The numbers tell a story that no headline can. Hong Kong nationals now own 25,972 homes across England and Wales — 13.2% of all foreign-owned properties — making them the single largest group of overseas property owners in the country. That figure grew 5.7% year-on-year through 2024, and with over 143,000 BNO visa applications already processed, the pipeline isn't slowing down.

But here's what the glossy property brochures won't tell you: buying UK property as a Hong Kong investor in 2026 is a fundamentally different game from what it was in 2021. The non-dom regime is gone. The Renters' Rights Bill has landed. Section 24 still punishes personal-name landlords. And the investors who are winning aren't the ones buying the cheapest flats — they're the ones who understand the tax architecture before they sign.

This guide breaks down exactly what you need to know.

The BNO Visa Effect: Why the UK Became Hong Kong's Default Investment Market

The British National (Overseas) visa scheme, launched on 31st January 2021, fundamentally rewired Hong Kong's relationship with UK property. The scheme allows BNO passport holders to live in the UK for up to five years, after which they can apply for settled status and eventually British citizenship.

The government's own projections estimated that up to 322,000 individuals from Hong Kong would arrive in the UK by 2026, bringing an estimated £2.9 billion in net economic benefit. Those projections are tracking close to reality.

The Investment Motivation Shift

What started as a relocation wave has matured into a sophisticated investment movement. A 2024 survey found that 70% of Hong Kong investors in the UK are now specifically seeking rental income — not just a place to live. This represents a critical shift from owner-occupier demand to professional buy-to-let activity.

The reasons are straightforward when you look at the comparative data:

- Hong Kong rental yields: 1.5–2.5% gross

- UK rental yields (Northern cities): 6–8% net

- Hong Kong average property price: approximately 2x London equivalent

- UK entry point (Manchester 3-bed): £180,000–£220,000

Between July 2020 and March 2021, Hong Kong investors purchased 1,932 properties in London alone, valued at £959 million. But the smarter money has since moved north — and for good reason.

