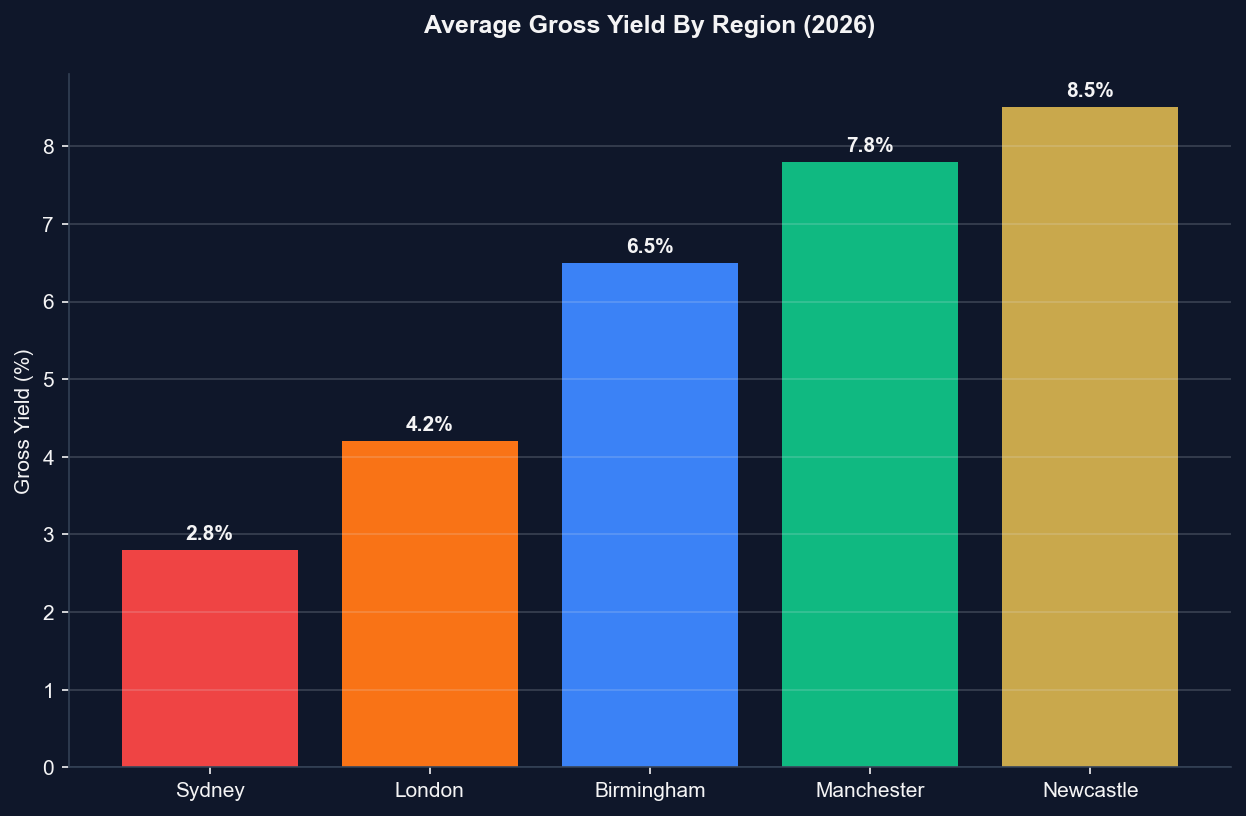

If you're an Australian looking to buy property in the UK, you already know the core reasons why: Australian yields are compressed, entry prices in Sydney and Melbourne are astronomical, and the UK offers a highly regulated market with strong regional rental returns.

However, the actual process of buying a house in the UK from 10,000 miles away can seem daunting. The UK legal system, the tax structures, and the mortgage requirements are entirely different from what you are used to back home.

This is a practical, no-nonsense, step-by-step guide designed specifically for Australian residents. We'll walk through exactly how to structure your purchase, secure expat finance, find an asset, and navigate the UK conveyancing system without ever needing to board a flight to Heathrow.

