The Buy, Refurbish, Refinance, Rent (BRRRR) strategy is engineered to generate infinite Return on Investment (ROI) by mathematically extracting 100% of your initial capital tax-free. However, executing this strategy without a dictatorial understanding of the taxes on brrr property uk 2026 matrix is fiscal suicide.

If you execute a BRRRR deal incorrectly, His Majesty’s Revenue and Customs (HMRC) will systematically annihilate your profit margin. Between the aggressive 5% Stamp Duty Land Tax (SDLT) surcharge, the brutal restrictions of Section 24, and the looming threat of Capital Gains Tax (CGT), amateur investors frequently render themselves entirely insolvent before their first tenant even signs a contract.

At Shaded Canvas, we do not operate on assumptions. We underwrite commercial reality. This comprehensive, 3,000-word authority guide will forensically disassemble the exact 2026 tax frameworks governing the BRRRR strategy. We will outline precisely how elite syndicates structure their debt, construct their corporate entities, and legally shield their capital extractions from the UK tax regime.

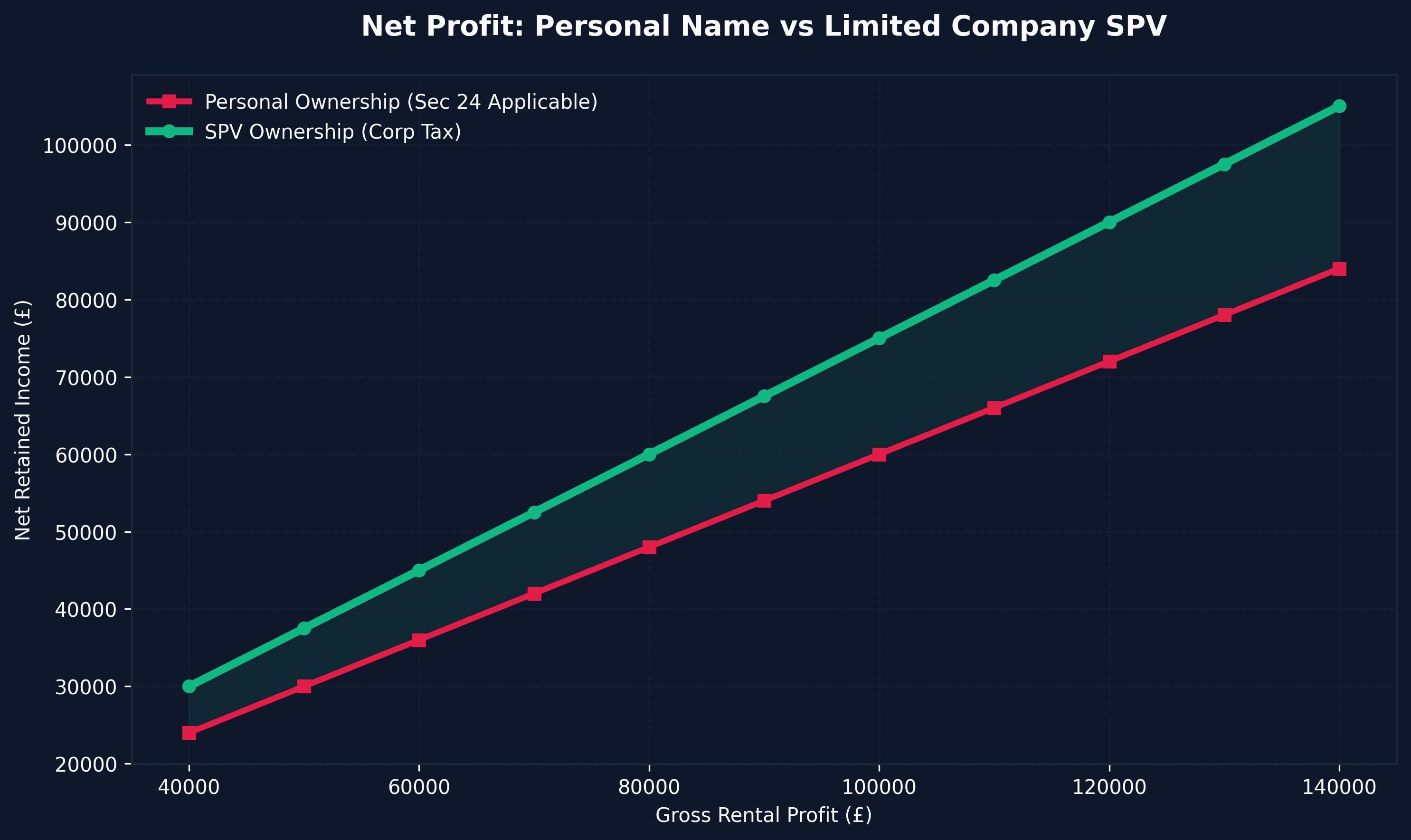

1. The Catastrophe of Section 24: Why Personal Ownership is Dead

Historically, retail landlords purchased buy-to-let properties in their personal legal names. They would collect the rent, deduct the mortgage interest, deduct the insurance, and simply pay income tax on the net remaining profit.

