Off-plan property investment represents one of the most polarizing asset classes in the United Kingdom. To its proponents, it is the ultimate leveraged capital growth engine—allowing investors to lock in tomorrow's valuations at today's prices using only a fraction of the total capital. To its critics, it is a high-risk gamble vulnerable to developer insolvency, stagnant market valuations, and mortgage lending crunches at completion.

The reality for 2026 straddles both narratives. The era of blindly purchasing unbuilt apartments and assuming a 20% capital uplift upon handover is over. The UK macroeconomic environment—characterized by fluctuating build costs, stringent financing matrices, and localized oversupply—demands exact, algorithmic execution.

If you want to extract yield from unbuilt developments, you must deploy the best buying off plan uk strategies 2026.

At Shaded Canvas, we underwrite off-plan acquisitions with the exact same fiscal brutality as our commercial BRRRR operations. This 3,000-word authority audit will forensically disassemble the four core off-plan strategies viable in 2026, the mathematical thresholds required to execute them, and the critical risk mitigation frameworks that separate elite institutional allocators from retail casualties.

1. The Core Mechanic: Leveraged Capital Growth

Before dissecting the specific strategies, we must establish the fundamental mathematics of the off-plan engine. The entire model hinges on leveraged capital growth prior to completion.

When you buy a standard UK property, you physically complete the purchase within three months. If the property grows in value by 5% over the next two years, you benefit from that 5% growth.

When you buy off-plan, you enter a legally binding contract (exchanging contracts) to purchase a property that will be built 18 to 36 months in the future. Crucially, you do not pay the full purchase price at exchange; you pay a deposit (typically 10% to 20%).

