How to Build a UK Property Portfolio in 2026: Strategy & Financing

Owning one buy-to-let is a hobby. Owning a valid Property Portfolio is a business. The goal is not just "more houses." The goal is the Snowball Effect: where the income from your existing assets pays for the next one.

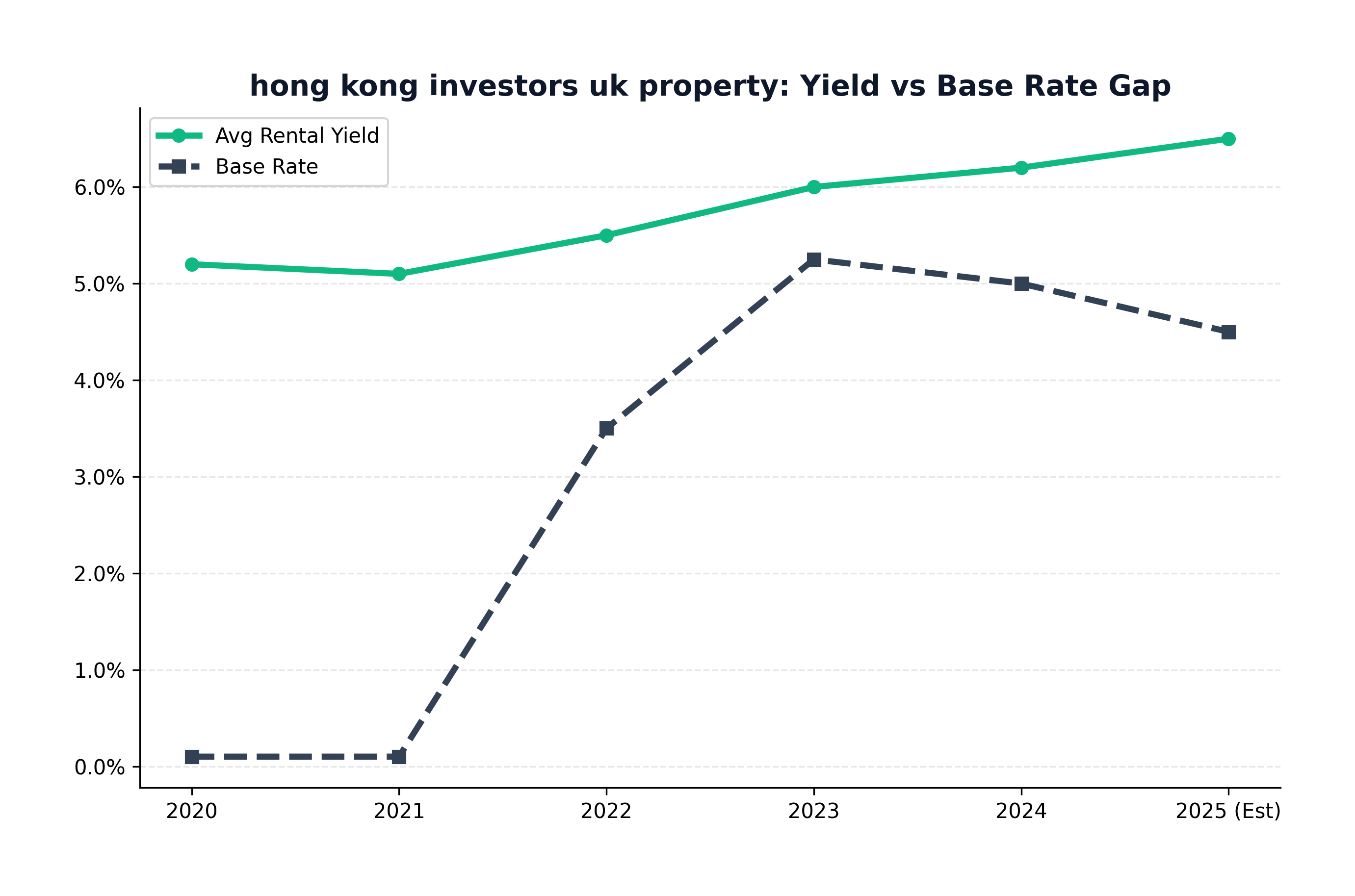

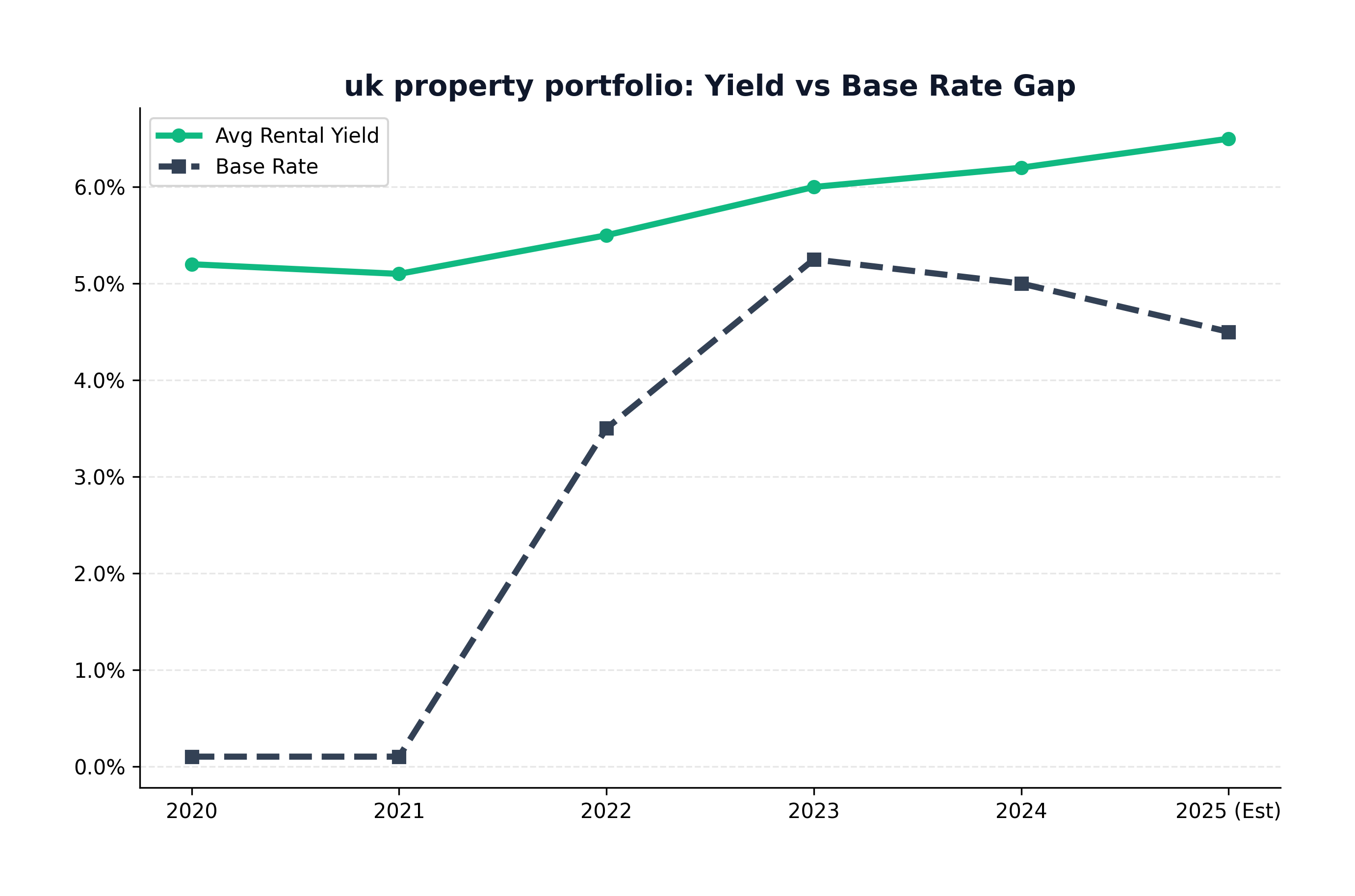

In 2026, high interest rates (sticking around 4-5%) mean you cannot just "buy and hope." You need a mathematical strategy. Here is the blueprint.

