The phrase "passive income" gets thrown around so casually in property circles that it's lost all meaning. Let's be clear from the start: property income is rarely passive. But with the right structures, the right properties, and the right team, you can build a portfolio that delivers consistent monthly cash flow with minimal weekly involvement.

This guide covers the strategies, structures, and locations that allow UK property investors to move from "I own a rental" to "I have a portfolio that funds my lifestyle."

What "Passive" Actually Means in Property

True passive income means money that arrives in your bank account without you actively working for it. By that strict definition, almost no property income is passive. There's always maintenance, tenant queries, regulatory compliance, and financial management.

What most investors actually mean when they say "passive income" is delegated income — a portfolio managed by professionals where your involvement is limited to strategic decisions and reviewing monthly statements.

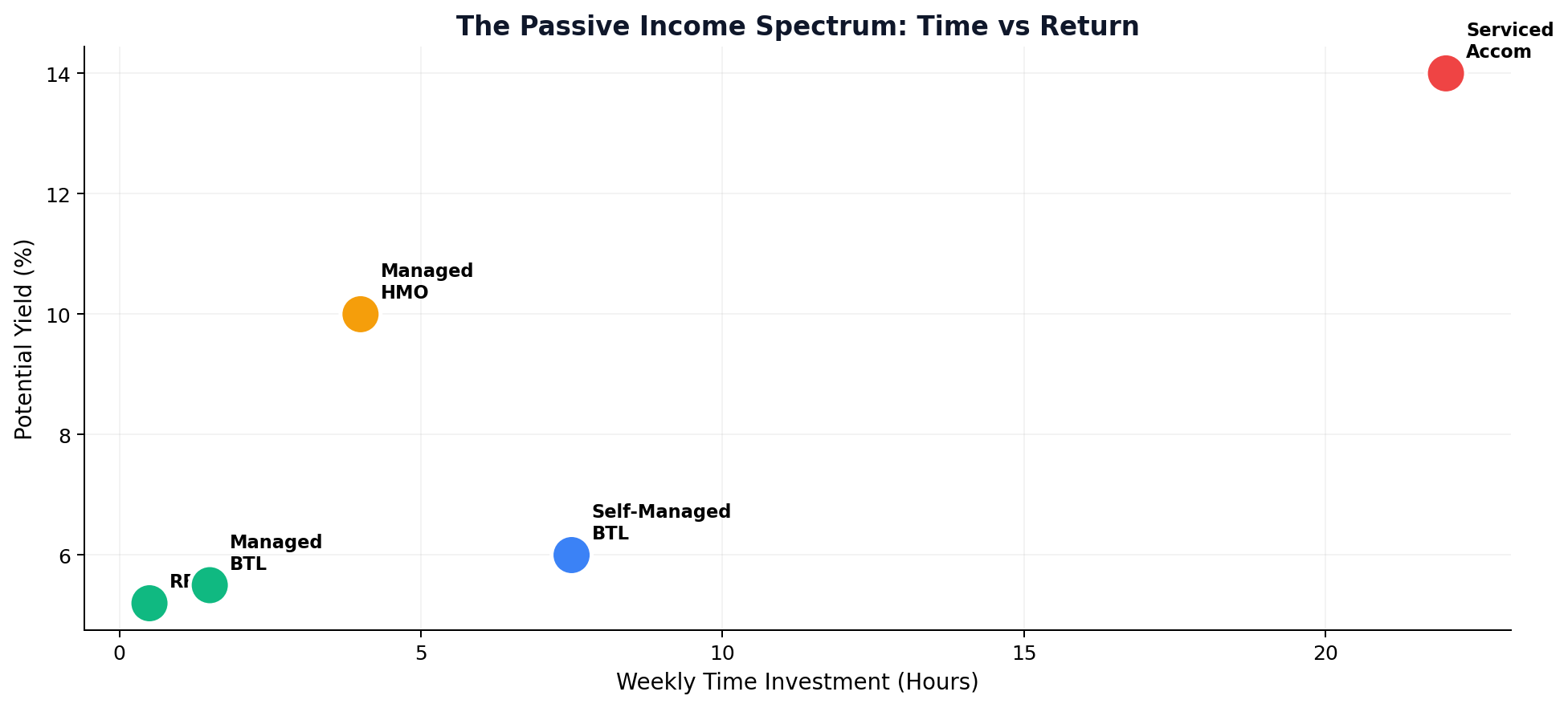

The spectrum looks like this:

| Strategy | Weekly Time Investment | Income Predictability |

|---|---|---|

| REITs (stock market) | 0 hours | High |

| Fully managed BTL | 1-2 hours | High |

| Self-managed BTL | 5-10 hours | High |

| Managed HMO | 3-5 hours | Medium-High |

| Serviced accommodation | 15-30 hours | Variable |

If you want genuinely hands-off income, you need to either invest in REITs/crowdfunding, or build a portfolio with professional management baked in from day one.

