Thinking of investing in Scotland? Forget everything you know about buying property in England.

You might be looking North for the yields (often 6-8% vs 4-5% in the South) or the lower entry prices (average £195k vs £306k). But Scotland is a different country with a different legal system, different taxes, and a radically different rental market.

Walk into a Scottish deal with an "English mindset," and you will either lose money or lose the deal entirely.

This guide is your translation manual. It covers the 2026 tax hikes, the "Offers Over" reality, and why you might actually prefer the Scottish system once you understand it.

1. The Buying Process: Speed vs Flexibility

In England, buying a house is a marathon where anyone can pull out at mile 25. In Scotland, it’s a sprint.

The "Missives" (No Gazumping)

In England, you wait months for "Exchange of Contracts." Until then, the seller can accept a higher offer (gazumping). In Scotland, solicitors exchange formal letters called "Missives." Once these are concluded (often within weeks), the deal is legally binding.

- Pro: Certainty. Once you're in, you're in.

- Con: You can't change your mind without severe penalties.

"Offers Over" vs Asking Price

Most Scottish properties are marketed as "Offers Over £150,000."

- The Reality: The selling price is usually 10-20% higher than this figure.

- The Trap: Banks lend on the Home Report value, not your bid. If the Value is £150k and you bid £170k, you adhere to pay the £20k difference in cash.

Freehold vs Leasehold

Good news: The feudal system is dead here. There is practically no leasehold. When you buy a flat, you own a share of the land and the roof. No shrinking leases, no ground rent scandals.

