Edinburgh is not just a postcard city. It is a rental powerhouse.

For years, investors have flocked to Manchester and Liverpool for yields, dismissing Edinburgh as "too expensive." They were wrong.

While entry prices are higher, Edinburgh offers a unique combination of stability, massive tenant demand, and—crucially—yields that rival the best in the UK.

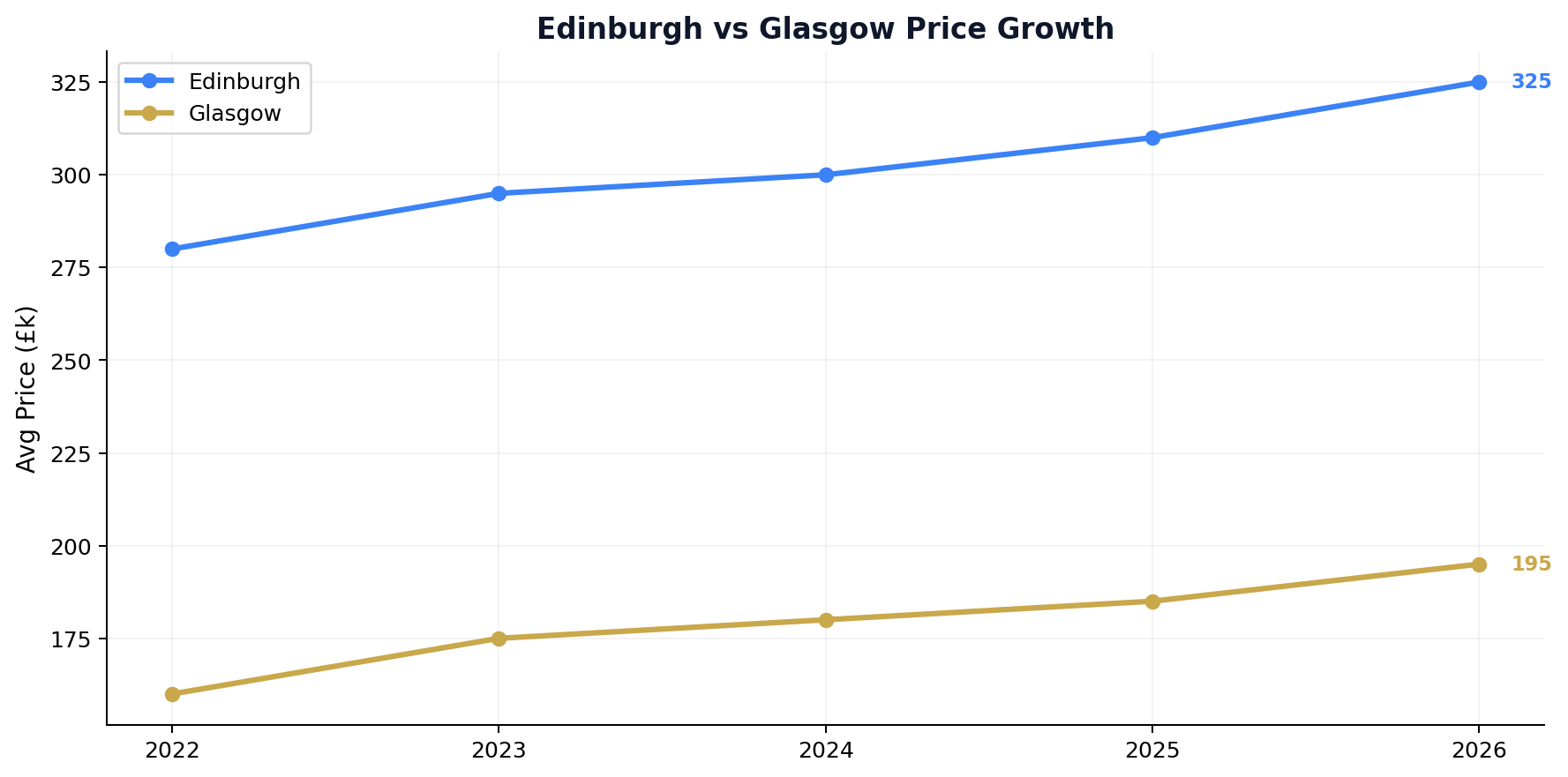

Rents in the capital have soared by 15.1% in the last year alone. House prices are up 5.7%. In a market where many UK cities are flatlining, Edinburgh is sprinting.

But investing here is not like buying in England. The legal system is different, the taxes are higher, and the competition is fierce. This guide will walk you through exactly how to invest in Edinburgh in 2026 without getting burned.

The "Need to Know": Scottish Property Law for Outsiders

Before you even look at a Rightmove listing, you need to understand three things. If you don't, you will waste months placing offers that never get accepted.

