If you have spent any time researching property investment in the United Kingdom, you have almost certainly encountered the acronym BRRRR. It saturates every YouTube channel, property podcast, and investment forum. But behind the hype, the majority of content creators fail to explain the raw, commercial mechanics that actually make it work—or that cause it to catastrophically fail.

So let us answer the fundamental question: what is the BRRRR method and how does it work?

BRRRR stands for Buy, Rehab, Rent, Refinance, Repeat. It is a systematic real estate investment strategy designed to allow private investors to recycle a single pot of seed capital indefinitely, acquiring multiple income-generating properties without requiring fresh savings for each new purchase. When executed correctly within the UK's fiscal and regulatory framework, it is the most powerful portfolio-scaling engine available to non-institutional investors.

At Shaded Canvas, we have underwritten and executed this exact framework across dozens of commercial-grade transactions. This comprehensive authority guide will forensically disassemble each of the five phases, explain the exact mathematics with real 2026 UK numbers, and expose the critical failure points that separate elite operators from bankrupt amateurs.

Phase 1: BUY — Acquiring the Distressed Asset

The first letter in the BRRRR acronym is the most misunderstood. You are not buying a clean, turnkey, move-in-ready property from Rightmove. You are specifically hunting for distressed, unmortgageable assets that the mainstream market cannot touch.

What Makes a Property "Distressed"?

A distressed property is one that a standard high-street mortgage lender will refuse to finance. Common disqualifying defects include:

- No functional kitchen or bathroom (lender minimum habitation standards)

- Structural subsidence or severe damp penetration

- Asbestos-containing materials

- Japanese Knotweed within 7 metres of the dwelling

- Properties without a valid EPC or with an EPC rating below E

- Fire-damaged or flood-damaged structures

Because mainstream lenders will not issue a mortgage on these assets, retail buyers are entirely locked out. This creates a massive pricing inefficiency. The distressed property that would be worth £200,000 in renovated condition is frequently available at auction or via motivated sellers for £80,000 to £120,000. That gap between the distressed purchase price and the renovated market value is the entire engine of the BRRRR method.

How Do You Finance the "Buy" Phase?

Since a standard mortgage is impossible, you must deploy Bridging Finance. A bridging loan is short-term, high-interest commercial debt (typically 1% per month) designed to "bridge" you from acquisition to the point where the property is refinanceable. In 2026, a standard bridging product offers 70-75% Loan-to-Value (LTV) against the purchase price.

Example: You identify a fire-damaged terrace in Bolton, Lancashire. The auction guide price is £85,000.

