To Whom It May Concern,

I will be giving away the biggest cheat codes that I have found so far along the way in the next coming chapters.

I ask that you please keep in mind that I will be sharing some hard facts about myself so do as Bruce Lee says: “Take what is useful and discard what is not.”

I believe that no matter what you are going through, there is always a solution to your problems — and the only person that is going to save you is you. You can’t change your circumstances, but you can change yourself.

Looking back, I am surprised at what I have managed to achieve whilst going through a lot of life’s curve balls and this is part of the story. The quality of your life depends on the questions you ask yourself. Instead of saying you can’t do something, break the problem down.

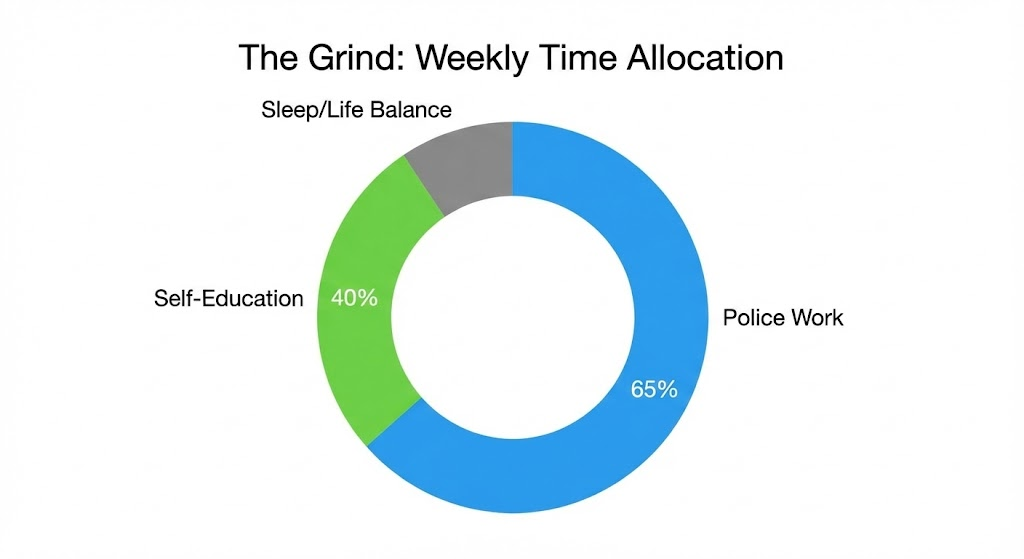

Setting the Scene: Cue Training Montage

I was on a £33,000-ish a year salary, working approximately 60-70h a week as a police officer. I knew I wanted to own property all over the world but had no idea how I was going to achieve this.

