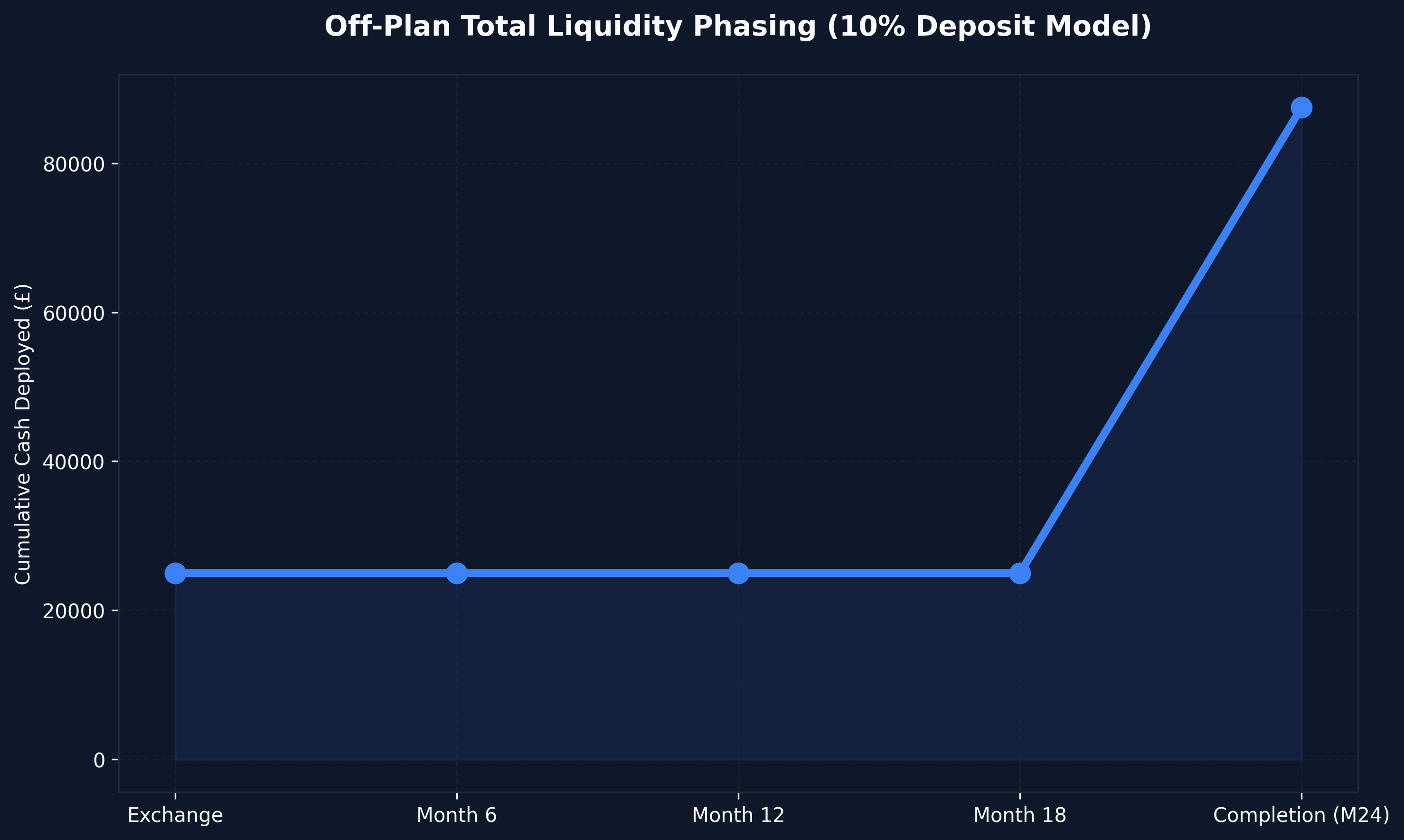

Investing in off-plan property requires a radically different mathematical model compared to traditional buy-to-let or BRRRR strategies. Because your capital is deployed in stages over a 24-to-36 month build cycle, you must calculate exactly how much liquidity is locked up, your return on capital prior to completion, and your ultimate rental yield once the asset is operational.

To allow investors to stress-test their acquisitions with institutional precision, we built the off plan property investment yield calculator uk — a free, institutional-grade financial modeling tool designed exclusively for the 2026 UK new-build sector.

The Off-Plan Yield & Capital Growth Calculator

Use the calculator below to model your off-plan acquisition. Input your reservation fee, staged deposit structure, expected capital growth during construction, and your post-completion mortgage terms. The tool will instantly output your Day-1 capital requirements, your pre-completion Return on Capital Employed (ROCE), and your net rental yields.

