Before deploying substantial capital into the UK real estate market, professional investors must ruthlessly model their expected returns. Operating on "gut feeling" or relying on an estate agent's optimistic brochure is a guaranteed path to negative cash flow.

If you want to survive the 2026 macroeconomic landscape—characterized by stabilized Bank of England base rates and stringent Interest Coverage Ratios (ICRs)—you absolutely must master the mathematics of property investment.

Use our free, interactive rental property yield calculator uk below to stress-test your acquisition parameters. This tool strips away the marketing fluff and computes the hard numbers, instantly generating your Gross Yield and, more importantly, your True Net Yield once the heavy burdens of Stamp Duty Land Tax (SDLT), refurbishment budgets, and rigorous management costs are applied.

Property Yield Calculator

Instantly calculate your gross & net returns

Acquisition Costs

Income & Ongoing Costs

Gross Yield

6.60%

True Net Yield

4.57%

Annual Income

£13,200

Monthly Profit

£850

Total Capital Deployed (Price + Fees + Refurb)

£223,000

The Mathematics of Real Estate: Why Yield Dominates 2026

If you are treating property merely as a slow-moving savings account praying for capital appreciation, you are playing a dangerous game. From 2010 to 2021, investors could afford to ignore weak rental yields. Capital growth was rampant, fueled by historically cheap debt. Investors bought cash-bleeding assets in prime locations and simply waited for the market to bail them out.

Today, the margin of error has compressed. With higher base rates affecting BTL mortgages and landlords facing heavier regulatory burdens, your asset must cash flow. Period.

Understanding the buy to let yield formula and precisely calculating your margins upfront is no longer optional; it is the fundamental baseline of serious property acquisition.

Breaking Down the Gross vs Net Yield Calculator

Far too many novice investors confuse Gross Yield with Net Yield, a critical misunderstanding that can result in thousands of pounds of unexpected losses. Let's delineate the two metrics using a gross vs net yield calculator approach.

1. Gross Yield: The Vanity Metric

Gross Yield is the raw, unrefined return of a property before any expenses are subtracted. It represents the total annual revenue generated by the asset divided by its upfront sticker price.

The Formula:

(Annual Rental Revenue ÷ Property Purchase Price) × 100 = Gross Yield %

Example Scenario: You acquire a terraced house in Birmingham for £210,000. It generates £1,200 per calendar month (pcm).

- Annual Revenue: £1,200 × 12 = £14,400

- Calculation: (£14,400 ÷ £210,000) × 100

- Gross Yield = 6.85%

While useful for rapidly screening hundreds of Rightmove listings, Gross Yield is fundamentally flawed. It ignores the friction of actually buying and running the house.

2. True Net Yield: The Professional's Metric

Net Yield is the metric that dictates if you will actually make money. It measures the profit remaining after all operational costs have been paid, weighed against the total capital you actually deployed to acquire the asset, not just the purchase price.

The Formula:

(Net Annual Profit ÷ Total Capital Deployed) × 100 = True Net Yield %

To accurately use a gross vs net yield calculator, you must calculate the true denominator and the true numerator.

Total Capital Deployed (The True Denominator):

- Purchase Price

- Stamp Duty Land Tax (SDLT) + 5% Investor Surcharge

- Conveyancing and Legal Fees

- Brokerage and Valuation Fees

- Upfront Refurbishment Costs (e.g., £15k for a new kitchen and EPC upgrade)

Net Annual Profit (The True Numerator):

- Gross Rent minus:

- Letting agent management fees (10-15%)

- Landlord insurance (buildings and liability)

- Maintenance and repair buffers (typically 5-8% of rent)

- Void periods

- Service charges and ground rent (if leasehold)

When utilizing a comprehensive rental property yield calculator uk, a supposed 7% gross yield can quickly reveal itself to be a sub-4% net yield once the grim reality of taxes and management fees are applied.

