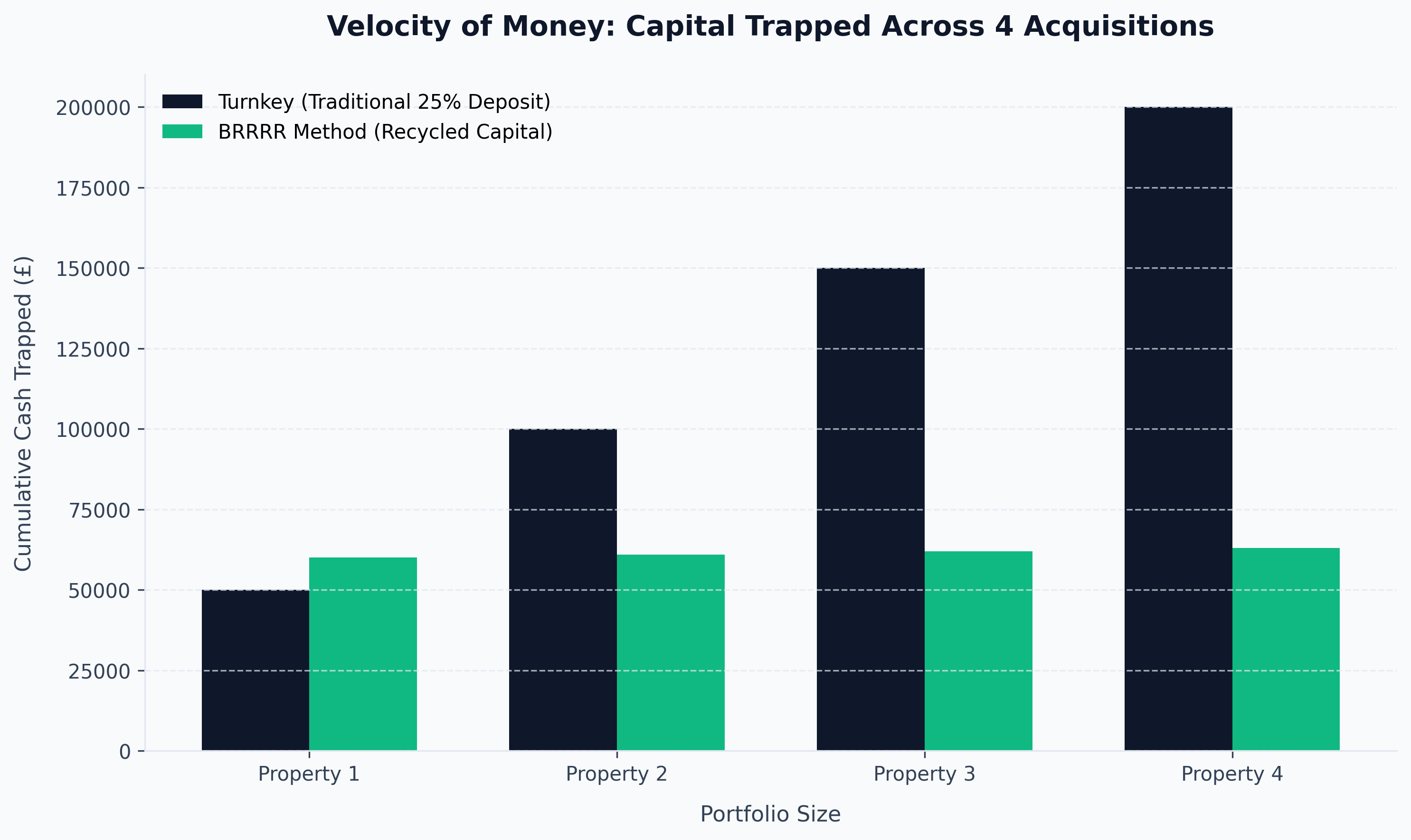

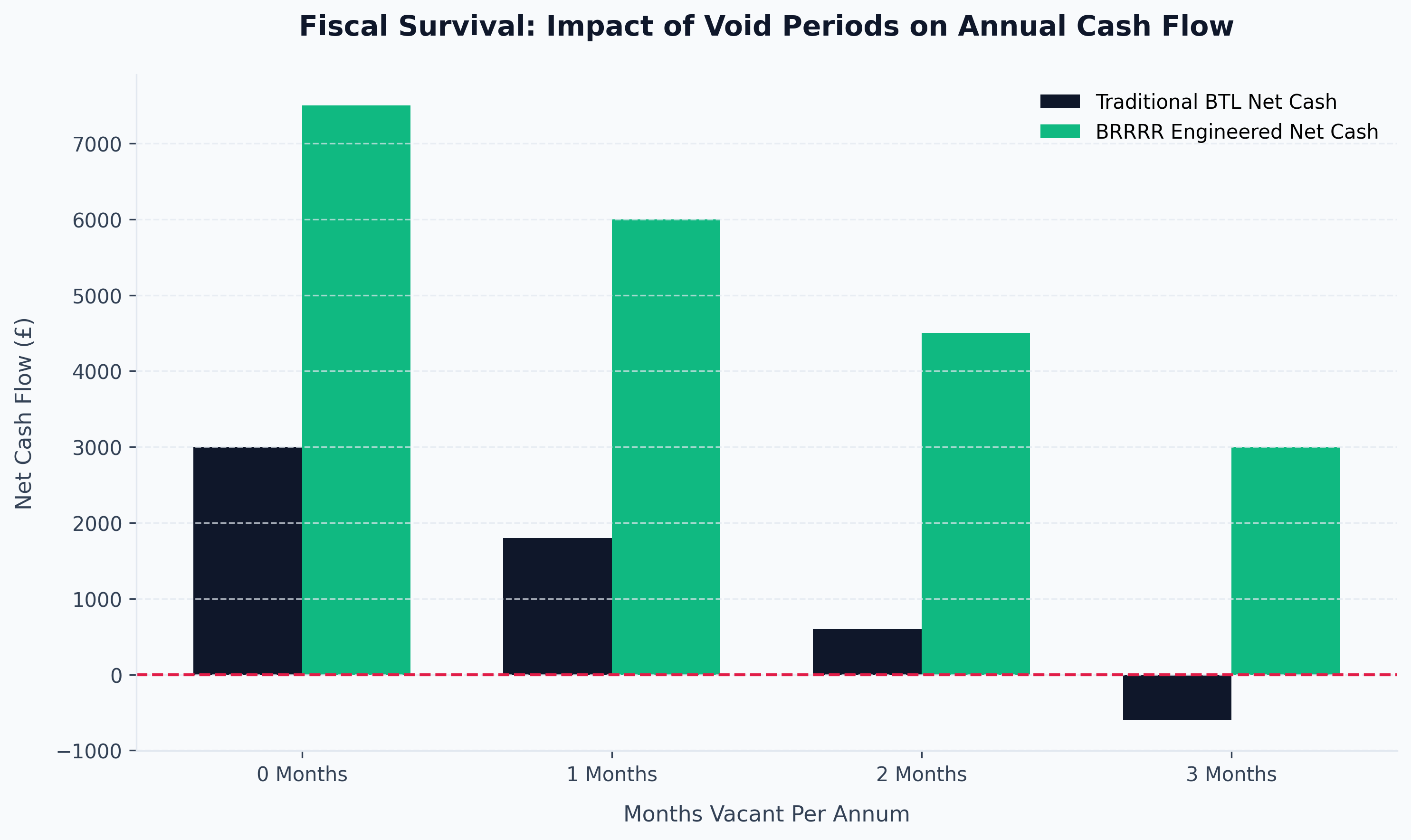

If you attempt to build a multi-million-pound UK property portfolio in 2026 using entirely your own liquid capital, you will fail. The mathematics of traditional, turnkey buy-to-let investing are structurally broken. If you acquire a £200,000 property using a standard £50,000 deposit, that capital is aggressively trapped inside the bricks for a decade, waiting for organic, macroeconomic inflation to silently bleed the equity back to you.

