The Buy, Refurbish, Refinance, Rent (BRRRR) strategy is frequently heralded across social media as the unquestionable holy grail of UK property investment. Influence-peddlers pitch it as a magical framework to build a multi-million-pound property portfolio starting with virtually zero capital.

At Shaded Canvas, we do not deal in internet mythology; we deal in algorithmic, multi-million-pound commercial reality. The truth is that BRRRR is the single most mathematically potent wealth accumulation engine available in the UK residential market. It physically allows you to engineer what hedge funds classify as "Infinite ROI."

However, it is simultaneously the most ruthless, unforgiving, and operationally dangerous strategy a landlord can attempt. While standard buy-to-let investors suffer 4% yield decay, a failed BRRRR investor suffers total capital annihilation via punitive bridging debt defaults and commercial down-valuations.

If you are evaluating the pros and cons of brrr property uk for a 2026 deployment, you must fundamentally strip away the hype. This comprehensive, 3,000-word authority guide will forensically disassemble the exact mathematical advantages, the structural systemic risks, and the true operational cost of executing BRRRR in the contemporary UK market.

Part 1: The Pros of BRRR Property in the UK

Why do elite property syndicates and institutional investors universally deploy the BRRRR framework? Because when executed with dictatorial precision, the mathematical, fiscal, and operational advantages are fundamentally unmatched by any other asset class.

Pro 1: Engineering "Infinite" Return on Investment (ROI)