- The bridging lender advances 75% = £63,750

- You contribute 25% deposit = £21,250

- Bridging fees (2% arrangement + legals) = ~£3,000

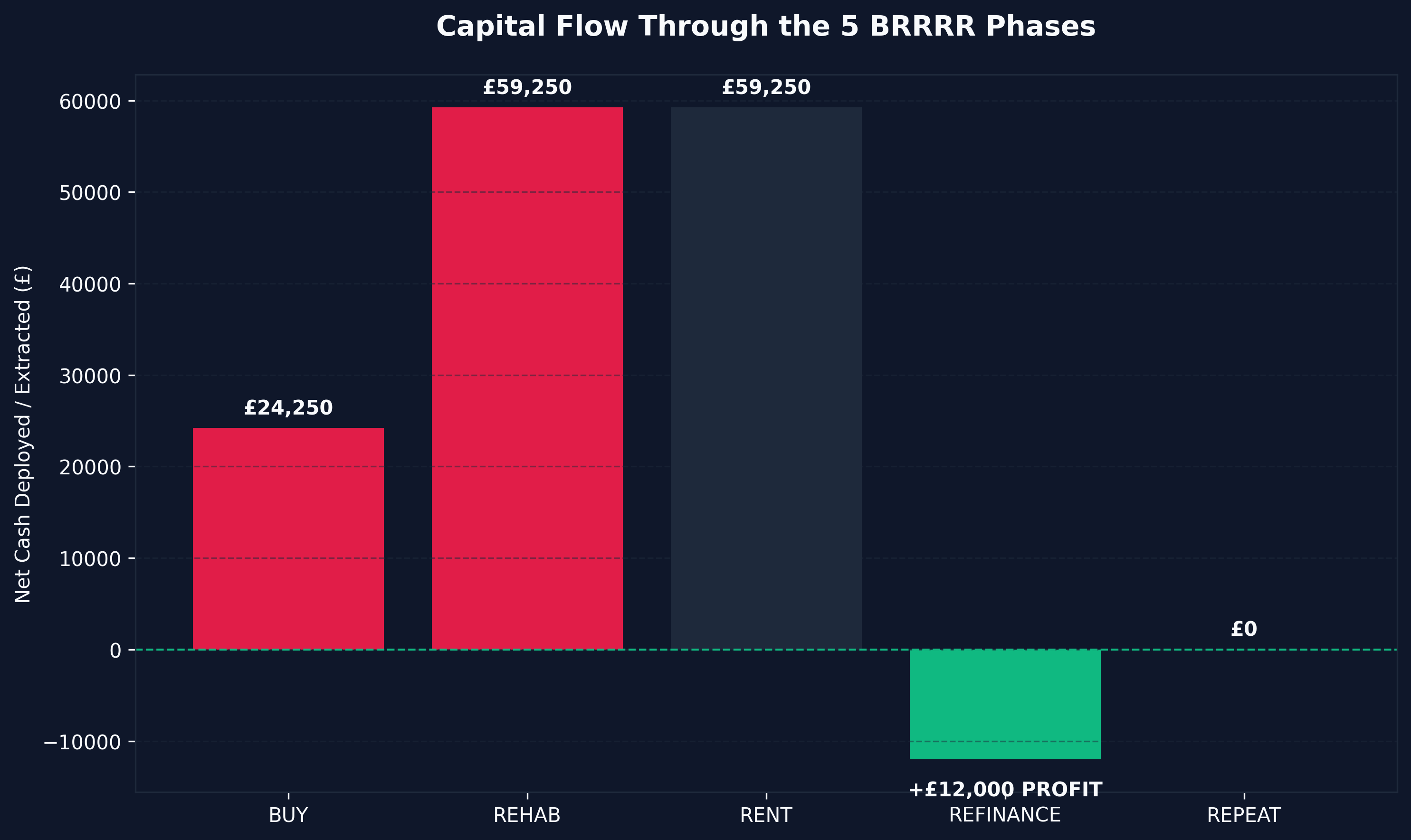

- Total Cash Required for Acquisition: ~£24,250

The critical point: this cash is not "spent." It is temporarily deployed. The entire objective of the BRRRR method is to extract this capital back out during the Refinance phase.

Phase 2: REHAB — Executing the Heavy Refurbishment

The "Rehab" phase is where the forced appreciation is physically manufactured. You are not painting walls and replacing carpet. You are executing a heavy, value-adding refurbishment that transforms an unmortgageable shell into a premium rental asset.

What Does a Typical BRRRR Rehab Involve?

