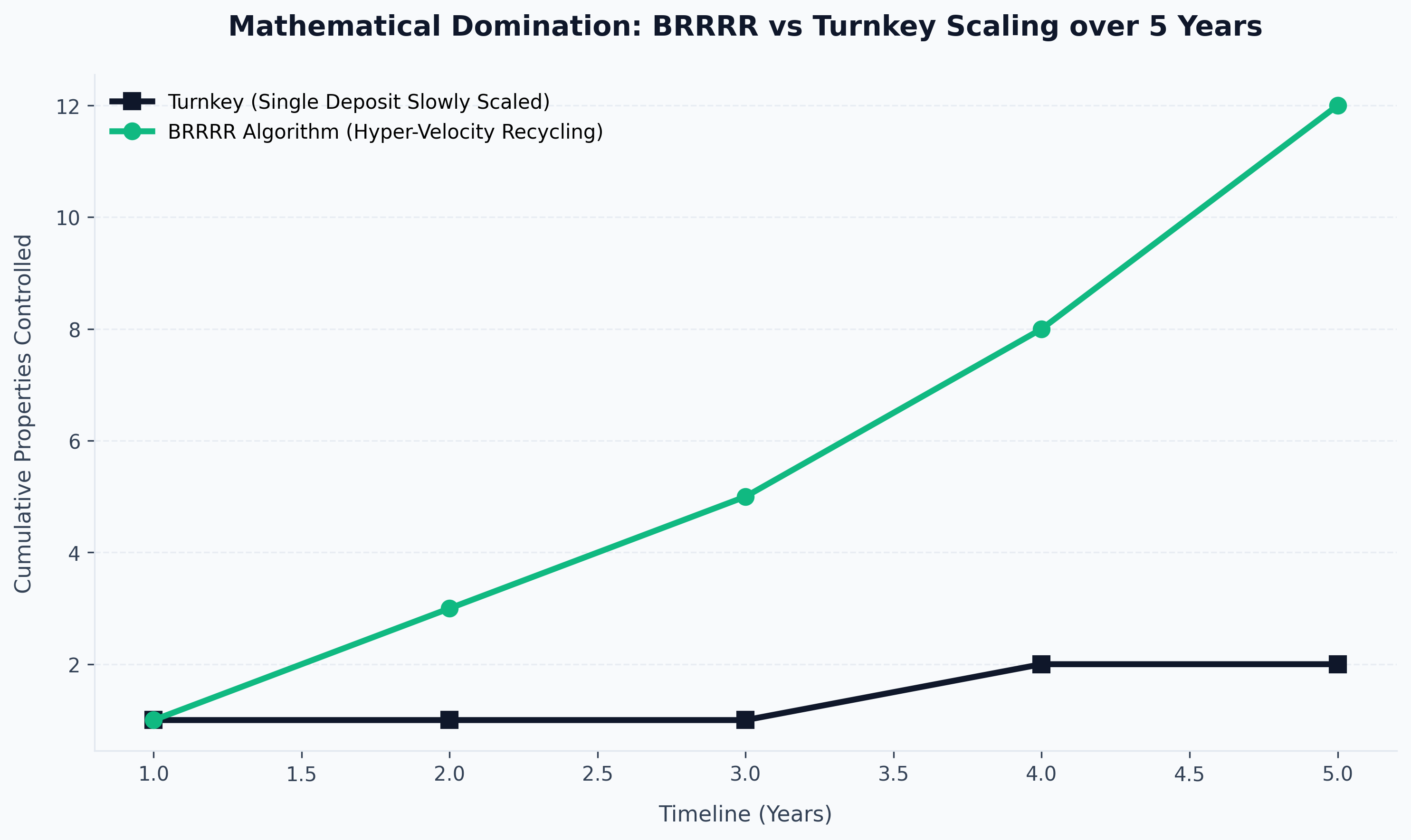

The Buy, Rehab, Rent, Refinance, Repeat (BRRRR) methodology is not simply a property acquisition technique; it is exactly how professional investors engineer algorithmic wealth. Traditional investing dictates locking your capital inside an asset for decades, helplessly praying for organic market inflation. The BRRRR strategy violently rejects this slow-motion capital death. It dictates the aggressive, systemic extraction of your liquid capital to achieve what mathematicians define as "Infinite ROI."

However, BRRRR is entirely unforgiving. If a standard buy-to-let investor miscalculates a yield, they suffer mediocre 3% annual returns. If a BRRRR investor miscalculates the mathematics around bridging finance, LTGDV stress testing, or the final commercial valuation, they systematically bankrupt themselves.

In the ruthless, high-interest-rate environment of 2026, relying on gut feeling is commercial suicide. You must possess absolute, dictatorial control over the brrrr strategy yield calculator uk. This comprehensive 2026 manual will forensically deconstruct the exact formulas, spreadsheets, and commercial underwriting logic used by elite UK property syndicates to flawlessly execute capital extraction.

2026 BRRRR Extraction Calculator

Simulate real-world capital extraction including bridging attrition and LTGDV stress tests.

1. Acquisition & Refurb

2. Finance & Strategy

Algorithmic Post-Mortem

1. The Core Metrics: Gross Yield vs. The BRRRR Mathematics

Before we deploy aggressive bridging finance into a distressed asset, we must violently decouple your mindset from the amateur concept of "Gross Yield."

If you ask an estate agent regarding the viability of a property, they will quote Gross Yield. (Annual Rent / Purchase Price) x 100. This is a useless, two-dimensional metric designed to sell overpriced apartments. It ignores the cost of debt, the taxation reality of Section 24, management friction, bridging costs, and crucial refurbishment capital.