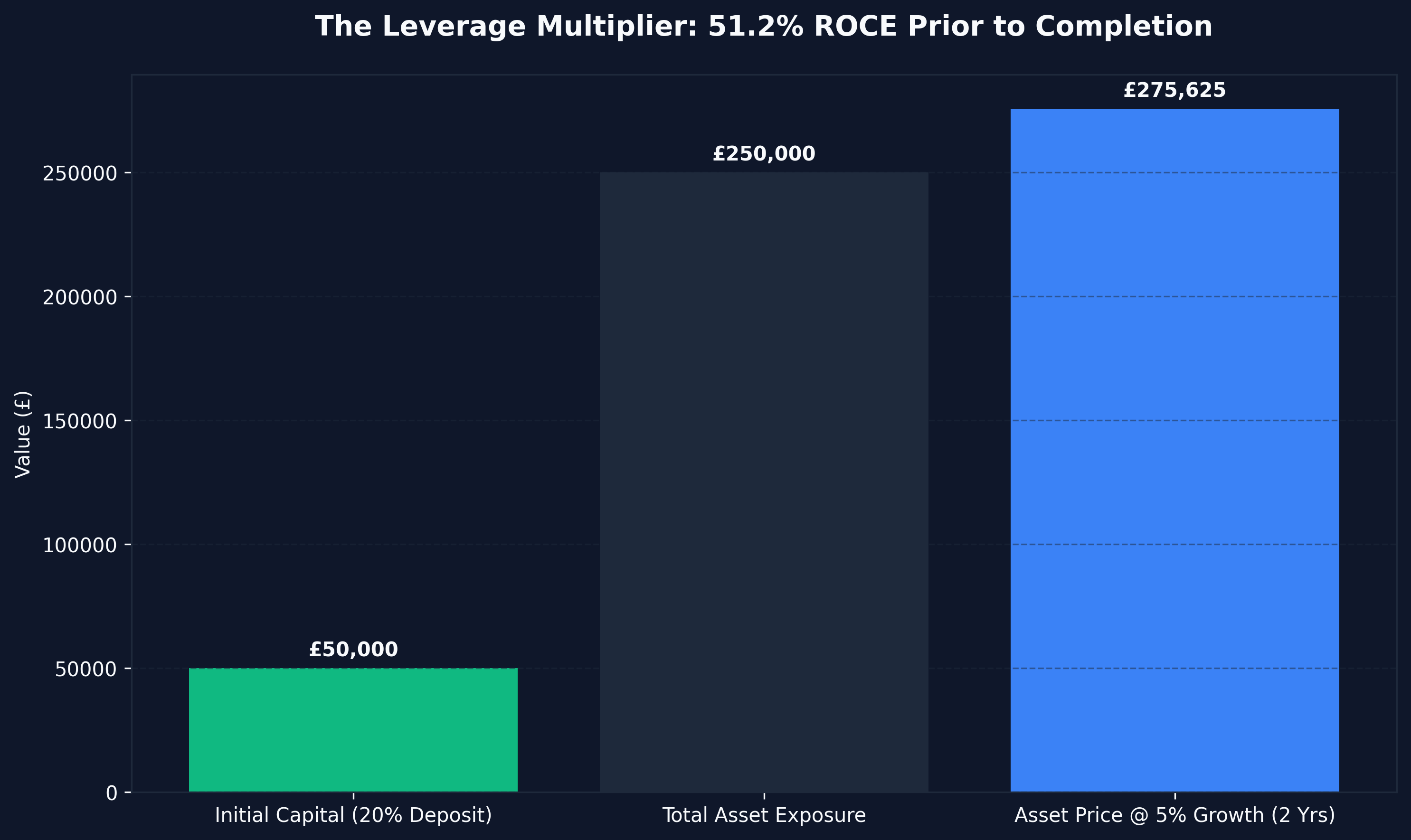

The Leverage Multiplier Effect

If you agree to buy a £250,000 unbuilt apartment and put down a 20% deposit (£50,000):

- Total Capital Deployed: £50,000

- Total Asset Exposure: £250,000

If that £250,000 asset grows in value by 5% per annum over a 24-month build cycle:

- Year 1 Growth: £12,500

- Year 2 Growth: £13,125

- Value at Completion: £275,625

You have generated £25,625 in raw capital growth. Crucially, you generated that growth using only your £50,000 deposit.

- Return on Capital Employed (ROCE) prior to completion: 51.2% (£25,625 / £50,000).

This multiplier effect is the reason high-net-worth investors and institutional syndicates heavily favour off-plan structures. You are controlling the appreciation of a quarter-million-pound asset using only fifty thousand pounds of liquidity.

Strategy 1: The "Buy and Hold" Yield Compression Model

The most common off-plan strategy for retail investors in 2026 is the classic "Buy and Hold." This involves paying the deposit during construction, securing a buy-to-let mortgage upon completion, and holding the asset long-term for rental yield and further capital appreciation.

While simple in theory, executing this effectively in 2026 requires understanding Yield Compression and Rental Escalation.

