The intersection of real estate and venture capital — the funding of technology companies disrupting property markets — has matured from niche curiosity to established asset class over the past decade. London has emerged as Europe's dominant PropTech hub, second globally only to New York, with a funding ecosystem spanning seed investors, growth-stage VCs, and corporate venture arms of the world's largest real estate companies. For founders seeking funding and investors evaluating allocation, this guide maps the landscape.

Figure: Yield vs Interest Rates

Figure: Yield vs Interest Rates

London as Europe's PropTech Capital

The UK PropTech sector attracted approximately £1.2 billion in venture funding in 2023, maintaining its position as the largest PropTech ecosystem in Europe despite a broader VC funding contraction. The concentration of financial services, legal, and real estate expertise in London creates a unique environment for B2B PropTech companies — their customers, advisers, and investors are all within a square mile. This density accelerates sales cycles and product iteration in ways that are difficult to replicate in smaller markets.

The market has evolved significantly since the consumer-facing property portals (Zoopla, PrimeLocation) attracted the early PropTech capital. Today's investment themes are predominantly B2B SaaS — software that helps institutional landlords, property managers, construction companies, and real estate investors operate more efficiently or make better decisions. The funding 'flight to quality' visible in 2023–2024 has concentrated capital in companies with demonstrable revenue, strong net revenue retention, and clear paths to profitability, rather than high-growth revenue stories with uncertain unit economics.

Figure: Regional Yield Heatmap

Figure: Regional Yield Heatmap

Key Investors and Funds

Pi Labs — The Specialist Seed Investor

Pi Labs is Europe's most dedicated early-stage PropTech investor, with a portfolio spanning construction technology, sustainability analytics, property management software, and marketplace platforms. The fund operates at pre-seed and seed stage, typically investing £500,000–£2 million as lead or co-lead, and provides hands-on support through its network of real estate operating partners. For early-stage PropTech founders, Pi Labs is the first institutional conversation worth having.

Concrete VC

Concrete VC bridges early-stage and growth, investing in companies with demonstrated product-market fit in the built environment sector. The fund has a European mandate but allocates heavily to UK companies given the ecosystem depth. Investment sizes range from £1–£5 million at Series A, with the fund providing strategic introductions to enterprise property company clients as a key value-add beyond capital.

JLL Spark — Corporate Venture Capital

JLL's corporate venture arm invests in PropTech companies aligned with its service offering — lease administration software, facilities management technology, real estate analytics. The strategic value for portfolio companies is access to JLL's global client base as a pilot or commercial partner. The trade-off is that CVC investors have strategic objectives that can diverge from a founder's desire for an independent exit.

Figure: Tax Trap: Personal vs Ltd

Figure: Tax Trap: Personal vs Ltd

Core Investment Themes for 2026

ESG and Decarbonisation Technology

The real estate sector accounts for approximately 40% of global carbon emissions and faces increasingly stringent regulatory requirements — the UK's Minimum Energy Efficiency Standards, the EU's Energy Performance of Buildings Directive, and investor-driven net zero commitments. Software companies that help asset owners measure, manage, and report embodied and operational carbon are attracting strong investor interest. Companies operating in this space include energy monitoring platforms, lifecycle assessment tools, and carbon accounting software adapted for real estate portfolios.

Construction Technology (ConTech)

The UK construction sector has chronic productivity problems — output per worker has barely improved in real terms over 30 years, project overruns are endemic, and the skills shortage is structural. Digital twins (virtual models of buildings updated in real time), AI-driven project management tools, and modular/off-site construction technology are attracting venture capital as investors see a large, fragmented, underdeveloped market ripe for software-driven efficiency gains.

Tenant Experience and Flexible Space

The shift toward hybrid working has accelerated demand for flexible office solutions and elevated tenants' expectations of their workplace experience. Software platforms serving this market — workplace management apps, visitor management systems, space analytics tools — have attracted growth capital as landlords compete to retain and attract tenants in a market where vacancy rates in secondary office space are rising.

Figure: Regulatory Roadmap

Figure: Regulatory Roadmap

How to Get Funded: What UK PropTech VCs Look For

The single most important signal for UK PropTech VCs in 2026 is commercial traction — paying customers, contractually committed revenue, and evidence of strong net revenue retention (the proportion of revenue retained plus expansion from existing customers). The 'just raise on a pitch deck' era has passed; investors are conducting significantly more due diligence on unit economics, churn, and competitive differentiation before committing.

EIS (Enterprise Investment Scheme) and SEIS (Seed Enterprise Investment Scheme) tax relief is available for qualifying investments in UK PropTech companies at seed and early stage, offering 30–50% income tax relief on investment and CGT exemption on gains. These schemes materially improve the economics of early-stage UK PropTech investing for individual investors and are a meaningful tool in fundraising conversations. Accelerators — including REACH UK (the National Association of Realtors' programme), Future Cities Catapult's programmes, and the UKGBC's innovation hub — provide non-dilutive support and market access that complements VC funding.