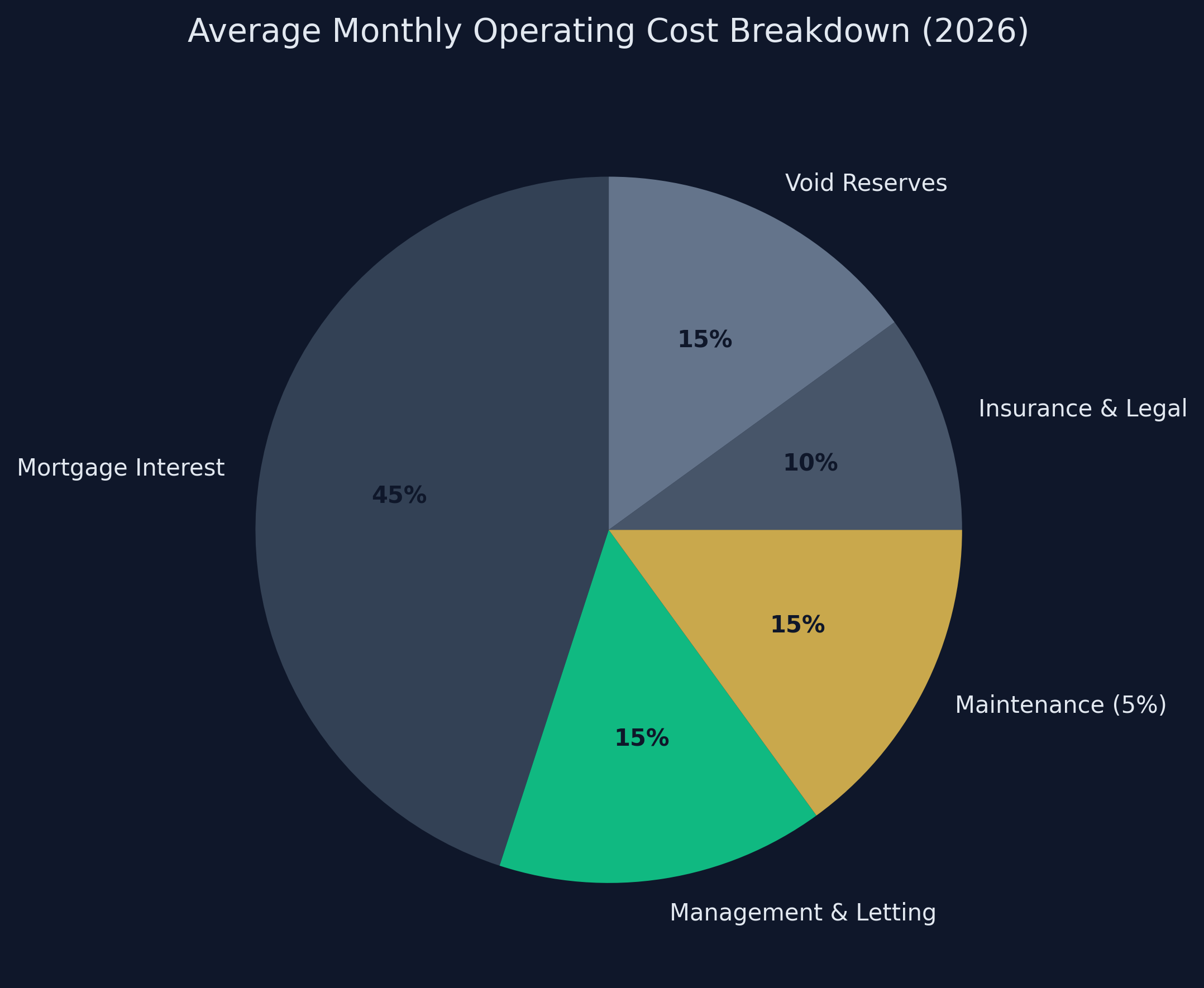

The Brutal Reality: Operating Costs Rental Property Investors Must Factor In

To achieve accuracy in your cash flow forecasting, you cannot underestimate the operating costs rental property landlords encounter. A common pitfall is assuming that because a property is newly refurbished, it requires zero OPEX (Operating Expenditure).

1. Management and Letting Fees

Unless you are prepared to handle 3 AM calls regarding a blown boiler or navigate the complexities of serving Section 21 notices, you will employ a letting agent. Fully managed services in the UK routinely charge between 10% and 15% plus VAT of the monthly rent.

2. The Maintenance Buffer

Professional financial modelers never assume zero repairs. You should automatically deduct 5% to 8% of the gross rent to build a maintenance sinking fund. Over a five-year holding period, you will face appliance breakdowns, minor plumbing issues, and eventual redecoration costs.

3. Factoring in Void Periods

An occupied property cash flows; an empty one bleeds money. Even in high-demand markets, tenant transitions inevitably result in void periods. Your baseline model should assume the property sits vacant for two to three weeks every year, costing you both lost rent and associated utility standing charges during that time.

4. Regulatory Certifications

The modern landlord operates a heavily regulated business. Annually, you must budget for gas safety certificates (CP12), Periodic Electrical Inspection Reports (EICR) every five years, and increasingly rigorous EPC compliance upgrades.