When Section 24 tax penalties, 5% interest rates, and soaring Service Charges annihilate your net yield, locking £50,000 away for £200 a month in cash flow is a commercial disaster.

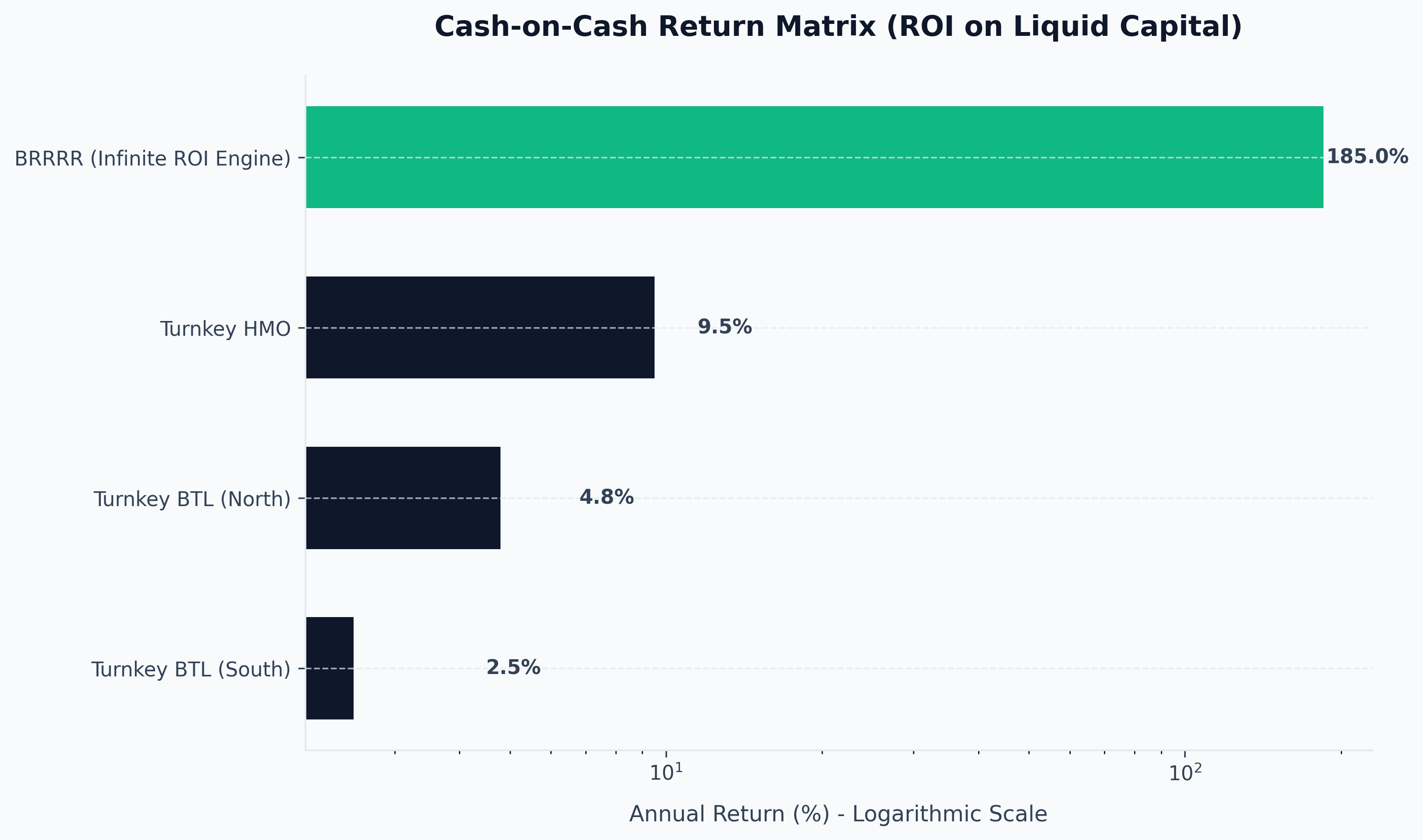

The elite tier of property investors completely bypass this slow-motion capital death. They do not leave their money in deals. They recycle it aggressively using the absolute pinnacle of high-velocity wealth generation: The BRRRR Strategy (Buy, Rehab, Rent, Refinance, Repeat).

