Executive Summary

The era of easy money and effortless property flips in the UK has officially ended. A market previously characterised by low interest rates and frantic buyer demand allowed investors to generate substantial profits from purely cosmetic renovations—a coat of paint, new carpets, and a basic kitchen. Today, in a landscape defined by elevated borrowing costs and cautious, risk-averse buyers, that strategy is a fast track to financial ruin. The modern UK property flipper must pivot from superficial updates to genuine, structural value creation.

This comprehensive guide dissects the most profitable house flipping strategies for 2026. We will explore advanced tactics such as structural value-add, title splitting, and the emerging trend of 'Green Flipping'. Crucially, we will also navigate the UK-specific hurdles that consistently trap novice investors, including the punitive 3% Stamp Duty Land Tax (SDLT) surcharge, the restrictive '6-Month Rule' imposed by high-street lenders, and the complex tax implications of trading property versus investing. Whether you are an experienced developer or a serious entrant to the market, this data-driven blueprint will equip you with the strategies required to extract maximum margin from the UK property market.

The Evolution of the UK Flip: Why 'Lipstick on a Pig' No Longer Works

The prevailing sentiment among experienced UK property investors—echoed loudly across professional forums and communities like r/UKProperty—is a profound disdain for the 'gray flip'. This refers to the ubiquitous, low-effort renovation characterised by cheap gray laminate flooring, stark white walls, and budget fixtures designed solely to mask underlying issues.

