The UK property market has long been the default wealth-building vehicle for British investors. But in February 2026, the landscape looks fundamentally different from the one your parents navigated. Base rates have shifted, Section 24 has fully bitten, and the Renters Reform Bill is reshaping what it means to actually own a rental property.

This is not another "10 Tips for Buy-to-Let Success" listicle. This is a data-driven analysis of how property equity investment actually works in the current regulatory and financial climate — who is deploying capital, where the numbers stack up, and where the market is quietly punishing the unprepared.

What Is Property Equity and Why Does It Matter?

Property equity is deceptively simple in definition but profoundly misunderstood in practice. At its core, it is the difference between a property's current market value and any outstanding mortgage or secured debt against it. A £300,000 property with a £200,000 mortgage carries £100,000 in equity.

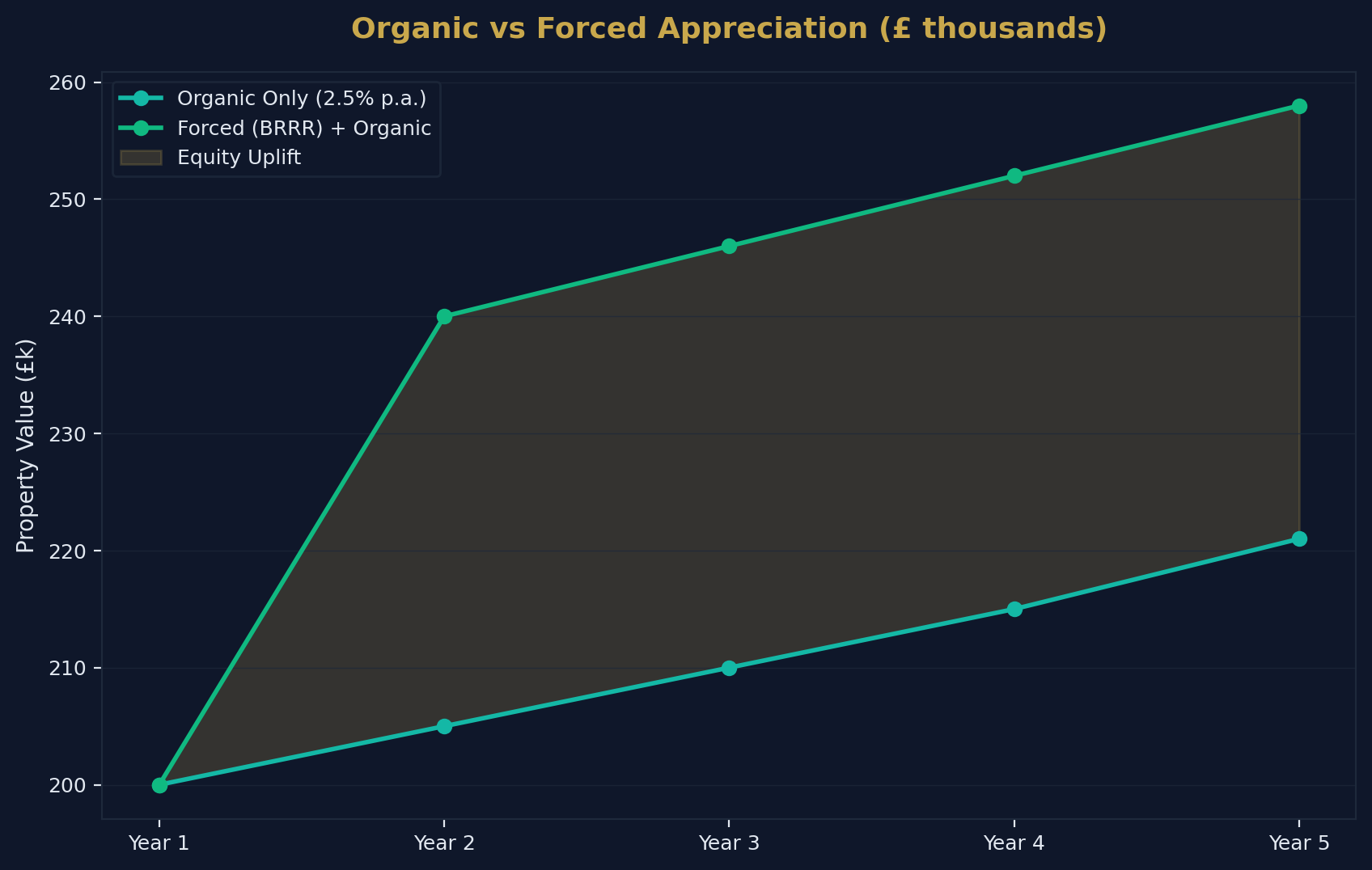

Organic Growth vs Forced Appreciation

Equity grows through two mechanisms. Organic appreciation relies on market forces — house price inflation, regional demand, infrastructure investment. The Office for National Statistics reported UK average house prices grew by approximately 2.4% year-on-year through late 2026, with forecasts for 2026 sitting between 2% and 3.5% depending on the source.

Forced appreciation, by contrast, is investor-driven. Purchase a property below market value, refurbish it to a higher standard, and the uplift in value creates equity that would have taken years of organic growth to achieve. This is the foundation of the BRRR strategy (Buy, Refurbish, Refinance, Rent) — though as we will explore later, the mechanics of this approach have changed materially. BRRR is just one of several viable property investment strategies in the UK, and choosing the wrong one for your capital base is an expensive mistake.

Paper Equity vs Realisable Equity

A critical distinction that separates experienced investors from beginners: paper equity is not the same as realisable equity. Your property may have £150,000 of equity on a desktop valuation, but your lender will only allow you to draw down to a maximum Loan-to-Value ratio — typically 75% for residential and 65-70% for commercial. Early repayment charges, valuation fees, and remortgaging costs further erode the usable figure.

Understanding this gap is essential before building any portfolio scaling strategy around equity extraction.

The Investor Landscape: Who Is Actually Deploying Capital?