However, the barrier to entry for BRRRR is not finding the distressed house; it is securing the hyper-specialized debt required to execute the transaction. This comprehensive guide will totally deconstruct exactly how to finance buy rehab rent refinance repeat transactions in the ruthless 2026 lending environment.

1. The Core Mechanics: Why Standard Mortgages Fail

Before deploying specialized capital, you must understand why traditional banking infrastructure fundamentally rejects the BRRRR methodology at step one.

When you locate a highly distressed asset—perhaps a burnt-out Victorian terrace, an abandoned commercial unit, or a house completely lacking a functional kitchen and bathroom—the seller will demand cash or ultra-fast completion.

If you apply for a standard Buy-to-Let (BTL) mortgage, the bank will send a surveyor. The surveyor will arrive, notice the property lacks a habitable kitchen or indoor plumbing, and declare it "Unmortgageable." A standard retail bank demands a "turnkey" asset generating immediate rental income to service the loan. They will instantly decline your application, and you will lose the deal.

To execute the "Buy" and "Rehab" phases of the BRRRR cycle, you need aggressive, short-term debt that actively embraces the destruction and reconstruction of the asset. You require Bridging Finance.

2. The "Buy" and "Rehab": Mastering Bridging Finance

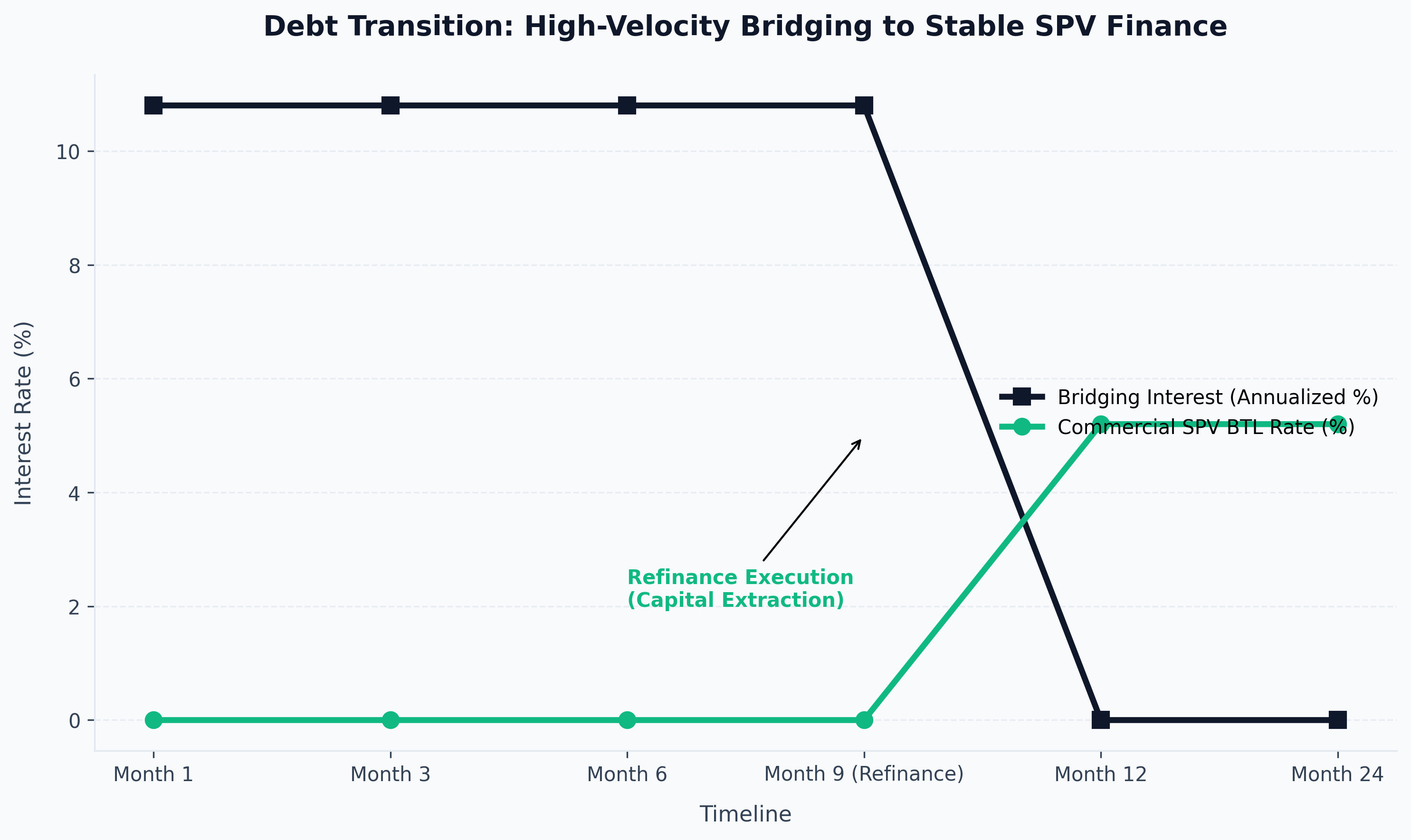

Bridging finance is short-term, expensive, institutional capital designed specifically to bridge the gap between acquiring an unmortgageable property and refinancing it onto a standard, long-term BTL mortgage once the asset is restored and fully tenanted.

In 2026, bridging lenders are incredibly sophisticated. They do not simply lend against the current value of the wreck; they lend against the mathematical probability of your future success.