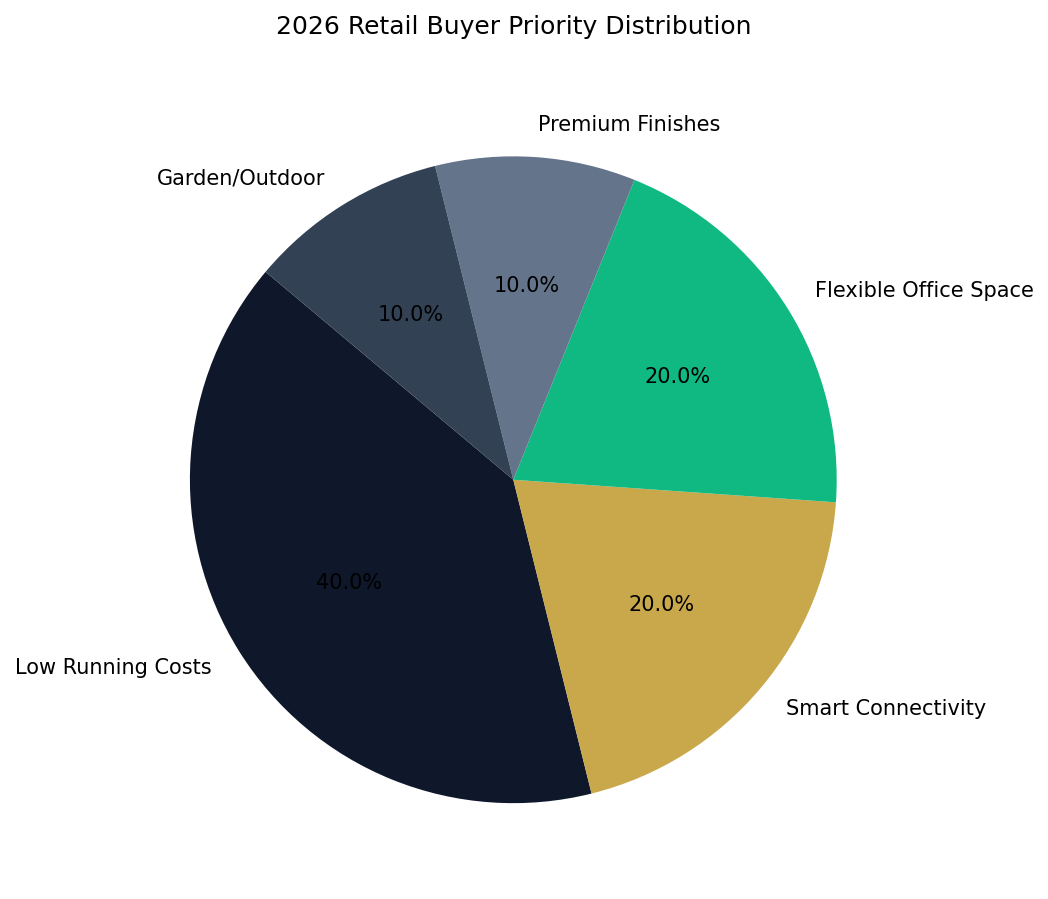

Buyers in 2026 are highly discerning. With mortgage rates placing significant pressure on affordability, first-time buyers and families expect turnkey properties that do not require immediate remedial work. They are increasingly willing to pay a premium for quality, but they will aggressively discount properties that feel cheaply finished. Therefore, relying on cosmetic changes to artificially inflate a property's After Repair Value (ARV) is no longer a viable strategy. The profit margin must be engineered through fundamental improvements that tangibly alter the property's utility, layout, or legal structure.

Strategy 1: The Structural Value-Add (BRR Variation)

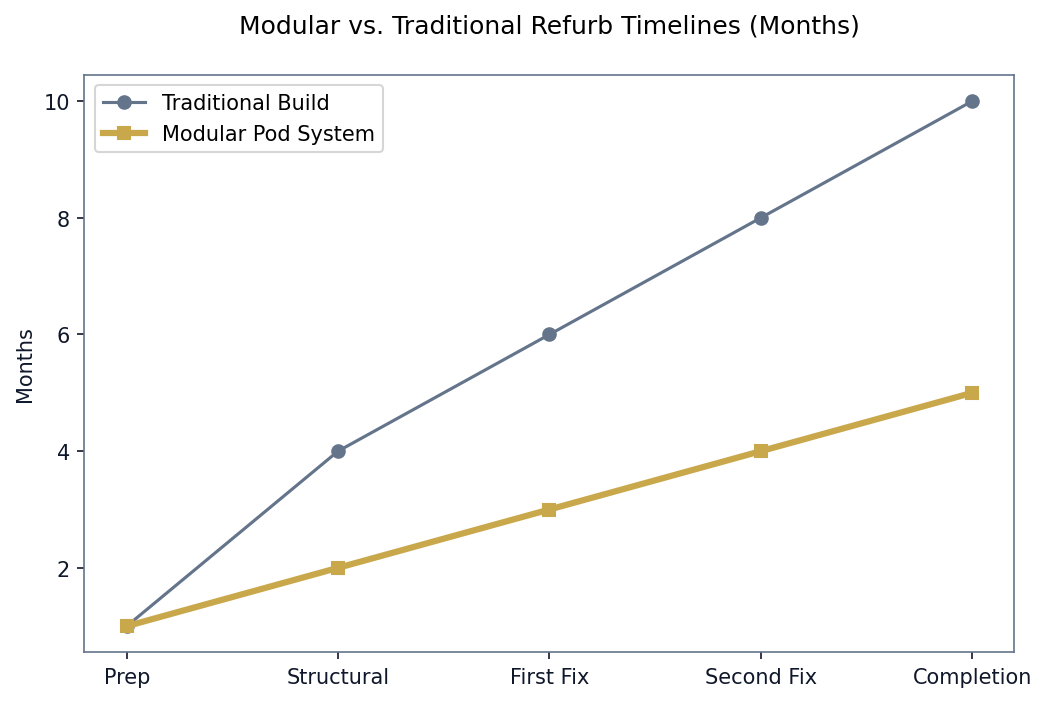

The cornerstone of modern property flipping is the structural value-add. This strategy involves acquiring a property that is fundamentally compromised—perhaps suffering from subsidence, severe damp, or simply an archaic layout—and executing a comprehensive renovation.