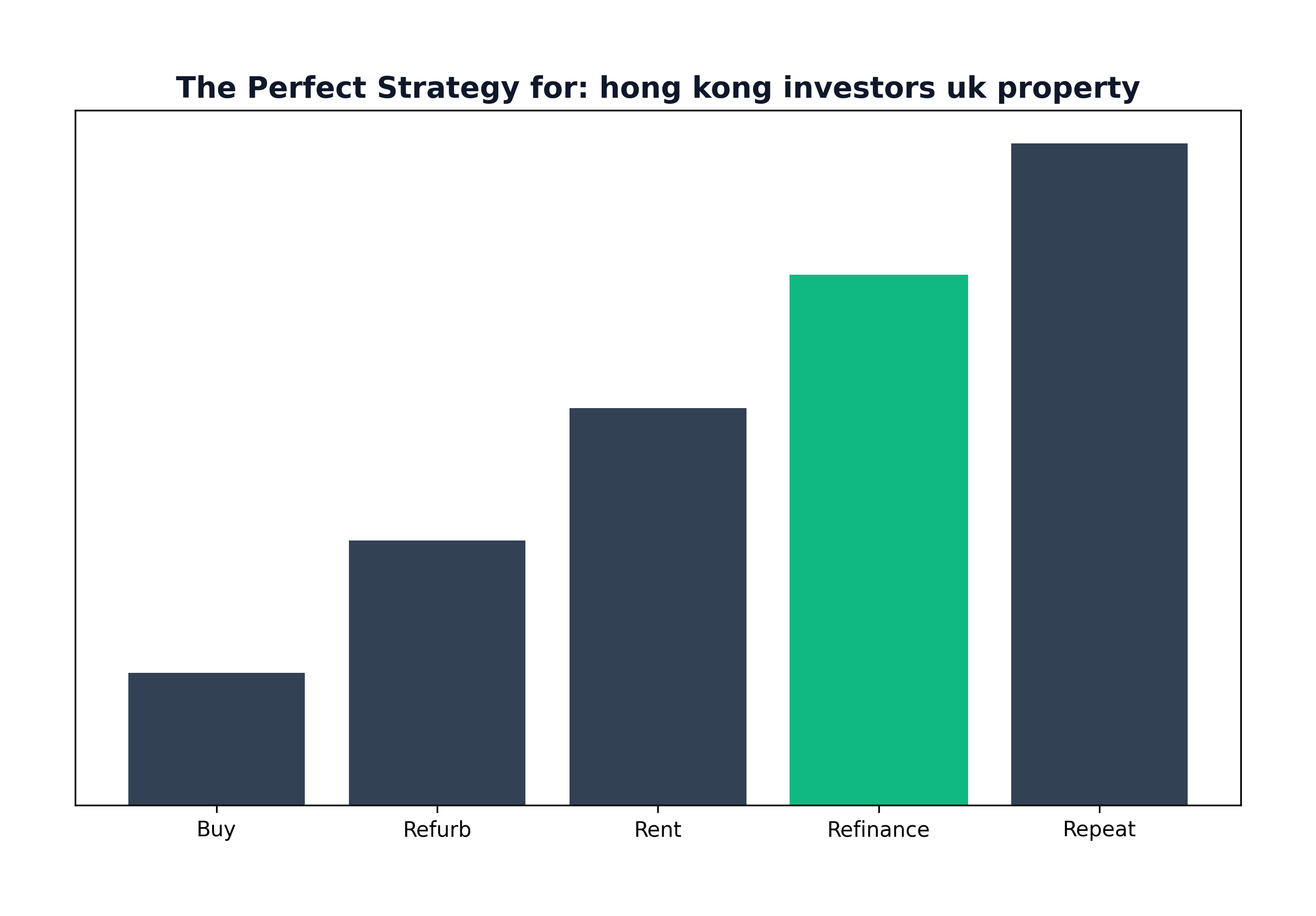

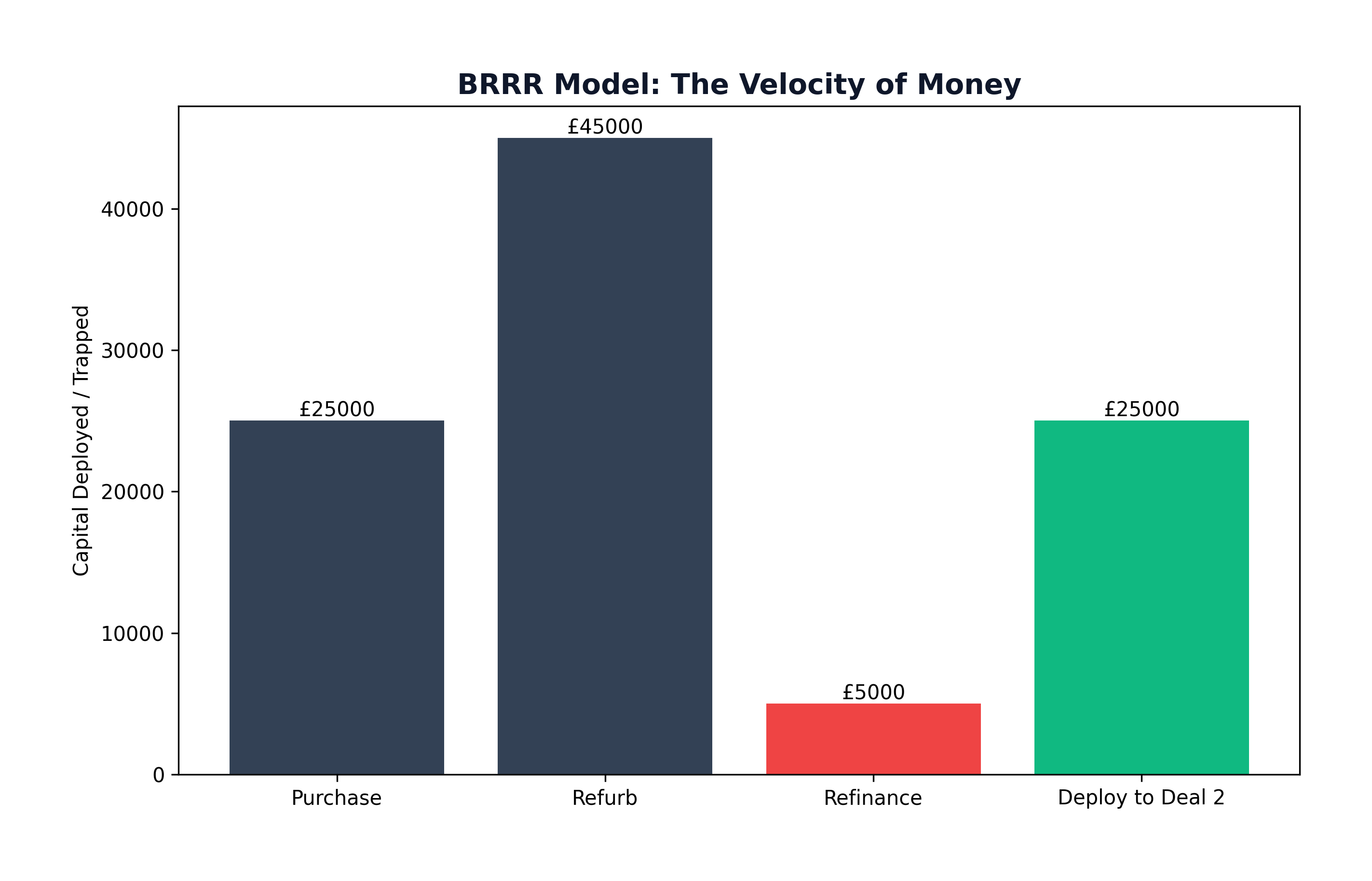

1. The Strategy: BRR (Buy, Refurbish, Refinance)

The fastest way to scale is BRR.