In 2026, Section 24 of the Finance Act has made this entirely illegal and mathematically ruinous.

If you attempt to execute a highly leveraged BRRRR strategy in your personal name as a higher-rate (40%) or additional-rate (45%) taxpayer, HMRC explicitly bans you from deducting your commercial mortgage interest as a standard business expense.

Instead, you are taxed ruthlessly on your Gross Operating Revenue. If your rental property generates £24,000 a year in rent, but your mortgage interest is £18,000, your true net profit is technically £6,000. Under Section 24, HMRC taxes you on the full £24,000. At a 40% tax bracket, your tax bill is £9,600.

- True Profit: £6,000

- HMRC Tax Bill: £9,600

- Net Result: You physically lose £3,600 of your own salary every single year just to keep the asset running.

This is the exact reason why the pros and cons of brrr property uk dictate that executing in your personal name is commercial suicide.

The Special Purpose Vehicle (SPV) Shield

To completely neutralize Section 24, 100% of elite BRRRR transactions must be executed via an SPV—a dedicated Limited Company designed exclusively to hold property. Limited Companies are fundamentally immune to Section 24. A Limited Company is taxed only on true Corporation Tax (ranging from 19% to 25% in 2026) applied directly to the net profit after all mortgage interest, bridging debt costs, and refurbishment expenses have been legally deducted.

