If you are analyzing the UK property map for robust capital growth and sustainable yields in 2026, Birmingham is impossible to ignore. For nearly a decade, the "Second City" has been heavily marketed to investors. However, as we move through 2026, the narrative is shifting. Birmingham is no longer an "emerging" market; it is a maturing economic powerhouse currently executing massive infrastructure and corporate relocation projects.

This comprehensive guide strips away the marketing fluff. We will break down exactly where the highest yields are located, assess the genuine impact of HS2, completely dissect the 2026 numbers, and provide a clear framework for property investment in Birmingham.

1. The 2026 Macro-Economic Landscape of Birmingham

Before analyzing specific postcodes or property types, an investor must understand the macro drivers keeping Birmingham’s property market buoyant.

Hyper-Aggressive Corporate Relocation

Birmingham is experiencing an unprecedented influx of top-tier corporate capital. While London remains the financial capital, the cost of operating there has driven massive decentralization.

- Financial Services: Giants like Goldman Sachs and HSBC have established major operational hubs in the city.

- Professional Services: EY’s significant expansion into the Paradise development signals deep long-term confidence.

- Tech & Media: The new BBC broadcasting centre in Digbeth and Atos's technology hub are aggressively expanding the city’s high-income professional workforce.

For property investors, corporate relocation is the ultimate catalyst. When high-paying jobs arrive, demand for premium build-to-rent (BTR) and high-quality private rented sector (PRS) accommodation surges immediately.

