title: "Buying First Investment Property UK: The Complete 2026 Guide" slug: "buying-first-investment-property-uk" description: "Everything you need to know about buying your first investment property in the UK in 2026. Data on yields, regions, taxes, and the new Renters' Rights Act."

Taking the plunge and buying your first investment property in the UK is one of the most significant financial decisions you can make. With the economic landscape settling after the turbulence of recent years, 2026 is emerging as a highly strategic entry point for new investors. Interest rates have stabilized, tenant demand remains structurally high, and long-term capital growth forecasts are strong.

However, the rules of the game have changed. Between the sweeping reforms of the Renters' Rights Act coming into full force, the implementation of Making Tax Digital, and shifting tenant expectations toward sustainable and smart homes, the "old way" of investing no longer works.

This definitive, data-driven guide is designed specifically for those buying their first investment property in the UK in 2026. We will walk you through exact regional hotspots, financing strategies, tax structuring, and compliance to ensure your first venture is both profitable and secure.

The UK Property Investment Landscape in 2026

Before deploying your capital, you must understand the macroeconomic factors shaping the housing market this year. 2026 sits in a transitional "sweet spot"—a period of moderated price growth before the next major upward cycle begins.

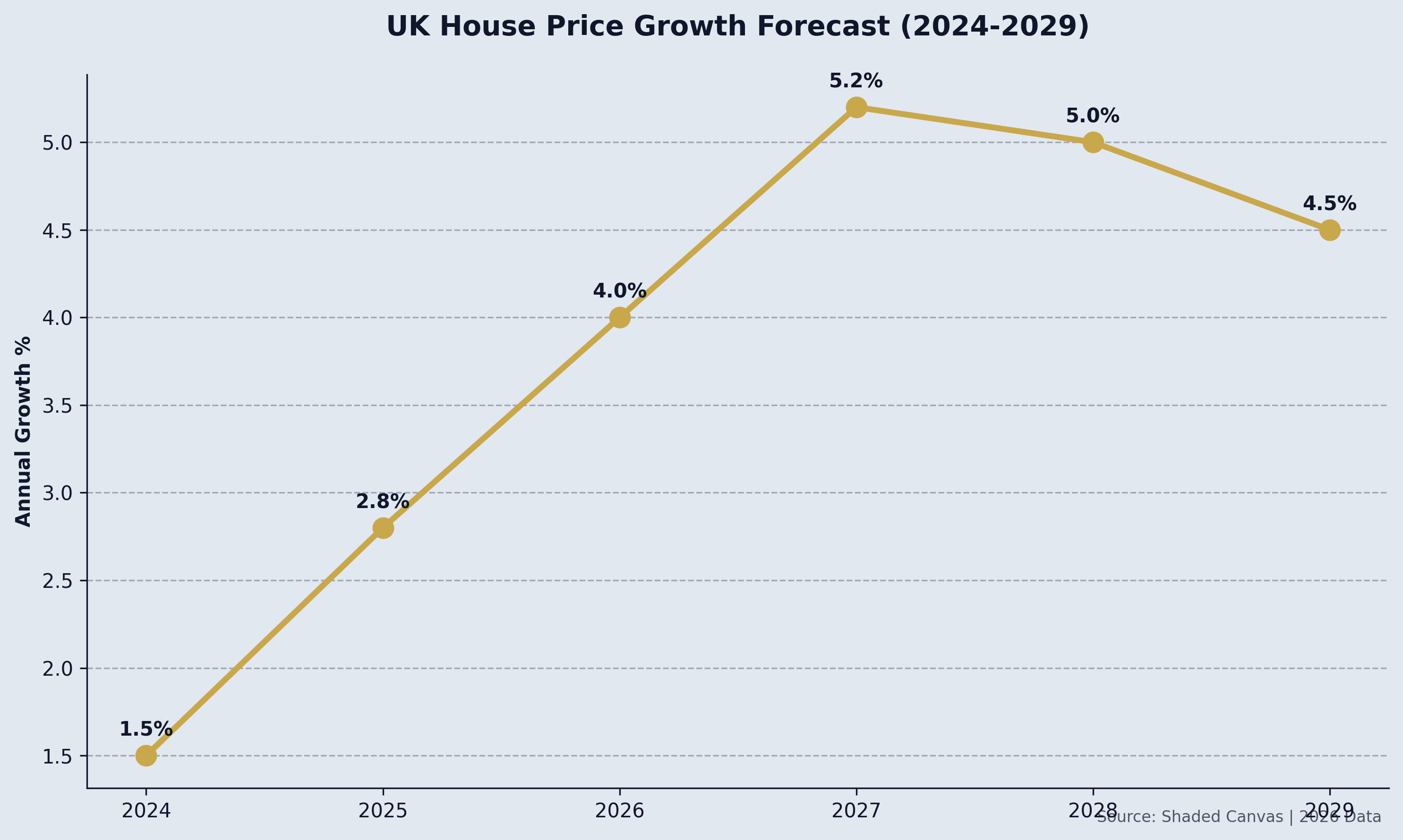

Capital Growth Forecasts (2026–2029)

According to leading analysts at Savills and Knight Frank, 2026 will see steady, moderate house price growth—projected between 3.0% and 4.5% nationally. The lingering effects of higher base rates mean we aren't seeing the rampant double-digit growth of the early 2020s. However, this is excellent news for first-time buyers, as it presents a window of better affordability and less aggressive bidding wars.

The true incentive lies in the mid-term forecast: UK house prices are projected to rise by 24.5% cumulatively over the five years to 2029. Securing an asset now means capturing the bulk of this impending growth cycle.

The Rental Market and Yields

The fundamental driver of buy-to-let returns in 2026 is the sheer imbalance between supply and demand. Renters are staying in properties longer due to the affordability hurdles of buying their own homes, while the supply of new rental stock has been constricting due to some older, less professional landlords exiting the market.