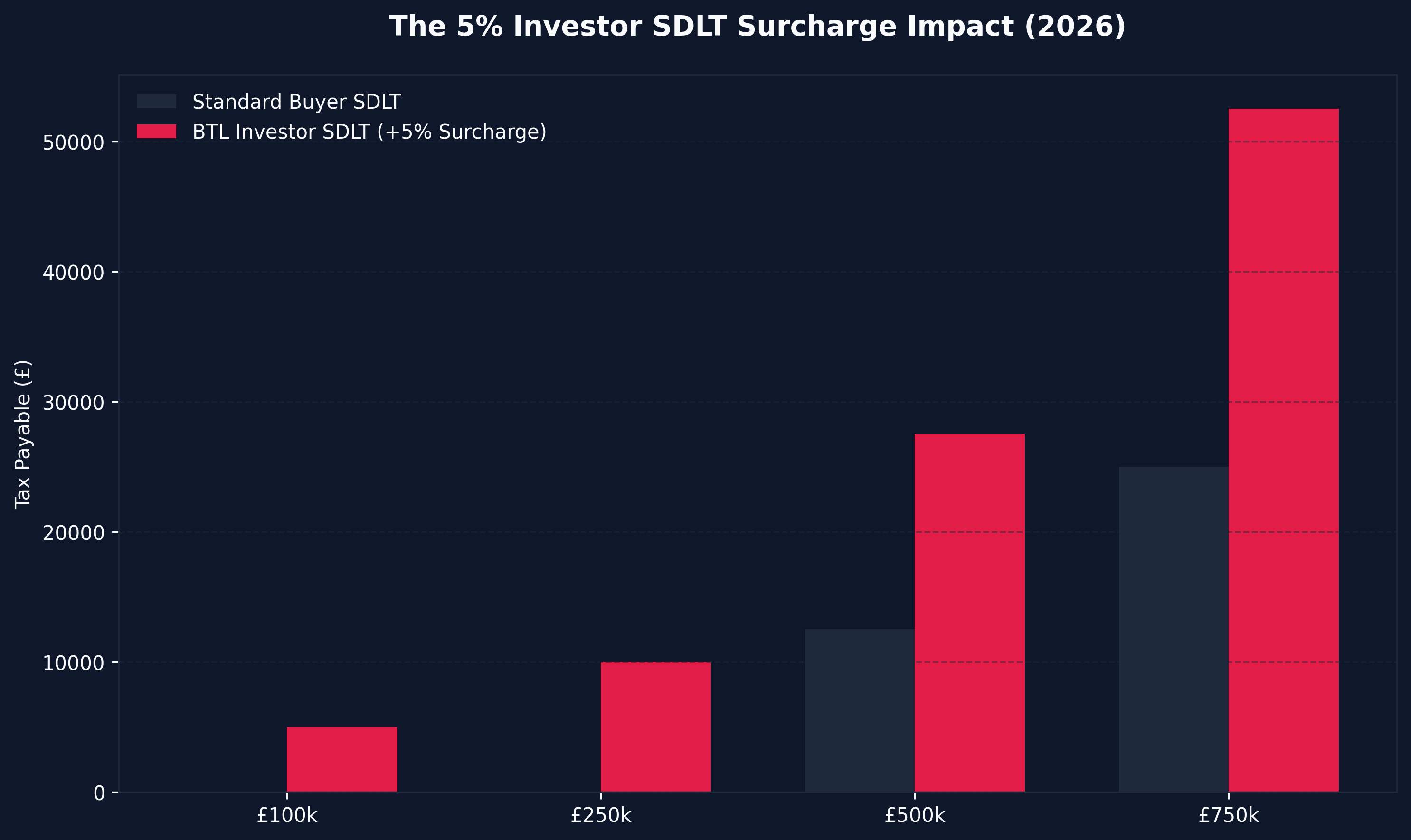

2. Stamp Duty Land Tax (SDLT): The Upfront Bloodletting

The first fiscal blow you will suffer when acquiring a distressed property for a BRRRR project is Stamp Duty Land Tax (SDLT).

Unlike a retail buyer purchasing a primary residence, a property investor operates under a punitive regime. The UK government levies an aggressive 5% Additional Property Surcharge on top of the standard SDLT rates for any buy-to-let acquisition or second home.

Crucially, executing the acquisition via a Limited Company does not grant you immunity. A Limited Company pays the 5% surcharge on its very first property purchase. There is no £125,000 tax-free allowance for corporate property investors. We highly recommend utilizing our advanced stamp duty buy to let calculator to stress-test these exact numbers before committing to an acquisition.

The 2026 Surcharge Brackets (England & NI)

When acquiring a distressed BRRRR asset, the SDLT is calculated linearly:

- £0 to £125,000: 5% Taxed

- £125,001 to £250,000: 7% Taxed (2% Standard + 5% Surcharge)

- £250,001 to £925,000: 10% Taxed (5% Standard + 5% Surcharge)

If you are an overseas investor or British expat attempting a BRRRR from abroad, you must add an additional 2% Non-UK Resident Surcharge. For overseas buyers, the lowest possible entry bracket is a staggering 7%.

How to Mitigate SDLT in BRRRR

While the 5% surcharge is difficult to escape, elite operators deploy specific structural tactics:

- Commercial / Mixed-Use Purchases: If you purchase a high-street shop with a dilapidated flat above it (a mixed-use asset), it is classed as commercial. Commercial SDLT rates apply, which entirely strips away the 5% residential surcharge. The maximum commercial SDLT rate is capped at just 5%.

