The term "Property Investment Advisor" is dangerous.

In the UK, anyone can print a business card and call themselves a Property Advisor. Unlike "Financial Advisor," which is a regulated title (protected by the FCA), "Property Advisor" has no legal definition.

This means you could be taking life-changing financial advice from a regulated expert—or from a failed estate agent working on commission.

This guide explains exactly who you should listen to, who you should pay, and who you should ignore.

1. The 3 Types of "Advisor"

Before you hire anyone, you need to know which of these three buckets they fall into.

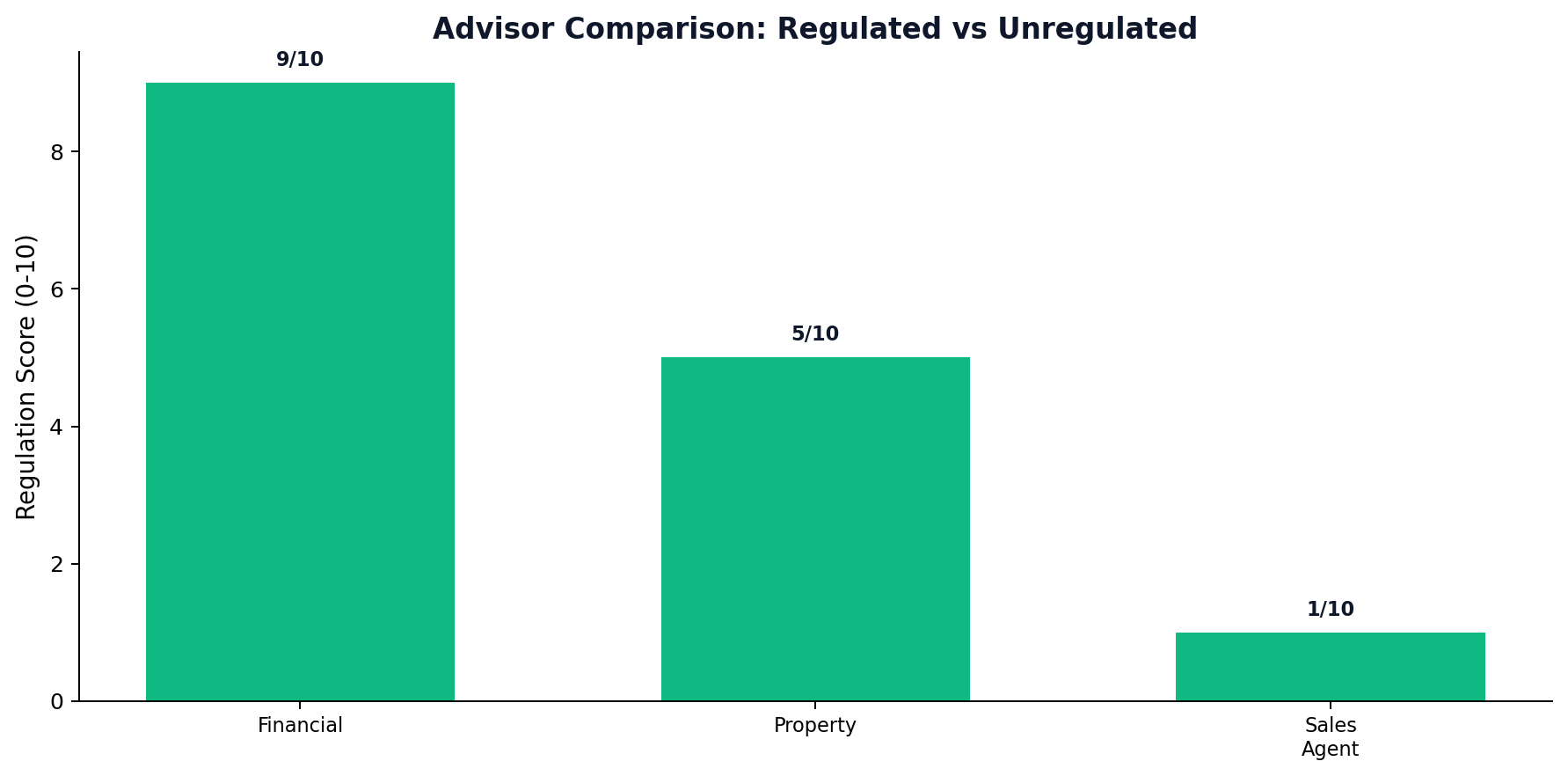

Type 1: The FCA-Regulated Financial Advisor

- What they do: Advise on regulated financial products (Pensions, ISAs, Unit Trusts, REITs).

- Regulation: Highly regulated. If they give bad advice, you can complain to the Financial Ombudsman.

- Property Role: They can help you invest in a Property Fund or put commercial property into a SIPP (Self-Invested Personal Pension). They cannot advise you on which specific house to buy.

Type 2: The Independent Property Advisor (Unregulated)

- What they do: Advise on property strategy, location, yield, and sourcing specific deals.

- Regulation: None. (They should belong to a Redress Scheme like PRS/TPO, but that’s it).

- Property Role: They act as a consultant. They charge a fee to build your portfolio.

- Risk: High. You are relying entirely on their personal expertise and integrity.

Type 3: The "Free" Advisor (The Salesperson)

- What they do: Sell off-plan apartments for developers.

- Regulation: None.

- Property Role: They are not advisors; they are sales agents. Their "advice" will always be: "Buy this specific flat in this specific building."

- Risk: Extreme. Their commission (often £10k-£20k) is built into the price you pay.