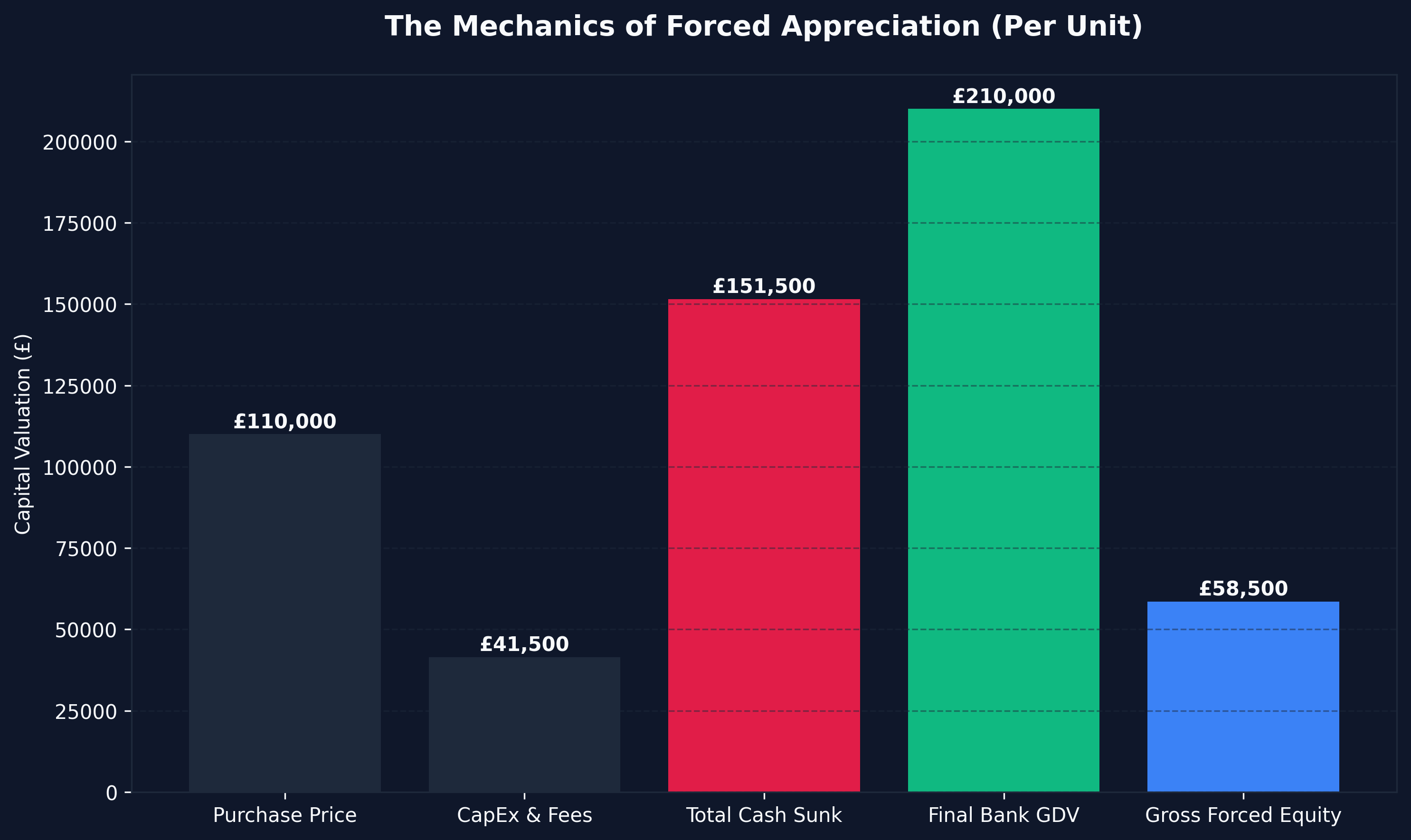

The absolute primary advantage of the BRRRR strategy is capital extraction. Traditional property investment mandates that your deposit is permanently "trapped" within the brickwork. If you buy a £200,000 house with a £50,000 deposit, that £50,000 is gone. It represents dead equity. To buy property number two, you must organically save another £50,000.

The BRRRR strategy violently circumvents this limitation. You purchase a distressed asset at a heavy discount using short-term bridging finance, force the appreciation via a heavy refurbishment, and then refinance based on the new, higher Gross Development Value (GDV).

If you execute flawlessly via a powerful brrrr strategy yield calculator uk, the new 75% LTV commercial mortgage is mathematically large enough to completely pay off the bridging debt and immediately return your initial deposit back to your bank account. When you extract 100% of your initial capital and leave £0 in the deal, your cash-on-cash return is infinitely high. Your money is free to be instantly hurled into property number two.