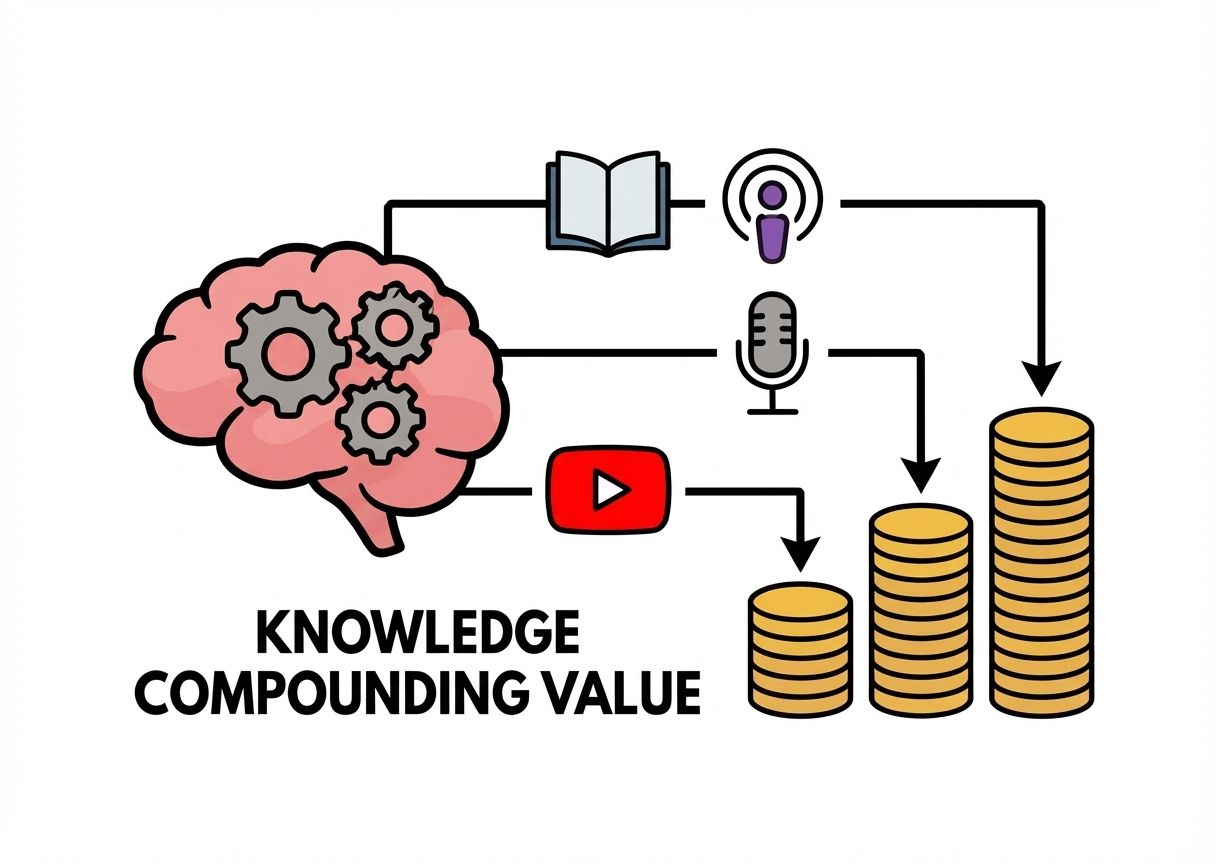

With zero experience in real estate or finance, I started studying everything I could find on those topics. Every night or morning (depending my shift), I’d dive into books, podcasts, YouTube videos – you name it – soaking up knowledge about property and personal finance.

I was essentially working a second “job” educating myself, easily putting in 40 hours a week of research on top of my police work. It was intense, but I was hooked on learning.

I also made it a point to talk to anyone and everyone with experience in property or business. I’d grab coffees with local landlords, chat up entrepreneurs, and basically make myself a sponge for advice. Most people are happy to talk about their success if you show genuine interest. I was that eager newbie asking a million questions.

CHEAT CODE: Become obsessed with learning your game – even if it means late nights. Knowledge is a cheat code that costs you nothing but time with the value of which compounding with time.

Becoming a Problem Solver (Networking 101)

All that studying paid off. Before I knew it, I had absorbed enough that I could spot problems and suggest solutions in conversations about property. Pretty soon I found myself helping people who were far more experienced than me solve their property/business dilemmas. Imagine that – a rookie like me giving tips to veterans!

How? Well, information is power. I had devoured so much material that I often knew of a strategy or idea that others hadn’t tried yet. By sharing those tips freely, I started building a little reputation as the “resourceful guy” among my growing network.

I wasn’t charging anything; I was just adding value wherever I could. This turned out to be crucial. People began to trust me because I genuinely wanted to help. I wasn’t angling for money (which weirdly has made more money than anything else I can think of). If I did have something that others didn’t was that being a police officer meant it was slightly easier for me to do legal research.