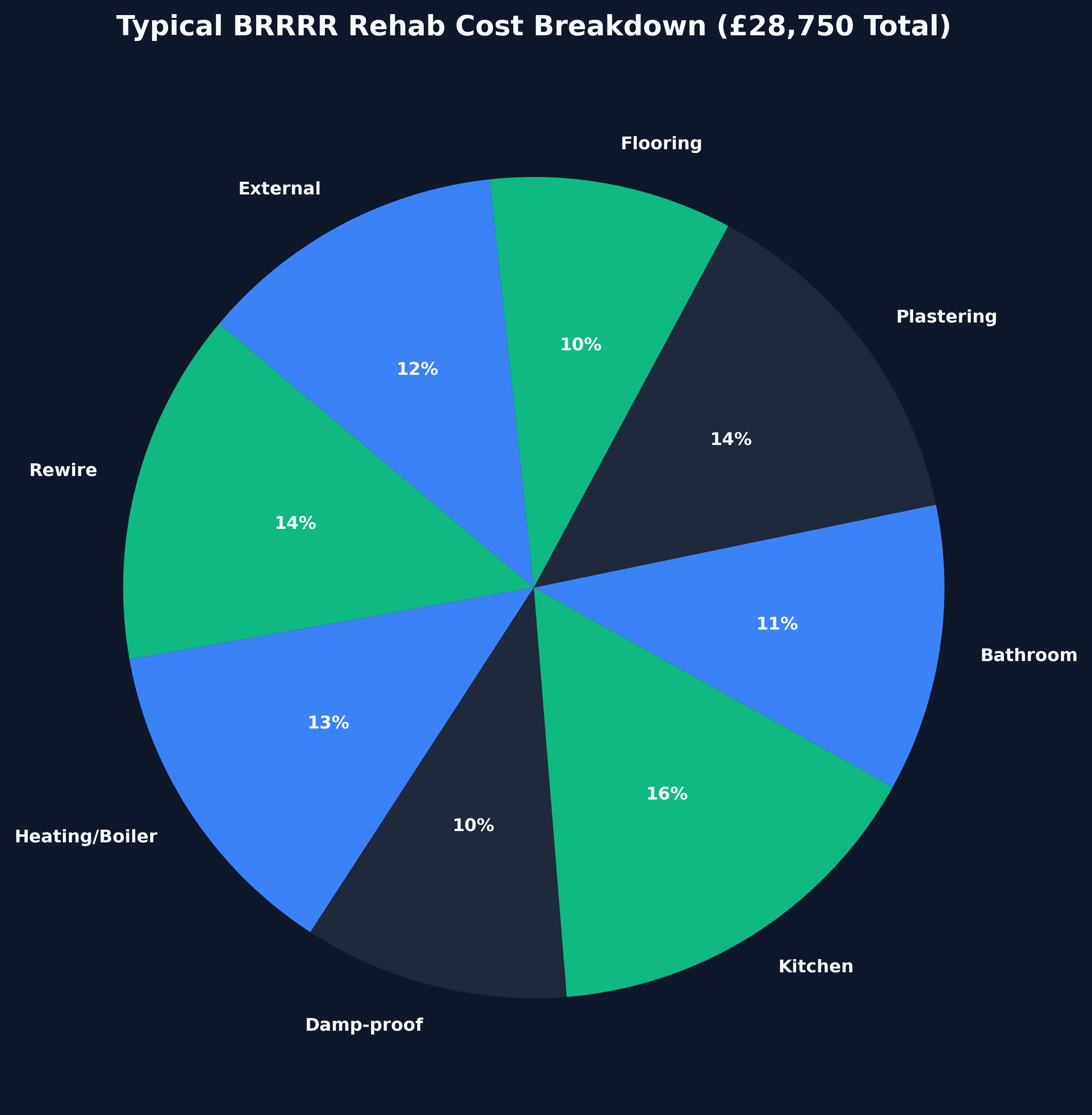

A standard heavy rehab on a Northern England terrace typically includes:

- Full rewire (£3,000 - £5,000)

- New central heating system and boiler (£3,000 - £4,500)

- Damp-proofing and tanking (£2,000 - £4,000)

- New kitchen installation (£3,000 - £6,000)

- New bathroom installation (£2,500 - £4,000)

- Full replastering and decoration (£3,000 - £5,000)

- New flooring throughout (£2,000 - £3,500)

- External works, pointing, and roof repairs (£2,000 - £5,000)

Total typical rehab budget: £25,000 to £40,000

The HMO Conversion Premium

Elite BRRRR operators frequently convert standard single-let properties into Houses in Multiple Occupation (HMOs). By subdividing a 4-bedroom house into individually lettable rooms with shared communal spaces, you can dramatically increase the gross rental yield from ~6% to 12-15%. This elevated yield makes the final refinance phase significantly easier because commercial lenders stress-test the rental income against the mortgage payment.

