount by buying a single 1-bed apartment.

However, in 2026, the rise of heavily regulated fractional property investment UK platforms has democratized this structure. Wealth platforms (like Shaded Canvas) pool the capital of 100+ retail investors to acquire the 20-unit block at the £200,000 wholesale price.

The retail investor benefits from the exact same 20% equity buffer and high-yield fundamentals as the £50M institutional fund, without needing to front the entire £4M acquisition cost.

This is fundamentally the safest new build investment strategy available, as the 20% discount acts as a massive shock-absorber against surveyors down-valuing the property (the dreaded Valuation Gap) upon completion.

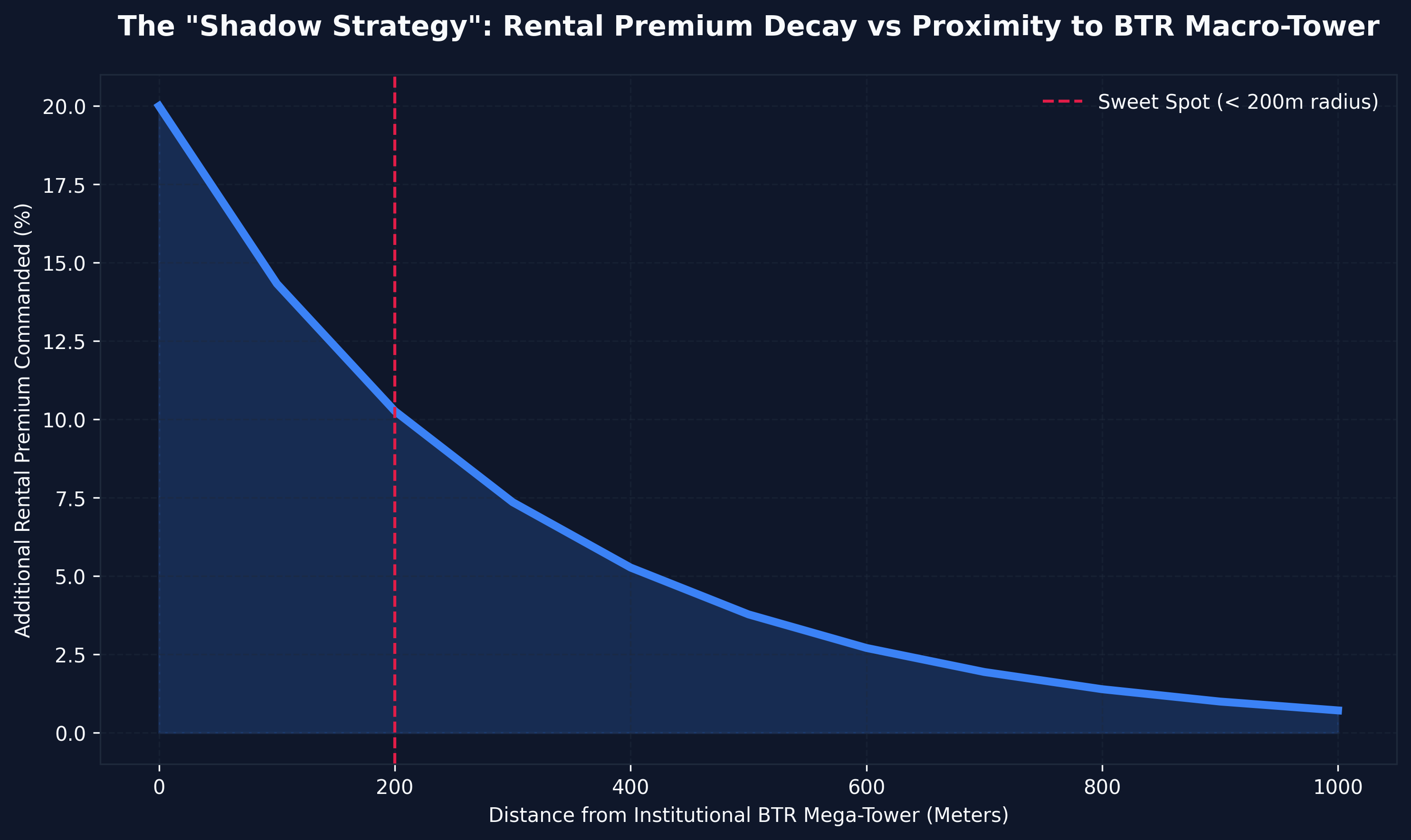

Strategy 4: The Build-To-Rent (BTR) "Shadow" Strategy

Build-to-Rent (BTR) is currently dominating the UK skyline. Mega-corporations (Legal & General, Goldman Sachs, Lloyds Bank) are building massive, 500-unit premium towers designed exclusively for renting. They do not sell these units; they hold them forever to collect the yield.

These BTR towers provide unprecedented levels of service: dog walking, ultra-fast Wi-Fi, resident events, and co-working spaces.

Retail landlords cannot compete with the amenities of a £100M BTR tower. However, retail landlords can execute the Shadow Strategy.

The Shadow Mechanics

BTR towers carry massive rent premiums. A 1-bed apartment in a generic block might cost £1,000 per month. The equivalent 1-bed in a Goldman Sachs BTR tower across the street will cost £1,400 per month.

The "Shadow Strategy" requires you to purchase a new build off-plan unit in a smaller, boutique development immediately adjacent to a planned institutional BTR mega-project.

Once the BTR tower completes, it acts as a massive gravitational pull for affluent young professionals. However, many of those professionals will balk at the £1,400 per month rent. They will look at the immediate surrounding streets.

Because your unit is brand new, hyper-modern, and situated 50 meters from the BTR mega-tower, you can shadow their pricing. You command a rental premium (£1,250 a month) from tenants who want the prestige of the location without the corporate BTR price tag. Furthermore, the massive regeneration infrastructure (cafes, transit) built to service the BTR tower fundamentally drives the capital value of your smaller asset upward.

Strategy 5: Integrating BRRRR with New Builds (The Broken Developer Model)

