The United Kingdom remains the second most targeted destination for cross-border real estate investment in Europe — behind only Germany in total transaction volume — and attracts capital from North America, the Middle East, Asia, and pan-European investors seeking stable, rule-of-law jurisdictions. For overseas investors evaluating a UK allocation in 2026, the opportunity set has broadened beyond Prime Central London to include compelling yield plays in Northern England, institutional-grade student accommodation, and impact-aligned <a href="https://blog.shadedcanvas.co.uk/post/<a href="https://blog.shadedcanvas.co.uk/post/<a href="https://blog.shadedcanvas.co.uk/post/pgim-real-estate-uk" style="color:#c9a84c;text-decoration:underline;font-weight:500">pgim-real-estate-uk" style="color:#c9a84c;text-decoration:underline;font-weight:500">pgim-real-estate-uk" style="color:#c9a84c;text-decoration:underline;font-weight:500">pgim. This playbook covers the full landscape.

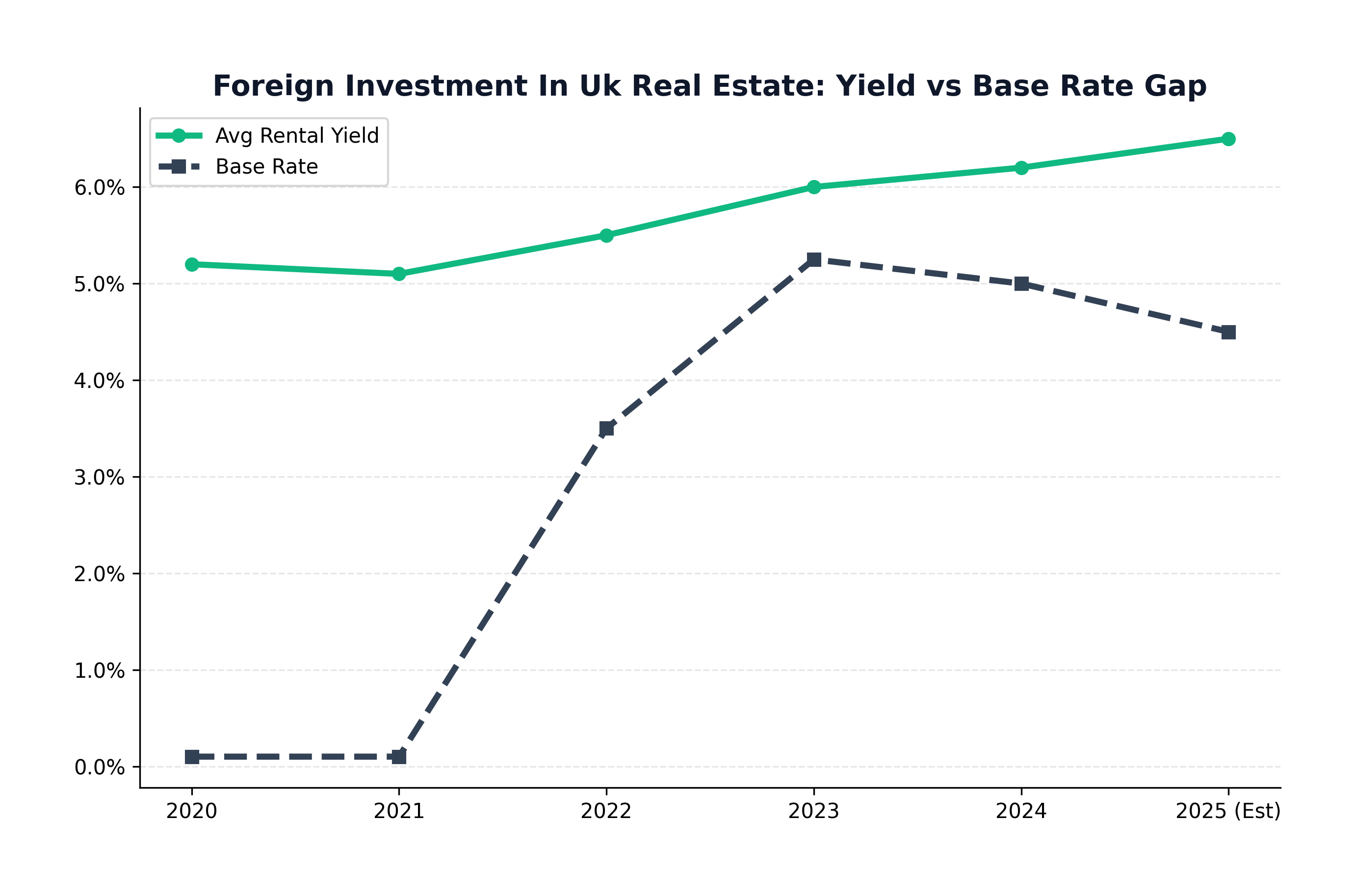

Figure: Yield vs Interest Rates

Figure: Yield vs Interest Rates

Why UK Is Still #2 in Europe for Cross-Border FDI

Despite political turbulence — Brexit, multiple changes of government, evolving tax treatment of non-domiciles — the UK's structural attractions for real estate investment have proven durable. English law remains the contractual standard for global finance, property rights are enforceable and transparent, and the market's depth (both in terms of liquidity and the diversity of asset classes available) is unmatched outside the United States.

The Register of Overseas Entities (ROE), introduced in August 2022 under the Economic Crime (Transparency and Enforcement) Act, has added compliance requirements for overseas owners of UK property — all foreign entities owning UK land must now register at Companies House with beneficial ownership details disclosed. The administrative burden is real but manageable; the more significant effect has been on owners of property held in offshore structures who previously maintained privacy. For compliant investors with clean structures, the ROE is an inconvenience rather than a barrier.