The BRRRR strategy utilizes entirely distinct, advanced commercial metrics:

1. The LTGDV (Loan to Gross Development Value)

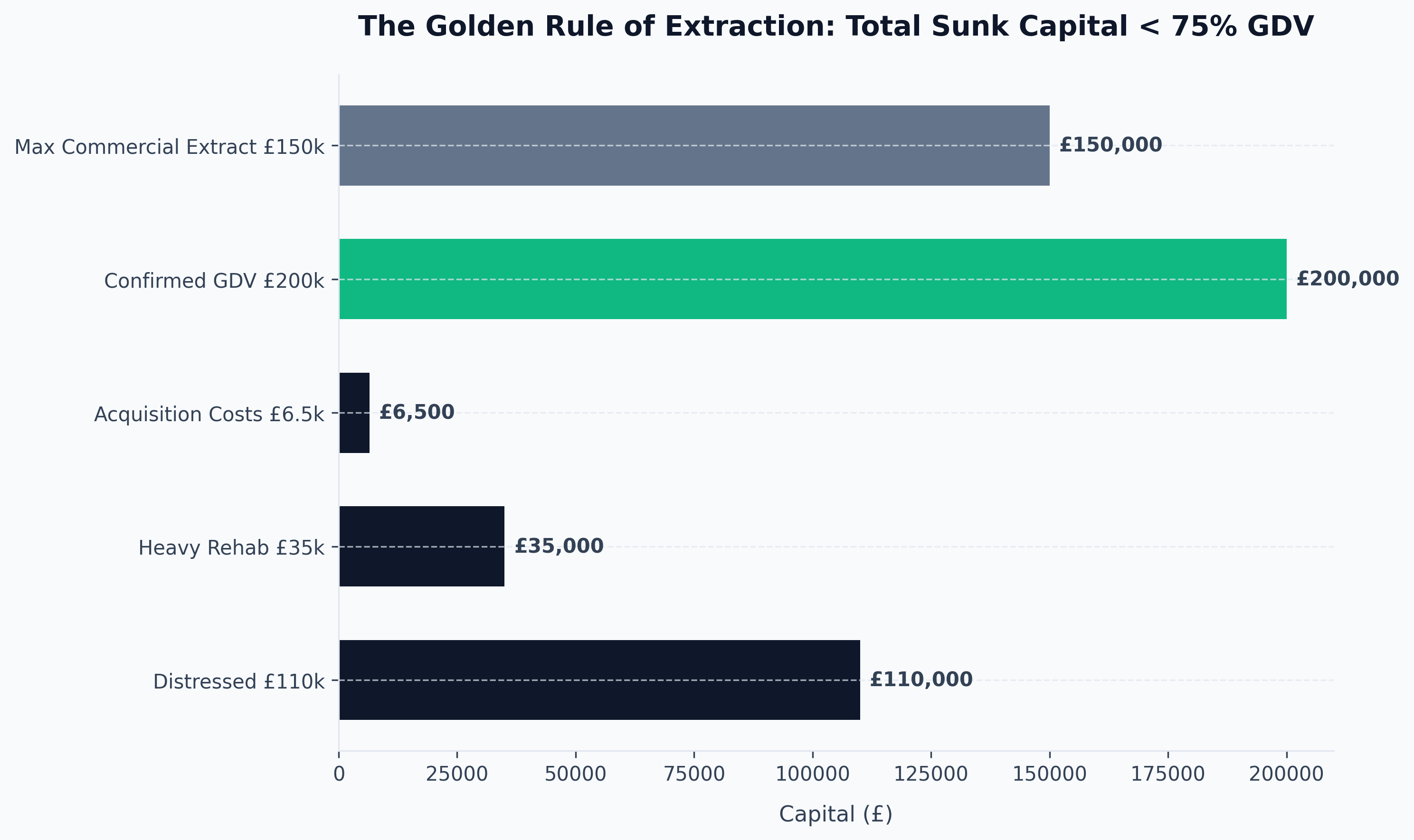

Bridging lenders do not care what the £100,000 distressed wreck is currently worth; they care what the final end product is mathematically worth once your £30,000 refurbishment is completed. This end figure is the Gross Development Value (GDV). To successfully execute a BRRRR, the final, long-term commercial mortgage you secure must be large enough to completely pay off the expensive short-term bridging loan used to acquire the asset. UK lenders strictly cap commercial BTL mortgages at 75% LTV. Therefore, your absolute golden rule is: Your Purchase Price + Buying Costs + Refurbishment Costs must fundamentally equal less than 75% of the final GDV.

2. Cash Left In (CLI)

This is the single most vital metric in the entire brrrr strategy yield calculator uk. The CLI is the exact numeric value of your personal liquid cash that remains permanently trapped in the bricks after the final refinancing event.

- A Failed BRRRR: You leave £35,000 trapped in the deal. You lack the capital to repeat the process.

- A Successful BRRRR: You leave £5,000 trapped in the deal.

- A Legendary BRRRR (Infinite ROI): You extract 100% of your capital, plus additional tax-free cash. Your personal CLI is £0, yet you control a massive cash-flowing asset.

