"Below Market Value" (BMV) is arguably the most abused marketing term in the UK property sector. If you spend five minutes scrolling through a property networking group or a property sourcing email list, you will be bombarded with claims of "20% BMV" deals.

For the uninitiated investor, this sounds like an instant wealth hack. The reality is that 95% of what is advertised as "Below Market Value" is simply a property that was artificially overpriced to begin with.

In this authority guide, we are going to brutally dissect the difference between a "True BMV" deal (which actually builds day-one equity) and a "Fake BMV" deal (which traps amateur capital). We will also examine the strict valuation criteria used by RICS surveyors, and why buying true distressed property almost always requires commercial bridging finance.

The "Fake BMV" Trap: Why A Discount Is Not Equity

The single biggest mistake new investors make is confusing a "discount" with "Below Market Value".

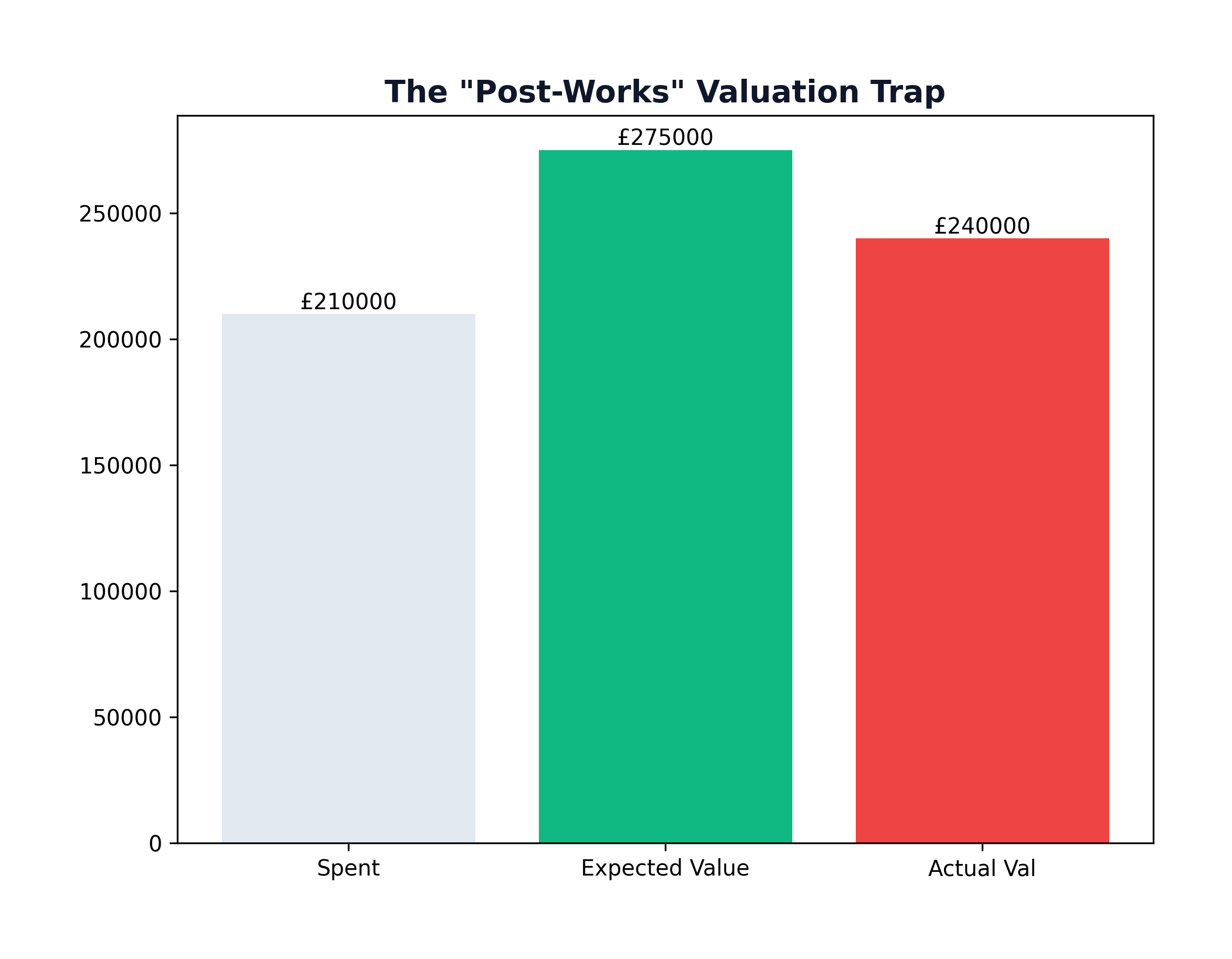

Imagine a developer builds a block of off-plan apartments in Manchester. The developer creates a brochure valuing the apartments at £250,000. To incentivize fast sales, they offer investors a "15% BMV Discount," dropping the asking price to £212,500.