Hotspots Beyond London: Where the Yield Numbers Work

The Northern Powerhouse: Manchester and Liverpool

Manchester has emerged as the UK's most compelling investment city outside London for overseas buyers seeking a combination of yield and growth. Average gross BTL yields in Greater Manchester sit at 6.5–7%, underpinned by one of the UK's fastest-growing rental markets — net in-migration, a large student population (60,000+ students across the city's universities), and an expanding financial and tech sector driving demand for quality rental accommodation. Liverpool delivers even higher yields (7–8% gross in some postcodes) at lower entry prices, with regeneration investment in the waterfront and city centre providing a capital growth narrative.

Student Accommodation (PBSA)

Purpose-Built Student Accommodation is one of the UK's most institutionally popular real estate sectors for overseas capital. The UK has 2.8 million students competing for approximately 700,000 purpose-built beds — a structural undersupply that supports strong occupancy rates (typically 97–99% in well-located cities) and consistent rent growth. Net yields of 5–7% are achievable in strong university cities, with Manchester, Nottingham, Leeds, and Edinburgh being the most frequently targeted by international capital. PBSA is attractive to overseas investors because it is operationally managed by specialist operators, removing the day-to-day management burden.

Social Housing and Impact Investing

The UK has a structural deficit of approximately 4 million social and affordable homes. This has created an emerging opportunity for private capital — particularly institutional and impact-focused overseas investors — to fund new supply through development partnerships or long-term lease arrangements with registered housing providers (housing associations). Net yields of 6–8% are achievable on well-structured social housing investments, with long leases (often 25 years), RPI/CPI-linked rent escalation, and government-backed tenants providing cash flow certainty that commercial property cannot match.