Step 1: Establish Your Purchasing Structure (SPV vs Personal)

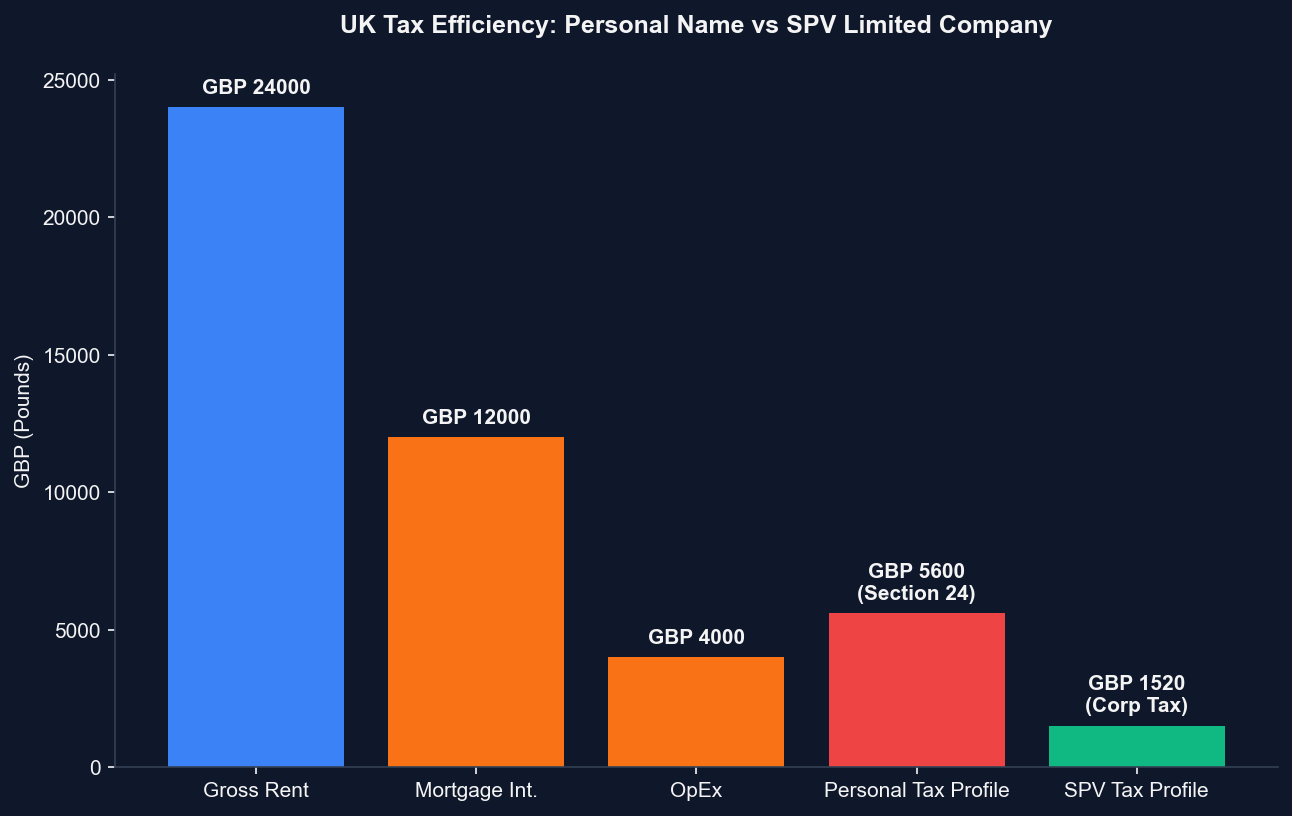

Before you look at a single property, you must decide how you are going to buy it. In the UK, you have two choices: buying in your personal name, or buying through a Special Purpose Vehicle (SPV)—which is simply a UK Limited Company set up to hold property.

For 95% of Australian investors in 2026, buying through an SPV is the only logical choice.

Why You Should Use an SPV

- Mortgage Interest Relief: If you buy in your personal name, UK tax laws (Section 24) prevent you from fully deducting your mortgage interest from your rental income. If you buy through an SPV, 100% of your mortgage interest is treated as a deductible business expense.

- Tax Control: An SPV pays UK Corporation Tax (19-25%) on profits. You only pay personal tax when you extract those profits as dividends, giving you total control over when you declare income to the ATO.

- Inheritance Tax Protection: Holding UK property directly can expose your global estate to UK Inheritance Tax. Corporate structures can help mitigate these punitive cross-border tax liabilities.

Action Item: Engage a dual-qualified UK/Aussie tax accountant to register your UK Limited Company. This process takes roughly 24 to 48 hours and can be done entirely online.