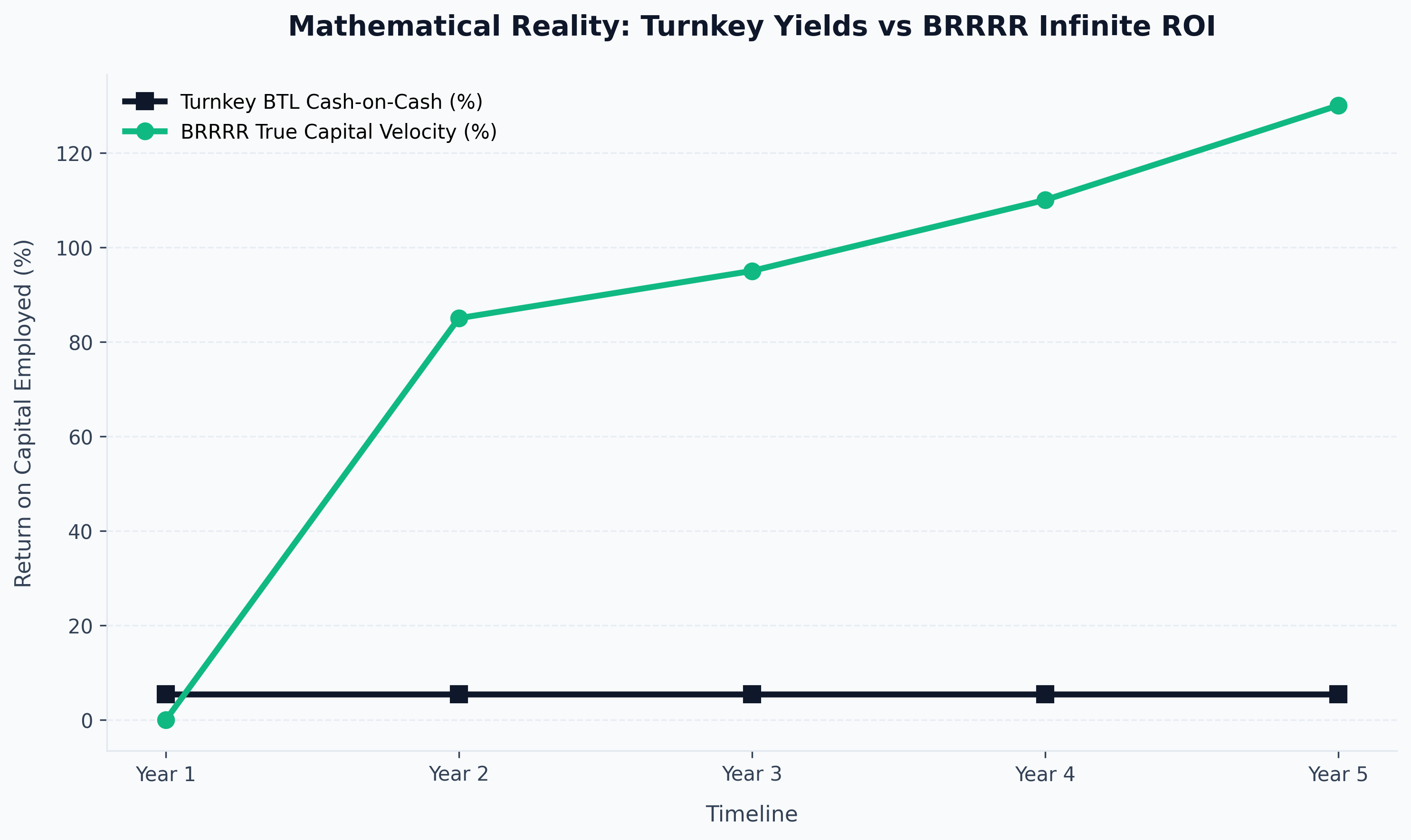

3. Return on Capital Employed (ROCE) / Cash-on-Cash Return

If you execute a near-perfect BRRRR and leave only £2,000 in the deal (your CLI), and the property generates £200 a month in net profit (£2,400 annually), your Cash-on-Cash return is not 6% or 8%. It is a staggering 120% per annum. You double your remaining liquid capital every single year.

2. Deconstructing the BRRRR Algorithm (The 2026 Formula)

We will now drag these theoretical concepts into the brutal reality of the 2026 UK market. We will execute a forensic, step-by-step breakdown using a theoretical brrrr strategy yield calculator uk to model a standardized acquisition in the Northern Powerhouse.

Step 1: The Distressed Acquisition (Buying Well)

You locate a heavily dilapidated 3-bedroom semi-detached house in Sheffield. It lacks a valid EPC, has severe penetrative damp, and requires a full rewire. A traditional retail buyer cannot secure a standard mortgage due to the lack of a functional kitchen.

- Estate Agent Asking Price: £140,000

- Your Aggressive Cash/Bridging Offer: £110,000 (Accepted)

- Estimated Refurb Cost (CapEx): £35,000

- Acquisition Sunk Costs (Stamp Duty, Legals, Broker Fees): £6,500

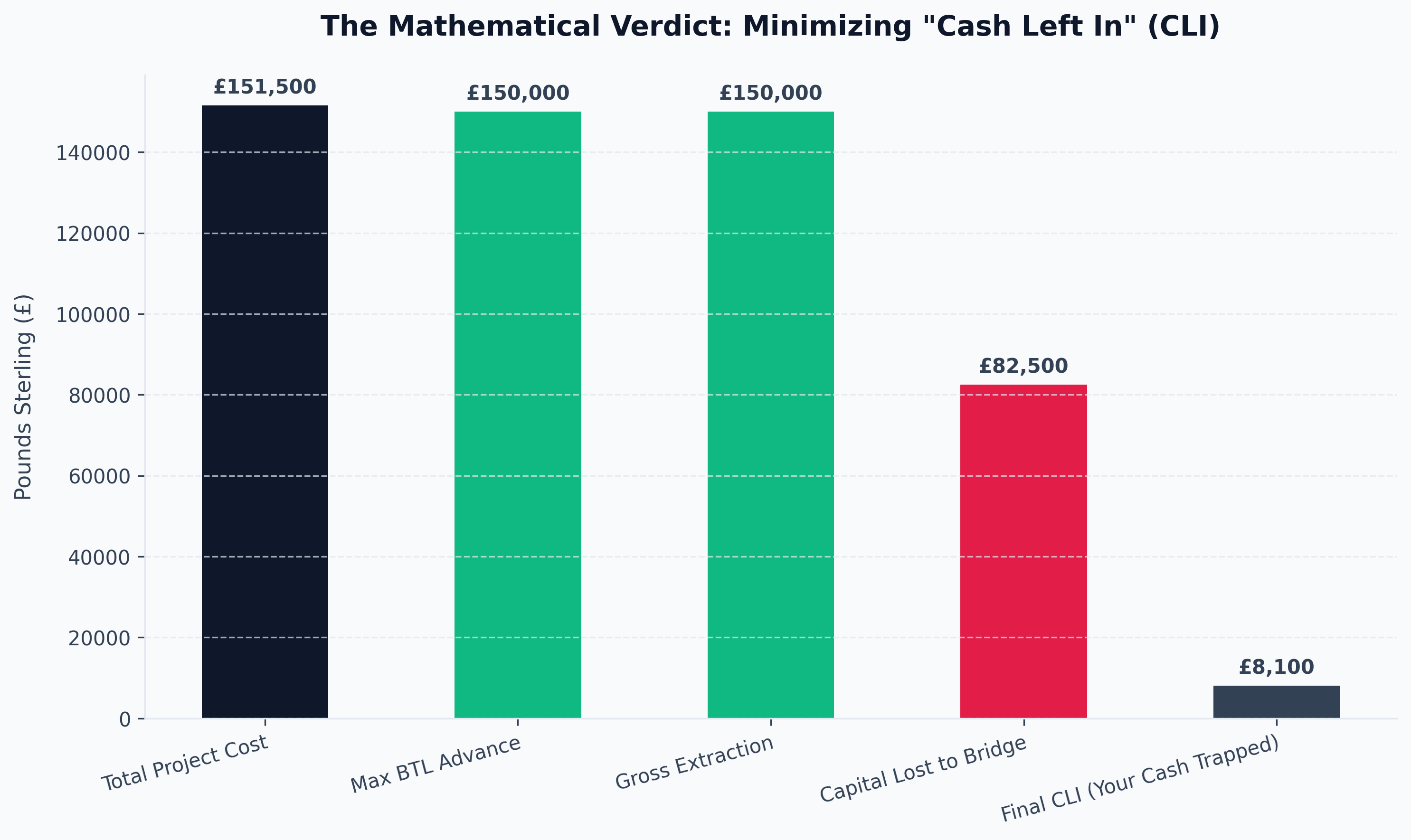

- Total Capital Required to Complete the Project: £151,500

(Crucially, before deploying £1, you utilized historical Land Registry sold data and local surveyor comparables to definitively lock in the target end valuation (GDV). You are 100% historically certain this street supports £200,000 valuations for fully modernized stock).