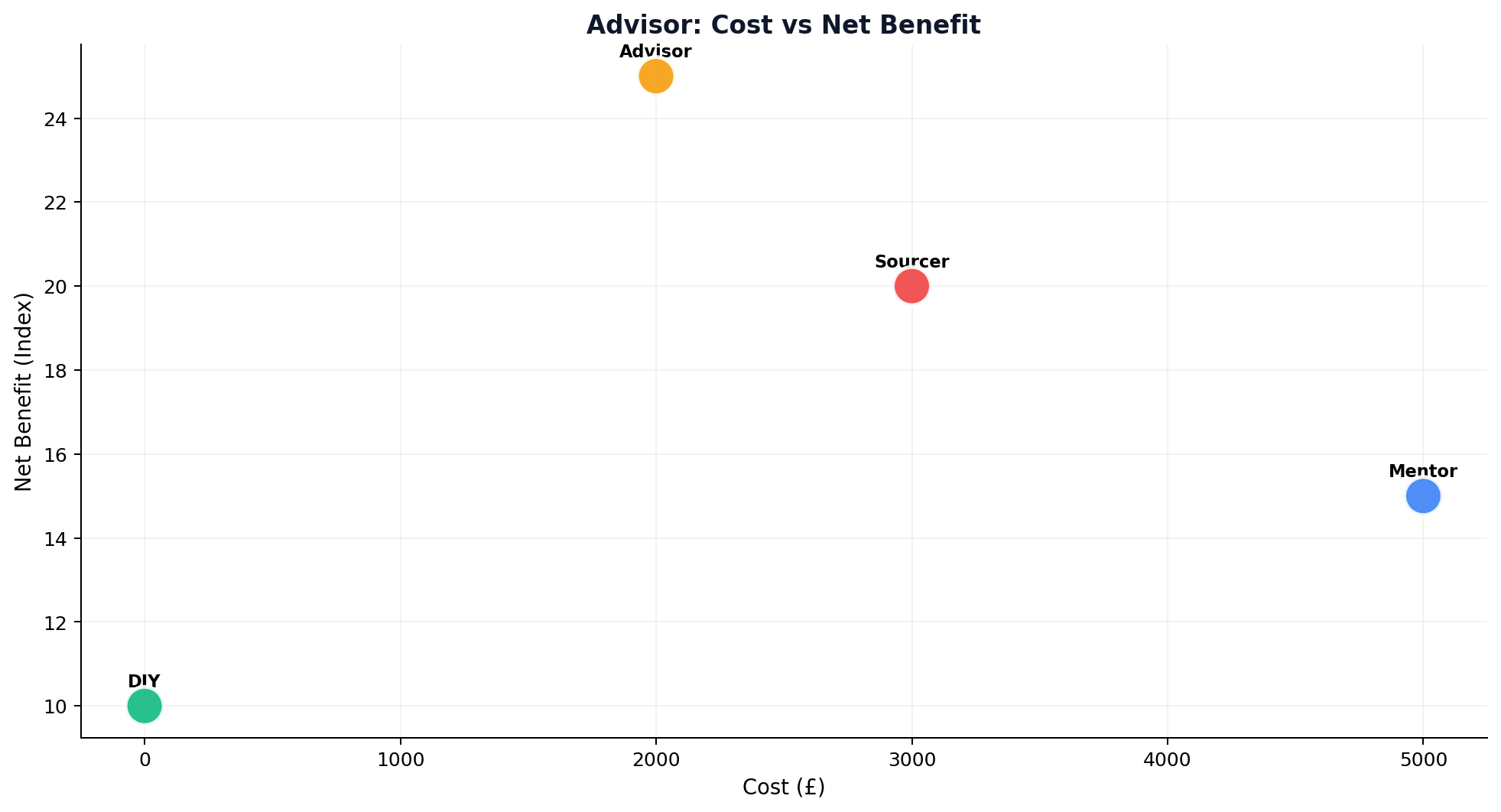

2. Do You Need an Advisor? (The Checklist)

Most investors do not need a retained advisor. You need education. However, there are exceptions.

You NEED an Advisor if:

- You have £200k+ to invest and zero time.

- You are an overseas investor (expat) who cannot view properties.

- You are buying a complex asset (e.g., a commercial building for your business pension).

You DO NOT NEED an Advisor if:

- You have £50k savings. (Paying a £3k fee eats 6% of your capital immediately).

- You want to be "hands-on."

- You are buying a simple Buy-to-Let in your local area.

3. How to Vet an Independent Advisor

If you decide to pay for advice, treat it like a job interview.

The "Whole of Market" Test Ask them: "What was the last property you told a client NOT to buy?" A real advisor kills more deals than they recommend. A salesperson recommends everything.

The Fee Structure Test Real advice is paid for.

- Good: You pay a retainer or a sourcing fee (e.g., £1,000 upfront, £2,000 on completion). They work for you.

- Bad: "Our service is free to you." They work for the seller.

The "Skin in the Game" Test Ask to see their personal portfolio. If they are advising you to buy HMOs in Liverpool, but they only own index funds, walk away.

4. The "Pension" Question

We get asked this daily: "Can I put my Buy-to-Let in a pension?" Generally, No. Residential property cannot go into a SIPP.

However:

- Commercial Property: Yes. You can use your pension to buy your business premises (or a shop/office). This is tax-efficient but requires an FCA-Regulated Advisor.

- REITs: You can invest in property shares (like British Land) via a pension.

5. Conclusion

There is a place for Property Advisors. A good one can save you £50,000 by stopping you from buying a lemon.

But you must understand who pays their wages.

- If you pay them, they are an Advisor.

- If the seller pays them, they are an Agent.

Never confuse the two.

Figure: Advisor Comparison

Figure: Advisor Comparison

Figure: Advisor Cost vs Benefit

Figure: Advisor Cost vs Benefit

Stop being a landlord. Start being an investor.

Shaded Canvas introduces serious capital to vetted UK property opportunities — targeting 12–16% net returns.

Start Investing →