For a new investor, this means zero vacancy rates and robust rental income. Zoopla expects rents for new lets to rise by a further 2.5% across 2026, pushing the national average gross rental yield to around 5.5%. However, as we will explore below, smart regional selection can secure yields of 8%, 9%, or even higher.

Step 1: Choosing Your Strategy and Location

When buying your first investment property in the UK, your location dictates your return profile. The classic debate is Capital Growth vs. Rental Yield. As a first-time investor, achieving a blend of both (or heavily leaning toward high yield to maintain cash flow) is generally the safest approach.

The North-South Divide

In 2026, the data points overwhelmingly toward Northern England and Scotland as the premier destinations for property investment. London and the South East offer stability and potential long-term prestige, but the entry prices are prohibitive for most first-time investors, and the rental yields rarely exceed 4%.

Conversely, cities in the North offer lower entry points (often £120,000 - £200,000) and exceptional rental returns.

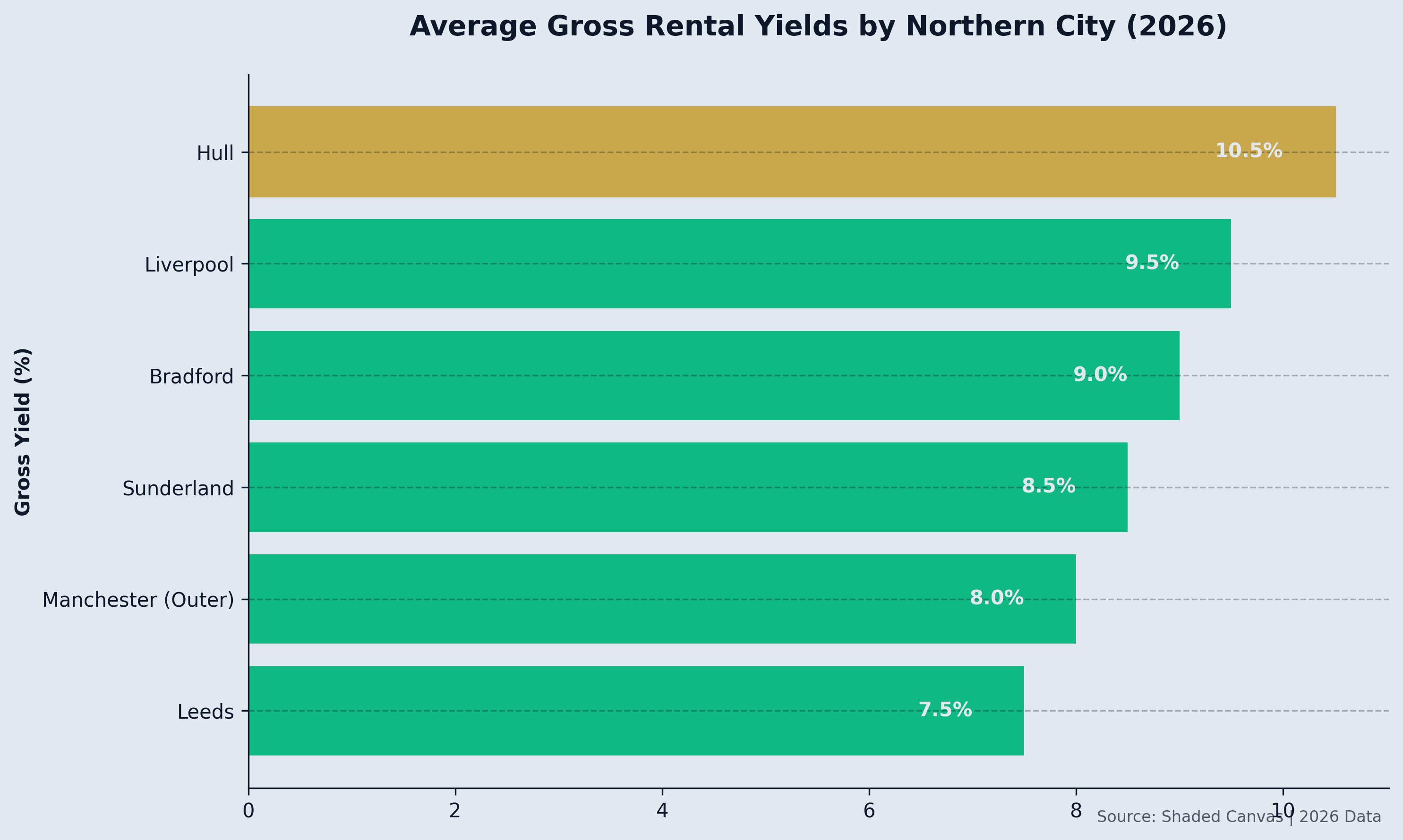

Top Hotspots for Your First Investment Property (2026 Data)

If you are looking for the best places to invest this year, these cities should be at the top of your due diligence list:

1. Manchester and Salford

Manchester remains the powerhouse of the Northern Powerhouse. Driven by massive corporate relocation, a booming tech sector, and high graduate retention, outer zones and Salford are generating healthy yields of 7.0% to 8.5%. The capital growth potential remains superior to most of the UK.

2. Liverpool

Famous for some of the highest yields in the country, specific postcodes in Liverpool (like L7, Kensington, and the Baltic Triangle) can achieve gross yields of 8% to 10%. Prices are highly accessible for first-time buyers, though thorough neighborhood research is essential.

3. Leeds and Bradford

Leeds boasts a massive student population and a thriving financial sector. Areas like Hyde Park (LS3) offer solid returns. Neighboring Bradford represents excellent deep-value investing, with yields frequently hitting 8% to 9.5% due to very low capital entry points.

4. Hull and Sunderland

For investors optimizing purely for cash flow and high yield over aggressive capital appreciation, coastal and industrial regeneration towns like Hull and Sunderland are currently charting yields between 8% and 11%.