1. "Offers Over" vs Guide Price

In England, the asking price is a ceiling. In Scotland, it is a floor. Most properties are marketed as "Offers Over £200,000." This means the seller expects more. The Rule of Thumb: You typically need to bid 10-20% above the Home Report valuation to secure a popular property.

2. The Home Report

The good news: You don't need to pay for a survey. Every seller must provide a "Home Report" which includes a Single Survey, an Energy Report, and a Mortgage Valuation. This is the source of truth for the property's value.

3. The Cash Trap (Mortgages vs Valuation)

Banks will only lend against the Home Report valuation, not your purchase price.

- Example:

- Home Report Value: £200,000

- Purchase Price: £220,000 (Your winning bid)

- Mortgage (75% LTV): £150,000 (75% of £200k)

- Your Cash Need: £50,000 deposit + £20,000 "gap" cash = £70,000 total. Crucial Lesson: You need significantly more cash to buy in Edinburgh than in Manchester.

4. LBTT and the "ADS" Tax

Stamp Duty doesn't exist here. It's Land and Buildings Transaction Tax (LBTT). And if this is an investment property (a second home), you pay the Additional Dwelling Supplement (ADS). As of late 2024, this is 8%. On a £250,000 buy-to-let, that is an extra £20,000 in tax before you even pay LBTT. Factor this into your ROI calculations, or you will go broke.

Area Guide: Where the Yields Are

Forget the New Town (EH3) unless you are buying a trophy asset. The yields there are 3-4%. For investment returns, you need to look elsewhere.