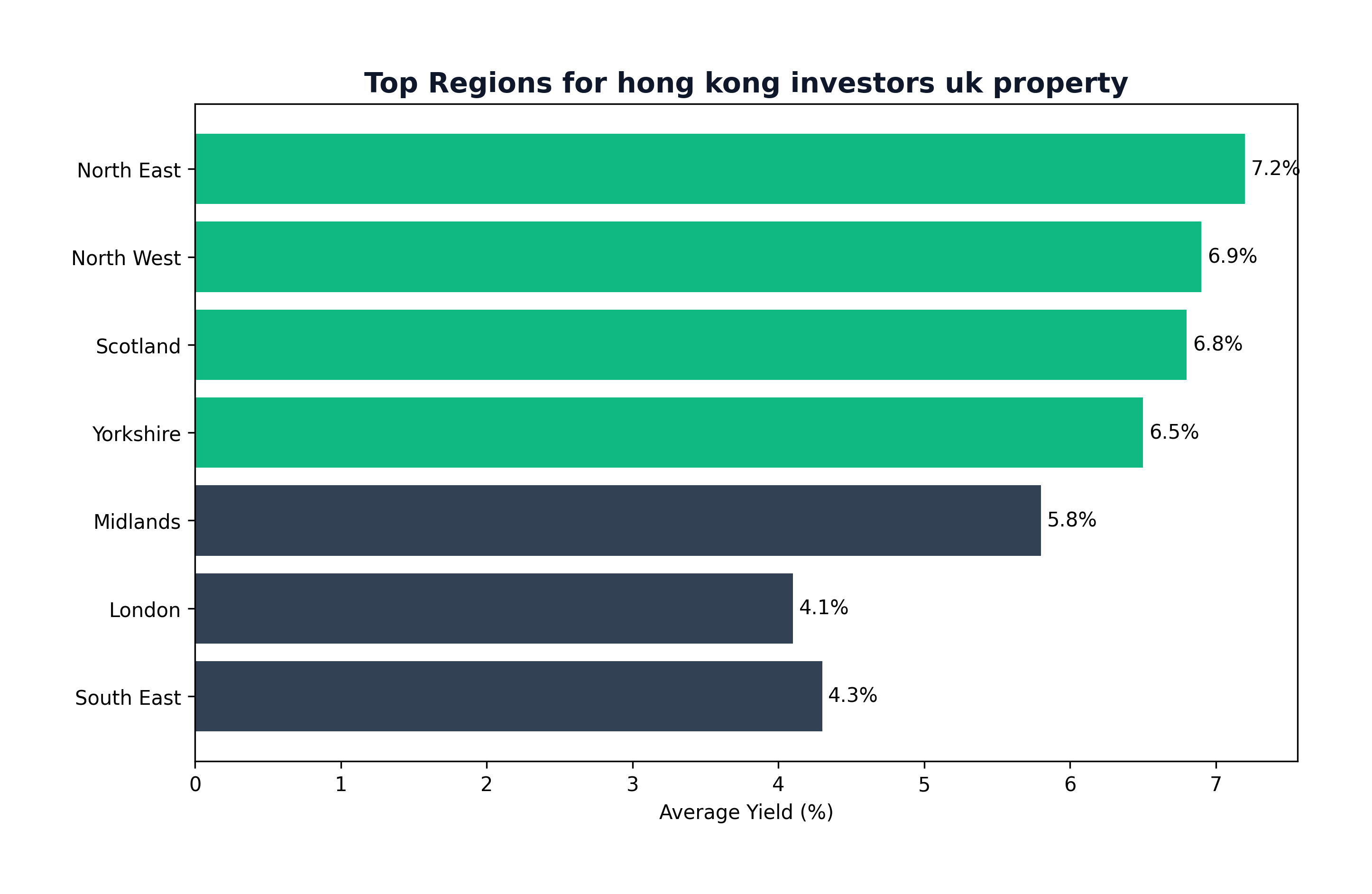

The Regional Yield Map: Where the Numbers Actually Work

London remains a brand that Hong Kong investors trust, but the data increasingly points elsewhere. Average rental yields in Zone 1-2 London sit at 3–4% gross, which barely covers financing costs after tax. Meanwhile, the Northern Powerhouse cities are delivering materially better returns.

City-by-City Comparison (Q1 2026 Data)

| City | Average Purchase Price (2-bed) | Gross Yield | Net Yield (post-management) | Void Rate |