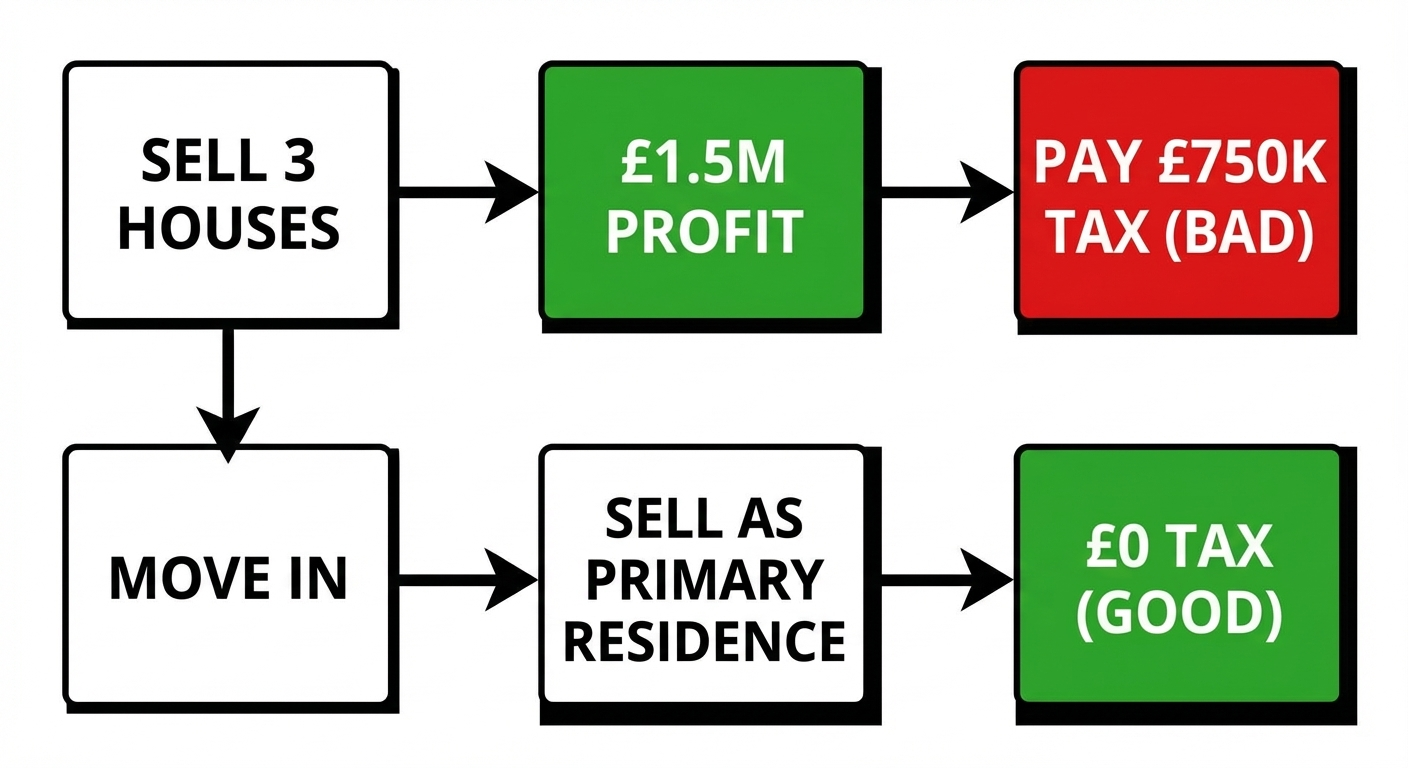

Client 1: A friend of mine told me he was selling his 3 houses which were all in his name. Bringing him approximately £500,000 in profit each when he sells them. This would have cost him approx £750,000 in taxes (1.5mill profit / 2 = 750,000).

I was in no way letting my friend who pays a crap load in tax as an employee give the government £750,000 when we both haven’t even seen that kind of money upfront.

I knew of the tax law that states that if you sell your primary residence, then you do not need to pay taxes on it. I confirmed it with an accountant and then gave him the plan of moving into his houses and selling them one by one. In hindsight, I should have charged him for that advice.

Chapter 2: The Good Stuff

I knew what I wanted which was buying a lot of houses, but I figured let me break the problem down of buying one house. Most people have two problems when it comes to buying a house: The deposit and Price of the house they can afford.