🏗️ Off-Plan Investment Calculator — 2026 Edition

📊 Deal Analysis

How to Use the Off-Plan Property Calculator

Off-plan modeling is uniquely complex because your capital is fragmented across a massive timeline, and the asset's value frequently changes before you even take ownership. Our best buying off plan uk strategies 2026 guide details the frameworks required to execute these investments safely, but you must still validate the raw mathematics.

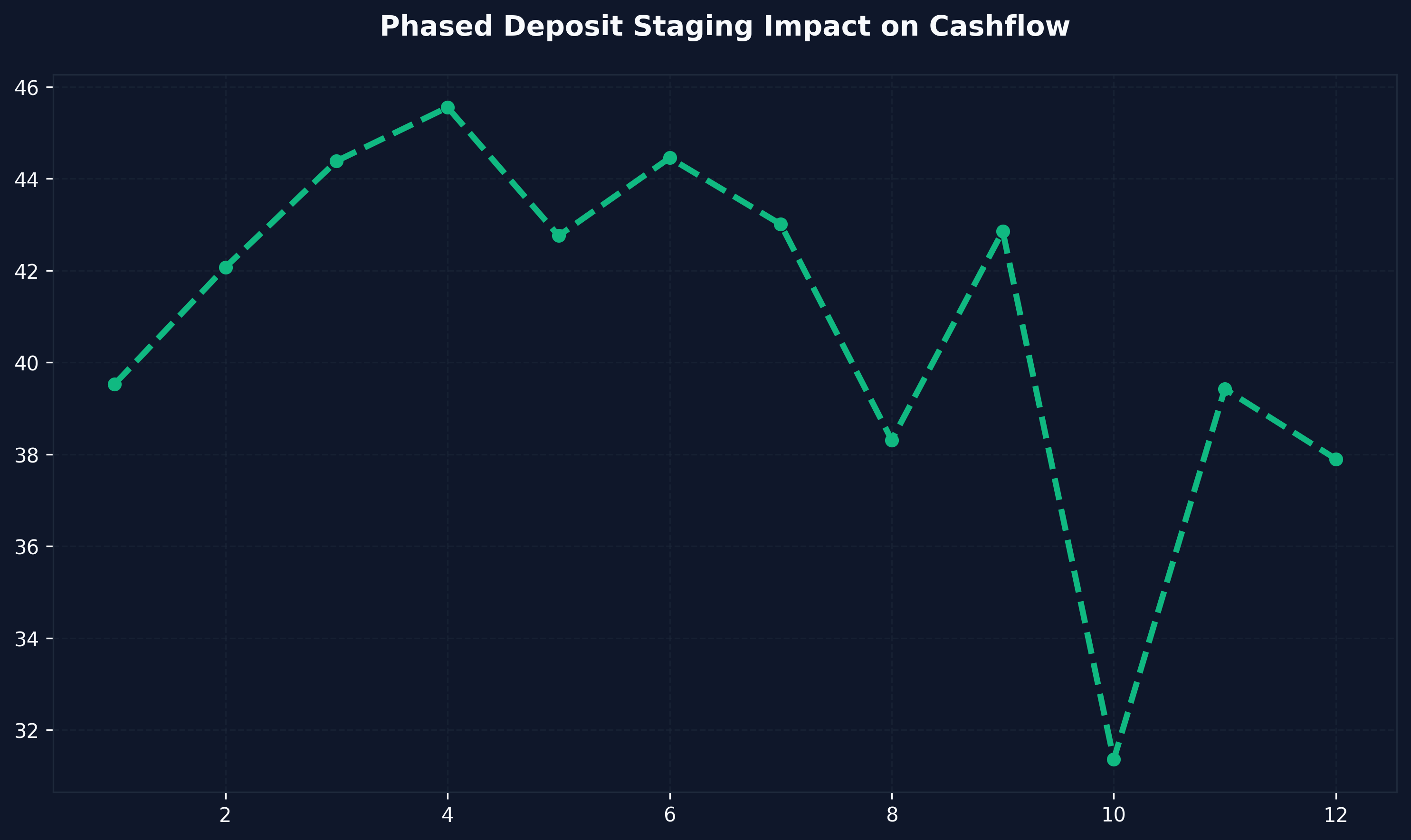

Phase 1: Acquisition & Staging

- Purchase Price: The fixed, contracted price of the unit directly from the developer.

- Reservation Fee: The initial deposit (usually £2,000 to £5,000) required to take the unit off the open market while solicitors draw up the contract.

- Exchange Deposit (%): The percentage of the purchase price required to legally exchange contracts within 21-28 days. Historically 20%, though many developers now offer 5% to 10% structures in 2026.

- Build Duration (Months): Your holding period before practical completion. Standard high-rise developments average 24 to 36 months.