|---|---|---|---|---|

| Liverpool (L1/L2) | £130,000 | 8.2% | 6.8% | 3.1% |

| Manchester (M1/M4) | £195,000 | 7.1% | 5.8% | 2.4% |

| Birmingham (B1/B5) | £175,000 | 6.9% | 5.6% | 2.8% |

| Leeds (LS1/LS2) | £155,000 | 7.4% | 6.1% | 2.9% |

| Glasgow (G1/G2) | £125,000 | 8.5% | 7.0% | 3.3% |

| London (Zones 1-2) | £520,000 | 3.8% | 2.5% | 1.8% |

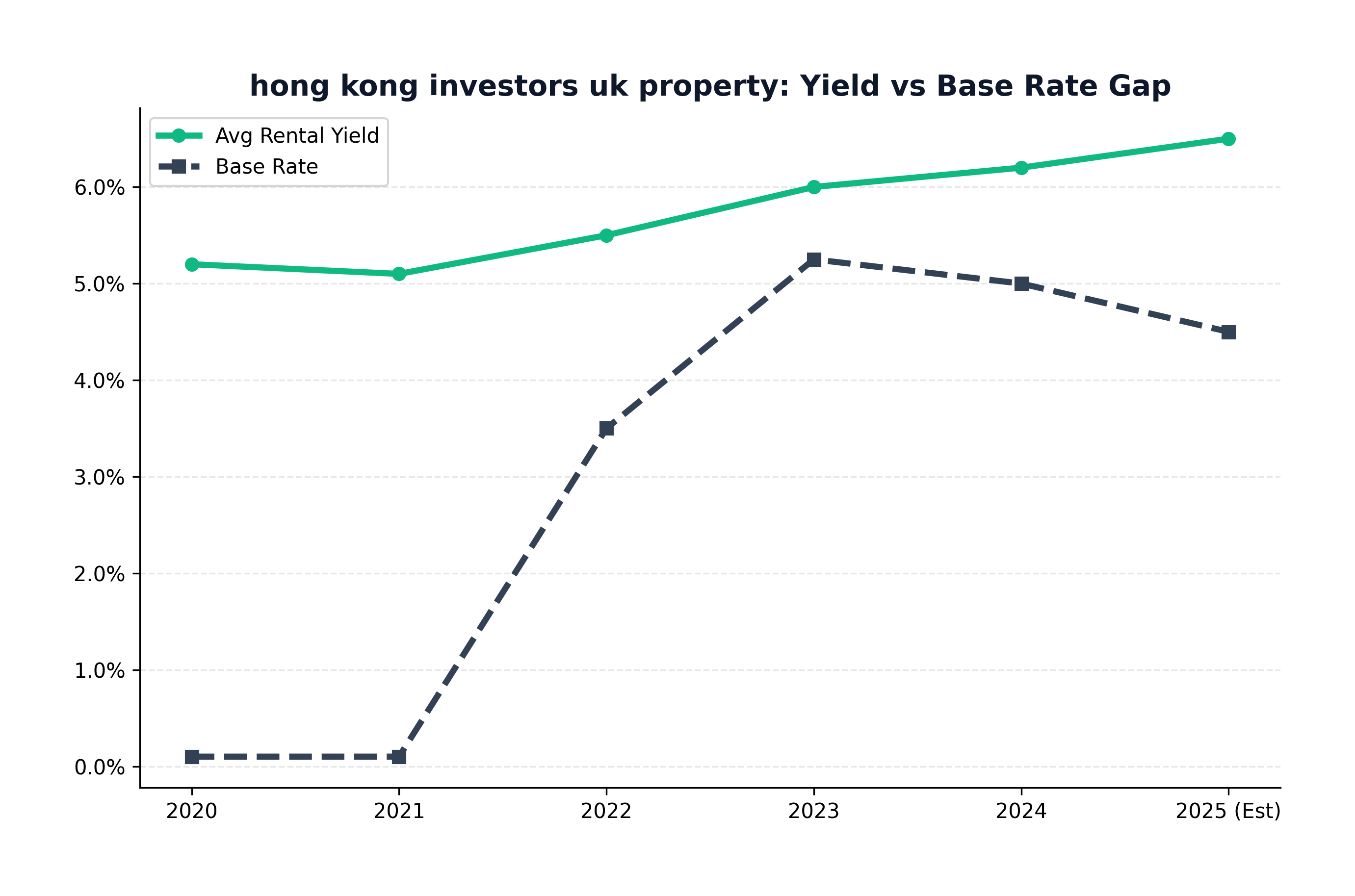

The pattern is clear. Savills projects UK house prices to rise 2% in 2026, contributing to an overall 24.5% increase over the four years to 2029. JLL is slightly more bullish at 3.5% for 2026, with a cumulative 19.9% growth between 2026 and 2029.

Rental growth forecasts are equally strong. Savills predicts UK rents will grow by 12% over four years to 2029. JLL expects cumulative rental growth of 17.1% over 2026–2029. Over 87% of UK landlords reported making a profit in 2026, with average yields hitting a 10-year high of 6.5% in Q2 2026.

For Hong Kong investors accustomed to capital appreciation plays with minimal yield, these are compelling fundamentals.

The Tax Architecture: What Nobody Tells You Until It's Too Late

This is where most Hong Kong investors lose money — not on the property, but on the tax structuring. The UK tax system is dramatically more complex than Hong Kong's flat 15% profits tax, and getting the structure wrong on day one can cost tens of thousands over a portfolio's lifetime.

Stamp Duty Land Tax (SDLT): The Entry Cost Stack

Hong Kong investors buying UK property face a three-layer SDLT stack:

- Standard SDLT rates (0–12% on sliding scale)

- Additional dwelling surcharge: +3% (applies if you own property anywhere in the world)

- Non-resident surcharge: +2% (applies if you've spent fewer than 183 days in the UK in the previous 12 months)

Worked Example — £250,000 Manchester Apartment:

| Component | Rate | Amount |

|---|---|---|

| Standard SDLT (£0–£250K) | 0% | £0 |

| Additional dwelling surcharge | 3% | £7,500 |

| Non-resident surcharge | 2% | £5,000 |

| Total SDLT | £12,500 |

That's an effective rate of 5% on a £250K property — a significant drag on returns that many investors only discover at exchange. One common strategy from the Reddit community: several HK families have sold their Hong Kong property before completing their UK purchase, eliminating the 3% additional dwelling surcharge and saving £7,500+ on a £250K transaction.