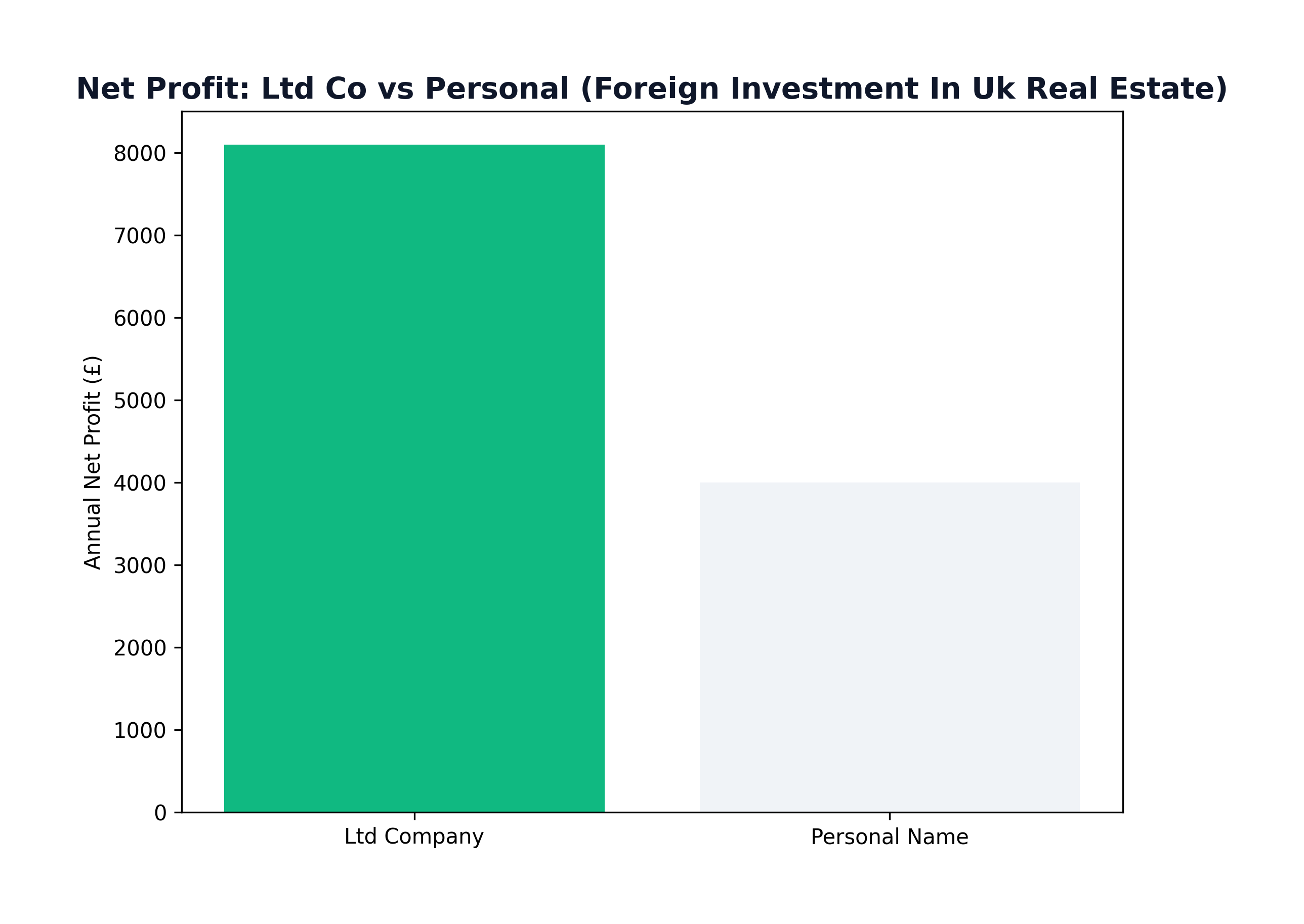

Figure: Tax Trap: Personal vs Ltd

Figure: Tax Trap: Personal vs Ltd

Legal and Tax Structure for Non-Resident Investors

The 2% SDLT surcharge for overseas buyers applies across England and Northern Ireland. Scotland and Wales have their own equivalents. This surcharge stacks on top of the 3% additional dwelling surcharge, meaning non-resident buyers of investment property in England face total SDLT at rates reaching 17% on portions above £1.5 million. For commercial property purchases, the SDLT structure is more straightforward, and the surcharges do not apply — making commercial assets particularly attractive for cost-conscious overseas buyers.

Capital Gains Tax applies to non-resident disposals of UK residential property (introduced 2015) and commercial property (introduced 2019) at the same rates applicable to UK residents — 18% basic rate and 24% higher rate for residential from April 2024. Non-residents must file a return within 60 days of completion. Using a UK SPV structure means the gain is crystallised at corporation tax rate (25%) on disposal of the underlying property, though the sale of the SPV's shares rather than the property itself may achieve different tax treatment — specialist advice is essential.