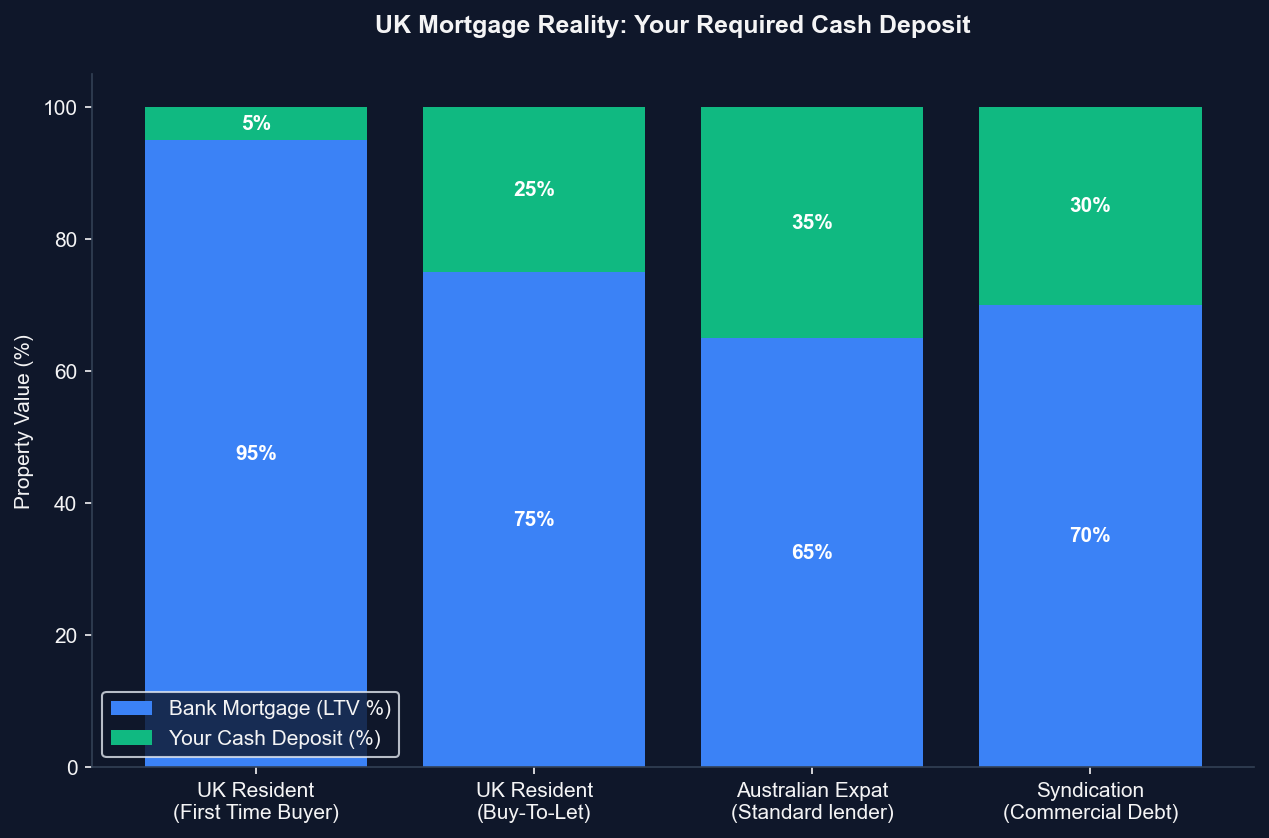

Step 2: Secure Your "Agreement in Principle" (AIP)

In Australia, getting mortgage pre-approval is relatively straightforward. In the UK, as a foreign national without a UK credit file, you fall into the "Expat/Foreign National" lending category. High-street banks (like Barclays or NatWest) will generally reject your application automatically.

The Expat Finance Reality

You need to work with a specialist whole-of-market broker who has direct relationships with lenders that manually underwrite Australian applicants.