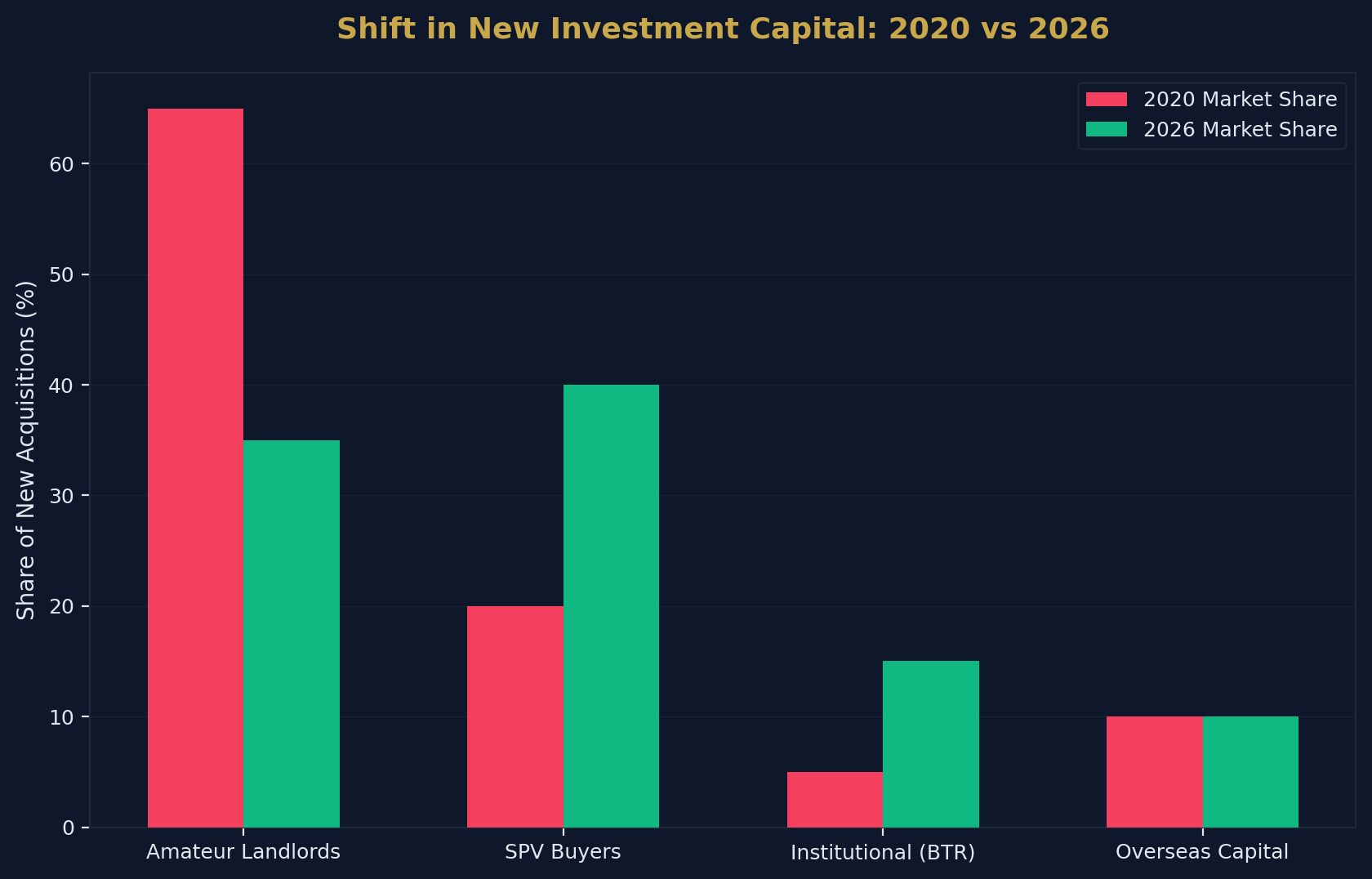

The composition of UK property equity investors has undergone a structural shift over the past five years.

The Shrinking Individual Landlord

The amateur landlord — the person who bought a second property in 2005 and has ridden the wave — is a declining species. HMRC data shows the number of individual landlords reporting rental income has plateaued since 2020, with a notable cohort exiting entirely. The reasons are well-documented: Section 24 tax changes, increased compliance costs, the looming abolition of Section 21 evictions, and the sheer administrative burden of modern tenancy management.

The Rise of the SPV Buyer

Filling that gap is the Special Purpose Vehicle (SPV) — a limited company established specifically for property investment. SPV purchases have grown consistently, with some mortgage brokers reporting that over 60% of new buy-to-let applications now come through limited company structures. The tax arithmetic is compelling for higher-rate taxpayers, though the operational reality is more nuanced (more on this in the SPV section below).

Institutional Capital: Build to Rent

The most significant shift is institutional. Build to Rent (BTR) investment reached record levels in 2026, with pension funds, insurance companies, and private equity firms pouring capital into purpose-built rental blocks. Firms like M&G Real Estate, Legal & General, and Harwood Capital are now competing directly with individual investors for tenant demand — and they bring professional management, economies of scale, and patient capital that small landlords simply cannot match.

Overseas and Diaspora Capital

International investors continue to view UK property as a safe haven, particularly buyers from the Middle East and East Asia. Sterling's relative weakness post-Brexit has made London assets particularly attractive on a purchasing power parity basis, though increasingly this capital is flowing into Manchester, Birmingham, and Leeds where yields are substantially higher. Hong Kong investors buying UK property now represent the single largest group of overseas owners, with BNO visa holders driving a wave of SPV-structured acquisitions in northern cities.

REITs and Listed Property

For investors who want exposure without direct ownership, Real Estate Investment Trusts (REITs) offer a liquid alternative. TR Property Investment Trust, a FTSE 250 constituent, provides diversified exposure across UK and European commercial property. The dividend yields — typically 3-5% — are modest compared to direct ownership, but the absence of management hassle, void risk, and leverage exposure makes this a genuine alternative for equity investors who value their time.

Equity Extraction Strategies: Remortgaging, BRRR, and the Velocity Problem

The engine of portfolio growth for most property equity investors is equity recycling — extracting built-up equity from existing properties to fund new acquisitions.