- Buy: A run-down property below market value (e.g., £100k).

- Refurbish: Add value (spend £20k, new value = £150k).

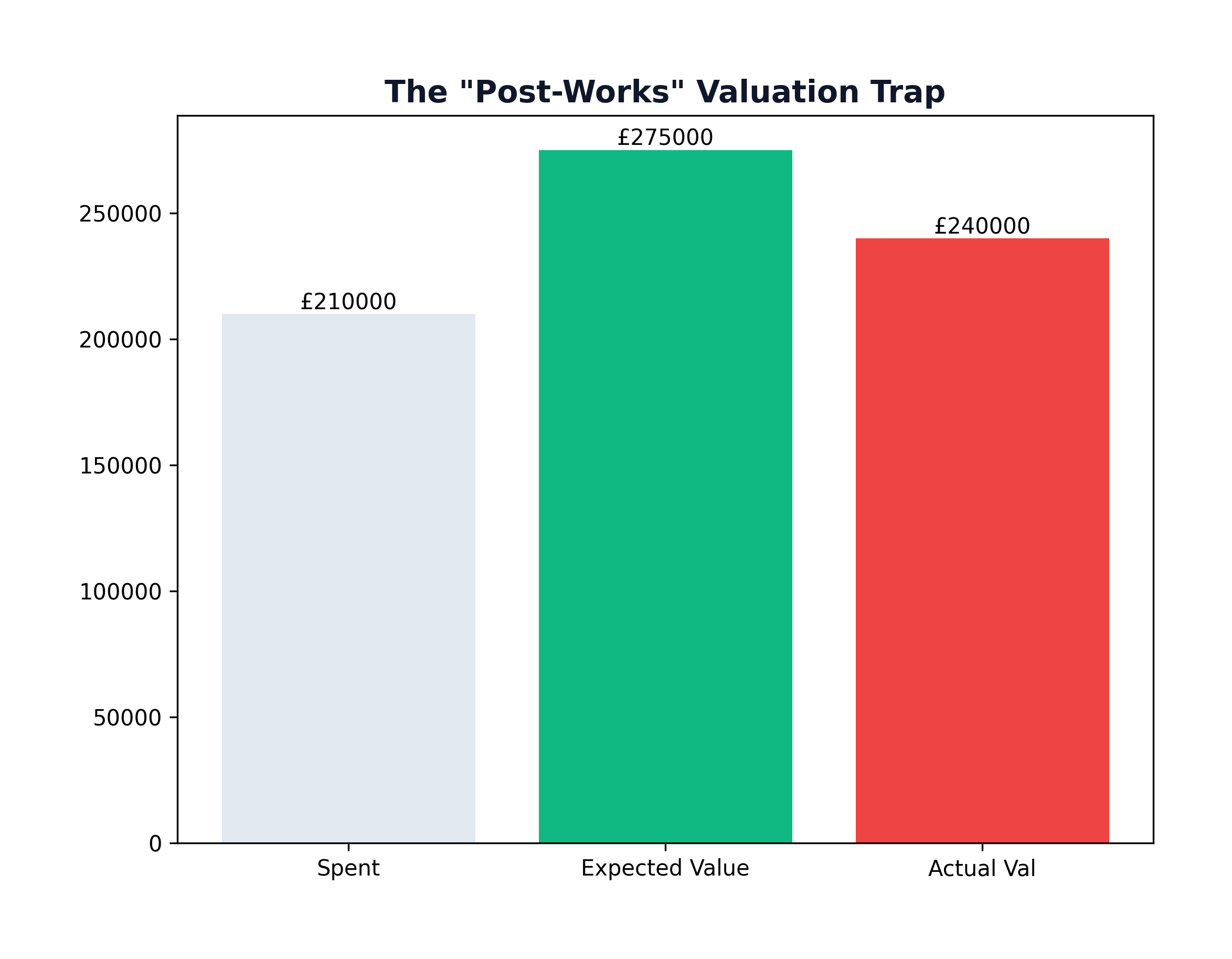

- Refinance: Pull your money out. A 75% mortgage on £150k releases £112.5k. You pay back your initial costs and have your deposit ready for Property #2.

2026 Update: Banks are stricter on valuations. Ensure your "added value" is real (e.g., adding a bedroom), not just cosmetic.

