Every property influencer operating on social media in 2026 is aggressively marketing the exact same blueprint: Buy a distressed property, refurbish it, rent it out, refinance to pull your cash back out, and do it again.

They promise infinite Return on Investment (ROI) and rapid portfolio scaling using exactly zero of your own money. The theory is objectively flawless. However, the execution in the hyper-regulated, high-tax environment of the UK property market is a completely different reality.

So, we must ask the fundamental commercial question: is buy rehab rent refinance repeat worth it uk?

At Shaded Canvas, we do not operate on Instagram theory; we operate on ruthless, algorithmic underwriting. The short answer is yes—the strategy is the single most powerful wealth-generation engine available to private investors. The long answer is that if you do not possess a dictatorial command over commercial bridging debt, Section 24 tax structures, and RICS valuation parameters, the strategy will bankrupt you within six months.

This 3,000-word authority audit will forensically disassemble the true 2026 viability of the Buy, Rehab, Rent, Refinance, Repeat strategy in the UK. We will expose the margins, the traps, and the exact mathematical thresholds required to make this strategy actually worth it.

1. The Mathematical Allure: Why the Theory is Flawless

Before we dissect the friction, we must acknowledge why the strategy remains the apex predator of real estate investment frameworks.

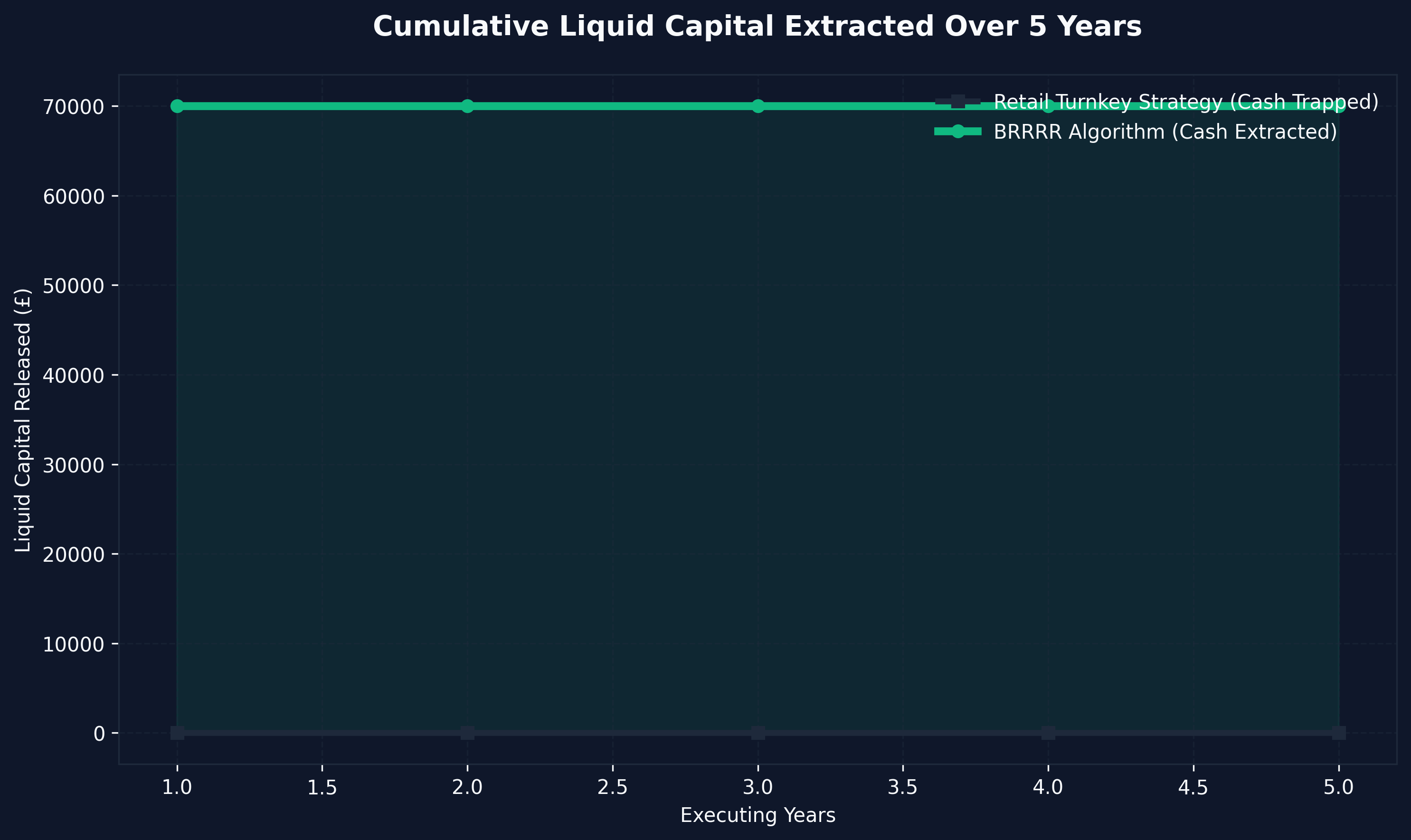

Traditional "Retail" Buy-to-Let (BTL) investing is a linear, unscalable model. If you save £50,000 and deploy it as a 25% deposit on a £200,000 turnkey property, that cash is "trapped" inside the brickwork. It might generate a 6% gross yield, giving you roughly £500 a month in net profit. To buy property number two, you have to spend another three years physically saving another £50,000 from your day job. At that velocity, retiring on real estate will take you forty years.