The 2026 Execution Framework

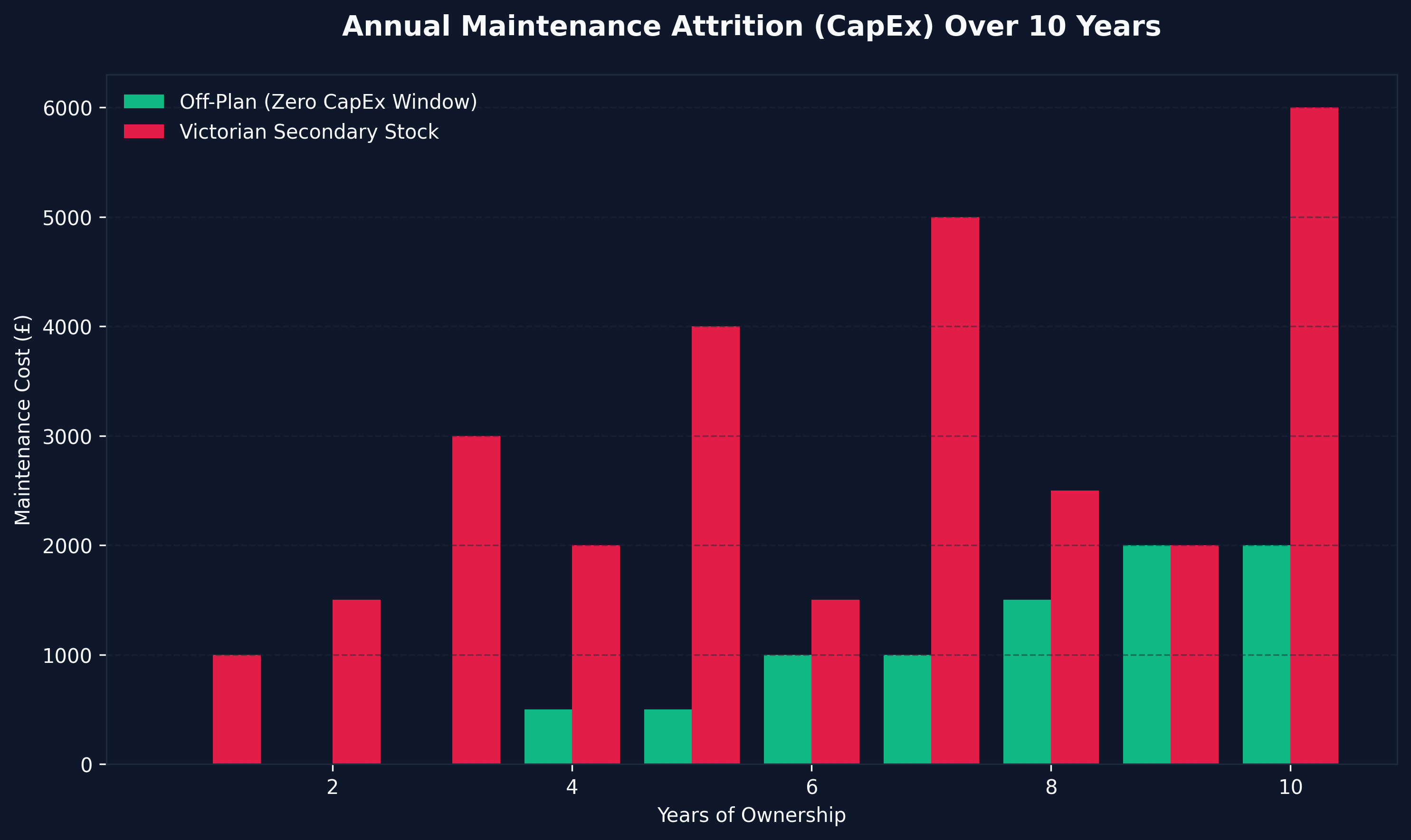

Because off-plan properties are priced at a premium ("new build premium"), the immediate gross rental yield upon completion is often lower than acquiring older, secondary housing stock. A new build apartment in Manchester might offer a 5.5% gross yield, whereas a Victorian terrace two miles away offers 7%.

The strategy relies on tenant acquisition quality and zero CapEx holding periods:

- Premium Tenant Demographics: New build developments attract affluent young professionals willing to pay a premium for amenities (gyms, co-working spaces, concierges). This demographic boasts lower default rates and higher income stability.

- The Zero CapEx Window: A key structural advantage of a new build is the 10-year structural warranty (e.g., NHBC) and the 2-year developer defects period. For the first five years of ownership, your capital expenditure (CapEx) for repairs—boilers, roofs, damp—is functionally zero.

When you factor in the zero CapEx requirement, the net yield of an off-plan apartment frequently surpasses the older Victorian terrace, which constantly bleeds cash through maintenance attrition.

The Completion Risk (The Valuation Gap)

The primary threat to the Buy and Hold strategy is the mortgage valuation gap. If you contracted to buy at £250,000, and two years later the market crashes and the bank surveyor values the completed unit at £230,000, the bank will only lend against £230,000.