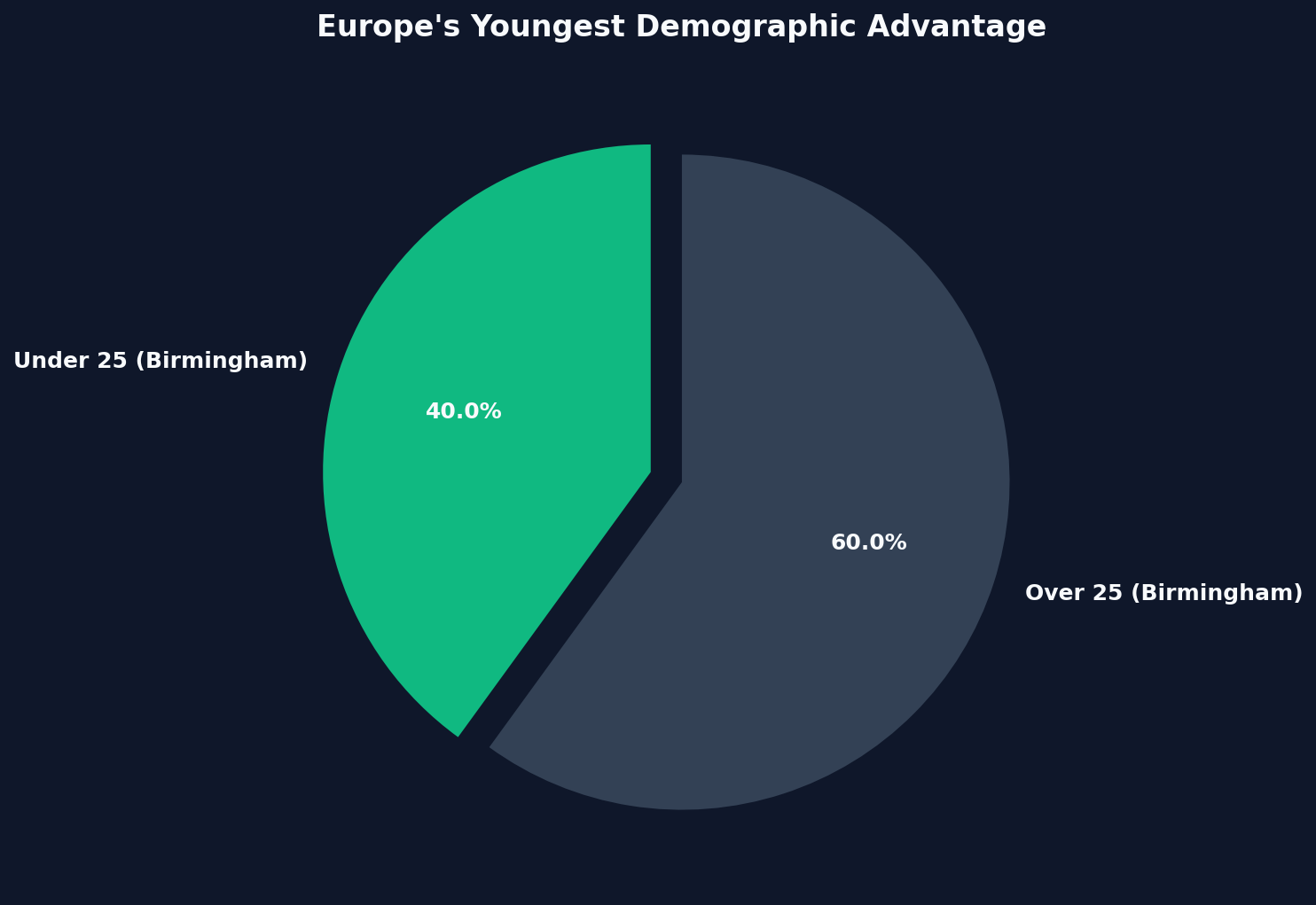

The Demographic Advantage: Europe’s Youngest City

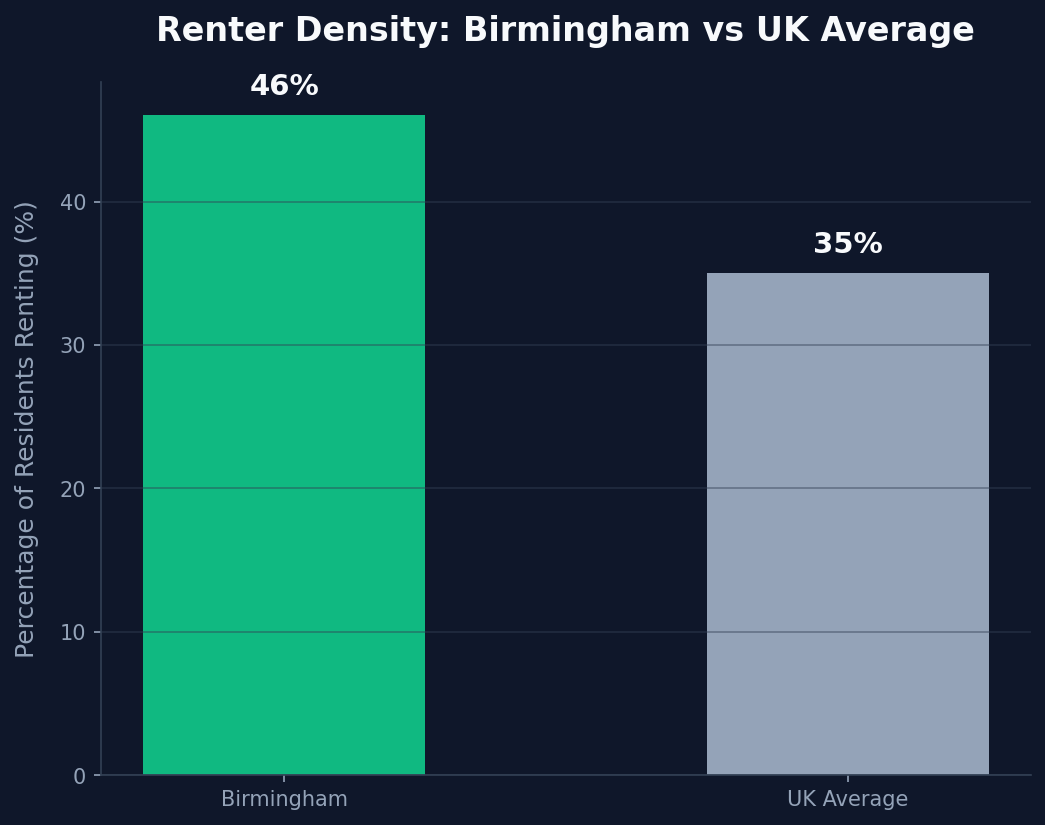

Birmingham boasts one of the most advantageous demographics in Europe for buy-to-let landlords: approximately 40% of its population is under 25.

Furthermore, 46% of Birmingham residents rent their homes, aggressively outpacing the national average of 35%. This creates a structurally locked-in, high-demand rental market fueled by students transitioning into young professionals who want to remain in the city.

The Supply and Demand Imbalance

Despite massive skyline changes, Birmingham is fundamentally undersupplied. The city council has consistently missed its housing delivery targets, creating a structural deficit. When relentless corporate and demographic demand collides with constrained supply, the mathematical outcome is sustained rental and capital growth.