The Power of the Extraction Phase

The Buy, Rehab, Rent, Refinance, Repeat strategy completely sequence-breaks this timeline. It leverages the concept of Forced Appreciation.

- Buy: You deploy £40,000 to buy an unmortgageable, derelict £100,000 house using an £80,000 bridging loan (75% LTV).

- Rehab: You deploy £30,000 of liquid cash to execute a heavy refurbishment, neutralizing the structural defects and installing a premium HMO finish. Total Cash Deployed: £50,000 (Deposit + Fees) + £30,000 (Rehab) = £80,000.

- Rent: You tenant the asset, proving the commercial income.

- Refinance: A RICS surveyor visits the newly renovated property. Because of the heavy structural improvements, they value the "Final Bank GDV" at £200,000. You apply for a standard 75% LTV commercial mortgage against this new £200k value. The bank lends you £150,000.

- The Math: You use that £150,000 to pay off the initial £80,000 bridging loan. You are left with £70,000 in liquid, tax-free cash. You physically pull your initial £80k investment almost entirely back out of the deal. You still own an income-generating asset, but you have £70,000 instantly available to execute property number two.

When modeled perfectly, your ROI is technically "infinite" because you have zero of your own capital left in the transaction, yet you command 100% of the asset's cash flow and capital appreciation. This is why it is worth it.

2. The Execution Reality: The Threat of Bridging Attrition

The strategy is only fully effective if you can acquire distressed assets that are completely unmortgageable (structural defects, no kitchen, Japanese Knotweed). Standard high-street lenders will not touch these properties. Therefore, you are forced to utilize Bridging Finance.