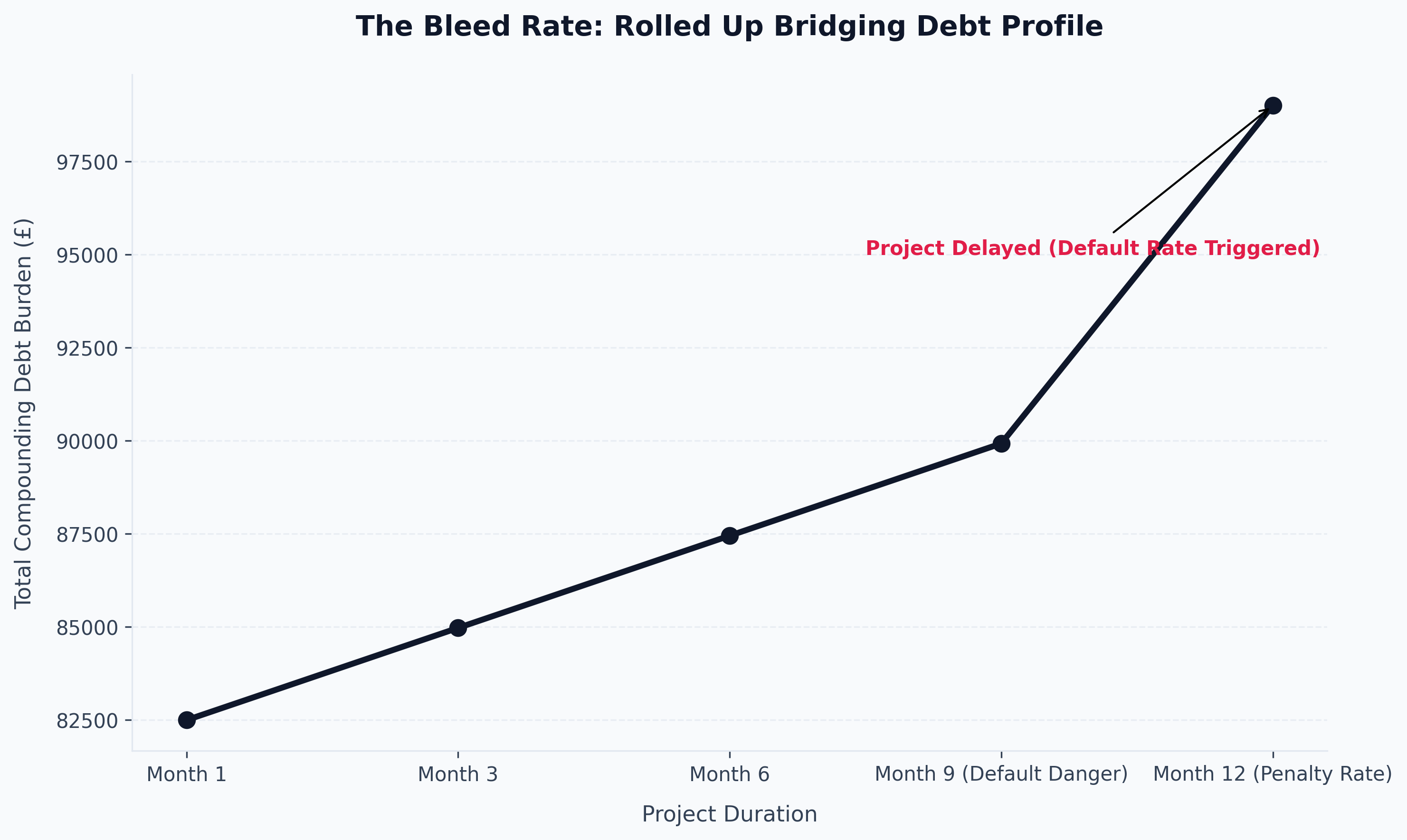

Step 2: The Bridging Debt Execution

You are not deploying £151,500 of your own cash. You utilize specialized, short-term bridging finance. The bridging underwriter offers you an aggressive 75% LTV against the day-one distressed valuation of £110,000.

- Gross Bridging Loan Secured: £82,500

- Lender Arrangement Fee (2%): -£1,650

- Retained Interest (1% per month for 6 months): -£4,950

- Net Loan Disbursed to Your Solicitor: £75,900

You utilize the £75,900 from the bridge, meaning you must physically transfer the remaining £75,600 of your own liquid cash to complete the purchase, pay the fees, and fund the heavy £35,000 refurbishment. Your cash is now dangerously exposed and entirely trapped in a building site.