Standard Remortgaging

The most straightforward approach. If your property has appreciated in value and your current mortgage is below 75% LTV, you can remortgage to release the difference. On a property now valued at £350,000 with an outstanding mortgage of £200,000, a remortgage to 75% LTV would release £62,500 in cash — enough for a deposit on another mid-market property in the North of England.

The BRRR Cycle in 2026

BRRR remains the most talked-about strategy in UK property investment circles. The cycle works as follows:

- Buy a property below market value (typically at auction or off-market)

- Refurbish to increase value and rental potential

- Refinance at the new, higher valuation to pull your capital back out

- Rent the property, generating cash flow while your original deposit is recycled into the next deal

The theory is elegant. The 2026 reality is harder. Lenders are increasingly conservative on post-refurbishment valuations, with multiple Reddit investors reporting that surveyors are down-valuing properties by 10-15% relative to comparable sales data. The consequence is that investors cannot extract their full deposit, slowing the "velocity" of capital recycling that makes BRRR attractive.

One property investor on Reddit captured it bluntly: "The velocity of money has slowed down significantly. You're leaving £15-20k stuck in every deal now."

Cross-Collateralisation Risk

Investors with multiple properties secured against each other face an additional hazard. If total loan values exceed combined property values during a downturn, the entire portfolio can enter negative equity simultaneously — even if individual properties would have been fine in isolation. This is a risk that sophisticated investors manage through deliberate separation of security, but many portfolio landlords stumble into it through convenience.

Equity Release for Over-55s

A distinct category. Equity release products (lifetime mortgages and home reversion plans) allow older homeowners to access their property wealth. However, the compound interest trap is severe — at 6% interest, a £100,000 lifetime mortgage doubles to £200,000 in just 12 years. As an investment strategy, releasing equity from your home to fund rental purchases only works if the rental yield significantly exceeds the equity release interest rate, which in the current market is a narrow margin indeed.

The SPV Question: Limited Company vs Personal Ownership

This is arguably the most debated topic in UK property investment, and the answer is less clear-cut than most YouTube gurus suggest.

The Tax Case for SPV

Since Section 24 fully removed mortgage interest relief for individual landlords (phased in from 2017, complete since April 2020), higher-rate taxpayers face a punishing effective tax rate on rental income. A landlord earning £50,000 in rental income with £30,000 in mortgage interest now pays tax on the full £50,000, receiving only a 20% basic-rate tax credit on the interest. For a 40% taxpayer, this is devastating — and while SPVs are the most common fix, they are not the only way to reduce taxes legally in the UK as a property investor.

A limited company, by contrast, deducts mortgage interest as a legitimate business expense before calculating Corporation Tax at 25% (since April 2023 for profits over £250,000; 19% for profits under £50,000, with marginal relief in between).

The Operational Reality

What the tax-saving projections rarely account for:

- SPV mortgage rates are typically 0.5-1% higher than equivalent personal buy-to-let rates

- Annual accounts and Corporation Tax returns cost £800-£1,500 per year through an accountant

- Extracting profits from the company triggers additional tax — either through dividends (taxed at your marginal rate) or salary (subject to NI)

- Director's loan accounts are complex and HMRC-scrutinised

- Mortgage product availability is narrower — fewer lenders, fewer product transfers

As one Reddit contributor in r/FIREUK noted: "The tax saving only kicks in for higher rate taxpayers with 4+ properties. For a single property investor, it's often more expensive."

| Metric | Limited Company (SPV) | Personal Ownership |

|---|---|---|

| Tax Rate on Profits | 19-25% (Corp Tax) | 20-45% (Income Tax) |

| Mortgage Interest Relief | Full deduction | 20% basic-rate credit only |

| Typical Mortgage Rate | 5.5-6.5% | 5.0-5.8% |

| Annual Compliance Cost | £800-£1,500 | £200-£400 |

| Profit Extraction | Dividend tax applies | Direct income |

| Best For | 40%+ taxpayers, 4+ properties | Basic-rate taxpayers, 1-3 properties |

Regional Equity Hotspots: Where the Numbers Actually Work

Not all property equity is created equal. Regional variations in yield, capital growth, and entry price create fundamentally different risk-return profiles.

