The financial mechanics of acquiring a new build property—particularly an off-plan apartment in a major regeneration zone—are fundamentally different from funding a traditional Victorian terrace.

When you buy secondary housing stock, you exchange and complete within a three-month window using a standard buy-to-let mortgage. When you buy a new build, you are navigating a 24-to-36 month build cycle, staged developer payments, valuation gaps, and commercial lending criteria that do not physically exist until the development receives practical completion.

If you fundamentally misunderstand how to finance new build property investment, you are exposing yourself to the ultimate off-plan catastrophe: contract default and the permanent loss of your deposit capital.

At Shaded Canvas, we underwrite complex property acquisitions daily. In this 3,000-word authority audit, we will break down the exact capital staging requirements for new build property in 2026. We will dissect developer payment plans, the transition from cash to commercial mortgages, the threat of the "Valuation Gap," and how elite investors leverage debt to execute these strategies safely.

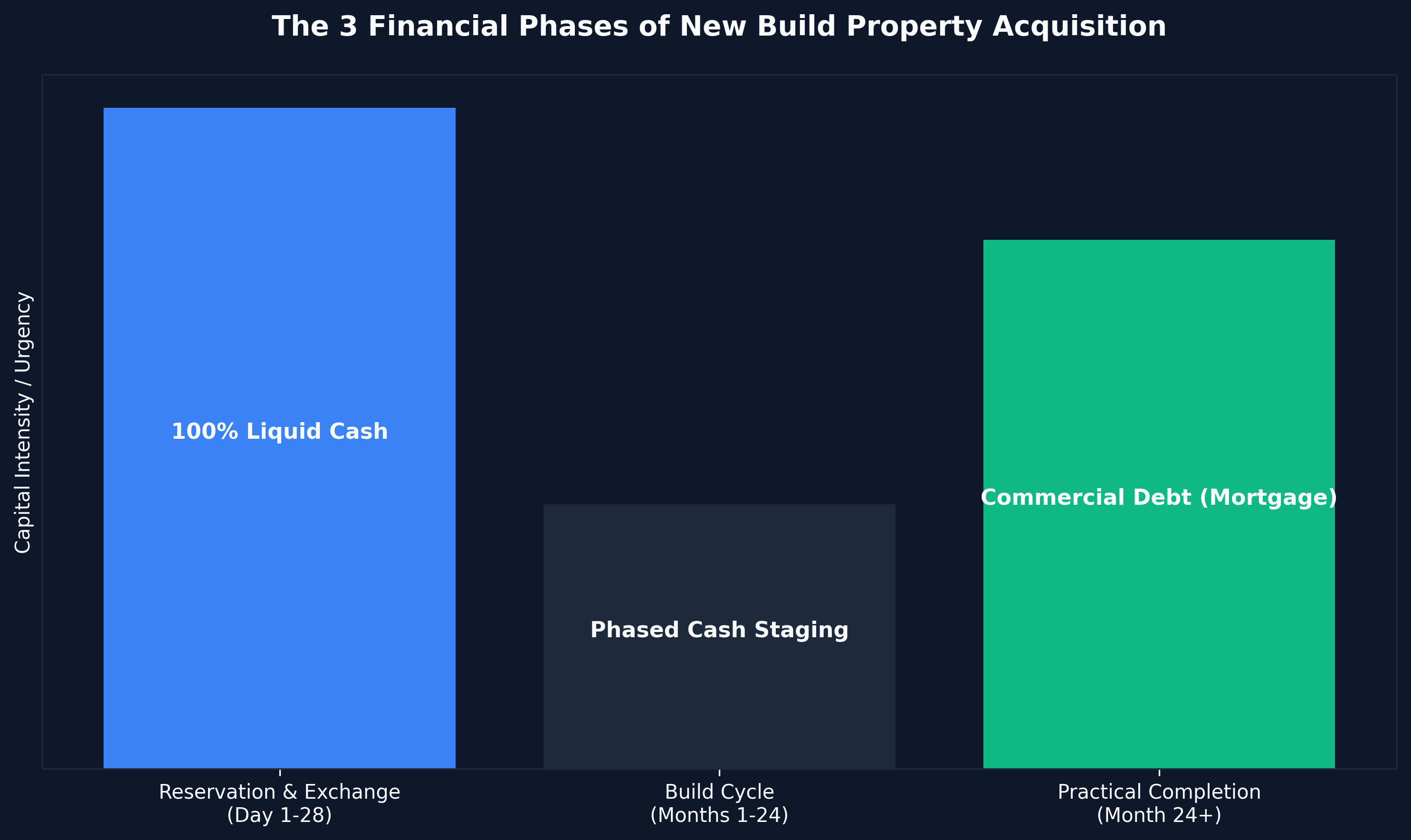

1. The Anatomy of a New Build Financial Cycle

To finance a new build, you must first understand the timeline. You are not buying a property; you are funding a construction contract that eventually yields a property.