Strategy 1: Buy-to-Let with Full Management

This is the most accessible path to property-based passive income. Buy a residential property, appoint a letting agent to handle everything, and receive net rent into your account each month.

How the Numbers Work (2026 Example)

Scenario: 2-bed terrace in Liverpool, purchased for £130,000

| Item | Annual Amount |

|---|---|

| Gross rent | £8,400 (£700/month) |

| Management fee (10%) | -£840 |

| Insurance | -£300 |

| Maintenance fund (10%) | -£840 |

| Mortgage (75% LTV, 4.5%) | -£5,265 |

| Void allowance (4 weeks) | -£700 |

| Net cash flow | £455/year (£38/month) |

That's the reality most people don't talk about. On a leveraged buy-to-let in 2026, actual cash flow is often thin. The real return comes from:

- Mortgage paydown: Your tenant is repaying your debt at ~£2,400/year in principal

- Capital appreciation: At 3% growth, that's ~£3,900/year

- Total return (cash + equity): £6,755/year on a £38,500 capital investment = 17.5% total return

The cash flow isn't exciting, but the total return is.

Scaling to Meaningful Income

To generate £3,000/month in net passive income from fully managed BTL properties:

| Scenario | Properties Needed | Capital Required |

|---|---|---|

| Cash purchases (unlevered) | 8-10 | £1M-£1.3M |

| 75% LTV (leveraged) | 25-40 | £250K-£400K deposits |

| Mix of leveraged + paid off | 15-20 | £500K-£700K |

The path for most investors is: build a leveraged portfolio over 10-15 years, then gradually pay down mortgages as rental income increases and properties appreciate. The portfolio that generates £38/month per property today generates £550/month per property once the mortgage is cleared.

