In 2026, the question on every prospective investor’s mind remains exactly the same as it was a decade ago: is property a good investment UK? The short answer is yes, but the landscape has fundamentally shifted. Gone are the days when simply buying a house and waiting was enough to guarantee spectacular, market-beating returns. To understand whether you should invest in property now, you need a comprehensive, data-driven look at the modern UK real estate market.

With fluctuating interest rates, shifting tax regulations (namely Section 24), and an increasingly regulated rental sector, the rules of the game have evolved. Whether you are wondering if buying a house is a good investment for your family's future, weighing up whether to buy a house or invest the money elsewhere, or trying to decide if buying a second property is a good investment, this comprehensive guide will break down the numbers, the risks, and the realistic rewards.

At Shaded Canvas, we believe in stripping away the "get rich quick" hype. Property investment is a marathon, not a sprint. In this guide, we dive deep into the data to explore exactly why property is a good investment, how different strategies compare, and provide our top property investment tips for navigating the 2026 market.

Why Is Property a Good Investment in 2026?

Real estate has historically generated more wealth for everyday investors than almost any other asset class. But what is driving that underlying strength today?

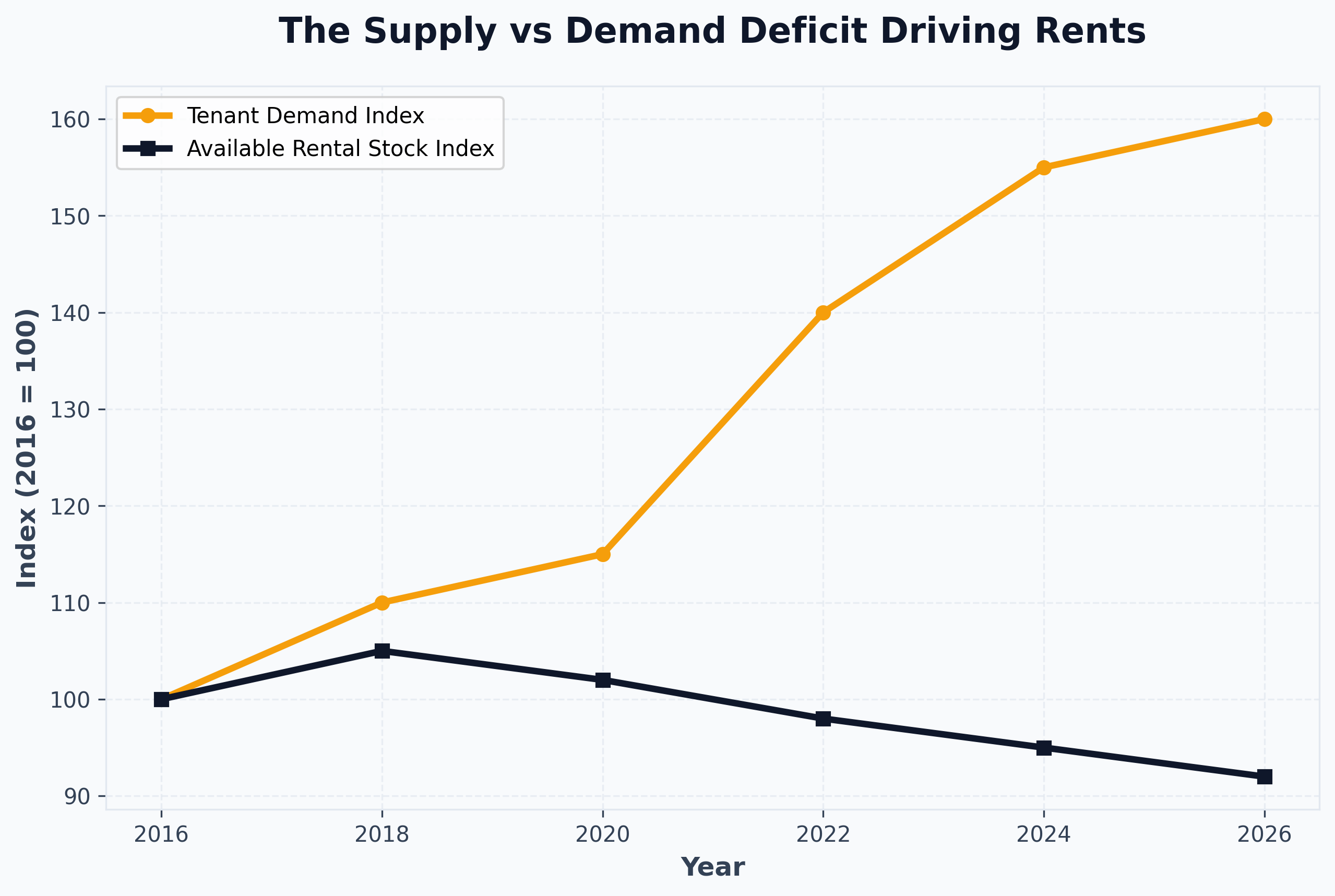

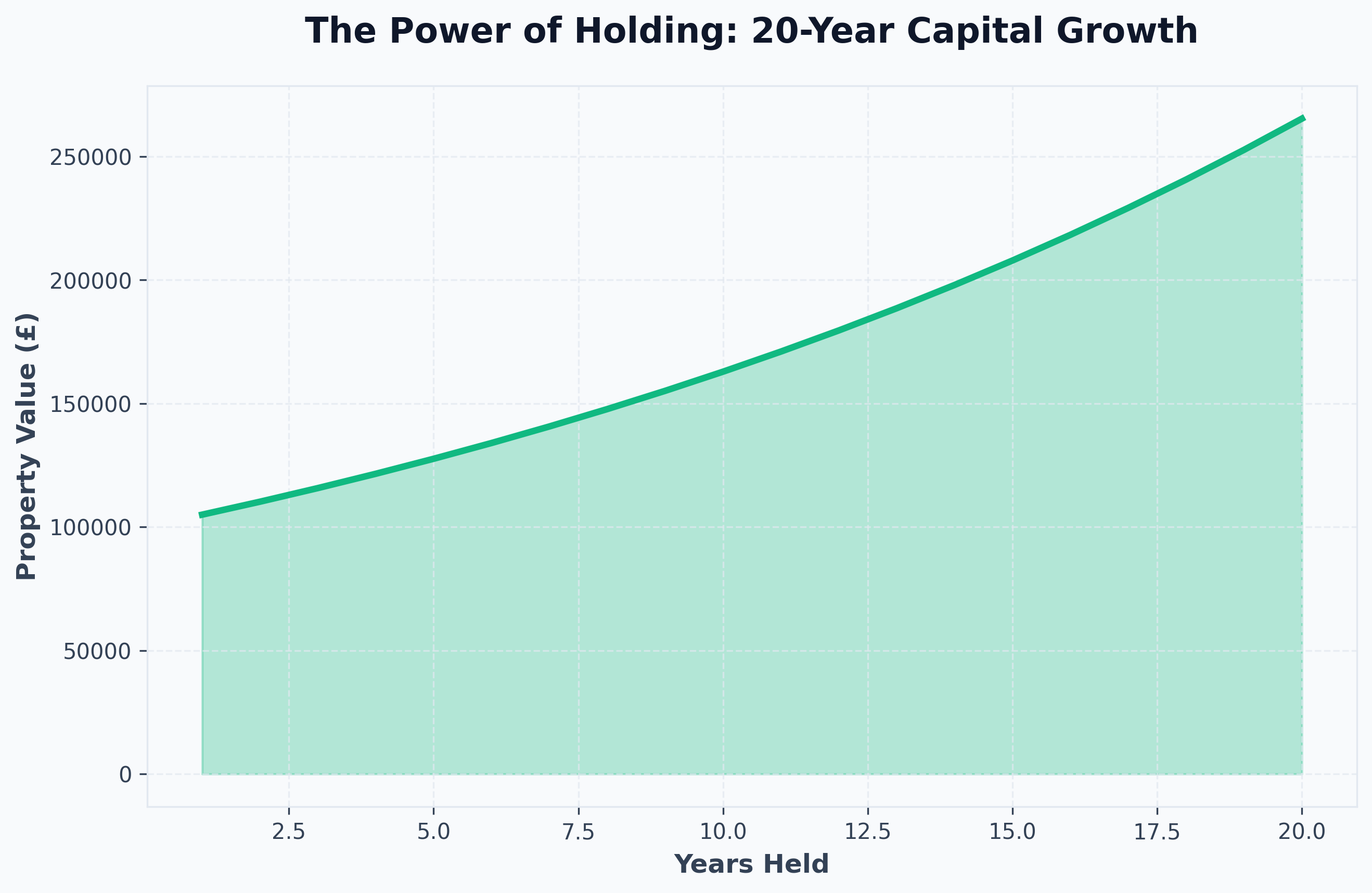

1. The Chronic Supply and Demand Imbalance

The UK faces a systemic housing shortage. The population is growing, but housing development consistently fails to meet government targets. This simple economic reality—high demand chasing limited supply—underpins long-term capital preservation and growth. While there may be short-term market dips, the structural deficit means property remains fundamentally resilient over the 15-to-20 year long term.