The financial cycle is divided into three inflexible phases:

- Reservation & Exchange (Day 1 - Day 28): Securing the unit and locking in the purchase price.

- The Build Cycle (Months 1 - 24): The period of construction where your initial capital is deployed, but the asset cannot yet be mortgaged.

- Practical Completion (Month 24+): The moment the building is physically finished, legally certified, and the final balance becomes due.

You must have a concrete, stress-tested financial strategy for all three phases before you transfer your first £1,000.

Phase 1: Reservation & Exchange Finance

You cannot mortgage an unbuilt property at Day 1. Banks lend against physical bricks and mortar, not promises on a developer's brochure. Therefore, the first phase of new build finance is entirely reliant on personal liquid cash.

The Reservation Fee

To take a unit off the market, the developer requires a reservation fee. In 2026, this ranges from £2,000 to £5,000. This is typically non-refundable and must be paid immediately via debit card or bank transfer.

The Exchange Deposit

Within 21 to 28 days of paying the reservation fee, your solicitor will finalize the legal contracts. At this point, you "Exchange Contracts," making the purchase legally binding.

You must transfer the Exchange Deposit minus your Reservation Fee. Historically, developers demanded 20% to 30% at exchange. However, due to the high-interest-rate environment of 2026 restricting retail liquidity, many developers now accept 5% to 15% exchange deposits.

Example:

- Purchase Price: £250,000

- Reservation Fee: £5,000

- Required Exchange Deposit (10%): £25,000

- Cash you must physically transfer to your solicitor within 28 days: £20,000.

If you do not have this liquid cash available immediately, you cannot enter the new build market as an active buyer. You must instead look at fractional pooling structures (see the fractional property investment UK guide).

Phase 2: The Build Cycle (Developer Payment Plans)

Once you have exchanged contracts, the 24-month build cycle begins. How you finance this period depends entirely on your negotiation with the developer.

In 2026, developers offer three primary staging structures. Assessing these structures is covered extensively in our guide on the best buying off plan uk strategies.

Structure A: The Traditional Void

You paid 20% at exchange. You pay nothing for two years. The remaining 80% is due at completion.

- Pros: Simple. Protects your cash flow during the build.

- Cons: You suffered a massive £50,000 initial liquidity drain yielding 0% interest for two years.

Structure B: Phased Monthly Staging

You pay 5% at exchange. You then pay a further 15% across 24 equal monthly installments during the build cycle. 80% is due at completion.

- Pros: Requires very little initial capital (e.g., £12,500 on a £250,000 unit). Keeps your broader capital base liquid in high-yield bonds or equities.

- Cons: You must possess absolute conviction in your monthly cash flow from your primary business or employment to cover the £1,500+ monthly developer invoices.

Structure C: Milestone Funding

You pay 10% at exchange. You pay 10% when the building reaches "topping out" (the roof is installed). The final 80% is due at completion.

- Pros: Your cash is only demanded when the developer proves physical progress. Mitigates the risk of the developer going insolvent while holding 20% of your cash and having achieved zero structural construction.

Critical Note on Build Cycle Finance: None of these staging payments can be financed with a traditional mortgage. They must be funded via personal savings, business dividends, or highly speculative secondary debt (e.g., personal loans), though using personal loans for property deposits heavily corrupts your mortgage application at Phase 3.

Phase 3: Practical Completion (The Mortgage Event)

The building is finished. The developer issues a Notice to Complete. You legally possess 14 to 28 days to transfer the final 70% to 80% of the purchase price.

This is the phase where you finally deploy commercial leverage. If you owe the developer £200,000 (an 80% balance on a £250,000 unit), you will secure a Buy-To-Let (BTL) mortgage to bridge this gap.

