Property sourcing remains one of the most dynamic sectors within the UK real estate market. As we navigate the complexities of 2026, including the implementation of the Renters' Rights Act and shifting economic conditions, the ability to secure funding for property deals is paramount. This comprehensive guide details exactly how to finance property sourcing UK strategies, ensuring you remain competitive and compliant.

The 2026 UK Property Market Context

Before diving into specific financing methods, it is essential to understand the landscape. In 2026, the UK property market has entered a phase of "steady momentum." Inflation has cooled toward the Bank of England's target, leading to gradual base rate cuts and improved mortgage affordability.

However, regulatory changes, such as the abolition of Section 21 and the shift toward open-ended tenancies, mean that investors are more cautious. They are demanding higher scrutiny and better yields from sourcers. Consequently, property sourcing compliance UK standards have tightened, and sourcers must deliver "compliance-ready" portfolios.

Understanding Deal Packaging Fees and Sourcing Capital

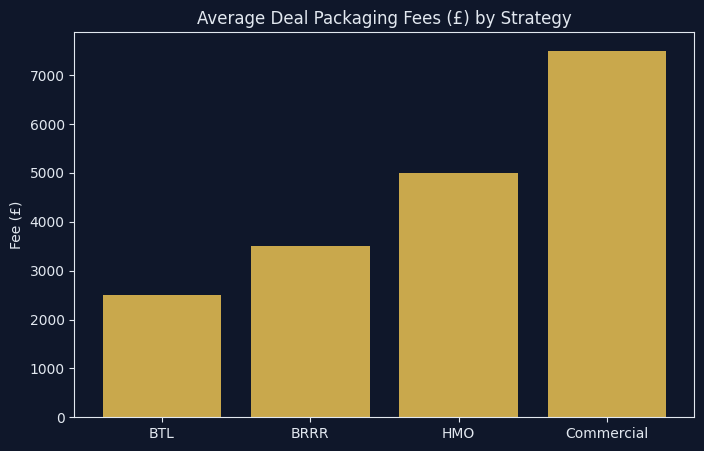

Many new sourcers assume they need substantial personal capital to start. While having initial funds helps with operational costs, the core of property sourcing involves finding mispriced assets and connecting them with investors. The revenue model relies on deal packaging fees—typically ranging from 1% to 3% of the purchase price, or a fixed fee of £3,000 to £5,000 per deal.

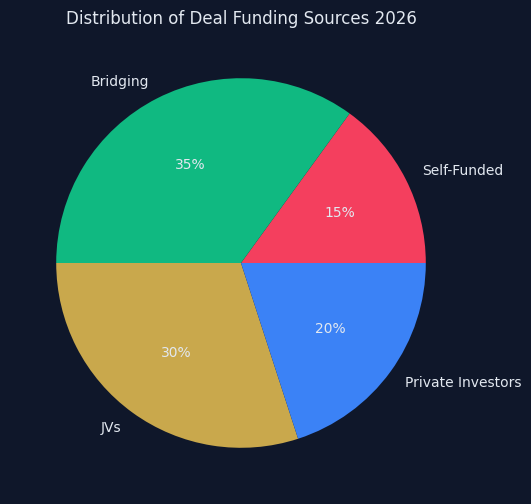

To scale a sourcing business, however, you eventually need to finance your own deals or facilitate the financing for your investors. Let's explore the primary avenues for financing in 2026.

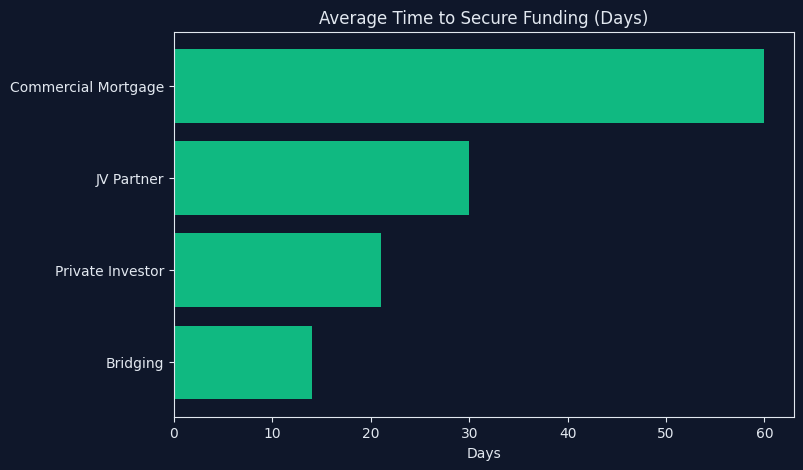

1. Bridging Finance for Sourcing

Bridging finance remains the lifeblood of agile property sourcing. It is short-term, high-interest funding designed to "bridge" the gap between a purchase and a more permanent financial solution (like a buy-to-let mortgage) or the sale of the property.

