Property sourcing in the UK is an industry clouded by contrasting opinions. On one side, busy professionals view property sourcers as their secret weapon—an extension of their investment strategy that buys them time and unlocks off-market gems. On the other side of the spectrum, investor forums like Reddit and Property118 are awash with horror stories: investors overpaying for "sloppy second" deals, falling prey to non-compliant operators, and watching their promised yields evaporate upon completion.

So, is using a UK property sourcer actually worth the £3,000 to £5,000 standard fee?

The short answer is yes, provided two absolute conditions are met: you understand the true timeline to amortise the sourcing fee, and you ruthlessly audit their legal compliance before signing the Terms of Business.

In this comprehensive, data-driven deep dive, we strip away the marketing fluff. We will model the exact break-even point for typical sourcing fees against 8% and 10% gross yields, detail the five mandatory compliance checkpoints every sourcer must pass, and equip you with the forensic techniques required to spot a "regurgitated" property deal from a mile away.

1. The Core Calculus: Time vs. Financial Leverage

At its foundation, paying a property sourcer is an arbitrage strategy: you are trading capital for time and access. The UK property market is remarkably inefficient; public platforms like Rightmove and Zoopla reflect retail pricing models. To achieve consistent Below Market Value (BMV) transactions or secure high-yielding Houses in Multiple Occupation (HMOs), an investor must either network relentlessly with motivated sellers and distressed landlords, or pay a middleman who already has that infrastructure built out.

Modelling the Break-Even Point of a Sourcing Fee

To determine if a sourcing fee is "worth it", we must treat that fee inherently as a capital expenditure (CapEx) against the lifetime yield of the asset.

Consider a standard scenario: You are acquiring a terraced house in the North West of England, a prime hotspot for high-yield buy-to-let (BTL) property.

- Purchase Price: £120,000

- Standard Sourcer Fee: £3,000 (often 2.5% of purchase price or a flat rate)

- Renovation / Strategy: Light refurbishment for a single-let BTL.