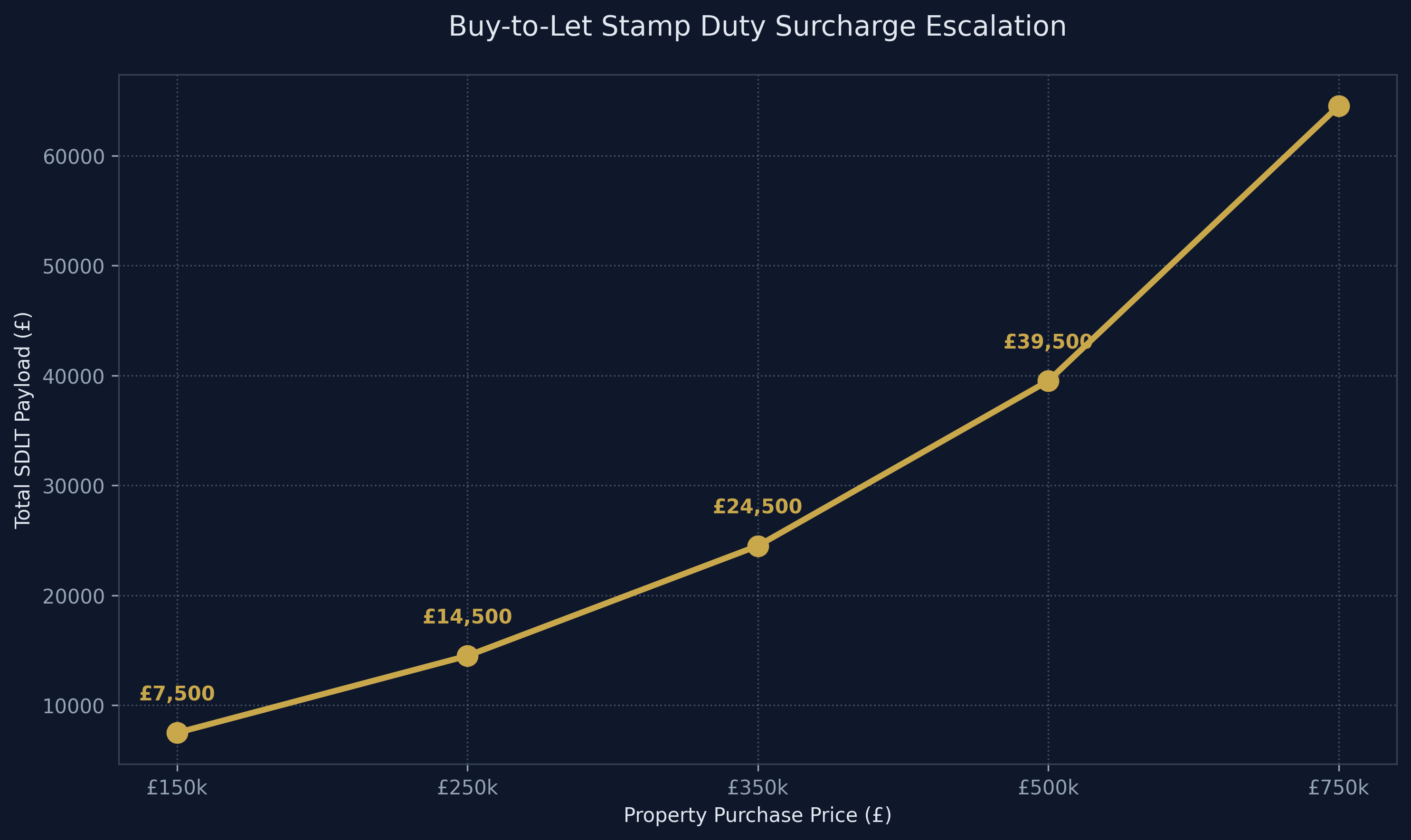

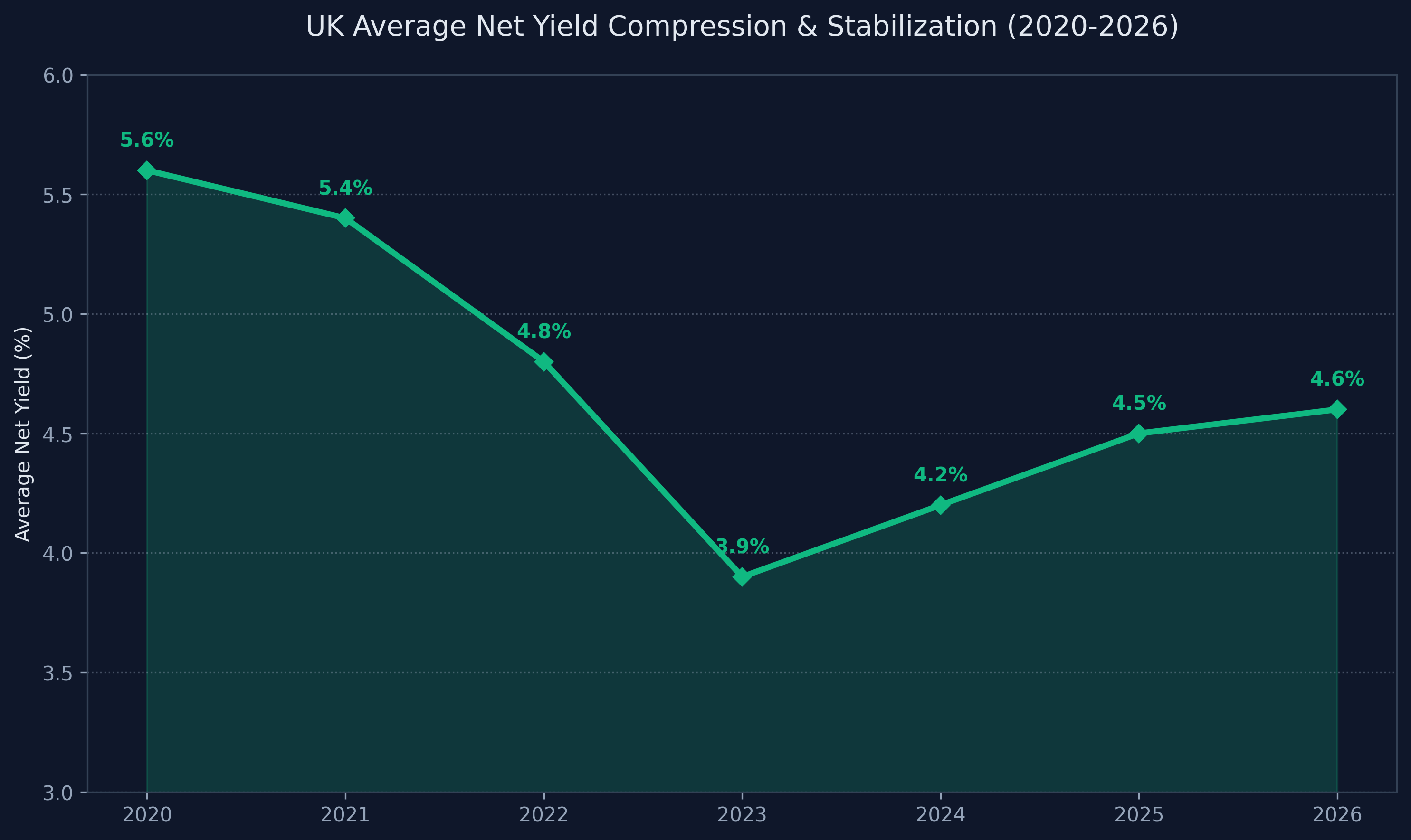

Navigating the 2026 Landscape: Stamp Duty Impact on Yield

The heaviest blow to a property investor's upfront capital in the UK is taxation. Using a stamp duty impact on yield calculator reveals the immense friction SDLT places on the BTL model.

The 5% additional property surcharge is relentless. It applies to the entire purchase price and entirely eradicates the nil-rate band that standard homebuyers enjoy. For instance, purchasing a £350,000 investment property will incur an agonizing £24,500 in SDLT. That £24,500 is fundamentally "dead capital" – it adds zero value to the asset but heavily inflates your "Total Capital Deployed," thereby crushing your True Net Yield.

When modeling acquisitions, you must calculate your "SDLT Recovery Time" – the number of months your net cash flow will have to operate just to earn back the tax handed to the government on day one.