2. Unpacking the HS2 Effect in 2026

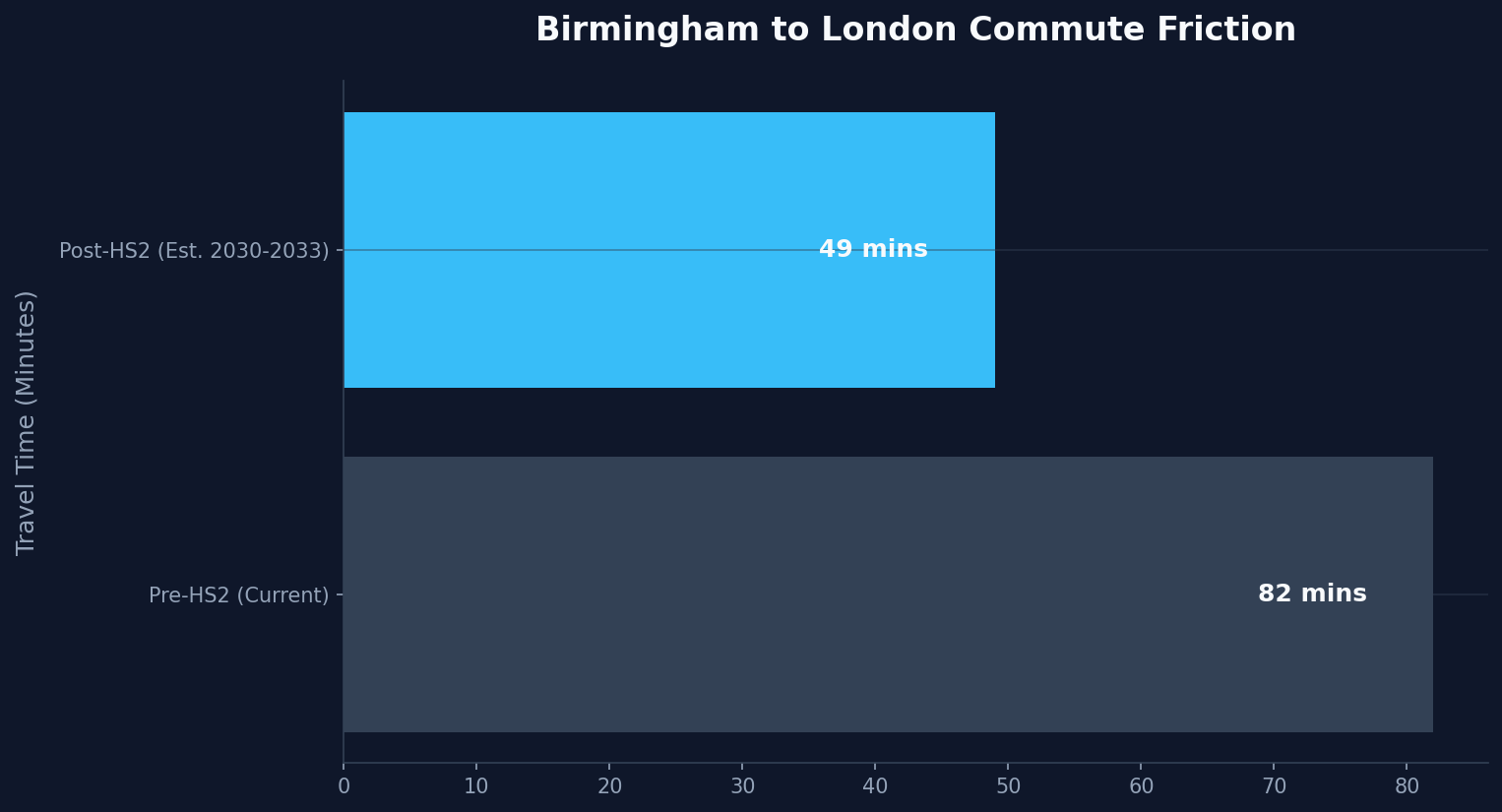

No discussion of property investment in Birmingham is complete without addressing High Speed 2 (HS2). While the Northern legs were controversially scrapped, the core London-to-Birmingham route is charging ahead, with the Curzon Street Station acting as the epicenter of physical regeneration.

Reduced Friction, Increased Valuation

When complete (projected between 2030 and 2033 for the final London Euston link), HS2 will slash the commute time between Birmingham and London to just 49 minutes.

This is a paradigm shift. It effectively brings Birmingham into the "London Commuter Belt" time radius. As London property prices and rents remain punitively high, Birmingham becomes a highly viable residence for workers who only need to be in the capital 2-3 days a week.

