London Property in 2026: A Market of Micro-Markets

London is not a single property market. It is 33 boroughs, each operating with its own supply-demand dynamics, pricing floor, yield profile, and growth trajectory. The investor who treats "London" as a monolithic opportunity — buying wherever they find a listing — will underperform the one who understands that a flat in Barking and a flat in Belgravia exist in fundamentally different financial ecosystems.

The data for 2026 tells a clear story: East and South London are delivering yields that rival Northern cities, while Central and West London continue to operate as capital preservation plays for international wealth. The Elizabeth Line has redrawn the yield map. Regeneration programmes are creating new micro-markets in real time. And the institutional build-to-rent sector is changing the competitive landscape for private landlords.

This analysis maps the current investment landscape across London's key areas, segmented by investment objective — whether that is maximum rental yield, long-term capital appreciation, or the increasingly valuable combination of both.

The High-Yield Zone: East London

East London has undergone the most dramatic investment transformation of any UK region over the past decade. Properties that sat unloved at the end of the District Line are now outperforming prime Central London postcodes on total returns. The catalyst is infrastructure — specifically, the Elizabeth Line — but the underlying fundamentals of population growth, employment diversification, and relative affordability are doing the heavy lifting.

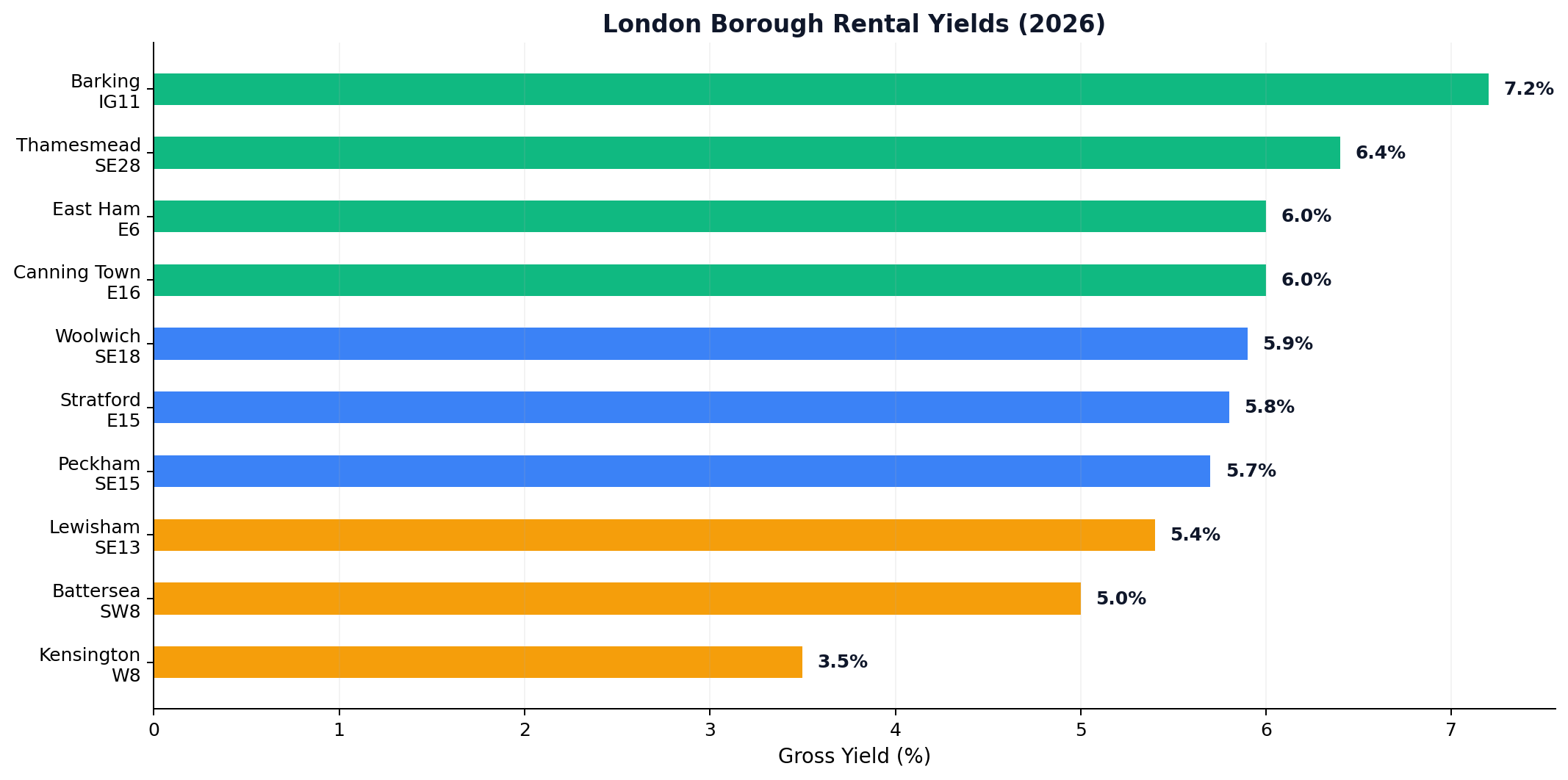

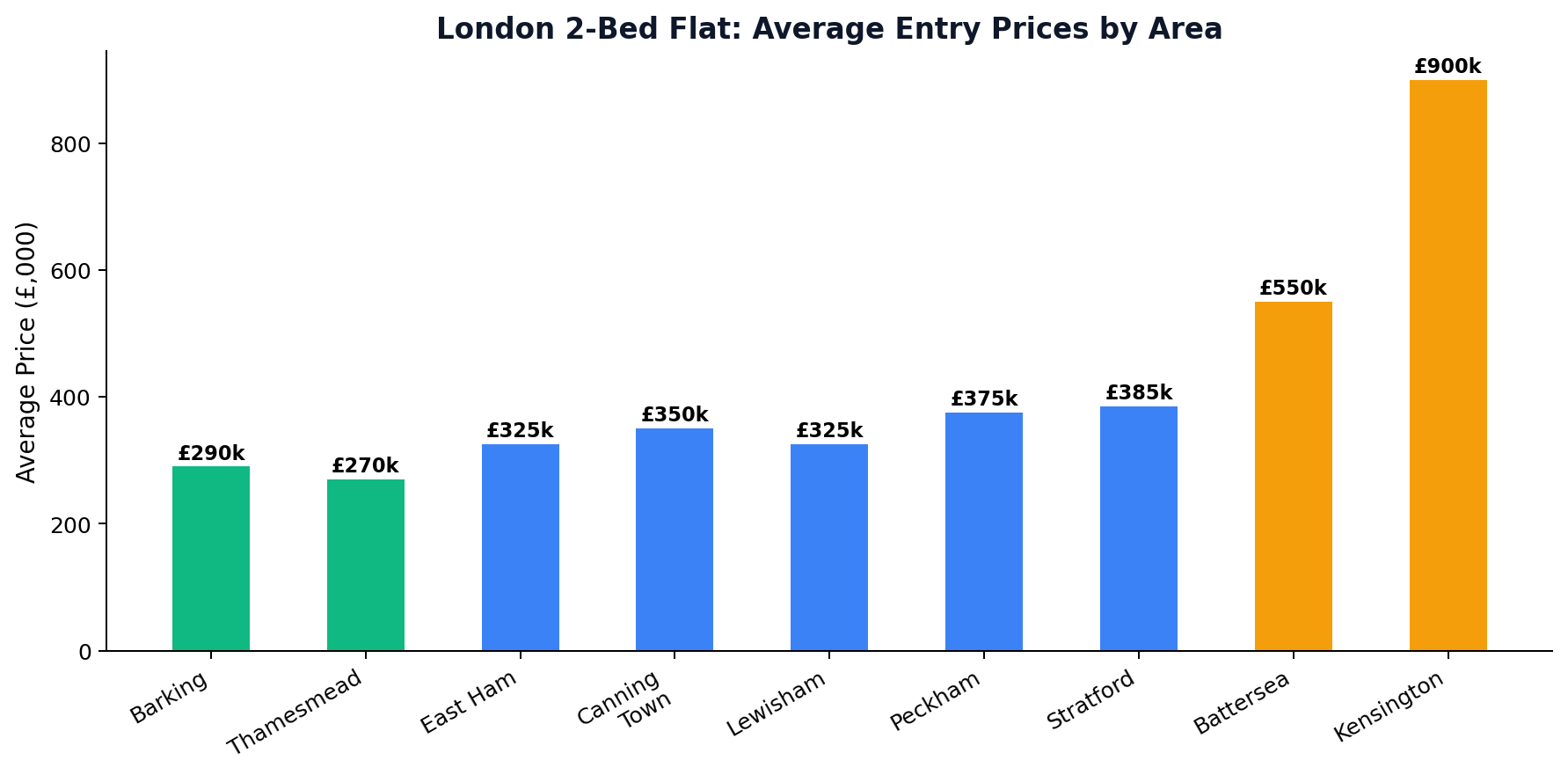

Barking (IG11) — 7.2% Gross Yield