- Projected Gross Yield: 8%

- Annual Gross Income: £9,600

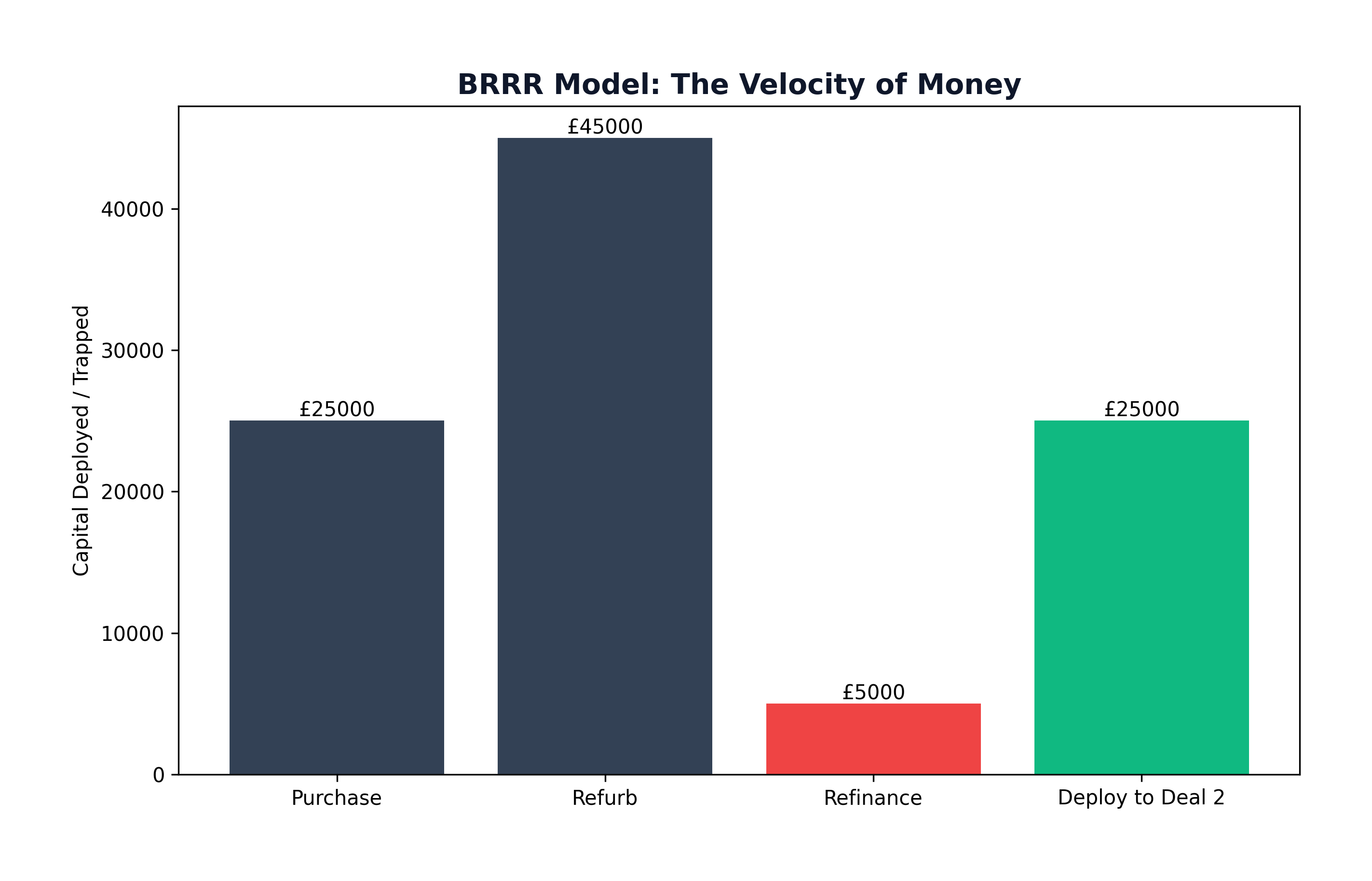

If we factor the £3,000 sourcing fee directly into your initial cash left in the deal (alongside your 25% deposit, Stamp Duty Land Tax, and conveyancing fees), the critical metric becomes the Recovery Period—how many months of net positive cash flow does it take to absorb that £3,000 fee before you are genuinely into "pure profit"?

| Investment Component | Cost Breakdown |

|---|---|

| Deposit (25%) | £30,000 |

| Stamp Duty (3% Surcharge) | £3,600 |

| Legals & Broker Fees | £1,500 |

| Sourcing Fee | £3,000 |

| Total Initial Capital Required | £38,100 |

If the property generates a net monthly cash flow of £350 (after mortgage interest, agents' fees, insurance, and maintenance provisions), the sourcing fee of £3,000 takes approximately 8.5 months to amortise out of real net cash flow.

The Verdict: If the property was genuinely locked in at 15% Below Market Value—giving you £18,000 in immediate equity—the £3,000 fee is exceptionally cheap leverage. However, if the sourcer merely found an on-market property that you could have bought at the same price yourself, that 8.5-month recovery period is entirely dead weight dragging down your Return on Capital Employed (ROCE).

2. Unmasking "Regurgitated" Deals: The Reddit Red Flag

One of the most persistent complaints unearthed when mining investor sentiment across Reddit (r/UKProperty) and specialised property forums is the phenomenon of the "regurgitated deal" or "sloppy seconds."

What is a Regurgitated Deal?

A regurgitated deal occurs when a property sourcer actively markets an asset to you that has already been rejected by their top-tier, experienced investors. This often happens because:

- The promised uplift upon refurbishment (the End Value or GDV) is mathematically flawed.

- The area is plagued by hyper-local issues (e.g., prohibitive Article 4 directions limiting HMO conversion, restrictive covenants, or uninsurable subsidence risks).

- The deal is effectively a "daisy-chain" scenario, where two or three different sourcers are adding their fees onto the same sub-par property, artificially inflating the headline cost.

How to Forensically Spot Recycled Opportunities

You must operate under the assumption that if an off-market deal was truly spectacular, the sourcer’s inner circle would have absorbed it within 24 hours. If a deal is being aggressively pushed to you—especially via mass email blasts—you must audit it rigorously.

The Verification Playbook:

- Check the Land Registry API: Reverse-search the street. Has the vendor recently remortgaged? Have similar properties sold repeatedly in rapid succession without value uplift?

- The Rightmove Cross-Check: Is it truly off-market? Often, sourcers repackage properties that have been sitting stagnant on Zoopla for 120 days. They slice a 5% "negotiated discount" off the inflated asking price and slap a £3,000 sourcing fee on top. This is not sourcing; this is an expensive retail transaction in disguise.

- Demand the "Why": Ask the sourcer directly: "If this property yields 10% net, why hasn't it been bought by your primary retained clients?" A legitimate sourcer will offer a transparent answer, such as a vendor requiring a specific cash-buyer timeline that other investors couldn't meet.

3. The 5-Point Legal Compliance Checklist (Non-Negotiable)

A shocking percentage of individuals operating as property sourcers on Instagram and TikTok are acting illegally. In the UK, property sourcing constitutes estate agency work under the Estate Agents Act 1979. This means the individual or company you pay must adhere to strict regulatory supervision.

Failing to verify these five compliance points doesn't just put your £3,000 fee at risk—it exposes your entire capital stack to fraudulent transactions, money laundering investigations, and catastrophic civil liabilities.