An amateur investor buys it, believing they just locked in £37,500 of instant equity.

When it comes time to complete six months later, the mortgage lender sends out an independent RICS (Royal Institution of Chartered Surveyors) valuer. The surveyor ignores the developer's shiny brochure. They look at the Land Registry data for identical apartments in the immediate postcode. They see that comparable apartments are actually selling for £210,000.

The surveyor down-values the property to £210,000. The investor did not get a 15% BMV deal; they paid £2,500 above the actual market value.

This is the "Fake BMV" trap. A discount from an arbitrary asking price is meaningless. Market value is dictated solely by recent, localized Land Registry sold data—not by estate agents, and certainly not by property sourcers.

Defining "True BMV": The Distress Premium

True BMV exists, but it is not found in a brochure. True BMV is the financial byproduct of distress.

A property is only genuinely Below Market Value if a RICS surveyor would evaluate its current condition, look at recent comparables, and confirm that you are purchasing the asset for mathematically less than what it would achieve on the open market today.

This distress generally falls into three categories:

- Vendor Distress (Time): The seller is facing repossession, divorce, or a broken chain, and requires a guaranteed cash completion within 14 days. They are willing to sacrifice 15% of the property's equity in exchange for absolute speed and certainty.

- Asset Distress (Condition): The property is uninhabitable. It lacks a functioning kitchen, bathroom, or suffers from severe structural defects like subsidence or Japanese Knotweed. Standard mortgage lenders will refuse to lend against it, locking out 90% of retail buyers.

- Legal Distress: The property has a defective lease, severe boundary disputes, or missing planning permissions.

True BMV deals are almost always "unmortgageable" in their current state. This is why professional investors rely on commercial bridging finance to acquire them.

The Financing Reality: Why True BMV Requires Bridging

If you find a genuine BMV property—say, a repossession completely gutted of its wiring and plumbing—you cannot buy it with a standard 75% LTV Buy-to-Let mortgage. The lender's surveyor will flag the property as uninhabitable and place a £0 retention on the loan.