When to Use Bridging Finance

- Auction Purchases: Auctions require completion within 28 days, making traditional mortgages unviable.

- Uninhabitable Properties: Traditional lenders will not mortgage properties lacking a functioning kitchen or bathroom. Bridging loans provide the capital to purchase and refurbish these assets.

- Below Market Value (BMV) Deals: Fast cash offers often secure significant discounts. Bridging allows sourcers or their investors to act as cash buyers.

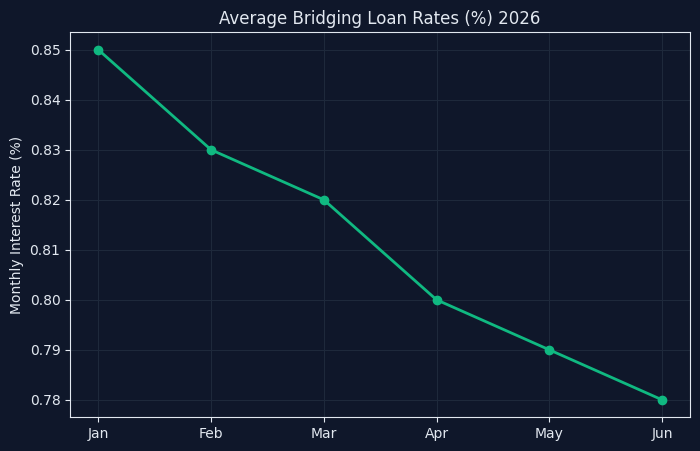

Securing Bridging Finance in 2026

Lenders in 2026 are heavily focused on the "exit strategy." Whether the plan is to refinance onto a long-term product or sell, the numbers must be robust. A well-documented property sourcing agreement and a clear outline of the refurbishment timeline are critical when presenting a case to a bridging lender.

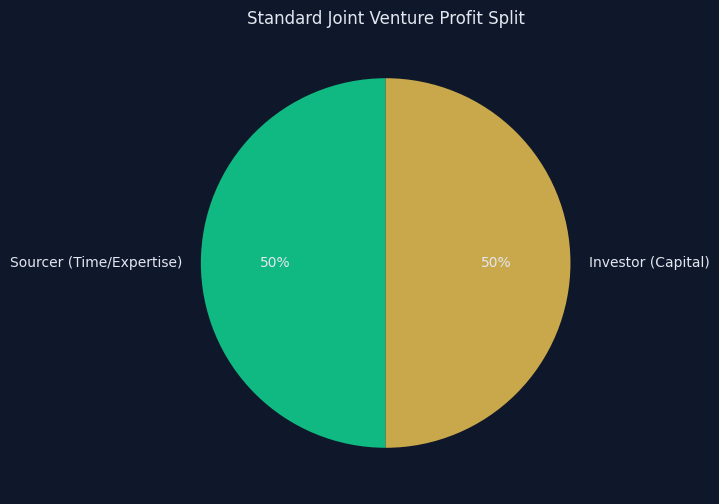

2. Joint Venture Property Investment (JVs)

A Joint Venture (JV) is a strategic partnership where two or more parties combine resources. In property sourcing, this typically involves a "time and expertise" partner (the sourcer) and a "capital" partner (the investor).

Structuring a JV

The sourcer finds the deal, manages the refurbishment, and handles the tenanting process. The capital partner provides the deposit, the refurbishment funds, and often secures the mortgage. Profits are then split, commonly on a 50/50 basis, after the initial capital is returned.

Why JVs are Thriving in 2026

With the increased complexity of planning reforms and building safety regulations, investors are actively seeking knowledgeable local experts. By entering a joint venture property investment, sourcers can scale their portfolios without hitting a financial ceiling, while investors gain access to lucrative deals they wouldn't have found themselves.

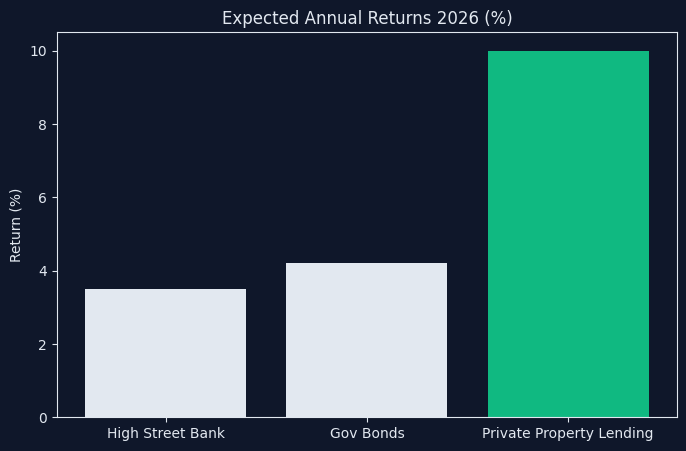

3. Private Investors for Property Sourcing

Raising capital from private individuals is another powerful way to finance deals. These are often high-net-worth individuals (HNWIs) or people with stagnant savings seeking better returns than traditional banks offer.