VAT Mitigation on Rehab Costs

A critical fiscal element: if the property has been genuinely empty and unoccupied for over two continuous years, the majority of the building labour and materials qualifies for a reduced 5% VAT rate instead of the standard 20%. On a £40,000 rehab, this single structural decision saves you £6,000 in liquid cash—directly improving your Cash Left In metric.

Phase 3: RENT — Proving the Commercial Income

Once the refurbishment is complete, you must tenant the property and prove it generates stable rental income. This phase serves two critical functions:

Function 1: Income Verification for Refinancing

Commercial mortgage lenders will not refinance a vacant property. They require a minimum of one month's proven rental income (some lenders require three months). The rental figure must pass the lender's Interest Coverage Ratio (ICR) stress test, typically requiring the gross rent to exceed 145% of the monthly mortgage payment at a stressed interest rate of 5.5%.

Function 2: Bridging Loan Servicing

While you wait for the refinance, the rental income helps offset (or fully covers) the monthly bridging loan interest payments. If your bridge charges £850/month and your HMO generates £1,800/month, the property is self-servicing the debt, preventing the catastrophic "bridging attrition" that kills amateur investors.

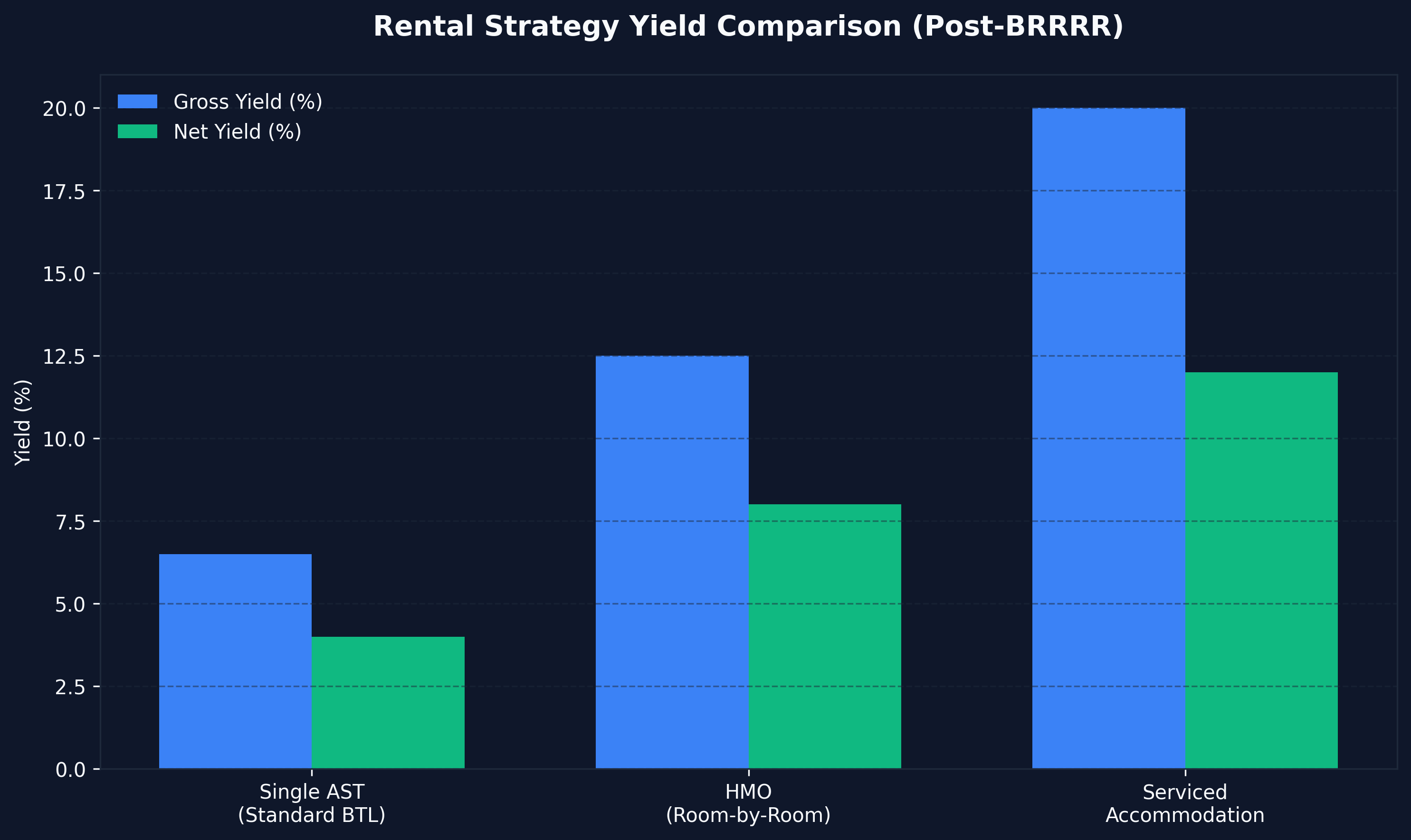

Optimal Rental Strategy

- Single AST Let: Lower yield (5-7%), simpler management, faster tenant placement.

- HMO (Room-by-Room): Higher yield (10-15%), significantly more management overhead, requires mandatory HMO licensing from the local council.

- Serviced Accommodation (SA): Highest potential yield (15-25%), but extreme operational complexity and no guaranteed occupancy.

For the BRRRR method to work mathematically, we recommend targeting a minimum 8% gross yield to comfortably pass lender stress tests and generate meaningful cash flow post-refinance.

Phase 4: REFINANCE — The Capital Extraction Engine

This is the phase that makes the entire BRRRR method revolutionary. It is the mathematical mechanism that separates this strategy from every other form of property investment.