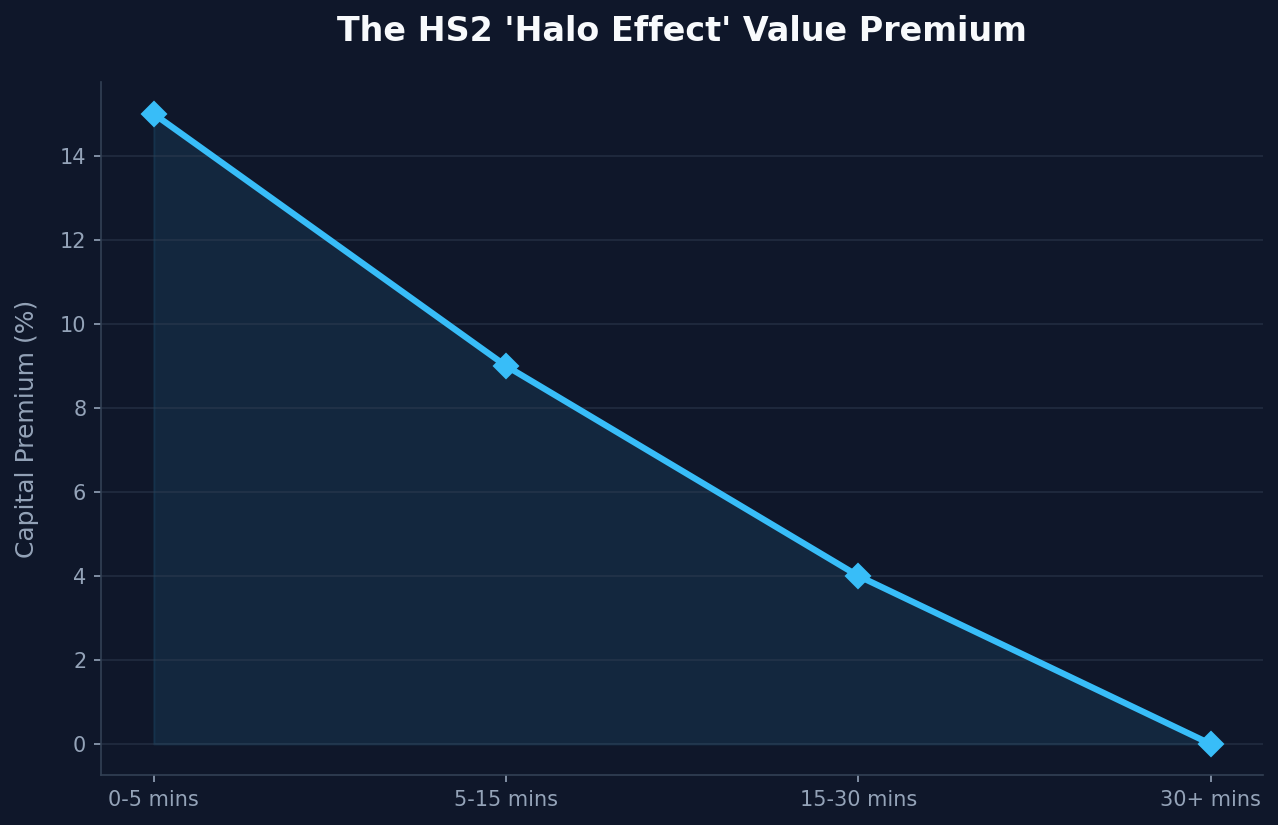

The Curzon Street Halo Effect

The physical area around the new Curzon Street Station—specifically Eastside and Digbeth—is experiencing a massive "halo effect" in valuations. Investors who secure assets within a 15-minute walk of this transport super-hub are positioned for the sheerest edge of the capital appreciation curve as the completion date nears.

3. Birmingham Property Prices and Capital Growth Forecasts

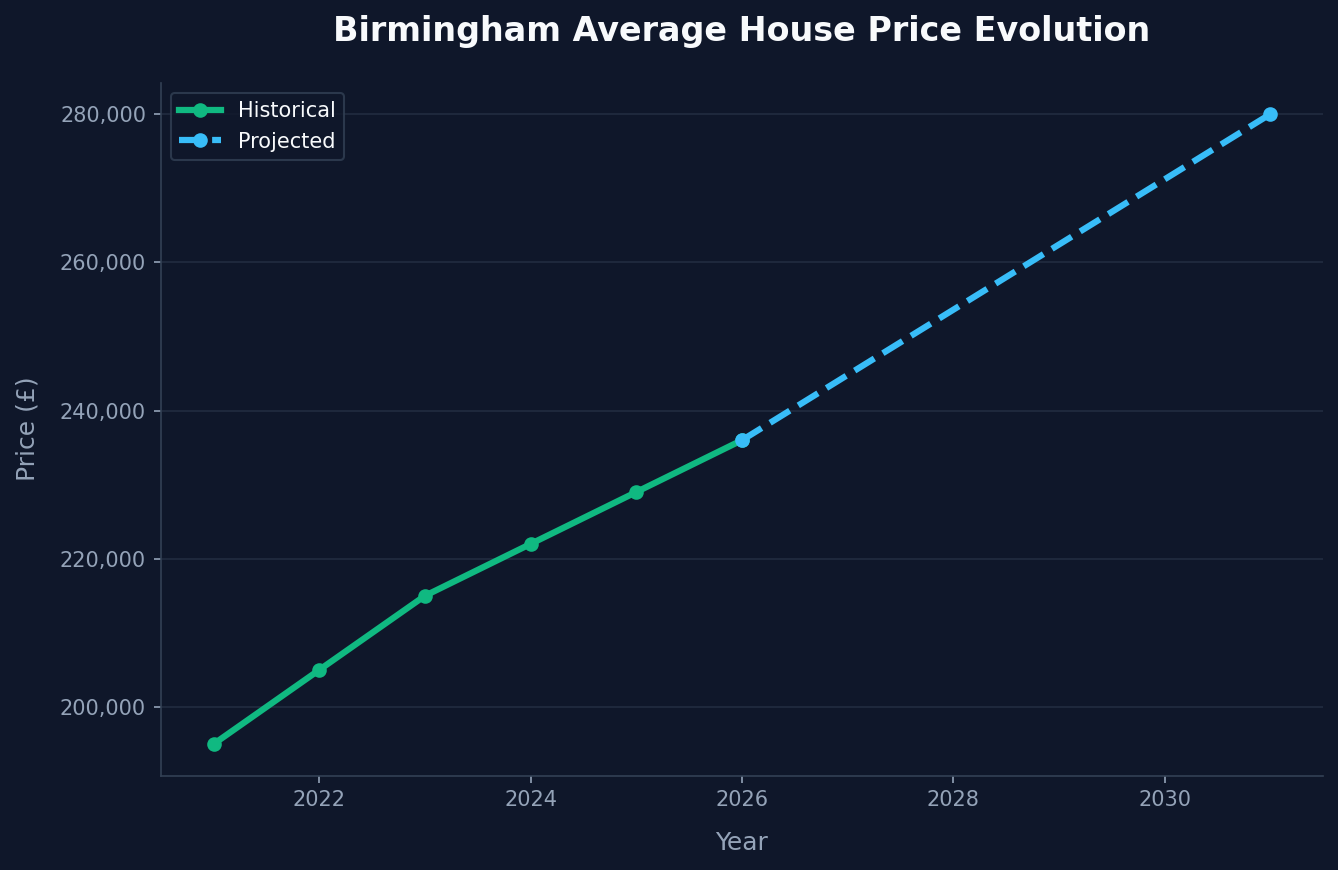

Affordability remains Birmingham's primary wedge against Southern markets. As of early 2026, the average property price in Birmingham sits around £236,000. This is significantly below the UK national average and less than half the price of the average London home.