5. Glasgow and Aberdeen

In Scotland, Glasgow’s Southside (e.g., Govanhill) and Aberdeen's recovering market (e.g., Rosemount) are catching the eye of yield-hungry investors, often delivering 7% to 9% returns on relatively low capital outlays.

Step 2: Financing Your First Investment

Securing finance for a buy-to-let (BTL) property is fundamentally different from securing a standard residential mortgage.

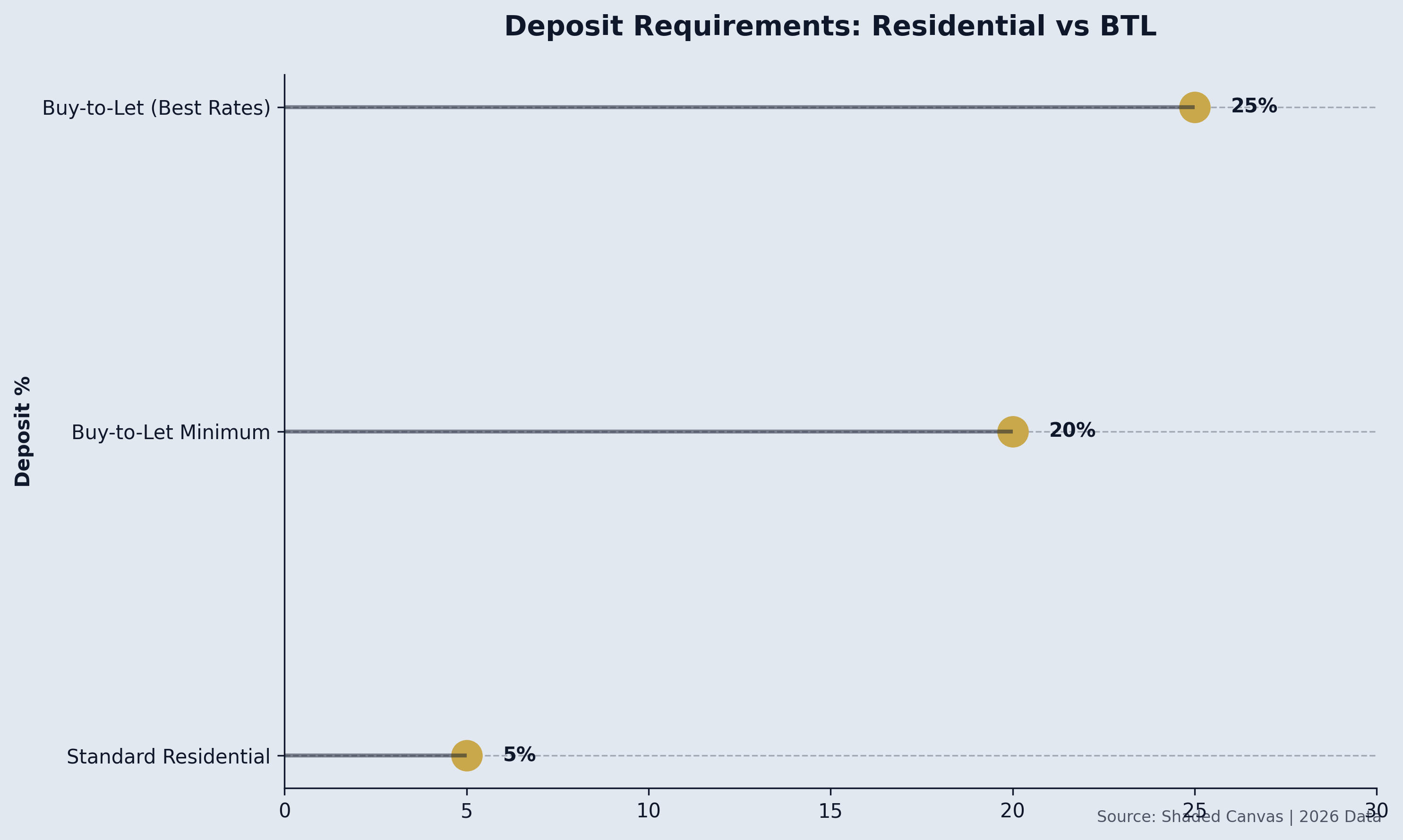

The Deposit Requirement

Unlike residential mortgages where 5% or 10% deposits are common, buying an investment property in the UK typically requires a minimum deposit of 25% of the property's value. Some lenders offer 20% products, but they usually come with significantly higher interest rates.

If you are buying a £150,000 property in the North, you will need £37,500 in cash, plus an additional £5,000 to £8,000 to cover stamp duty, legal fees, and potential minor refurbishments.

