If you are executing the Buy, Rehab, Rent, Refinance, Repeat strategy in the United Kingdom, you cannot afford to underwrite your deals on gut feeling. Every single acquisition must be stress-tested against precise financial parameters: gross yield, net yield, Cash Left In (CLI), Return on Capital Employed (ROCE), and the critical Interest Coverage Ratio (ICR) that commercial lenders will use to approve or deny your refinance application.

This is why we built the definitive buy rehab rent refinance repeat yield calculator uk — a free, institutional-grade tool that models the entire BRRRR cycle in real-time, allowing you to instantly identify whether a deal is commercially viable before you commit a single pound of bridging finance.

The Free BRRRR Yield Calculator

Use the calculator below to model your next BRRRR deal. Input your acquisition parameters, rehab budget, target rental income, and refinance terms. The calculator will instantly output your projected gross yield, net yield, total capital extraction, Cash Left In, and Return on Capital Employed.

🏗️ BRRRR Yield Calculator — 2026 UK Edition

📊 Deal Analysis

How to Use the Buy Rehab Rent Refinance Repeat Yield Calculator

The calculator above is designed to model the full lifecycle of a single BRRRR acquisition. Here is a step-by-step guide to interpreting the inputs and outputs:

Input Parameters Explained

Phase 1 — BUY:

- Purchase Price: The auction or off-market price of the distressed, unmortgageable property. For Northern England BRRRR strategies, this typically ranges from £60,000 to £120,000.

- Bridging LTV: The percentage of the purchase price your bridging lender will advance. Standard is 70-75%.

- Bridging Interest Rate: Monthly interest charged on the bridge. In 2026, expect 0.75% to 1.25% per month.

- Arrangement Fee: The one-time fee charged by the bridging lender. Typically 1.5% to 2.5%.

- SDLT / Legal Fees: Your <a href="/post/stamp-duty-on-buy-to-let" style="color:#c9a84c;text-decoration:underline;font-weight:500">Stamp Duty Land Tax (including the 5% investor surcharge) plus solicitor fees.

Phase 2 — REHAB:

- Rehab Budget: The total capital expenditure required to transform the asset from unmortgageable to premium rental condition. A heavy rehab typically costs £25,000 to £45,000.