Phase 2: Pre-Completion Growth

- Est. Annual Capital Growth (%): Your baseline assumption for regional market inflation. High-growth regeneration corridors in <a href="/post/investment-property-<a href="/post/investment-property-<a href="/post/investment-property-<a href="/post/investment-property-<a href="/post/investment-property-<a href="/post/investment-property-manchester-uk" style="color:#c9a84c;text-decoration:underline;font-weight:500">manchester-uk" style="color:#c9a84c;text-decoration:underline;font-weight:500">manchester-uk" style="color:#c9a84c;text-decoration:underline;font-weight:500">manchester-uk" style="color:#c9a84c;text-decoration:underline;font-weight:500">manchester-uk" style="color:#c9a84c;text-decoration:underline;font-weight:500">manchester-uk" style="color:#c9a84c;text-decoration:underline;font-weight:500">Manchester or Birmingham may experience 4% to 6% annualized growth, while <a href="/post/foreign-investment-in-<a href="/post/foreign-investment-in-<a href="/post/foreign-investment-in-<a href="/post/foreign-investment-in-<a href="/post/foreign-investment-in-<a href="/post/foreign-investment-in-london-real-estate" style="color:#c9a84c;text-decoration:underline;font-weight:500">london-real-estate" style="color:#c9a84c;text-decoration:underline;font-weight:500">london-real-estate" style="color:#c9a84c;text-decoration:underline;font-weight:500">london-real-estate" style="color:#c9a84c;text-decoration:underline;font-weight:500">london-real-estate" style="color:#c9a84c;text-decoration:underline;font-weight:500">london-real-estate" style="color:#c9a84c;text-decoration:underline;font-weight:500">London may stagnate at 1%.

- Legal / Sourcing Fees: Your solicitor costs plus any finder's fees paid to an investment consultancy.