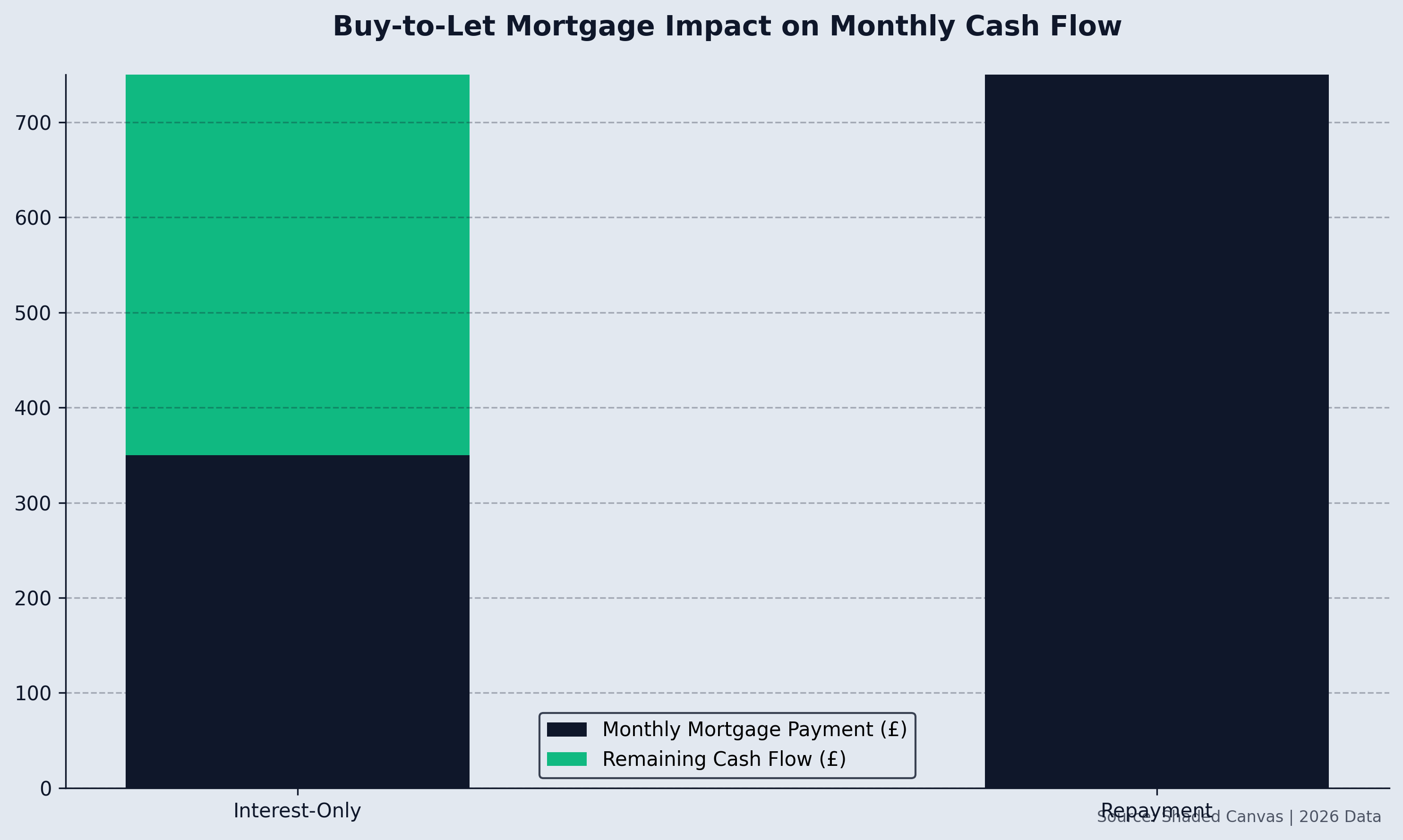

Interest-Only vs. Repayment Mortgages

Most experienced investors and nearly all first-time BTL buyers opt for Interest-Only mortgages. Why? Because it maximizes monthly cash flow. You only pay the interest on the loan, keeping your monthly outgoings low and allowing you to pocket the remaining rental income as profit (or build a contingency fund).

The strategy relies on the property increasing in value over time (capital growth) to eventually pay off the principal, or refinancing the property in the future.