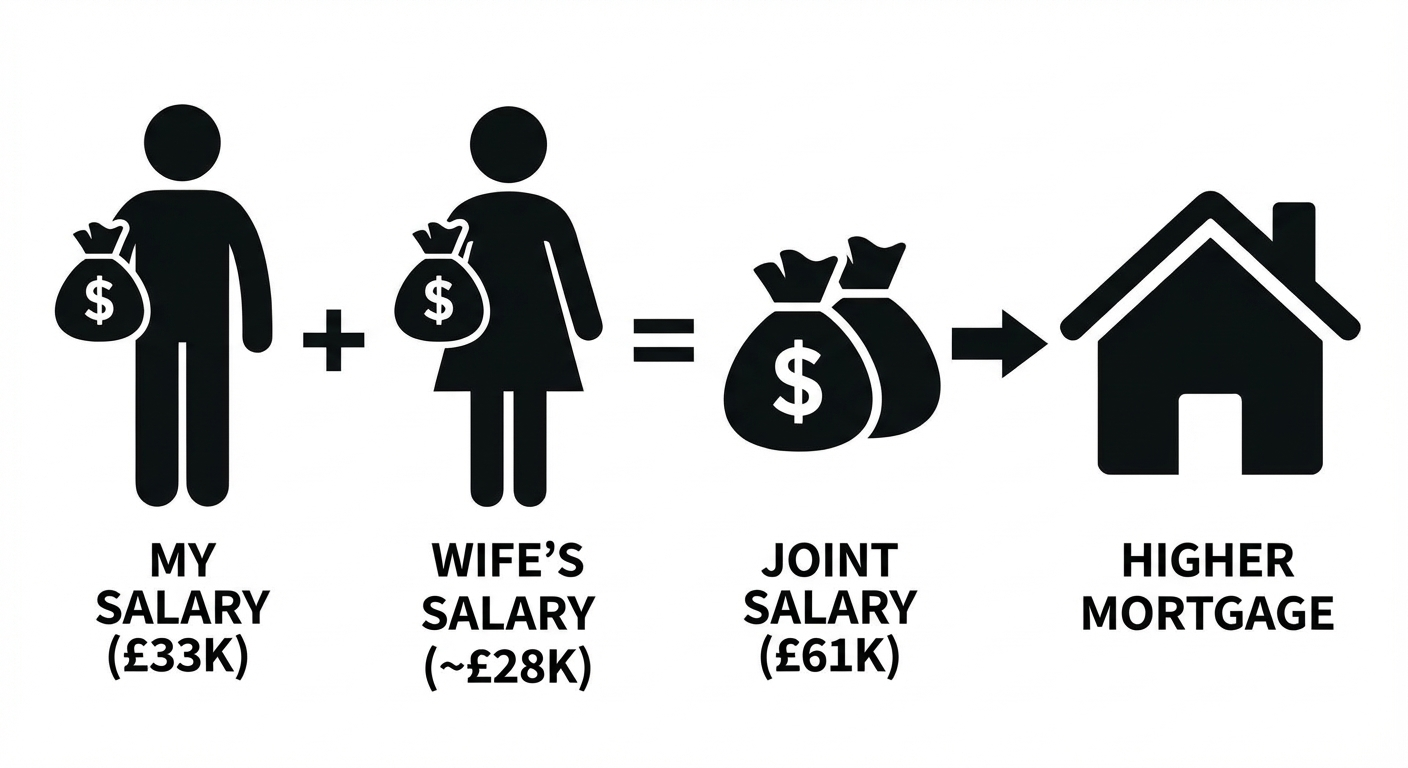

Most high street banks will only lend approx. 4.5 times your yearly salary. So I tackled the second problem first because I knew I wanted a house, not far from the underground (train), freehold, 100% mine, in London and to be honest with my salary I was not feeling very optimistic.

There is two solutions to that problem, open a company and pay myself a salary for 3 - 6 months (banks usually only check that much, and it would mean you will be paying tax on that money) or get a mortgage with my wife. I chose the latter.👩❤️👨

This bought our joint salary up to £61,000-ish at the time, meaning we could now get a £270,000 loan from the bank for a house.