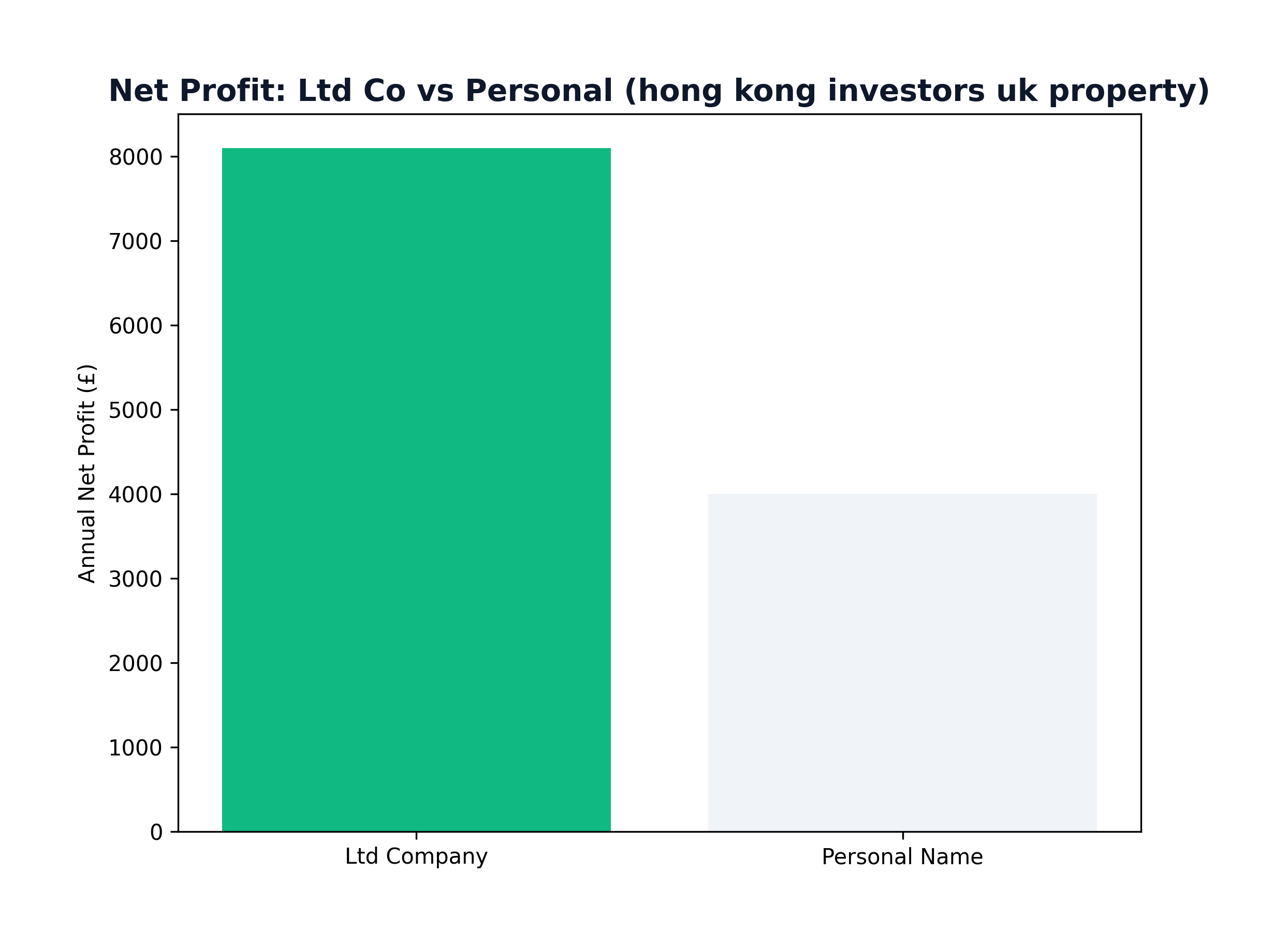

Income Tax vs Corporation Tax: The Critical Decision

This is, without exaggeration, the single most important financial decision a Hong Kong BTL investor will make.

| Metric | Personal Name | Ltd Company |

|---|---|---|

| Tax on rental profit | 20–45% (income tax) | 25% (corporation tax) |

| Mortgage interest relief | Restricted (Section 24 — 20% credit only) | Fully deductible |

| Capital gains on sale | 18–28% | 25% (rolled into corporation tax) |

| Inheritance tax exposure | Full (40% above £325K) | Reduced via share transfer |

| Upfront costs | Lower | Higher (accountant, company setup) |

For any portfolio above 2 properties, the Ltd company route is almost always superior. Section 24 — which restricts mortgage interest deductions to a basic 20% tax credit for personal-name landlords — doesn't apply to companies. On a £200K mortgage at 5.5% interest, that's a £2,200/year tax saving through the Ltd company structure alone.

The Non-Dom Bombshell: April 2026 Changes

This is critical and most competitor articles don't mention it. The UK's non-domicile tax regime was abolished from April 2026. Previously, Hong Kong investors who were "non-dom" could use the remittance basis to avoid UK tax on overseas income — essentially keeping their Hong Kong earnings outside the UK tax net.