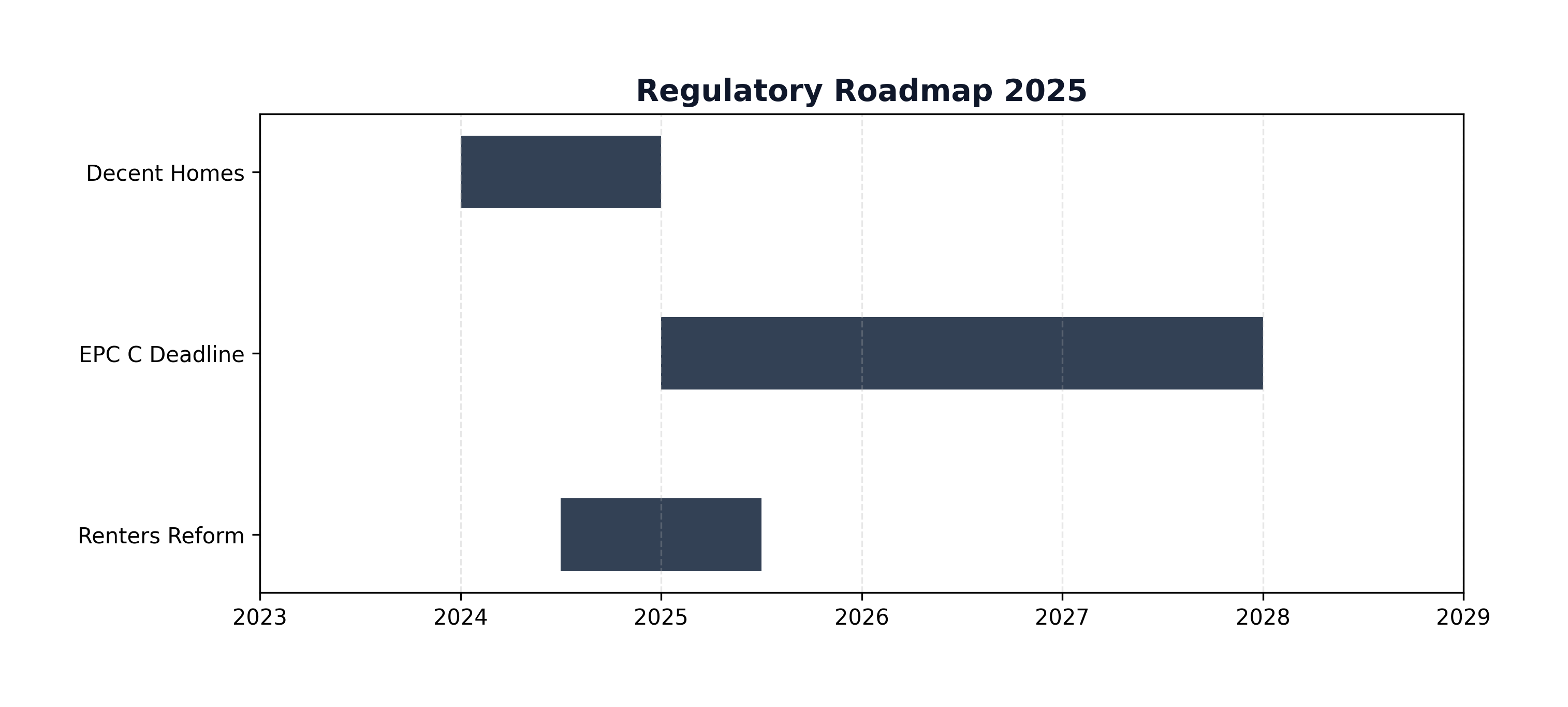

Figure: Regulatory Roadmap

Figure: Regulatory Roadmap

Financing for Overseas Buyers

UK mortgage availability for non-resident buyers has improved since 2020, with several specialist lenders actively targeting international HNWIs. Maximum LTVs are typically 65–75% for residential and 60–70% for commercial, with lenders requiring evidence of foreign income, bank references, and in some cases a UK footprint (existing UK bank account, previous UK property ownership). Currency risk — the risk that exchange rate movements erode returns when profits are converted back to the investor's home currency — is significant on leveraged positions and should be hedged using forward contracts or currency options where practical.