The Fiscal Danger of Short-Term Debt

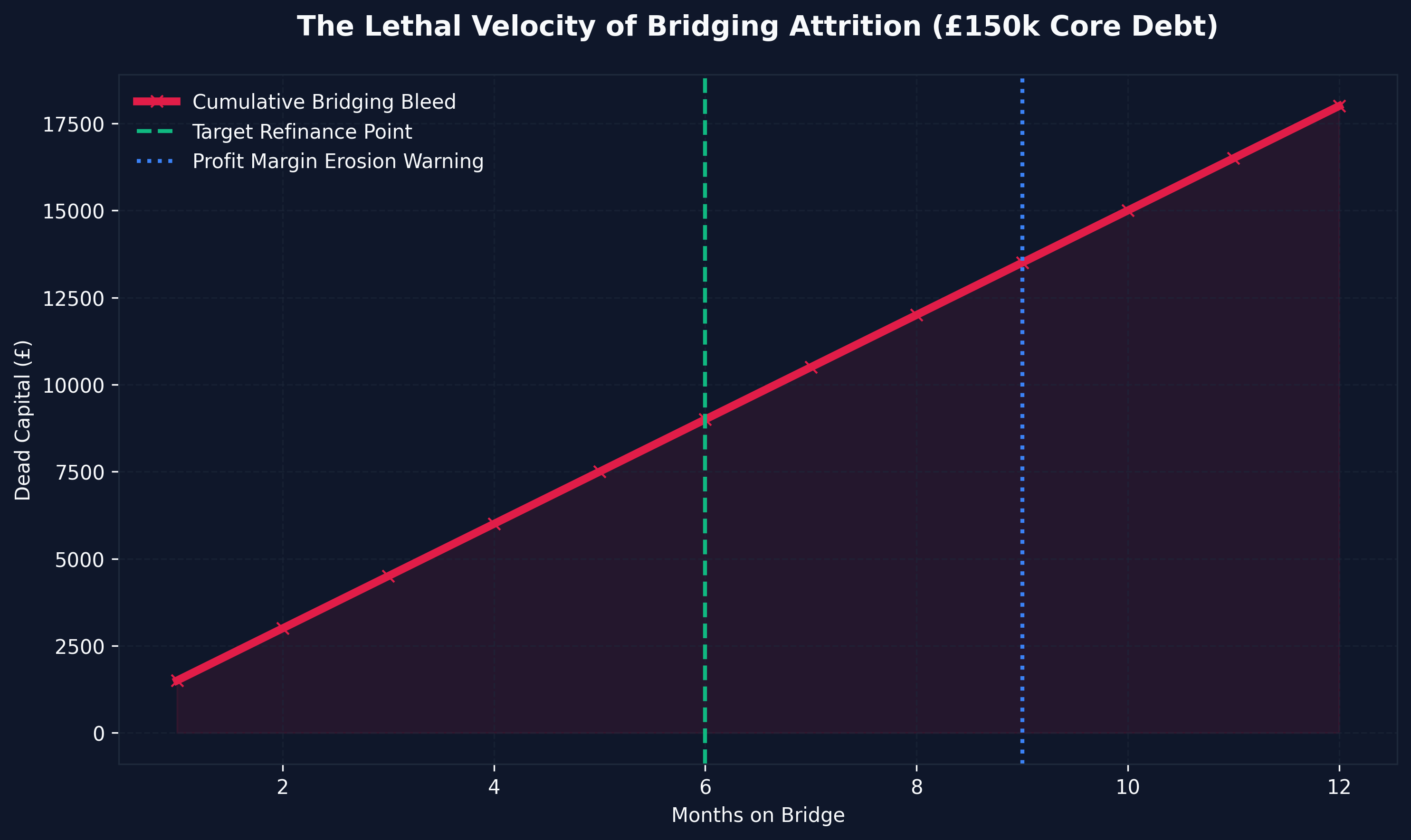

Bridging loans are the financial equivalent of high-yield explosives. They are incredibly powerful moving from point A to point B, but if delayed, they will detonate your entire profit margin.

In 2026, standard bridging debt operates at roughly 1% per month in interest, plus a 2% entry fee and a 1% exit fee. If you borrow £150,000 to bridge an acquisition:

- The bank charges a £3,000 arrangement fee on day one.

- The interest bleed is £1,500 every single month.

The entire Buy, Rehab, Rent, Refinance, Repeat strategy relies on velocity. If your contractor ghosts you, or planning permission delays your HMO conversion by four months, you are bleeding £1,500 a month in "dead money." A six-month delay incinerates £9,000 of your target equity.

This is the primary reason why amateur investors fail. They cannot control their supply chains. If the rehab phase drags from 12 weeks out to 9 months, the bridging attrition entirely wipes out the forced appreciation. If you cannot execute heavy refurbishments with military precision, the strategy is absolutely not worth it.

3. The End-Boss: RICS Commercial Down-Valuations

You can execute the perfect acquisition, complete the rehab on time and under budget, and secure premium tenants. But none of it matters if you fail the "Refinance" phase.