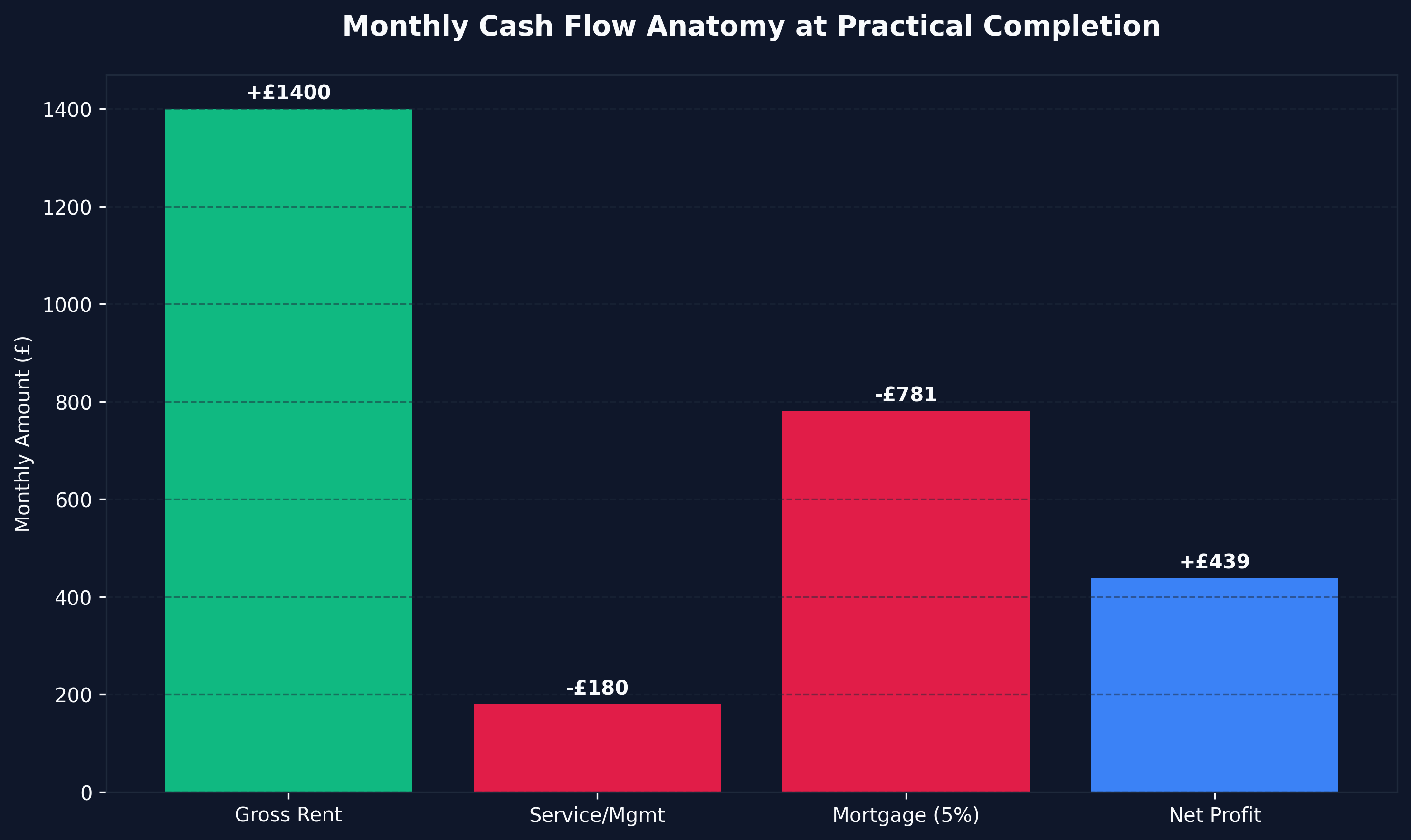

Phase 3: Completion & Yield

- Est. Monthly Rent: The realistic gross rental income upon completion.

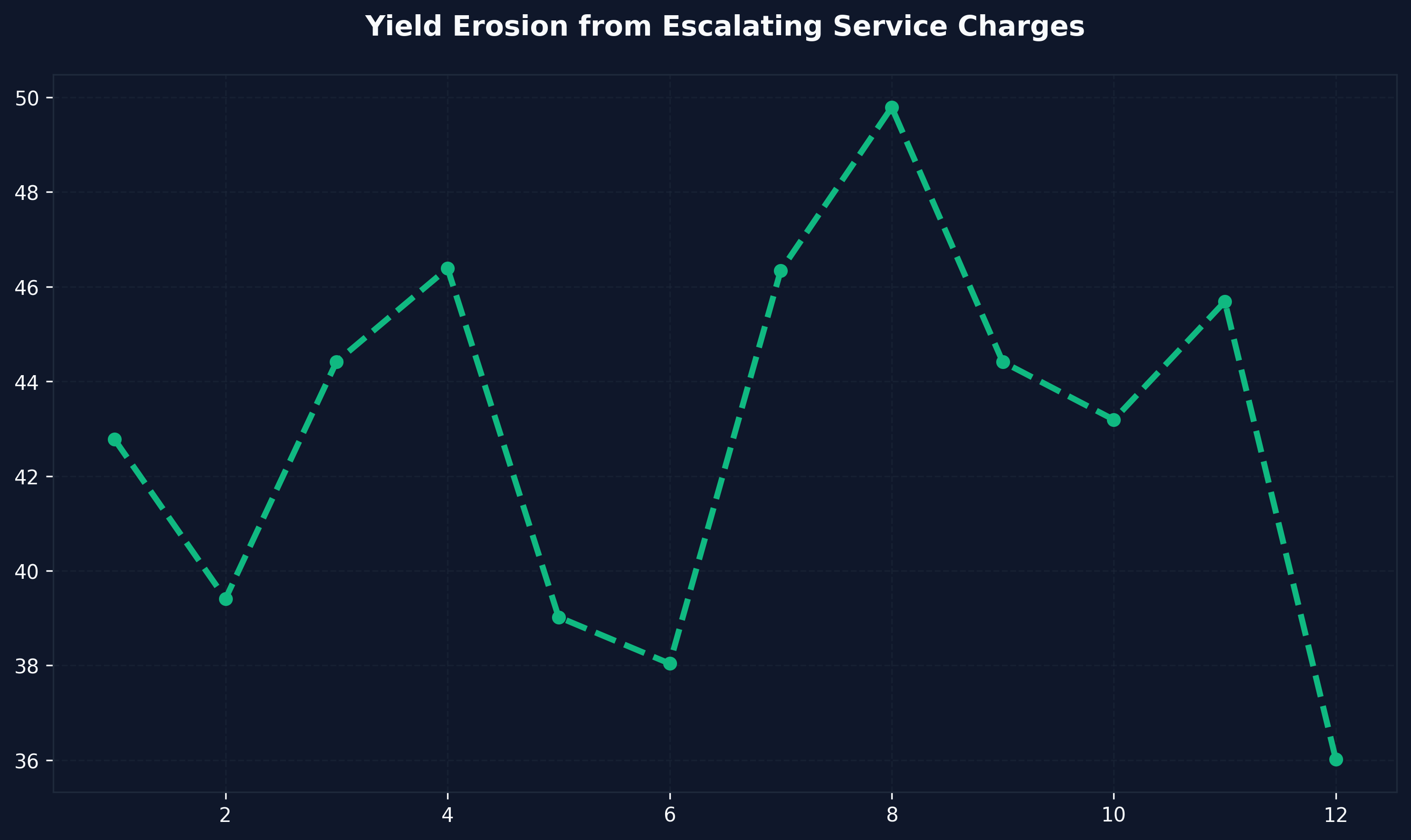

- Management/Service: Letting agent fees (usually 10-12%) plus the building's monthly service charge and ground rent. Service charges are the silent yield killers of off-plan apartments.