The Northern Powerhouse

Liverpool continues to offer some of the highest gross rental yields in England at 6.5-7.5%, with average property prices still below £180,000 in many investment postcodes. Manchester commands slightly higher prices but benefits from population growth, corporate relocations, and a £1 billion+ city centre pipeline. Leeds has emerged as the quiet performer, with yields around 6-6.5% and strong tenant demand driven by the financial services and digital sectors.

The Midlands Corridor

Birmingham remains the standout, propelled by HS2 infrastructure investment (despite delays), the Commonwealth Games legacy, and a young, growing population. Average yields sit around 5.5-6%, with specific postcodes in Digbeth and the Jewellery Quarter outperforming.

London: A Different Game

London yields are structurally lower — 3-4% gross in most boroughs — making it a capital growth play rather than a cash flow strategy. The maths only works for equity investors with substantial deposits who are betting on long-term appreciation. Nedbank Private Wealth noted London is anticipated to outperform other regions for the first time since 2015, but this is a game for patient capital.

Scotland and Wales

Motherwell in Scotland is predicted to see above-average price growth, driven by affordability relative to Glasgow. Welsh rental demand is strengthening in Cardiff and Swansea, though regulatory differences (Wales has its own Renting Homes Act) add complexity.

Property Equity vs Global Equities: The Uncomfortable Comparison

This is the conversation that most property investment content deliberately avoids.

The Performance Gap

A widely-cited analysis on r/UKPersonalFinance calculated that global equities (VWRL) outperformed UK property by approximately 30% over 2016-2024. Even accounting for leverage (a typical property investor uses 75% LTV, effectively a 4:1 leverage ratio), the risk-adjusted returns of a diversified equity portfolio held in a tax-sheltered ISA wrapper were superior for most investors.

When Property Wins

Property equity investment does outperform in specific scenarios:

- Forced appreciation through BRRR or development generates returns that passive index funds cannot replicate

- Leverage amplifies returns in a rising market — a 5% house price increase on a 75% LTV property delivers a 20% return on equity

- Rental income provides cash flow that can service the debt, making property genuinely self-financing — a form of real estate passive income that equity dividends rarely replicate

- Tax efficiency through SPVs can create net returns that exceed post-tax equity portfolio returns for higher-rate taxpayers

When It Doesn't

- After accounting for management fees, void periods, maintenance, insurance, and compliance costs, net rental yields are typically 2-3% lower than gross yields

- Property is illiquid — selling takes 3-6 months versus clicking "sell" on a brokerage platform

- Concentration risk is extreme — a single property in a single postcode is the antithesis of diversification

- The hassle premium is real. As one Reddit user put it: "'Passive income' is a myth unless you pay a fully managed agent 12%+ VAT"

The honest answer is that neither asset class is universally superior. The right choice depends on your tax position, risk tolerance, time availability, and whether you genuinely enjoy property management or simply endure it.