Pro 2: Exponential Portfolio Velocity

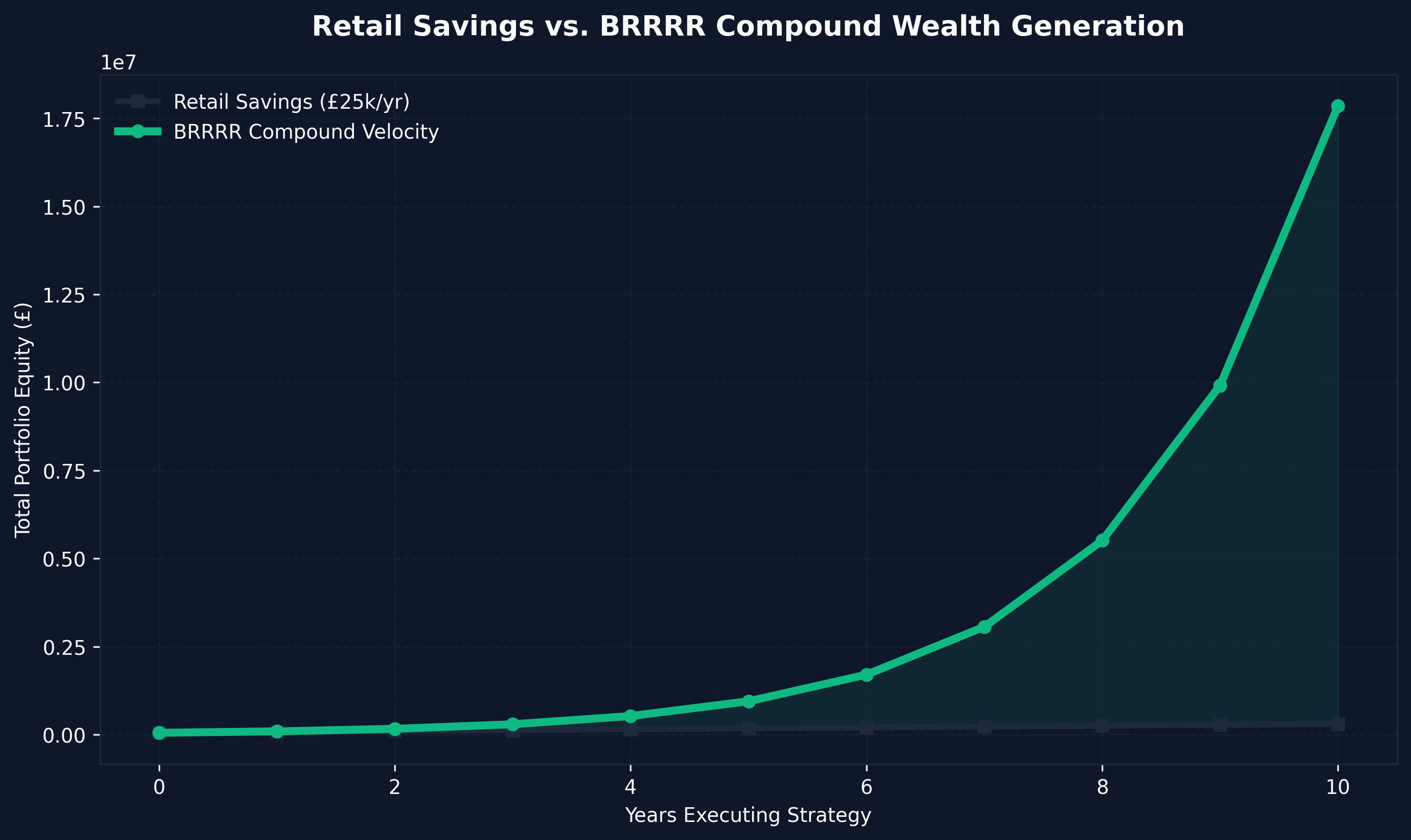

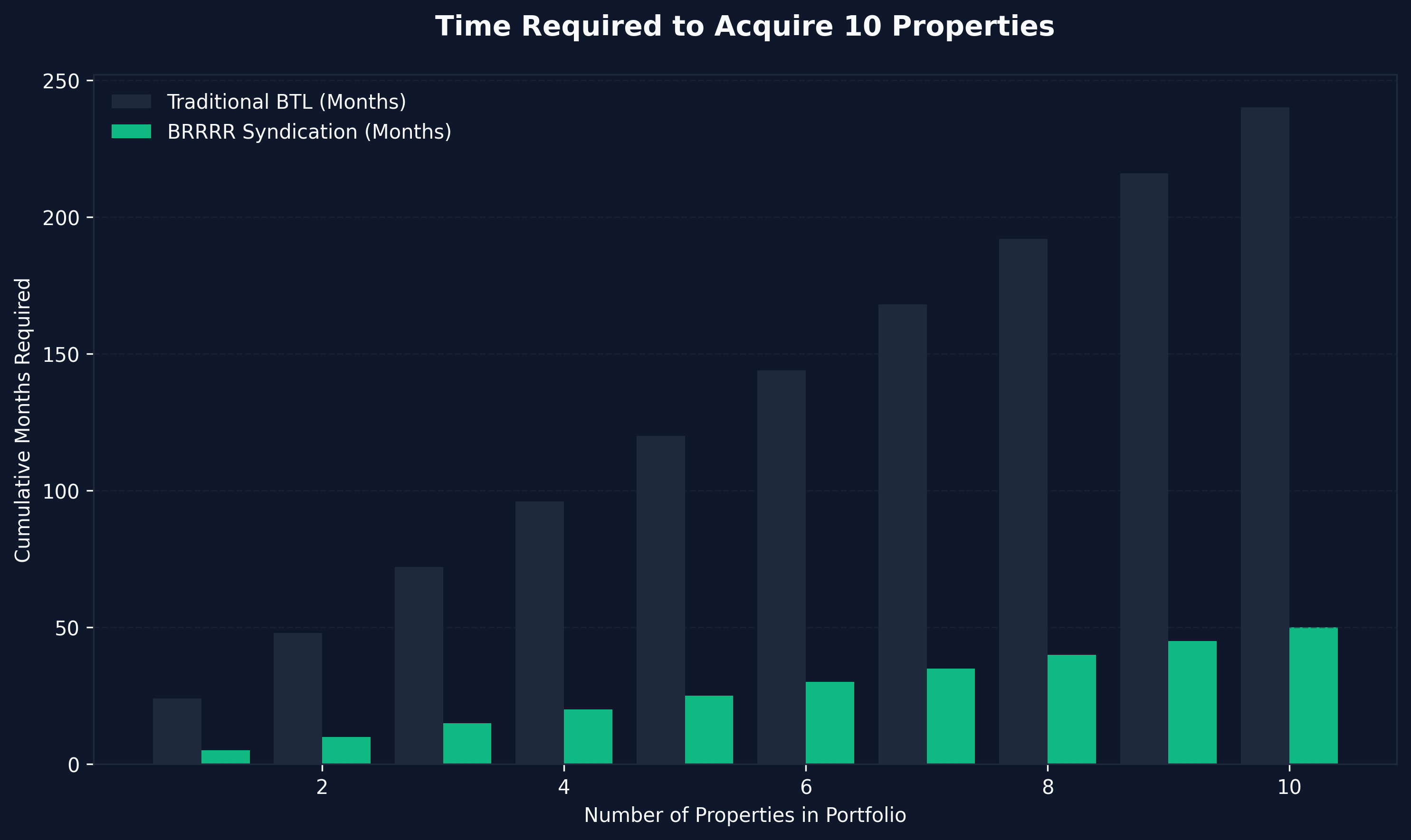

Because you are systematically recycling the exact same core capital stack, the speed at which you can scale is exponential. A traditional retail investor saving £25,000 a year from an executive salary takes twenty years to build a 10-property portfolio. A dedicated BRRRR investor utilizes one £100,000 capital stack to purchase, refurbish, refinance, and extract. They then deploy that same £100,000 three times in a single calendar year.

This velocity of money creates algorithmic, compounding portfolio growth that is entirely disconnected from your personal W-2 savings rate.

Pro 3: Total Control Over Asset Quality and EPC Ratings

In 2026, the UK government is radically enforcing Energy Performance Certificate (EPC) mandates. Most legacy Victorian buy-to-let properties are structurally obsolete, rated at EPC E or D, and will soon be entirely illegal to rent without facing catastrophic fines.

When you execute a BRRRR, you are fundamentally stripping the asset back to the brick. This grants you absolute, dictatorial control over the energy efficiency and finish. You can unilaterally install commercial-grade insulation, intelligent heating matrices, and A-rated infrastructure. The pros of brrr property uk here are twofold:

- You entirely future-proof your asset against legislative risk.

- Elite, modern, hyper-efficient homes attract elite, high-income corporate tenants who are willing to pay a heavy premium.

Pro 4: Unlocking Institutional "HMO" & Commercial Yields

The standard single-family AST will always struggle to hurdle the restrictive 125% Interest Coverage Ratios (ICR) demanded by banks. However, because you are heavily refurbishing the property during a BRRRR cycle, you possess the capability to change its fundamental use class.

Instead of flipping a 3-bedroom house back onto the generic rental market for £900 per month, the BRRRR methodology enables you to execute heavy structural modifications to transition the asset into a highly lucrative 5-bedroom House in Multiple Occupation (HMO). We comprehensively outline this yield delta in our guide on highest yielding property uk. By forcing the internal configuration into an HMO format, you instantly jack the gross rent to £2,800+ per month, utterly destroying the algorithmic restrictions of standard buy-to-let mortgages.

Part 2: The Cons of BRRR Property in the UK (The Brutal Friction)

If the pros of BRRRR are infinite wealth, the cons are sudden, systemic bankruptcy. Internet influencers deliberately omit the severe, hyper-aggressive threats that 2026’s macro-economic environment poses. Here is the uncensored reality.