Under the new rules, after 4 years of UK residency, you will pay UK tax on your worldwide income. For HK investors who moved under BNO in 2021 or 2022, this threshold has already been crossed or is imminent.

The implication is direct: rental income from any remaining Hong Kong property, investment dividends, and capital gains on overseas assets are now all within HMRC's reach. This makes UK-based structuring (Ltd company, pension contributions, ISA allowances) even more valuable as a tax-efficiency tool.

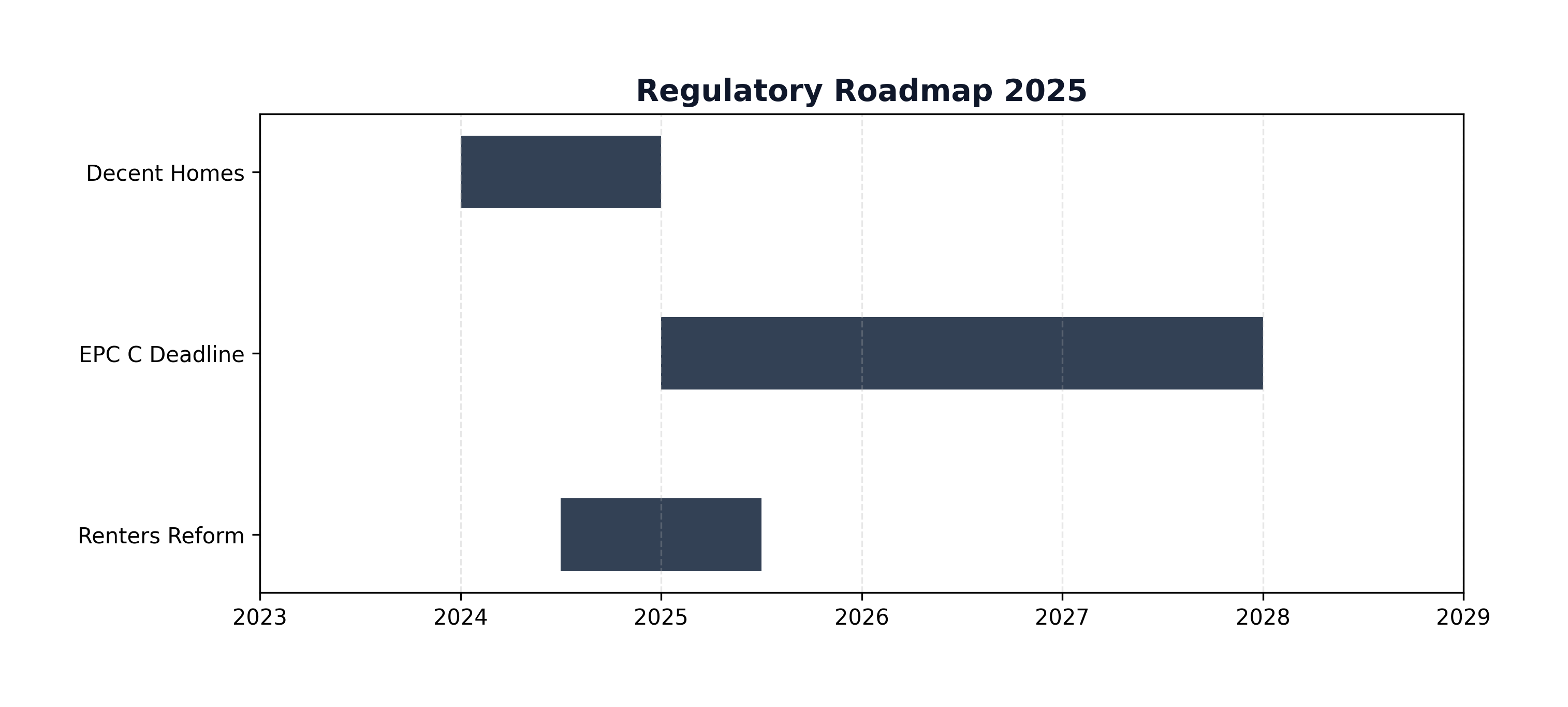

The Renters' Rights Bill: What It Means for Overseas Landlords

The Renters' Rights Bill, expected to receive Royal Assent before September 2026, introduces the most significant changes to the private rental sector in a generation. For Hong Kong investors managing properties from 6,000 miles away, the implications are substantial.

Key Changes

- Section 21 abolished: No-fault evictions are gone. Landlords must now use Section 8 with legitimate grounds (rent arrears, anti-social behaviour, landlord occupation).