- Multiple Dwellings Relief (MDR): (Note: Heavily restricted/abolished pending 2026 Chancellor reviews, always consult a tax advisor). Historically, purchasing multiple properties allowed investors to average out the purchase price to lower the overall SDLT band.

- The Rule of Six: Purchasing six or more distressed residential units from a single vendor in one transaction automatically categorizes the portfolio as commercial, totally removing the 5% residential surcharge.

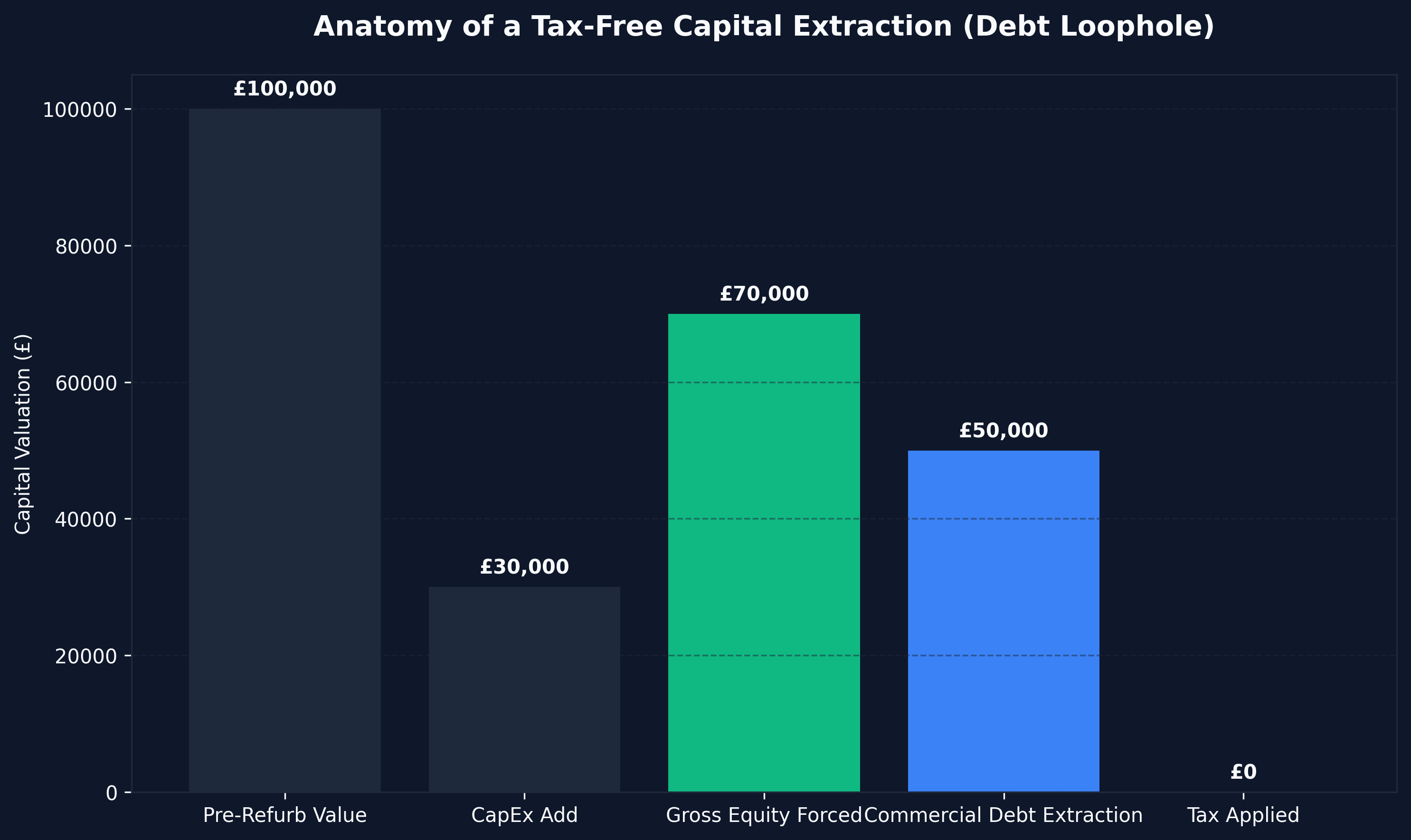

3. Capital Gains Tax (CGT) and The Extraction Loophole

The most poorly understood element of the taxes on brrr property uk 2026 matrix is Capital Gains Tax (CGT), specifically regarding the "Refinance" phase of the BRRRR cycle.

Amateurs frequently ask: "If I buy a house for £100k, spend £30k on it, and the bank values it at £200k... do I pay tax on that £70,000 of forced profit?"

The definitive answer is no. This is the absolute engine of the BRRRR strategy. You do not pay Capital Gains Tax, Income Tax, or Corporation Tax on the £70,000 of equity you forced into the asset, and you do not pay tax when you extract that cash via a commercial mortgage.

Why is Capital Extraction Tax-Free?

When you refinance the property, the bank is giving you a £150,000 (75% LTV) commercial mortgage. You are taking on debt, not income. In the eyes of HMRC, borrowing money from a commercial institution is not a taxable event. You simply use the £150,000 mortgage to pay off your £80,000 bridging loan, and the £70,000 left over is wired directly into your Limited Company bank account.

That £70k is 100% tax-free, liquid capital that you immediately deploy into buying business with no money or executing BRRRR property number two.

When DOES Capital Gains Tax Apply?

CGT (or Corporation Tax on chargeable gains if in an SPV) is only triggered upon a disposal event. If you decide you hate being a landlord and you physically sell the £200,000 house on the open market, you have crystallized the gain. HMRC will meticulously calculate the difference between your acquisition/refurbishment costs and the final sale price, and tax the profit.

In an SPV, this is taxed at the Corporation Tax rate. In a personal name, it is taxed at the residential Capital Gains Tax rates (historically 18% for basic rate, 24% for higher rate taxpayers, subject to Chancellor alterations). The core philosophy of BRRRR is to never sell. You simply hold the asset, let inflation erode the commercial debt, and continuously extract equity every 5 to 7 years.