Regulatory Headwinds: The Renters Reform Bill and Beyond

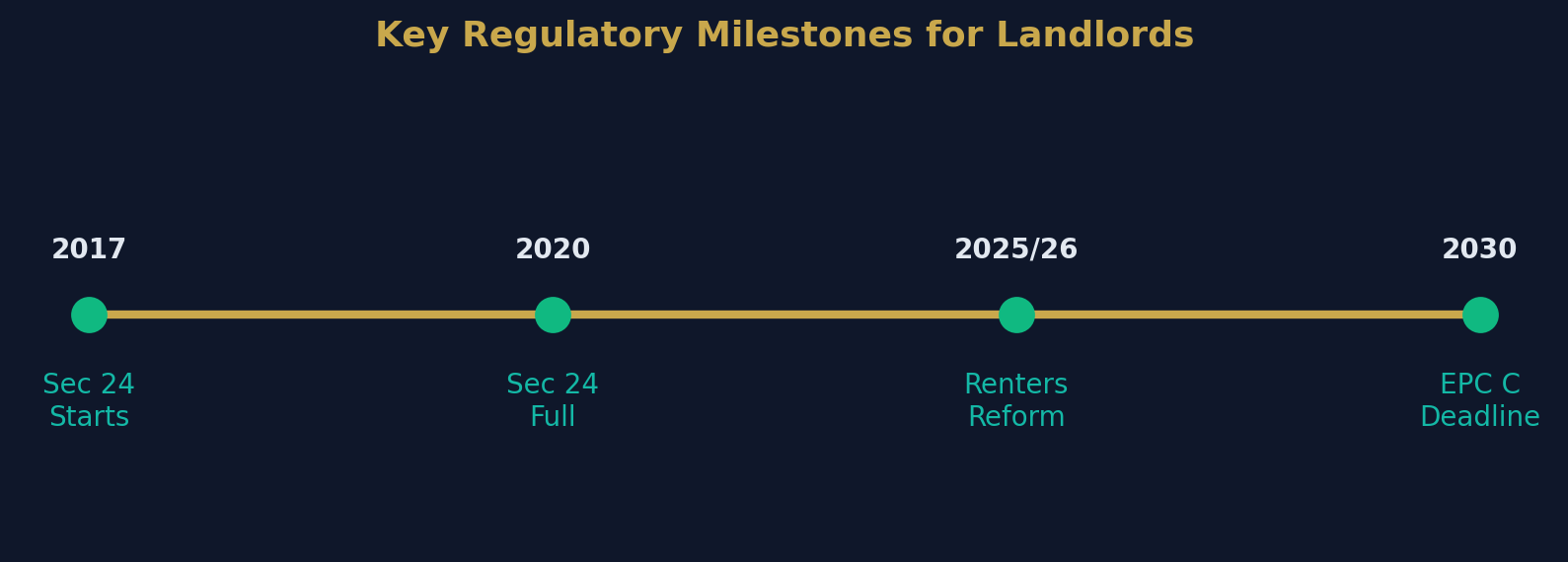

Section 21 Abolition

The Renters Reform Bill, now progressing through Parliament, will abolish Section 21 "no-fault" evictions. For equity investors, this fundamentally changes the risk profile of residential letting. The ability to regain possession of your property — to sell it, refurbish it, or deal with problematic tenants — becomes contingent on satisfying specific statutory grounds.

Multiple YouTube landlords have cited this as their primary reason for selling. One stated bluntly: "I'm exiting because I can't guarantee I'll get my own property back."

EPC Requirements

From 2028, all new tenancies will require a minimum Energy Performance Certificate (EPC) rating of Band C. For older properties — particularly Victorian terraces and pre-war stock that form the backbone of many investment portfolios — achieving Band C may require £10,000-£25,000 in upgrades including external wall insulation, new windows, and heat pump installation. This is a direct hit to equity, as the expenditure often exceeds the resulting valuation uplift.

Holiday Let Tax Changes

Previously, Furnished Holiday Lets (FHLs) benefited from favourable tax treatment, including full mortgage interest deduction and capital allowances. These advantages are being removed, eliminating one of the last personal tax-efficient property investment structures and pushing more investors toward the SPV route.

Risk Management for Equity Investors

Stress-Testing Your Portfolio

Every property equity investor should model their portfolio against three scenarios:

- Base case: 2-3% annual appreciation, current interest rates maintained

- Downturn: 10% price correction, interest rates rise 1%, 3-month void period

- Worst case: 20% correction, interest rates at 7%, 6-month void, major repair required

If your portfolio survives the downturn scenario without requiring capital injection, you are adequately capitalised. If it fails the worst case, you have concentration or leverage risk that needs addressing.

Cash Reserve Requirements

A minimum of 6 months' mortgage payments per property in liquid reserves is the professional standard. Many amateur investors hold no reserves, relying on rental income to cover all costs — a strategy that works until a boiler fails during a void period.

Insurance and Legal Structures

Buildings insurance, landlord liability insurance, rent guarantee insurance, and legal expenses cover should be viewed as non-negotiable. The cost — typically £300-£500 per property annually — is trivial relative to the downside risk of an uninsured event.