The "Buy, Rehab, Rent, Refinance, Repeat" (BRRRR) strategy is traditionally reserved for heavily dilapidated, unmortgageable secondary stock. (See: What is the BRRRR Method?).

However, a highly localized variation exists in the new build space during periods of economic distress: The Broken Developer Model.

In 2026, due to fluctuating supply chains and high financing costs, smaller SME developers occasionally run out of liquid capital halfway through a build. The bank pulls their funding, and the half-finished site is handed to receivers.

The Execution

Aggressive investors purchase these partially-completed "new builds" from the receivers at 50p on the pound using high-interest bridging finance.

They then deploy heavily structured construction teams to finish the remaining 30% of the build (installing kitchens, landscaping, final compliance sign-offs). Once signed off by building control, the asset is instantly classed as a completed "New Build."

- Purchase Price (From Receiver): £120,000

- Cost to Complete (Rehab): £40,000

- Total Capital Deployed: £160,000

- End GDV as a "New Build": £260,000

- Brutal Equity Creation: £100,000

The investor then refinances the completed new build onto a traditional commercial Buy-to-Let mortgage at 75% LTV, extracting their £160,000 capital in full, whilst retaining a cash-flowing asset with a 10-year warranty.

It is the most complex orchestration of off-plan mechanics and the BRRRR framework available in the market. Model the exact mathematics using our specialized Buy Rehab Rent Refinance Repeat Yield Calculator UK.

Summary: Navigating 2026

The best new build property investment strategies 2026 rely entirely on acknowledging the systemic risks of the sector and pricing them into your models before you exchange contracts.

Whether you are targeting a 130% ROCE via a pre-completion flip, executing the BTR shadow strategy to inflate your rental yields, or utilizing a fractional wealth platform to access institutional block discounts, the underlying mathematics must dictate your actions.

Never pay the "Retail Premium" blindly. Ensure your chosen strategy fundamentally insulates you against down-valuations, escalating service charges, and developer insolvency.

Stop being a landlord. Start being an investor.

Shaded Canvas introduces serious capital to vetted UK property opportunities — targeting 12–16% net returns.

Start Investing →