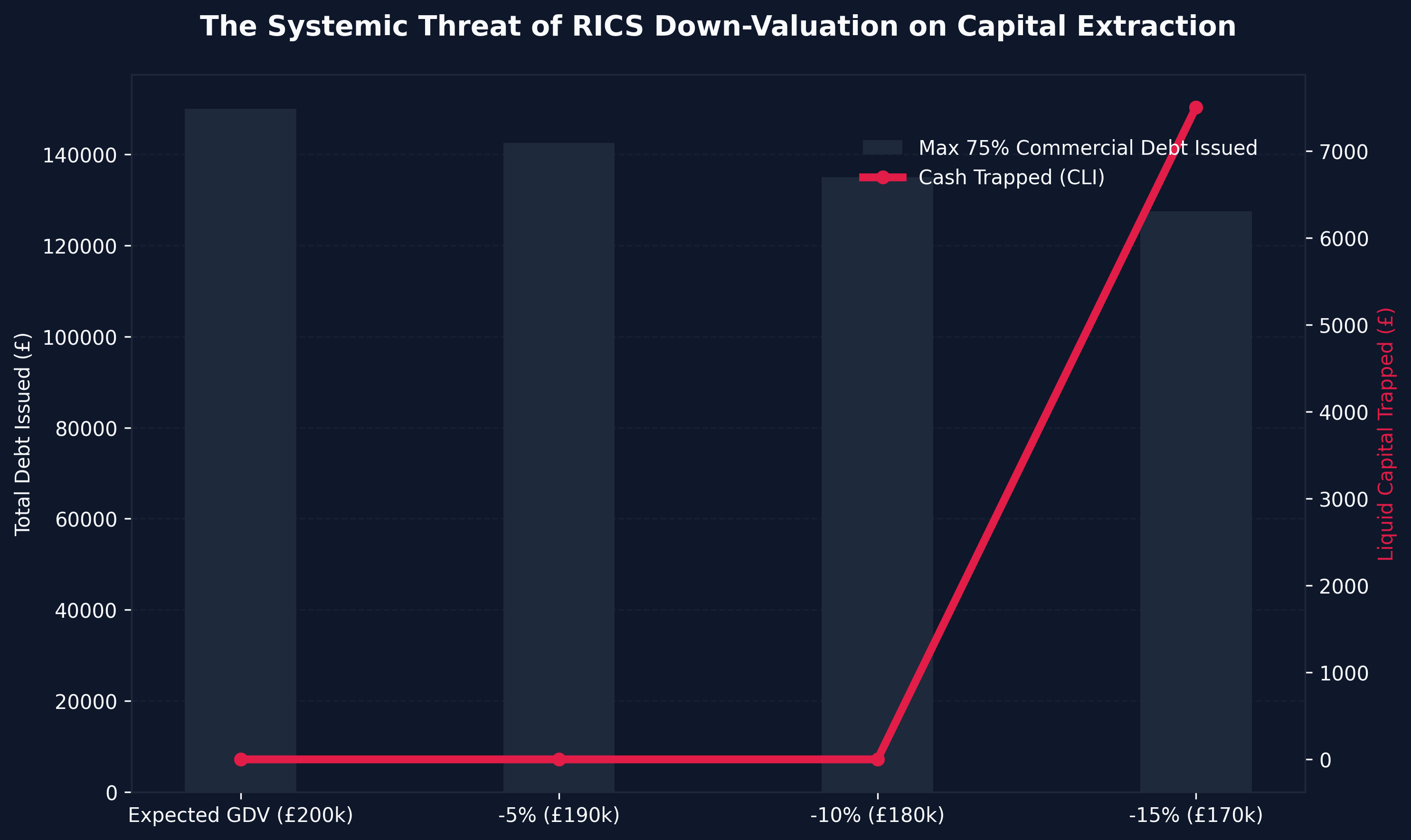

The entire extraction loop hinges on a RICS-accredited commercial surveyor agreeing with your £200,000 Gross Development Value (GDV) assessment. If the surveyor walks into the property and decides the asset is only worth £175,000, your entire extraction algorithm collapses.

The Cash-Left-In (CLI) Trap

If the surveyor down-values the asset to £175,000, the bank will only lend you 75% of that figure (£131,250). Suddenly, you do not have enough commercial debt to pay off your bridging loan and pull your £80,000 out of the deal. The £25,000 shortfall means that money is permanently "trapped" in the deal as Cash Left In (CLI).

While leaving £25k in a cash-flowing asset is still a vastly superior ROI to the £50k trapped in a traditional Retail BTL, you no longer possess the liquidity to immediately execute property number two. The "Repeat" phase of the framework fractures.