The Mechanics of the New Build Mortgage

You cannot apply for a mortgage two years in advance. Mortgage offers are typically valid for six months. Therefore, you must engage a specialist new build broker approximately 4 to 5 months prior to the developer's estimated practical completion date.

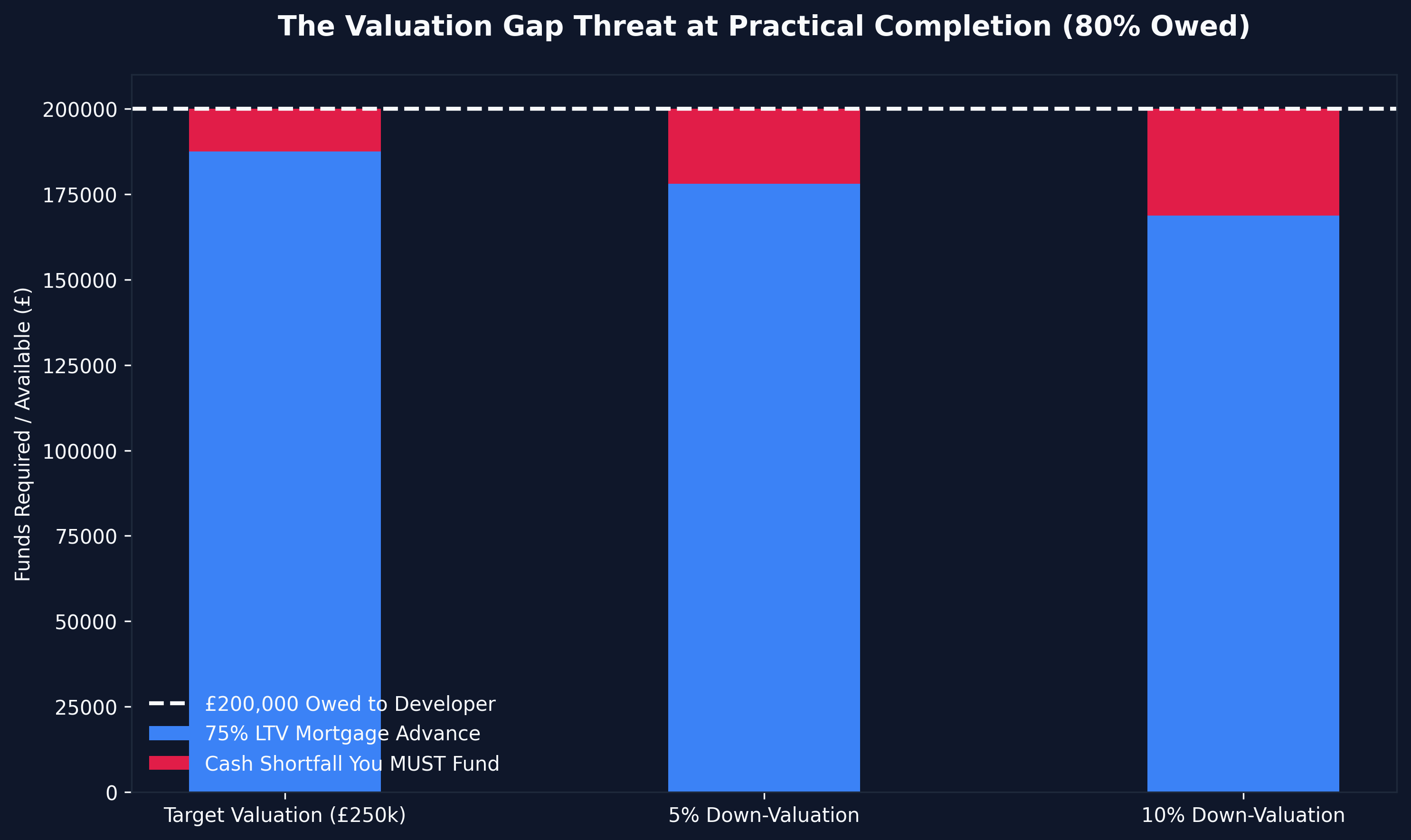

The broker will arrange a valuation. A RICS surveyor will visit the site (usually inspecting a "show apartment" if your unit is not fully finished) to confirm the asset's value. If the surveyor values the property at the original £250,000 purchase price, your BTL lender offers a 75% Loan-To-Value (LTV) mortgage.