Barking delivers the highest rental yield in London at approximately 7.2% gross. Average property prices sit around £280,000–£320,000 for a two-bed flat, with monthly rents achieving £1,500–£1,800. The area benefits from excellent transport links (District Line, Hammersmith & City, C2C to Fenchurch Street), a young and growing population, and a pipeline of new developments including the Barking Riverside project — 10,800 new homes with its own London Overground station.

The investor calculus: At a 7.2% gross yield and entry prices £200k below the London average, Barking offers the mathematical certainty that very few London postcodes can match. The risk is reputational — the area does not carry the cachet of inner London - and capital appreciation has been more modest than neighbouring Stratford. But for yield-focused investors, this is the number to beat.

East Ham (E6) — 6% Yield + 22% Five-Year Growth

East Ham is the balanced play — combining a solid 6% gross yield with 22% price growth over the past five years. This is rare in London. Most high-yield areas sacrifice growth, and most growth areas sacrifice yield. East Ham delivers both because it sits at the intersection of several growth drivers: Elizabeth Line connectivity, proximity to the Royal Docks enterprise zone, and a diverse local economy supporting consistent rental demand.

Average prices for two-bed flats: £300,000–£350,000. Monthly rents: £1,500–£1,700.

Stratford (E15/E20) — 5.8% Yield

Stratford has evolved from its Olympic legacy into London's most significant secondary commercial hub. The arrival of UCL's East campus, the expansion of Westfield, and the clustering of tech and creative industries in and around the Queen Elizabeth Olympic Park have created a deep, diversified tenant pool. Yields at 5.8% are respectable for Zone 3, and the long-term growth story remains compelling as the area continues to densify.