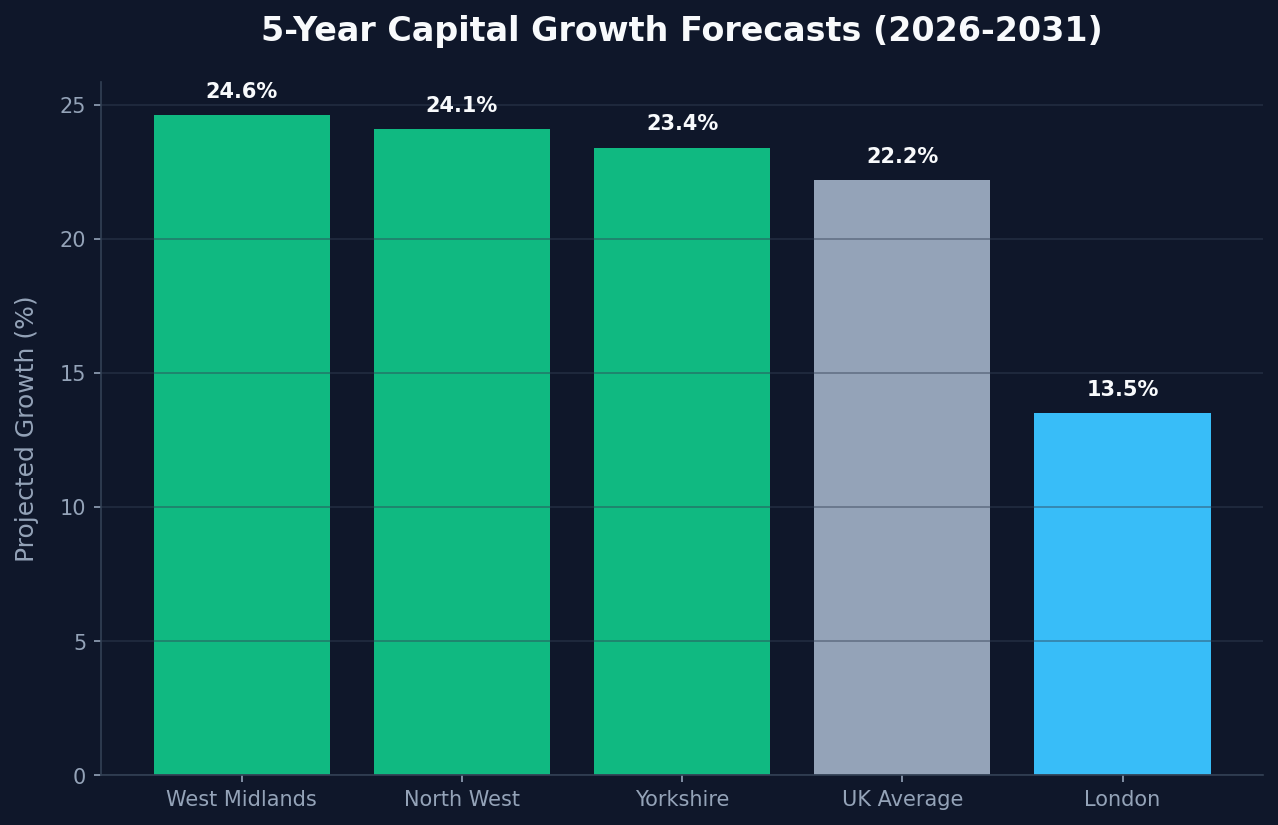

5-Year Capital Growth Projections

The consensus among institutional analysts points to steady, above-average growth:

- Savills projects the West Midlands region to comfortably outperform the UK average, forecasting an aggressive 24.6% house price growth over the next five years.

- More conservative estimates standardise around 3% to 6% annual growth through to 2030.

This means a £236,000 asset acquired today could analytically push well past £280,000 by 2031.

The Reality Check: Birmingham's "deeply undervalued" era is concluding. It is transitioning into a fundamentally strong, highly liquid market. Investors should expect steady, compounded growth rather than overnight spikes.

4. Where are the Highest Rental Yields in Birmingham?

Capital growth builds wealth, but rental yield pays the mortgage. High residential yields are critical in a market contending with high interest rates and the 5% stamp duty surcharge.