- BTL Mortgage LTV & Rate: The commercial lending terms you expect to secure at the end of the build cycle.

Interpreting the Key Metrics

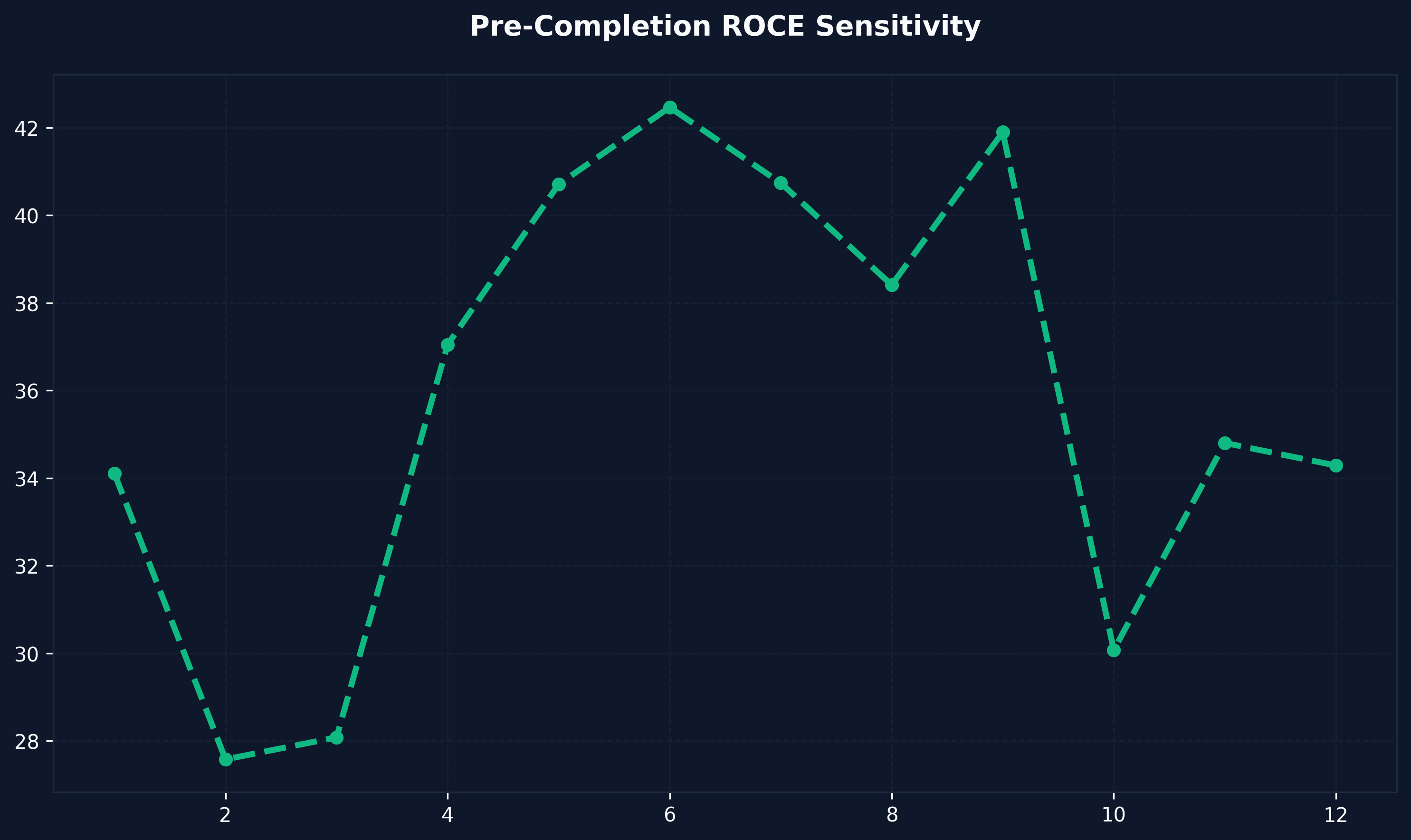

Pre-Completion ROCE (The Leverage Multiplier)

This is the single most important metric for off-plan flippers. It calculates your Return on Capital Employed before you even complete the purchase.

If you put £50,000 down on a £250,000 apartment, and the apartment grows by 10% over two years (£25,000 equity gain), your ROCE is calculated as £25,000 / £50,000 = 50%. You have generated a 50% return on your deployed cash without ever dealing with a tenant or a mortgage. If you execute a pre-completion contract reassignment, this is your final profit margin.