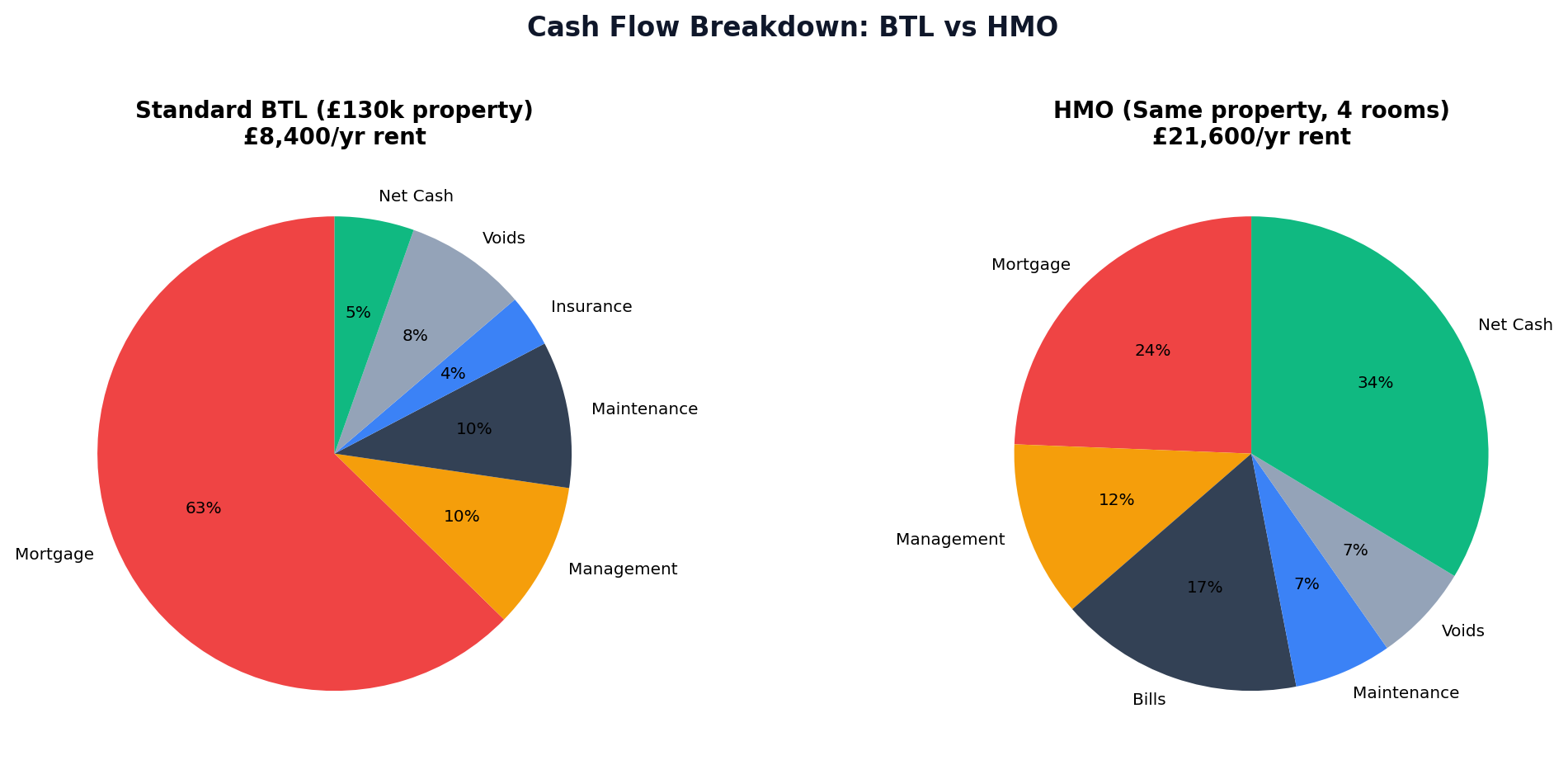

Strategy 2: HMOs — Higher Yield, Higher Involvement

HMOs (Houses in Multiple Occupation) deliver significantly higher cash flow per property than standard buy-to-let, making them attractive for investors who want to reach their income target with fewer properties.

Cash Flow Comparison

Same £130,000 terrace in Liverpool:

| Metric | BTL | HMO (4 rooms) |

|---|---|---|

| Monthly gross rent | £700 | £1,800 |

| Management (12%) | -£84 | -£216 |

| Bills (HMO landlord pays) | £0 | -£300 |

| Maintenance | -£70 | -£120 |

| Mortgage | -£439 | -£439 |

| Void/contingency | -£58 | -£120 |

| Monthly net cash flow | £49 | £605 |

The HMO generates 12x the monthly cash flow. But there are trade-offs:

- Conversion costs (£15,000-£40,000 depending on scope)

- Licensing requirements and fees

- Higher tenant turnover on individual rooms

- More intensive management requirements

- Article 4 restrictions in many areas

To hit £3,000/month with HMOs, you typically need 5-7 properties versus 25-40 for leveraged BTL.