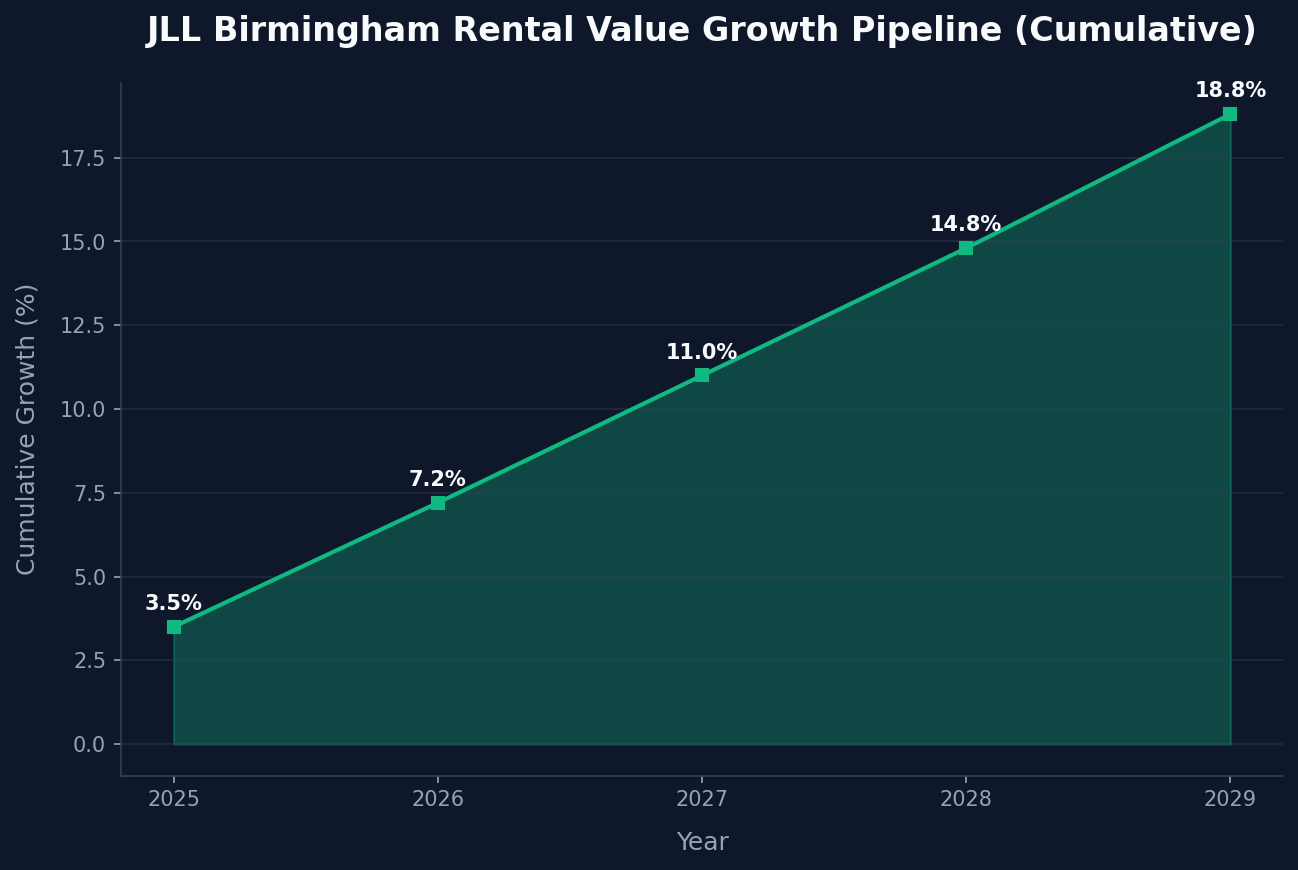

Currently, Birmingham is delivering an average gross rental yield around 5.4%, which severely beats London’s 3.5% average. Rents are also heavily forecasted to spike by 18.8% between 2025 and 2029.