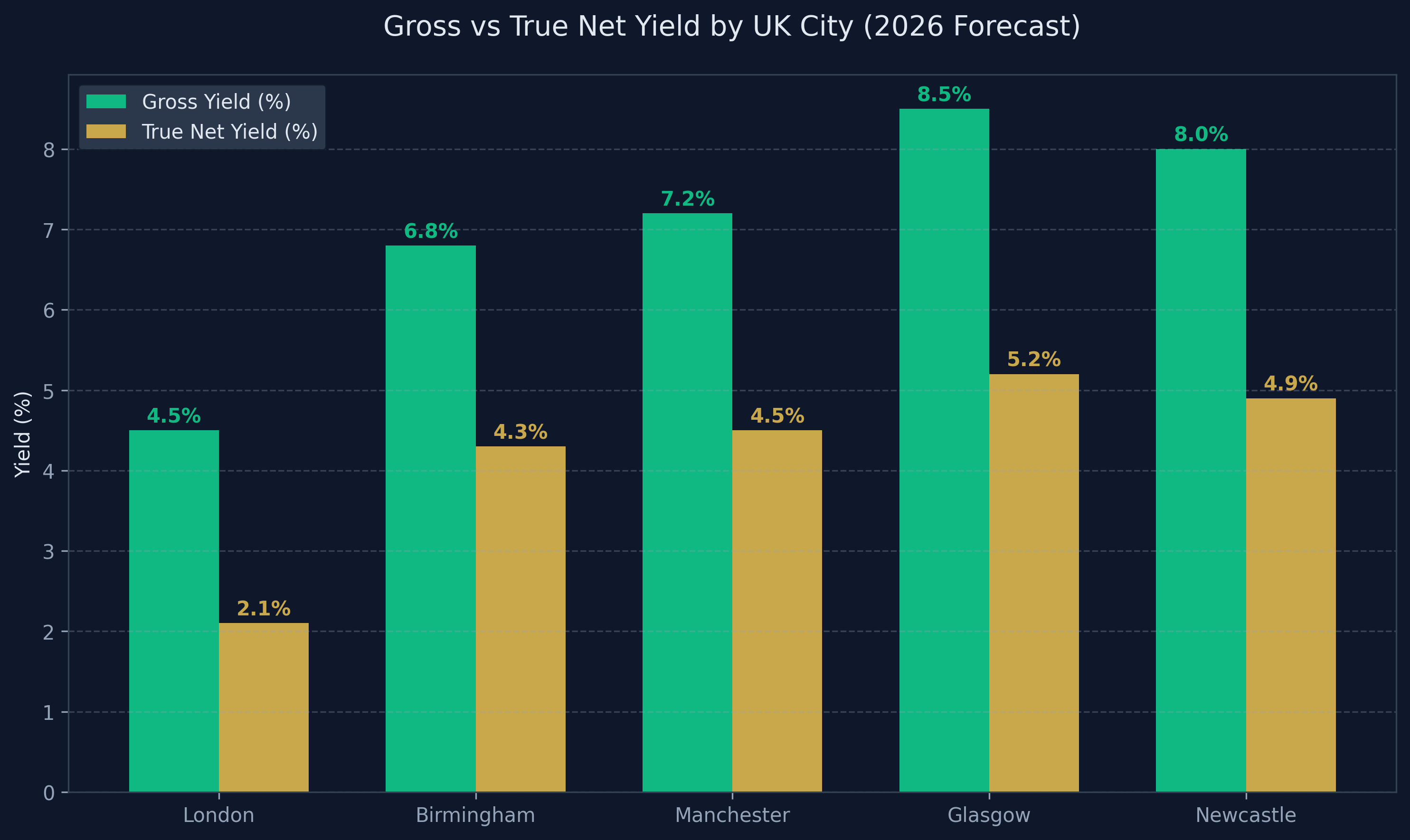

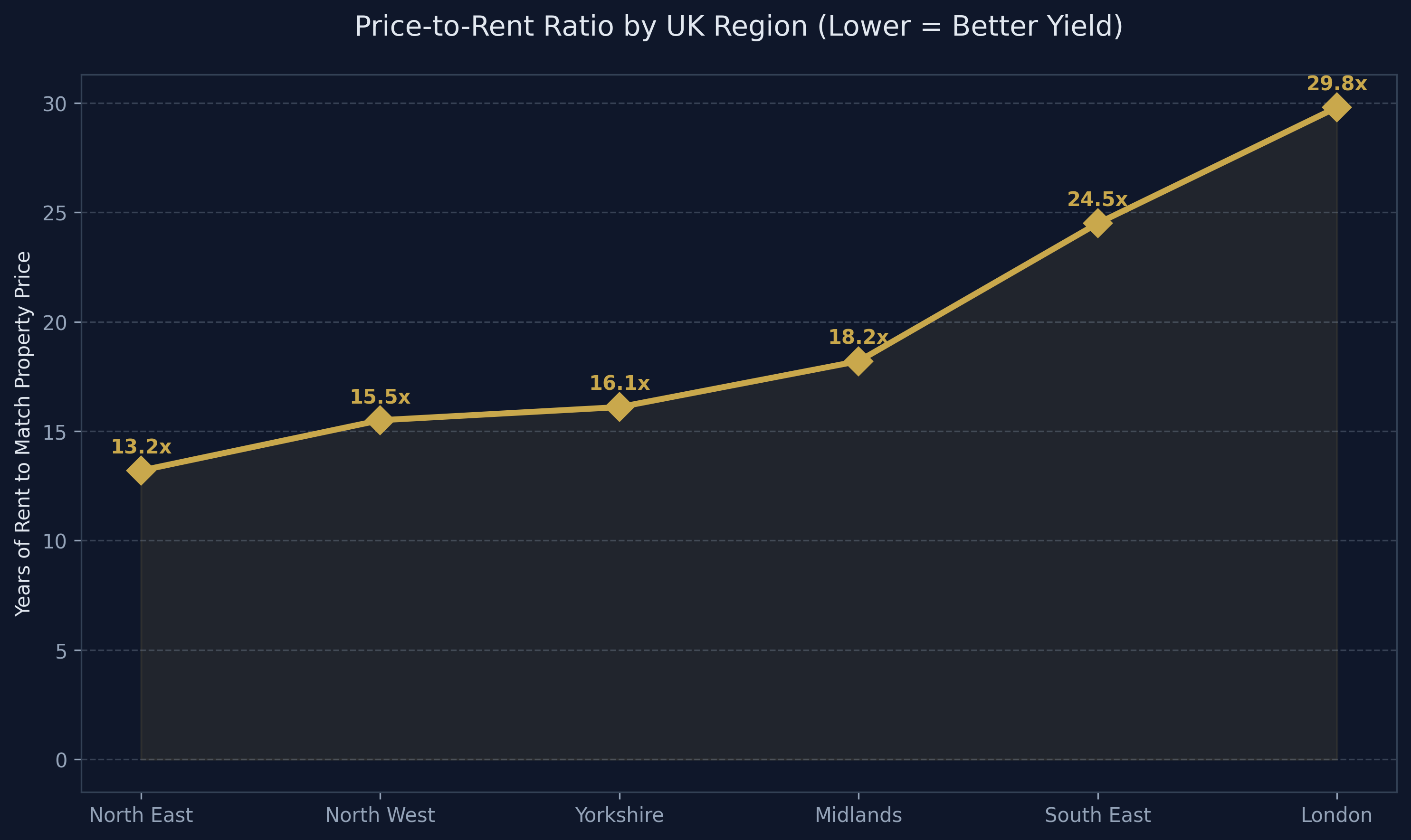

What Constitutes a Good Rental Yield UK 2026?

A frequent question generated when utilizing a rental property yield calculator uk is: "What is the benchmark I should be aiming for?" The definition of a good rental yield uk 2026 is geographically fragmented.

The Standard Single-Let Metrics

For traditional, 2-3 bedroom residential homes, investors should be seeking a baseline Gross Yield of 6.0% to 7.5%.

- <a href="/post/foreign-investment-in-<a href="/post/foreign-investment-in-london-real-estate" style="color:#c9a84c;text-decoration:underline;font-weight:500">london-real-estate" style="color:#c9a84c;text-decoration:underline;font-weight:500">London and the Commuter Belt: Yields here are chronically compressed due to hyper-inflated capital values. Gross Yields typically hover between 3.5% and 4.8%. Investors in these zones are largely executing wealth-preservation strategies, betting entirely on long-term capital appreciation rather than monthly cash flow.

- The Midlands and the North: Markets like <a href="/post/investment-property-<a href="/post/investment-property-manchester-uk" style="color:#c9a84c;text-decoration:underline;font-weight:500">manchester-uk" style="color:#c9a84c;text-decoration:underline;font-weight:500">Manchester, Sheffield, Leeds, and Liverpool offer the golden ratio where property prices remain accessible while tenant demand pushes rents upward. These regions can reliably deliver Gross Yields of 6.5% to 8.0%, making the mathematics of leveraged investment far more palatable.