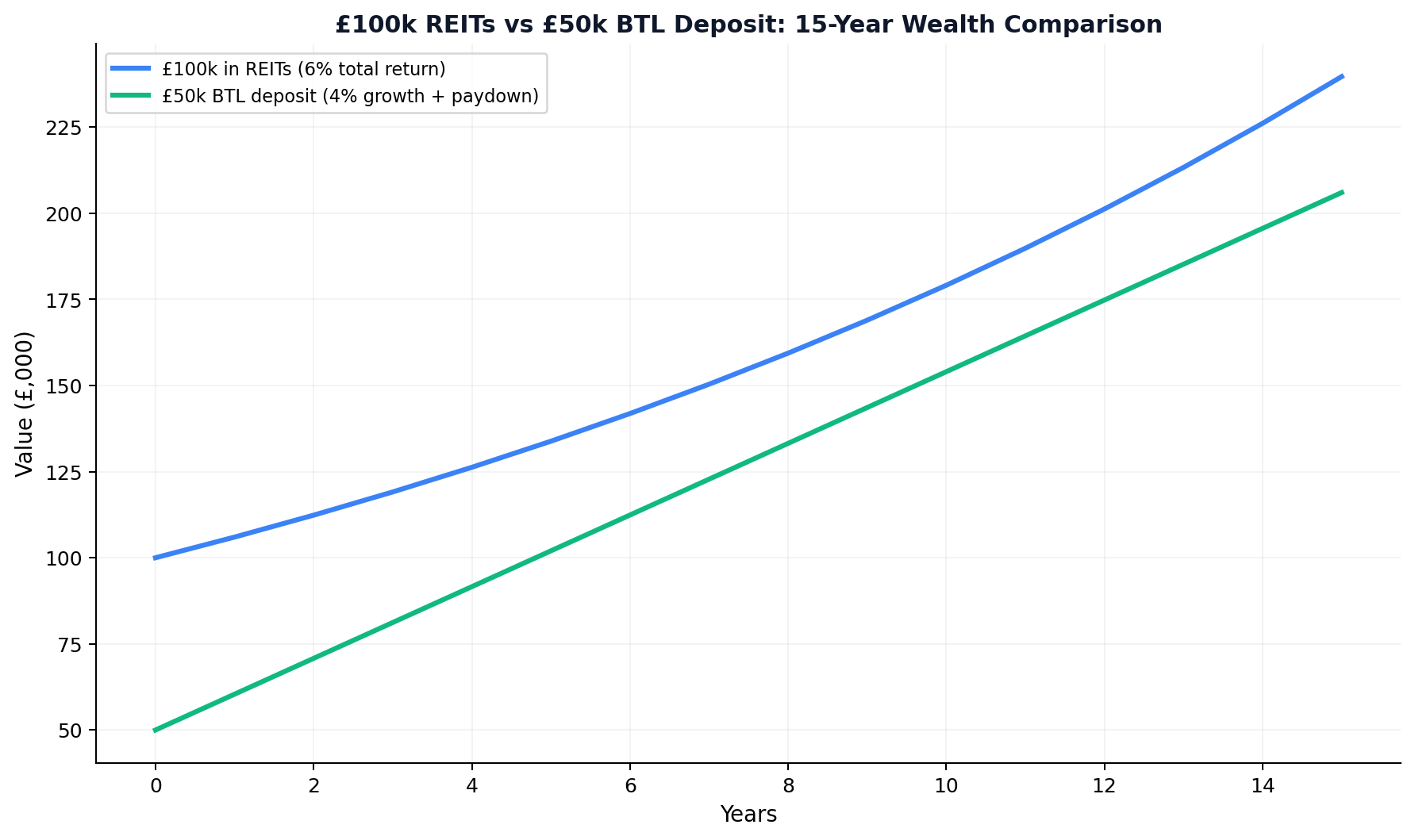

Strategy 3: REITs — No Property, No Problems

For investors who want property market exposure without the physical asset ownership, Real Estate Investment Trusts offer genuine passive income.

UK-listed REITs are legally required to distribute at least 90% of rental income as dividends. You can buy and sell shares like any stock, hold them in a tax-free ISA, and receive dividends quarterly.

Leading UK REITs (2026)

| REIT | Sector | Approx Dividend Yield |

|---|---|---|

| British Land | Diversified | 5.5% |

| Land Securities | Office/Retail | 5.8% |

| Tritax Big Box | Industrial/Logistics | 4.8% |

| UNITE Group | Student Accommodation | 3.5% |

| Primary Health Properties | Healthcare | 6.2% |

The ISA Advantage

£20,000 invested annually into a Stocks & Shares ISA holding REITs generates tax-free dividends and capital gains. Over 10 years, that's £200,000 in tax-free property exposure.

To generate £3,000/month from REITs at 5% average yield: You need approximately £720,000 invested. No mortgage, no tenant calls, no EPC upgrades. Just dividends.

The Trade-Off

No leverage. A £100,000 REIT investment gives you £100,000 of property exposure. A £100,000 deposit on buy-to-let gives you £400,000 of property exposure. In a rising market, leverage wins. But in a falling market, the REIT investor sleeps better.

Strategy 4: Property Crowdfunding

Platforms allow investors to pool capital for property purchases or development loans, with minimum investments from £100 to £5,000. You earn a share of rental income and/or capital gains.

Advantages: Very low entry point, diversification, no direct management Risks: Platform risk, illiquidity (often locked in for 3-5 years), unproven long-term track records Typical Returns: 4-8% annually

This works as a supplementary strategy rather than a primary income source.

Strategy 5: Student Accommodation (Purpose-Built)

PBSA investments — typically studio or cluster flats in university cities — offer strong occupancy rates (often 95%+) and are fully managed by specialist operators. Investors buy a unit, and the management company handles everything from marketing to maintenance.