Con 1: The Devastating Nature of Bridging Debt

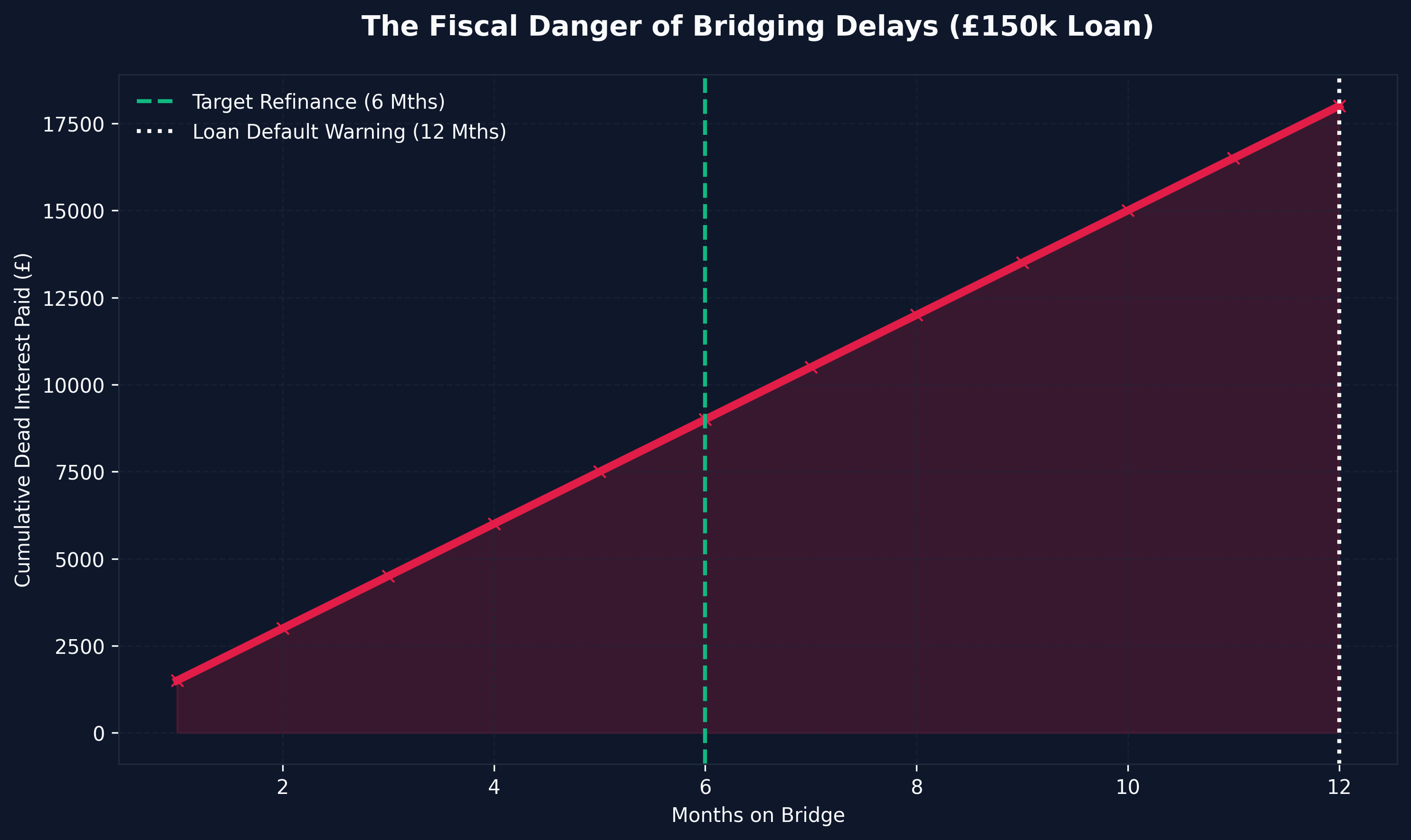

To acquire distressed, unmortgageable assets (houses without kitchens, severe structural damp), you cannot use a retail High-Street mortgage. You are forced to utilize specialized "Bridging Finance." Bridging finance is a hyper-aggressive, incredibly expensive, short-term debt instrument.

In 2026, a standard bridging loan costs roughly 1% per month in pure interest (12% per annum), alongside hefty 2% entry and exit fees. If you borrow £150,000 on a bridge, your interest bill is a catastrophic £1,500 every single month. If your contractor abandons the site, or local planning permission takes four months longer than anticipated, your profit margin is systematically bled to death. If you breach the usual 12-month loan term without refinancing, default interest rates (often 2% to 3% per month) will instantly cannibalize your equity and trigger commercial repossession.

Con 2: Operations and Supply Chain Risk (The CapEx Overrun)

Executing a heavy "back-to-brick" refurbishment is not a Saturday DIY project. It is commercial construction management. The UK is currently suffering a catastrophic shortage of elite, reliable tradesmen. Consequently:

- Labour costs have exploded.

- Raw material costs (timber, plaster, copper) are highly volatile.

- Contractors can go insolvent mid-build.

