In the world of property investment, "Cash is King." While some investors chase capital growth in London, smart cash-flow investors are looking North, where rental yields can hit 9-11%.

Understanding where to find the highest yielding property in the UK—and more importantly, why those areas are high yielding—is critical for building a portfolio that pays you every single month.

This guide ranks the top areas for 2026, analyzes the trade-offs, and warns you about the "Yield Traps" that catch out beginners.

What is a "Good" Rental Yield?

Before we look at the map, let's define success.

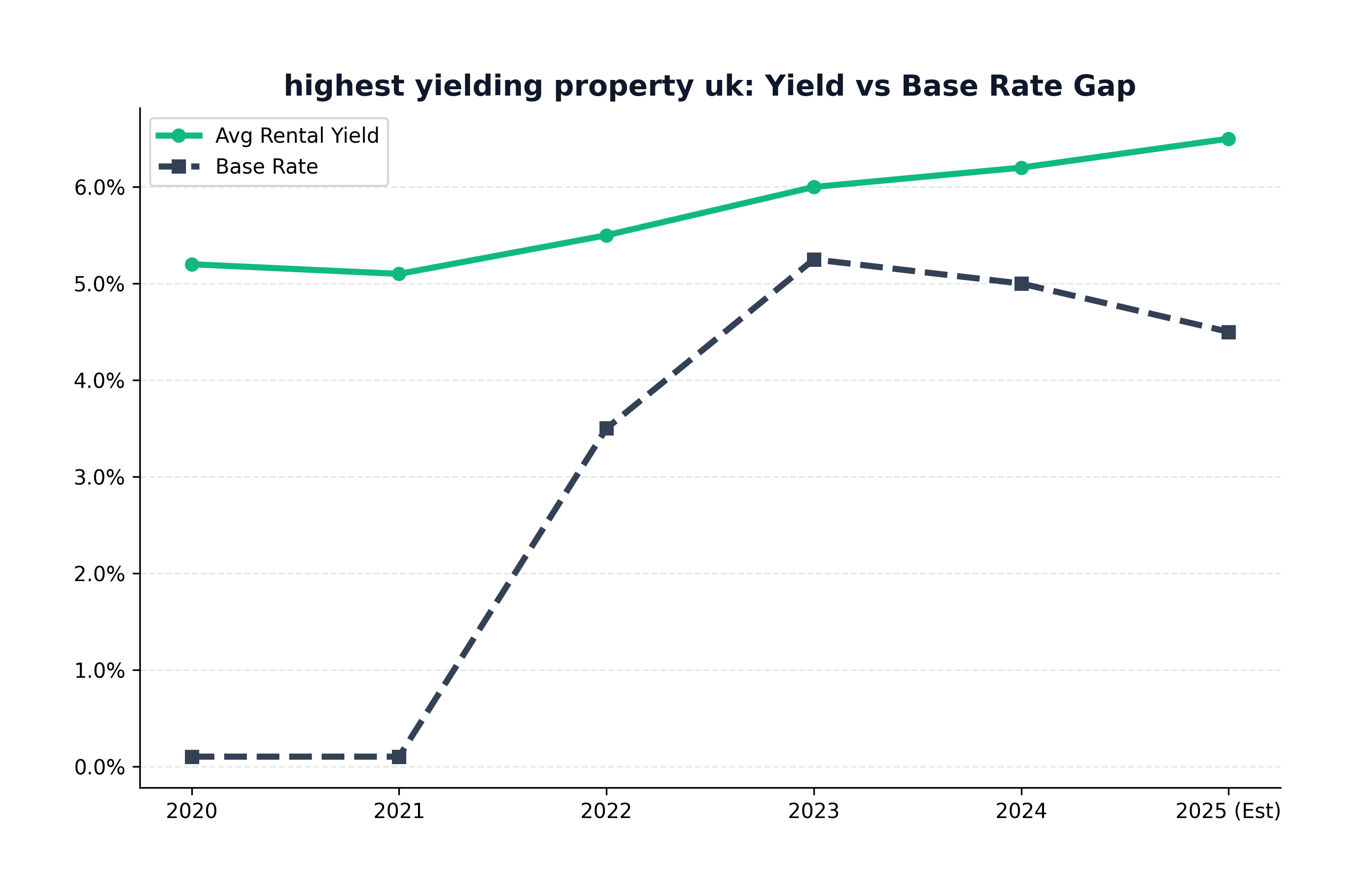

- Average UK Yield: ~5-6%

- Good Yield: 7-8%

- High Yield: 9%+

Formula: (Annual Rental Income / Purchase Price) x 100 = <a href="/post/highest-yielding-property-uk" style="color:#c9a84c;text-decoration:underline;font-weight:500"><a href="/post/highest-yielding-property-uk" style="color:#c9a84c;text-decoration:underline;font-weight:500"><a href="/post/highest-yielding-property-uk" style="color:#c9a84c;text-decoration:underline;font-weight:500"><a href="/post/highest-yielding-property-uk" style="color:#c9a84c;text-decoration:underline;font-weight:500"><a href="/post/highest-yielding-property-uk" style="color:#c9a84c;text-decoration:underline;font-weight:500"><a href="/post/highest-yielding-property-uk" style="color:#c9a84c;text-decoration:underline;font-weight:500"><a href="/post/highest-yielding-property-uk" style="color:#c9a84c;text-decoration:underline;font-weight:500"><a href="/post/highest-yielding-property-uk" style="color:#c9a84c;text-decoration:underline;font-weight:500">Gross Yield</a></a></a></a></a></a></a></a> %

Warning: This is Gross Yield. It does not include voids, maintenance, or taxes. Always calculate your Net Yield before buying.