Best Cities for Student Accommodation

- Manchester: 80,000+ students, chronic undersupply of quality accommodation

- Leeds: Rapidly growing student population, strong rental demand

- Nottingham: Two major universities, affordable entry prices

- Liverpool: Large student base, yields of 7-8% on PBSA

- Birmingham: Growing university sector, significant regeneration

The key risk is operator quality. Research the management company's track record thoroughly before committing capital.

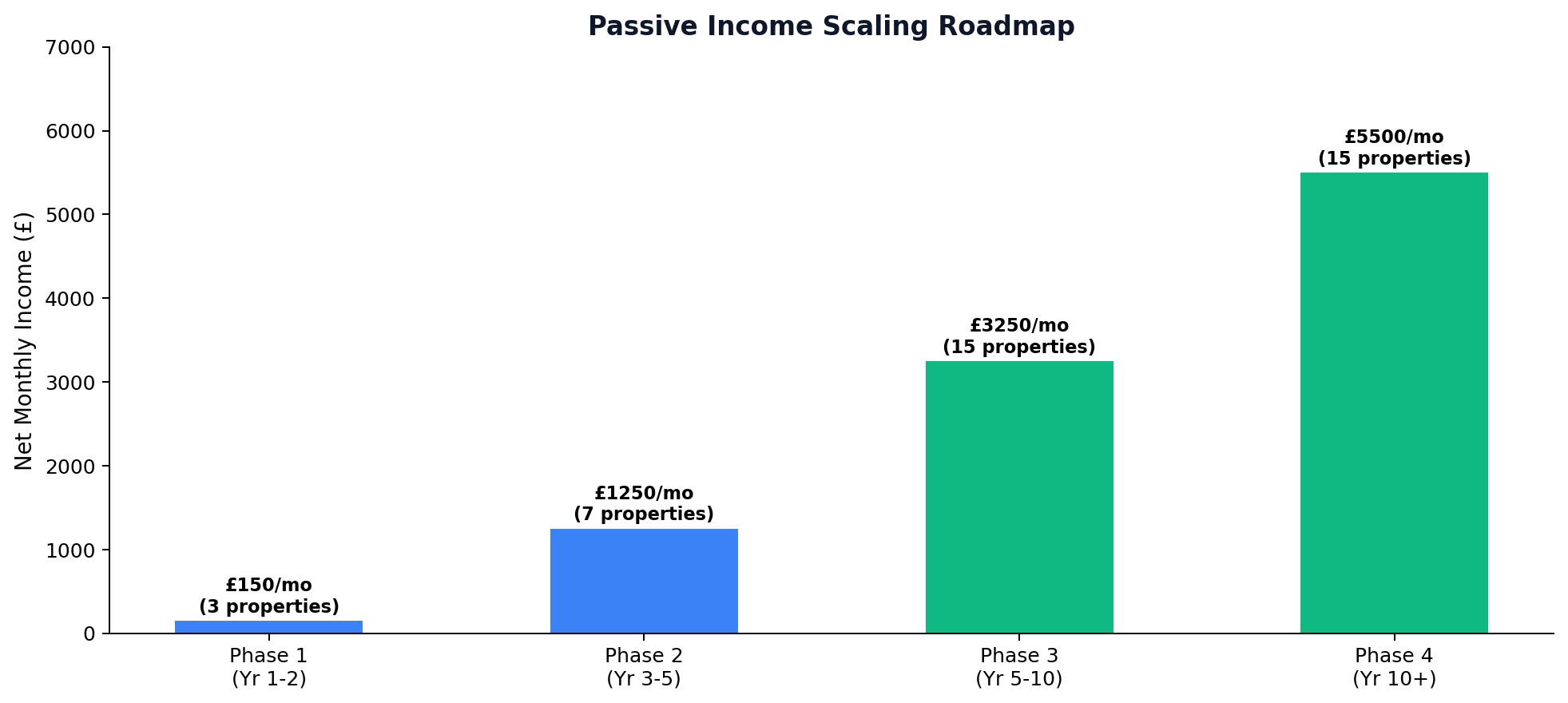

Building the Passive Income Machine: A Practical Roadmap

Phase 1: Foundation (Year 1-2)