Elite syndicates mitigate this terminal risk by relentlessly cross-referencing local comparable evidence, inviting surveyors to review the property before the rehab commences, and maintaining vast cash reserves to absorb minor down-valuation hits. If you are executing this protocol on your last £60k of savings, a 15% down-valuation is a critical operational failure.

4. The Taxation Matrix: SPVs and Section 24

In addressing the core question of whether the blueprint is viable, we must analyze the UK tax regime.

If you attempt to execute this highly leveraged model in your personal name as a higher-rate taxpayer, Section 24 of the Finance Act will systematically crush you. HMRC will ban you from deducting your commercial mortgage interest, taxing you brutally on your Gross Operating Revenue and forcing the asset into negative cash flow.

If you do not grasp the taxes on buy rehab rent refinance repeat uk 2026, you cannot operate.

The Mandatory SPV Structure

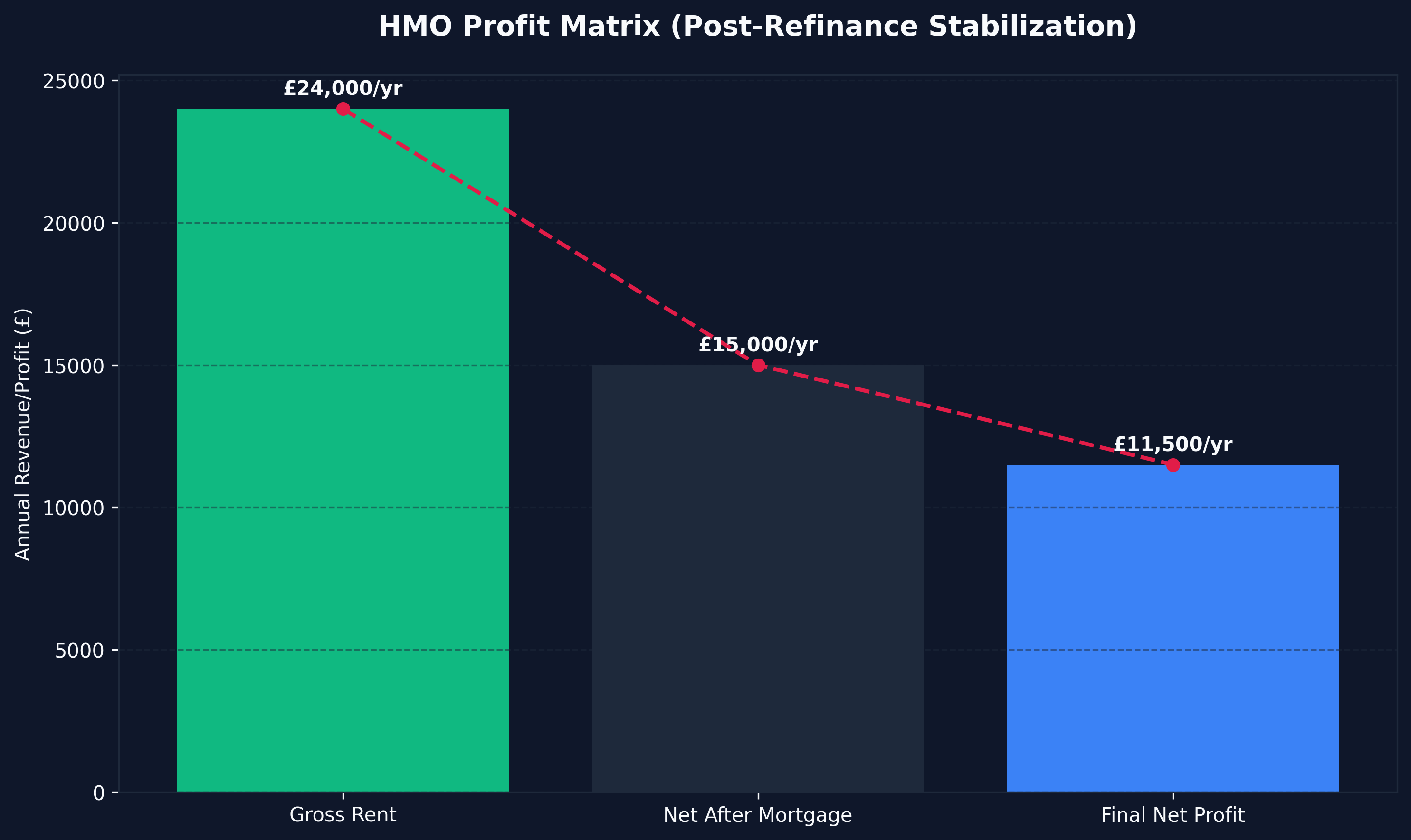

To make the strategy "worth it" in 2026, 100% of your transactions must be wrapped inside a Special Purpose Vehicle (SPV) Limited Company. An SPV is immune to Section 24, allowing you to legally deduct all bridging costs, mortgage interest, and management fees before paying a flat 19-25% Corporation Tax on the true net profit.