Targeting Unmortgageable Properties

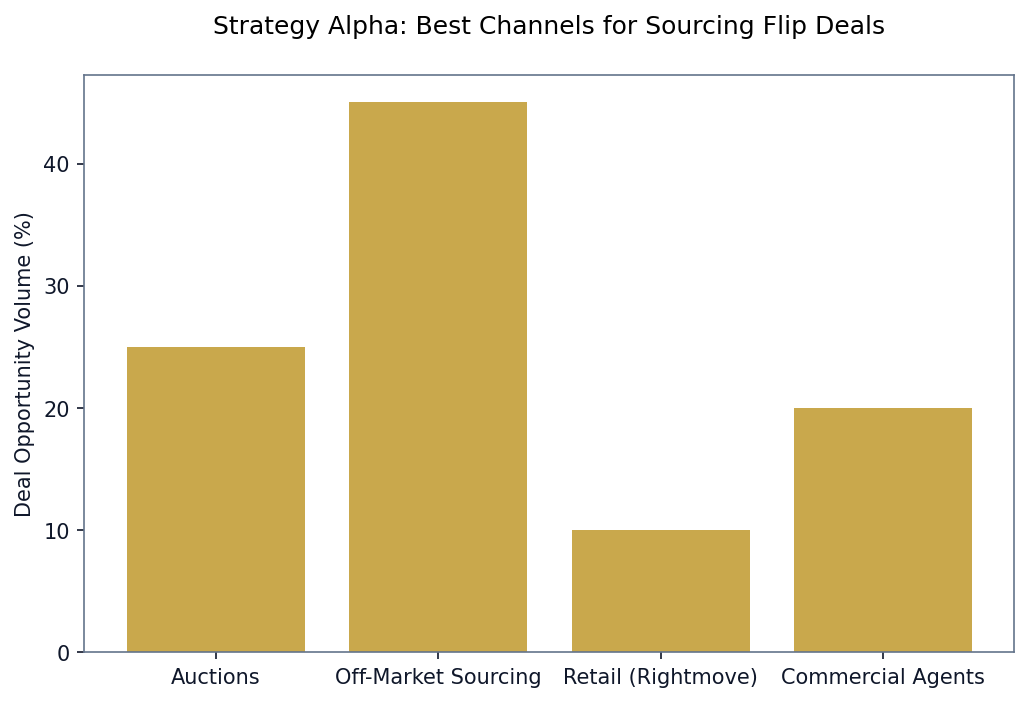

The competitive advantage in this strategy lies in the acquisition phase. Properties lacking a functioning kitchen or bathroom, or those deemed uninhabitable, are classified as 'unmortgageable' by traditional high-street lenders. This dramatically reduces the pool of potential buyers, largely eliminating owner-occupiers and restricting competition to cash buyers and those utilising specialist bridging finance. This lack of competition is the catalyst for securing the property at a significant discount to its theoretical market value.

The 70% Rule in the UK Context

To ensure profitability, professional flippers strictly adhere to the 70% Rule. This heuristic dictates that your total Maximum Allowable Offer (MAO) should not exceed 70% of the property's anticipated ARV, minus the projected renovation costs.

MAO = (ARV x 0.70) - Renovation Costs

For example, if a property's ARV is projected at £300,000, and the structural renovation will cost £45,000:

- £300,000 x 0.70 = £210,000

- £210,000 - £45,000 = £165,000 (Maximum Allowable Offer)

This 30% margin is not your net profit. It provides the critical buffer required to absorb the high costs of bridging finance, Stamp Duty (including the 3% surcharge), legal fees, estate agent commissions, and an essential 15-20% contingency fund for unexpected build costs.