Building a Property Equity Portfolio: A Practical Roadmap

Step 1: Equity Audit

Before acquiring anything new, establish exactly how much realisable equity you hold. Commission desktop valuations on all existing properties, calculate your current LTV positions, and identify which properties have the most extractable equity at 75% LTV.

Step 2: Structure Decision

Consult a property-specialist accountant (not a generalist) to model the tax implications of personal vs SPV ownership based on your specific tax position, existing portfolio size, and growth ambitions. This decision is difficult to reverse once made.

Step 3: Location and Strategy Selection

Match your capital availability, risk tolerance, and time commitment to an appropriate strategy:

- £30-50k available, time-poor: Single BTL in a Northern city through a managed agent

- £50-100k available, hands-on: BRRR in the Midlands or North West

- £100k+ available, seeking scale: Multi-unit freehold blocks or small HMOs

- Capital rich, time-poor: REIT allocation or BTR fund participation

Step 4: Financing and Stress-Testing

Secure mortgage agreements in principle before property searching. Stress-test at 7% interest rates regardless of current product rates. Budget for 15-20% above quoted refurbishment costs — the market consistently underdelivers on build timelines and budgets.

Step 5: Professional Team Assembly

Your minimum viable team:

- Mortgage broker (whole-of-market, property investment specialist)

- Accountant (property tax specialist, not your family's generalist)

- Solicitor (conveyancing with investment property experience)

- Lettings agent (local, with managed service if you value your evenings)

- Surveyor (for pre-purchase due diligence, not just the lender's panel surveyor)