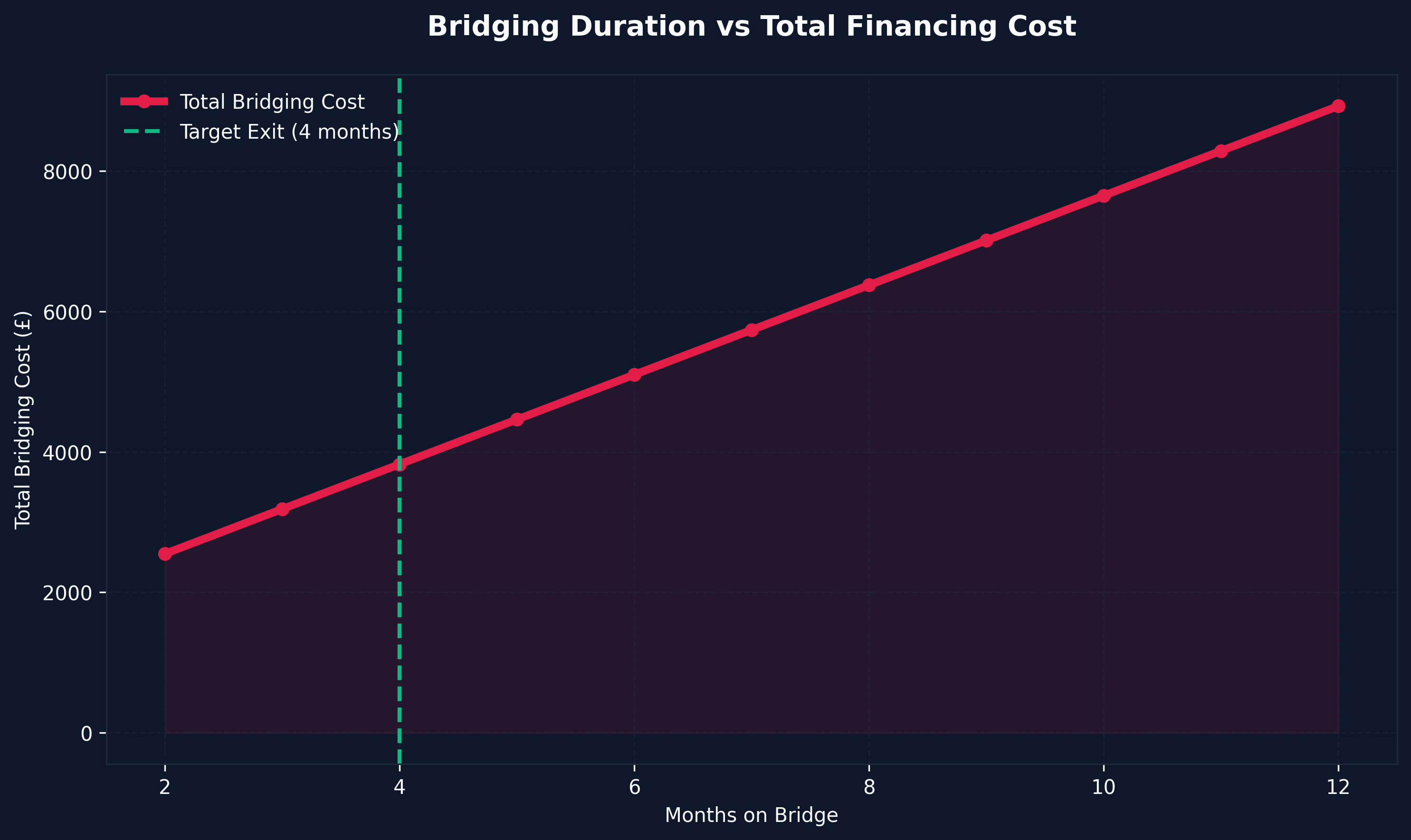

- Duration: How many months the refurbishment will take. Every extra month increases your bridging cost. Elite operators target 3-4 months; amateurs frequently overshoot to 6-9 months.

Phase 3 — RENT:

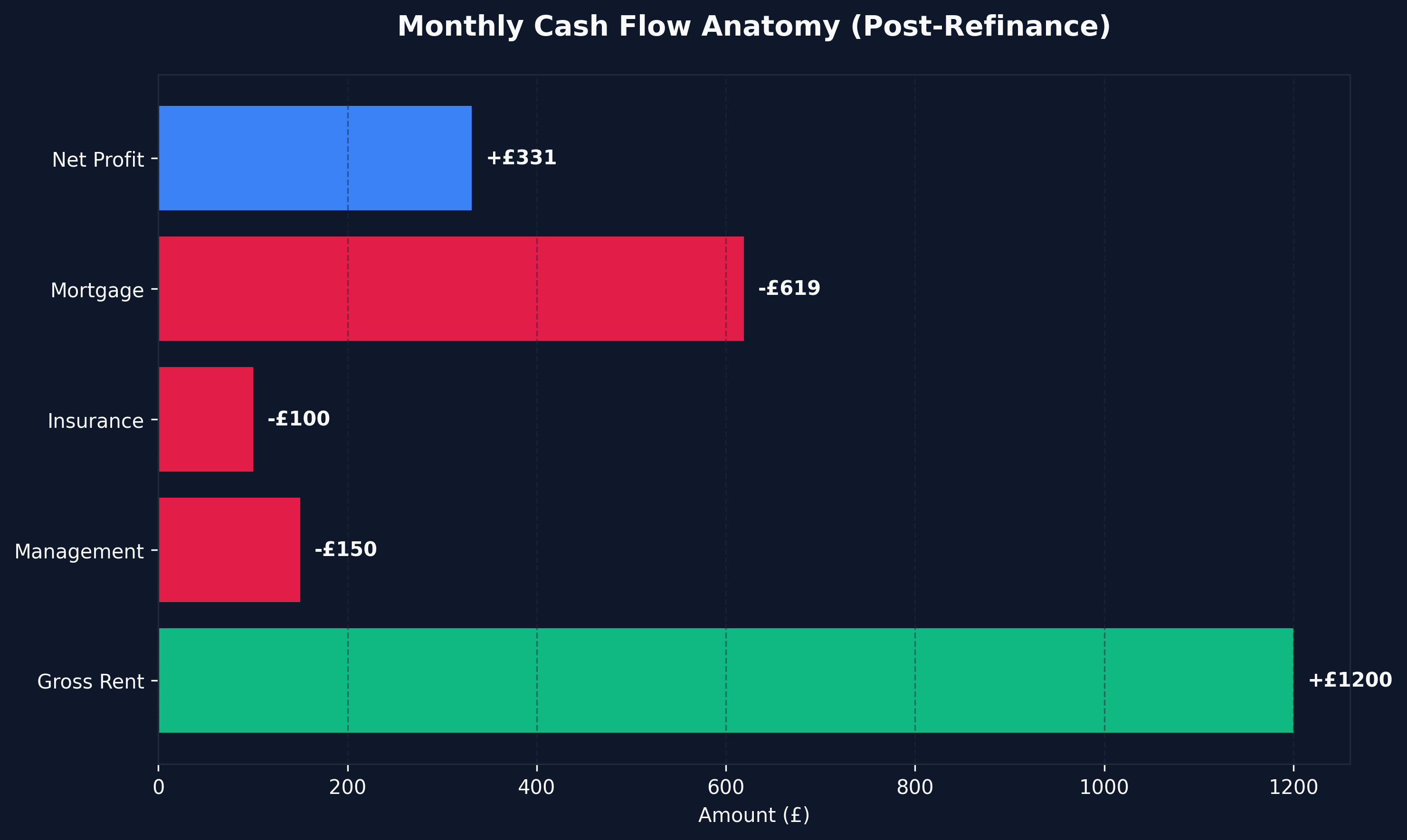

- Monthly Gross Rent: The total rent collected from the asset per month. For HMOs, this is the combined room-by-room total.

- Management + Insurance: Monthly operational costs including letting agent fees, landlord insurance, and maintenance reserves.

Phase 4 — REFINANCE:

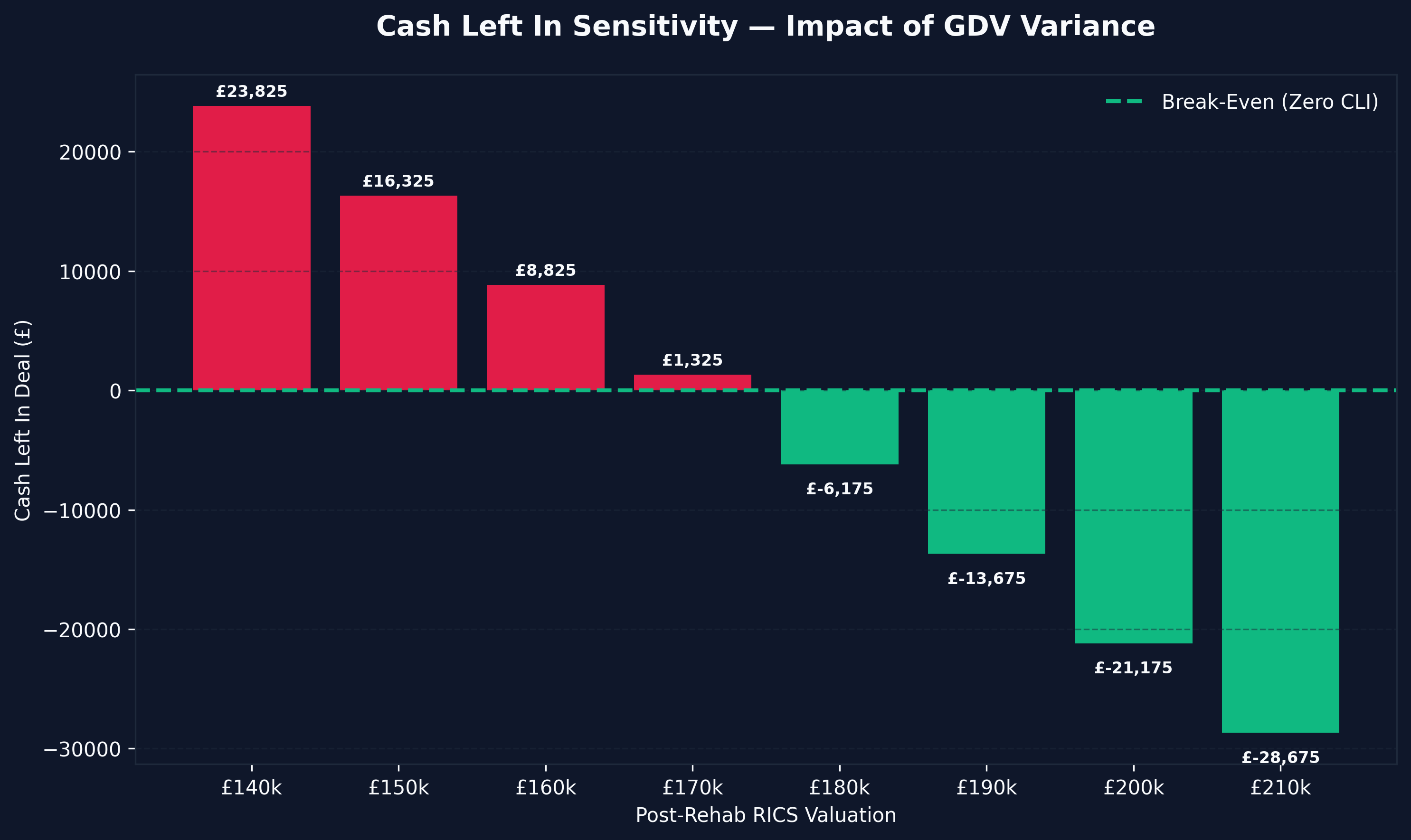

- Post-Rehab Valuation (GDV): The value a RICS surveyor assigns to the property after your refurbishment. This is the single most important number in the entire strategy.

- Commercial Mortgage LTV: The loan-to-value ratio on the final refinance. Standard is 75%.

- Mortgage Interest Rate: The annual interest rate on your commercial buy-to-let mortgage. In 2026, expect 4.5% to 6%.

Output Metrics Explained

- Cash Left In (CLI): The amount of your personal capital permanently trapped in the deal after refinancing. If this number is negative, you have successfully executed a "no money left in" deal — the holy grail of BRRRR.

- Gross Yield: Annual rent divided by the GDV. Lenders want to see 6%+ minimum.

- Net Yield: Annual profit (after mortgage and costs) divided by the GDV.