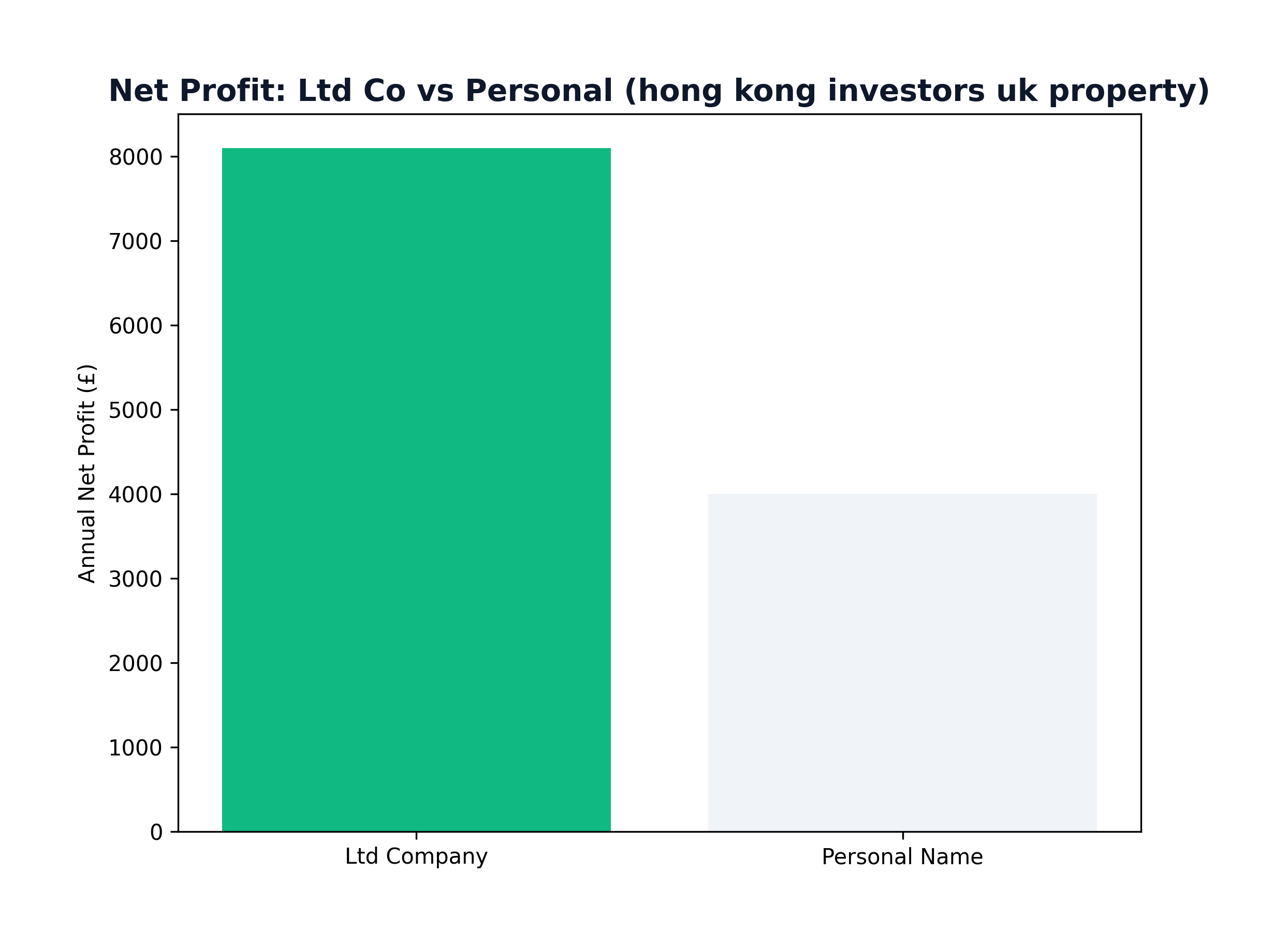

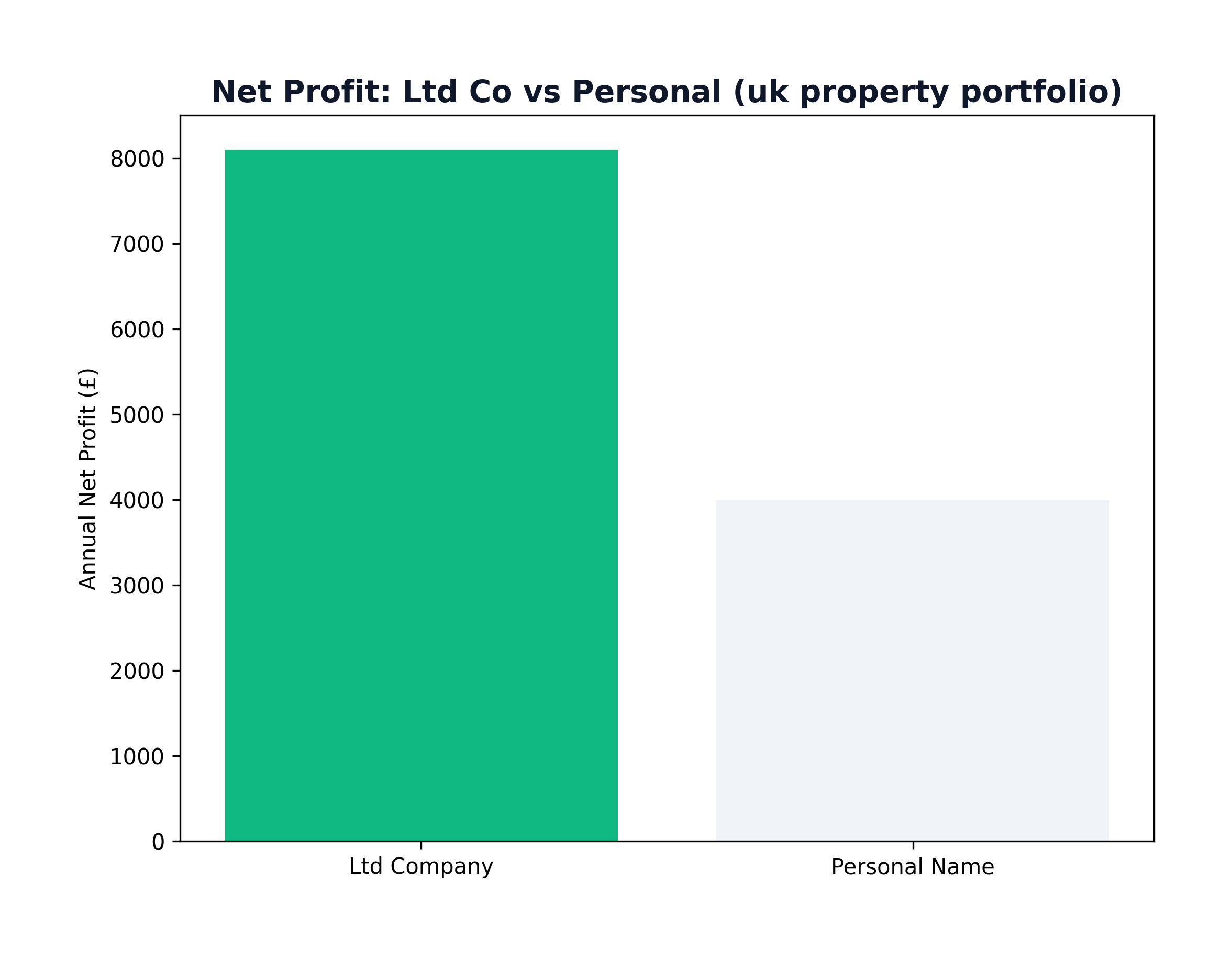

2. The Structure: Limited Company (SPV)

If you are a higher-rate taxpayer, buying in your personal name is financial suicide due to Section 24.

- Personal Name: You are taxed on revenue (before mortgage interest).

- Limited Company: You are taxed on profit (after mortgage interest). Corporation tax is 19-25%, which is far lower than 40-45% income tax.