If you modeled your BRRRR assuming a £40,000 CapEx budget, and structural rot forces that bill to £60,000, that extra £20,000 is directly extracted from your personal liquid capital. It becomes "dead equity" permanently trapped in the house, fatally wounding your ability to rapidly scale the process.

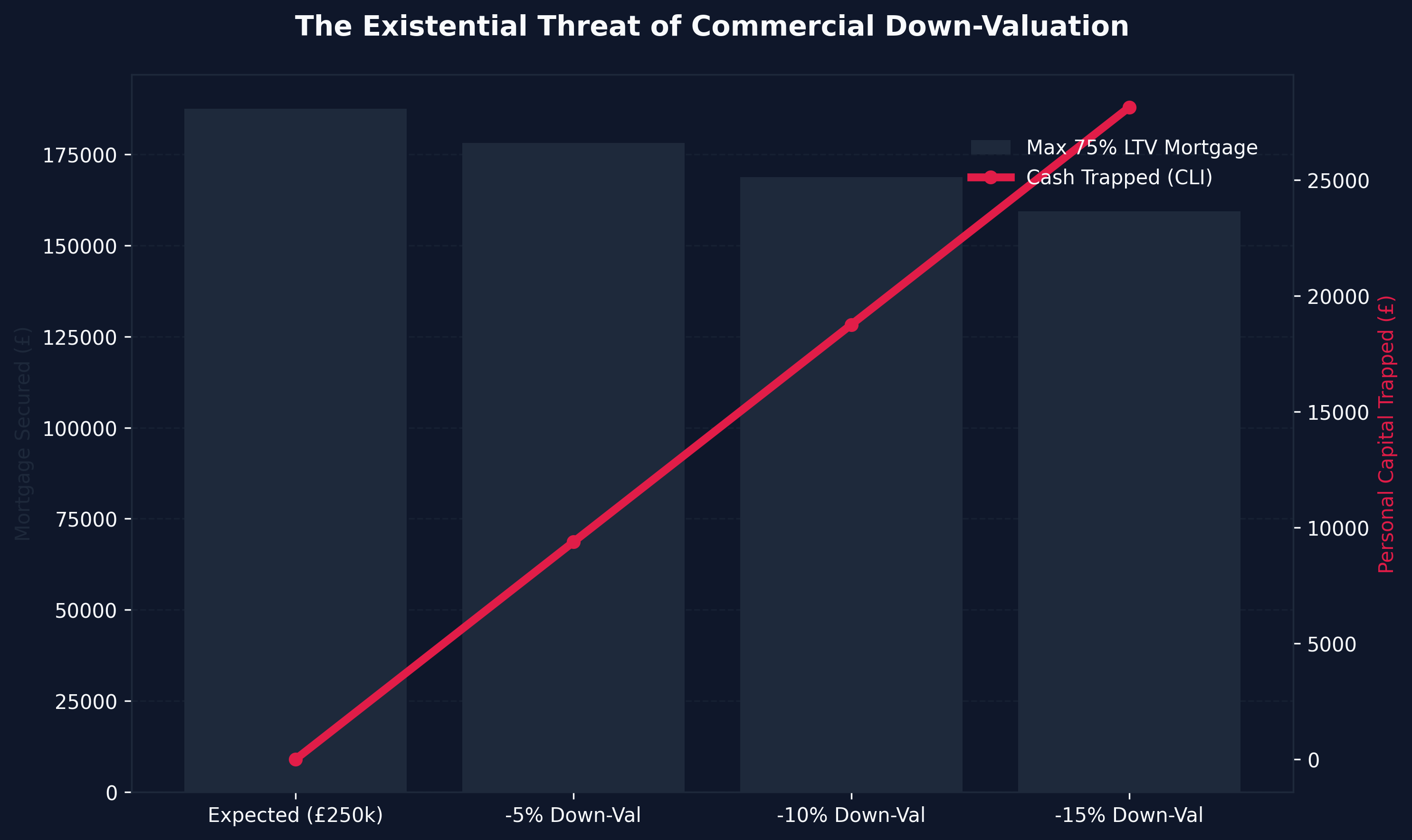

Con 3: The Existential Threat of Commercial Down-Valuation

This is the single most terrifying aspect of the pros and cons of brrr property uk matrix. The entire success of a BRRRR extraction hinges upon a bank's surveyor agreeing with your final Gross Development Value (GDV).