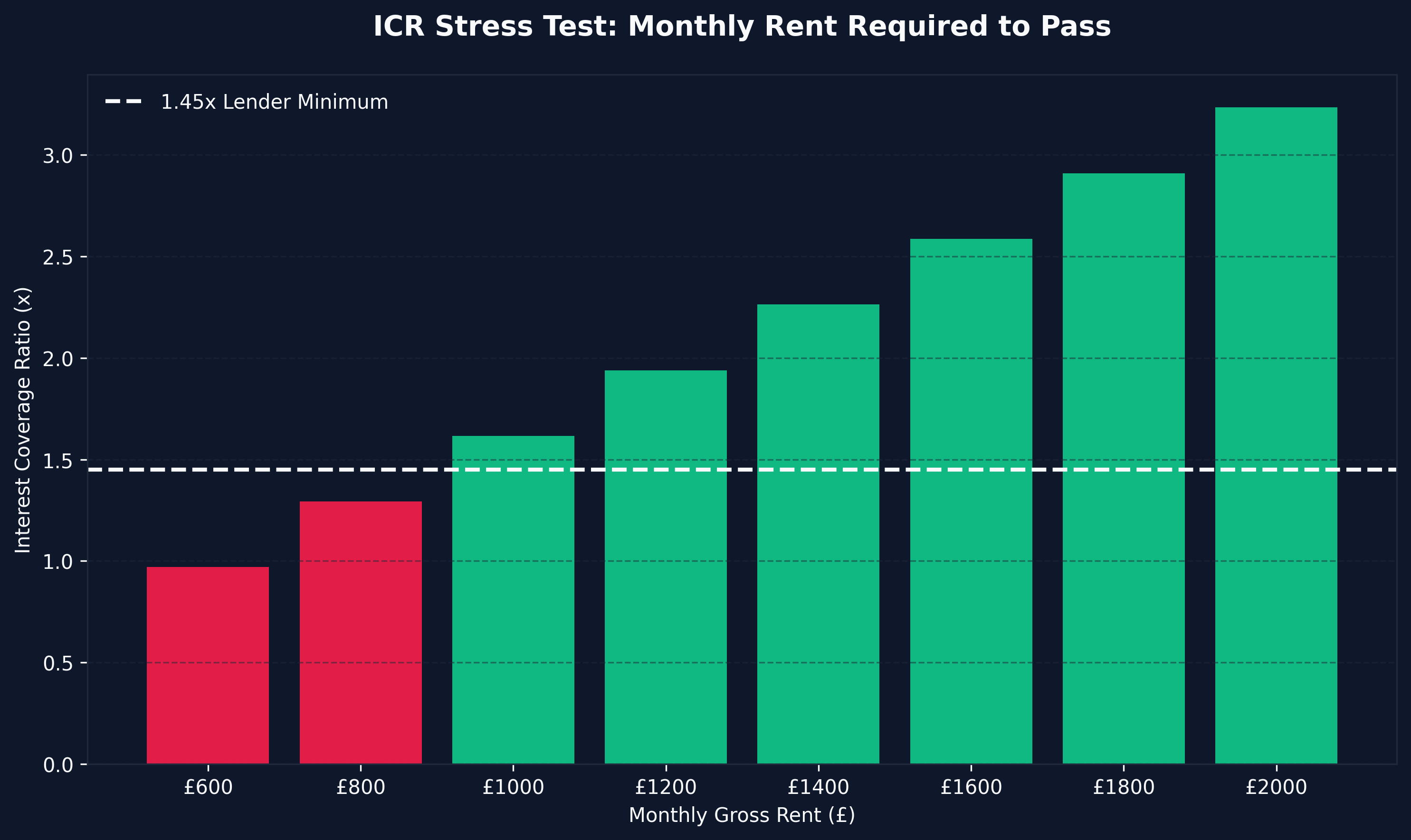

- ICR (Interest Coverage Ratio): Gross rent divided by monthly mortgage payment. Commercial lenders require a minimum 1.25x to 1.45x at a stressed rate.

- ROCE (Return on Capital Employed): Your annual net profit divided by your Cash Left In. If CLI is zero or negative, your ROCE is mathematically infinite — the defining characteristic of a perfect BRRRR execution.

The Mathematics Behind the Calculator

Understanding what the BRRRR method is and how it works is the essential precursor to using this calculator effectively.

The Forced Equity Engine

The calculator's core algorithm models the concept of Forced Appreciation. By purchasing a distressed asset at 40-60% of its renovated market value and then executing a heavy rehabilitation, you physically manufacture the equity gap. The calculator quantifies this gap and determines whether the resulting commercial mortgage is large enough to extract 100% of your deployed capital.