How the Refinance Works

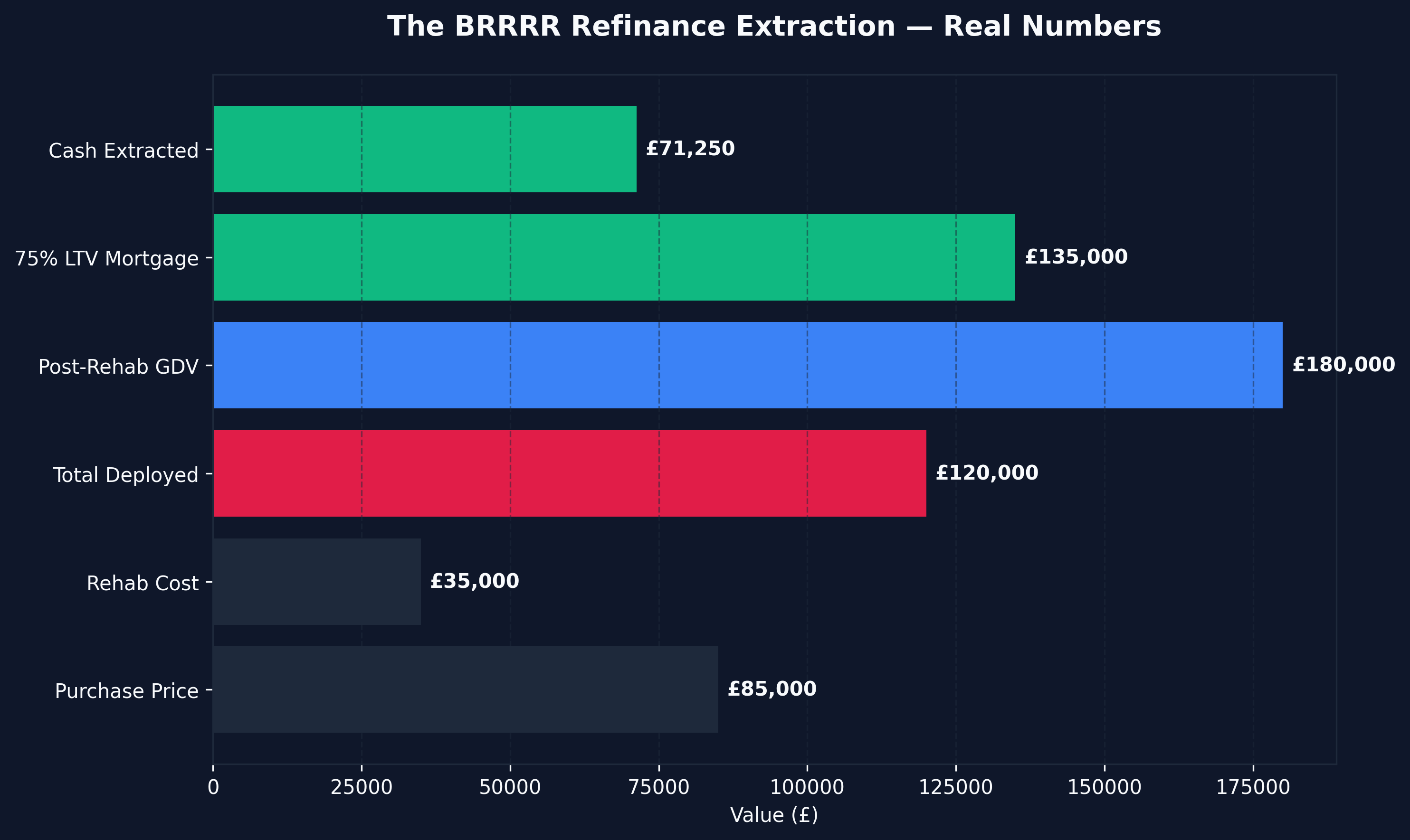

Once the property is tenanted and generating proven income, you instruct a RICS-accredited surveyor to conduct a formal commercial valuation. Because you purchased a distressed shell at £85,000 and spent £35,000 rehabilitating it into a premium rental asset, the surveyor should value the property at its true market value in renovated condition.

Example Continuation:

- Purchase Price: £85,000

- Rehab Cost: £35,000

- Total Capital Deployed: £120,000 (including fees)

- Post-Rehab RICS Valuation (GDV): £180,000

- Commercial Mortgage at 75% LTV: £135,000

You take that £135,000 commercial mortgage and use it to pay off the original £63,750 bridging loan. The remaining cash (£135,000 - £63,750 = £71,250) is wired directly back into your bank account.

The Critical "Cash Left In" (CLI) Calculation

- Total Personal Cash Deployed: £24,250 (deposit) + £35,000 (rehab) = £59,250

- Cash Extracted via Refinance: £71,250

- Net Position: +£12,000 in PROFIT, with zero of your own money left in the deal.

You now own a rental property generating £1,200/month in gross income, secured by a standard 25-year commercial mortgage, and you have extracted 100% of your initial seed capital plus an additional £12,000 in pure profit. Your Return on Capital Employed is mathematically infinite because you have zero capital remaining in the transaction.

Why is the Extracted Cash Tax-Free?

This is the question that confuses most beginners. The £71,250 you extracted is not income—it is commercial debt. You borrowed money from a bank. In the eyes of HMRC, raising a mortgage is not a taxable event. The cash is 100% tax-free, liquid capital. Understanding the complete taxes on buy rehab rent refinance repeat uk 2026 matrix is essential to executing this phase correctly.

Phase 5: REPEAT — Recycling the Capital

The final phase is the simplest to understand but the most powerful in practice. You take the £59,250+ of extracted capital and deploy it immediately into the next distressed acquisition.

Because the BRRRR method is designed to return 100% (or more) of your seed capital on each cycle, a single pot of £60,000 can theoretically acquire an unlimited number of properties over time. The compounding effect is extraordinary:

- Year 1: Execute 2 BRRRR deals. Portfolio = 2 properties, ~£2,400/month gross rent.

- Year 2: Execute 2 more deals. Portfolio = 4 properties, ~£4,800/month gross rent.

- Year 3: Execute 3 deals (using accumulated rental profit to supplement). Portfolio = 7 properties, ~£8,400/month gross rent.