- Open-ended tenancies: Fixed-term ASTs are replaced by rolling periodic tenancies. Tenants can leave with 2 months' notice at any time.

- Rent increases capped: Annual rent increases above market rate can be challenged through the First-tier Tribunal.

- Decent Homes Standard: Private rental properties must meet minimum quality standards, with local authorities empowered to enforce.

The Overseas Landlord Risk

The abolition of no-fault evictions creates a specific risk for overseas investors. If a tenant stops paying rent, the possession process now requires:

- A valid Section 8 ground

- Court application and hearing (potentially 4–6 months)

- Bailiff enforcement if tenant doesn't leave voluntarily

Managing this process remotely is extremely difficult. This makes your choice of letting agent more important than ever — you need an agent with demonstrated experience in tenant disputes and a proven track-record of low void periods.

Reddit advice consistently recommends interviewing at least 3 letting agents before committing, asking specifically for their average void period, their portfolio size, and their process for handling arrears.

The BRRR Strategy: How Experienced HK Investors Scale

The Buy, Renovate, Refinance, Repeat (BRRR) model has become increasingly popular among Hong Kong investors with UK experience. One documented case from the property investment community illustrates the mechanics:

- Purchase: 3-bed terraced house in Manchester, £185,000

- Renovation: Kitchen, bathroom, full redecoration — £25,000

- Post-works valuation: £260,000

- Remortgage at 75% LTV: £195,000 (recovers purchase price + most renovation costs)

- Monthly rent: £1,100 (7.1% gross yield on original cost)

The investor repeated this process four times in three years, building a 4-property portfolio largely using recycled capital. The key to making BRRR work from Hong Kong is having a trusted local project manager and a mortgage r who understands bridging-to-term refinancing.

Warning: Off-Plan Purchase Risks

Conversely, off-plan purchases from abroad carry significant risk. Multiple developments in Manchester and Birmingham have been delayed 12–18 months beyond their projected completion dates, and some investors have lost deposits entirely when developers entered administration.

The due diligence checklist for off-plan from overseas should include:

- Developer's track record (minimum 3 completed schemes)

- Deposit protection via solicitor's escrow account (not paid directly to developer)

- Independent legal review of the purchase contract

- Stage payment structure (not full deposit upfront)

Currency Dynamics: The Hidden Yield Booster

The HKD/GBP exchange rate has been a tailwind for Hong Kong investors. The rate moved from approximately 10.5 in 2022 to around 9.8 in 2026 — meaning a £300,000 property that would have cost HK$3.15M in 2022 effectively costs HK$2.94M in 2026. That's a HK$210,000 discount from currency movement alone, before any property appreciation.

However, currency works both ways. Investors should consider:

- Forward contracts: Lock in an exchange rate for 6–12 months ahead of completion

- Multi-currency accounts: Wise, HSBC Expat, and Revolut Business all offer competitive HKD/GBP conversion

- Timing purchases: Currency analysts suggest monitoring Bank of England rate decisions — GBP typically weakens in the 24 hours following a rate cut

The lack of discussion around currency hedging in competitor articles is a significant gap. For an investor deploying HK$3M+, a 3% currency swing represents HK$90,000 — more than most management fee bills.

Hidden Costs That Destroy Yields

The headline yield figures look attractive, but realistic net yield calculations must account for costs that many Hong Kong investors overlook until their first annual accounts.

The Full Cost Stack

| Cost Category | Annual Amount (typical 2-bed, £180K) | % of Gross Rent |

|---|---|---|

| Letting agent fees | £1,080–£1,620 | 10–15% |

| Maintenance reserve | £600–£1,200 | 5–10% |

| Insurance (landlord) | £180–£300 | 1.5–2.5% |

| Gas safety / EICR | £120–£180 | 1–1.5% |

| Council tax (void periods) | £400–£600 | 3–5% |

| Accountancy fees (Ltd) | £600–£1,200 | 5–10% |

| Mortgage interest (5.5%, 75% LTV) | £7,425 | 62% |

Council tax — Band D averaging £2,000–£2,500/year — is a frequently overlooked liability. While tenants pay during occupancy, the landlord is responsible during void periods. On a cheaper property with a 4-week void, that's an additional £200 straight off the bottom line.

Management fees of 10–15% are standard for fully managed service from a letting agent. This is non-negotiable for overseas landlords — self-management from Hong Kong is practically impossible given the requirements for property inspections, maintenance coordination, and tenant communication.