Gross vs. Net Bridging Loans

When securing bridging finance, lenders structure the debt fundamentally differently from a retail mortgage. Because the property is empty and generating zero rent during the "Rehab" phase, you cannot physically make a monthly interest payment. Therefore, bridging lenders utilize Retained or Rolled-Up Interest.

- Gross Loan: The total amount of debt the lender creates on their books.

- Net Loan: The actual liquid cash physically transferred to your solicitor to buy the house.

The lender calculates 12 months of interest in advance (e.g., 0.9% per month), adds their 2% arrangement fee, and deducts this entire chunk of capital from the Gross Loan on day one. You do not make a single monthly payment during the rehab phase. The debt simply compounding silently in the background until the final refinance.

LTV vs. LTGDV

To safely finance a BRRRR, you must master the two critical acronyms governing the bridging underwriter's matrix:

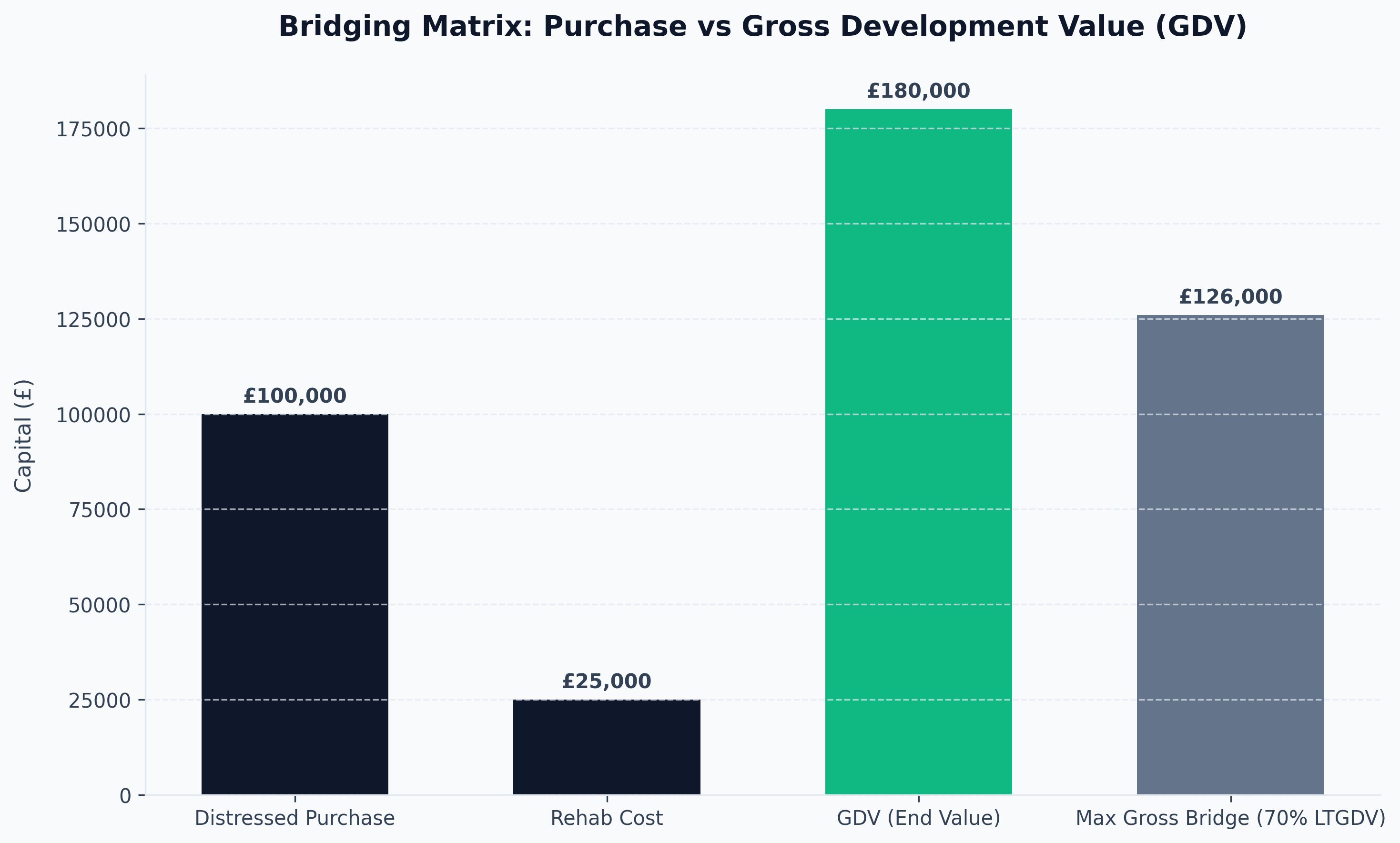

- LTV (Loan-to-Value): This dictates the maximum they will lend on Day One against the current, distressed valuation. In 2026, standard max bridging LTV is 70% to 75%. If you buy a wreck for £100,000, the absolute maximum Gross Loan is £75,000. Once fees and rolled-up interest are deducted, your Net Loan might only be £64,000. You must bring the remaining £36,000 (plus stamp duty and legals) in pure cash.

- LTGDV (Loan to Gross Development Value): This is the ultimate safety net for the lender. GDV is what the house will be worth after your rehab is finished. Lenders completely refuse to let their Gross Loan exceed 70% of the final LTGDV. If the numbers are too tight, they will brutally slash your Day One loan, forcing you to inject more cash.