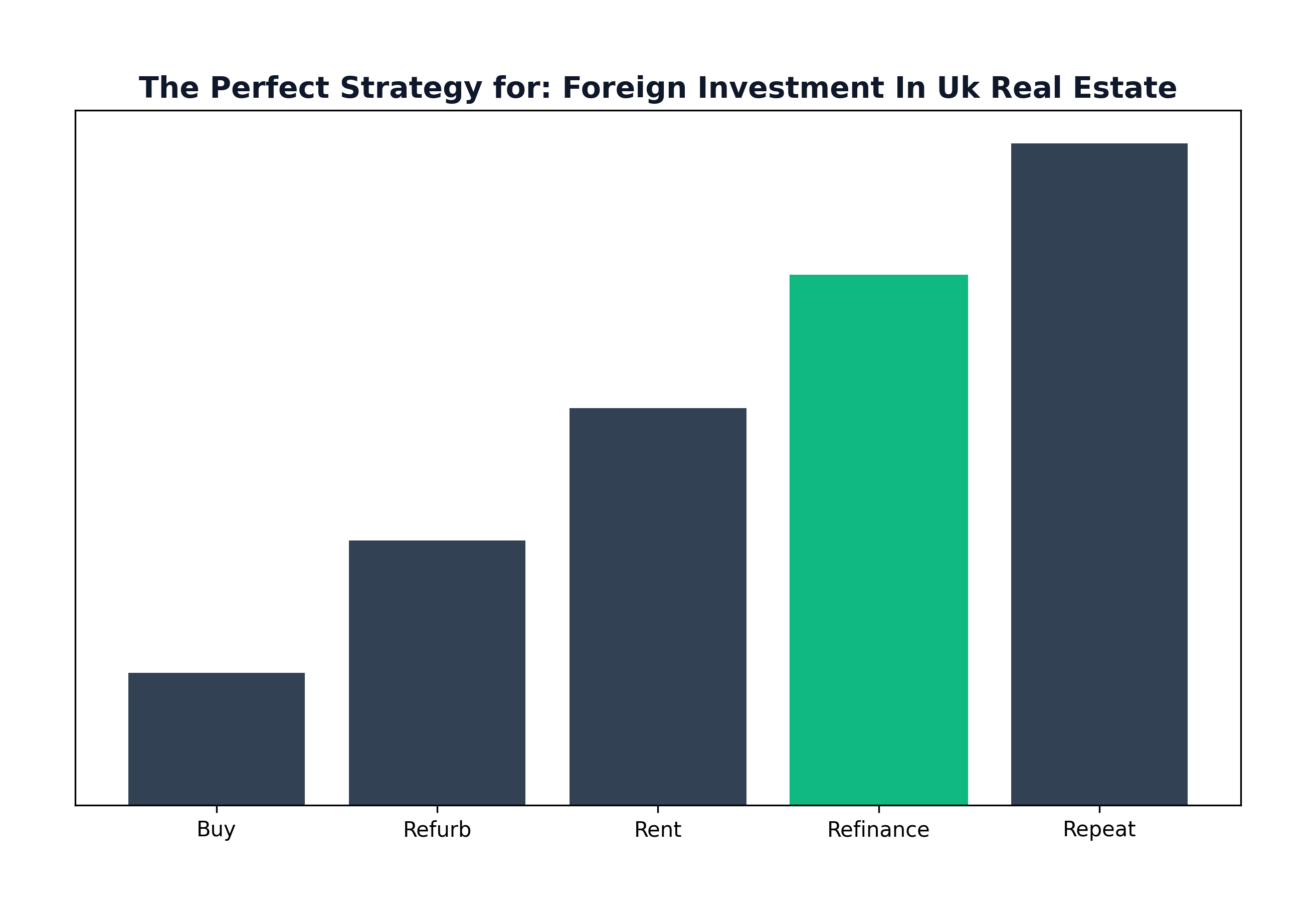

Figure: Strategy Cycle

Figure: Strategy Cycle

Risks and Regulatory Considerations

The National Security and Investment (NSI) Act 2021 gives the UK government powers to review and intervene in transactions that could affect national security. While the primary targets are technology, defence, and critical infrastructure transactions rather than standard commercial property, developers and investors in sensitive locations or with connections to strategic assets should obtain early legal advice on NSI applicability.

The buy-to-let market has cooled for small-scale investors, but the structural shift — from individual landlords exiting to institutional landlords entering — creates opportunity for overseas capital at scale. Section 21 'no fault' evictions will be abolished under the Renters Reform Act (timing still uncertain but directionally inevitable). This increases tenancy security and aligns the UK more closely with European norms, which institutional investors from the continent find reassuring rather than threatening.