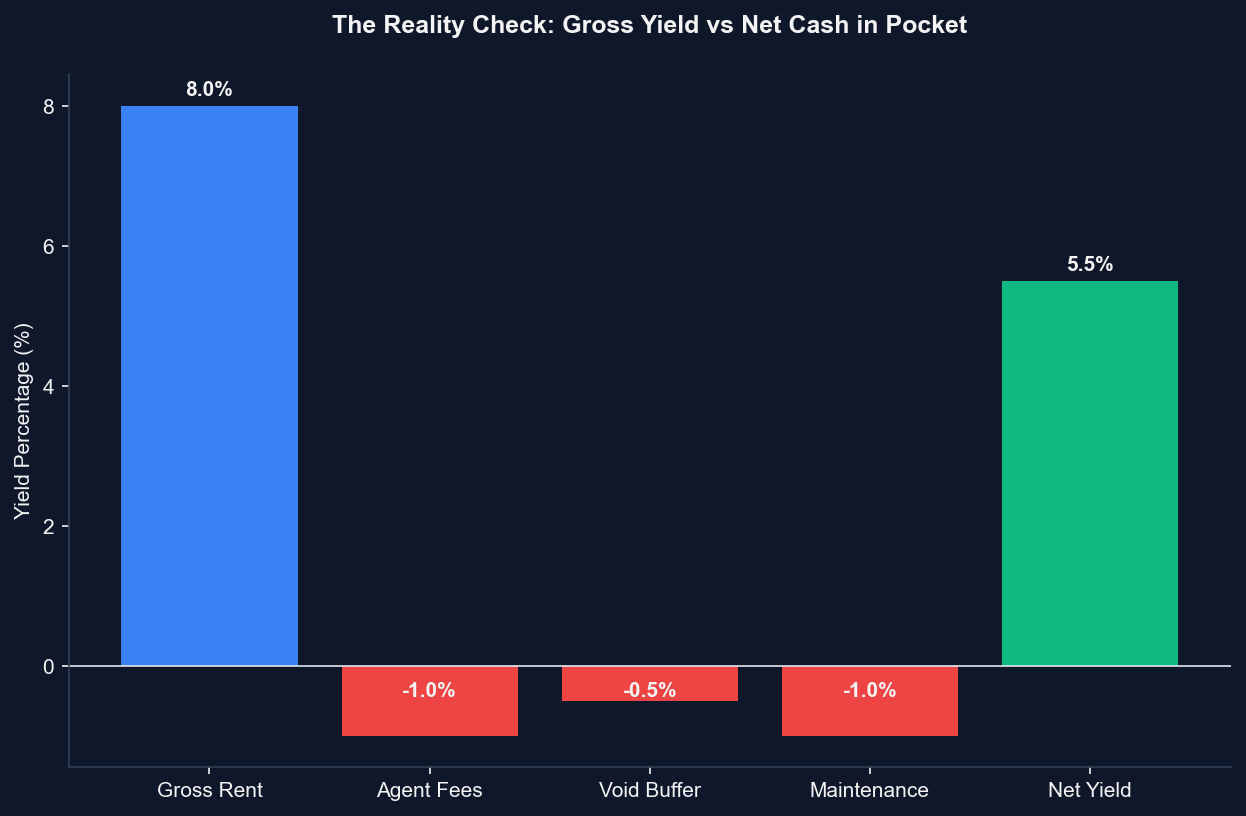

- The Deposit: Expect to need a deposit of at least 25% to 35% (a Loan-to-Value of 65% to 75%).

- The Rate: Expat mortgages carry a "risk premium." Expect to pay around 0.5% to 1.5% higher than a local UK resident.

- The Paperwork: Anti-Money Laundering (AML) checks are intense. You will need to provide certified passport copies, proof of address, and 3 to 6 months of bank statements proving exactly where your deposit funds originated.

Action Item: Contact a specialist UK expat mortgage broker. Provide your financial documentation and secure an Agreement in Principle (AIP) so you know exactly what your purchasing budget is.