- GDV (Gross Development Value): £250,000

- Mortgage Advance (75%): £187,500

- Balance Owed to Developer: £200,000

- Cash Shortfall: £12,500.

You must physically transfer that final £12,500, plus Stamp Duty Land Tax (SDLT), to your solicitor to complete the transaction.

Run these exact numbers through our bespoke off plan property investment yield calculator uk to model your specific cash shortfall at completion.

The Ultimate Threat: The Valuation Gap

Understanding how to finance new build property investment requires understanding why financing fails. The most catastrophic failure point in new build investing is the Valuation Gap.

When you agreed to pay £250,000 for the apartment two years ago, the developer baked a "New Build Premium" (usually 10% to 15%) into the price.

If the broader UK property market stagnates during the two-year build cycle, the RICS surveyor arriving at Month 23 will not value the apartment at £250,000. They will value it based on current market comparables, which might be £220,000.

The Mathematics of a Down-Valuation Disaster

- Contracted Purchase Price: £250,000

- Developer Balance Owed: £200,000 (assuming you paid 20% during the build)

- New RICS Valuation: £220,000

- Mortgage Advance (75% of new valuation): £165,000

You owe the developer £200,000. The bank is only giving you £165,000. You now have a £35,000 Cash Shortfall.

You have 28 days to find £35,000 in cash. If you cannot, you default on the contract. The developer terminates the agreement, keeps your £50,000 initial deposit, and potentially sues you for the remaining £35,000 deficit if they are forced to sell the unit to a third party at the lower £220,000 valuation.

Mitigating the Valuation Gap

Elite investors combat the valuation gap through heavy cash reserving. Do not deploy £50,000 into an off-plan deposit if £50,000 is your entire net worth. You must hold an additional 10% to 15% of the purchase price in liquid reserves (bonds, high-interest savings) specifically to bridge a potential down-valuation at completion.