2. The Power of Leverage

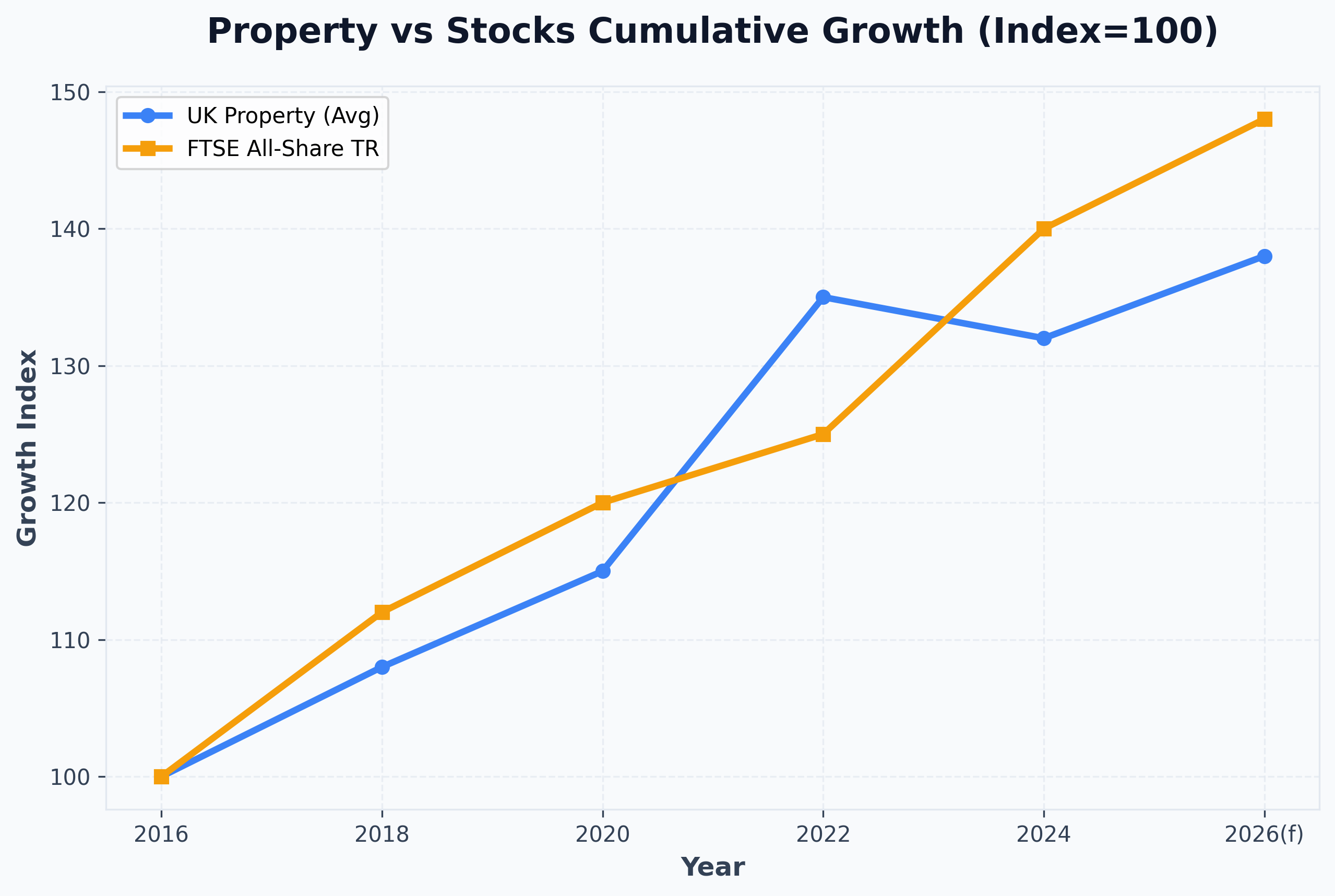

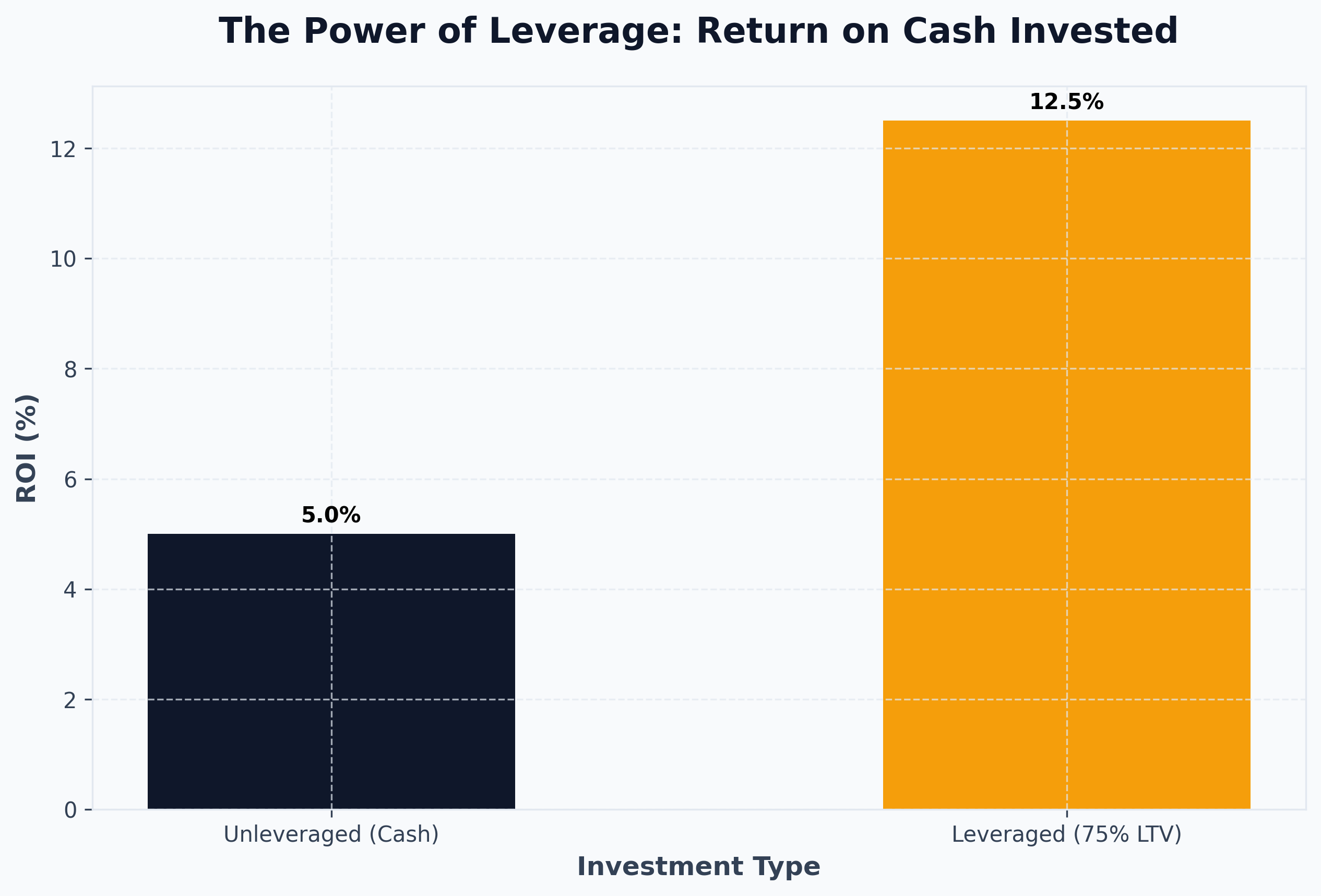

One of the primary reasons why property is the best investment for many people is leverage. If you invest £50,000 in the stock market (perhaps when deciding whether to invest or buy property) and the market goes up 10%, you make £5,000.

If you use that £50,000 as a 25% deposit on a £200,000 property, and the property goes up 10%, your asset increases by £20,000. That represents a 40% Return on Investment (ROI) on your initial cash stake before we even factor in rental income. Leverage