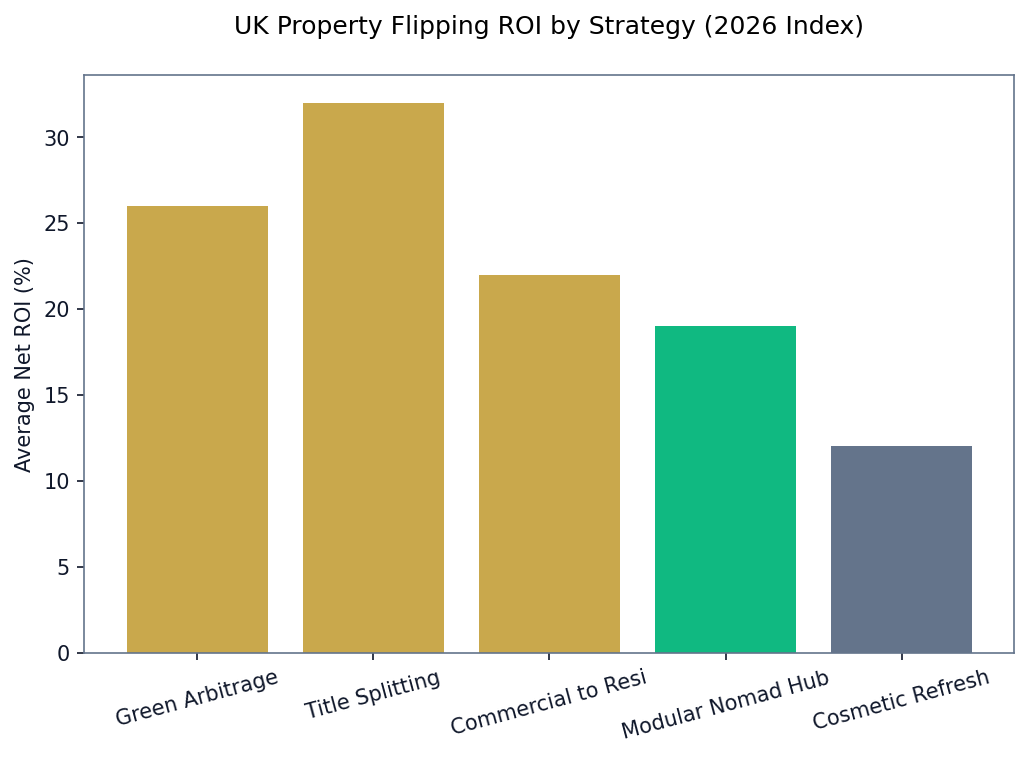

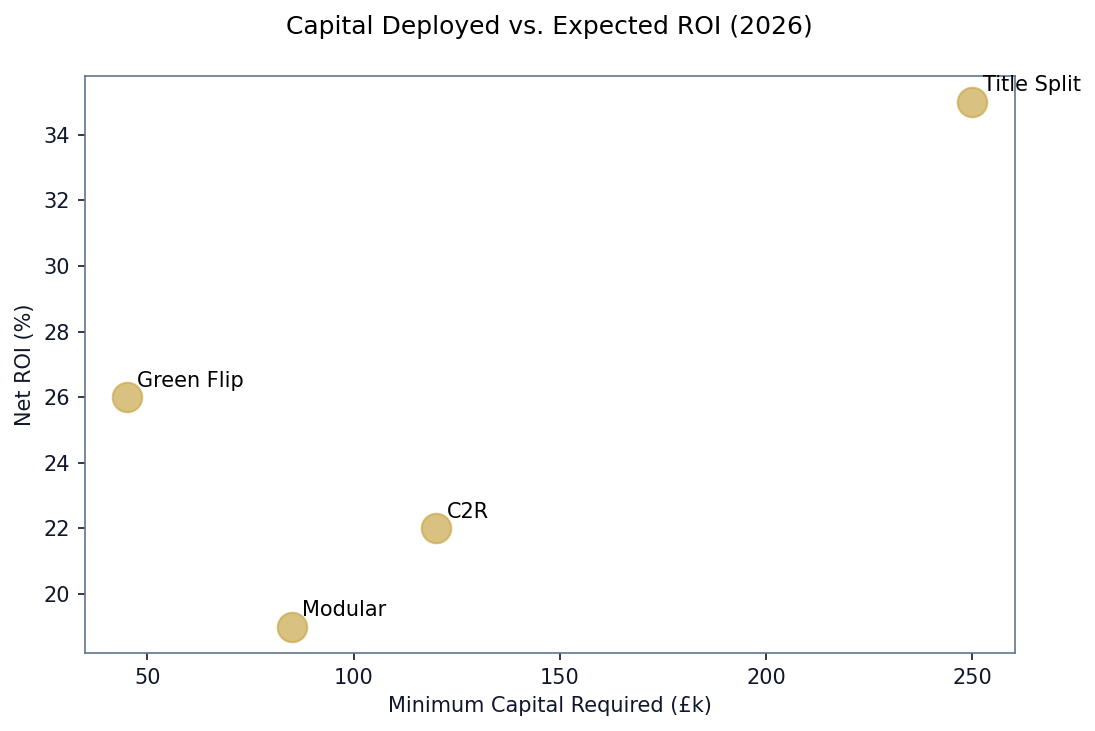

Strategy 2: Title Splitting and Commercial Conversions

For investors seeking higher yields and greater absolute returns, moving beyond single-dwelling renovations is essential. Value can be created rapidly through legal restructuring and leveraging planning policies.

The Mechanics of Title Splitting

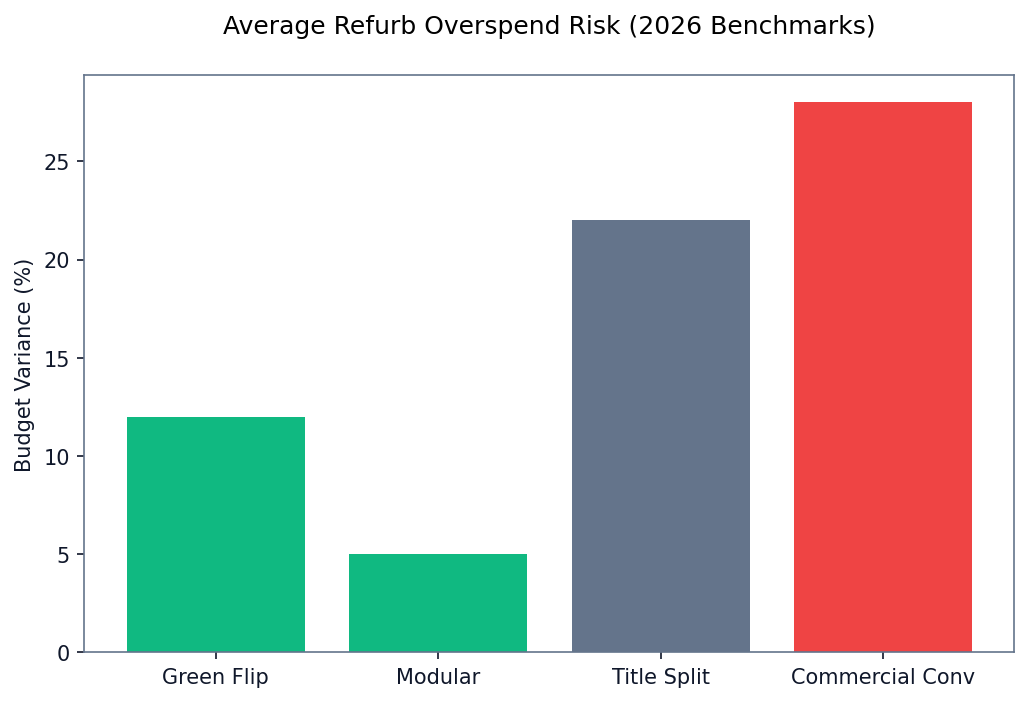

Title splitting involves purchasing a large freehold property—such as a substantial Victorian townhouse or a defunct commercial building—and legally dividing it into multiple leasehold units (e.g., three separate flats). While the physical conversion requires significant capital, the true value is unlocked when the individual leasehold titles are created and sold separately. The aggregate value of the individual flats almost invariably exceeds the ceiling price of the single freehold dwelling. This strategy requires a robust power team, including a specialist conveyancing solicitor and an architect experienced in local planning guidelines.