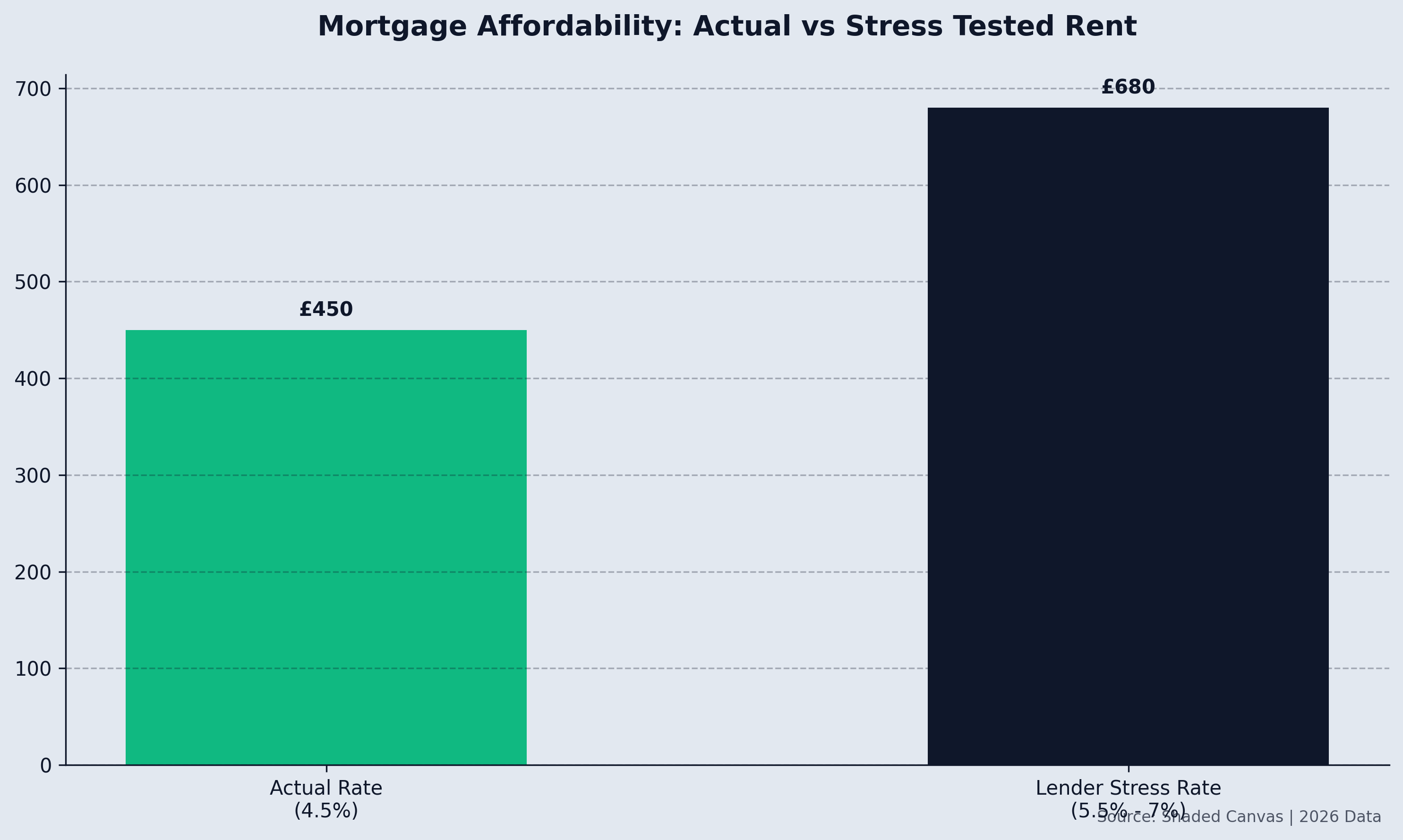

Stress Testing and Affordability

Lenders do not care much about your personal salary when approving a BTL mortgage (though a minimum income of £25,000 is often required). Instead, they care about the property's income.

Under PRA (Prudential Regulation Authority) rules, lenders will "stress test" your investment. The rental income typically needs to cover 125% to 145% of the mortgage payment, calculated at an artificial stress rate (often around 5.5% or higher), regardless of your actual mortgage rate. This ensures you won't default if base rates spike.

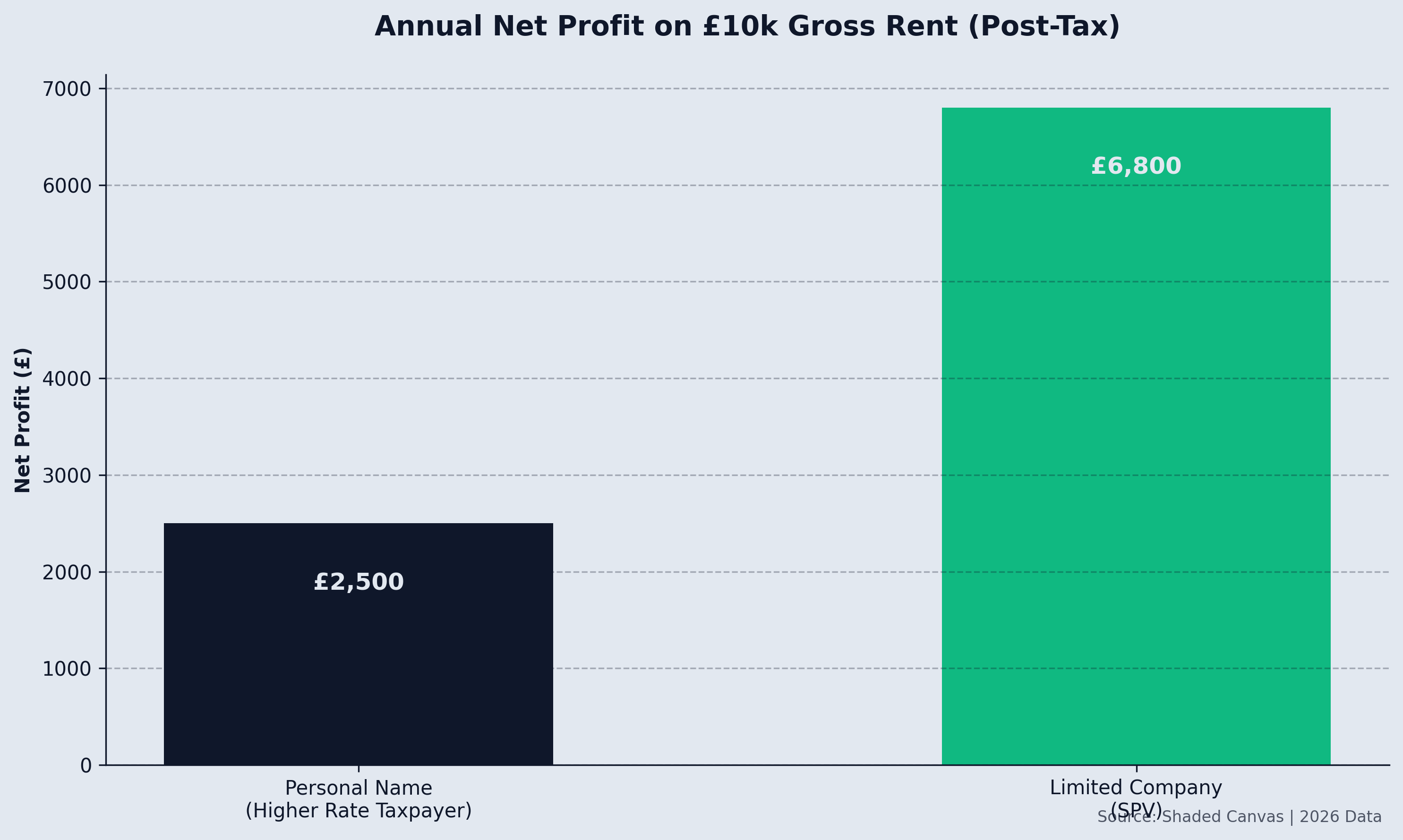

Step 3: Tax Structuring (Personal vs. Limited Company)

One of the biggest mistakes a first-time investor can make in 2026 is buying in their personal name without consulting an accountant. The tax landscape has fundamentally shifted.

The Impact of Section 24

Before 2017, you could deduct all your mortgage interest payments from your rental income before paying tax. The controversial "Section 24" tax changes removed this ability for personal landlords. Instead, you are taxed on your total rental revenue, and only given a basicrate tax credit (20%) for your mortgage interest.

For higher-rate (40%) and additional-rate (45%) taxpayers, this can be disastrous, sometimes resulting in a tax bill that wipes out your entire profit.