Step 3: The Refurbishment and Rent Engineering

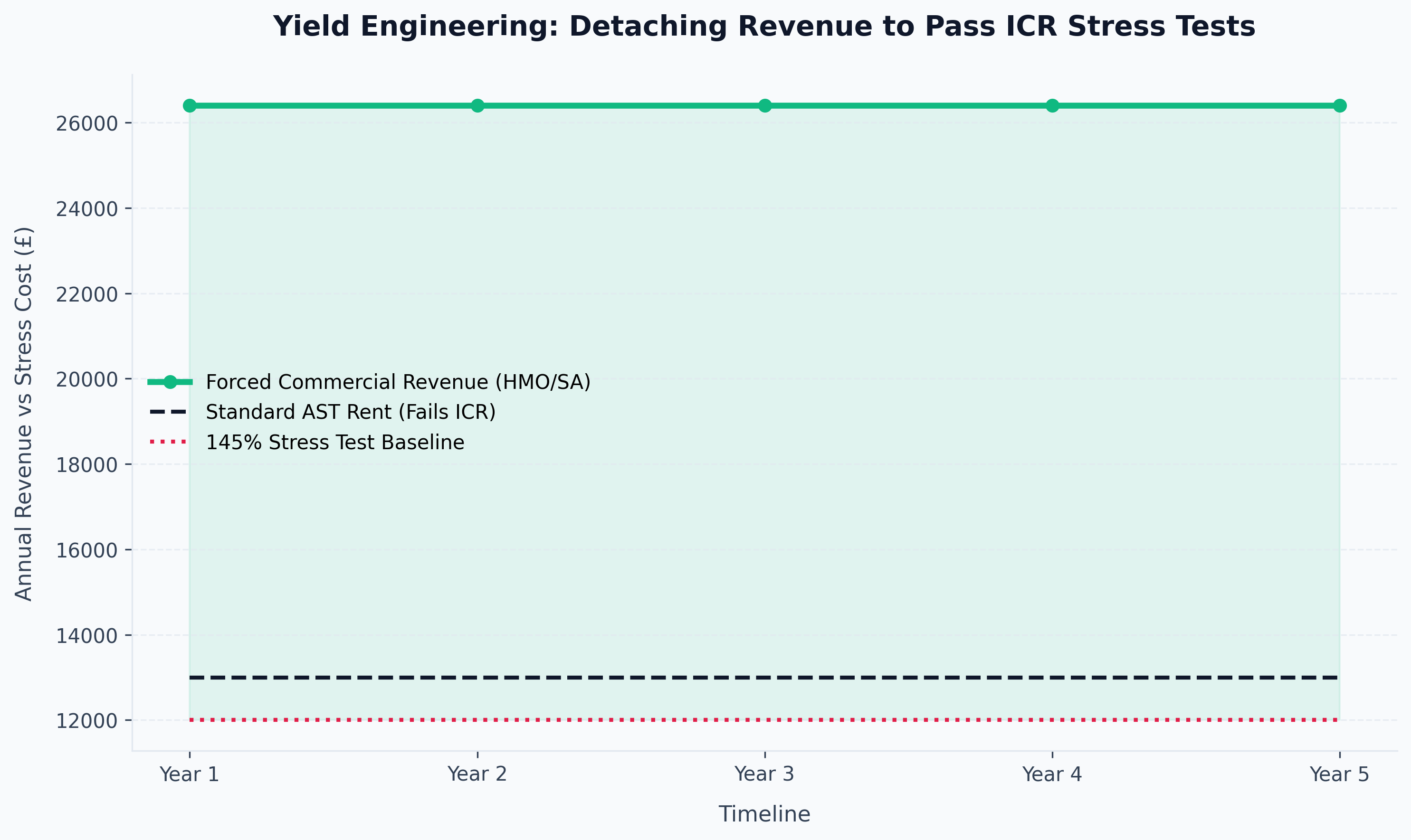

Over the next 12 weeks, your build teams aggressively execute the project. The damp is rectified, the property is stripped to the brick, rewired, and heavily insulated to exceed the impending 2028 EPC 'C' mandates. To force the final commercial valuation as high as mathematically possible, you do not rent it as a standard family home. You convert the downstairs reception room, securing HMO licensing to legally operate it as a 4-bedroom professional HMO.

Instead of generating £950 per month on a single AST, the 4 rooms rent for £550 each, yielding £2,200 per month (£26,400 gross per annum).

Step 4: The Refinance and Capital Extraction (The Magic)

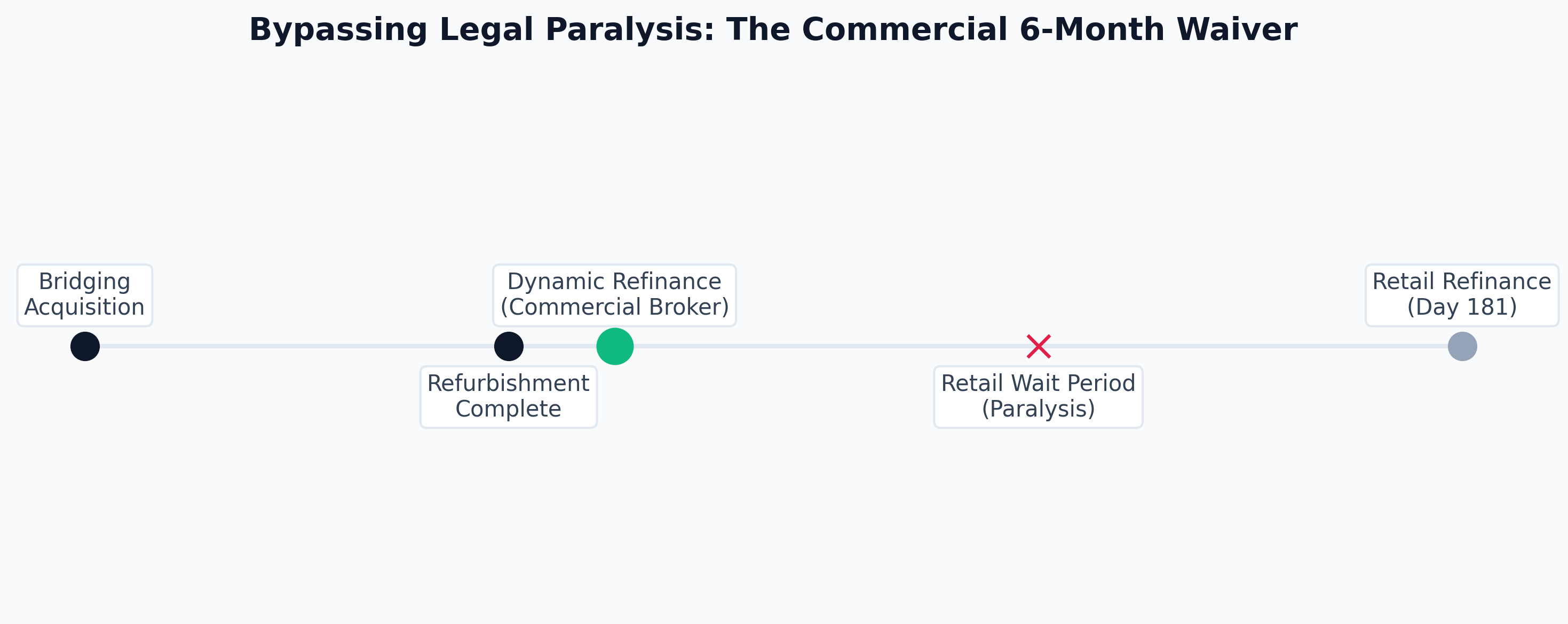

Week 14. The tenant contracts are signed. The asset is generating immense commercial revenue. You contact your specialized commercial mortgage broker to trigger the extraction phase. Because you utilized an elite broker, they have negotiated access to a commercial lender who explicitly waives the standard "Six-Month Rule," permitting you to refinance instantly without an artificial waiting period.