Permitted Development (PD) Rights

Permitted Development (PD) rights allow investors to bypass the protracted and uncertain full planning application process for specific types of conversions. A highly lucrative strategy under current UK regulations (specifically Class MA) is the conversion of vacant commercial spaces (offices, retail units) into residential dwellings.

Because commercial properties are frequently valued based on their commercial yield rather than their residential potential, they can often be acquired at a lower 'pound per square foot' rate. Converting these spaces into high-demand residential units via PD rights offers a streamlined path to significant capital uplift.

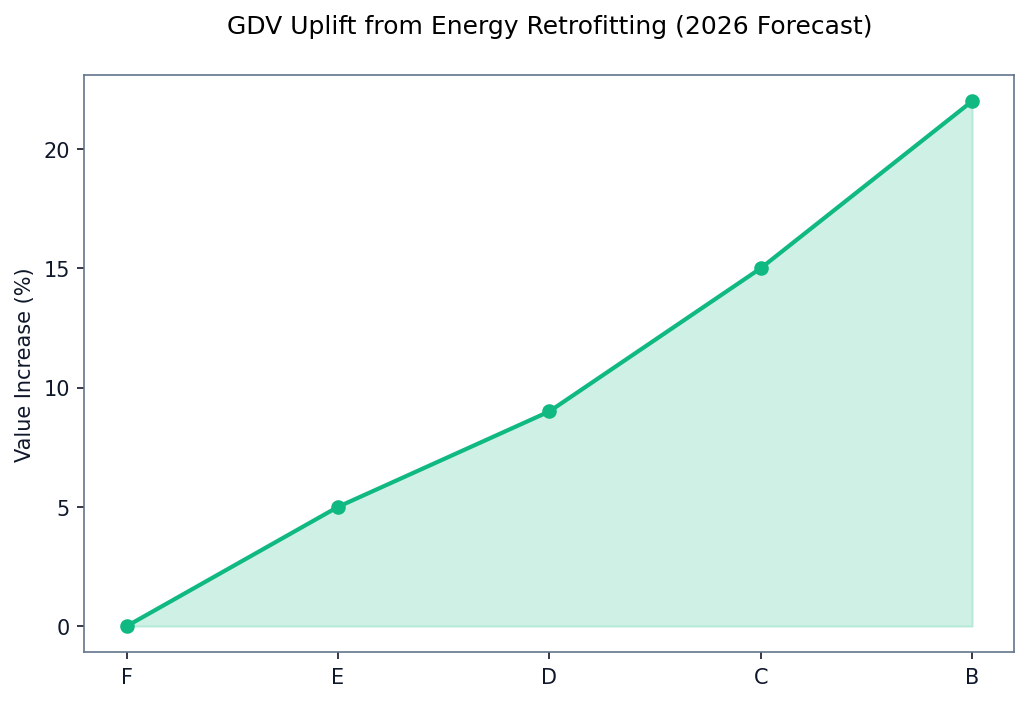

Strategy 3: 'Green Flipping' and EPC Arbitrage

A rapidly emerging strategy driven by both legislative pressure and consumer demand is 'Green Flipping' or EPC Arbitrage. With energy costs remaining a primary concern for UK households, properties with poor Energy Performance Certificate (EPC) ratings (E, F, or G) are facing reduced buyer interest and consequent price discounting.

The EPC Premium

Savvy investors are actively targeting these energy-inefficient homes. The strategy involves undertaking a deep retrofit—installing high-performance insulation (external wall, cavity, or loft), upgrading to double or triple glazing, and replacing antiquated boilers with modern heat pumps or high-efficiency systems.