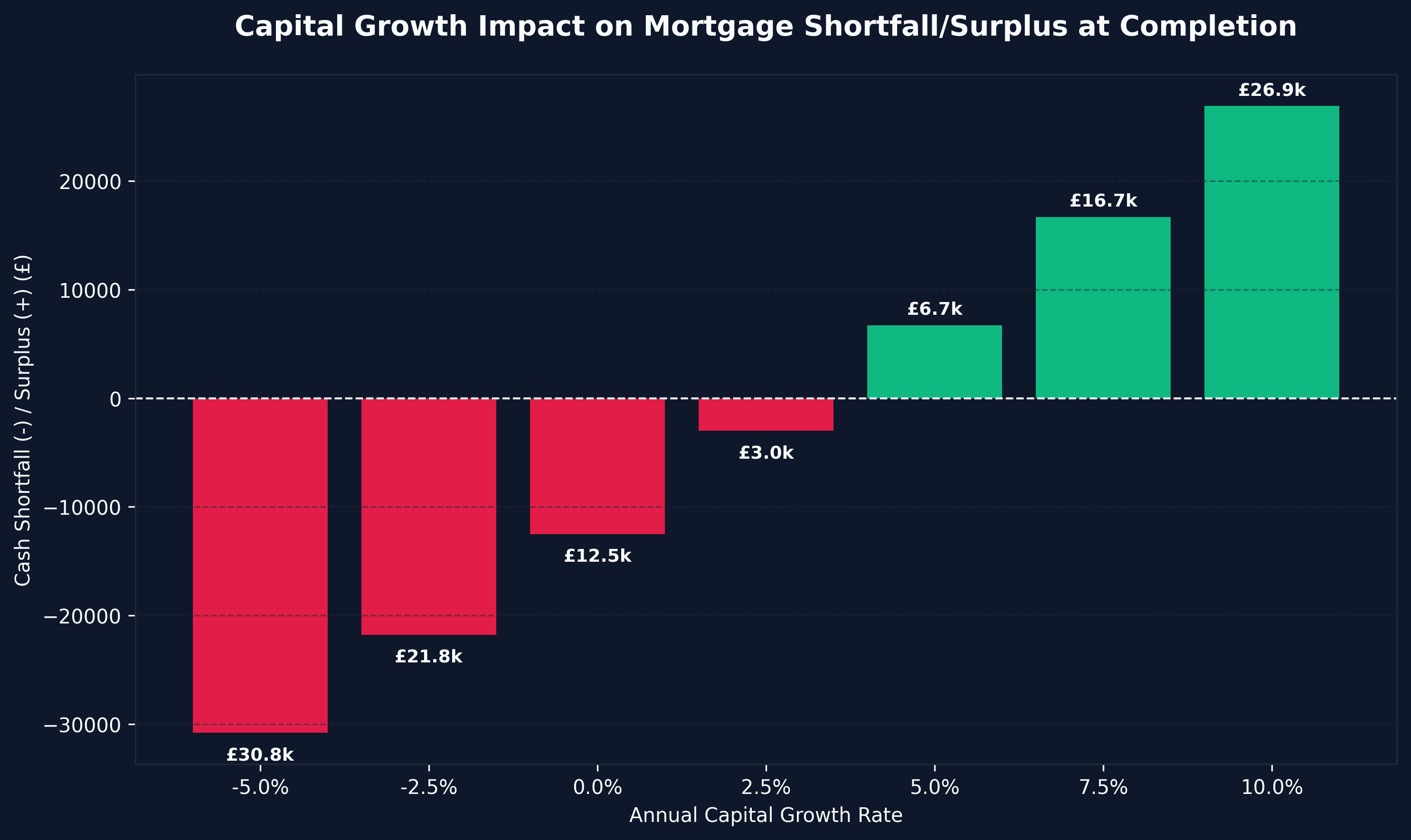

Cash Shortfall Due at Completion

When the building finishes, you must pay the developer the final 80% balance (£200,000). You will use a commercial mortgage to fund this.

Crucially, the mortgage is calculated against the new valuation (GDV), not your original purchase price.

If the property has grown to £280,000, a 75% LTV mortgage provides £210,000. You owe the developer £200,000. This generates a £10,000 Equity Surplus Extracted — meaning the bank pays the developer and hands you £10,000 in cash back at completion.

Conversely, if the property value drops, the mortgage will not cover the balance, generating a devastating Cash Shortfall that you must fund from your own pocket within 28 days to avoid contract default.