Average prices: £350,000–£420,000 for two-bed apartments. Monthly rents: £1,600–£1,900.

Canning Town and Custom House (E16) — 6% Yield

These neighbouring areas offer strong yields driven by DLR and Jubilee Line connectivity, proximity to the ExCeL London exhibition centre, and an ongoing wave of residential development. The Silvertown Tunnel (opening 2026) and the Royal Docks regeneration will further enhance the area's connectivity and economic activity.

Average prices: £320,000–£380,000. Monthly rents: £1,500–£1,750.

The Growth Zone: Regeneration Areas

For investors prioritising capital appreciation over immediate yield, London's regeneration zones offer the potential for outsized returns — but only if you enter early enough in the cycle. Buying into a regeneration area after the media hype has peaked is a reliable way to overpay.

Thamesmead (SE28) — 6.4% Yield + Regeneration Upside

Thamesmead is London's most ambitious long-term regeneration bet. Peabody Housing Association's masterplan calls for 11,500 new homes and the transformation of the area's infrastructure over 30 years. Current entry prices are among London's lowest — two-bed flats from £250,000–£290,000 — with yields of 6.4% providing solid income while you wait for the regeneration premium to be priced in.

The risk is timeline. Thamesmead's transformation will take decades, not years. If you need capital appreciation within 3–5 years, this is the wrong location. If you can hold for 10+, the risk-reward ratio is exceptional.