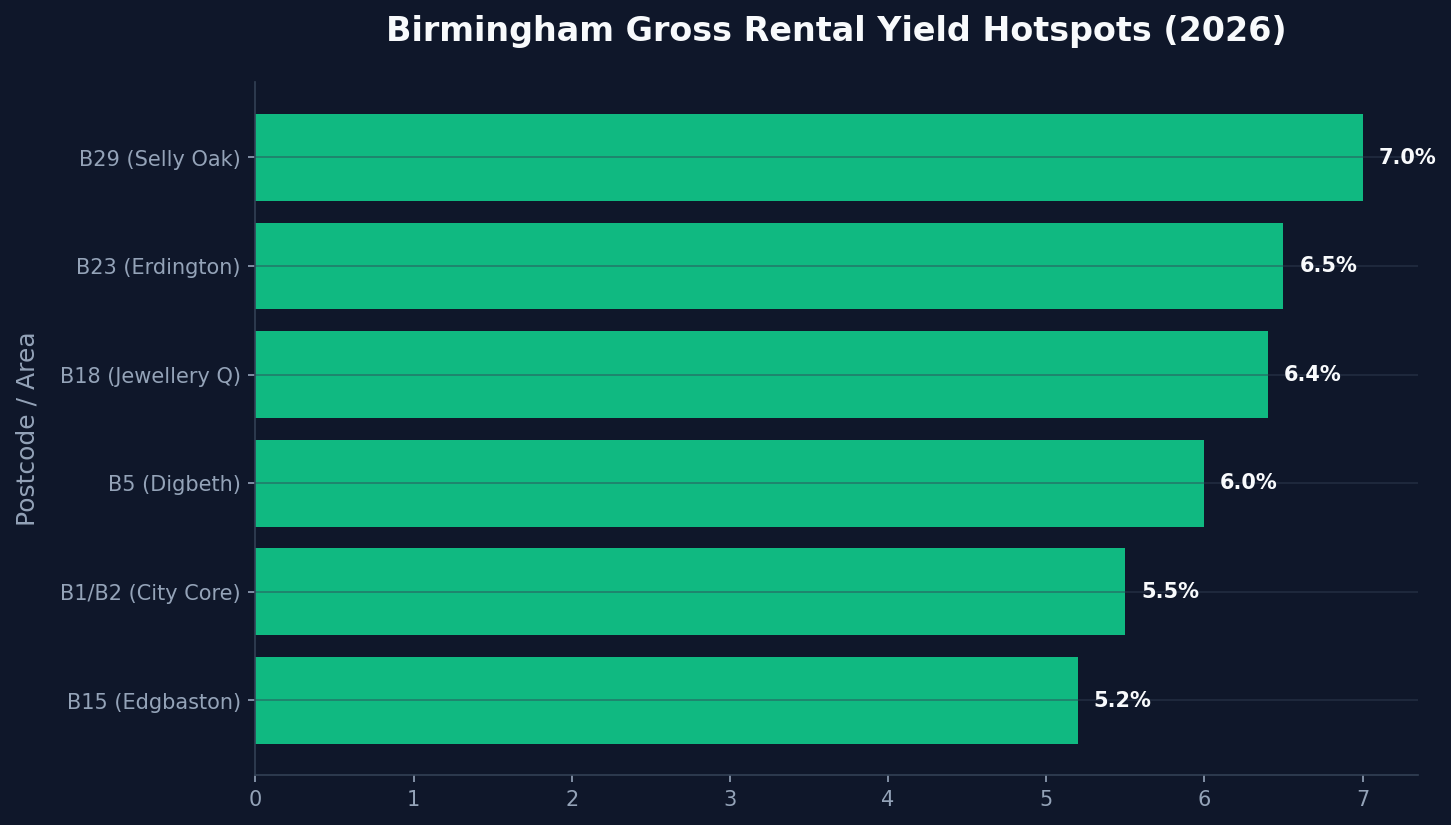

Here is a breakdown of the highest yielding zones in 2026:

Tier 1: The High-Yield Hotspots (6.0% - 7.5% Gross)

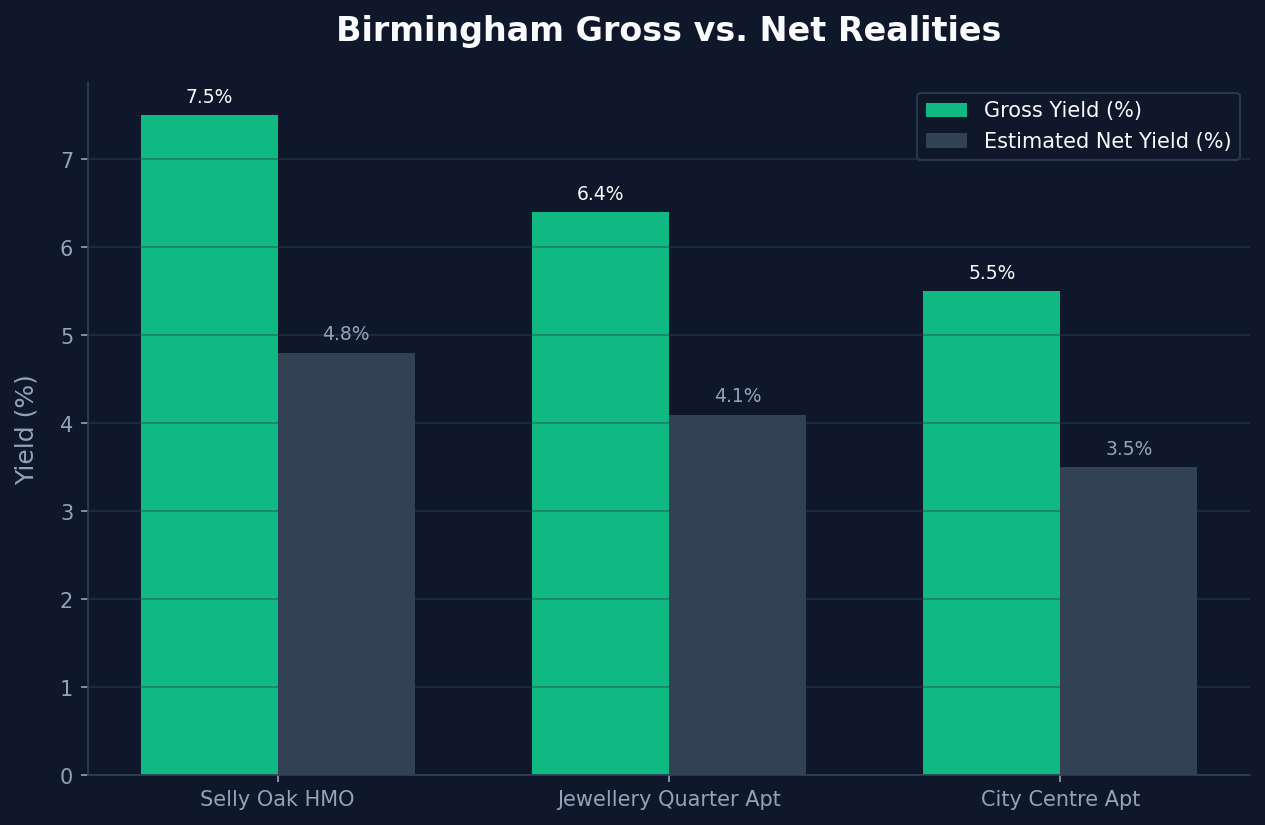

- Selly Oak (B29): The undisputed king of student yields. Driven by proximity to the University of Birmingham and the QE Hospital, HMOs (House in Multiple Occupation) and purpose-built student accommodation here routinely push 6.5% to 7.5% gross returns.