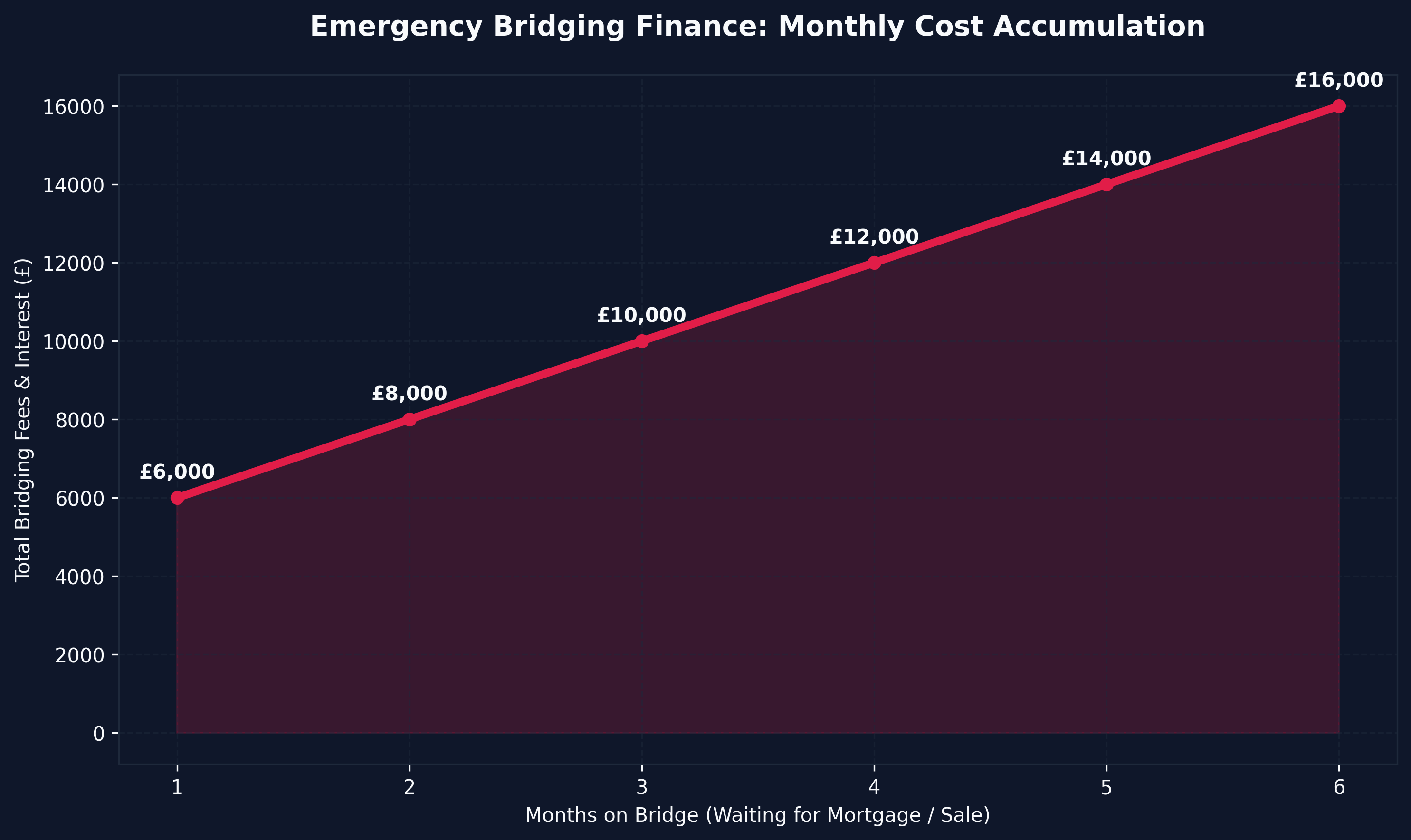

Alternative Finance: Short-Term Bridging

If you face a massive valuation gap, or if your buy-to-let mortgage application is delayed, you must secure emergency capital to complete the purchase and avoid contract default. This is the domain of Bridging Finance.

A bridging loan is a high-speed, short-term commercial loan designed to span a capital gap (typically lasting 3 to 12 months).

How Bridging Saves a New Build Contract

If you have 10 days until the developer's Notice to Complete expires and your BTL mortgage has fallen through, a bridging lender can deploy £200,000 within 72 hours.

- The Cost: Bridging finance is exorbitantly expensive. In 2026, expect to pay a 2% arrangement fee and 1% interest per month.

- The Exit Strategy: A bridging lender will only issue the funds if they possess absolute certainty regarding how they will be repaid. Your "exit strategy" is typically securing a standard BTL mortgage three months later once the paperwork is sorted, or immediately listing the completed property for sale on the open market.

Bridging is the exact financing mechanism used by investors executing the what is the brrrr method strategy, where properties are purchased unmortgageable, refurbished using bridging finance, and then refinanced onto commercial mortgages.

Tax Structuring and Financial Efficiency

Financing a new build is not purely about debt acquisition; it is about debt structuring. The legal entity you use to finance the asset dictates your ultimate net yield.