The Pitch

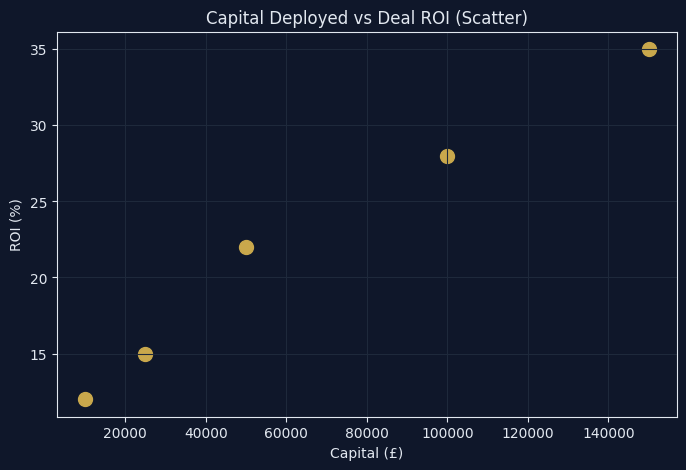

When approaching private investors for property sourcing, the pitch must be flawless. You are essentially asking them to act as a private bank. You must offer a fixed return over a specific period (e.g., 8% to 12% per annum over 12 months) secured by a first or second charge on the property or a personal guarantee.

Compliance is Non-Negotiable

Raising private finance falls under strict Financial Conduct Authority (FCA) regulations. In 2026, property sourcing compliance UK requires rigorous Anti-Money Laundering (AML) checks and clear, legally binding loan agreements. Never solicit funds publicly unless you are fully compliant with PS13/3 regulations regarding the promotion of non-mainstream pooled investments.

4. Angel Investors and Syndication

For larger projects, such as commercial-to-residential conversions or large HMOs, syndication is becoming increasingly popular. This involves pooling funds from multiple investors to fund a single, substantial deal.

While lucrative, syndication requires complex legal structures (often involving Special Purpose Vehicles - SPVs) and stringent regulatory adherence. It is a strategy best reserved for experienced sourcers with a proven track record of successful deal delivery.

Crafting the Property Sourcing Agreement

Regardless of how a deal is financed, the bedrock of a successful transaction is the property sourcing agreement. This contract dictates the relationship between the sourcer and the investor.

In 2026, this agreement must explicitly cover:

- The exact deal packaging fees and payment milestones.

- The scope of the sourcer's responsibilities (e.g., just finding the deal vs. managing the project).

- Compliance declarations, proving the sourcer is registered with the Property Ombudsman, ICO, and HMRC for AML.

- A clear refund policy if the deal falls through due to factors outside the investor's control.

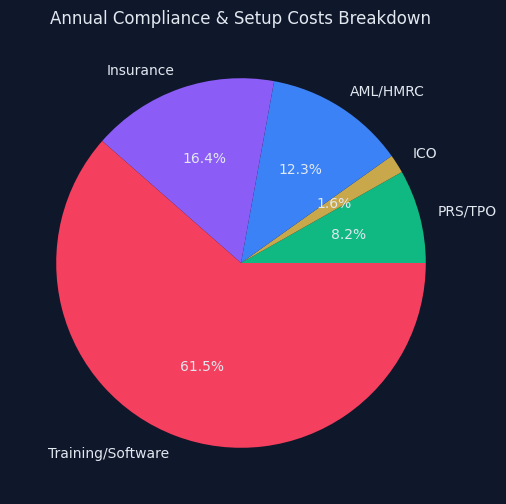

Building a Compliance-Ready Business

Financing property sourcing is intrinsically linked to compliance. Lenders and savvy investors conduct extensive due diligence. Ensure your business meets all 2026 standards:

- Redress Scheme: Registration with the Property Ombudsman (TPO) or the Property Redress Scheme (PRS).

- Professional Indemnity Insurance: Adequate cover is mandatory.

- Anti-Money Laundering (AML): Registration with HMRC and robust systems for checking client ID and source of funds.

- Data Protection: Registration with the Information Commissioner’s Office (ICO).

Conclusion: The Road Ahead

Learning how to finance property sourcing UK operations effectively is what separates successful property businesses from struggling amateurs. By mastering bridging finance, structuring equitable joint ventures, and navigating the private investor landscape with strict adherence to 2026 compliance standards, you position your sourcing business for sustainable, long-term growth in a dynamic market.

Stop being a landlord. Start being an investor.

Shaded Canvas introduces serious capital to vetted UK property opportunities — targeting 12–16% net returns.

Start Investing →