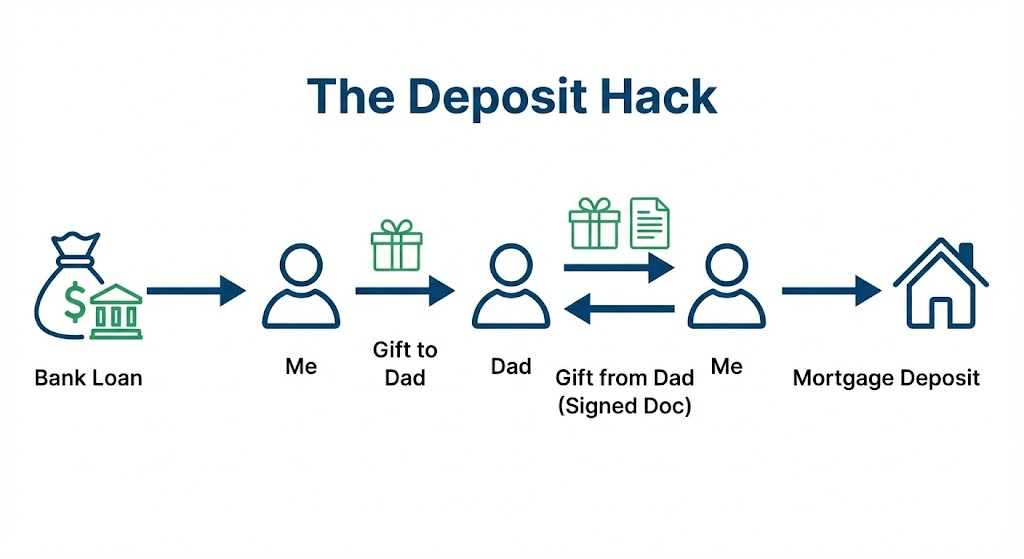

Our next issue is that the bank needed 10% deposit/down payment on the house to be in our accounts in cash before they accept to give us the mortgage for a house (even though the mortgage repayment amount was way lower than our rent).

I spoke to a lot of people and the idea of getting a loan from the post office taking it to the bank and being like, I have the deposit money was stuck in my head.

The next issue I found was that banks don’t want you taking out a loan for the deposit (as it will essentially become a 100% mortgage), so I sent that money that I got as a loan to my dad as a “gift”, he then sent it back to me as a “gift”, signed a word document I wrote up in 2 min saying this money is a gift and he has no stake in any house I buy and (pow), I now had the deposit and the salary to get a decent-ish house in east London.

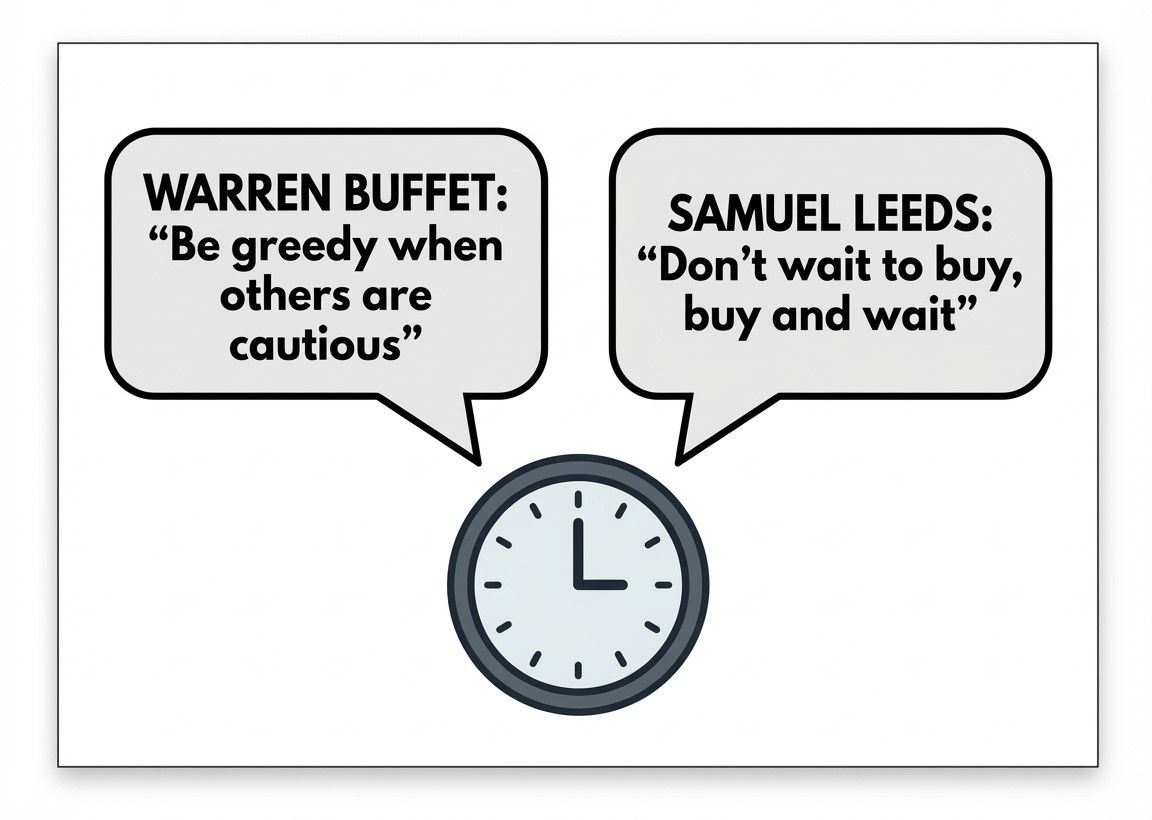

At the time I was looking for a house covid had struck, everything was uncertain and everyone around me was telling me to wait to see what happens before buying a house.