Woolwich (SE18) — 5.9% Yield

The Elizabeth Line station at Woolwich has already catalysed significant development, including Berkeley Group's Royal Arsenal Riverside project (5,000+ homes) and the ongoing Woolwich Exchange redevelopment. Yields of 5.9% combined with improving infrastructure (DLR extension, Elizabeth Line, and the proposed Woolwich-to-Silvertown public transport link) make this a strong mid-term growth play.

Battersea and Nine Elms (SW8/SW11) — 4.5–5.6% Yield

The Northern Line Extension (opened September 2021) and the Battersea Power Station redevelopment have transformed this stretch of the South Bank. The area now hosts the US Embassy, Apple's UK headquarters (at Battersea Power Station), and a cluster of high-specification residential towers.

Yields are moderate at 4.5–5.6%, but the area targets premium tenants — international professionals, corporate relocations, and diplomatic staff — who provide reliable income streams and lower void risk. Entry prices are high (£450,000–£650,000 for one-to-two bed apartments), making this a play for capital-rich investors.

King's Cross and Islington — Capital Growth Play

The King's Cross regeneration — £2.3 billion invested over 20 years — is now substantially complete, making it a case study rather than a live opportunity. Property values have already reflected the regeneration premium. However, the surrounding areas of Caledonian Road, Holloway, and lower Islington still offer relative value, with yields of 4.5–5.5% and strong fundamentals driven by proximity to four major railway stations and the growing tech/media cluster anchored by Google's UK headquarters.

The Capital Preservation Zone: Prime Central London

Prime Central London — Mayfair, Belgravia, Knightsbridge, Kensington, Chelsea — operates on different economic logic. Yields are 3–4% at best, and operational costs (service charges, management fees, regulatory compliance) are significantly higher than outer London.

The investment case for PCL rests on three pillars:

- Scarcity premium. The stock of prime Central London property is finite and cannot be replicated. Planning restrictions, conservation areas, and the sheer density of the built environment limit new supply.

- Global demand. PCL competes with Manhattan, Hong Kong, Singapore, and Dubai for international capital. Geopolitical instability in other markets periodically drives inflows to London.

- Currency diversification. Sterling-denominated assets offer a hedging benefit for investors holding USD, EUR, or Middle Eastern currencies.

The reality check: PCL values have been largely flat in real terms since 2014, underperforming the UK average. The post-Brexit SDLT surcharge, the non-dom tax reforms (effective April 2026), and the overseas buyer surcharge have all reduced demand at the ultra-prime end. PCL is a wealth preservation strategy, not a growth strategy.