multiplies your gains (though it must be noted, it also multiplies potential losses).

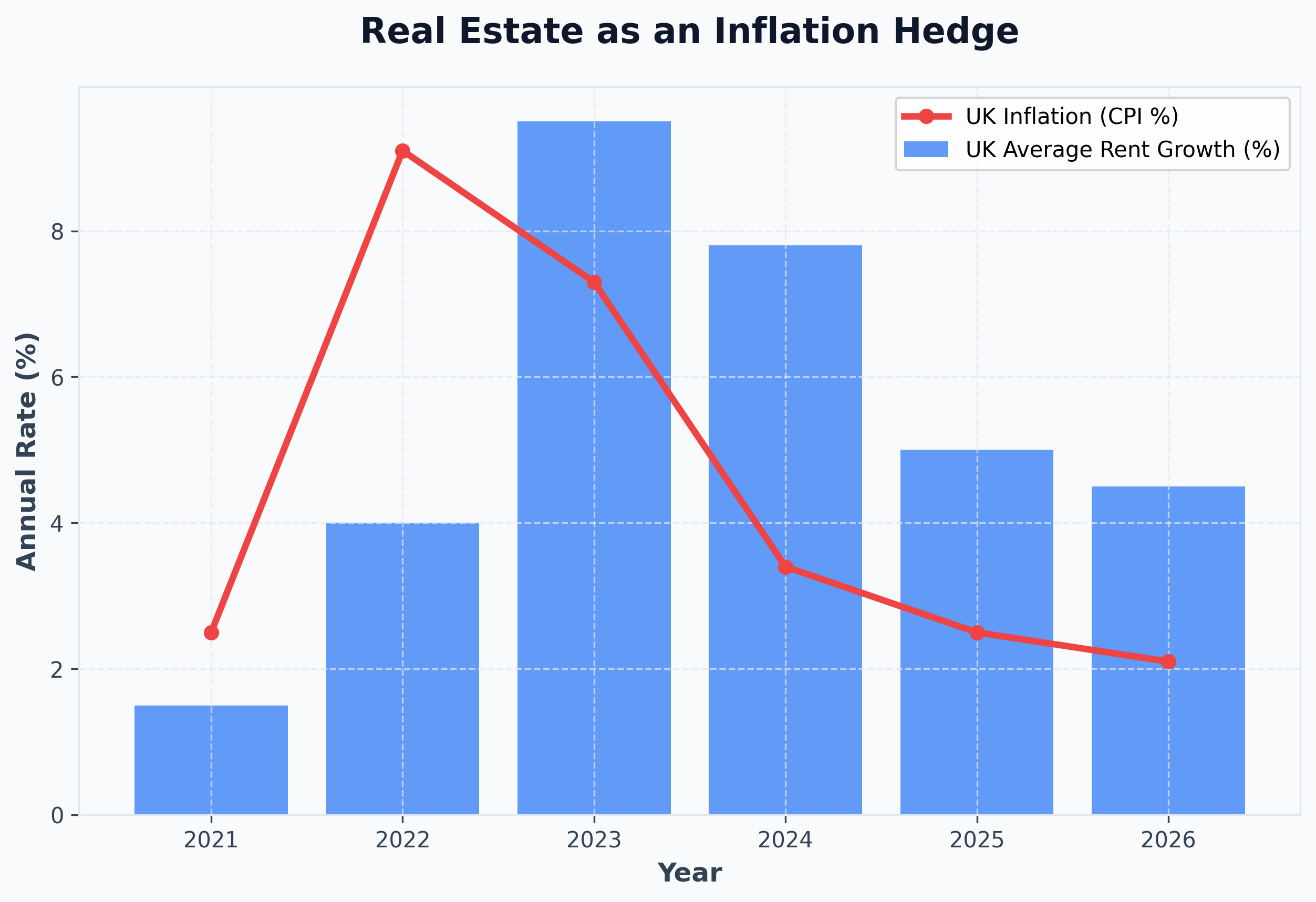

3. Hedging Against Inflation

Property acts as a tangible hedge against inflation. During inflationary periods—like the one experienced globally in the early 2020s—the cost of building materials and labor rises, pushing up new-build prices and dragging existing property values up with them. Simultaneously, inflation erodes the real value of your mortgage debt. Rents also tend to rise in line with wage inflation, protecting your monthly cash flow in real terms.