The bank's surveyor arrives. They analyze the heavy structural improvements, the elite EPC C rating, and the hyper-aggressive £26,400 commercial revenue stream. They sign off on the target end valuation.

- New Confirmed GDV: £200,000

You secure a 5-year fixed commercial SPV mortgage at 75% LTV against the new £200,000 valuation.

- The New Gross Mortgage: £150,000

The solicitor utilizes this massive £150,000 injection to immediately execute the capital extraction:

- They pay off the original £82,500 Gross Bridging Loan.

- The remaining £67,500 is wired as tax-free liquid cash directly back into your corporate SPV bank account.

Step 5: The Final Mathematical Post-Mortem

Did your brrrr strategy yield calculator uk predict success or failure?

- Your Personal Cash Injected (Day 1): £75,600

- Cash Extracted (Refinance): £67,500

- Final Cash Left In (CLI): £8,100

You utilized £75,000 to construct the project, but mathematically extracted 90% of it entirely tax-free. You now completely control a £200,000, high-yielding, fully refurbished asset, but you only possess an £8,100 operational risk exposure to the deal. You simply take the £67,500 you extracted and hurl it violently at property number two.

3. The 3 Hidden Friction Points That Destroy BRRRR Mathematics

Amateurs frequently study the theoretical BRRRR formula, construct a spreadsheet, and assume they have mastered the strategy. In 2026, the market is hyper-efficient, and severe friction points are ruthlessly waiting to annihilate your profit margins. A true brrrr strategy yield calculator uk must anticipate and aggressively buffer the following three commercial threats:

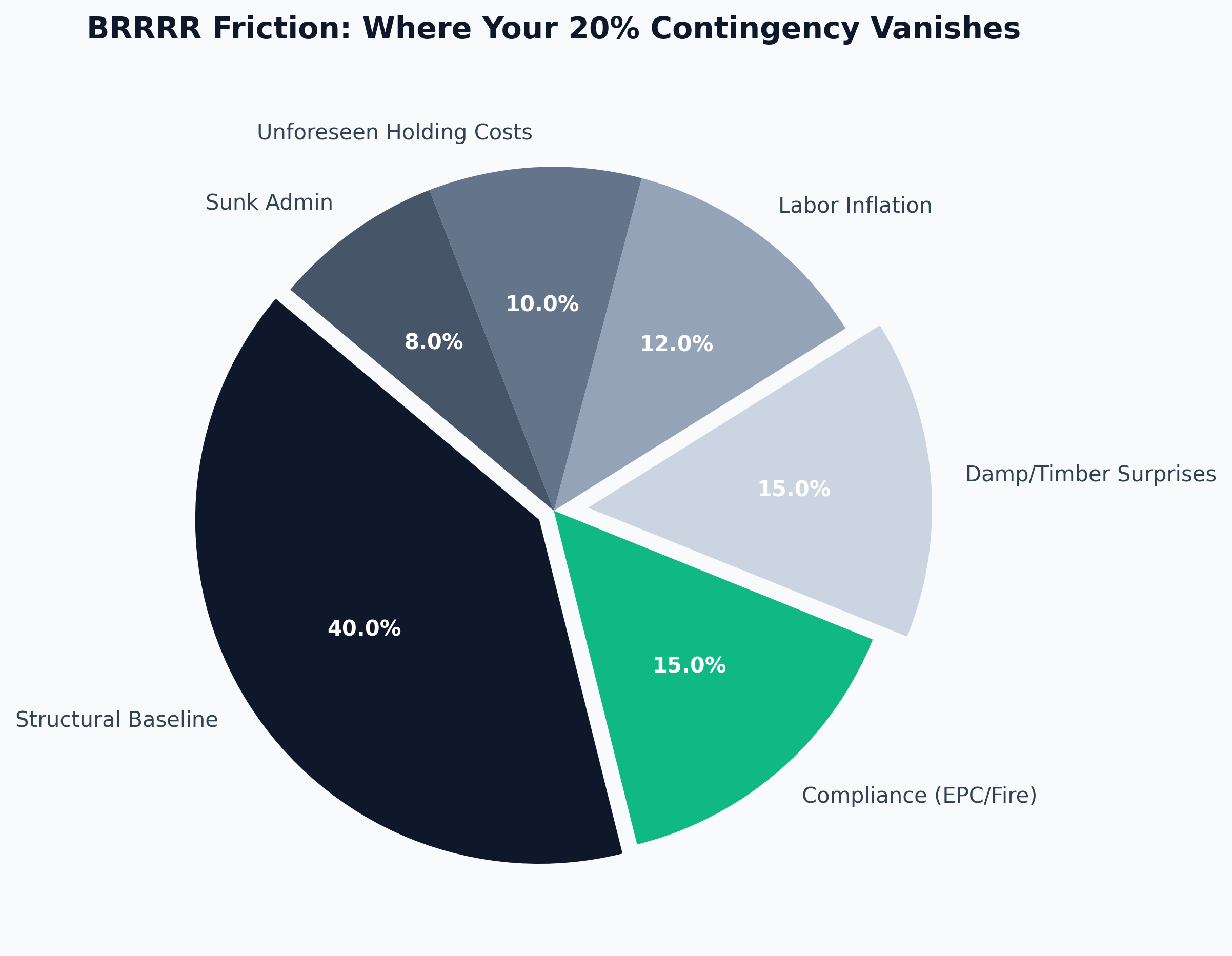

1. Structural Cost Overruns via Macro Supply Chain Friction

A standard 15% CapEx contingency buffer is structurally insufficient in 2026. The extreme scarcity of highly skilled, reliable tradesmen (electricians, roofers) combined with post-Brexit supply chain rigidity means raw materials can spike 10% mid-build. If your rigid £30,000 rehab spikes to £42,000 due to unforeseen structural timber rot, that extra £12,000 is directly transferred into your final "Cash Left In" figure, fatally compromising your ability to scale to property number two. Elite investors physically overcapitalize their development phase, holding an untouchable 20% to 25% cash reserve specifically to ensure the bridging loan does not default.