The Limited Company Solution (SPV)

Because of Section 24, the majority of new investment properties are now purchased through a Special Purpose Vehicle (SPV)—a Limited Company set up strictly for holding property.

The Benefits:

- Full Interest Deductibility: Limited companies are exempt from Section 24. You can deduct 100% of your mortgage interest as a business expense.

- Corporation Tax: You pay Corporation Tax (currently 19% to 25% depending on profit size) on your net profits, rather than personal income tax rates of 40% or 45%.

- Reinvesting Profits: If you plan to build a portfolio, leaving the money inside the company to buy the next property is highly tax-efficient.

The Drawbacks:

- Extraction Costs: If you want to spend the rental income personally, you have to pay dividend tax to extract it from the company.

- Higher Rates: Limited company BTL mortgages often have slightly higher interest rates and setup fees than personal mortgages.

- Admin: You will need to file company accounts, which incurs annual accountancy fees.

For most people buying their first investment property with the intention of growing a portfolio, the Limited Company route is the de facto standard in 2026.

Step 4: Navigating 2026 Regulations and Compliance

Being a landlord is operating a highly regulated business. The landscape in 2026 features sweeping legislative changes that you absolutely must understand before buying.

The Renters' Rights Act 2025 (Effective May 2026)

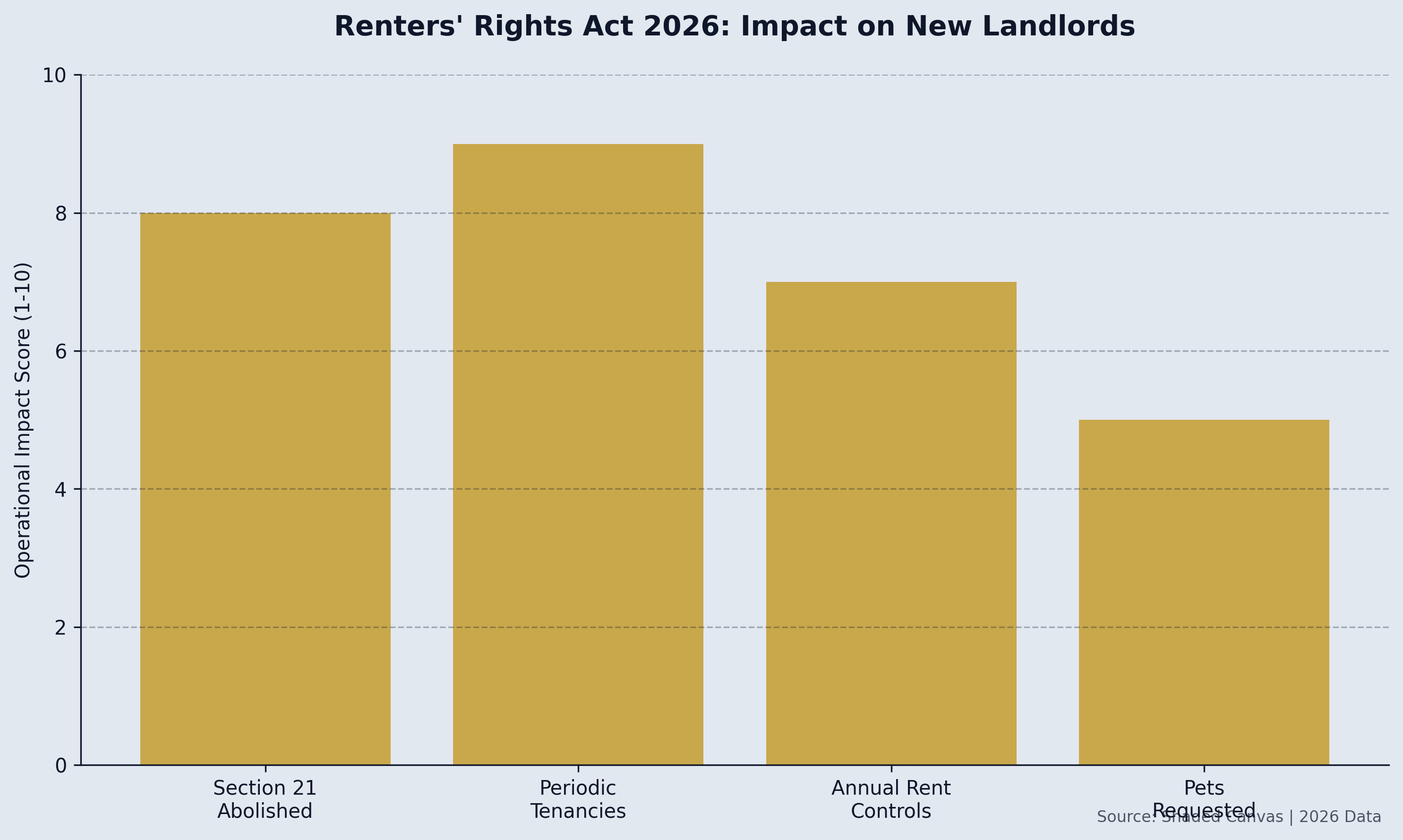

This legislation marks the biggest shake-up of the private rented sector in a generation. For all established and new tenancies from roughly May 2026 onwards, the following applies:

- Abolition of Section 21: The infamous "no-fault" evictions are gone. You can no longer ask a tenant to leave simply because their contract ended. To regain possession of your property, you must provide a legitimate reason defined under Section 8 (e.g., selling the property, moving in yourself, severe rent arrears, or anti-social behavior).

- Periodic Tenancies: Traditional 6- or 12-month fixed-term Assured Shorthold Tenancies (ASTs) are largely abolished. All tenancies will be rolling periodic tenancies. A tenant can give you two months' notice to leave at any time.