4. Dual Income Streams: Capital Growth & Yield

Unlike gold (which pays no dividend) or many dividend stocks (which offer little capital growth), a well-selected property offers two distinct returns:

- Capital Growth: The increase in the property's underlying capital value over time.

- Rental Yield: The monthly cash flow generated by tenants.

Is Buying a Second Property a Good Investment?

For those who already own their primary residence, the next logical step often feels like buying a buy-to-let. So, is a second home a good investment?

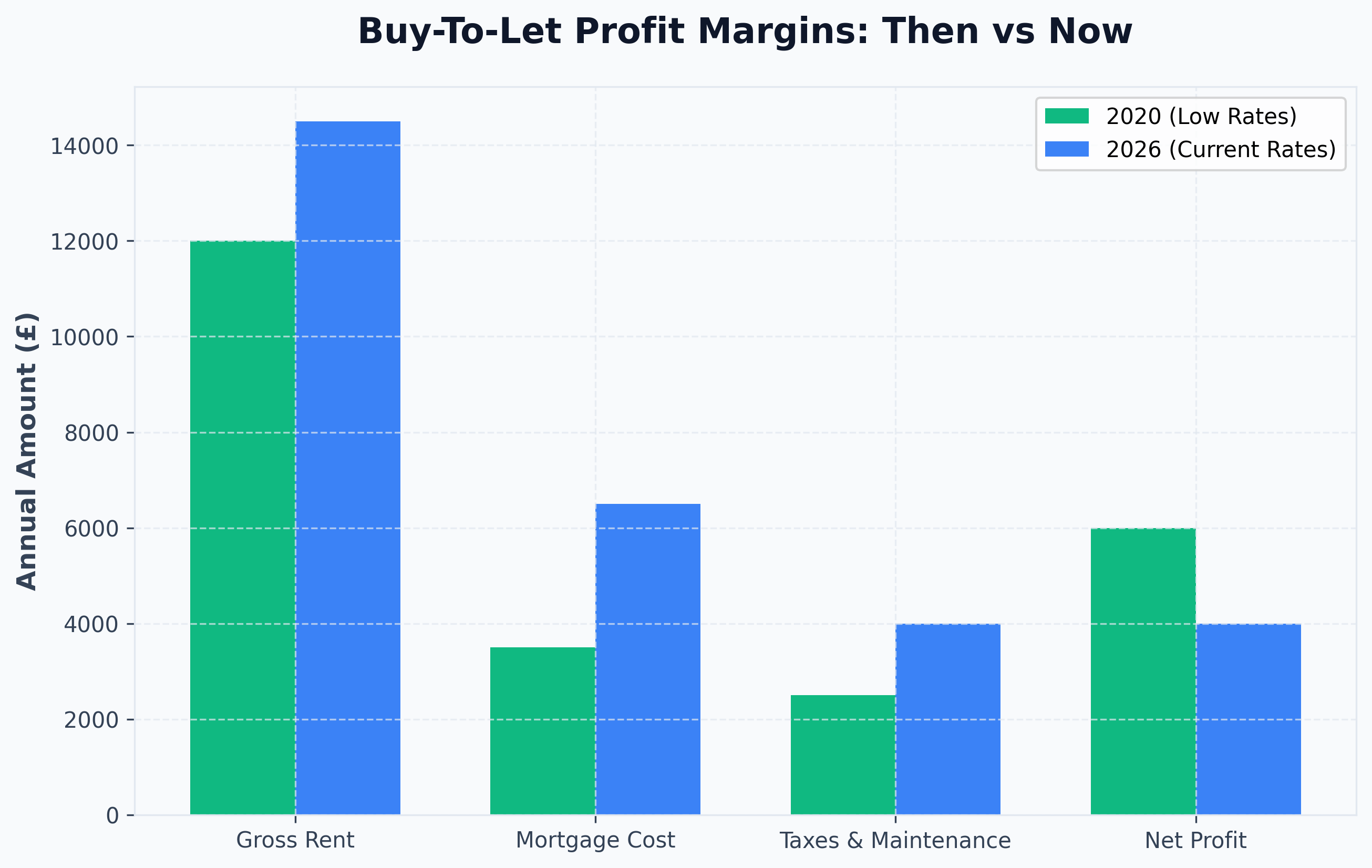

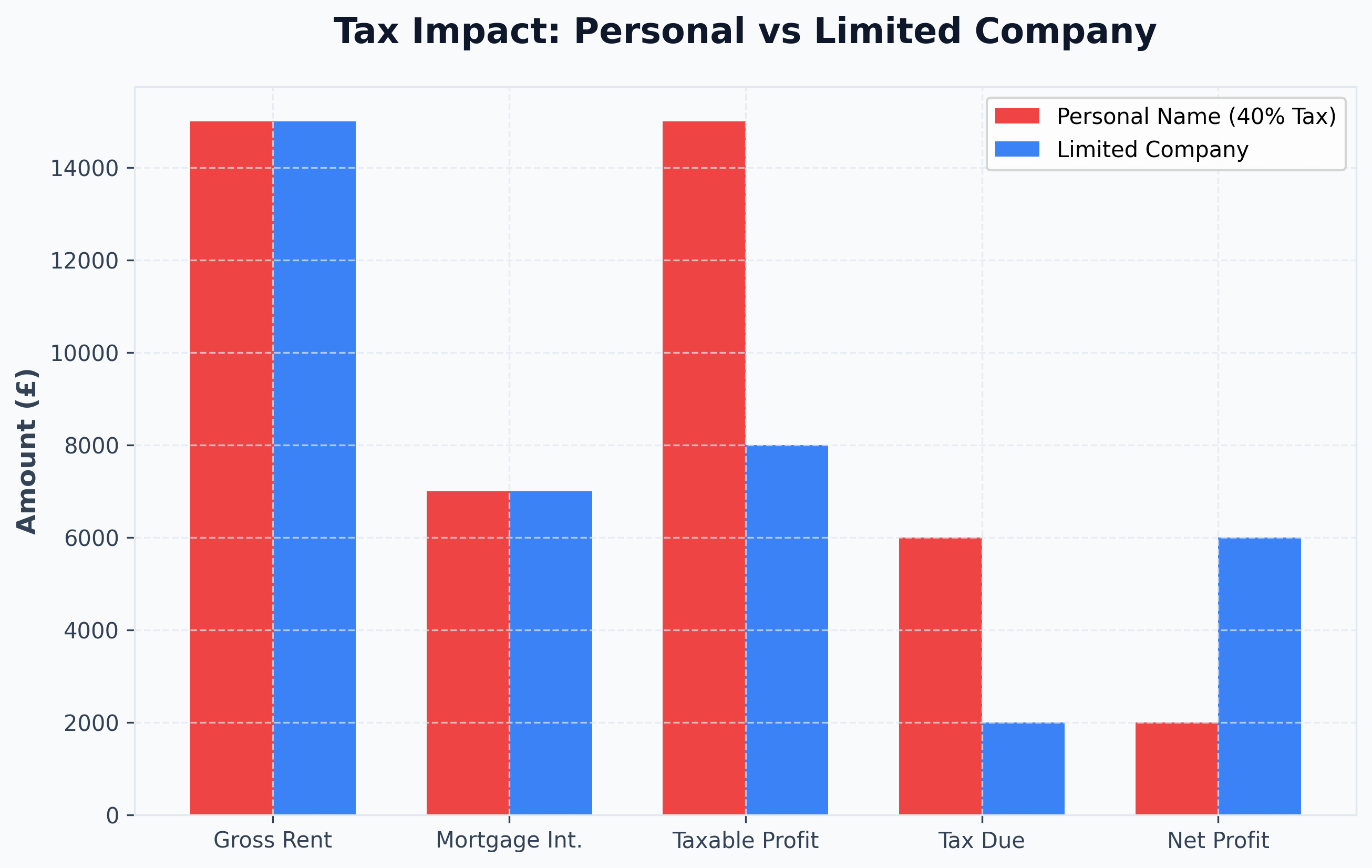

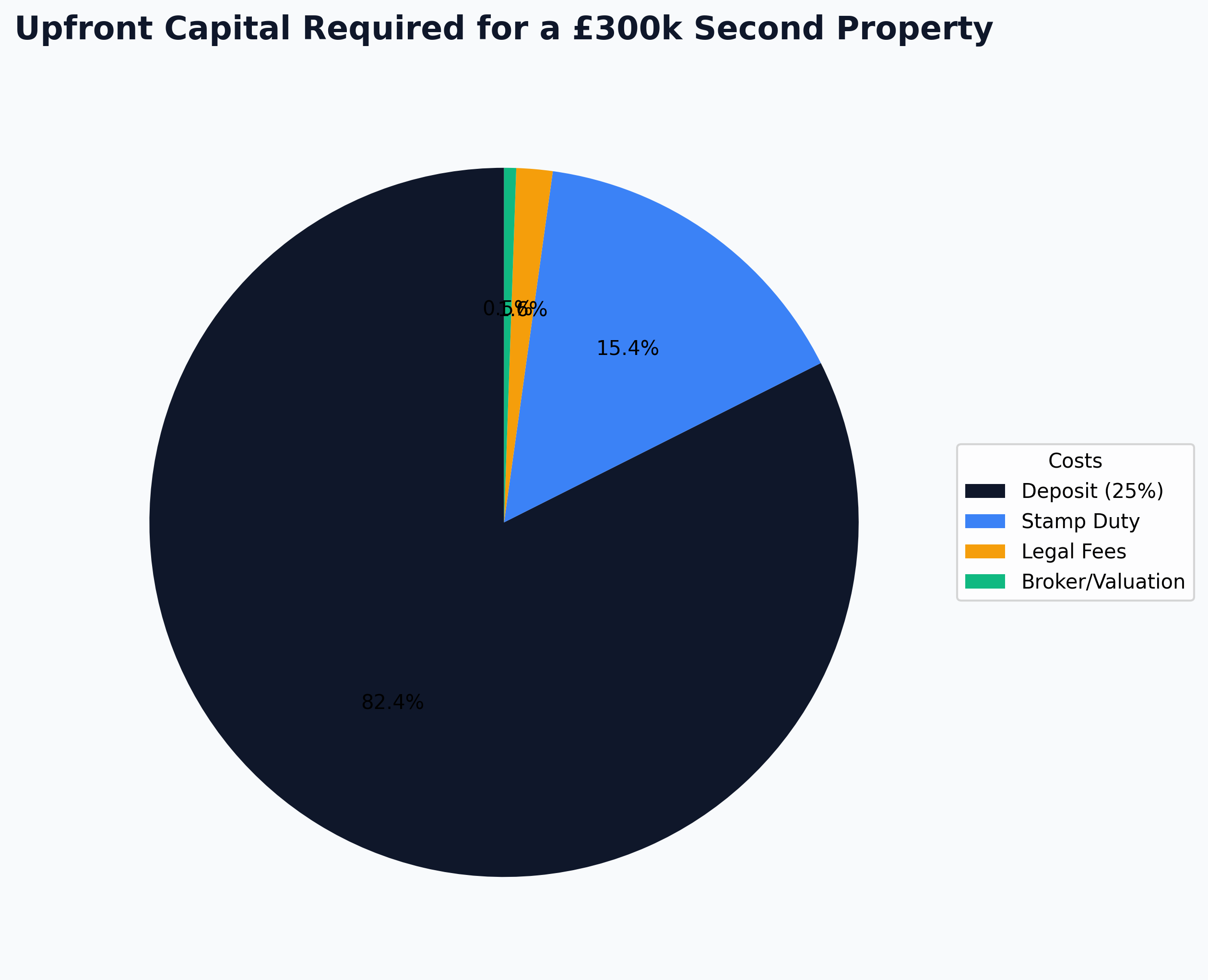

The answer depends heavily on your tax strategy. The introduction of the 3% (or higher, depending on your UK country) Stamp Duty Land Tax (SDLT) surcharge on second homes means you start your investment journey with an immediate capital hit. Furthermore, Section 24 tax rules mean private landlords can no longer deduct mortgage interest from their rental income before calculating tax—pushing many into the higher 40% tax bracket purely because of gross rental turnover.