The Refurbishment Drawdown Facility

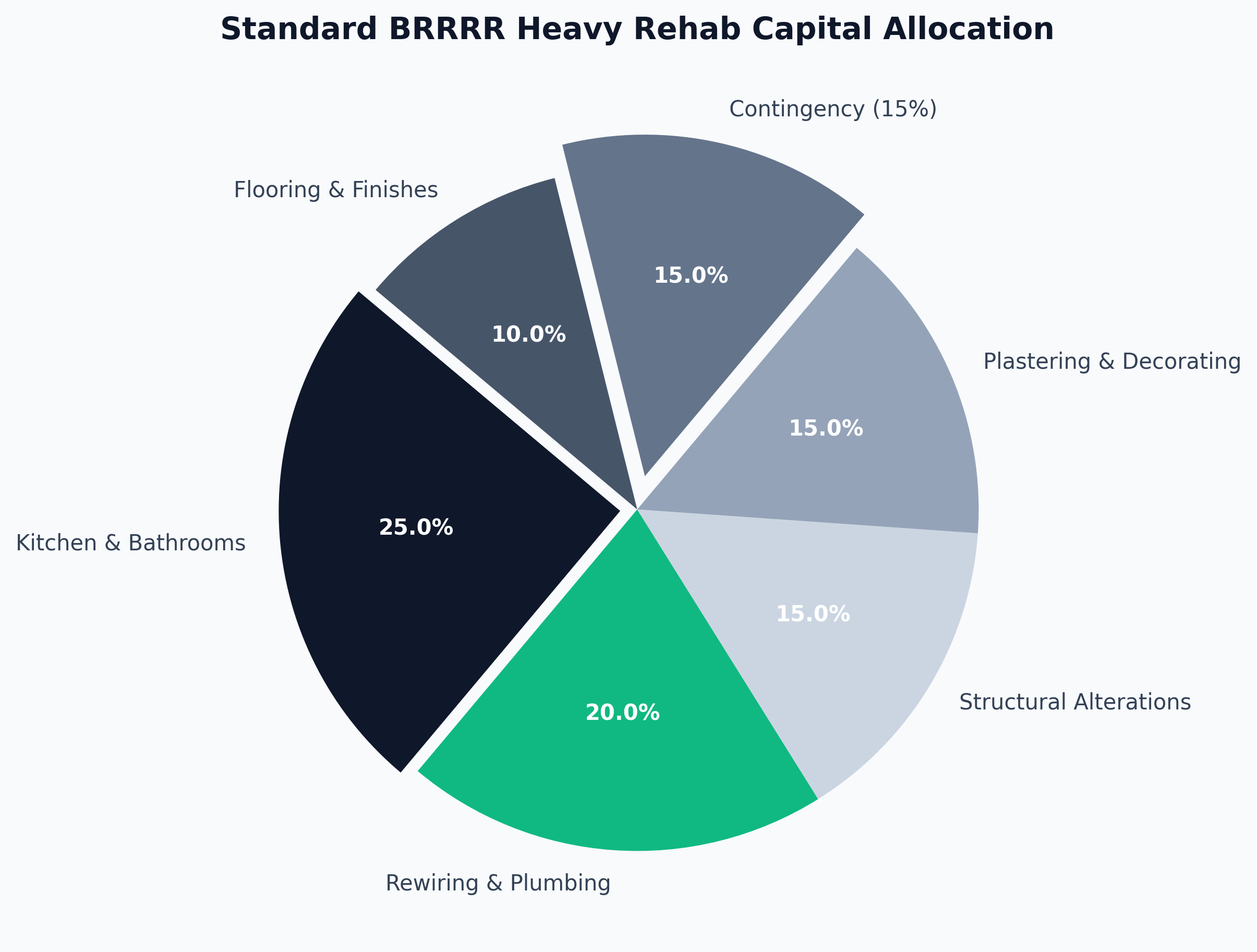

If you are executing a "Heavy Refurb" (e.g., structural extensions, loft conversions, HMO reconfigurations), your rehab costs might exceed £50,000. You do not have to deploy 100% of your own cash for the build. Elite lenders offer 100% Build Cost Funding deployed via a drawdown facility. You buy the asset utilizing the 70% LTV on day one. You deploy £15,000 of your own cash to complete Phase 1 of the build (e.g., ripping the roof off and water-tightening). The bank's Asset Manager inspects the site, verifies the value added, and instantly wires you your £15,000 back to deploy into Phase 2.

3. The "Rent": Forcing the Commercial Valuation

You have successfully acquired the distressed asset using a bridge. You deployed your £30,000 CapEx budget. The house is now a stunning, high-yielding 6-bedroom HMO or a beautiful family AST.

Before you trigger the "Refinance" phase, you must execute the "Rent" phase with absolute precision. A property with a signed tenancy agreement is a commercial asset; an empty, finished house is a high-risk liability.