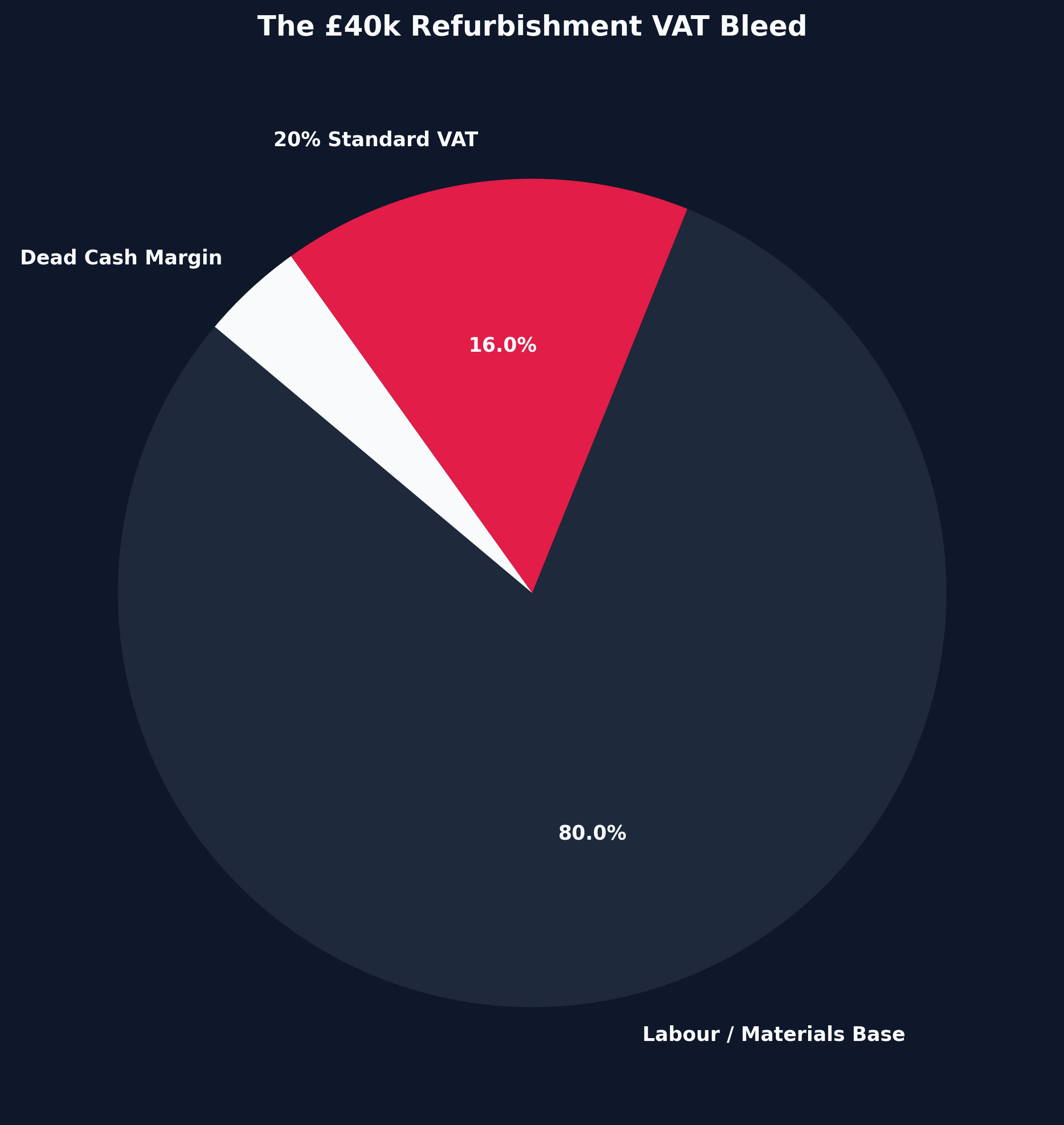

4. VAT on CapEx and Refurbishment Costs

The "Refurbish" phase of the BRRRR strategy requires immense capital expenditure. You are ripping out walls, rewiring, and installing state-of-the-art kitchens. A brutal hidden tax is Value Added Tax (VAT). In the UK, standard building work is heavily taxed at the standard VAT rate of 20%.

If your contractor quotes you £40,000 for the heavy refurbishment, you must prepare to pay £48,000 once VAT is applied. That extra £8,000 is entirely unrecoverable for a standard residential landlord. A residential property company cannot register for VAT to reclaim the cost of building materials because residential rent is an "exempt" supply. That £8,000 is directly deducted from your "Cash Left In" metric, severely limiting your ability to scale.

VAT Mitigation Strategies: The 5% Loophole

If you are executing advanced, highly distressed BRRRR strategies, you can access the powerful 5% VAT reduction threshold.

- Empty Property Relief: If you purchase a property that has been definitively empty and unoccupied for over two chronological years, you can legally command your main contractors to charge you only 5% VAT on the vast majority of the building labour and materials.

- Change in Number of Dwellings: If you purchase a massive 5-bedroom house and physically convert it into three separate 1-bedroom apartments, the construction work required to execute that conversion qualifies for the heavily reduced 5% VAT rate.

- Commercial to Residential Conversions: Permitted Development Rights (PDR) allow you to convert abandoned office buildings into residential apartments. This construction work also legally qualifies for the 5% VAT threshold.

If you execute a £50,000 commercial-to-residential refurbishment, dropping the VAT rate from 20% down to 5% instantly saves you £7,500 in hard, liquid cash.