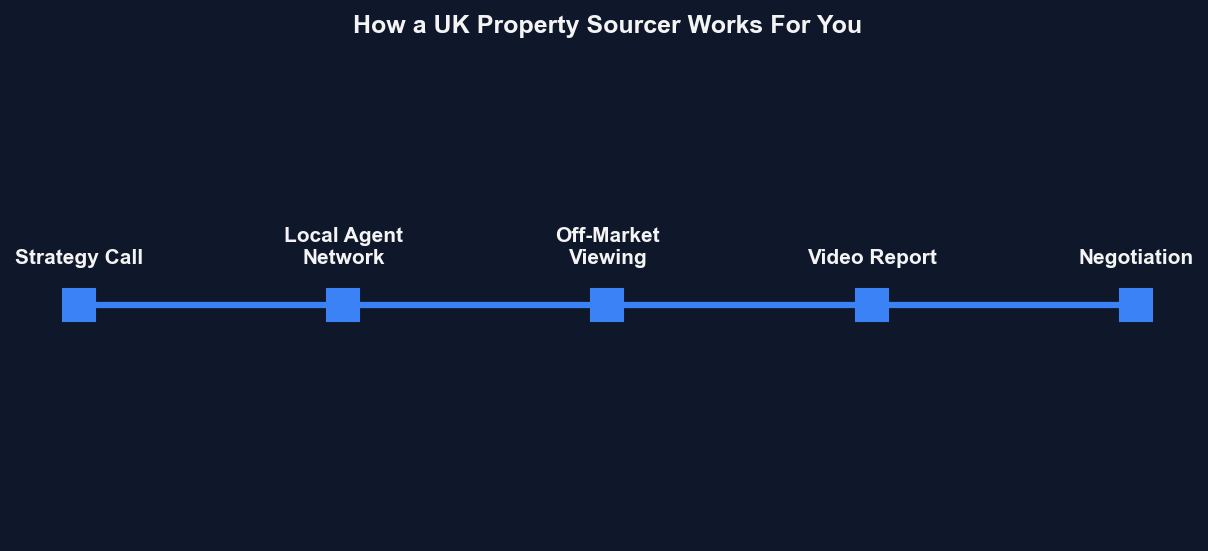

Step 3: Source the Right Property

You cannot rely on local property portals (like Rightmove or Zoopla) to build a high-yielding portfolio from Australia. By the time a "good deal" hits the open market, local investors have already passed on it. Furthermore, you cannot inspect the property, assess the neighborhood, or verify the condition of the roof.

How to Buy from Afar

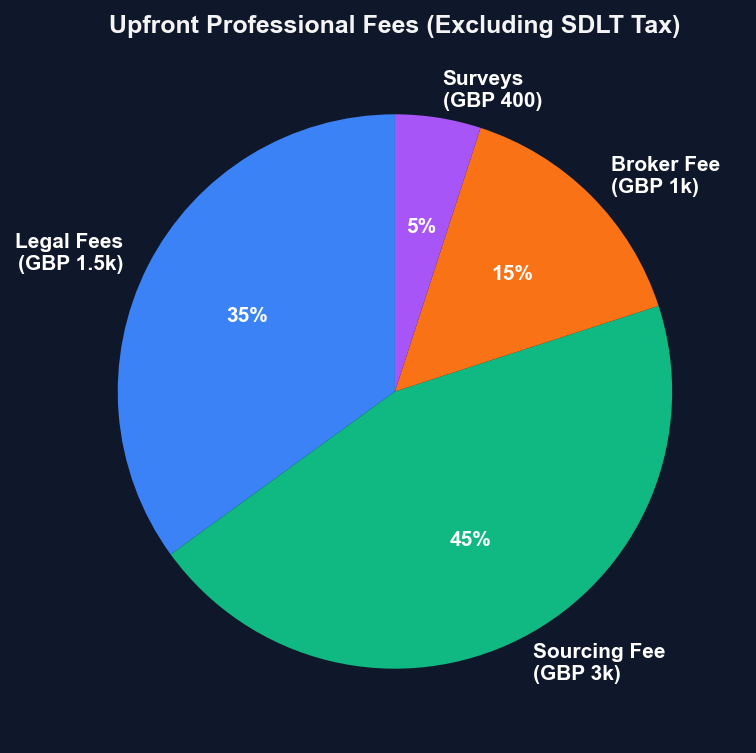

- Property Sourcing Companies: You can hire a compliant, regulated UK property sourcer. They act as your buyer's agent. They find off-market deals, inspect the property, record video walkthroughs, and negotiate the price on your behalf. Expect to pay a sourcing fee of £3,000 to £5,000 upon a successful purchase.

- Turnkey/Off-Plan Investments: Buying new-build apartments or fully refurbished properties directly from developers. This requires less maintenance but often comes at a premium price.