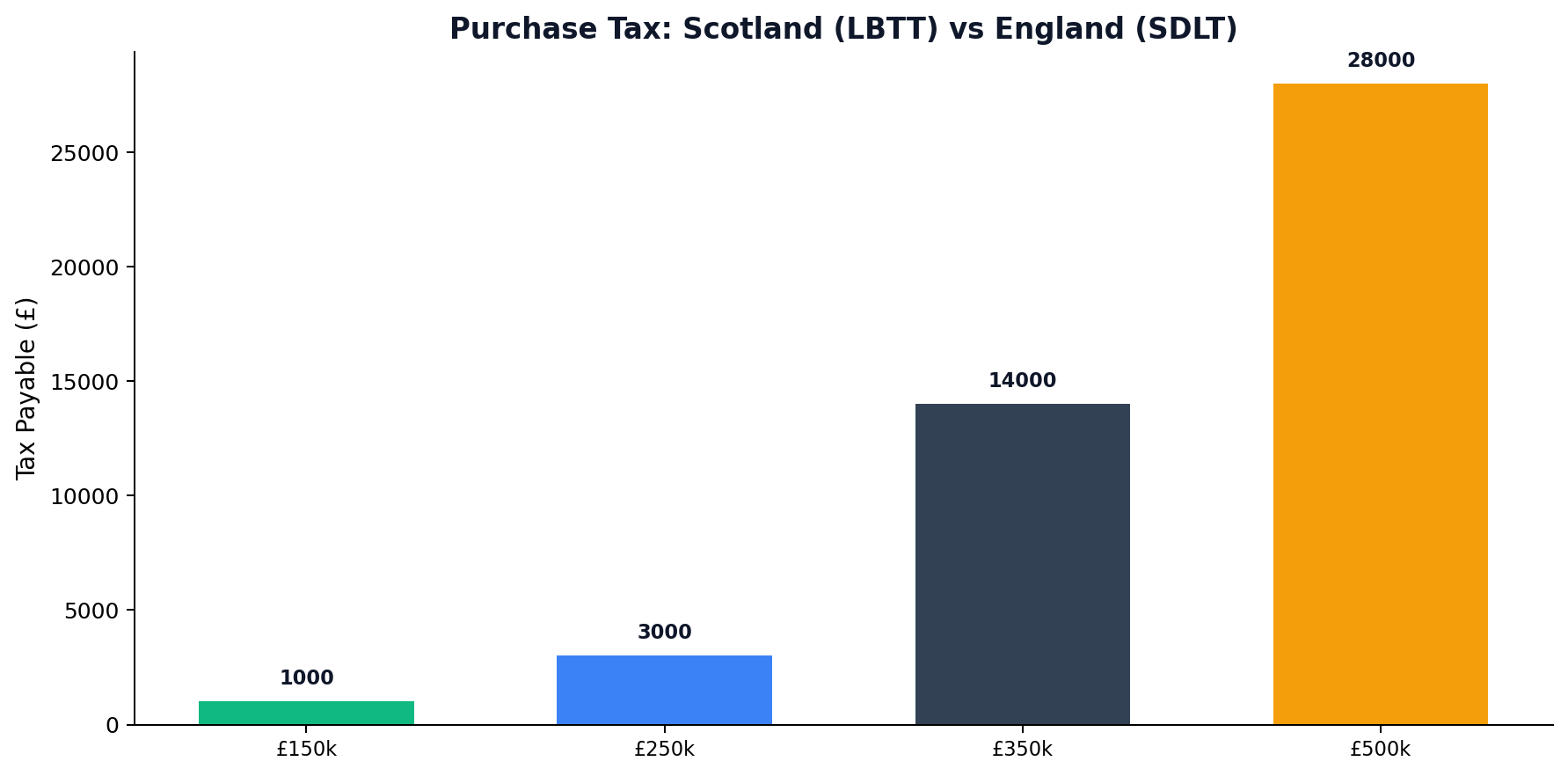

2. The Tax Trap: ADS is now 8%

This is the biggest shock for 2026 investors.

In England, you pay a 3% Stamp Duty surcharge for a second home. In Scotland, you pay Land and Buildings Transaction Tax (LBTT) plus the Additional Dwelling Supplement (ADS).

As of December 2024, the ADS rate is 8%.

Let's do the math on a £200,000 investment property:

- England (Stamp Duty): £6,000 (3% surcharge)

- Scotland (LBTT + ADS): £17,100 (£1,100 LBTT + £16,000 ADS)

The Upshot: You need £11,100 more upfront cash to buy the exact same value property in Scotland. You must factor this into your ROI.

3. The Rental Market: The PRT

In England, you have Assured Shorthold Tenancies (6 or 12 months). In Scotland, you have the Private Residential Tenancy (PRT).

- No Fixed Terms: A tenant moves in today and can give 28 days' notice to leave tomorrow. You cannot insist on a "12-month contract."

- Evictions: "No Fault" evictions are gone. You need a specific reason (e.g., selling, moving in, rent arrears) to evict.

- Rent Increases: You can only increase rent once every 12 months, and tenants can challenge "unreasonable" increases via Rent Service Scotland.

Is it a nightmare? No. Most tenants want to stay long-term. But it shifts the power dynamic. You have to be a good landlord to keep good tenants.