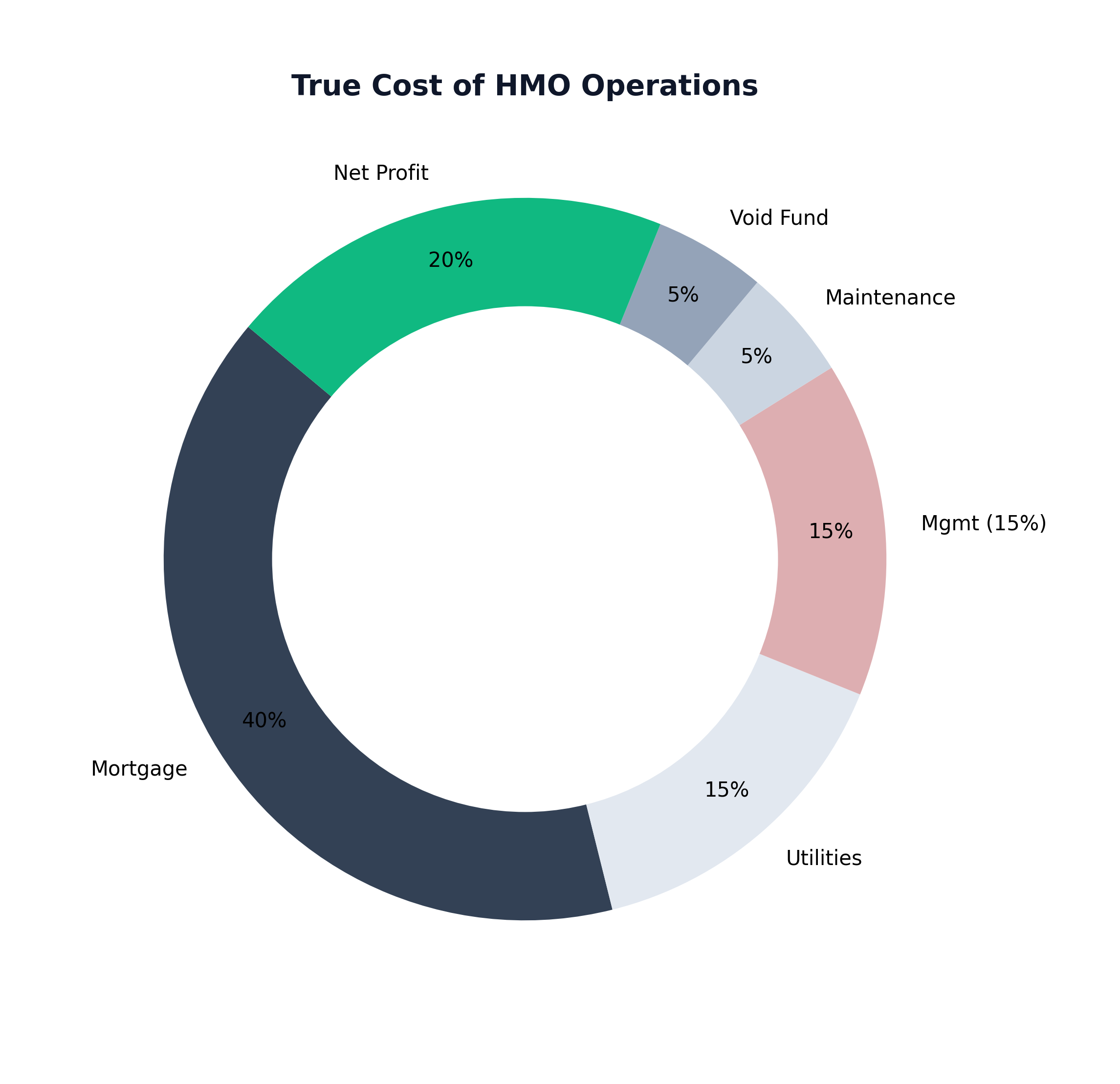

3. The Balance: Yield vs. Capital Growth

A healthy portfolio needs two engines:

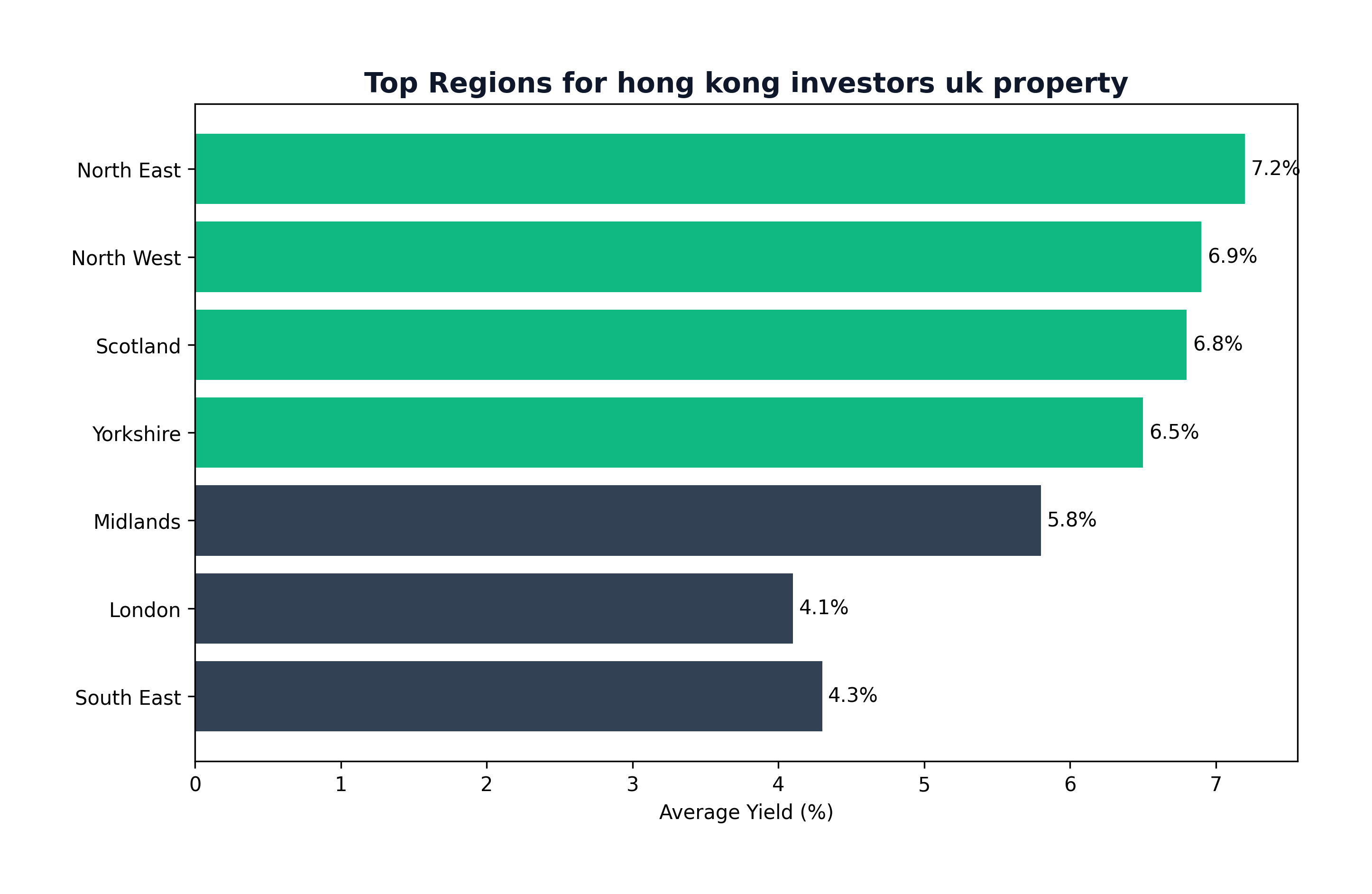

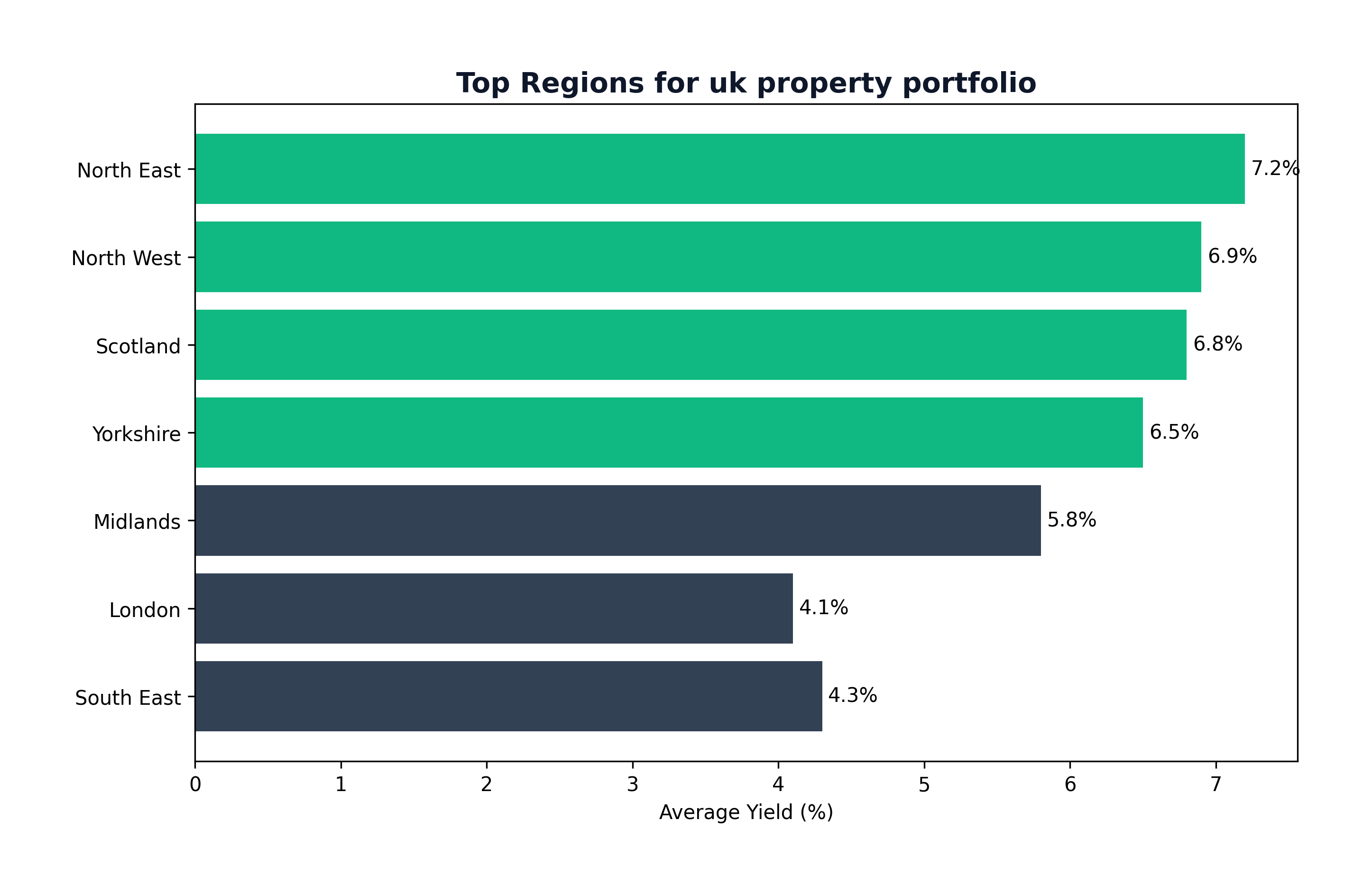

- The Engine (Yield): Properties in the North (Liverpool, Leeds, Hull). These generate monthly cash flow to pay bills and save for deposits.

- The Rocket (Growth): Properties in the South (London, Bristol). These cost money to hold (low yield) but double in value every 10-15 years. Rule: Use the Engine to pay for the Rocket.

4. Financing: Portfolio Mortgages

Once you hit 4+ properties, lenders view you as a "Portfolio Landlord."

- Pros: You can get a single "Portfolio Mortgage" covering all your assets. One monthly payment, less admin.

- Cons: If one property value crashes, it can drag down the LTV of the whole group.

conclusion: The First 10 Years

Building a portfolio is not a get-rich-quick scheme. It is a get-rich-slow scheme.

- Year 1-3: The "Grind." You are saving deposits from your job.

- Year 4-7: The "Snowball." Property income starts funding new deposits.

- Year 8+: The "Compound." Capital growth allows you to refinance heavily and scale rapidly.

Actionable Checklist:

- Incorporate a Special Purpose Vehicle (SPV) Limited Company.

- save your first £30k-£40k deposit.

- Identify a "Goldilocks" area: High demand, low entry price (e.g., M14 in Manchester).

📚 Related Reading

- Buy dirt

- Property Equity Investors UK: The Hard Truth About Building Wealth Through Bricks in 2026

- Highest Yielding Property UK: Top Hotspots for 2026

- Hobbies That Make Money: Real "Cheat Codes" for Turning Your Passion Into Profit

- Property Investments Manchester: The Definitive Investor's Guide to the UK's Most Dynamic City in 2026

Stop being a landlord. Start being an investor.

Shaded Canvas introduces serious capital to vetted UK property opportunities — targeting 12–16% net returns.

Start Investing →