2. The Commercial Down-Valuation (The Death Blow)

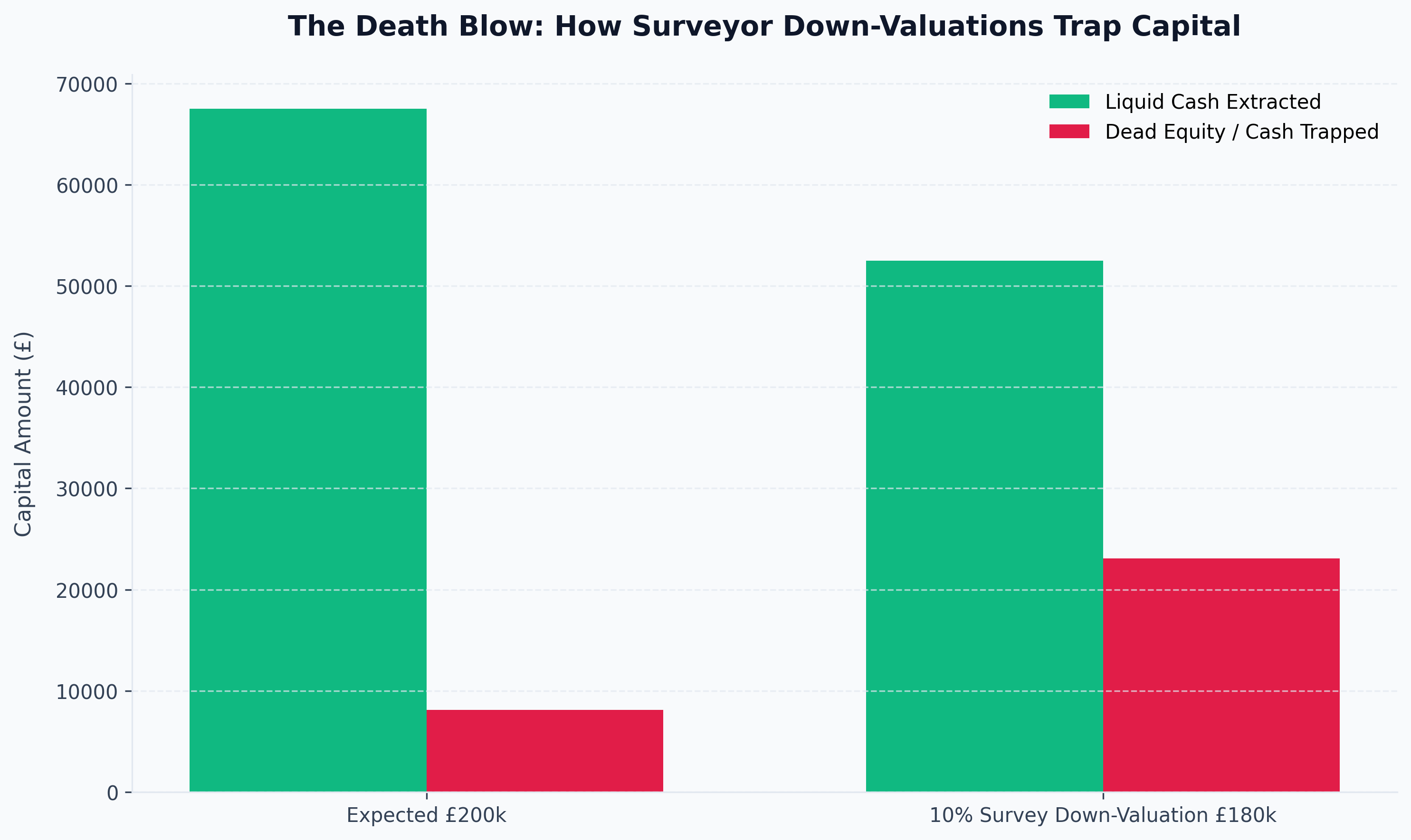

The absolute most devastating event in a BRRRR transaction is the final bank surveyor refusing to agree with your theoretical £200,000 End Valuation (GDV). Surveyors are fundamentally pessimistic, risk-averse data scientists hired by the bank to explicitly protect the bank's capital. If the local market has slowed, or the surveyor simply feels you "over-developed" the house for a low-yield street, they will radically slash the valuation.

- Theoretical Scenario: You rely on a £200,000 valuation to extract 75% (£150,000) and pay off your bridge.

- The Brutal Reality: The surveyor "down-values" the asset to £175,000.

- The Consequence: Your maximum 75% loan drops violently from £150,000 to £131,250. You are suddenly £18,750 short of the capital required to execute the extraction. That £18,750 is instantly locked into the asset as dead equity, deeply wounding your Cash Left In metric.

3. The Interest Coverage Ratio (ICR) Stress Test Failure

As explicitly covered in our comprehensive UK buy to let yield metrics guide, simply achieving the £200,000 GDV is useless if the rental income fails the bank's robotic ICR algorithms. Even if the surveyor agrees the house is worth £200k, if you require a £150,000 mortgage at 5.5% interest, the bank mandates the rent must cover 125% (for an SPV) or 145% (for a personal name) of the interest bill. If your gross rent is fundamentally too low to clear the algorithmic hurdle, the bank explicitly refuses to lend you the £150,000, severely restricting your final LTV, and forcing you to leave tens of thousands of pounds trapped in the asset.

Conclusion: The Era of Algorithmic Accuracy

In the wildly volatile UK property market of 2026, relying on rudimentary "gross yield" calculations or desktop spreadsheets is the fastest route to insolvency. The BRRRR methodology is the most potent wealth-generation system in global real estate, but it is mathematically unforgiving.

If you attempt to execute capital extraction without factoring in 1% monthly bridging costs, rolled-up institutional interest, commercial valuation risk, and SPV taxation shielding, the fiscal friction will tear your capital apart.

Build the ultimate brrrr strategy yield calculator uk. Stress-test your CapEx buffer at 120%. Stress-test your final commercial refinance rate at 6.5%. Assume the bank will down-value the GDV by 10%. If the mathematics of the deal still survive those catastrophic simulations and spit out a highly lucrative Capital Extraction matrix, you execute the acquisition aggressively.

To dominate in 2026, you must stop operating like a high-street landlord and start underwriting like an institutional hedge fund.