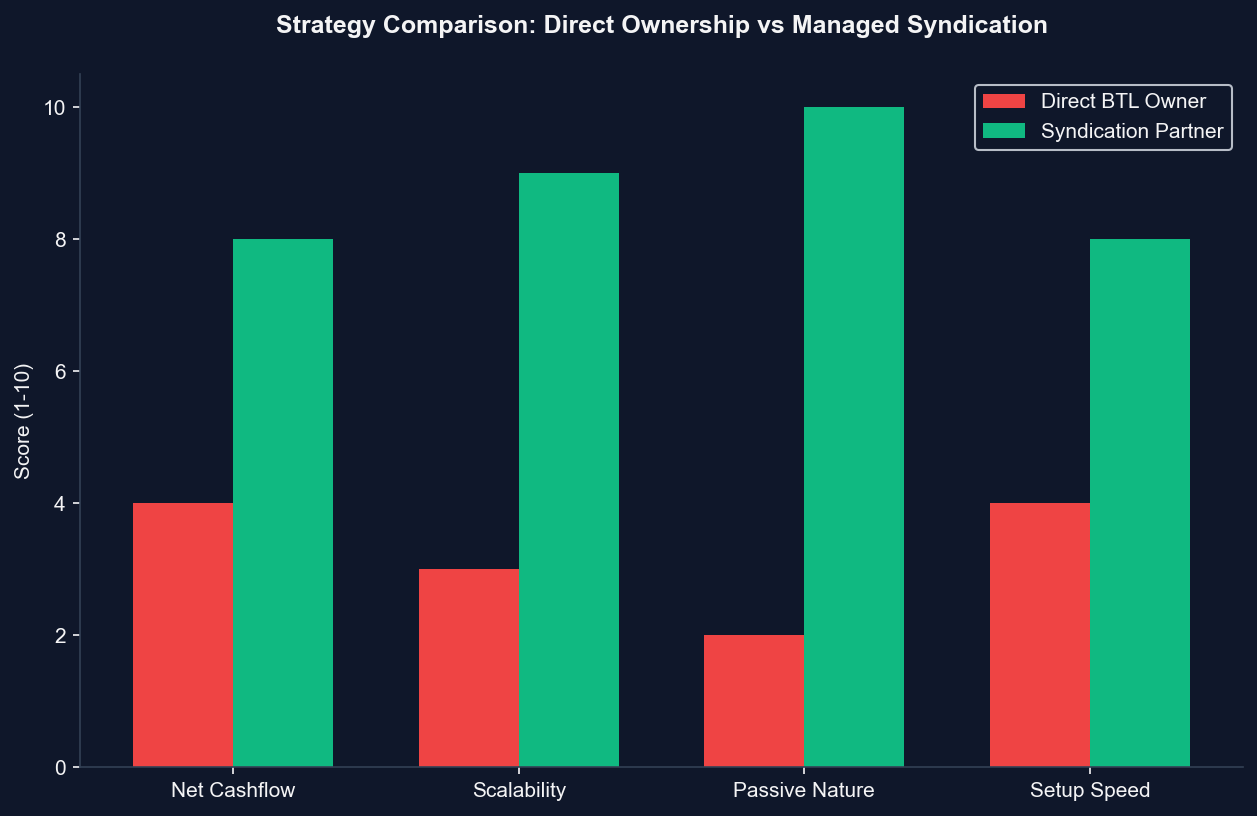

- Managed Syndications: If you want truly passive income, you pool your capital into an SPV alongside others to buy large, high-yielding assets (like HMOs).

Action Item: Do not guess the market. Retain a professional sourcing agent who specializes in your target region (e.g., Manchester, Birmingham, or the North East) and let them bring fully vetted deals to your inbox.