If you expected a 75% LTV mortgage (£187,500), you will now only receive £172,500. You are legally contracted to complete the purchase at £250,000. This leaves a £27,500 cash shortfall that you must fund from your own personal savings within 28 days of the completion notice. If you cannot fund the gap, you default on the contract, lose your entire £50,000 initial deposit, and face litigation from the developer.

This highlights the absolute necessity of maintaining heavy liquid cash reserves when executing off-plan strategies.

Strategy 2: Pre-Completion Flipping (Contract Reassignment)

For aggressive, highly capitalized investors, pre-completion flipping is the apex predator of off-plan strategies. This involves securing a unit specifically to sell the contract to a third party before the building is completed.

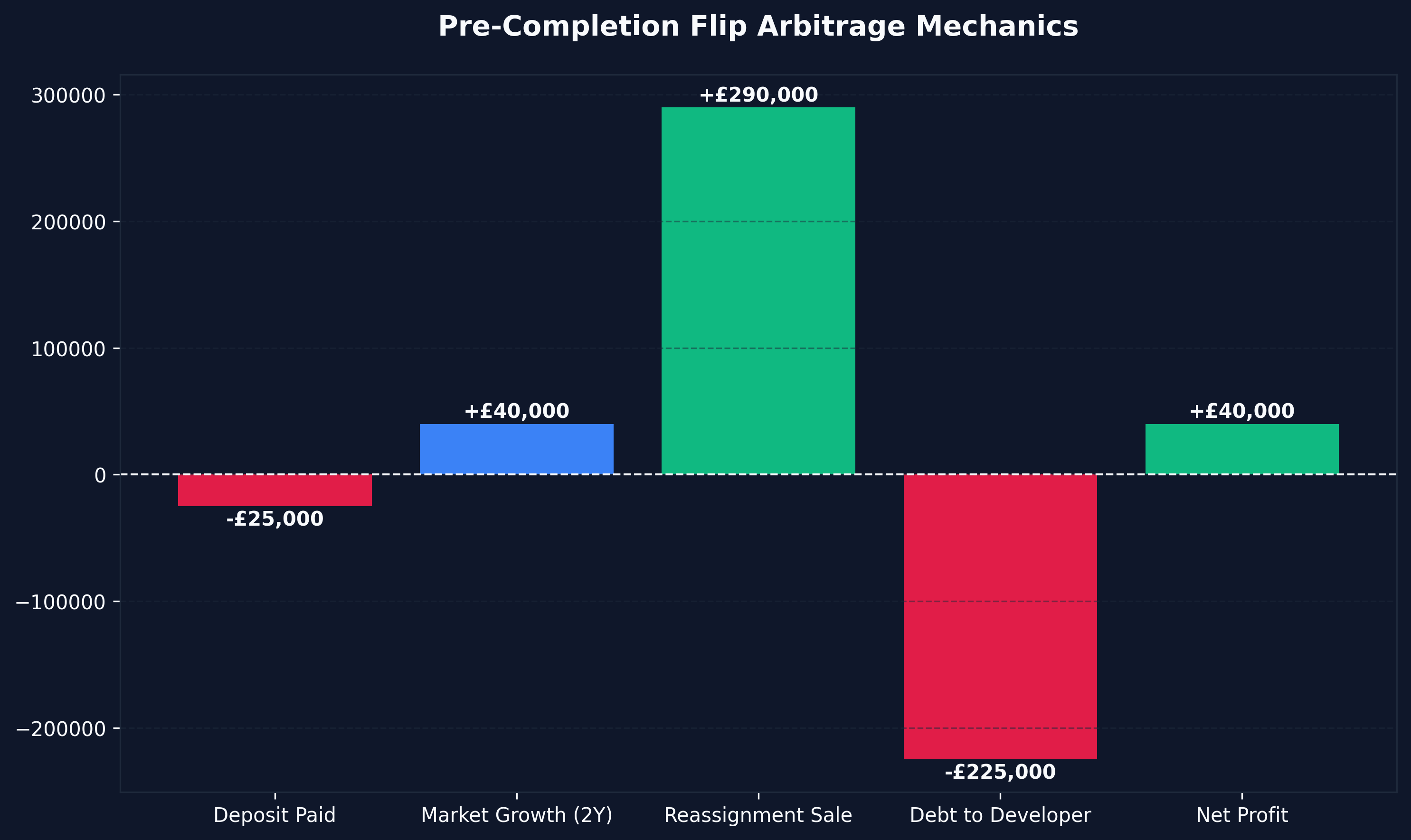

The Mechanics of the Flip

- Year 1: You exchange contracts on a £250,000 unit, paying a 10% deposit (£25,000).

- Year 2: The development nears structural completion. The market value of the unit rises to £290,000 due to inflation and derisking (the building actually exists now).

- The Reassignment: Instead of applying for a mortgage and completing the purchase, you "reassign" (sell) your contract to another buyer.

- The Math: The new buyer pays £290,000. That money is split: £225,000 goes to the developer (the outstanding balance you owed), £25,000 goes back to you (your initial deposit), and the remaining £40,000 goes to you as pure capital profit.

You just generated a £40,000 profit on a £25,000 investment (160% ROCE) without ever taking out a mortgage or paying Stamp Duty Land Tax (SDLT), because you never legally completed the purchase.