Furthermore, you must optimize the rehab CapEx. Elite investors hunt for properties that have been empty for over two years, legally qualifying the entire £40,000 refurbishment for a massively reduced 5% VAT bracket instead of the standard 20%. That single strategic pivot instantly saves £6,000 in fluid cash, dramatically improving the extraction metrics.

5. Alternative Syndication: Bypassing the Operational Friction

For high-net-worth professionals—surgeons, software engineers, banking executives—the core question is not whether the mathematics of the strategy work; it is whether the massive operational friction justifies the time investment.

Executing a Buy, Rehab, Rent, Refinance, Repeat cycle requires you to act as an aggressive acquisitions manager, a hyper-efficient project manager wrangling hostile scaffolding firms, and a ruthless financial controller battling commercial surveyors. For a busy professional earning £150k a year in their primary vocation, managing a £40,000 wet-rot refurbishment in a terraced house three hours away is an atrocious misallocation of high-value time.

The Syndicated "Lazy BRRRR" Model

If the active operational complexity is too high, the mathematical pivot is syndication. By deploying capital into real estate venture capital uk, you physically participate in the algorithmic returns of elite developers executing massive commercial BRRRR strategies.

You inject £100,000 into a fractional syndicate. The syndicate locates the distressed block of flats, secures the commercial bridge, executes the 12-month heavy refurbishment, and secures the final institutional valuation out. You participate in the compound wealth velocity of the BRRRR structure, but the operational friction, the bridging attrition risk, and the contractor management are entirely offloaded onto the institutional operator.

Conclusion: Is it actually worth it?

The objective, mathematical answer to "is buy rehab rent refinance repeat worth it uk" is an absolute Yes, but only if you respect it as a highly volatile commercial banking operation, not a passive income hobby.

If you can mathematically control bridging attrition, successfully navigate commercial down-valuations through ruthless comparable analysis, and shield your capital within an SPV to neutralize Section 24, the strategy will accelerate your portfolio velocity by an order of magnitude over traditional retail investing.

It is the only framework that mathematically permits private investors to acquire a £5,000,000 commercial property portfolio utilizing a fixed £150k seed capital pot. The returns are borderline algorithmic. But if you underestimate the friction, you will simply become standard yield fodder for the high-street bridging banks.

2026 FAQs: Analyzing Strategy Viability

How much seed capital do I realistically need to start in 2026?

While influencers claim you can execute with "No Money Down," the commercial reality is you require liquid cash. If you are targeting a £100k distressed purchase with a £30k rehab, you will need approximately £30k for the 25% bridging deposit, £5k for bridging setup fees, SDLT, and legals, plus the £30k cash to physically fund the rehab before the bank releases any drawdowns. A highly realistic, safe liquid runway to execute your first true commercial BRRRR in the North of England is £60,000 to £75,000 to ensure you are immune to bridging delays.

What is the most common reason for failure in this strategy?

The number one point of failure is Refurbishment Scope Creep combined with Bridging Attrition. Amateurs underestimate the heavy CapEx required (e.g., discovering widespread damp or structural rot mid-project). This blows the budget and delays the project by 3 months. Those 3 months of delays incur massive punitive interest charges from the bridging lender. The combination of £15k extra build costs plus £5k extra bridging interest permanently traps the investor's cash in the deal, shattering the extraction algorithm.

Does the strategy work in London and the South East?