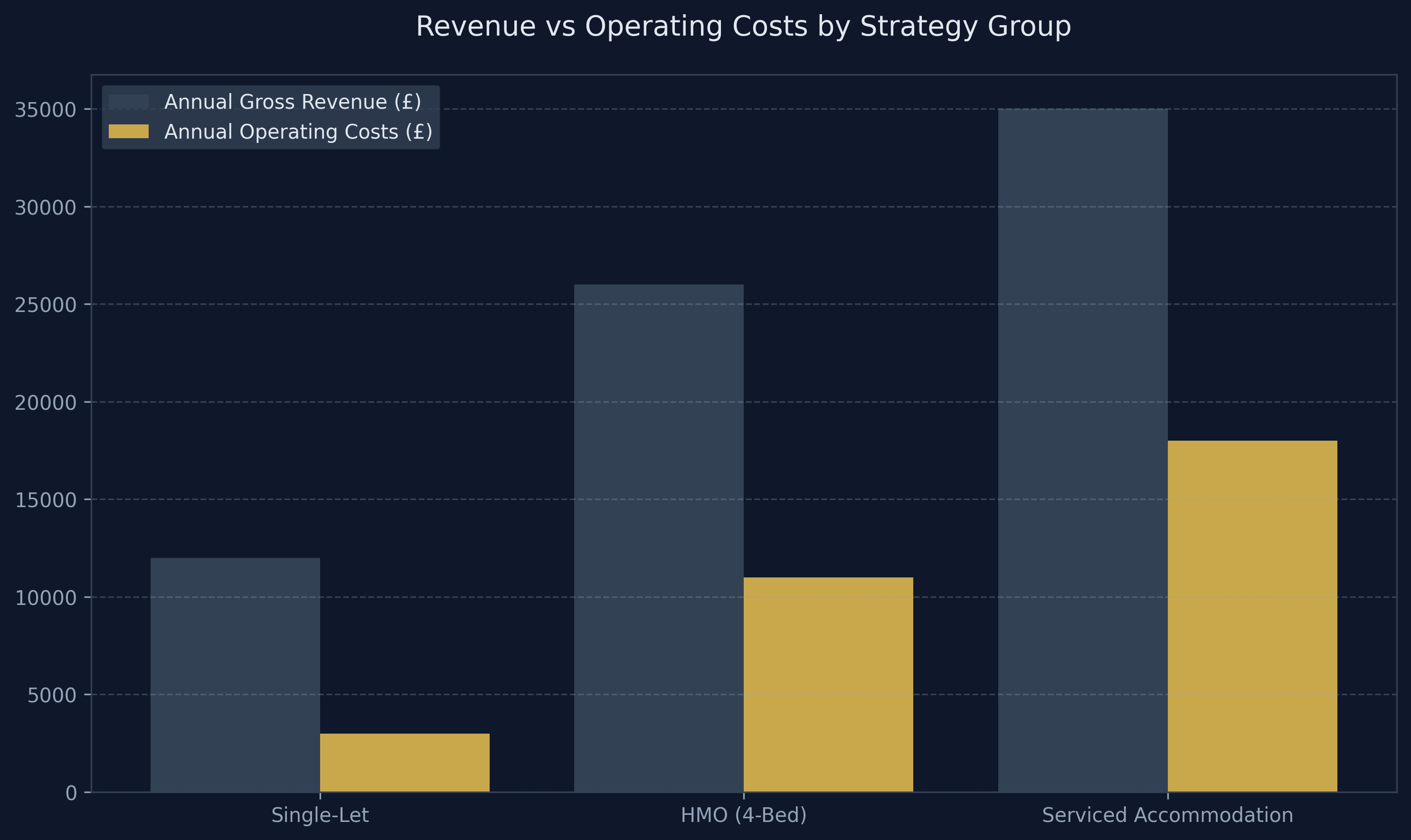

The HMO Yield Premium

If a 6.5% yield is insufficient for your cash flow goals, the alternative strategy is the House in Multiple Occupation (HMO). By converting a single property into multiple en-suite rooms, landlords can supercharge the gross revenue, frequently achieving Gross Yields between 9% and 13%.

However, achieving an impressive Gross Yield on an HMO requires absorbing substantial utility costs (gas, electric, council tax, broadband are typically included in the rent) and significantly higher ongoing management. The gap between Gross and Net yield in the HMO sector is massive.

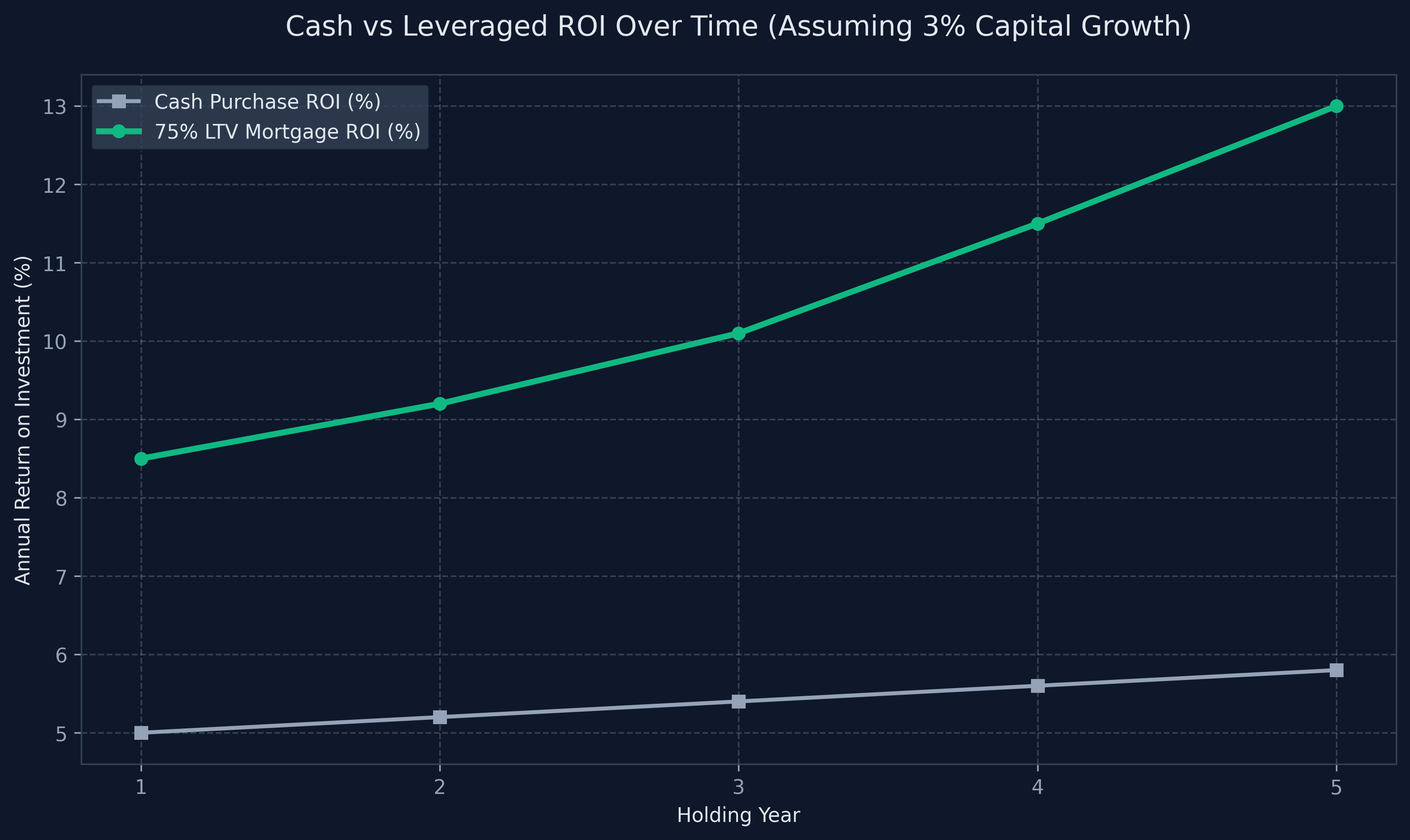

The Core Metric: ROI Calculation Property

While yield measures the performance of the asset itself, it does not measure the performance of your cash. For that, you need a targeted roi calculation property matrix.