The Limited Company Solution

For many investors in 2026, the best property investment structure is a Special Purpose Vehicle (SPV) Limited Company. By holding the property in a company, mortgage interest is once again fully deductible against corporation tax, and profits can eventually be extracted more tax-efficiently via dividends.

If you are buying your first house as an investment (meaning you do not own a primary residence), you avoid the 3% stamp duty surcharge, but you also sacrifice first-time buyer benefits.

Should I Invest or Buy a House?

This is the classic dilemma for young professionals: buy to let vs residential.

If you are renting and have capital saved, you might be asking: should I buy a house or invest?

- Buying your primary residence: You secure your living situation, stop paying another landlord's mortgage, and benefit from tax-free capital gains on your primary home. However, you tie up all your capital and take on a significant liability.

- Rentvesting (Renting where you live, buying an investment): You maintain flexibility by renting in an expensive city (like London) where buying is prohibitive, but you deploy your capital into high-yielding property up North to generate cash flow.

There is no universally correct answer to "to invest in property or not"; it depends entirely on your lifestyle goals, risk tolerance, and the local yield dynamics.

Is Buy To Let Still a Good Investment?

We frequently hear the question: is buy to let still a good investment given the increased regulations and higher interest rates compared to the 2010s?

The era of "accidental landlords" making easy money is indeed over. High mortgage rates squeeze monthly profits. However, professional, strategic investing remains highly lucrative. The key is understanding that property good investment now requires an active approach.

Top Strategies for 2026: The Best Property Investment Advice

If you are wondering how does property investing work today and looking for the best property investment advice, here are the core models working right now:

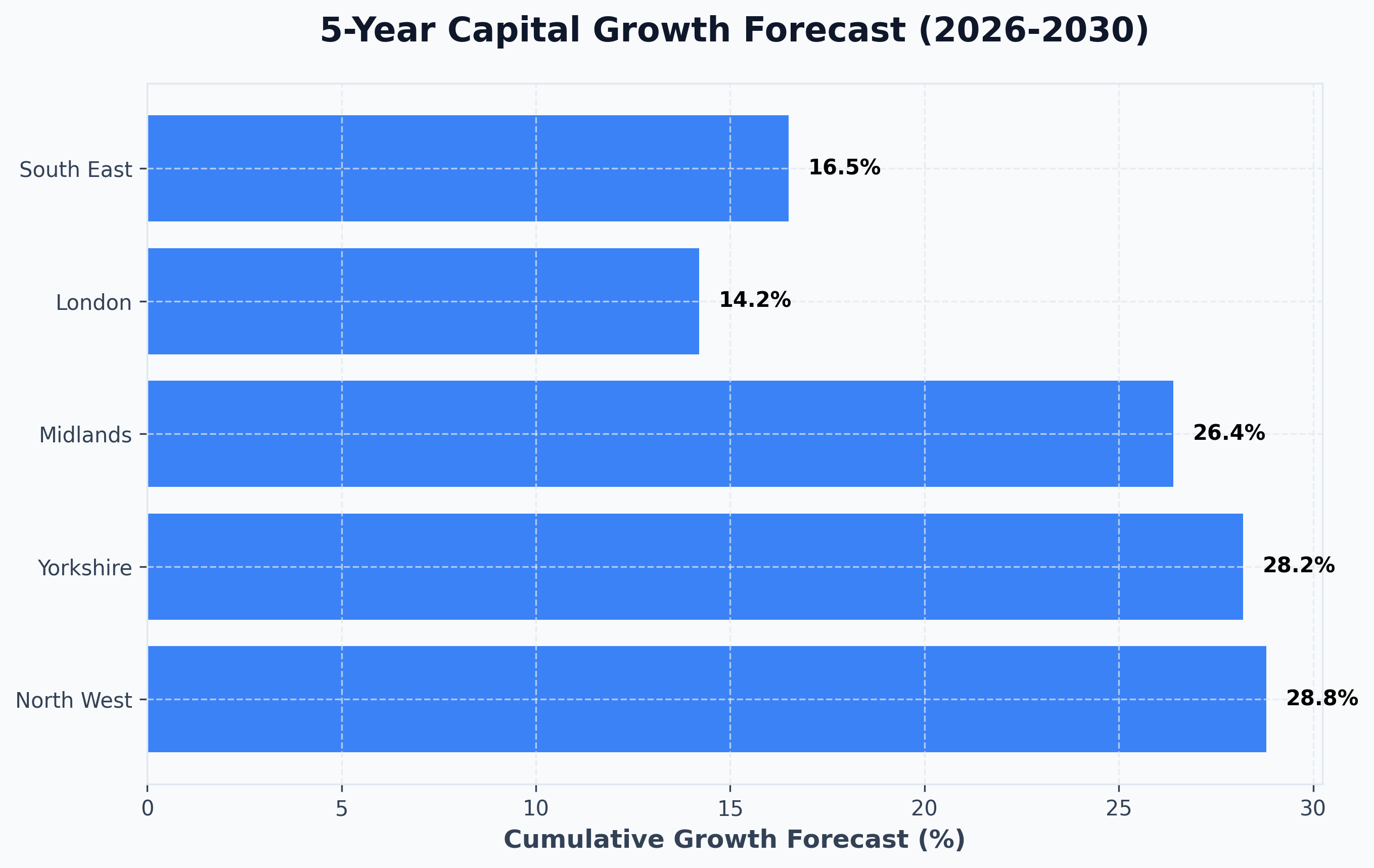

- High-Yield Vanilla BTL in the North: Shifting focus away from the expensive South East towards cities in the North West and Yorkshire where capital entry is lower (£100k-£150k) and yields sit comfortably at 6-8%.

- Houses in Multiple Occupation (HMOs): Renting properties room-by-room. While management intensive and highly regulated, HMOs offer significantly higher gross yields (10-14%), providing a buffer against higher interest rates.

- The BRRR Strategy (Buy, Refurbish, Refinance, Rent): Buying distressed or dated properties, adding value through renovation, and refinancing to pull initial capital back out. This is the best property investment strategy for accelerating portfolio growth with limited starting capital.

- Buy to Sell Property Investment (Flipping): Generating lump sums of cash rather than passive income. Requires deep knowledge of local markets and tight control over refurbishment costs.

Is Buying Property Still a Good Investment? Weighing the Risks

While we have established strong reasoning for why it works, good house investment advice demands that we look at the downside risks. Before deciding whether you should you invest in property, consider these factors:

- Illiquidity: Property cannot be sold overnight. If you need emergency cash, extracting equity can take months. Ask yourself: is tying up this cash safe for my personal financial situation?

- Interest Rate Exposure: If you buy at a 75% LTV, a spike in interest rates at remortgage time can wipe out your monthly cash flow. Stress-testing your investments at 6% or 7% interest rates is crucial.

- Legislative Risk: The UK government frequently changes the rules for landlords. From energy efficiency (EPC) mandates to changes in eviction rules (the Renters' Reform Bill), landlords face higher compliance barriers than ever before.

- Void Periods and Bad Tenants: A property that sits empty costs you money every single day. A bad tenant can cost thousands in legal fees and property damage. Professional property management is often worth its weight in gold.

The Verdict: Time to Invest in Property?

So, back to the core question: is property a good investment UK?

Yes. Despite the headlines and the shifting regulatory environment, buying a house a good investment remains a factual statement for those who approach it as a business rather than a passive hobby. The key is acting decisively but strategically.

If you have capital sitting in a bank account losing purchasing power to inflation, it is always the right time to invest in property—provided the numbers on the specific deal stack up. You must analyze the yield, stress-test the mortgage, and buy in an area with strong economic fundamentals.

FAQ: Your Property Investment Questions Answered

To round off our property investment tips, here are quick answers to the most common questions we receive regarding the market in 2026.

Should you invest in property now?

Yes, if your timeframe is long-term (10+ years). Attempting to "time the market" perfectly to catch the absolute bottom is a fool's errand. Time in the market historically beats timing the market.

Is buying a house still a good investment compared to stocks?

Stocks offer liquidity and true passivity, but lack the powerful multiplier effect of leveraged debt (mortgages) and the tax advantages of depreciation and leveraged capital gains. The wealthiest investors typically hold a balanced portfolio of both.

What is the best property investment strategy for a beginner?

A standard single-let property in a high-demand commuter belt outside major cities (like Manchester, Leeds, or Birmingham). It offers the lowest barrier to entry, the easiest management, and the lowest risk profile while you learn the ropes.

Are there good regions where properties to invest yield the highest?

Currently, the North East, Scotland, and parts of the North West offer the highest rental yields in the UK. However, capital growth in the North East has historically been slower than the North West and Midlands.

How do I get more house investment tips?

Education is your greatest asset. Before deploying tens of thousands of pounds, spend time reading, analyzing rightmove data, speaking to local letting agents, and consulting with professional advisors.

At Shaded Canvas, we provide deep-dive analytics and strategy for serious investors looking to build generational wealth through UK real estate. Keep exploring our blog for more detailed breakdowns on market trends and investment models.

Stop being a landlord. Start being an investor.

Shaded Canvas introduces serious capital to vetted UK property opportunities — targeting 12–16% net returns.

Start Investing →