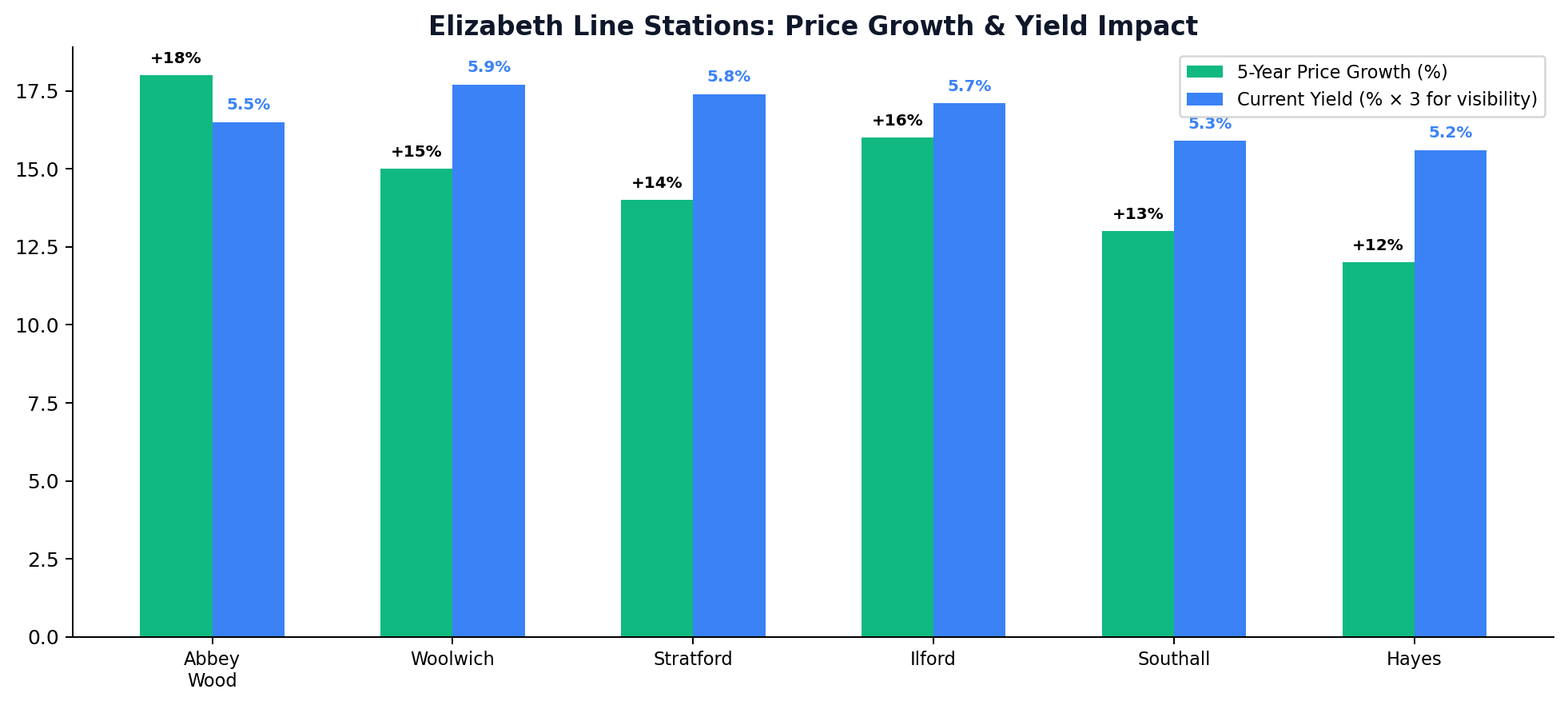

The Elizabeth Line Effect: Quantifying the Impact

The Elizabeth Line (Crossrail) is the single most significant driver of London property values in the current cycle. Research from Knight Frank and the GLA shows that properties within 1km of an Elizabeth Line station have outperformed the London average by 10–20% since the line's opening in May 2022.

Key stations and price impact:

| Station | Borough | 5-Year Price Growth | Current Avg. Yield |

|---|---|---|---|

| Abbey Wood | Greenwich | 18% | 5.5% |

| Woolwich | Greenwich | 15% | 5.9% |

| Stratford | Newham | 14% | 5.8% |

| Ilford | Redbridge | 16% | 5.7% |

| Southall | Ealing | 13% | 5.3% |

| Hayes & Harlington | Hillingdon | 12% | 5.2% |

The lesson is clear: transport infrastructure drives property values. For investors looking ahead, the proposed Crossrail 2 (Wimbledon to Tottenham Hale via Central London) and the Bakerloo Line Extension (to Lewisham) represent the next wave of infrastructure-led growth — if and when they receive government approval.

The Emerging Opportunity: South London

South London has historically been undervalued relative to equivalent North London postcodes — a legacy of poorer transport links and more limited regeneration investment. This is changing rapidly.

Lewisham (SE13) — 5.4% Yield

The proposed Bakerloo Line Extension to Lewisham would transform its connectivity, adding a second Tube line to complement the existing DLR and National Rail services. Even without the extension, Lewisham's proximity to Canary Wharf (10 minutes by DLR) and its relative affordability (two-bed flats from £300,000–£350,000) are driving steady demand.

Peckham (SE15) — 5.7% Yield

Peckham has evolved from edgy to established over the past decade, with a thriving independent food, art, and retail scene driving demand from young professionals. Yields of 5.7% and entry prices around £350,000–£400,000 for two-bed flats reflect a market that still offers value relative to neighbouring Camberwell and Dulwich.

Catford (SE6) — 5.5% Yield

The Catford Town Centre regeneration — a £3 billion masterplan including 2,300 new homes, a new town centre, and improved public realm — positions this area as one of South London's most significant growth opportunities. Current prices (two-bed flats from £280,000–£330,000) are well below the London average, with yields at 5.5%.