Do not sign a Terms of Business document, and certainly do not transfer a sourcing fee, until you have confirmed the following five pillars of compliance:

1. HMRC Anti-Money Laundering (AML) Supervision

This is a legal baseline constraint. Any business acting as a property sourcing agent must be registered with HMRC for AML supervision. This ensures they are legally vetting both buyers and sellers, preventing your funds from becoming entangled in illicit supply chains. Ask for their HMRC registration number and verify it directly.

2. Membership of an Approved Redress Scheme

By law, every estate agent and property sourcer must belong to one of two government-approved redress schemes: The Property Ombudsman (TPO) or the Property Redress Scheme (PRS). If the sourcer provides false yield estimations or misrepresents a structural defect and refuses to refund your fee, the redress scheme provides you with an independent, legally binding dispute resolution framework.

3. Professional Indemnity (PI) Insurance

Imagine paying a sourcer who recommends a property for HMO conversion, only for you to discover post-completion that the property sits within an Article 4 directive zone preventing the conversion. Professional Indemnity insurance guarantees that if the sourcer provides negligent financial or structural advice, there is a financial safety net to compensate you in civil court. Without PI insurance, you are suing a shell company with zero assets.

4. Registration with the Information Commissioner’s Office (ICO)

Property sourcing requires handling highly sensitive financial data, passports, bank statements, and biometric verification. Sourcers must hold an active registration with the ICO to ensure they handle your data strictly in accordance with GDPR regulations.

5. Client Money Protection (CMP) Registration (If Handling Client Funds)

While sourcers rarely hold rent, some handle reservation fees. If your money enters an account controlled by the sourcer, they must possess active Client Money Protection.

4. The Value Matrix: When a Sourcer is Absolutely Essential

Having established the heavy risks and required diligence, we must acknowledge why elite investors continue to leverage professional sourcers.

When you partner with a compliant, data-first sourcer, the mathematics of wealth creation accelerate exponentially.

Sector-Specific Advantage

If you are transitioning from single-let BTLs to commercial-to-residential conversions, Title Splitting, or large-scale HMOs, the learning curve is steep. The nuances of commercial lending rates, planning permissions (Permitted Development Rights), and complex building regulations mean that making a mistake costs tens of thousands. Paying a £5,000 sourcing fee to acquire a fully-appraised, high-yielding commercial conversion is fractional risk management. You are paying for their 10,000 hours of commercial zoning mastery.

Geographic Scalability

For Southern-based investors attempting to tap into the high rental yields of the North East, Yorkshire, or the North West, geographical distance is the enemy of due diligence. A locally embedded sourcer understands the micro-geography: they know that the west side of a specific street achieves £150 more in monthly rent simply because of a school catchment boundary, while the east side is plagued by anti-social behaviour. This hyper-local street-by-street intelligence cannot be scraped from an API; it requires boots on the ground.

Direct-to-Vendor Networks (The True Off-Market)

The ultimate value proposition of a sourcer is their black book. Top-tier sourcers invest thousands in direct marketing (leafleted drop campaigns, distressed landlord targeting, probate networking). They intercept motivated sellers long before an estate agent inflates the listing price. If your sourcer secures a £200,000 property for £160,000 because of a pre-existing relationship with an exhausted landlord, their fee pays out in instant, tangible equity on day one.

Core Takeaways: Balancing the Scales

The question "is a property sourcer worth it in the UK" requires you to look in the mirror. If you possess abundant free time, local market intelligence, and strong negotiation skills, you can source your own deals and optimise your initial capital outlay.

However, if you are a cash-rich, time-poor professional looking to deploy capital efficiently and bypass the retail market, a fully compliant, heavily vetted sourcer is the most powerful catalyst for portfolio growth available.

Your primary directive is to shift your mindset from "passive buyer" to "forensic auditor." You are not hiring a mystic who prints money; you are employing an independent contractor subject to intense scrutiny.

Next Steps for Immediate Execution

- Demand the Compliance Document Suite: Before looking at a single deal in a sourcer's portfolio, ask for an email attaching their HMRC AML number, PRS/TPO membership certificate, ICO registration, and PI insurance schedule. If they hesitate, cease communication immediately.

- Reverse Target Your Requirements: Do not blindly accept whatever property a sourcer emails out. Give them a hyper-specific mandate: "I require a freehold semi-detached house within three miles of the Manchester Ring Road, requiring light structural work, with a proven post-refurbishment yield floor of 7.5%." Ensure they hunt for you, rather than hunting you to sell their dead stock.

- Audit the Mathematics Rigorously: Run every presented deal through an independent surveyor and use advanced BRRR (Buy, Refurbish, Refinance, Rent) modelling spreadsheets to calculate the exact month your initial capital invested—inclusive of the sourcing fee—recovers. Do not trust their promotional PDFs.

Stop being a landlord. Start being an investor.

Shaded Canvas introduces serious capital to vetted UK property opportunities — targeting 12–16% net returns.

Start Investing →