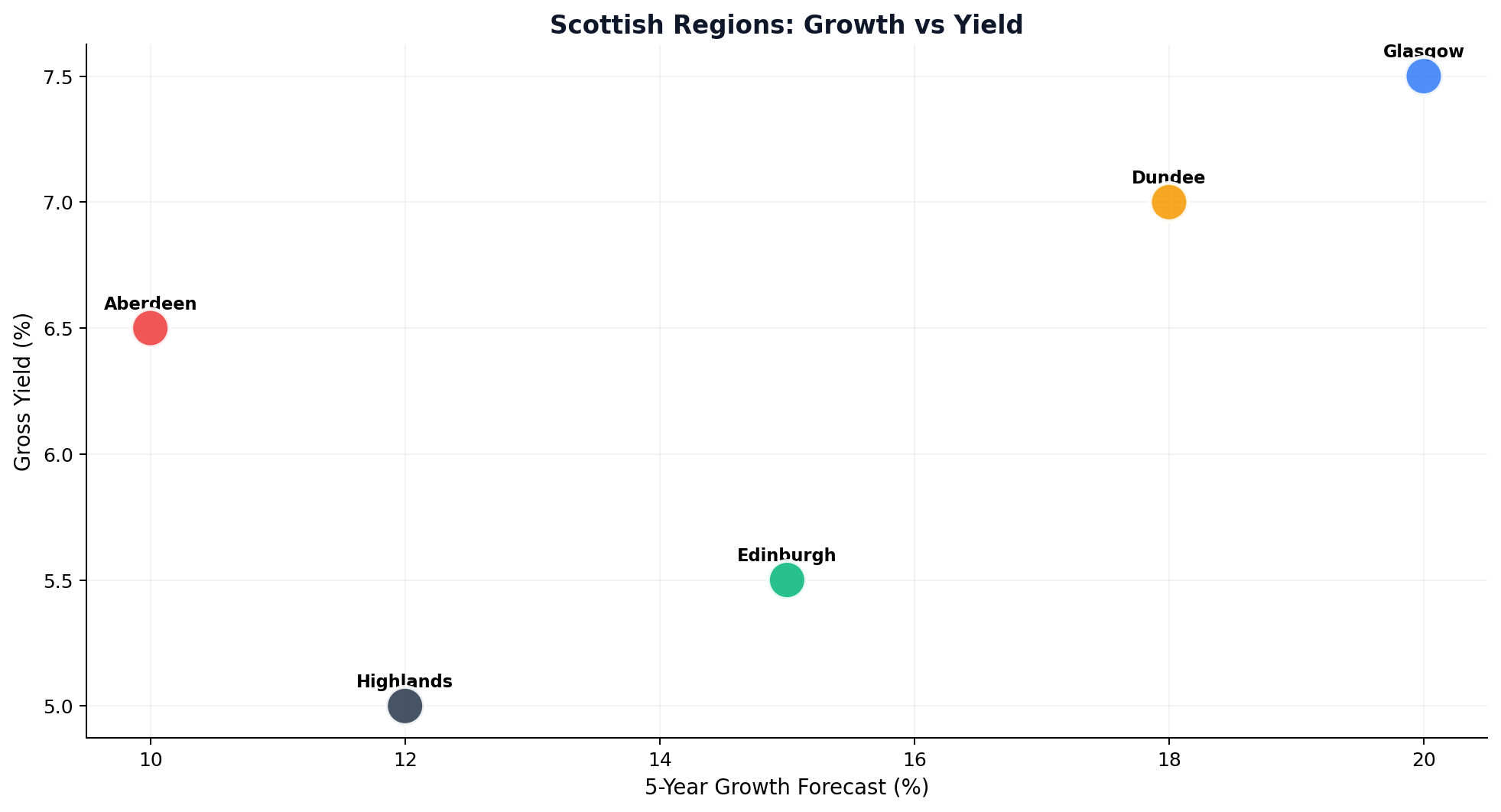

4. Best Investment Areas for 2026

Where should you put your money?

Glasgow: The Yield Engine

- Why: Huge student population (Stratclyde, Glasgow Uni) and a shortage of housing.

- Areas: Dennistoun (trendy, rising capital), Govanhill (high yield, rougher), West End (expensive, safe).

- Returns: 6-8% Gross Yield is achievable.

Dundee: The Emerging Market

- Why: £1bn waterfront regeneration (V&A Museum). It's where investors go when priced out of Glasgow.

- Entry: You can still buy flats for £100k - £120k.

- Returns: 7-9% Yields. High cash flow.

Aberdeen: The "Energy Capital"

- Why: Prices crashed after the 2014 oil slump. They are now recovering. High salaries in the energy sector mean good tenants.

- Risk: Highly correlated to oil/renewables industry health.

5. Strategy: How to Structure the Deal

Given the 8% ADS tax, "flipping" (buy-sell) is much harder in Scotland. The transaction costs eat your profit.

The Winning Strategy for Scotland:

- Long-Term Hold: Buy for 10-20 years to spread out that initial tax hit.

- Limited Company: If you are a higher-rate taxpayer, buying via a Ltd Co (SPV) is almost essential to offset mortgage interest (Section 24 applies UK-wide).

- High Yield Essential: Because your upfront costs (ADS + "Offers Over" gap) are higher, you need a higher monthly yield to get a decent Return on Capital Employed (ROCE). Target 7%+.

Conclusion: Scotland offers incredible stability and freehold ownership that English investors can only dream of. But entry is expensive. Bring cash, think long-term, and get a Scottish solicitor before you even look at a property.

Figure: LBTT vs SDLT Comparison

Figure: LBTT vs SDLT Comparison

Figure: Scottish Regions Growth vs Yield

Figure: Scottish Regions Growth vs Yield

Stop being a landlord. Start being an investor.

Shaded Canvas introduces serious capital to vetted UK property opportunities — targeting 12–16% net returns.

Start Investing →