- Your Expectation: You finish the refurb and assume it is worth £250,000. You need to pull out a 75% LTV mortgage (£187,500) to pay off your bridging debt and extract your cash.

- The Surveyor's Reality: The surveyor arrives. They are risk-averse, highly conservative algorithmic operators protecting the bank. They decide the market is softening and rigidly "down-value" your new asset to £210,000.

- The Catastrophe: Your new 75% LTV mortgage maxes out at £157,500. This is a devastating £30,000 shortfall. You must suddenly generate £30,000 of your own liquid cash instantly just to pay off the bridging lender, leaving tens of thousands of pounds terminally trapped in the property.

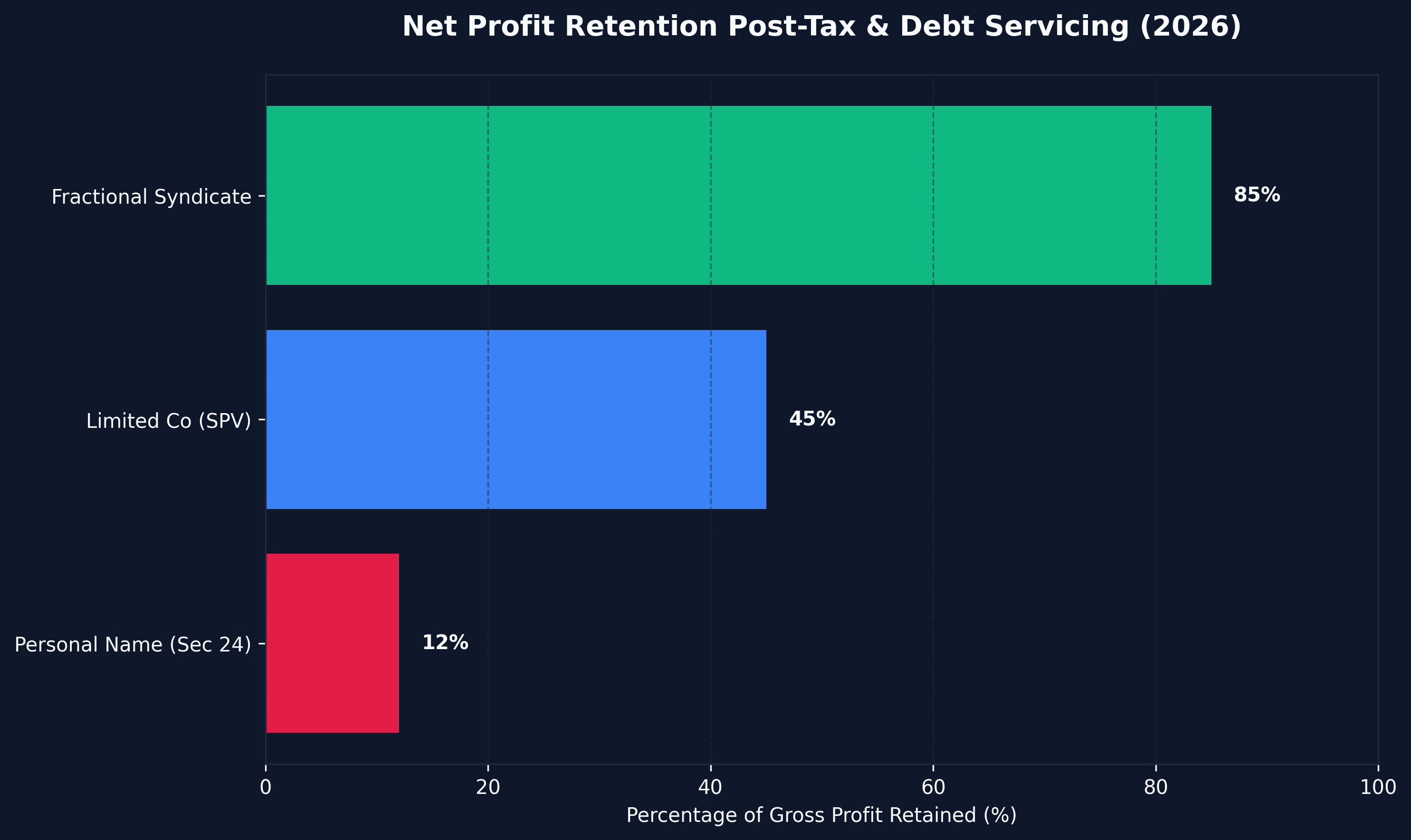

Con 4: Aggressive Taxation and Section 24

In 2026, executing a BRRRR strategy in your personal name is fiscal suicide. Under Section 24, HMRC explicitly bans you from deducting your mortgage interest payments from your rental income before calculating tax. If you execute a highly-leveraged BRRRR in your personal name, you will be violently taxed on your Gross Operating Revenue, frequently forcing higher-rate taxpayers into net negative territory.

You must execute via a specialized Special Purpose Vehicle (SPV) Limited Company. While this solves Section 24, operating a Limited Company introduces layers of friction: higher accountancy fees, punitive corporative mortgage rates, and the 5% Stamp Duty Land Tax surcharge on every single acquisition. Ensure you utilize our stamp duty buy to let calculator to model this correctly.

Part 3: The Alternative to BRRRR Risk

When analyzing the profound pros and cons of brrr property uk in the current climate, many institutional and high-net-worth individuals realize the active operational risk is simply too intense.

BRRRR demands that you act as a full-time acquisition manager, debt structurer, construction foreman, and surveyor negotiator.

The Low-Risk Pivot: Fractional Property Investment UK

If you desire the immense, algorithmic yields of commercial property, but refuse to assume the £800-per-month bridging risk, the risk-adjusted alternative is fractional syndication. As outlined in our masterguide on what is a property syndicate uk, fractional investing allows you to deploy capital directly alongside elite, specialized BRRRR operators.

You leverage the power of their institutional debt structures, their elite builder networks, and their ruthless off-market acquisition engines, entirely passively. Rather than risking £150,000 of your own liquid capital on a single unproven site, you allocate capital into a diversified, pre-audited fractional portfolio.

Conclusion: You Must Choose Your Path