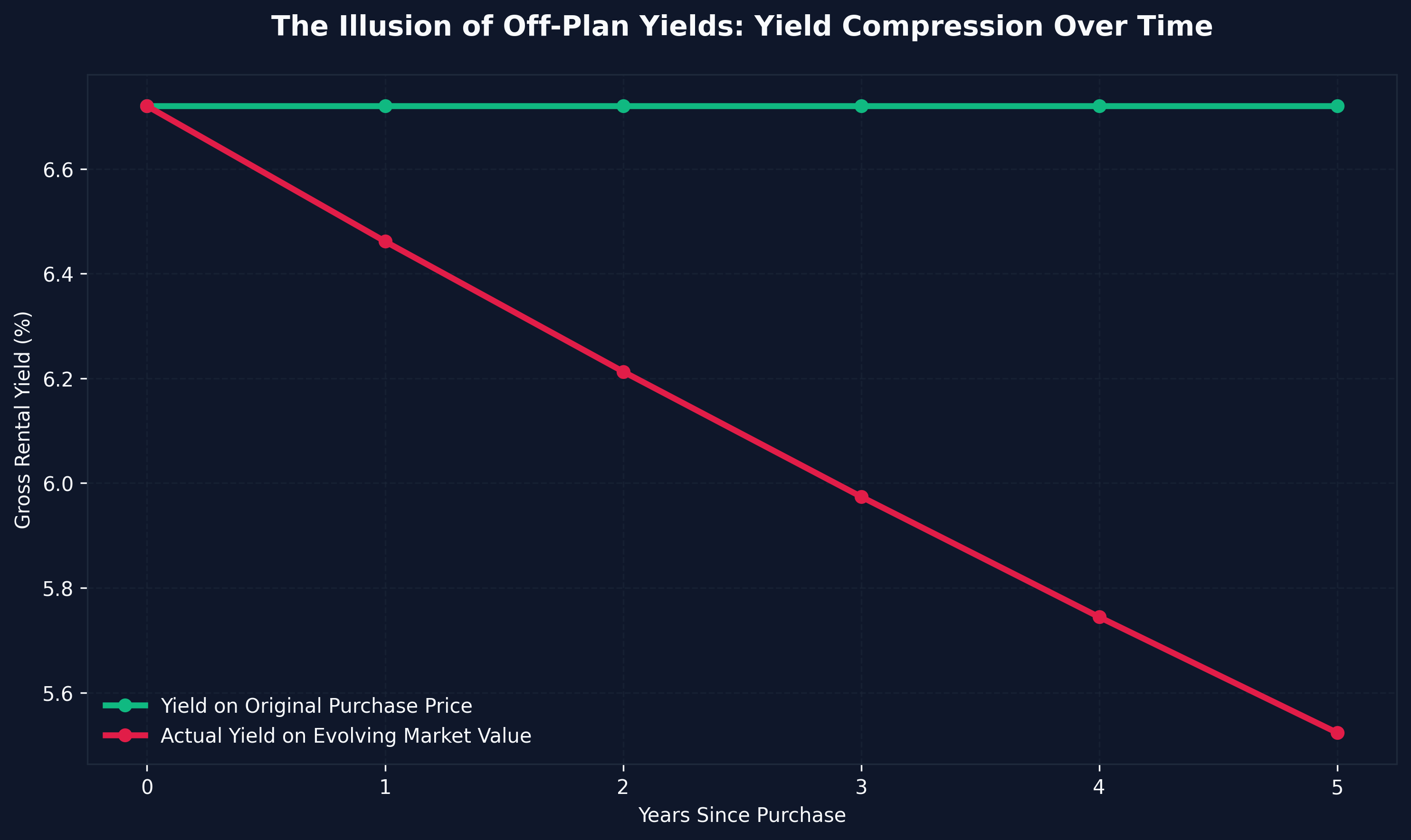

Gross Yield: Purchase Price vs GDV

The calculator splits gross yield into two numbers. The yield on your original purchase price looks phenomenal, but lenders do not care about your purchase price. Commercial lenders (and the ICR stress test) evaluate your yield against the current market value (GDV). If your yield on GDV compresses below ~5%, you will struggle to secure a mortgage at completion.