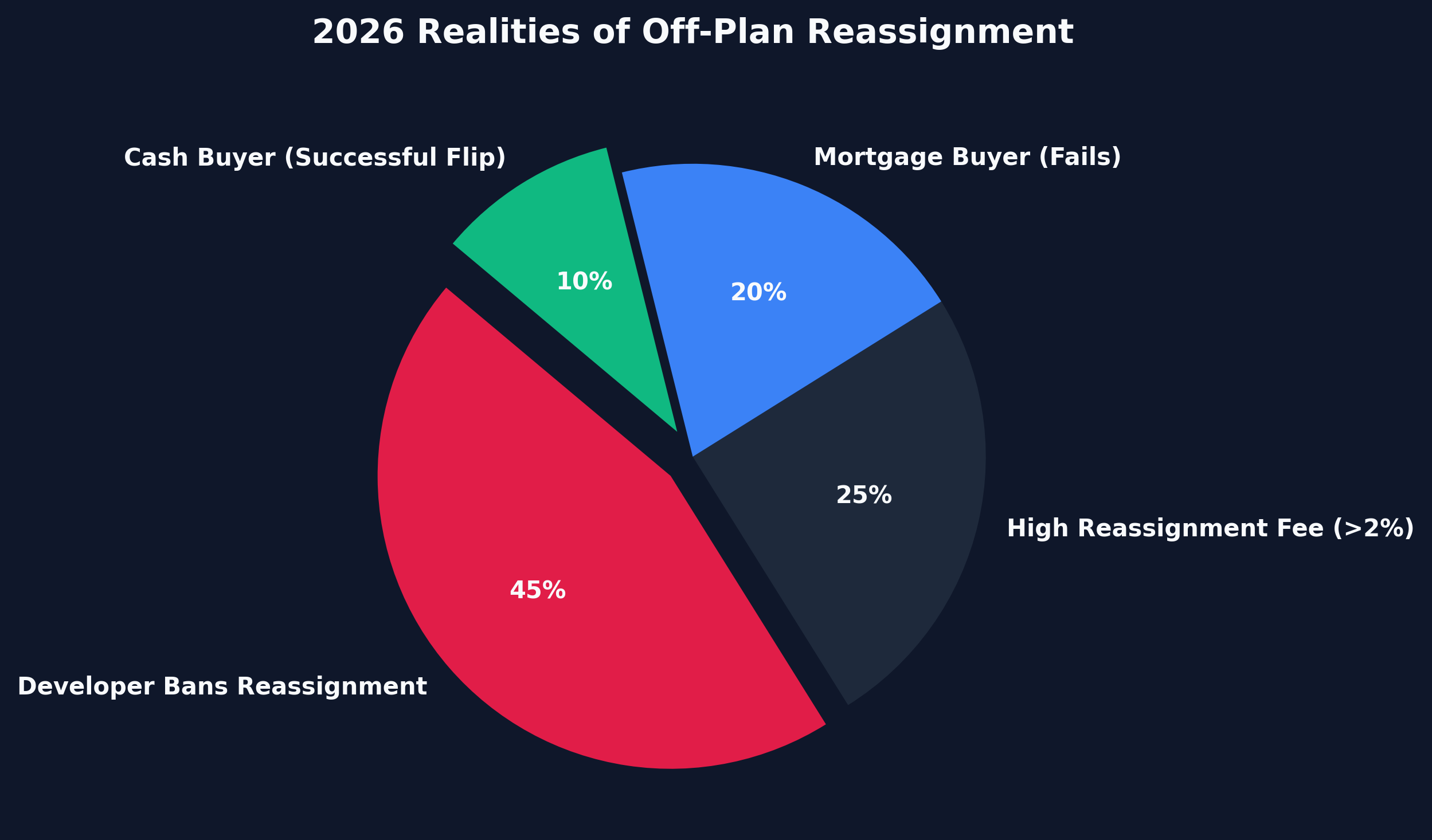

The 2026 Warning Matrix

While mathematically spectacular, flipping is the highest-risk strategy in the property sector. In 2026, you must navigate severe operational friction:

- Reassignment Clauses: Developers hate flippers because they compete with the developer's own remaining stock. 90% of off-plan contracts in 2026 expressly ban reassignment, or charge exorbitant fees (e.g., 2% of the purchase price) to permit it.

- The Cash Buyer Requirement: You cannot reassign a contract easily to someone who requires a mortgage. The new buyer usually must be a cash buyer, massively reducing your available exit liquidity pool.

- The Nuclear Obligation: If you cannot find a buyer to take your contract before completion, you are legally bound to complete the £250,000 purchase yourself. If you were banking on a flip and do not have the cash or mortgage capacity to complete, you will face catastrophic financial ruin.

Flipping off-plan is a volatile, high-stakes arbitrage mechanism reserved strictly for elite operators with vast cash reserves who can afford to complete the purchase if the flip fails.