Within five years, a disciplined operator starting with £60,000 can realistically build a portfolio generating £10,000+ per month in gross rental income, secured against £1,000,000+ in appreciating UK property assets. This is the raw, mathematical power of the BRRRR method.

The Critical Failure Points: Why Most People Fail

Understanding what the BRRRR method is and how it works theoretically is straightforward. Executing it successfully in the volatile 2026 UK property market is an entirely different matter.

Failure Point 1: Bridging Attrition

If your rehab drags from 12 weeks to 9 months due to contractor delays, planning issues, or supply chain failures, the bridging loan interest (£850+/month) will systematically erode your entire profit margin. For a deeper analysis of this risk, review our assessment on whether the strategy is actually worth it.

Failure Point 2: RICS Down-Valuations

If the commercial surveyor values the property below your target GDV, the bank will issue a smaller mortgage. You will not extract enough cash to cover your initial outlay, permanently trapping capital in the deal and breaking the "Repeat" cycle.

Failure Point 3: Section 24 Tax Annihilation

If you execute the BRRRR method in your personal name as a higher-rate taxpayer, Section 24 of the Finance Act bans you from deducting your mortgage interest as a business expense. HMRC will tax you on your gross rental income, frequently pushing the asset into negative cash flow. The solution is mandatory: execute via a Special Purpose Vehicle (SPV) Limited Company. A full breakdown of this is available in our taxes on BRRR property uk 2026 guide.

Failure Point 4: Insufficient Cash Reserves

Beginners frequently deploy 100% of their available capital into the first deal, leaving zero buffer for unexpected rehab costs or bridging extensions. A disciplined operator always maintains a minimum cash reserve of £10,000 to £15,000 above the projected deal costs.

The Alternative: Syndicated BRRRR Exposure

For high-earning professionals who understand the mathematical superiority of the BRRRR method but cannot dedicate the operational bandwidth required to manage refurbishments, bridging loans, and tenant placement, the solution is syndication.

By deploying capital into a real estate venture capital uk framework, you participate in the compounding returns of institutional-grade BRRRR operations. The syndicate operator handles all five phases—acquisition, rehabilitation, tenanting, refinancing, and recycling—while you receive a proportional share of the capital growth and rental yield.

Conclusion

The BRRRR method—Buy, Rehab, Rent, Refinance, Repeat—is objectively the most powerful private wealth-generation framework available in UK real estate. It mathematically permits a single investor to recycle a fixed pot of seed capital into an infinitely scalable portfolio of income-generating assets.

However, it demands absolute mastery of commercial bridging structures, forensic due diligence on distressed acquisitions, ruthless project management during the rehab phase, and a dictatorial understanding of RICS valuation parameters. It is not a passive income hobby—it is a complex, highly leveraged commercial banking operation.

If you respect the mathematics and execute with discipline, the BRRRR method will compress a forty-year retirement timeline into five years.

2026 FAQs: Understanding the BRRRR Method

Can I use the BRRRR method with no money?

Technically no. While creative financing structures exist (joint ventures, private lending), the commercial reality is you need liquid capital to fund the 25% bridging deposit and the rehab costs. A realistic entry point for a Northern England BRRRR deal in 2026 is £50,000 to £75,000 in available cash.

How long does a single BRRRR cycle take?

A well-executed cycle typically takes 6 to 9 months from acquisition to completed refinance. The fastest operators complete cycles in 4 months; delays can push this to 12+ months. The key bottleneck is always the rehab phase duration.

Is the BRRRR method legal in the UK?

Absolutely. Every phase of the strategy—purchasing distressed property, renovating it, renting it, and refinancing with a commercial mortgage—is entirely legal and commonplace. The key is ensuring your tax structure (SPV vs personal name) is correctly configured to avoid punitive Section 24 consequences.

Stop being a landlord. Start being an investor.

Shaded Canvas introduces serious capital to vetted UK property opportunities — targeting 12–16% net returns.

Start Investing →