- Rent Controls (Increases): You can only increase the rent once per year. You must give two months' notice, and the increase must align with fair market rates. The tenant has the right to challenge unreasonable hikes at a tribunal.

- Pets in Let Properties: Tenants have a statutory right to request a pet, which landlords cannot unreasonably refuse (though you can require them to hold pet insurance).

While this sounds intimidating to a first-time investor, it simply emphasizes the need to buy quality property, vet tenants thoroughly, and use professional management.

Making Tax Digital (MTD)

From April 2026, HMRC is rolling out Making Tax Digital for Income Tax (MTD for ITSA). If your total property and/or self-employment income exceeds £50,000, you will no longer be able to submit a single annual tax return. You will be required to keep digital records using compliant software and submit quarterly updates to HMRC, plus a final declaration.

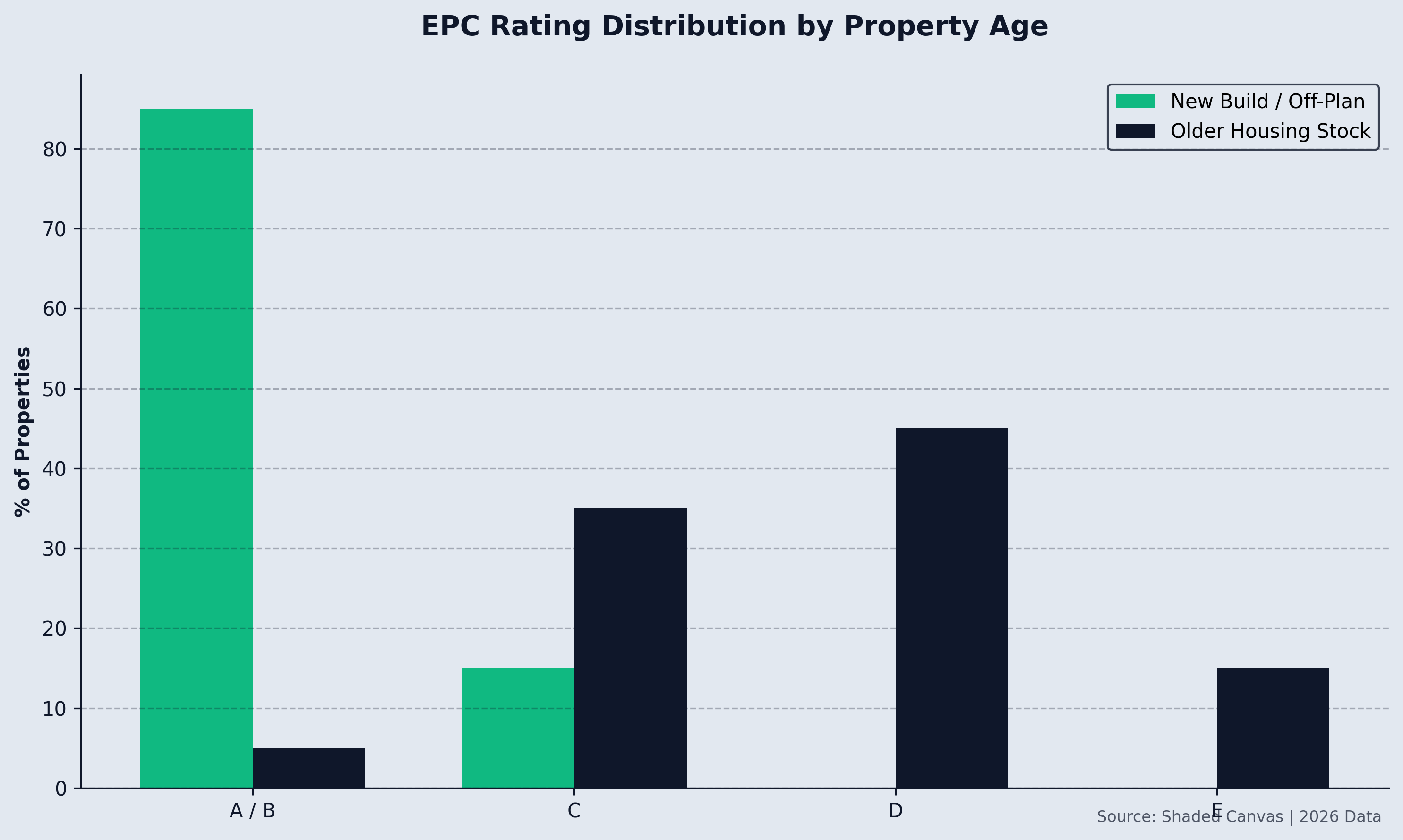

Energy Performance Certificates (EPC) and Sustainability

The push for green housing is accelerating. Not only are tenants demanding cheaper-to-run homes amidst high energy costs, but regulations are tightening. While previous strict deadlines for EPC 'C' ratings were delayed, the trajectory is clear.

When buying your first investment property, favor new-builds or recently renovated homes with high EPC ratings (A, B, or C). Avoid older, poorly insulated properties unless you have budgeted specifically for extensive energy retrofits, as these assets will become increasingly difficult to let and sell in the future.

Step 5: What Type of Property Should You Buy?

Your first investment property should ideally be "vanilla"—steady, reliable, and low-hassle. Leave complex high-risk strategies for your third or fourth property.