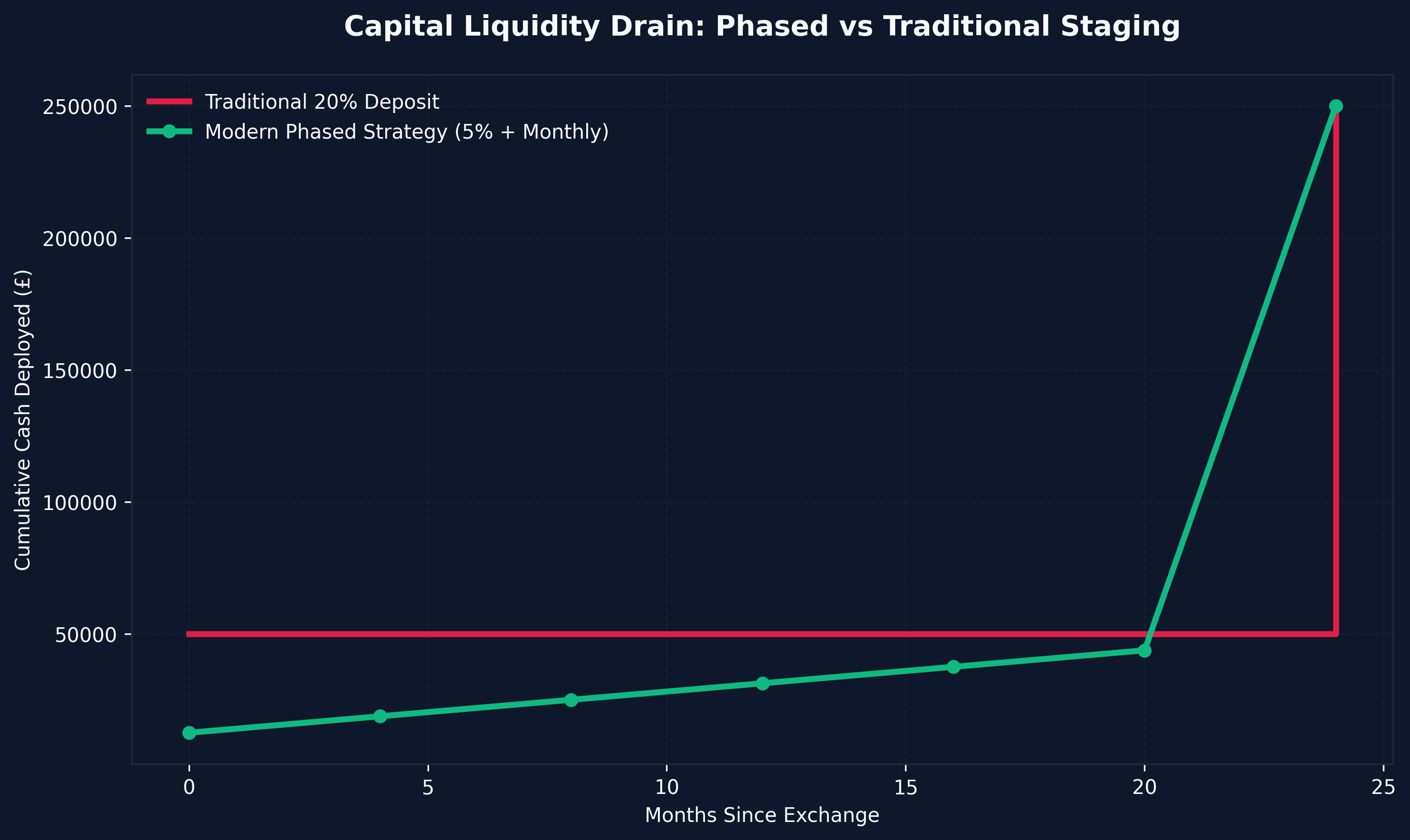

Strategy 3: Phased Payment Staging

This strategy focuses on mitigating risk and suppressing initial capital outlay by targeting developers offering highly unusual payment architectures.

Traditionally, an off-plan purchase requires 20% upon exchange, and 80% upon completion two years later. That locks up £50,000 of your liquidity for 24 months earning zero yield.

In 2026, due to increased financing costs for developers, elite investors negotiate Phased Staging Models or Monthly Payment Plans during the build cycle.

The 5% Stated Execution

Instead of demanding 20% upfront, the developer accepts:

- 5% upon exchange of contracts (£12,500)

- 15% staged across 24 monthly payments during construction (£1,562 per month)

- 80% upon completion via mortgage

The Strategic Advantage: You secure the £250,000 asset and lock in the price using only £12,500 of Day-1 liquidity. Your remaining capital stays in high-yield bonds or equities, generating a return while the property is built. Furthermore, you spread the cash flow hit over two years, eliminating the massive lump-sum liquidity drain.

If the developer goes insolvent during month 8, you have only lost your initial 5% and your 8 monthly payments, rather than the entire 20% lump sum.

Strategy 4: The Build-to-Rent (BTR) "Block" Arbitrage

The off-plan market in 2026 is structurally shifting towards institutional Build-to-Rent (BTR) models. These are massive, 300-unit towers custom-built for the rental market, owned by pension funds like Legal & General or M&G.

However, smaller regional developers attempt to emulate this model via Block Arbitrage. Instead of buying a single off-plan unit, a private syndicate (or high-net-worth individual) agrees to purchase an entire block (e.g., 10 to 15 off-plan units) in a suburban development at a severe bulk discount.