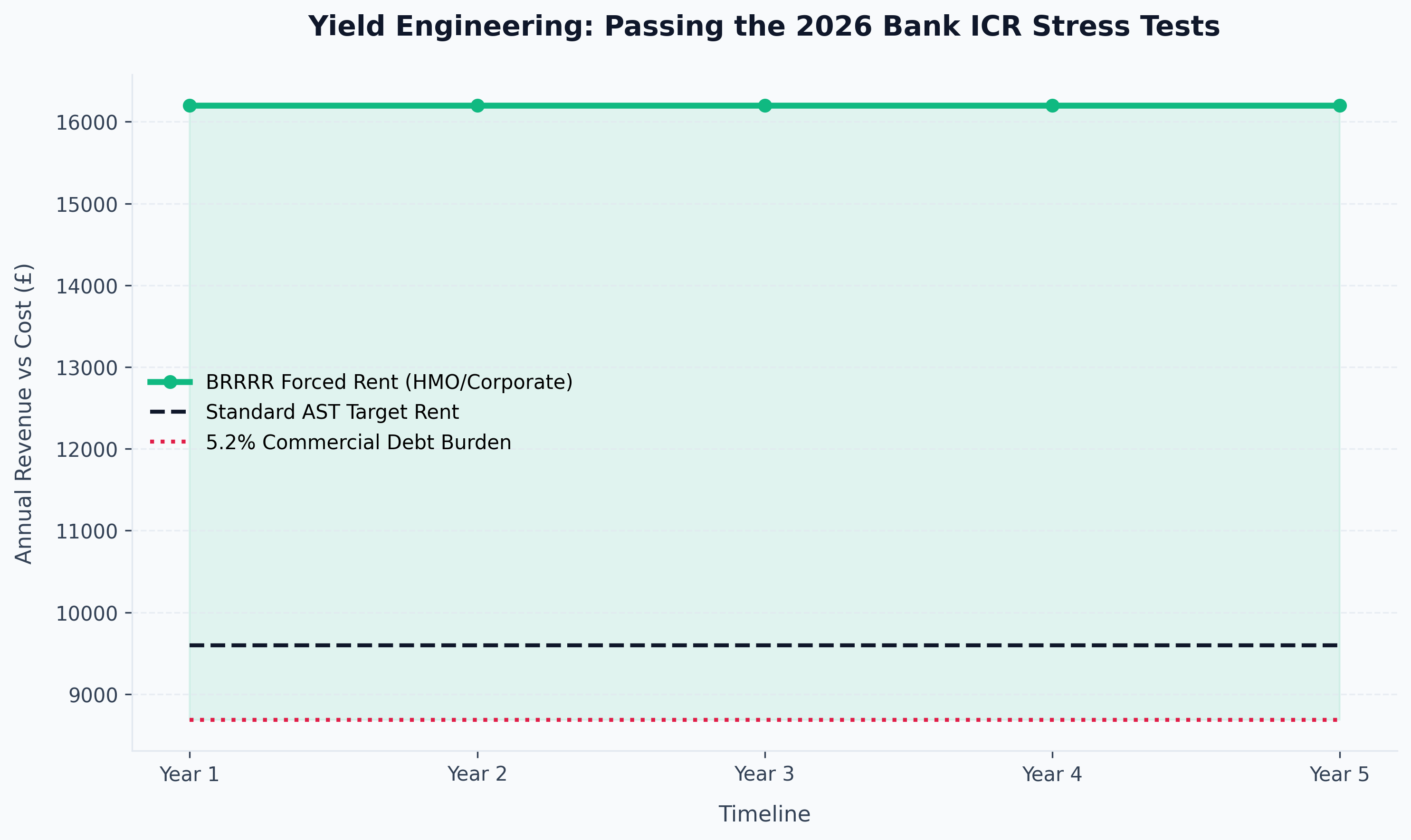

The Yield Engineering

In 2026, when you refinance the property, the incoming long-term mortgage lender (the bank buying out your expensive bridging loan) will mandate a drastic stress test. To pass this Interest Coverage Ratio (ICR) test at 5.5% interest rates, your Gross Rent must be artificially engineered as high as possible. Do not accept standard market rent. You must furnish the property aggressively, include hyper-fast commercial broadband, and target corporate lets to violently push the monthly rental income. The higher the rent, the higher the commercial valuation the surveyor can justify, and the more capital you can physically extract.

4. The "Refinance": Extracting the Initial Capital

This is the entire point of the strategy. The Refinance phase is where you execute the legalized magic trick of infinite cash-on-cash return.

You must transition the property away from the expensive 1% per month Bridging Loan, onto a stable, 5-year fixed 5.2% commercial Buy-to-Let mortgage inside your Limited Company (SPV).