Wealth Transfer: The Family Investment Company (FIC) Strategy

For Hong Kong families with established UK property portfolios, the Family Investment Company has emerged as the preferred vehicle for intergenerational wealth transfer.

A FIC is a private limited company where:

- Parents hold voting/control shares (maintaining decision-making authority)

- Children hold growth shares (receiving future value appreciation and dividends)

- The company holds the property assets (corporation tax on profits, no IHT on share transfers)

The inheritance tax advantage is significant. A £1M property portfolio held personally would generate a £270,000 IHT liability (40% on value above £325K nil-rate band). The same portfolio within a FIC can be gradually transferred to the next generation through dividend distributions to growth shareholders, with no IHT event triggered.

Multiple threads in the UK property investment community recommend engaging a specialist solicitor for FIC setup — this is not a DIY structure. Setup costs typically run £3,000–£5,000, but the tax savings over a generation can be measured in hundreds of thousands.

Mortgage Options for Hong Kong-Based Buyers

Securing UK mortgage finance from Hong Kong is entirely feasible, but the landscape is narrower than for UK residents. Understanding which lenders operate in this space — and what they require — can save months of wasted applications.

Specialist Lenders for Overseas Buyers

The primary lenders serving Hong Kong-based buyers include:

- HSBC Expat (Jersey): The most established route for HK nationals. Typically offers 75% LTV with rates 0.5–1% above domestic equivalents. Requires a minimum income of £100,000 and an existing HSBC relationship.

- Barclays International: Offers expat buy-to-let mortgages at up to 70% LTV. Accepts HKD income with certified translations of payslips and tax returns.

- Specialist brokers (e.g., Liquid Expat Mortgages, Offshoreonline): These aggregate access to 15+ lenders including private banks. Broker fees of 1–1.5% are standard but often worthwhile given the complexity.

Interest Rate Expectations

As of early 2026, overseas BTL mortgage rates typically range from 5.25% to 6.5% depending on LTV, property type, and lending criteria. This compares to domestic BTL rates of 4.5–5.5%. The premium reflects the additional underwriting risk and servicing complexity of lending to overseas borrowers.

For a £200,000 mortgage at 5.75% on an interest-only basis, monthly payments run approximately £958. Against a gross monthly rent of £1,050 (on a £250K property yielding 5%), the debt service coverage ratio sits at 1.10x — tight but workable, and well within most lender requirements of 125–145% rental coverage at a 5.5% stress test rate.

Documentation Requirements

HK-based applicants should prepare for a lengthier application process — typically 6–10 weeks versus 3–4 for domestic buyers. Required documentation includes:

- Last 3 months' payslips (translated and certified if in Chinese)

- Latest tax return or Employer's Return (BIR56A)

- 6 months' bank statements showing salary credits

- Proof of deposit source (gift letters, sale proceeds, savings history)

- Credit report from a recognised HK bureau (TransUnion HK)

One critical detail: most UK lenders will not accept bank statements from mainland Chinese banks. Funds must be routed through a Hong Kong-domiciled institution or an international bank with a recognised UK presence.

The Five Most Expensive Mistakes HK Investors Make

Based on patterns observed across investment communities and professional advisory networks, these are the errors that cost Hong Kong investors the most:

1. Buying in Personal Name Without Tax Modelling

The default instinct — particularly for first-time investors — is to buy in their personal name because it feels simpler. Without running the numbers through a buy-to-let tax calculator that accounts for Section 24, marginal income tax rates, and future CGT liability, investors routinely leave £3,000–£8,000 per year on the table. A 30-minute conversation with a property-specialist accountant before your first purchase pays for itself within the first tax year.

2. Ignoring the EPC Requirement

From April 2026, all new tenancies in England and Wales require a minimum Energy Performance Certificate (EPC) rating of C. Properties rated D or below cannot be legally let to new tenants. Many older terraced houses in the Northern cities favoured by HK investors currently sit at D or E. Upgrading typically costs £5,000–£15,000 (insulation, boiler replacement, double glazing) — a cost that must be factored into the purchase analysis, not discovered at the point of re-letting.

3. Underestimating Void Periods

The average void period across England is 21 days between tenancies. In student-heavy areas or seasonal markets, this can extend to 4–8 weeks. During voids, the landlord bears mortgage payments, council tax, insurance, and utility standing charges. A realistic cash flow model should assume 1 month void per year as a baseline.