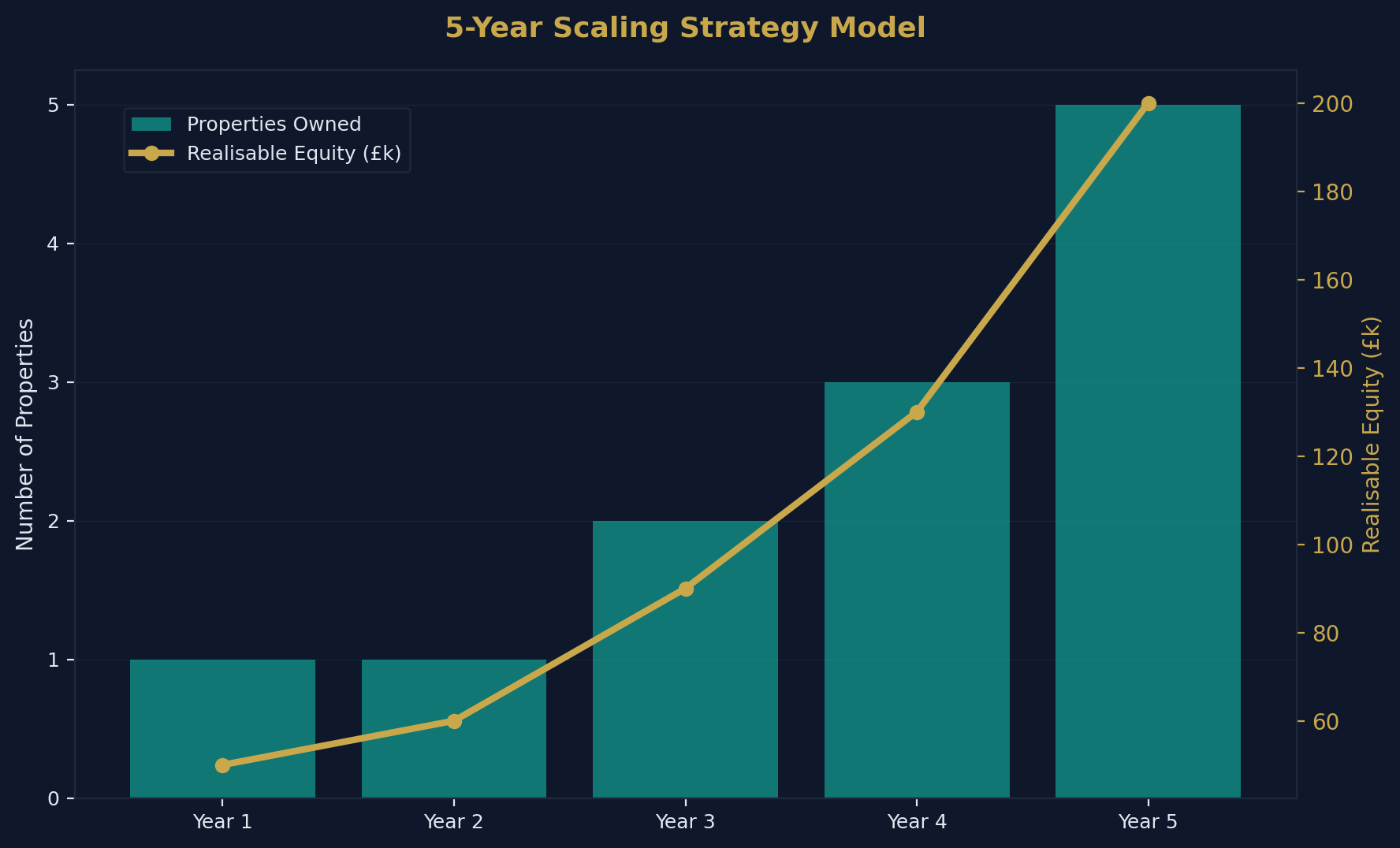

Year 1-5 Scaling Timeline

- Year 1: First acquisition, establish systems, learn the operational reality. Many investors underestimate how long it takes to accumulate your first £100,000 — the capital base that makes everything else possible

- Year 2: Refine strategy based on real data; consider second acquisition if cash flow permits

- Year 3-4: Begin equity recycling from appreciated or refurbished assets

- Year 5: Portfolio review — exit underperformers, consolidate into higher-yielding assets

FAQ: Property Equity Investment in the UK

How much equity do I need to start investing in property?

A minimum of £30,000-£50,000 in realisable equity or savings is realistic for a first investment property outside London. This covers a 25% deposit on a £150,000-£200,000 property plus stamp duty (additional rate at 5% from October 2024), legal fees, and an initial cash reserve. London requires significantly more — typically £80,000+ for a viable entry point.

Can I use equity from my home to invest?

Yes, through remortgaging or a further advance on your existing residential mortgage. Most lenders will allow you to borrow up to 85-90% LTV on your primary residence, though the released funds will need to meet affordability criteria for any subsequent buy-to-let application. Be aware that you are increasing the debt secured against your home — if property values fall, your personal residence is at risk.

What returns should I realistically expect?