Figure: Strategy Cycle

Figure: Strategy Cycle

Notable UK PropTech Success Stories

Plentific, the property maintenance and operations platform, has raised over $100 million in growth capital and expanded internationally — exemplifying the B2B SaaS model that UK PropTech investors currently favour. LandTech (site sourcing software for residential developers) has built strong recurring revenue from the housebuilding sector and represents the 'enabling infrastructure' category of PropTech that investors find attractive for its embedded, essential nature.

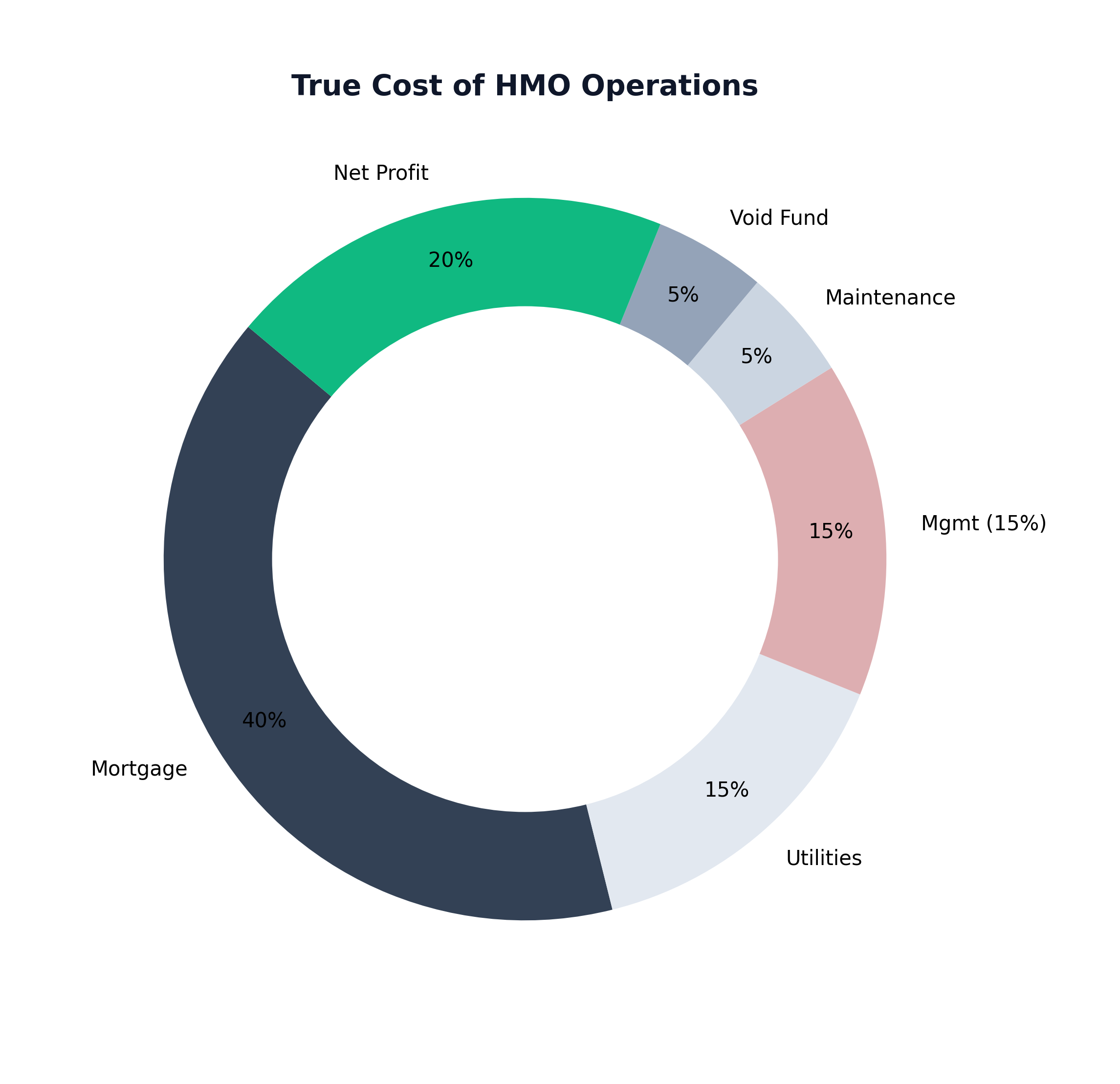

Figure: HMO Expense Breakdown

Figure: HMO Expense Breakdown

The AI and Tokenisation Outlook

Artificial intelligence is beginning to permeate every layer of real estate — automated valuation models, AI-driven lease abstraction, predictive maintenance algorithms, and generative AI tools for property marketing. The companies attracting investment are those deploying AI to solve specific, high-value workflow problems (legal document review, energy optimisation, credit scoring for renters) rather than applying AI as a general marketing label. Blockchain-based tokenisation of real estate — fractional digital ownership of physical assets — remains a sector with significant theoretical promise and limited commercial traction. The regulatory framework for tokenised real assets is still developing, and institutional adoption has been slower than early projections suggested.

Stop being a landlord. Start being an investor.

Shaded Canvas introduces serious capital to vetted UK property opportunities — targeting 12–16% net returns.

Start Investing →