By elevating a property from an EPC rating of E or F to a solid B or C, investors unlock a tangible 'green premium'. Buyers are increasingly willing to pay more for homes that offer long-term protection against volatile energy markets and comply with increasingly stringent environmental regulations. This strategy aligns physical improvement with shifting market psychology.

Strategy 4: Assisted Sales and Planning Gain

Not all flipping strategies require massive capital deployment or heavy construction. Alternative approaches allow investors to leverage their expertise and network to generate profit with reduced financial exposure.

Assisted Sales

An assisted sale is a low-capital strategy where the investor does not actually purchase the property. Instead, you target a highly motivated seller whose property is unmortgageable or languishing on the market due to poor condition, but who lacks the capital to renovate it themselves.

You enter into a legally binding Joint Venture (JV) agreement. You fund and manage the renovation process using your capital and build team. Upon the sale of the renovated property, the original owner receives an agreed 'base price' (their original asking price or slightly below), and you receive the entire uplift in value, minus your renovation costs. This strategy is highly tax-efficient, entirely bypassing the punitive 3% Stamp Duty surcharge and the necessity for expensive bridging finance.

Planning Gain (The 'Paper Flip')

The 'Paper Flip' involves generating profit purely through the planning system, without laying a single brick. Investors identify properties with significant untapped potential—such as a house with an oversized side plot, or a dilapidated bungalow on a large footprint.

The investor purchases the property (often using an option agreement rather than an outright purchase) and applies for planning permission to build an additional dwelling or a multi-unit development. Once planning is granted, the site's value increases dramatically. The investor then sells the property with the 'Planning Approved' status to a developer, capturing the uplift created by navigating the complex planning bureaucracy.

Navigating UK-Specific Hurdles: The 6-Month Rule

Executing a successful flip in the UK requires more than just construction management; it demands an intimate understanding of the financial and legal landscape. A primary obstacle that frequently catches novice flippers off guard is the '6-Month Rule'.

The Mortgageability Trap

The 6-Month Rule is a widespread policy among UK high-street mortgage lenders (such as Santander, HSBC, and NatWest). It dictates that they will refuse to lend to a buyer if the vendor (the flipper) has owned the property for less than six months. This policy is designed to prevent fraudulent back-to-back transactions and artificial price inflation.

If you complete a rapid cosmetic flip in eight weeks and immediately list the property, your buyer pool will be severely restricted. Anyone requiring a standard mortgage will likely be denied funding. You will be forced to sell to a cash buyer (who will demand a discount) or wait out the six-month period.