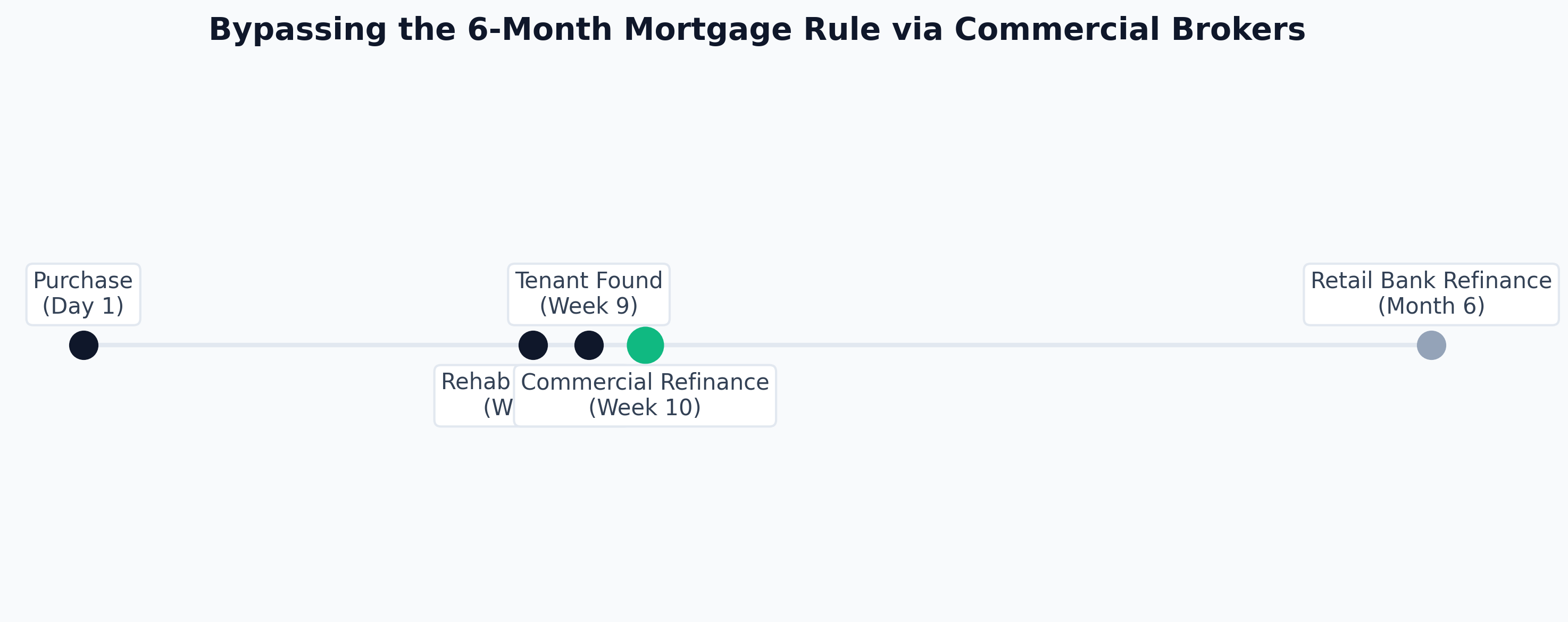

The Six-Month Rule Mitigation

Historically, the UK mortgage market was governed by the "Six-Month Rule," arbitrarily preventing investors from refinancing a property within six months of the original purchase date (to prevent money-laundering via rapid flipping). In 2026, this rule still exists broadly across High Street retail banks. However, specialized, broker-access-only commercial lenders actively waive the six-month rule explicitly for BRRRR investors. If you finish your rehab in 8 weeks and tenant it in week 9, you can refinance and extract your cash in week 10. You must execute the original purchase using the correct commercial lender network via an elite broker, otherwise you will be trapped on expensive bridging rates until month seven.

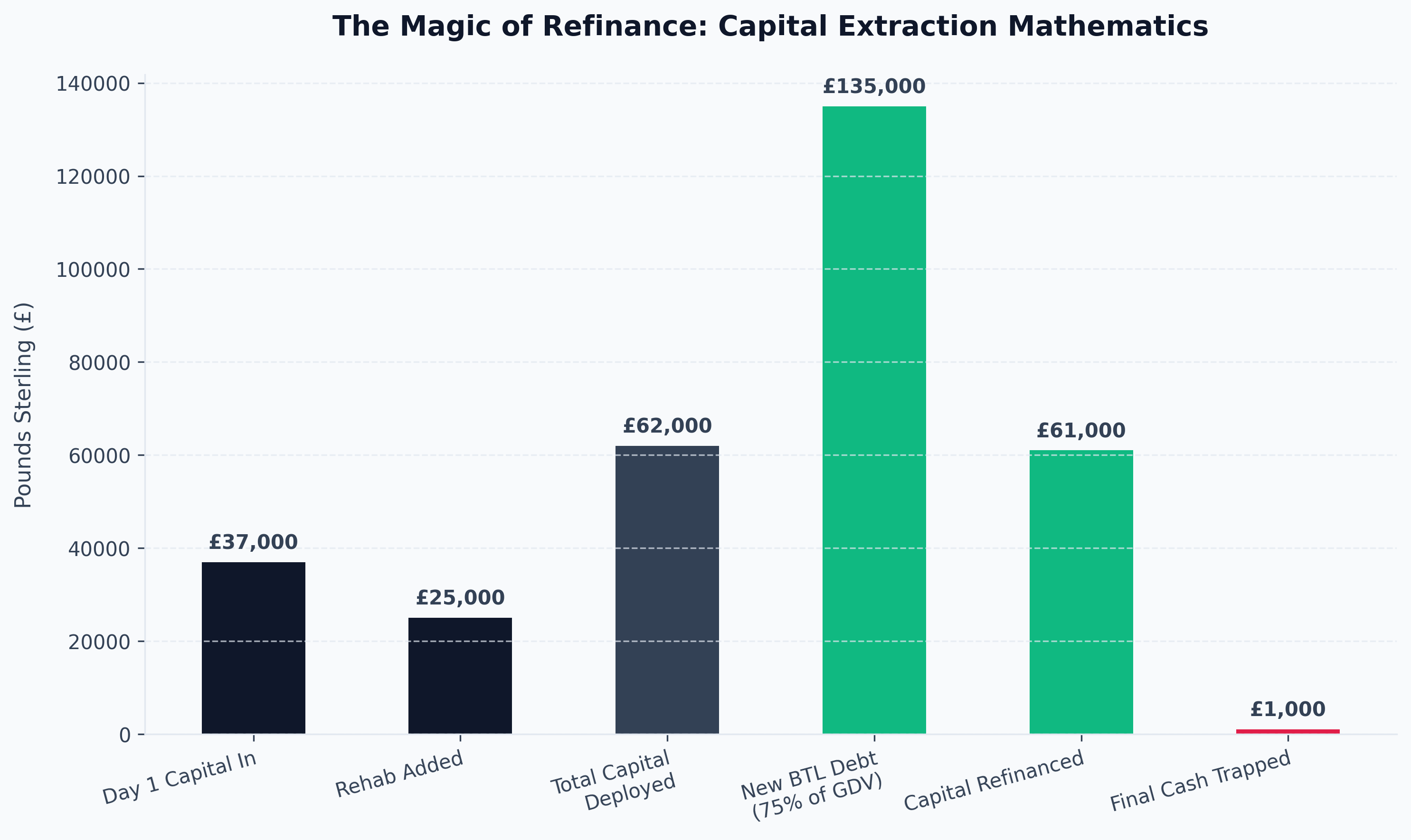

The Extraction Mathematics (The Holy Grail)

Let's brutally break down the numbers of a successful BRRRR capital extraction:

- Purchase Price (Distressed): £100,000

- Buying Costs (SDLT + Legals + Broker): £7,000

- Rehab Costs (New kitchen, bathroom, rewire): £25,000

- Total Capital Deployed (If Cash): £132,000

Instead of using £132,000 of your own cash, you used Bridging Finance at 70% LTV.

- Your Day-One Cash Injection: £30,000 (Deposit) + £7,000 (Fees) + £25,000 (Rehab) = £62,000 of your liquid cash deployed.

Three months later, the rehab is complete. The tenant is paying £950 per month. The surveyor arrives and confirms your aggressive refurbishment has forced the End Value (GDV) of the property up to £180,000. You apply for a new, long-term 75% LTV BTL Mortgage against the new £180,000 valuation.