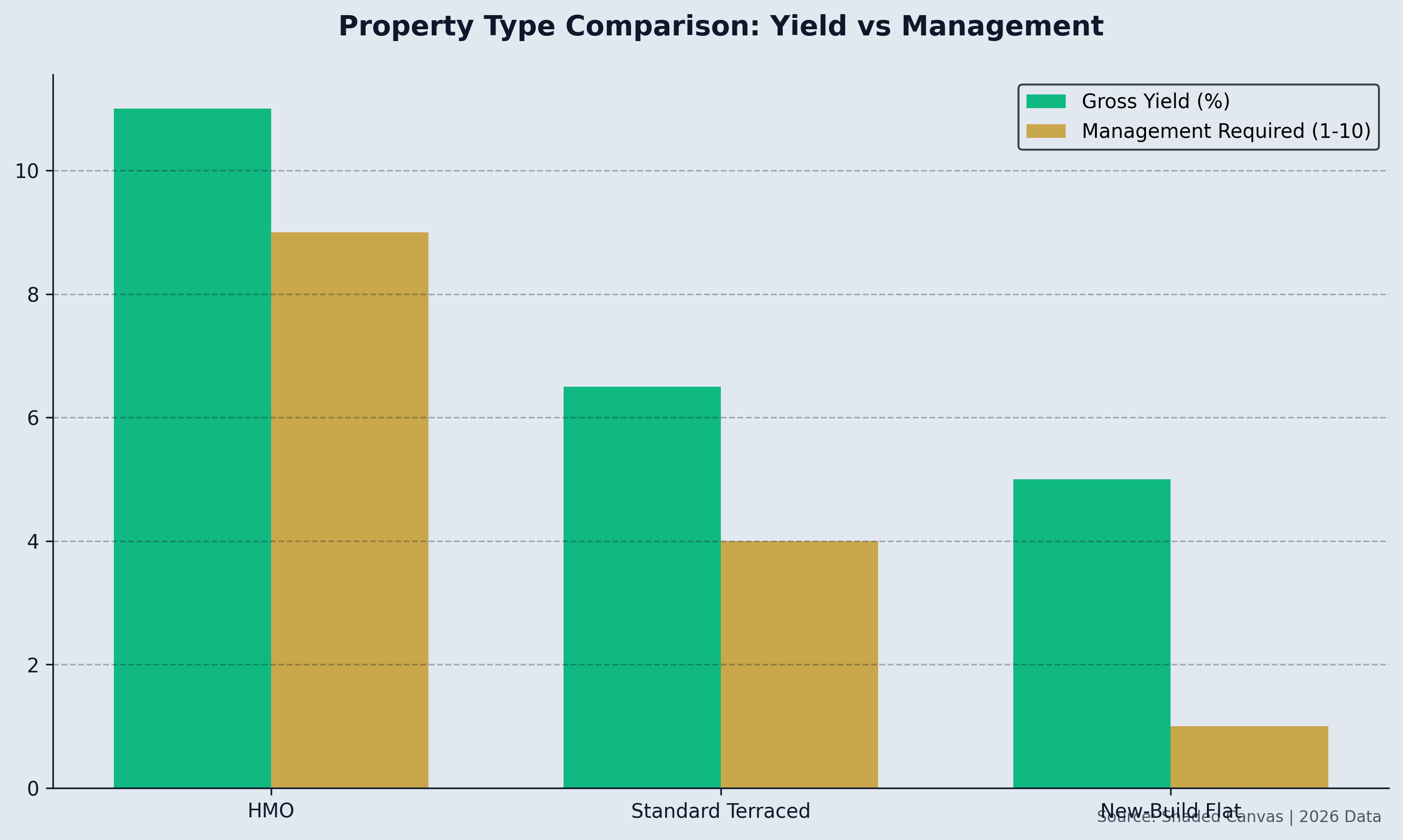

1. New-Build and <a href="https://blog.shadedcanvas.co.uk/post/off-plan-investment-property-uk" style="color:#c9a84c;text-decoration:underline;font-weight:500">Off-Plan Apartments

These are currently highly favored by first-time investors.

- Pros: Highly appealing to young professional tenants, compliant with strict modern energy standards (EPC), minimal maintenance layout, and you benefit from builder warranties (e.g., NHBC). Buying off-plan (before it is built) can also secure a discount and allow for capital growth before you even complete.

- Cons: Often carry a "new-build premium" on the purchase price, and you are subject to service charges and ground rents which eat into your yield.

2. Standard Terraced or Semi-Detached Houses

The backbone of the UK rental market, particularly in the North and Midlands.

- Pros: Excellent for attracting families and long-term tenants ensuring minimal void periods. You own the freehold, so there are no surprise service charges to worry about. Capital appreciation is historically very stable.

- Cons: You are responsible for all external maintenance (roofs, gutters, structural issues). They may require modernization to achieve top-tier rents.

3. HMOs (Houses in Multiple Occupation)

Renting out rooms individually to young professionals or students.

- Pros: Massive cash flow. An HMO can generate double or triple the gross yield of a single-let property.

- Cons: Extremely high-management, intense regulatory burdens (HMO licensing, strict fire safety laws), high tenant turnover, and greater wear and tear. Not recommended for a first-time investor unless you are purchasing a turnkey, fully-managed product.

Summary Checklist for Your First Investment

To recap, if you want to successfully navigate the UK property investment market in 2026, follow this blueprint:

- Target the North: Look to Manchester, Liverpool, Leeds, or Scotland for a blend of affordability and strong 6-9% yields.

- Secure a 25% Deposit: Have your capital ready, along with a buffer for stamp duty and legal fees.

- Use a Broker: Find a specialist BTL mortgage broker to navigate strict stress-testing and secure the best interest-only rates.

- Consult an Accountant: Seriously consider setting up a Limited Company (SPV) to bypass the damaging effects of Section 24 tax rules.

- Buy 'Vanilla': Stick to high-quality new-build apartments or standard 2/3 bedroom houses for your first asset. Prioritize high EPC ratings.

- Use a Letting Agent: With the Renters' Rights Act in play, do not attempt to self-manage your first property. Pay the 10-12% fee to a professional agent to ensure strict legal compliance and tenant vetting.

Buying your first investment property in the UK is a journey of due diligence. By relying on current data and structuring your investment professionally from day one, you build a resilient foundation for long-term wealth generation.

Stop being a landlord. Start being an investor.

Shaded Canvas introduces serious capital to vetted UK property opportunities — targeting 12–16% net returns.

Start Investing →