I then remembered a two simple sayings. One that Warren Buffett said “be cautious when people are greedy and be greedy when people are cautious”, the other was from Samuel Leeds which was “don’t wait to buy property, buy property and wait”.

I checked the statistics of house prices and checked price history for random houses on the street and I found that regardless of a recession or not, UK house prices doubled every 7-12 years without fail.

This meant that all I needed to do was live in my house or rent it if house prices dropped. We were looking every day for months and saw a lot of houses that needed a “makeover”, until we found our home for £300,000.

Completion on the house was delayed because of covid but this was a blessing in disguise as I was £270 short on the £300,000 and this gave us time to save for some work to be done on the house.

I won’t bore you with the details but we were looking for approximately 2 months for any second hand kitchens and found an ex-display kitchen with all the bells and whistles for £475 (best bargain to date).

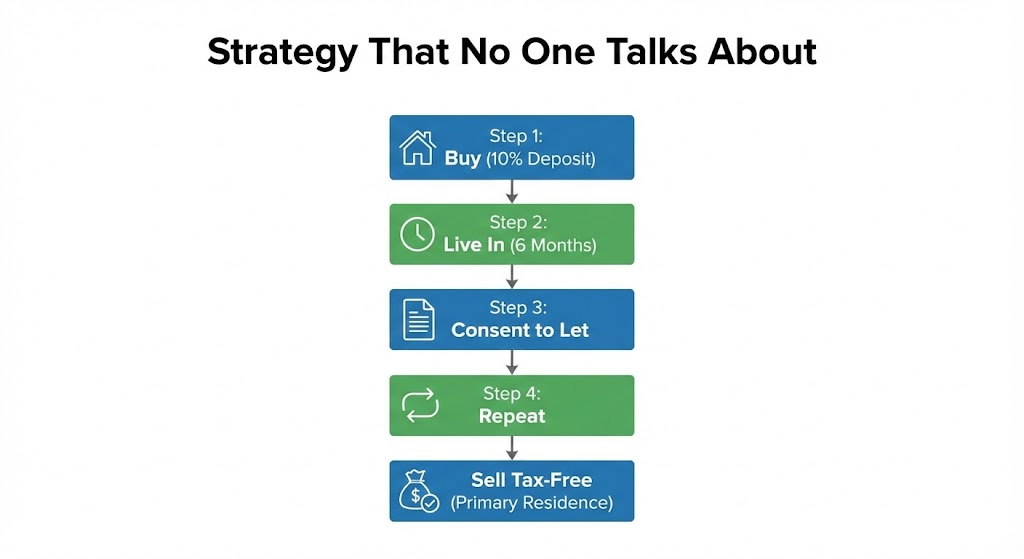

Strategy That No One Talks About

Step 1: Buy a house to live, You only need a 10% deposit to get a mortgage on a buy to live property (you need less money than a buy to let which requires a minimum 20% deposit)

Step 2: Live in the house for 6 months (do any work you need to get it rent ready and ofc enjoy having the place)

Step 3: Get consent to let from the bank (most people don’t know that most banks will give you a piece of paper after 6 months of purchasing the property saying you can rent your house out whilst keeping the deposit at 10% and the interest rate frozen at what you agreed upon).

Step 4: Buy another house and do steps 1 - 4 on repeat.

Step 5: When house prices go up, move into your houses and sell them one by one as you move into them as there is a tax law saying that if you sell your “primary residence” then you don’t pay tax on it.

You may be taxed on the income from the rent but this is nothing in comparison to the amount you get from selling your house tax free after a couple of years.

Side note: Whilst doing this strategy I came across many pitfalls that could have completely stopped me in my tracks and found many other more efficient ways to make your first £100,000.

📚 Related Reading

- How to Reduce Taxes Legally: The UK Commercial Property Cheat Code

- The Drop Servicing Model: How I Closed a £120k Deal Without Doing the Work

- Property Equity Investors UK: The Hard Truth About Building Wealth Through Bricks in 2026

- Best Capital Growth Property UK: Where Property Prices Are Actually Heading in 2026 and Beyond

- Passive Income Property UK: How to Build a Rental Portfolio That Actually Pays You in 2026

Stop being a landlord. Start being an investor.

Shaded Canvas introduces serious capital to vetted UK property opportunities — targeting 12–16% net returns.

Start Investing →