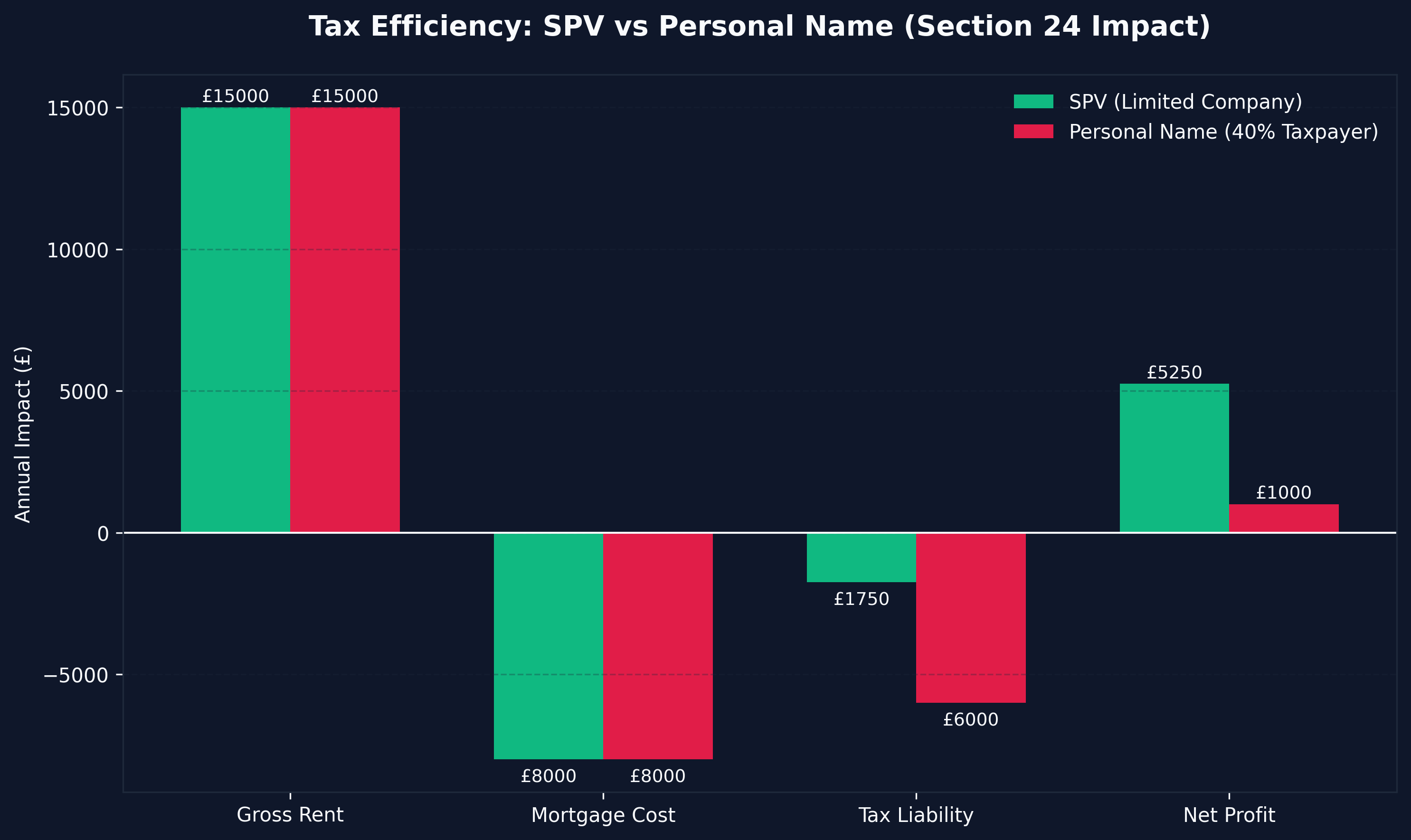

The Section 24 Threat (Personal Names)

If you secure the new build BTL mortgage in your personal name, you are subject to Section 24 of the Finance Act. This prevents you from deducting mortgage interest from your rental income before calculating your tax liability. If you are a higher-rate (40%) taxpayer, Section 24 can mathematically completely eliminate your net profit, forcing you to pay tax on money you never actually touched.

The SPV Corporate Structure

To circumvent Section 24, 85%+ of new build investments in 2026 are financed through Special Purpose Vehicles (SPVs)—dedicated Limited Companies set up solely to hold property.

- The Advantage: An SPV pays Corporation Tax (19% to 25%) on profit after the mortgage interest has been deducted. This preserves your yield.

- The Financing Reality: Commercial mortgage rates for Limited Companies are often 0.5% to 1% higher than personal mortgages. However, the tax efficiency almost always mathematically outweighs the higher interest rate.

We dissect these structural tax implications in granular detail in our taxes on buy rehab rent refinance repeat uk 2026 audit. The tax principles for BRRRR properties and New Build properties held in an SPV are identical.

Summary: The Shaded Canvas Checklist for New Build Finance

If you intend to deploy capital into the 2026 off-plan property market, your financial architecture must be flawless.

- Possess Liquid Day-1 Cash: Ensure you have 5% to 20% of the purchase price entirely liquid and unencumbered to exchange contracts.

- Stress-Test the Valuation Gap: Assume the property will down-value by 10% upon completion. Do you have the cash reserves to plug the shortfall? If not, do not exchange contracts.

- Model the BTL Mortgage: Run the projected rental income against typical 2026 commercial BTL stress tests (usually requiring 145% coverage at a 5.5% stressed rate). If the new build does not yield at least 5.5% gross, you will not be able to secure a 75% LTV mortgage at practical completion.

- Structure as an SPV: Consult a specialist property tax accountant before paying the reservation fee to establish the correct Limited Company architecture.

Financing a new build is fundamentally an exercise in risk management. The investors who fail are those who view off-plan property as a guaranteed 20% capital uplift and ignore the brutal mechanical realities of the two-year capital staging process.

Stop being a landlord. Start being an investor.

Shaded Canvas introduces serious capital to vetted UK property opportunities — targeting 12–16% net returns.

Start Investing →