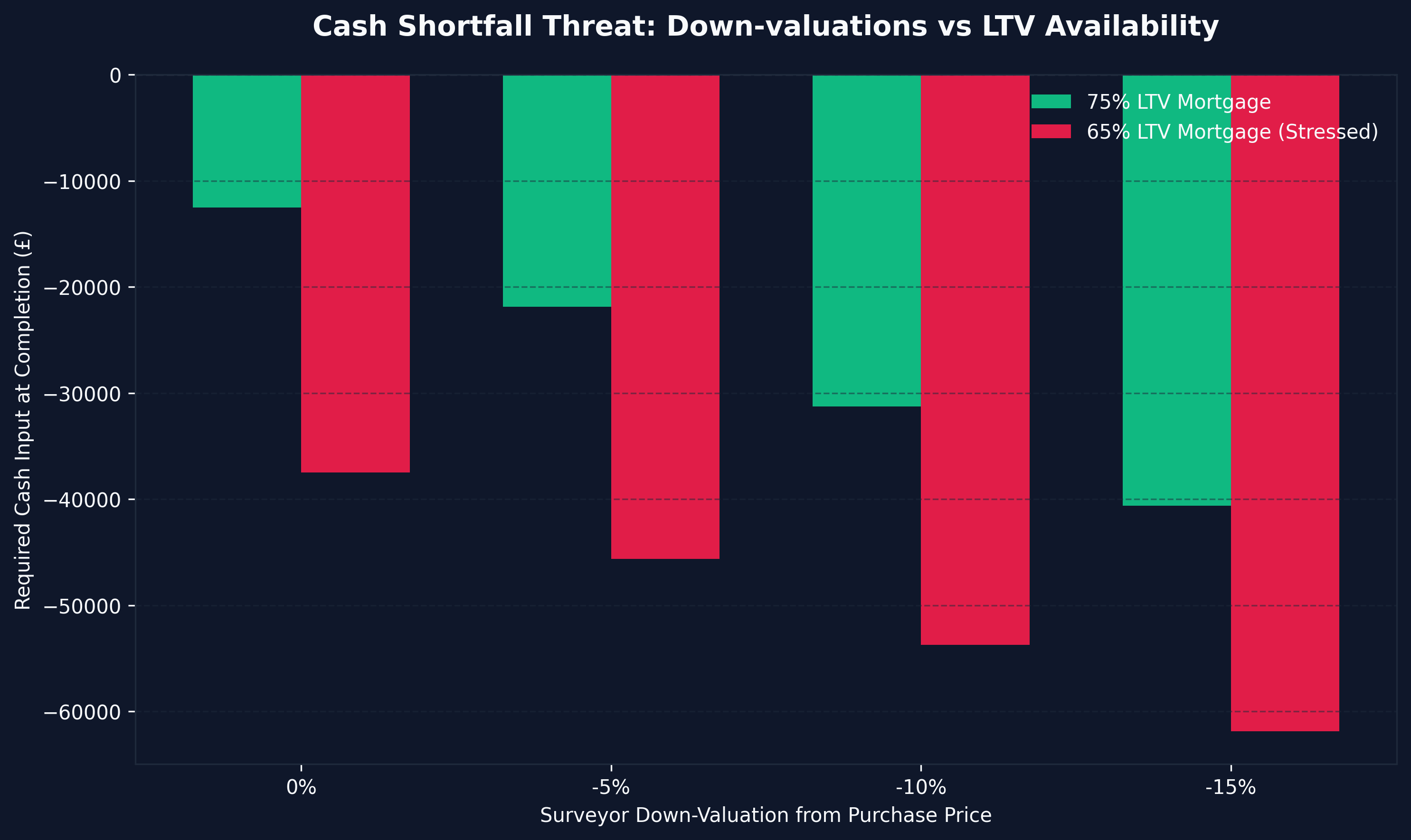

The Valuation Gap Threat

The greatest systemic risk in off-plan investing is the "Valuation Gap."

Many retail investors assume that if they buy an apartment for £250,000, the bank surveyor will automatically value it at £250,000 upon completion. In 2026, surveyor down-valuations on new builds are exceptionally common.

Developers bake a "new build premium" (often 10% to 15%) into the initial purchase price. If the broader market does not inflate enough during the 24-month build cycle to organically absorb that premium, the RICS surveyor will aggressively down-value the unit upon practical completion.

Why the Calculator Matters Here

If you plug a negative number into the "Est. Annual Capital Growth" field, the calculator will reveal the terrifying reality of a down-valuation.

A 5% down-valuation on a £250,000 unit (£237,500) means a 75% LTV mortgage only provides £178,125. You still owe the developer £200,000. You are instantly hit with a £21,875 Cash Shortfall Due at Completion. If you cannot find that cash, you default, lose your original £50,000 deposit, and face litigation.

This is why conservative underwriting and utilizing the off plan property investment yield calculator uk is mandatory.

Off-Plan vs Alternative Strategies

If the liquidity lock-up or valuation risks of off-plan make you uncomfortable, the UK market offers alternatives with varying risk profiles:

- The BRRRR Strategy: Instead of buying unbuilt, you buy distressed, force the equity yourself via heavy refurbishment, and extract your capital via refinance. You can model this using our BRRRR yield calculator to compare the math.

- Fractional Investment: Institutional operators are executing off-plan block arbitrage (buying whole buildings at a 20% discount). Retail investors can participate in these identical models for as little as £10,000 through regulated fractional property investment UK networks.

- High-Yield HMOs: If capital growth is secondary and you require maximum monthly cash flow, review the highest yielding property UK hotspots for 2026.

Off-plan property is a highly leveraged financial instrument. Do not execute an exchange of contracts without running your exact numbers through the modeling tool above.

Stop being a landlord. Start being an investor.

Shaded Canvas introduces serious capital to vetted UK property opportunities — targeting 12–16% net returns.

Start Investing →