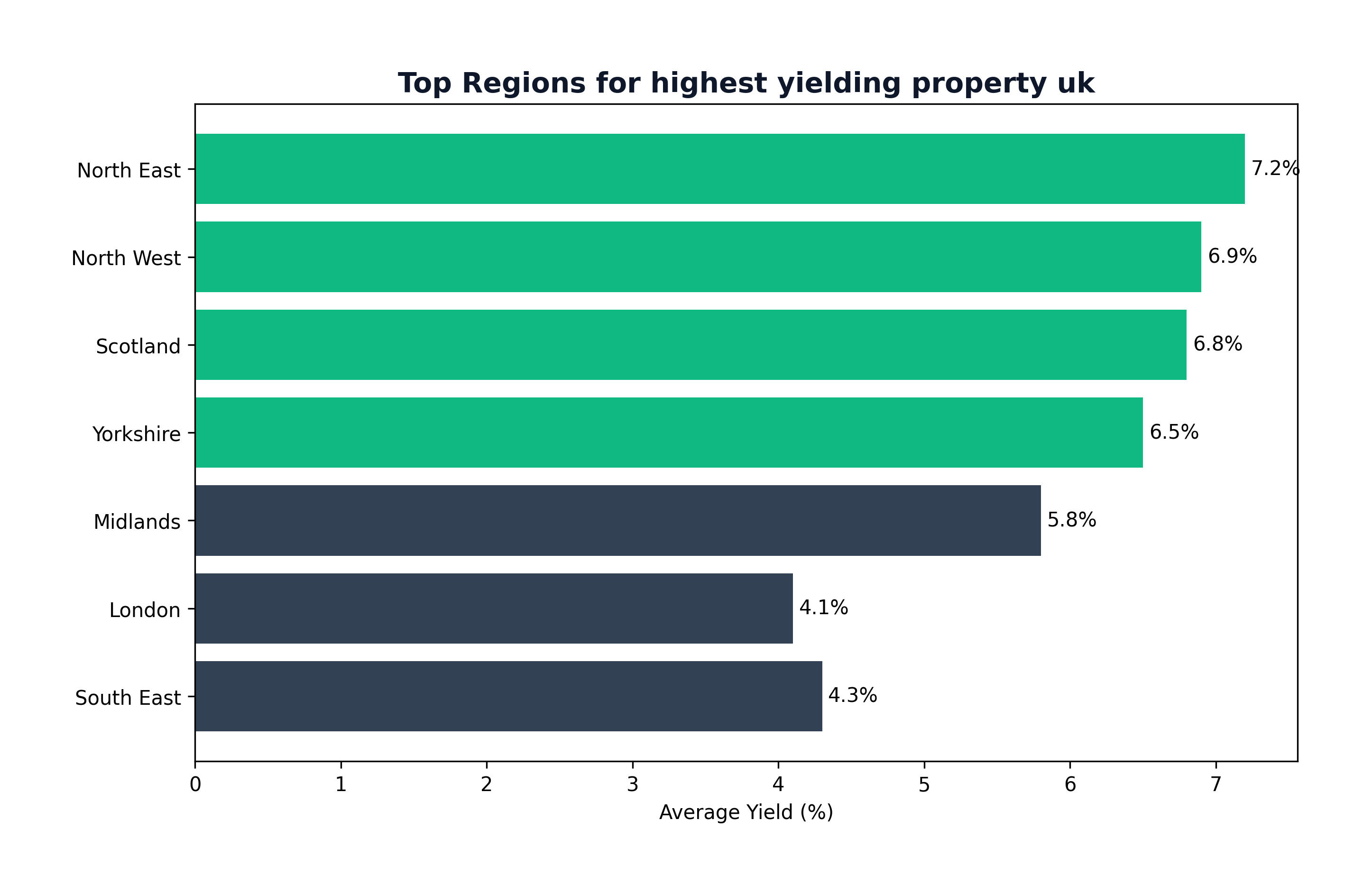

Top 5 Highest Yielding Areas for 2026

Based on current data and 2026 projections, these are the regions delivering the best cash flow.

1. Hull (HU1, HU2)

- Expected Yield: 9-11%

- Why: Ultra-low entry prices (often <£100k) combined with steady demand. Hull has seen significant regeneration, but prices haven't caught up yet.

- Risk: Capital growth has historically been slow.

2. Bradford (BD1)

- Expected Yield: 8-10%

- Why: A city undergoing a makeover. With its "City of Culture 2026" status, investment is pouring in. Large student population creates HMO opportunities.

- Risk: Specific streets can vary wildly in quality. Local knowledge is essential.

3. Liverpool (L1, L6, L7)

- Expected Yield: 7-9%

- Why: The "Goldilocks" zone. Liverpool offers high yields and strong capital growth potential (~6-8% forecasted). L7 (Kensington) is a student HMO powerhouse.

- Risk: Article 4 directions limit new HMO conversions in many areas.

4. Sunderland & North East

- Expected Yield: 8-9%

- Why: Similar to Hull, favorable price-to-rent ratios. Large manufacturing base (Nissan) and university drive tenant demand.

- Risk: Economic dependence on specific industries.

5. Glasgow (G1, G4)

- Expected Yield: 7-9%

- Why: Shortage of student accommodation has driven rents up massively.

- Risk: Scotland's tenancy laws (no fixed terms, rent caps) are stricter than England's.

The "Yield vs. Growth" Debate

Why doesn't everyone buy in Hull? Because High Yield often correlates with Lower Capital Growth.

- London: Low Yield (3-4%), High Growth Potential.

- North East: High Yield (9%), Lower Growth Potential.

The Strategy: If you need income now to replace your salary, prioritize yield (The North). If you have a high salary and want to build long-term wealth for retirement, prioritize growth (The South / Major Cities).