Sector Watch: Build-to-Rent and Its Impact on Private Landlords

The institutional build-to-rent (BTR) sector is growing rapidly in London, with over £5 billion invested in purpose-built rental developments in 2024 alone. Major operators include Legal & General, Greystar, Quintain, and Grainger.

For private landlords, BTR creates both a challenge and an opportunity:

- Challenge: BTR developments offer professional management, on-site amenities (gyms, co-working, concierge), and flexible lease terms that private landlords cannot easily match. In areas with significant BTR supply, private landlords face downward pressure on rents.

- Opportunity: BTR is concentrated in specific developments and locations. Private landlords who own in adjacent areas can benefit from the increased tenant awareness and demand that BTR marketing generates, without competing directly on amenities.

The Tax Position for London Investors

London's higher property values amplify the impact of every tax change. Key considerations for 2026:

- SDLT on additional properties: The 5% surcharge (increased from 3% in October 2024) means a £400,000 London investment property now incurs £27,500 in SDLT — a significant upfront cost that must be factored into your yield calculations.

- Non-resident surcharge: An additional 2% for overseas buyers, bringing the total additional property SDLT on a £400,000 purchase to £35,500.

- Section 24: Hits London investors hardest because higher property values mean larger mortgages and therefore larger non-deductible interest payments. A limited company structure is almost mandatory for leveraged London portfolios.

- Capital Gains Tax: CGT rates for residential property are 18% (basic rate) or 24% (higher rate) — lower than the previous 28% rate following the October 2024 Budget changes.