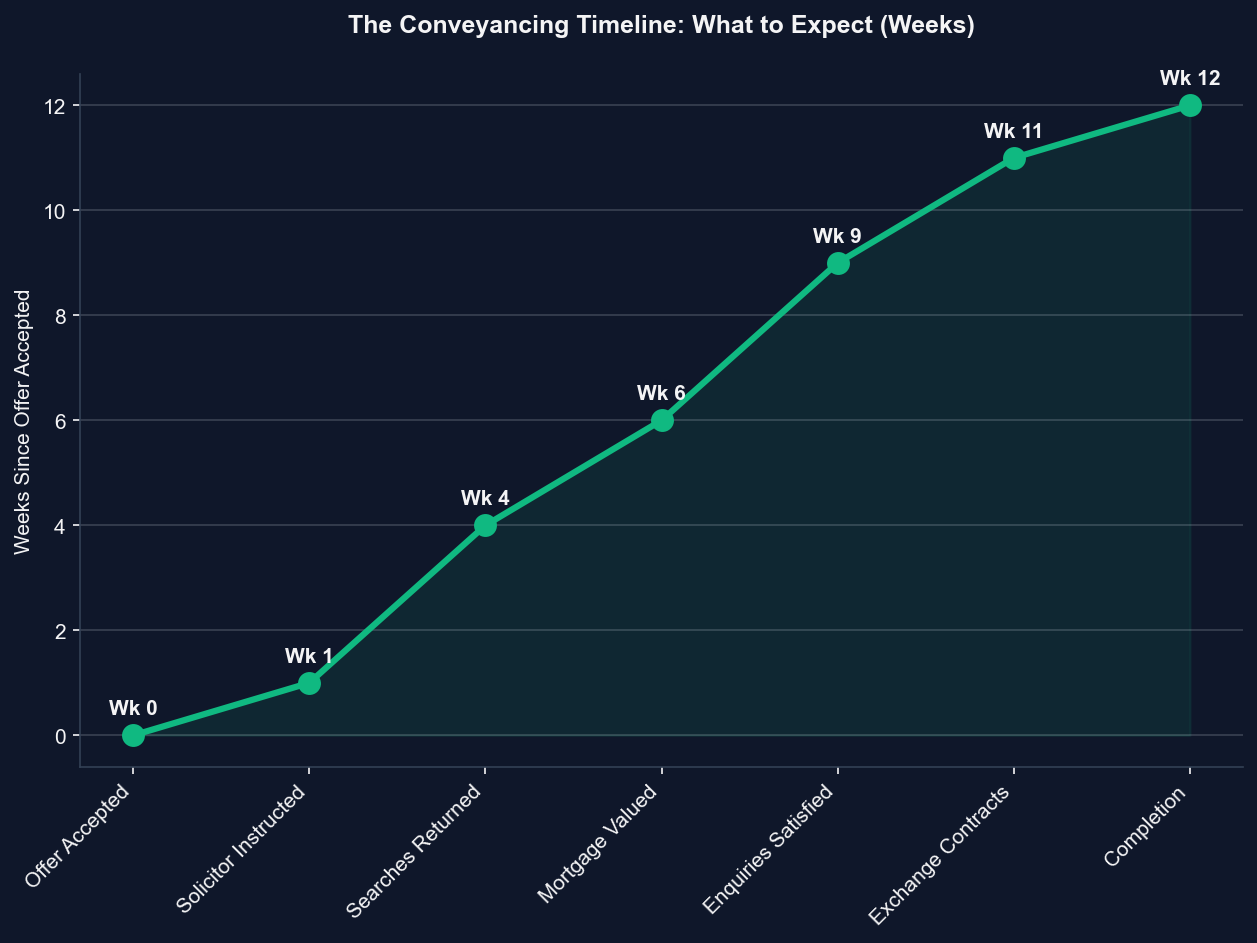

Step 4: The Legal Process (Conveyancing)

Once your offer is accepted, the UK legal process—known as "conveyancing"—begins. This is notoriously slow. In Australia, a settlement might take 30 to 60 days. In the UK, expect it to take anywhere from 8 to 16 weeks.

The Conveyancing Timeline

- Instruct a Solicitor: You must hire a UK-based property solicitor. Ensure they have experience dealing with foreign buyers and SPVs.

- Searches and Enquiries: Your solicitor will order "searches" (checking local council records for planning issues, flood risks, etc.) and raise "enquiries" with the seller's solicitor regarding the property's title.

- The Valuation: Your mortgage lender will send a surveyor to value the property and ensure it is safe to lend against.

- Exchange of Contracts: Once all enquiries are satisfied, you sign the contract, transfer your deposit (usually 10%), and the solicitors "exchange." At this point, the purchase is legally binding. If you pull out now, you lose your deposit.

Action Item: Instruct a proactive solicitor immediately upon offer acceptance. Prepare to be patient, but email them weekly for updates to keep your file at the top of their pile.