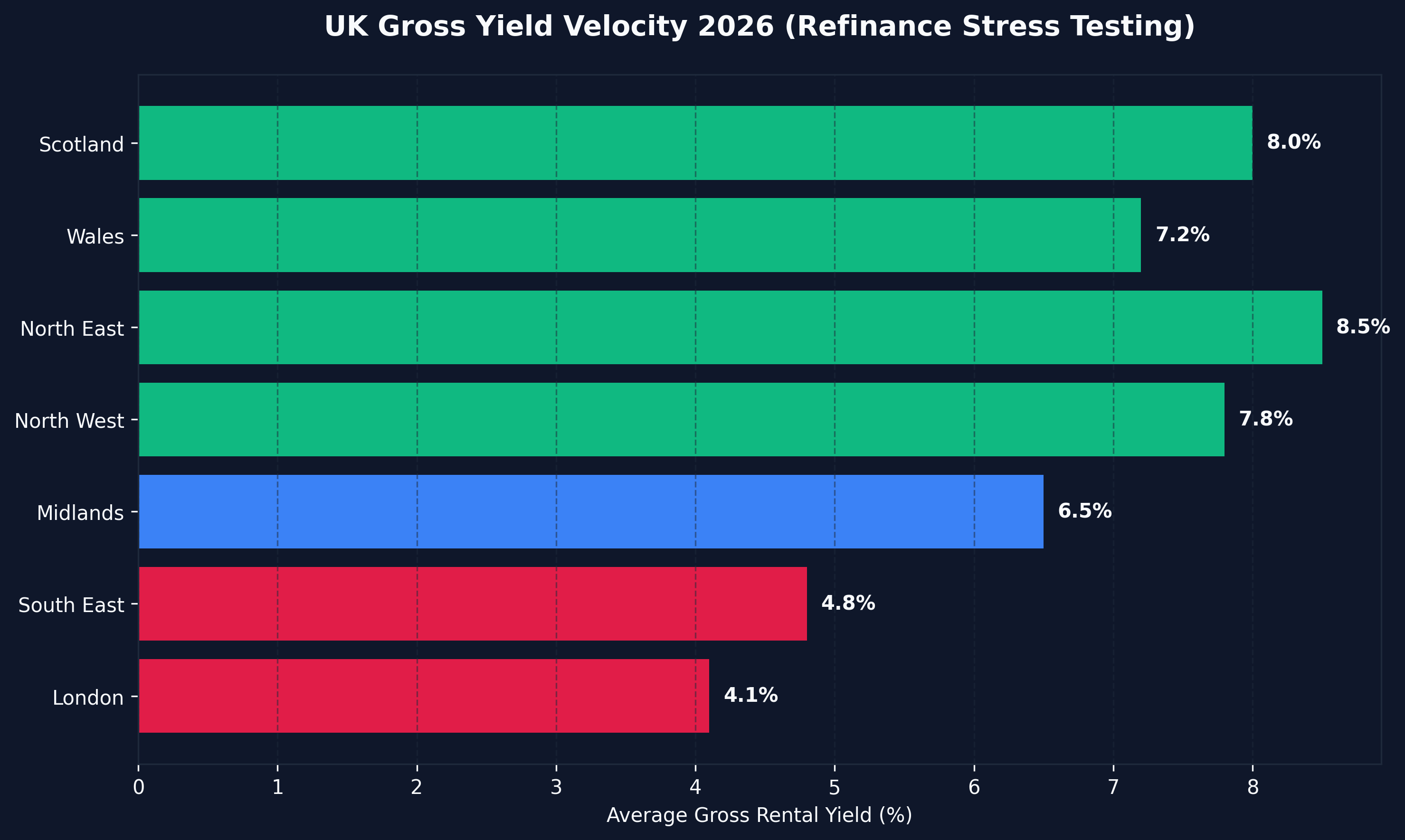

Mathematically, yes, but the barrier to entry is extreme. Yields in London are compressed, meaning the final rental income often struggles to pass the stress-tests required by commercial lenders for the final refinance. Because property values are so high (e.g., £500k entry points), you are risking massive bridging loan attrition parameters (£5,000+ a month in pure interest). The majority of elite operators execute the strategy exclusively in the Midlands, the North West, and Wales, where entry costs are low and rental yields naturally hover between 8% and 12%, allowing for flawless commercial refinancing.

Stop being a landlord. Start being an investor.

Shaded Canvas introduces serious capital to vetted UK property opportunities — targeting 12–16% net returns.

Start Investing →