2026 FAQ: The Granular Details of Capital Extraction

To further bulletproof your underwriting models, we rigorously analyze the most frequently encountered friction points within the BRRRR matrix.

Why do some investors fail to refinance after 6 months?

This is the systemic failure of the "Six-Month Rule." Historically, the majority of retail UK mortgage lenders operated under strict anti-money laundering (AML) protocols preventing any investor from refinancing an asset within six calendar months of the original Land Registry purchase date. If you utilized ultra-expensive bridging finance (costing £800 a month in interest), finished your heavy refurbishment in two months, and tenanted the property in month three, you were legally forced to sit entirely paralyzed for three additional months, bleeding thousands of pounds in dead bridging interest, desperately waiting for day 181 to trigger the extraction. The 2026 Solution: Elite investors entirely bypass the High Street. They utilize specialized, hyper-connected commercial brokers who maintain direct access to institutional "Challenger Banks" and specialized commercial lenders who explicitly waive the six-month rule, permitting dynamic Day-1 refinancing the moment the tenant contract is physically signed.

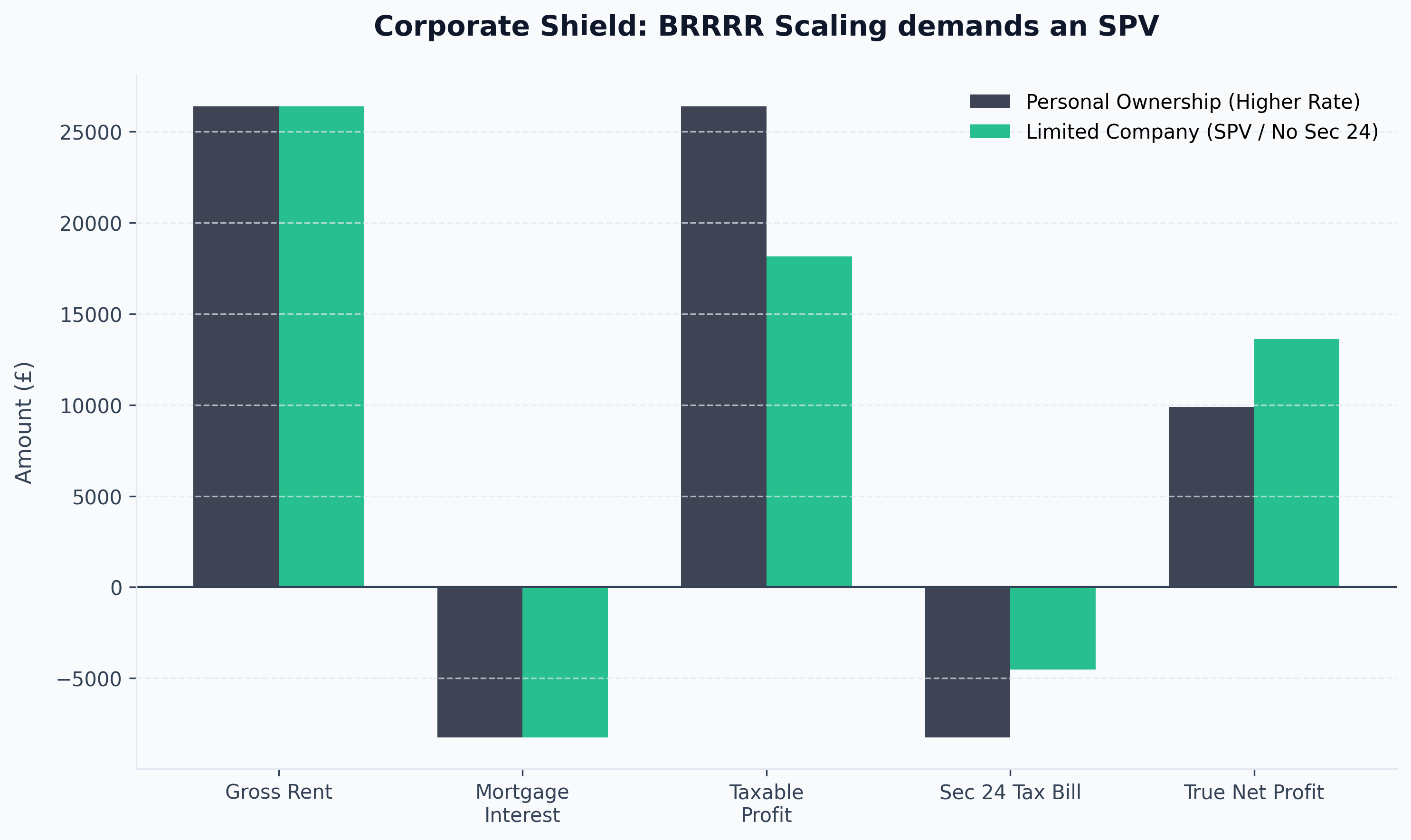

Can I execute a BRRRR transaction in my personal name?

Technically, yes. Financially and mathematically, absolutely not. As extensively documented in our guide on financing property investment, executing leveraged acquisitions in an individual name as a higher-rate taxpayer (40%+) is fiscal suicide in 2026. Section 24 prevents you from legally deducting the massive commercial mortgage interest payment as a business expense. You are taxed aggressively on your Gross Operating Profit, forcing you to utilize your own post-tax salary simply to pay the HMRC bill. Furthermore, retail banks apply a brutally restrictive 145% ICR stress test against personal applications, massively reducing the size of the mortgage you can secure, actively crippling your ability to extract capital. Execute entirely via a Limited Company (Special Purpose Vehicle).

What happens if I miscalculate the LTGDV and the bridging loan expires?

Bridging loans are hyper-aggressive, short-term debt instruments, typically lasting 9 to 12 months. They are not designed for long-term holds. If your refurbishment project suffers catastrophic delays (e.g., waiting 6 months for local council planning permission to construct an extension), and you hit the 12-month expiry date without refinancing, you trigger extreme fiscal penalties. The lender will transition you to a punitive default interest rate (frequently 2% to 3% per month), entirely annihilating your profit margin, and they possess the legal right to aggressively repossess the asset. You must possess ruthless project management infrastructure. If planning permission is required, you must execute via specialized "Development Finance" rather than a standard bridge.

Stop being a landlord. Start being an investor.

Shaded Canvas introduces serious capital to vetted UK property opportunities — targeting 12–16% net returns.

Start Investing →