4. Choosing the Cheapest Letting Agent

Management fees of 8% versus 12% look like a saving on paper — but the cheapest agents typically have the highest void rates, the slowest maintenance response times, and the weakest tenant vetting processes. For overseas landlords, the quality of your letting agent is effectively the quality of your investment. The premium agents charge 12–15% for a reason: proactive maintenance, robust referencing, quarterly property inspections, and dedicated account managers rather than call-centre triage.

5. Not Planning for Capital Gains on Exit

Many HK investors focus entirely on yield and forget about the exit. If you're non-resident and sell a UK residential property, you'll pay CGT at 18% (basic rate) or 28% (higher rate) on the gain. For a property purchased at £180,000 and sold at £260,000, that's a gain of £80,000 and a potential tax bill of £14,400–£22,400. Building this into your 5-year return model prevents unpleasant surprises and may influence your hold period strategy.

Landlord Insurance: What Overseas Owners Actually Need

Standard buildings insurance is just the starting point. Overseas landlords face a specific risk profile that requires tailored cover:

- Rent guarantee insurance: Covers lost rental income if a tenant defaults. Typically costs £150–£300/year for policies covering up to 12 months' rent. Given the extended possession timelines under the Renters' Rights Bill, this has shifted from "nice to have" to essential.

- Legal expenses insurance: Covers solicitor costs for tenant disputes, possession proceedings, and compliance issues. Usually bundled with rent guarantee for an additional £50–£100/year.

- Unoccupied property cover: Critical during void periods or renovation phases. Standard policies exclude claims on properties empty for more than 30 consecutive days — a separate unoccupied policy is needed.

- Landlord liability insurance: Protects against tenant or visitor injury claims. Minimum cover of £2M is recommended and typically costs £80–£150/year.

The Buying Process: A Step-by-Step Timeline for Hong Kong Residents

For first-time investors buying from Hong Kong, the process typically runs 12–16 weeks from offer acceptance to completion.

Timeline

- Weeks 1–2: Secure a mortgage Agreement in Principle (AIP). HSBC Expat and Barclays International are the most active lenders for HK-based borrowers.

- Weeks 2–4: Property search and offer. Use a buying agent or attend virtual viewings via your letting agent.

- Weeks 4–6: Instruct a UK solicitor. They must be on your mortgage lender's panel. Conveyancing for overseas buyers requires enhanced ID verification — expect to provide apostilled copies of your HKID and passport.

- Weeks 6–10: Survey, searches, and legal due diligence. Your solicitor handles local authority searches, environmental reports, and title checks.

- Weeks 10–12: Mortgage offer issued. Transfer deposit funds via your chosen FX provider.

- Weeks 12–16: Exchange and completion. You'll need to sign documents remotely via your solicitor's witness arrangements, or appoint a Power of Attorney.

Critical Documents for HK Buyers

- Valid passport and HKID (apostilled)

- Proof of funds (3 months bank statements, source of wealth letter)

- Proof of address in Hong Kong (utility bill, rates demand)

- BNO visa grant letter (if applicable)

- Overseas tax identification number

What Happens Next: The 2026–2029 Outlook

The macro tailwinds for Hong Kong investment into UK property remain strong:

- BNO pipeline: 322,000 projected arrivals by end of 2026, with family reunification extending demand

- Yield environment: 6.5% average yields at a 10-year high, with rental supply constrained

- Price growth: 2–4% annual appreciation forecast through 2029, with Northern cities outperforming

- Currency advantage: GBP weakness relative to HKD persists, enhancing purchasing power

- Regulatory clarity: Post-Renters' Rights Bill, the rules are clear — professional landlords who adapt will thrive

The investors who succeed won't be the ones chasing the cheapest property on Rightmove. They'll be the ones who structure correctly from day one — Ltd company, appropriate insurance, competent local management, and a clear understanding of the tax landscape. The difference between a 3% and a 7% net yield isn't the property. It's the structure.

Shaded Canvas provides data-driven investment analysis for UK property investors. This article is for informational purposes only and does not constitute financial advice. Always consult a qualified tax adviser before making investment decisions.

📚 Related Reading

- How to Reduce Taxes Legally: The UK Commercial Property Cheat Code

- The Drop Servicing Model: How I Closed a £120k Deal Without Doing the Work

- Property Equity Investors UK: The Hard Truth About Building Wealth Through Bricks in 2026

- Best Capital Growth Property UK: Where Property Prices Are Actually Heading in 2026 and Beyond

- Passive Income Property UK: How to Build a Rental Portfolio That Actually Pays You in 2026

Stop being a landlord. Start being an investor.

Shaded Canvas introduces serious capital to vetted UK property opportunities — targeting 12–16% net returns.

Start Investing →