Return on Investment (ROI) evaluates the net profit generated relative specifically to the actual cash deposit you deployed. This is where leverage (BTL Mortgages) fundamentally alters the equation.

If you purchase a £200,000 house in cash, your £10,000 net profit represents a 5% ROI. If, however, you purchase that same £200,000 house using a £50,000 deposit and a 75% LTV mortgage, your metrics change. Assuming the mortgage interest costs you £7,500 annually, your net profit drops to £2,500. Yet, because you only deployed £50,000 of your own cash (plus SDLT and fees, let's say £65,000 total), your actual cash-on-cash ROI jumps:

(£2,500 net profit / £65,000 cash deployment) = 3.8% ... Wait, in a low-yield scenario, heavy debt can actually reduce your cash return. But if the gross yield stands at a robust 8.5%, the leveraged ROI can easily spike to 12-15%, demonstrating precisely why BTL investors utilize debt to accelerate portfolio growth.

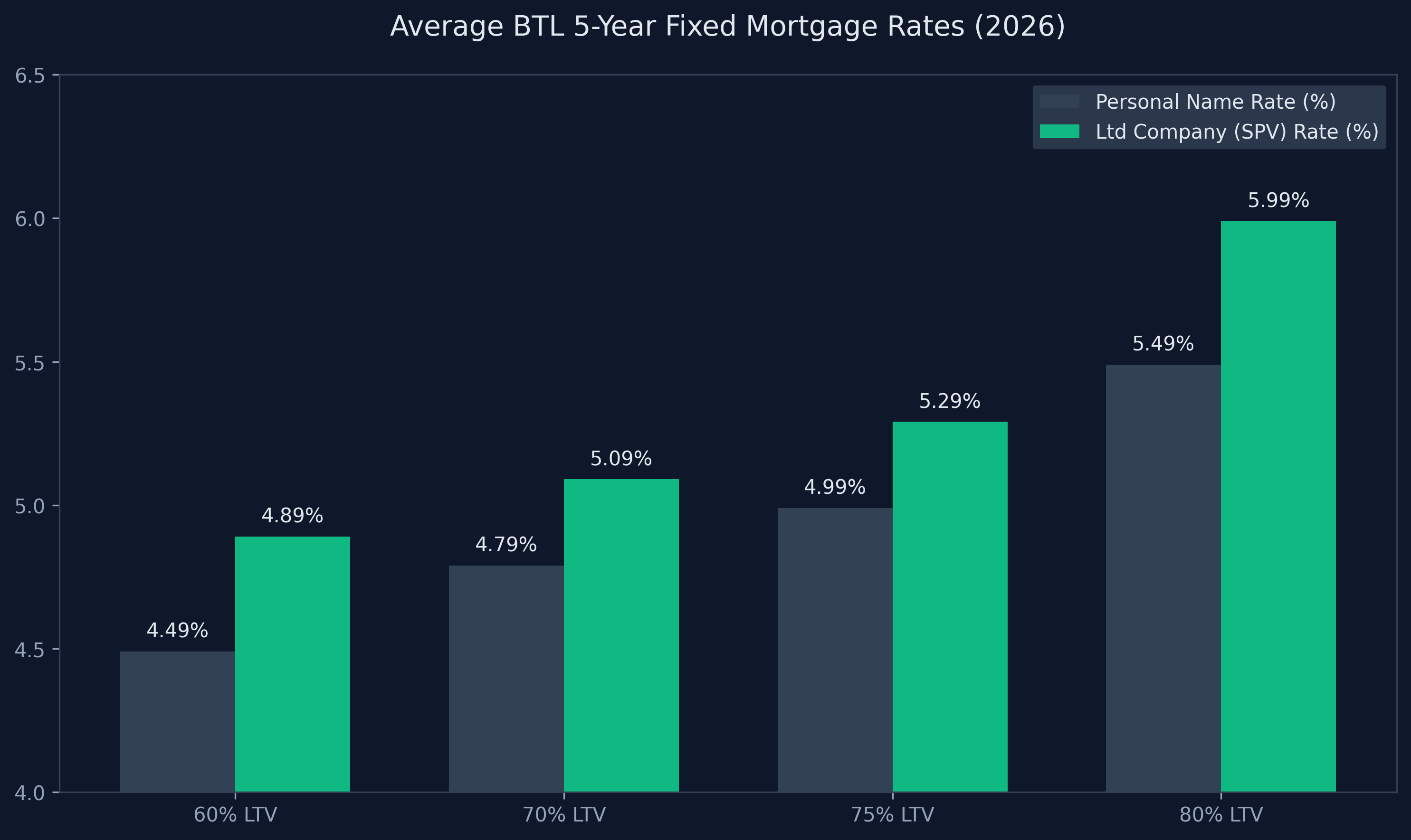

Interest Coverage Ratios (ICRs)

You cannot arbitrarily apply immense leverage in 2026. Commercial lenders enforce strict ICRs, typically demanding that the property's rental income covers 125% to 145% of the mortgage interest (stress-tested at a hypothetical 5.5% rate or higher). If your yield is too weak, the lender will simply refuse the loan or demand a much heavier deposit, neutralizing the benefits of leverage.

The Future of UK Property Yields

We are witnessing a structural shift in the UK housing market. The era of the "amateur landlord" is dissolving. Increased regulatory friction, heightened taxation via Section 24 (which restricts mortgage interest tax relief for individual owners), and the looming necessity for EPC retrofitting are forcing landlords to treat property precisely as a business.

The most successful investors in 2026 are those who possess absolute clarity over their numbers. They leverage Limited Company SPV structures to shield their profits from penal upper-rate income taxes, they source properties meticulously below market value, and they continuously stress-test acquisitions against variable base rates.

Every decision must begin and end with accurate mathematical forecasting. The definitive first step is establishing absolute reliance on a robust rental property yield calculator uk. If the spreadsheet bleeds, the deal fails. It is merely a numbers game; ensure you are calculating yours with precision.