- Erdington (B23): A classic affordability play. Lower capital entry points combined with solid working-class tenant demand push yields comfortably into the 6% to 7% bracket.

- Jewellery Quarter (B18): Historically known for capital growth, the massive influx of young professionals has pushed rental limits up, allowing for yields around 6.4%. It is Birmingham’s premium lifestyle destination.

Tier 2: The Core Capital Growth + Solid Yield Zones (5.0% - 6.0% Gross)

- Digbeth (B5): The creative quarter and epicenter of the £1.9bn Smithfield masterplan and BBC relocation. While capital prices are rising fast (compressing yields slightly), investors are still achieving a very healthy 5.5% to 6.5%. This is the prime capital appreciation play.

- Edgbaston (B15): The affluent, leafy suburb. While capital entry is high, family and executive rental demand is ironclad, returning reliable yields around 5.0% to 5.5%.

- City Centre Core (B1 / B2): High-end apartments catering to the corporate crowd. Yields sit steadily around 5.5%.

(Note: Ensure you run these gross figures through a strict net calculation incorporating service charges, letting fees, and void periods. A realistic net yield in Birmingham typically lands between 3.5% and 4.5%).

5. Optimal Investment Strategies for Birmingham in 2026

Throwing money at a random flat in the city centre is not a strategy. To extract maximum ROI, your asset must match the micro-market demand.

Strategy 1: The Premium "Build-to-Rent" (BTR) Play

- The Target: Corporate professionals migrating from London (Goldman Sachs, HSBC).

- The Asset: 1- or 2-bedroom luxury apartments in the Jewellery Quarter, Westside, or City Centre Core. Must have amenities (gyms, co-working spaces).

- The Play: High capital growth, incredibly low void periods, high-quality tenants.

Strategy 2: The Infrastructure Capitalizer

- The Target: Young professionals and forward-looking renters.

- The Asset: Off-plan or newly built apartments specifically in Digbeth or Eastside.

- The Play: Acquiring assets close to the HS2 Curzon Street station and the Smithfield regeneration zone before the final massive value uplift occurs upon project completion.

Strategy 3: The High-Cashflow HMO

- The Target: Students and young graduates.

- The Asset: 4 to 6 bedroom houses in Selly Oak, Perry Barr, or Edgbaston fringes.

- The Play: Maximizing monthly cashflow. Be highly aware of Birmingham City Council's Article 4 directives—converting a standard residential house (C3) into a small HMO (C4) requires explicit planning permission in many wards. Always buy a property with existing HMO status to bypass this friction.

6. Risks to Manage in the Birmingham Market

No investment is without friction. When analysing Birmingham, factor in these specific risks:

Service Charge Inflation in City Centre Blocks

Many new, glossy developments come heavily burdened with aggressive service charges that can rapidly decimate your net yield. Before buying an apartment, relentlessly scrutinize the leasehold terms, the historical service charge increases, and the cladding (EWS1) status of the building.

Article 4 Directions (HMO Restrictions)

Do not assume you can buy a cheap 3-bedroom house in a student area and convert it into an HMO. Birmingham has tightly regulated HMO density. Always verify local planning overlays before executing a multi-let strategy.

5% Buy-to-Let Stamp Duty Surcharge

As covered extensively in our Stamp Duty guides, the brutal 5% residential surcharge on additional properties severely impacts your initial capital outlay. You must build this exact cost into your Year 1 yield modeling.

7. The Final Verdict: Is Property Investment in Birmingham Worth It in 2026?

The mathematical data makes a highly compelling case. Birmingham currently offers the elusive "Golden Triangle" of property investment:

- Low Capital Entry: At £236k, it remains highly accessible compared to the South East.

- High Rental Yield: Pushing past 6% in core areas, the cashflow mathematics work even in a higher interest rate environment.

- Aggressive Capital Growth Drivers: Anchored by HS2, the BBC, and major financial institutions.

For investors priced out of London or seeking to diversify away from lower-yielding Southern markets, Birmingham in 2026 represents one of the most structurally sound investment environments in the UK.

Your Action Plan

- Define Your Metric: Decide if you are optimizing for pure monthly cashflow (HMOs in Selly Oak) or long-term capital appreciation (Apartments in Digbeth).

- Run the SDLT Numbers: Use a buy-to-let calculator to firmly establish your total acquisition costs.

- Target the Halo Zones: Focus your search parameters tightly around areas receiving direct infrastructure funding (HS2, Metro extensions, Smithfield).

Disclaimer: The property market carries inherent risks and values can decrease as well as increase. This guide is for educational purposes and does not constitute formal financial advice.

Stop being a landlord. Start being an investor.

Shaded Canvas introduces serious capital to vetted UK property opportunities — targeting 12–16% net returns.

Start Investing →