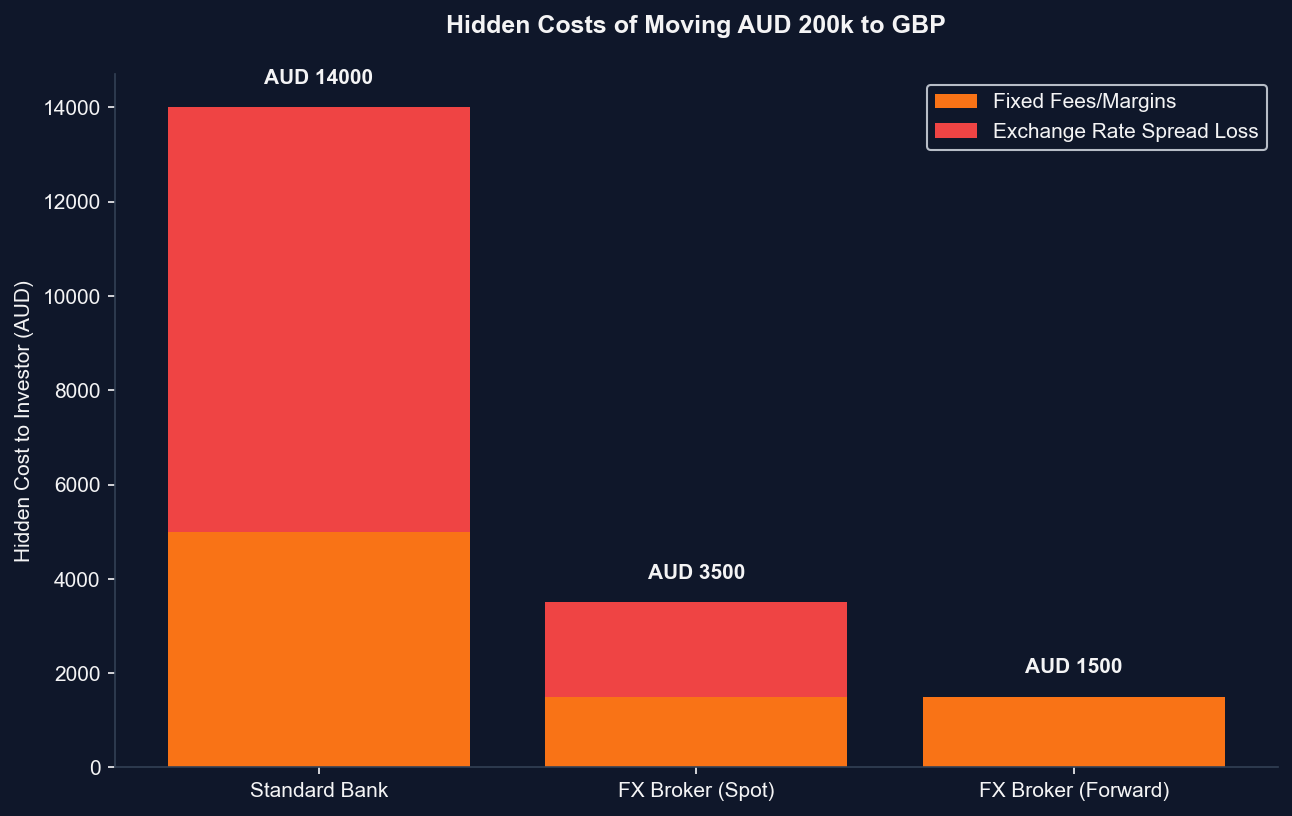

Step 5: Transferring Funds and Currency Exchange

When getting close to the "Exchange of Contracts," you will need to move your AUD into GBP. Do not use your standard Australian bank to transfer hundreds of thousands of dollars to the UK. The retail exchange rates and hidden fees will cost you thousands.

Use an institutional foreign exchange (FX) broker (like Wise, Currencies Direct, or Smart Currency Exchange). They offer commercial rates, low transfer fees, and the ability to "forward contract" (locking in a favorable exchange rate today for a transfer you need to make in a month's time).

Step 6: Completion and Handover

"Completion Date" is the UK equivalent of settlement. On this day:

- Your mortgage lender releases the remaining funds to your solicitor.

- Your solicitor transfers the full purchase price to the seller.

- You officially own the property.

Setting Up the Management

Because you are 10,000 miles away, self-managing is impossible. Before completion, you must interview and appoint a local letting agent.

- Letting Agent Fees: Typically 10% to 15% + VAT of the monthly rent for a "fully managed" service.

- Their Responsibilities: They will find the tenant, run background checks, collect rent, handle emergency maintenance (e.g., a broken boiler), and ensure the property complies with strict UK regulations like Gas Safety certificates and EPC ratings.

Action Item: Appoint a specialized, local letting agent who uses modern property management software, ensuring you get transparent, real-time updates on your asset from your phone in Australia.

The Fast Track: Bypassing the Chaos

The 6-step process above is how you buy a standalone Buy-to-Let (BTL) property in the UK. Many Australians execute this path successfully, but it requires assembling a trusted team of sourcers, brokers, solicitors, and letting agents from scratch.

If your primary goal is simply to deploy AUD into a high-yielding, GBP-denominated asset without dealing with solicitors, boiler repairs, or tenant sourcing, the modern alternative is managed syndication.

In a syndication, you partner with a firm (like Shaded Canvas) that has already done the heavy lifting. The SPV is formed, the high-yielding asset is sourced, the institutional finance is secured, and the operations team is already in place. You simply acquire shares in the SPV, sit back, and receive professional quarterly reports and dividends.

Buying UK property from Australia doesn't have to be a headache. Whether you choose to build your own team and execute directly, or buy into a managed syndication, the rewards of the UK market are waiting. Establish your structure, get your finance in order, and start building your Sterling portfolio.

Stop being a landlord. Start being an investor.

Shaded Canvas introduces serious capital to vetted UK property opportunities — targeting 12–16% net returns.

Start Investing →