The pros and cons of brrr property uk are definitive. If built correctly, the mathematical architecture of the BRRRR strategy generates raw, algorithmic wealth faster than any other vehicle in the United Kingdom. It unlocks infinite ROI, geometric portfolio scaling, and bulletproof EPC-rated assets.

However, it is governed by extreme fiscal violence. The threat of commercial down-valuations, catastrophic bridging attrition rates, and unpredictable CapEx spikes means the barrier to entry for amateur operators is functionally impossible to clear.

If you possess the risk tolerance, the capital buffers, and the operational ruthlessness required, you execute the BRRRR. If you prioritize algorithmic yield, capital protection, and absolutely zero operational stress, you pivot directly to fractional property investment.

FAQs: Addressing the Nuance of BRRRR

What is the strict "Six-Month Rule" in UK Refinancing?

Historically, UK lenders operated under rigid anti-money laundering frameworks that explicitly banned any investor from refinancing a property within six calendar months of its initial purchase. If you finished your BRRRR refurb in 8 weeks, you were forced into a paralyzing 4-month wait on punitive bridging finance. In 2026, elite institutional brokers bypass this by utilizing "Day-1 Refinance" commercial lenders who explicitly waive the six-month rule, provided the fundamental GDV uplift is structurally documented.

Do you pay Capital Gains Tax when you refinance during a BRRRR?

No. This is one of the most powerful elements of the strategy. When you successfully force equity and extract your capital via a commercial mortgage refinance, that extracted cash is entirely tax-free. You are simply drawing down debt against an asset; you have not triggered a taxable disposal. You only pay CGT when you physically sell the asset on the retail market.

Is BRRRR viable in London and the Southeast in 2026?

Technically possible, mathematically improbable. The BRRRR equation relies intimately on achieving high-margin gross yields to clear the strict 125% ICR stress tests demanded by commercial lenders. The hyper-inflated purchase prices in the capital fundamentally crush the percentage yields. The strategy flourishes aggressively in the Midlands, the North West, and Scotland, where the delta between the acquisition cost and the final rental ceiling is geometrically wider. Review our how to invest in property uk guide for an exact regional tier breakdown.

Stop being a landlord. Start being an investor.

Shaded Canvas introduces serious capital to vetted UK property opportunities — targeting 12–16% net returns.

Start Investing →