- New Mortgage Size: £135,000 (75% of £180,000)

- Payoff the Bridge + Rolled Interest: -£74,000

- Cash Remaining to YOU: £61,000

You deployed £62,000 of your own cash. You extracted £61,000 upon refinance. You successfully left only £1,000 trapped in a high-yielding, appreciating asset generating infinite, perpetual net cash flow.

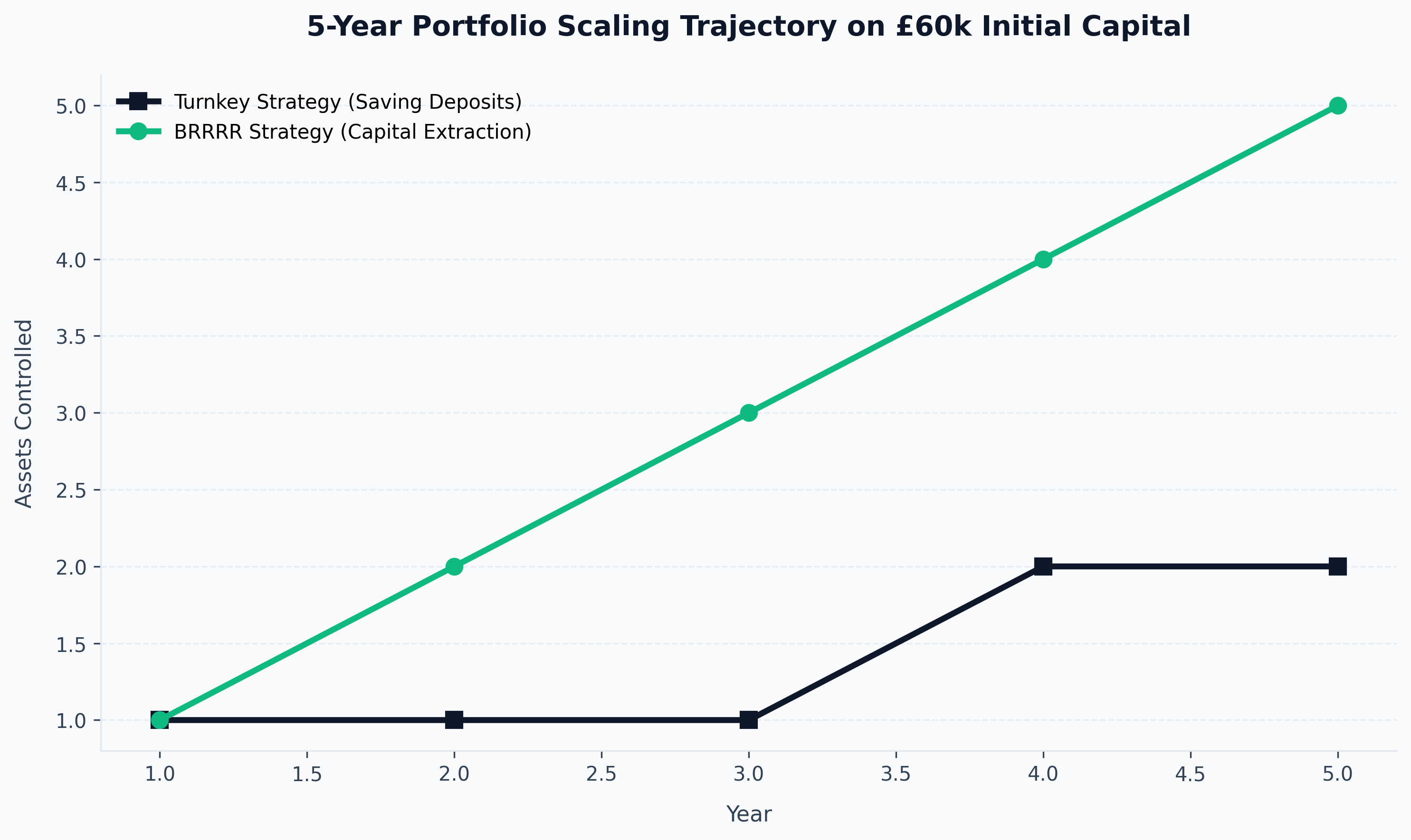

5. The "Repeat": Scaling Velocity

When you extract your capital in the BRRRR cycle, it is completely tax-free. You are not selling the asset (which triggers Capital Gains Tax); you are simply drawing down new debt against the newly created equity. Debt is not a taxable event.

You take that £61,000 and instantly deploy it into Property Number Two. Then Property Number Three. Instead of taking 15 years to save enough retail deposits from your 9-to-5 salary to buy three houses, you utilized the exact same £60,000 chunk of capital to acquire three houses in 18 months.

Engineering the Next Acquisition

The hardest phase of "Repeat" is maintaining the discipline required to not deploy compromised capital. In a brutal 2026 market, many investors fail the repeat phase because they overpay for their second acquisition out of sheer impatience, failing to force the 20% equity margin required to extract all their cash. If you leave £15,000 trapped in deal two, and £25,000 trapped in deal three, your capital velocity grinds to a halt. You must execute deals fundamentally below market value, or the mathematics of the refinance will severely punish you.

Conclusion: The Ultimate Portfolio Strategy

Learning how to finance buy rehab rent refinance repeat transactions is the absolute dividing line between amateur landlords and institutional wealth builders. Traditional banking wants you to slowly park capital for 25 years. Bridging and commercial SPV structuring allows you to violently accelerate that timeline.

Master the bridging debt. Force the GDV equity through aggressive refurbishment. Negotiate the commercial six-month refinance waiver via a specialized broker. Extract the capital tax-free. Repeat until entirely financially detached.

Stop being a landlord. Start being an investor.

Shaded Canvas introduces serious capital to vetted UK property opportunities — targeting 12–16% net returns.

Start Investing →