Net rental yields (after management fees, maintenance, insurance, and void allowance) typically range from 3-5% depending on location and strategy. Capital appreciation is inherently unpredictable but has averaged 3-4% annually across the UK over the long term. Combined, a well-managed property investment might deliver 6-9% total return annually — before tax and financing costs.

How do I protect my equity during a downturn?

Three strategies: maintain low LTV ratios (below 65% provides meaningful buffer against price corrections), hold adequate cash reserves (6 months' costs per property minimum), and diversify geographically if your portfolio is large enough. Avoid cross-collateralisation where possible, and never rely on a single tenant or property type for all your income.

Is property equity investment Shariah-compliant?

Conventional mortgage-based property investment involves interest (riba), which is not permissible under Shariah principles. However, there are Shariah-compliant home purchase plans available in the UK from providers like Gatehouse Bank and Al Rayan Bank, which use diminishing musharakah (shared ownership) structures instead of interest-bearing loans. These products typically require higher deposits and may have more limited availability, but they allow Muslim investors to participate in property equity growth without compromising their faith principles.

This article is for informational purposes only and does not constitute financial, legal, or tax advice. Property investment carries risk, including the risk of capital loss. Always seek independent professional advice before making investment decisions.

Stop being a landlord. Start being an investor.

Shaded Canvas introduces serious capital to vetted UK property opportunities — targeting 12–16% net returns.

Start Investing →