5 Essential Tactics to Enhance Your Property's Cash Flow Post-Acquisition

Running a rental property yield calculator uk doesn't stop the moment you receive the keys. Proactive landlords constantly seek pathways to optimize and elevate the yield profile of their standing portfolio. If your current net yield is stagnating in the low 4% range, here are five granular, actionable strategies to compress expenses and force revenue upward.

1. Refinance Through an SPV to Mitigate Section 24

If you are holding high-yielding property in your personal name and sit within the higher or additional rate tax brackets (40% or 45%), you are being crippled by Section 24 tax regulations. These rules prevent you from fully deducting your mortgage interest as a standard business expense, meaning you are effectively paying tax on gross revenue rather than genuine net profit.

By incorporating your portfolio into a Limited Company Special Purpose Vehicle (SPV), you undergo a fundamental shift in tax treatment. SPVs pay Corporation Tax (which maxes out at 25% but is often lower for smaller profits), entirely bypassing the crippling personal income tax bands. Furthermore, SPVs can cleanly deduct 100% of mortgage interest as a direct operating expense. Running your metrics through a gross vs net yield calculator under an SPV constraint often transforms a heavily taxed, low-yield personal asset into a highly profitable corporate venture.

2. Execute Micro-Refurbishments for Premium Rent

Tenant expectations in 2026 have radically evolved. The standard of Private Rented Sector (PRS) stock has increased, and professional tenants willing to pay premium rents demand premium finishes.

You do not need to execute a £40,000 "back-to-brick" renovation to shift the needle. Targeted, high-ROI micro-refurbishments yield the best results:

- The Kitchen Refresh: Instead of tearing out cabinets, professionally respray the doors in deep navy or sage green, install brass hardware, and swap the worktop layout.

- Flooring: Replace tired carpets with high-durability luxury vinyl tile (LVT) in herringbone patterns. It is pet-proof, spill-proof, and immediately elevates the aesthetic of the listing.

- Smart Tech Integration: Install smart thermostats (like Hive or Nest) and video doorbells. These small additions signal a premium technology-oriented environment, easily justifying an additional £50-£75 per calendar month in localized markets.

3. Transition to the Serviced Accommodation (SA) Model

If the standard residential buy to let yield formula is yielding insufficient localized returns (e.g., hitting a ceiling of 6% gross in a city centre), pivoting the asset strategy to Short-Term Lettings (Serviced Accommodation / Airbnb) can unlock phenomenal cash generation.

By targeting corporate relocations, weekday contractors, and weekend tourism, an apartment that achieves £1,200 pcm on a standard Assured Shorthold Tenancy (AST) might easily generate £2,800 to £3,500 gross per month on the short-term market.

The Caveat: The SA model carries extreme OPEX. Your operating costs rental property matrix will explode to include constant cleaning fees, high-speed commercial broadband, channel manager software, inflated utility consumption, and 15-20% platform commissions (Airbnb/Booking.com).

4. Relentlessly Negotiate Operational Friction

Landlords often bleed yield through sheer laziness. Your operating expenses are not fixed laws of physics; they are highly negotiable business contracts.

- Management Fees: If you have handed a letting agent a portfolio of 4 properties resulting in £50,000 of annual rent roll, you should absolutely not be paying their standard 12% retail rate. Negotiate aggressively for a portfolio rate of 8-9%.

- Insurance Block Policies: Do not insure properties individually using retail comparator websites. Utilize a specialist commercial broker to weave your portfolio into a single, unified block policy. The economies of scale instantly compress premiums.

- Pre-Emptive Maintenance: Service boilers annually before winter. Clear guttering in November. Spending £200 on preventative maintenance eliminates the £1,500 emergency call-out fee when the roof leaks on Christmas Eve.