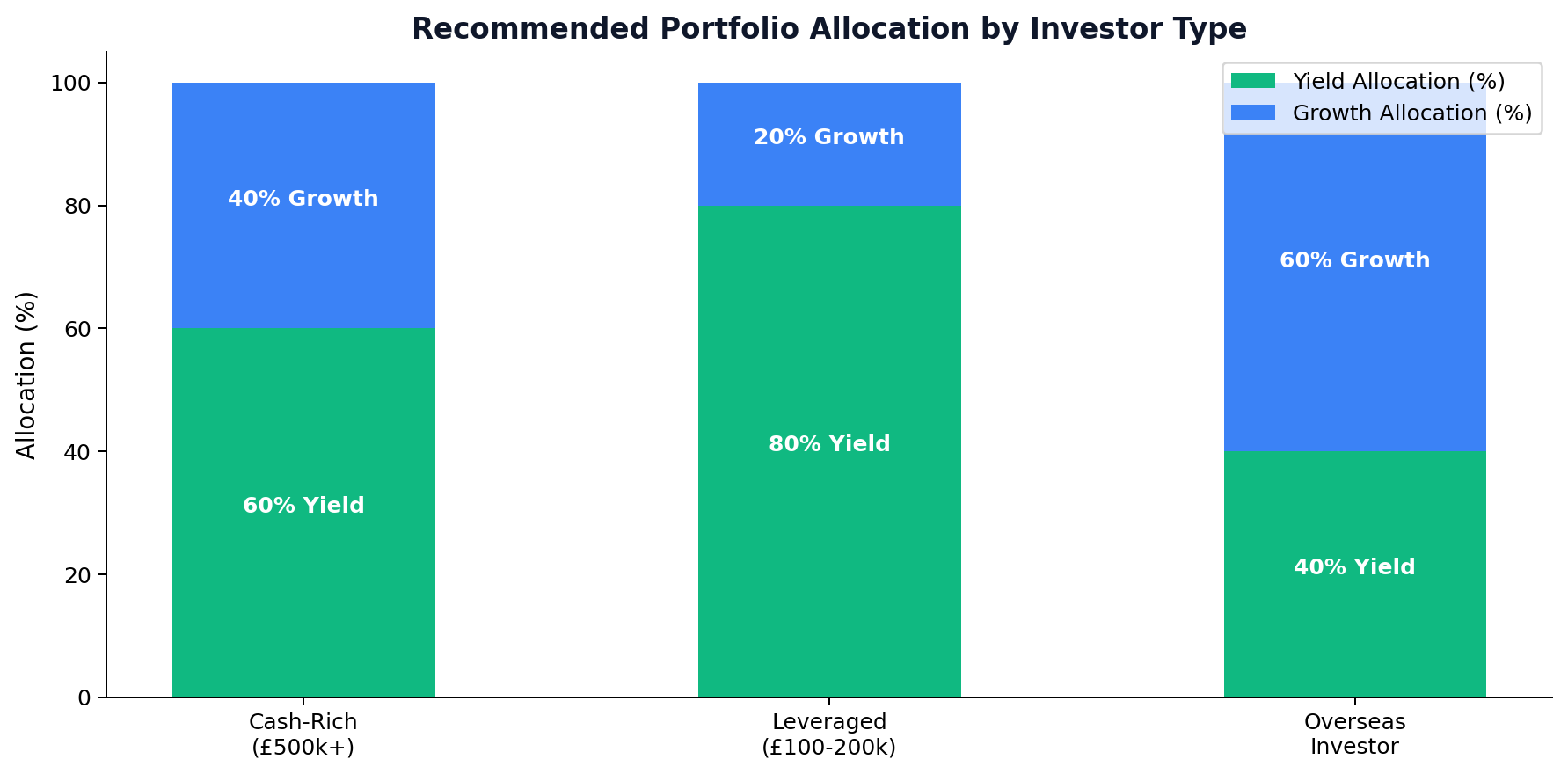

Investment Strategy: Matching Your Capital to the Right London Market

Cash-Rich Investor (£500k+)

Target: Prime/Super-Prime PCL for capital preservation, or a diversified portfolio of 2–3 East London flats for yield.

PCL allocation (40%): One-bed in Kensington or Chelsea — £400–500k, 3.5% yield, minimal management. Yield allocation (60%): Two-to-three flats in Barking/East Ham/Canning Town — £280–350k each, 6–7% yield, generating meaningful monthly cash flow.

Leveraged Investor (£100–200k deposit)

Target: One-to-two properties in East or South London where yields exceed mortgage costs.

Priority postcodes: IG11 (Barking), SE28 (Thamesmead), E6 (East Ham), SE13 (Lewisham). Strategy: Buy, let, refinance after 2–3 years of growth, deploy released equity into next purchase. Critical: Must achieve 6%+ gross yield to cover 5.5% mortgage rate and operating costs.

Overseas Investor

Target: New-build in a managed development with on-site property management.

London remains attractive for overseas investors despite the SDLT surcharges, due to the rule of law, transparent legal system, and liquidity of the market. The currency play also matters — a weakening pound increases purchasing power for USD, EUR, and AED-denominated capital.

Conclusion: The London Paradox

London property is simultaneously the most expensive and the most resilient market in the UK. It punishes lazy investors with below-inflation yields and rewards strategic ones with compounding capital growth that no other UK market can match over 20-year horizons.

The data is clear: the east of the city is where the numbers work right now. The Elizabeth Line has created a new yield corridor from Barking to Stratford that delivers income while you wait for the capital growth. South London's emerging areas — Lewisham, Catford, Peckham — offer the next wave of regeneration-driven appreciation.

But the core principle remains unchanged: London rewards patience. The investors who bought in Canary Wharf in 1998, in Stratford in 2008, or in Battersea in 2015 understood that London's growth story plays out over decades, not quarters.

Next Steps:

- Map your target postcodes and verify current rental levels on Rightmove and OpenRent.

- Model your purchase with the 5% additional property SDLT surcharge and current mortgage rates to confirm the yield works.

- If buying from overseas, engage a UK solicitor familiar with the enhanced due diligence requirements and factor in the 2% non-resident surcharge.

📚 Related Reading

- Best Capital Growth Property UK: Where Property Prices Are Actually Heading in 2026 and Beyond

- Passive Income Property UK: How to Build a Rental Portfolio That Actually Pays You in 2026

- Property Investments Manchester: The Definitive Investor's Guide to the UK's Most Dynamic City in 2026

- Buy dirt

- Hobbies That Make Money: Real "Cheat Codes" for Turning Your Passion Into Profit

Stop being a landlord. Start being an investor.

Shaded Canvas introduces serious capital to vetted UK property opportunities — targeting 12–16% net returns.

Start Investing →