5. Wealth Extraction: Getting Cash OUT of the SPV

The ultimate bottleneck in the taxes on brrr property uk 2026 framework occurs once the BRRRR is generating cash. You successfully executed the strategy via a Limited Company. The corporate SPV is shielding you from Section 24, and the HMO is generating £2,000 a month in net profit.

That money belongs to the company, not you personally. If you attempt to transfer that cash into your personal bank account to buy a Ferrari, HMRC will hit you with devastating Dividend Tax or Income Tax.

Strategy 1: The Director's Loan Repayment (Tax-Free)

When you initially bought the property, you physically transferred your personal savings (e.g., £50,000) into the SPV to fund the deposit and refurb. You did not "give" the company the money; you legally loaned it the cash via a Director's Loan Account (DLA).

Therefore, when the property is generating rental profit, or you extract £50,000 via a commercial refinance, the Limited Company can legally "repay" the loan back to you. Repaying a debt is not income. It is 100% tax-free. You can pull the first £50,000 of profit out of the company without paying a single penny in personal income tax.

Strategy 2: Dividend Engineering

Once the DLA is fully repaid, extracting further cash incurs Dividend Tax. Elite investors leave the cash inside the SPV. They utilize the corporate profit to fund the deposit for the next BRRRR property, creating a totally enclosed, highly efficient holding company structure that compounds wealth entirely outside the corrosive grip of personal income tax.

Alternatively, if you require the lifestyle income but want to entirely bypass the operational and fiscal friction of running a Limited Company BRRRR structure, the mathematical pivot is syndication. By deploying capital into real estate venture capital uk, you participate in the algorithmic returns of elite developers, structured through tax-efficient institutional frameworks, without ever touching a bridging loan or dealing with an HMRC SPV audit.

Conclusion: The BRRRR Tax Matrix

The BRRRR strategy is not a "get rich quick scheme"—it is a complex, hyper-leveraged commercial banking operation.

If you understand the taxes on brrr property uk 2026, you recognize that the true power of the strategy lies not just in forced appreciation, but in its ability to generate vast sums of tax-free liquidity via debt extraction. By shielding rental income in an SPV, hunting for 5% VAT conversion loopholes, and weaponizing the Director's Loan Account, you construct an impregnable algorithmic wealth engine.

Failure to respect this architecture results in punitive SDLT surcharges, severe bridging attrition, and total Section 24 annihilation. If you cannot underwrite the tax, you cannot execute the extraction.

2026 FAQs: Resolving Complex BRRRR Taxation

Do I pay Corporation Tax on the extracted refinance cash?

No. Corporation tax is paid on the net profit generated by the rental income (after deducting mortgage interest and management fees). Extracting £50,000 from the property via a commercial remortgage is classed as raising corporate debt. A bank loan is a liability, not income. Therefore, you pay absolute zero Corporation Tax on the capital extracted during the "Refinance" phase.

Are bridging loan fees and interest tax-deductible?

Yes, absolutely. Bridging finance is an explicit commercial cost of executing the business model. The massive 2% arrangement fees, the expensive valuation reports, and the punitive 1% monthly interest charges are all hyper-legitimate business expenses. The SPV deducts 100% of these financing costs from your gross rental income before calculating your final Corporation Tax liability, heavily lowering your overall tax exposure.

Can I flip a BRRRR property instead of renting it out?

You can, but it completely alters the tax structure. The BRRRR strategy is designed to hold the asset and refinance. If you buy, refurbish, and immediately sell the property for a profit, you are executing a "Flip." If you flip inside an SPV, the entire profit margin is subject to Corporation Tax. If you execute a flip in your personal name, HMRC may classify you as a "Trader" rather than an investor. This means the profit is subject to harsh Income Tax (up to 45%) rather than the lower Capital Gains Tax rate. Elite investors do not flip; they refinance, extract tax-free debt, and hold the appreciating asset forever.

Stop being a landlord. Start being an investor.

Shaded Canvas introduces serious capital to vetted UK property opportunities — targeting 12–16% net returns.

Start Investing →