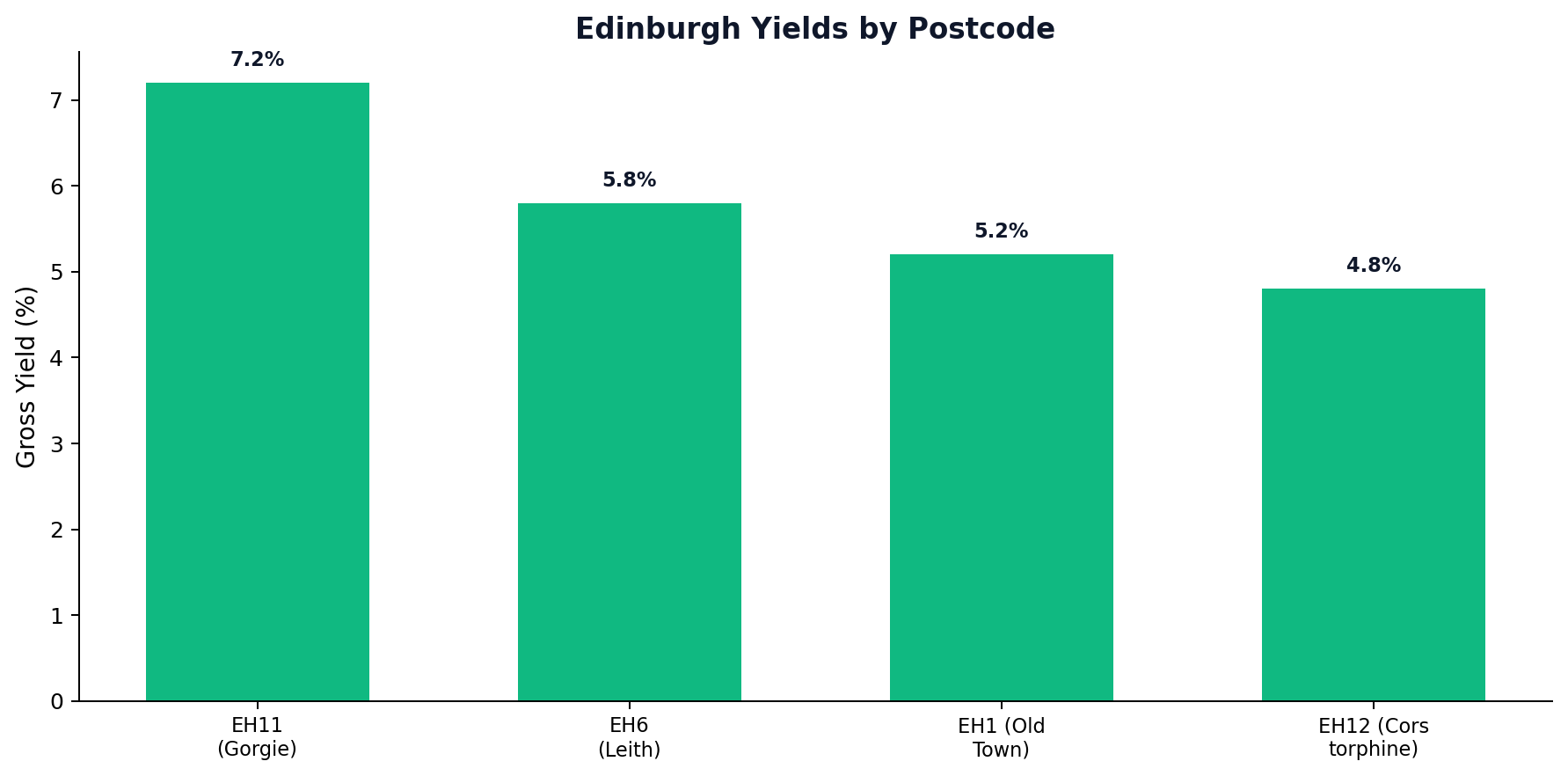

1. The Yield King: EH11 (Gorgie & Dalry)

- Profile: Working-class tenements, students, young professionals.

- Why here? It is walkable to Haymarket Station and the Financial District, but prices are still reasonable.

- Yields: 6-7% is standard.

- Strategy: Buy a 1-bed or 2-bed tenement flat. Renovate the kitchen/bathroom. Rent to young pros.

2. The Capital Growth Play: EH6 (Leith)

- Profile: The "Coolest Neighbourhood in the UK" (according to Time Out). Trendy bars, waterfront, historic docks.

- Why here? The Tram Extension (opened 2023) has revolutionized connectivity. You can be in the city centre in 10 minutes.

- Yields: 5-6%, but capital appreciation is higher than EH11.

- Strategy: 2-bed flats near The Shore or Leith Walk.

3. The Long Game: EH5 (Granton)

- Profile: Formerly industrial waterfront, now the site of massive regeneration (£1.3bn project).

- Why here? It's the "next Leith." Prices are lower, but the ceiling is high as the new marina and housing developments complete.

- Yields: 5.5% - 6.5%.

4. The Blue Chip: EH10 (Bruntsfield & Morningside)

- Profile: Affluent, leafy, school catchments.

- Why here? It is "safe." Values do not drop. Tenant demand is absolute (wealthy students, families).

- Yields: Low (4%), but this is a wealth preservation play.

The Student Market & The HMO Trap

Edinburgh has four universities and a massive student housing crisis. You might think, "I'll buy a 4-bed flat and rent to students!"

Stop.

Edinburgh Council has one of the strictest HMO licensing regimes in the world.

- HMO Cap Areas: In many parts of the city (Marchmont, Bruntsfield, Tollcross), there is a "zero growth" policy. You cannot get a new HMO license because the concentration of students is already too high.

- The Planning Trap: To turn a flat into an HMO, you often need planning permission and a license. They are separate hurdles.

The Strategy:

- Buy an existing HMO: You pay a premium, but the license is (usually) transferrable.

- Avoid HMOs: Stick to 1-bed and 2-bed flats for professionals. The yields are almost as good, and the regulation is far lighter.

Short-Term Lets (The Festival Factor)

Everyone knows about the Edinburgh Festival Fringe. For August, rents triple. You can make £3,000 - £5,000 in a single month.

But... The Scottish Government introduced Short-Term Let Licensing in 2023. It is now illegal to operate an Airbnb without a license. In tenement buildings (flats with shared stairs), getting a license is extremely difficult due to neighbour objections. Advice: Unless you are buying a main-door property or a detached house, assume you cannot run it as a short-term let.

Financial Example: The "Real Cost"

Let's look at a typical EH11 1-bed flat.

- Home Report Value: £180,000

- Purchase Price (Winning Bid): £200,000

- LBTT + ADS (Tax): £16,000 (approx)

- Legal + Misc: £2,000

Cash Required:

- 25% Deposit (on £180k): £45,000

- Gap Funding (Price - Value): £20,000

- Tax & Fees: £18,000

- Total Cash In: £83,000

Returns:

- Rent: £1,100/mo (£13,200/yr)

- Gross Yield: 6.6% on purchase price.

- Mortgage (5% on £135k): £6,750/yr

- Net Cash Flow: £6,450/yr + Capital Growth.

Figure: Edinburgh Yields by Postcode

Figure: Edinburgh Yields by Postcode

Figure: Edinburgh vs Glasgow Price Growth

Figure: Edinburgh vs Glasgow Price Growth

Conclusion: Is Edinburgh Worth It?

If you have the cash, yes.

Edinburgh is a "Tier 1" investment location. It offers the stability of London with the yields of a northern city. The tenant demographic is highly educated, reliable, and affluent.

However, the barrier to entry is high. You cannot buy here with a 5% deposit and a dream. You need significant capital to cover the "Offers Over" gap and the ADS tax.

The Golden Rule: target EH11 for your first deal. It offers the perfect balance of yield, affordability, and tenant demand.

Stop being a landlord. Start being an investor.

Shaded Canvas introduces serious capital to vetted UK property opportunities — targeting 12–16% net returns.

Start Investing →