The Execution

- Retail Price per Unit: £200,000

- Syndicate Bulk Price (10 Units): £160,000 per Unit (20% Discount)

- Total Capital Commitment: £1.6 Million

The syndicate secures the block off-plan at a 20% discount below retail value. Upon completion, the syndicate immediately possesses 20% "Day-One Equity."

They then deploy a commercial block-valuation mortgage against the entire building. Because the building is valued collectively at £2 Million, a 75% commercial mortgage provides £1.5 Million. The syndicate essentially paid for the entire 10-unit development utilizing only £100,000 of their own seed capital.

This is the off-plan equivalent to the Buy Rehab Rent Refinance Repeat Strategy, but substituting the heavy refurbishment phase with aggressive pre-construction wholesale negotiation.

If this scale of operation appeals to you, but you lack the £1.6 Million covenant to negotiate with developers, you must explore fractional property investment UK structures, which pool retail capital to execute these exact institutional bulk-discount strategies.

The Critical Threat Vector: Developer Insolvency

Every off-plan strategy — whether a basic hold or an aggressive flip — shares the ultimate systemic risk: Developer Insolvency.

If you pay a £50,000 deposit and the developer goes bankrupt halfway through construction, the building stops. The bank that lent the developer the primary construction finance assumes control of the site as the senior creditor.

Where do you sit in the hierarchy? You are an unsecured creditor. The bank takes its money back first. The administrators take their fees second. You, the deposit holder, are at the absolute bottom of the pile. In the overwhelming majority of developer insolvencies, retail investors lose 100% of their deposit capital forever.

The 2026 Insolvency Mitigation Protocol

To survive in the 2026 off-plan market, you must implement aggressive structural mitigations before deploying capital.

- The Section 75 Charge / Unilateral Notice: Elite solicitors will apply a restriction (a Unilateral Notice) against the developer's land registry title for the amount of your deposit. This elevates your status from an unsecured creditor to a secured creditor, meaning if the developer collapses, you have a legal charge against the land.

- Deposit Protection Bonds: You must ensure the developer offers a recognized deposit protection scheme, such as the NHBC Buildmark or structural warranties that explicitly cover insolvency prior to practical completion.

- Averting "Fractional Funding" Models: Never buy into developments where the developer uses your deposit money to physically fund the construction (often seen in dubious student pod models or hotel room investments). Reputable developers secure full institutional development finance before digging the first hole; your deposit must simply sit in a ring-fenced escrow account.

For a deeper dive into mitigating systemic risk across non-traditional assets, review our breakdown of whether UK property is still a good investment today.

Geopolitics and Yield Selection

Identifying the strategy is only half the equation; deploying it in the correct municipality is what generates the alpha.

London is fundamentally exhausted for retail off-plan strategies. The entry pricing is too high (£500,000 minimum) and the yields are structurally compressed (3-4% gross), guaranteeing massive negative cash flow under current mortgage rates.

The premier execution zones for off-plan capital growth in 2026 are highly specific regeneration corridors in the North West and the Midlands.

Review our comprehensive data analyses on investment property in Manchester and the macro-dynamics of property investment in Birmingham to understand why institutional capital is aggressively rotating away from the capital and flooding these specific regional hubs with off-plan development finance.

Conclusion

The era of effortless off-plan speculation is permanently closed. The 2026 market demands algorithmic precision and an absolute intolerance for untested developers.

The best buying off plan uk strategies 2026 rely entirely on your capital position. If you possess massive liquid reserves and institutional negotiation skills, pre-completion flipping and bulk block arbitrage offer staggering ROCE multipliers. If you are executing standard retail operations, focus aggressively on phased payment structures, maximizing the zero-CapEx timeline, and relentlessly guarding your deposit against insolvency.

Off-plan property remains uniquely capable of generating maximum capital exposure with minimum seed capital, but the execution must be flawless.

Stop being a landlord. Start being an investor.

Shaded Canvas introduces serious capital to vetted UK property opportunities — targeting 12–16% net returns.

Start Investing →