- Purchase 2-3 standard buy-to-let properties in high-yield locations

- Appoint professional management from day one

- Focus on properties that cash flow positively from month one

- Target income: £100-£200/month net

Phase 2: Acceleration (Year 3-5)

- Add 1-2 HMOs for higher cash flow

- Remortgage existing properties to release equity for deposits

- Start building REIT position in ISA

- Target income: £1,000-£1,500/month net

Phase 3: Optimisation (Year 5-10)

- Pay down highest-rate mortgages

- Replace underperforming properties

- Diversify across locations and property types

- Target income: £2,500-£4,000/month net

Phase 4: Freedom (Year 10+)

- Majority of mortgages cleared or significantly reduced

- Cash flow from portfolio covers all living expenses

- Reinvestment optional — income now exceeds needs

- Target income: £5,000+/month net

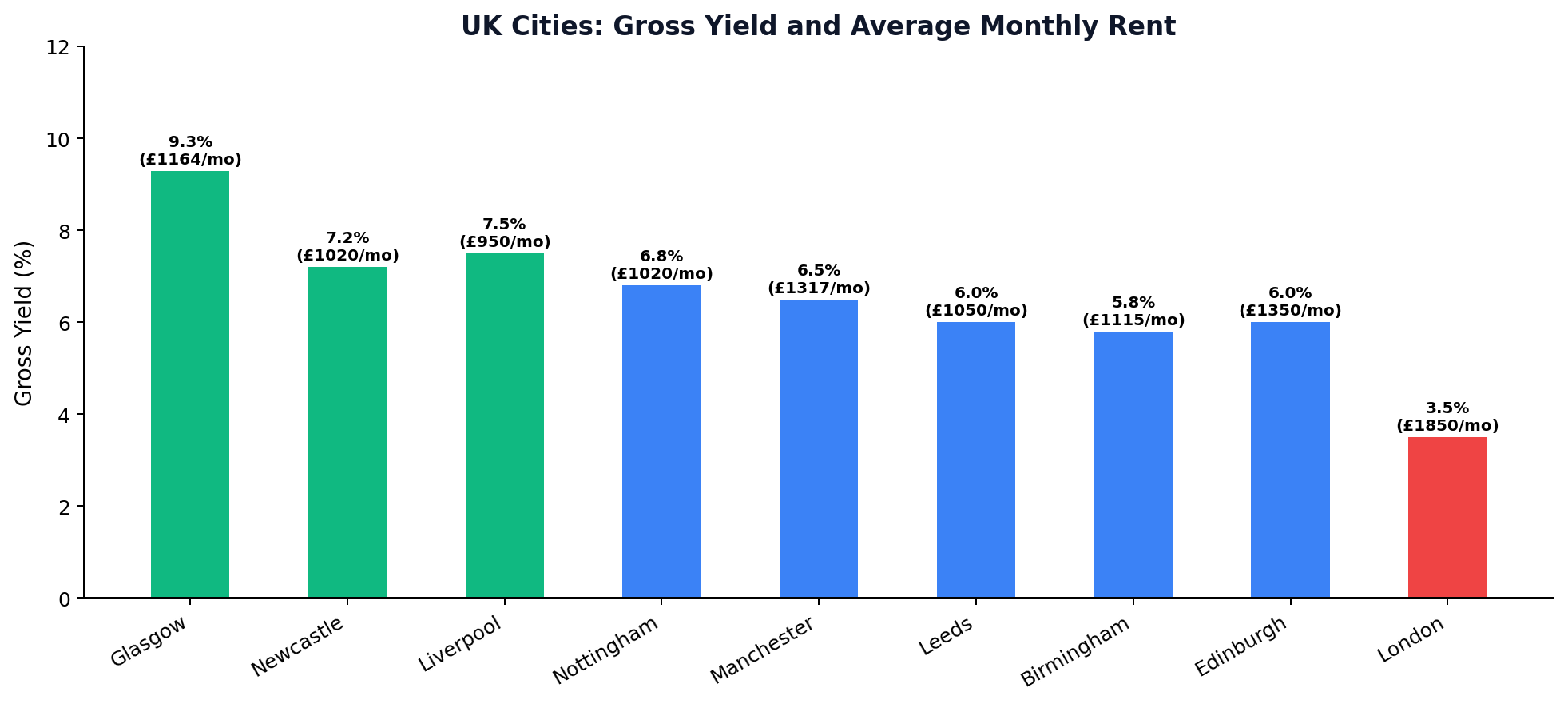

The Best Locations for Rental Income in 2026

Regional cities dominate the yield tables:

| City | Avg Gross Yield | Avg Property Price | Avg Monthly Rent |

|---|---|---|---|

| Glasgow | 9.3% | £191,000 | £1,164 |

| Liverpool | 7.5% | £165,000 | £950 |

| Manchester | 6.5% | £225,000 | £1,317 |

| Nottingham | 6.8% | £180,000 | £1,020 |

| Leeds | 6.0% | £210,000 | £1,050 |

| Birmingham | 5.8% | £230,000 | £1,115 |

| Newcastle | 7.2% | £170,000 | £1,020 |

| Edinburgh | 6.0% | £338,000 | £1,350 |

The North and Midlands consistently outperform the South for yield. London averages 3-4% gross — barely enough to cover mortgage payments, let alone generate passive income.

Tax Structures That Protect Your Income

Personal vs Limited Company

For passive income investors, the ownership structure matters enormously.

Personal ownership: Rental income is added to your salary and taxed at your marginal rate (20%, 40%, or 45%). Section 24 means you only get basic-rate tax relief on mortgage interest.

SPV (Limited company): Corporation tax at 25%. Full mortgage interest deduction. Profits retained in the company are taxed once. Profits extracted via salary/dividends are taxed again.

The Rule of Thumb: If you're a higher-rate taxpayer AND building a portfolio, SPV ownership is almost always more efficient. If you're a basic-rate taxpayer with 1-2 properties, personal ownership may still work.

Making Tax Digital (April 2026)

From April 2026, landlords earning over £50,000 from property must:

- Maintain digital accounting records

- File quarterly updates to HMRC

- Submit a final declaration annually

This doesn't change your tax liability, but it changes your admin requirements. Use cloud accounting software (Xero, QuickBooks, FreeAgent) from day one.

The Passive Income Reality Check

Let's be honest about what property income looks like in practice:

What Instagram shows: "£5,000/month passive income from my property portfolio 🏠💰"

What reality looks like: A carefully built portfolio of 10-15 properties, accumulated over 8-12 years, with professional management costing 10-12% of rent, ongoing maintenance budgets, occasional void periods, regulatory compliance costs, and accountancy fees. Net income of £3,000-£5,000/month after all costs — but only after significant time and capital investment.

That's still an excellent outcome. A property portfolio generating £3,000-£5,000/month in net income represents genuine financial security. It's just not the "buy one flat and retire" fantasy that social media promotes.

FAQ: Passive Income Property UK

How much money do I need to start earning passive income from property? A minimum of £30,000-£40,000 covers a 25% deposit plus purchase costs on a £120,000-£150,000 buy-to-let in a northern city. This generates approximately £50-£200/month in net income (leveraged).

What's the best property investment for passive income? Fully managed buy-to-let in high-yield cities (Glasgow, Liverpool, Manchester) offers the best balance of income, simplicity, and scalability. HMOs offer higher per-property cash flow but require more involvement.

Can I make £3,000 a month from property? Yes. Typically requires 5-7 HMOs or 15-20 paid-off BTL properties or a combination. Most investors reach this level after 8-15 years of consistent portfolio building.

Are REITs better than buy-to-let for passive income? REITs are genuinely passive but lack leverage benefits. They're ideal for ISA-based investing alongside physical property. Many experienced investors use both.

Is rental income taxed in the UK? Yes. Rental income is subject to income tax (personal) or corporation tax (limited company). Within an ISA, REIT dividends are tax-free.

📚 Related Reading

- How to Make £3,000 in Passive Income Every Month

- Property Equity Investors UK: The Hard Truth

- How to Reduce Taxes Legally in the UK

- Low-Risk Investments That Actually Work

- Part-Time Retirement: Take a Year Off Every 5 Years

📚 Related Reading

- Best Capital Growth Property UK: Where Property Prices Are Actually Heading in 2026 and Beyond

- Property Investments Manchester: The Definitive Investor's Guide to the UK's Most Dynamic City in 2026

- Off Plan Property for Sale UK: The 2026 Investor's Playbook

- Buy dirt

- Hobbies That Make Money: Real "Cheat Codes" for Turning Your Passion Into Profit

Stop being a landlord. Start being an investor.

Shaded Canvas introduces serious capital to vetted UK property opportunities — targeting 12–16% net returns.

Start Investing →