Investors often start with high-yielding properties to build a "war chest" of cash flow, then diversify into growth assets later.

The "Yield Trap": Beware of Cheap Houses

You see a 3-bed terrace in Burnley for £50,000. It rents for £500/pcm. That’s a 12% yield! Amazing, right?

Not always.

- Tenant Profile: Cheap areas often attract transient tenants with unreliable income.

- Maintenance: A new roof costs the same in Burnley as it does in Birmingham. A £5,000 repair on a £50k house wipes out 2 years of profit.

- Voids: If it sits empty for 3 months, your 12% yield becomes 9%.

Rule: Never buy purely on a spreadsheet number. Investigate the fundamentals of the area options (Jobs, Transport, Crime Rate).

Conclusion: Where to Put Your Money?

For 2026, Liverpool remains our top pick for a balanced portfolio, offering 7-8% yields with genuine growth prospects. For pure cash flow hunters, Bradford and Hull are the kings of ROI.

Remember: "Gross Yield is Vanity, Net Yield is Sanity."

Next Steps:

- Calculate the Net Yield of your target area (subtract 15% for management/maintenance).

- Check if the area has an Article 4 direction (restricting HMOs).

- Visit the street at night before offering.

📚 Related Reading

- How I save nearly £2,000 a Year on Groceries for a Family of 4

- How to Reduce Taxes Legally: The UK Commercial Property Cheat Code

- The Drop Servicing Model: How I Closed a £120k Deal Without Doing the Work

- How Environment Affects Business Success

- Passive Income Property UK: How to Build a Rental Portfolio That Actually Pays You in 2026

Stop being a landlord. Start being an investor.

Shaded Canvas introduces serious capital to vetted UK property opportunities — targeting 12–16% net returns.

Start Investing →