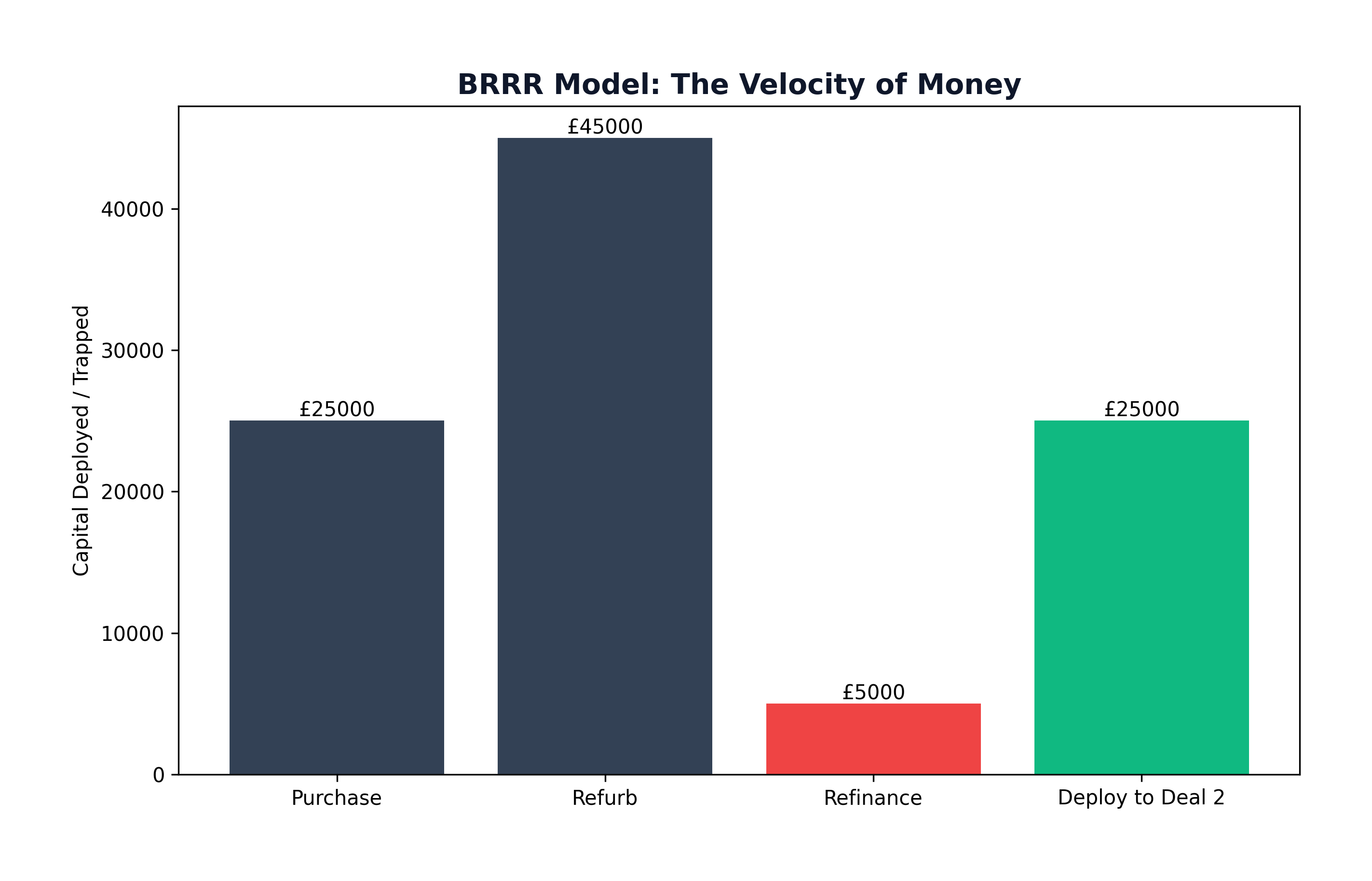

To execute this deal, you must use a commercial bridging loan.

Bridging finance is short-term, expensive debt. You will typically pay 1% per month in interest, alongside a 2% arrangement fee.

The Math of Bridging a BMV Deal: If you buy a distressed £100,000 property (with a true end value of £150,000) using a £70,000 bridge for six months:

- Arrangement Fee: £1,400

- 6 Months Interest: £4,200

- Total Finance Friction: £5,600

You must deduct this £5,600 from your perceived "instant equity." If your property sourcing company is not factoring commercial bridging costs into their Return on Capital Employed (ROCE) calculations, they are fundamentally misleading you.

The Property Sourcing Paradox

Many amateur investors rely on property sourcing companies to find BMV deals. The paradox is that genuine BMV deals are highly lucrative; if a sourcer finds a property with £40,000 of real equity built-in, why would they sell that lead to you for a £3,000 fee instead of buying it themselves?

The answer is usually one of two things:

- They lack the capital: The sourcer does not have the liquid cash or bridging facilities to execute the deal themselves.

- The deal is Fake BMV: The "equity" is an illusion based on aggressive End Value (GDV) estimates, and the sourcer is simply monetizing a standard market-value lead.

Before paying any sourcing fee for a "BMV" property, you must demand a rigorous breakdown of their comparables. Do not accept Rightmove "For Sale" listings as comparables. Demand exact Land Registry sold data from the last six months, within a 0.25-mile radius, for identical property types.

Is BMV Worth It? The Final Verdict

Yes, pursuing True BMV property is the most mathematically efficient way to build a high-yielding portfolio, as it allows you to recycle your capital through the Buy, Refurbish, Refinance (BRRR) model.

However, it is not a passive strategy. It requires navigating expensive commercial finance, managing complex refurbishments, and ruthlessly verifying data against RICS standards. If you are looking for a passive investment, buy a standard yield property at market value. If you want to force appreciation and scale rapidly, learn to hunt for true distress.

📚 Related Reading

Stop being a landlord. Start being an investor.

Shaded Canvas introduces serious capital to vetted UK property opportunities — targeting 12–16% net returns.

Start Investing →