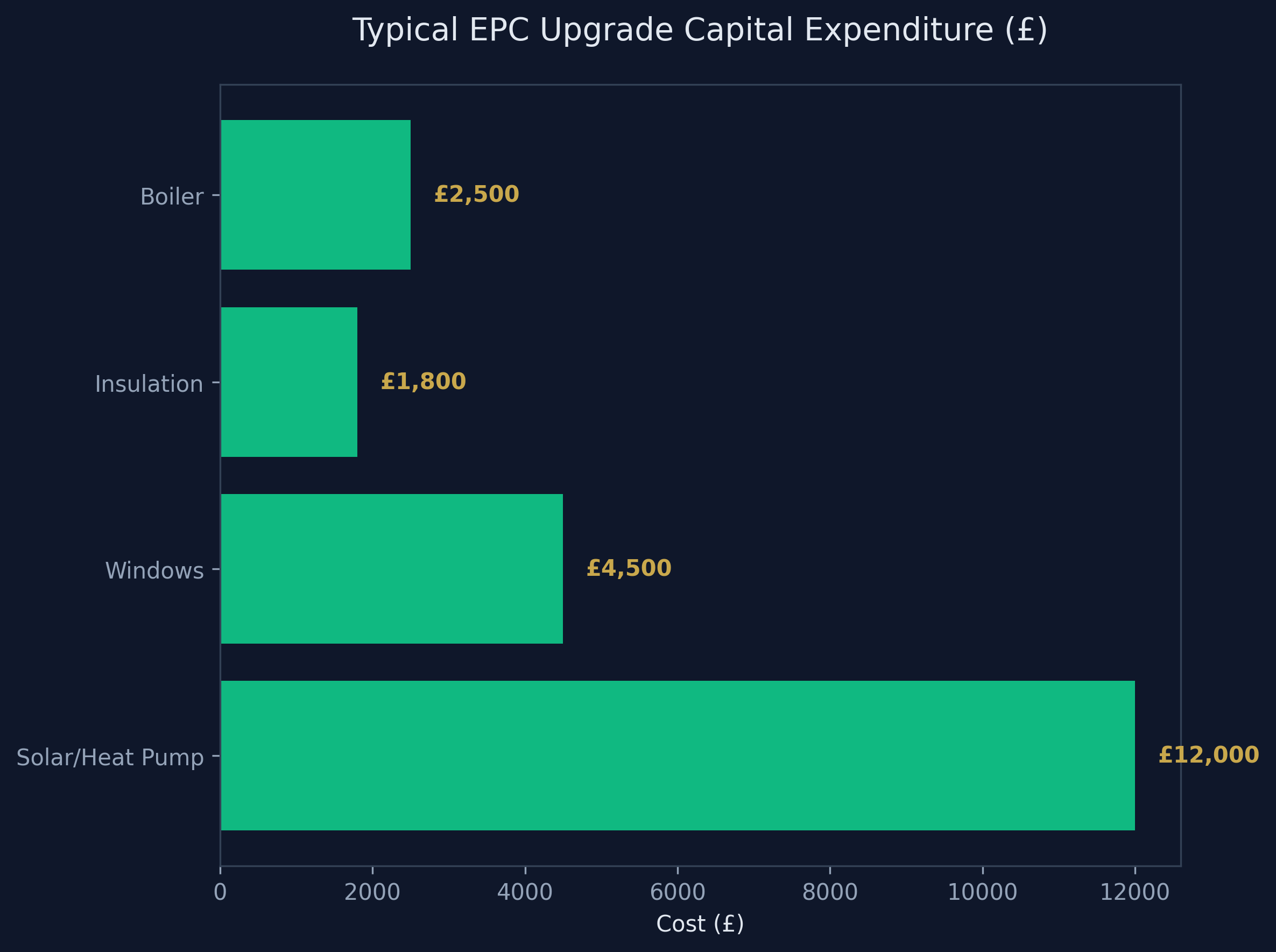

5. Optimize the EPC Rating Proactively

We have previously touched upon the stamp duty impact on yield, but the upcoming EPC regulations possess an equally violent sting to your long-term ROI. Government mandates driving the minimum standard toward 'C' mean heavily penalizing legislation for non-compliant properties.

If your asset sits at an 'E', you must bake energy-efficient upgrades into your capital expenditure model immediately. Waiting until the regulatory deadline allows contractors to hike prices due to immense market demand. Install modern heat retention measures now; not only does it future-proof the legality of your asset, but 'A' or 'B' rated properties qualify for "Green Mortgages" which offer notably lower interest rates, slicing your heaviest operational cost right at the source.

Advanced Deal Analysis: Stress Testing the Void Danger

The greatest enemy modeled by a rental property yield calculator uk is the void period. High interest rates are manageable if they are predictable; a sudden three-month localized vacancy is lethal to cash flow.

Professional deal analysis requires viewing a prospective asset through the lens of worst-case scenarios.

- Assess the Demographic Ceiling: If you acquire a 4-bedroom detached house in an area where the median household income is £35,000, setting your rent projection at £2,500 pcm is a fundamental misunderstanding of the market. The macroeconomics simply do not support the product.

- Micro-Location Proximity: Does the asset physically sit within a 15-minute walk of major rail infrastructure, a hospital, or a university? Those micro-locations offer absolute insulation against void periods. When the wider economy contracts, properties adjacent to structural employment hubs retain their tenant demand.

Finally, an accurate roi calculation property matrix must forecast the exit strategy. A spectacular yield over 7 years means very little if the localized heavy industry closes down, collapsing the capital value of the asset by 25% just as you intend to liquidate. Yield generates the cash, but capital preservation secures the wealth. Master the calculator, respect the numbers, and invest with absolute mathematical detachment.

Comprehensive Property Investment FAQ (2026 Focus)

As investors calibrate their strategies utilizing the rental property yield calculator uk, a myriad of complex tactical questions arise. Below, we address the critical pain points defining the modern UK housing market.

Q: Can I completely avoid the 5% Stamp Duty Surcharge? A: Not on a standard single-residential acquisition. The 5% surcharge is legally pervasive. The only structural exemptions exist within commercial real estate, mixed-use properties (which fall under commercial SDLT rules), and the "Rule of Six" (purchasing six or more residential units in a single transaction, thereby triggering commercial taxation thresholds). Utilizing a stamp duty impact on yield tool will quickly confirm that attempting offshore routing or SPV structuring does not bypass this domestic levy.

Q: Is a 5% Gross Yield viable in London in 2026? A: It depends entirely on your capital structure. If you are deploying 100% cash, a 5% gross yield will result in a positive, though modest, true net yield. However, if you are applying 75% LTV leverage utilizing a commercial BTL mortgage at 5.5% interest rates, a 5% gross yield is mathematically destructive. Your operating costs rental property liabilities will physically exceed the rental income, operating the asset at an active monthly loss. The capital appreciation must be astronomical to justify subsidizing the asset from your own salary.

Q: How do interest-only mortgages impact the yield equation? A: Interest-only mortgages are the lifeblood of the professional BTL sector. They drastically compress your monthly debt obligation compared to a traditional repayment mortgage. This maximizes your monthly cash flow (and thereby your Net Yield) allowing you to reinvest the surplus liquidity into acquiring further assets. However, it means the principal loan amount never decreases; you are relying entirely on inflation and capital growth to build equity over the 25-year term.

Q: What is the most accurate way to calculate ROI on a refurbishment project? A: To master the roi calculation property matrix for a refurbishment (BRRR) project, strictly track every single pound of deployed cash.

- Note the purchase price deposit.

- Add the SDLT and legal fees.

- Add the exact refurbishment cost (£20,000).

- Refinance the property at the new, elevated valuation.

- Extract the newly generated equity from the mortgage.

- Subtract the extracted equity from your total initial cash deployment. Your final ROI is calculated purely against whatever residual cash you were unable to pull back out. If you pull all your cash back out, your ROI sits at infinity.

Q: Why do HMOs generate higher yields than Single Lets? A: A standard buy to let yield formula reveals that renting a physical space to four independent individuals on separate tenancy agreements generates significantly higher total gross revenue than renting the identical square footage to a single family unit. You are heavily monetizing the physical footprint of the asset. However, the caveat is intense operational expenditure: the landlord is legally liable for utilities, council tax, commercial-grade fire alarms, licensing fees, and elevated maintenance.

Q: Are Limited Company (SPV) mortgages more expensive? A: Historically, yes. SPV mortgage products typically carried interest rates 0.5% to 1.5% higher than personal-name BTL products, alongside significantly heavier arrangement fees. However, as the industry has structurally shifted toward corporatization to escape Section 24 taxes, the competitive lender landscape has narrowed this gap. In 2026, the premium for an SPV mortgage is often marginal, and the massive corporation tax advantages comprehensively outweigh the slightly elevated interest rate.

Q: Does EPC rating actually affect the capital value of an investment? A: Imminently, yes. A property possessing an EPC rating of 'E' or 'F' is effectively distressed housing stock. Savvy investors utilizing a gross vs net yield calculator will aggressively undercut the asking price of an inefficient property, knowing they must directly absorb £10,000+ of immediate capital expenditure to legally rent the asset once the new government compliance deadlines hit. Conversely, an energy-efficient 'B' rated property commands a clear market premium.

Q: Should I include Ground Rent and Service Charges in my calculations? A: Absolutely. This is the single largest pitfall for investors acquiring leasehold apartments. Service charges in major UK cities can easily exceed £2,000 annually and are subject to violent inflationary hikes by management companies. When running the rental property yield calculator uk, these charges must be subtracted from your gross rent before calculating the net profit. Failing to account for a heavy service charge will instantly annihilate the yield of what otherwise appears to be a lucrative apartment.

Stop being a landlord. Start being an investor.

Shaded Canvas introduces serious capital to vetted UK property opportunities — targeting 12–16% net returns.

Start Investing →