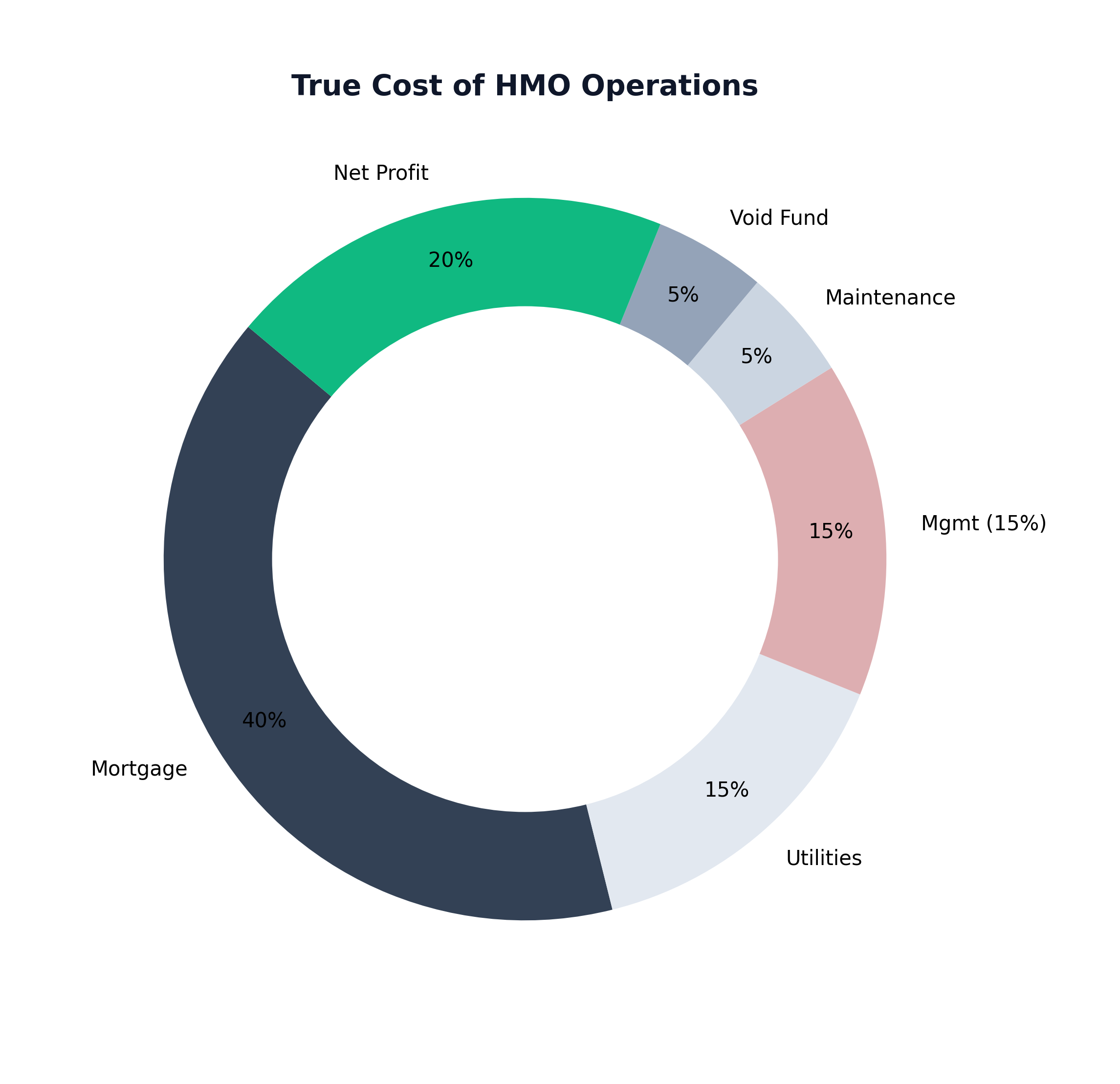

Figure: HMO Expense Breakdown

Figure: HMO Expense Breakdown

Strategies for Success: Building Your UK Team

Remote due diligence for overseas investors is manageable with the right local infrastructure. Essential team members: a specialist BTL or commercial property mortgage broker with non-resident experience; a conveyancing solicitor with foreign buyer expertise; a RICS-qualified surveyor for any physical asset; and a UK property manager where self-management is not practical. Combining these with a buying agent — particularly for off-market or new development opportunities — creates a professional chain that significantly reduces the risk of buying the wrong asset at the wrong price.

Stop being a landlord. Start being an investor.

Shaded Canvas introduces serious capital to vetted UK property opportunities — targeting 12–16% net returns.

Start Investing →