Bridging Attrition Sensitivity

A critical insight: adjusting the "Rehab Duration" input by even 2-3 months can swing your CLI by thousands of pounds. This is the bridging attrition effect. Every additional month on the bridge adds roughly £850 to £1,500 in dead interest charges, directly reducing your extraction capacity.

If you are concerned about whether this friction makes the strategy viable for your personal circumstances, our comprehensive analysis on whether buy rehab rent refinance repeat is worth it in the UK breaks down the exact failure thresholds.

The Tax Layer

The calculator models pre-tax cash flow. For the full fiscal picture — including SPV Corporation Tax structures, the Section 24 income tax trap, and VAT mitigation on rehab costs — consult our detailed taxes on buy rehab rent refinance repeat uk 2026 guide.

Worked Example: Modelling a Bolton HMO Conversion

Let's walk through a real-world deal using the calculator's default parameters:

Inputs:

- Purchase Price: £85,000 (3-bed fire-damaged terrace, Bolton auction)

- Bridging: 75% LTV, 1%/month interest, 2% fee

- Rehab: £35,000 over 4 months (full gut renovation + HMO conversion)

- Rent: £1,200/month HMO (4 rooms at £300 each)

- GDV: £180,000 (RICS valuation post-rehab)

- Refinance: 75% LTV commercial mortgage at 5.5%

Outputs:

- Total Cash Deployed: ~£59,250

- Cash Extracted: ~£71,250

- Cash Left In: -£12,000 (PROFIT! You pulled out MORE than you put in)

- Gross Yield: 8.00%

- ICR: 1.45x (passes lender stress test)

- ROCE: Infinite (zero capital remaining in deal)

This is a textbook perfect BRRRR execution. You own an asset worth £180,000, generating £1,200/month in gross rent, and you have zero of your own capital in the transaction. The £59,250 is immediately available to execute deal number two.

Common Mistakes When Using a BRRRR Calculator

Mistake 1: Inflating the GDV

The most dangerous error is overestimating the Post-Rehab Valuation. Social media influencers routinely claim their "GDV will be £250,000" based on aspirational Rightmove listings rather than hard comparable evidence. When the RICS surveyor arrives and values the property at £200,000, the entire extraction model collapses.

Rule: Always underwrite your GDV conservatively. Use the lowest three comparable sales within 0.5 miles over the last 6 months. If the average comp is £185,000, model your GDV at £175,000.

Mistake 2: Ignoring Bridging Costs

Amateurs input only the purchase price and rehab budget as their "total cost" and forget about the £4,000 to £8,000 in bridging fees and interest. The calculator accounts for this automatically, but make sure your real-world cash reserves do too.

Mistake 3: Underestimating Rehab Duration

A 3-month rehab at 1% bridging costs you £2,550 in interest. A 9-month rehab costs £7,650. That £5,100 difference often determines whether you extract 100% of your capital or leave £5,000 trapped in the deal.

FAQs: Using the BRRRR Yield Calculator

What gross yield should I target for a viable BRRRR deal?

For commercial lenders to approve your refinance, the gross yield must pass an ICR stress test at 145% coverage at a 5.5% stressed rate. In practice, this means targeting a minimum 8% gross yield. The calculator will flag your ICR automatically — if it's below 1.45x, the deal will likely fail at the refinance stage.

What is a good Cash Left In (CLI) target?

The gold standard is £0 or negative CLI. This means you extracted 100% (or more) of your capital. However, leaving £5,000 to £10,000 in a deal generating £500+/month net profit is still an exceptional outcome compared to traditional buy-to-let where £50,000+ is permanently trapped.

Can I use this calculator for standard buy-to-let deals?

Yes. Simply set the Bridging LTV to 0%, the Arrangement Fee to 0%, and input your standard mortgage deposit as the purchase price. The yield and cash flow calculations will still apply perfectly. However, for standard BTL yield modelling, our dedicated rental property yield calculator may be more appropriate.

Stop being a landlord. Start being an investor.

Shaded Canvas introduces serious capital to vetted UK property opportunities — targeting 12–16% net returns.

Start Investing →