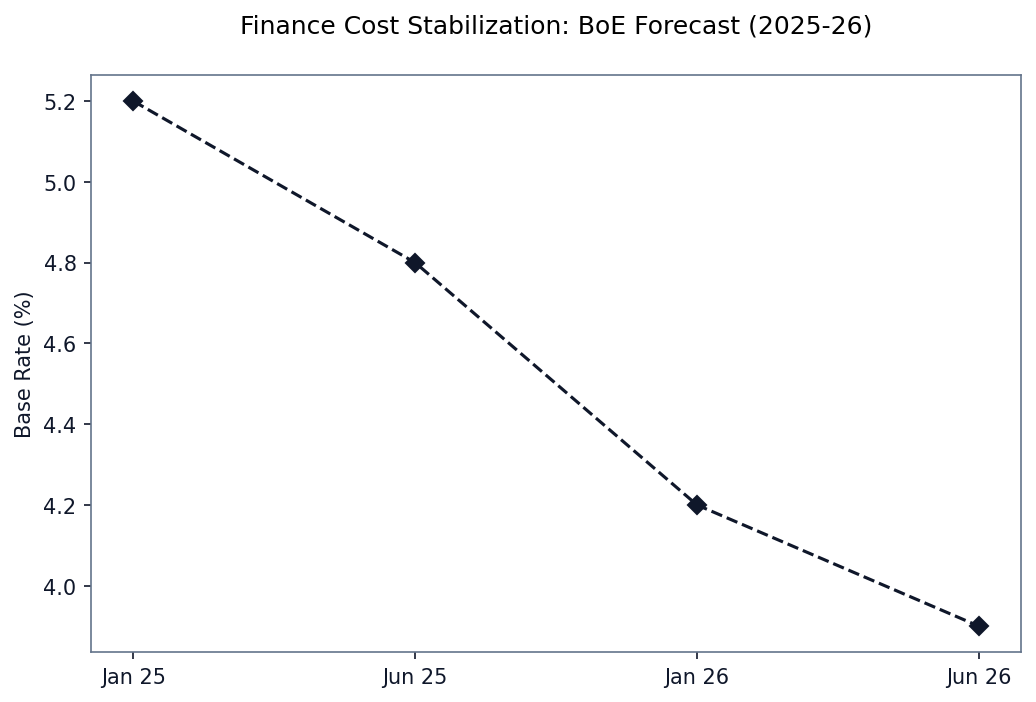

This holding period must be rigorously factored into your financial modelling. If you are utilising bridging finance at 1% per month, holding an empty property for an additional four months to satisfy this rule will decimate your profit margin.

Tax Implications: Income Tax vs. Capital Gains Tax

The tax treatment of property flipping is fundamentally different from traditional Buy-to-Let investing. Failing to structure your acquisitions correctly can result in a devastating tax bill that eradicates your net profit.

Flipping as a Trade

HM Revenue & Customs (HMRC) draws a strict distinction between investing for capital appreciation and trading for income. If you buy a property with the explicit primary intention of renovating and selling it for a profit, HMRC will almost certainly classify this as a 'trade'.

Consequently, any profit generated is subject to Income Tax (which can reach up to 45% for higher-rate taxpayers) and National Insurance Contributions (NICs), rather than the significantly lower Capital Gains Tax (CGT) rates applicable to property investments.

The SPV Advantage

To mitigate this aggressive tax burden, the vast majority of professional flippers operate through a Limited Company, specifically a Special Purpose Vehicle (SPV).

By flipping properties within an SPV, profits are subject to Corporation Tax (currently 19% to 25%), which is substantially lower than upper-tier personal income tax rates. Furthermore, operating via a limited company provides a layer of limited liability protection. The funds can be retained within the company structure to finance subsequent flips, delaying personal tax liabilities until the capital is extracted as dividends.

Actionable Next Steps

Transitioning from theoretical knowledge to a profitable flip requires decisive action and rigorous due diligence. The current market does not forgive amateur mistakes.

Before committing capital to your first project, ensure you have implemented the following foundational steps:

- Assemble Your Power Team: A successful flip relies entirely on the quality of your contractors and legal representatives. Secure a reliable, vetted builder who understands investor timelines. Crucially, engage a 'flip-friendly' conveyancing solicitor who can execute transactions rapidly and understands the nuances of bridging finance.

- Avoid Leasehold Traps: Be exceptionally wary of flipping leasehold flats, particularly those with leases under 85 years or those burdened with opaque, escalating service charges. The legal complexities of extending a lease or dealing with a slow freeholder can stall a flip indefinitely.

- Mandate a Level 3 Survey: Never bypass a comprehensive structural survey (Level 3 RICS). Hidden defects such as Japanese Knotweed, severe subsidence, or the presence of spray foam insulation in the loft space can render a property entirely unmortgageable and financially ruinous.

- Secure Pre-Approved Finance: Do not search for properties without knowing your funding capacity. Engage a specialist commercial finance broker to understand the exact bridging rates, LTV limits, and exit strategy requirements you must adhere to.

- Stress-Test the Deal: When appraising a potential flip, apply a stress test. Recalculate your profit margin assuming the renovation takes two months longer than anticipated, costs 20% more, and the final ARV is 10% lower than your initial estimate. If the project remains profitable under these conditions, it is a viable investment.ment.

Stop being a landlord. Start being an investor.

Shaded Canvas introduces serious capital to vetted UK property opportunities — targeting 12–16% net returns.

Start Investing →