Financing a multi-let property, whether a House in Multiple Occupation (HMO) or a Multi-Unit Freehold Block (MUFB), requires a sophisticated understanding of the UK's evolving lending landscape in 2026. As the market adapts to new regulatory frameworks, including the Renters' Rights Bill, and changing interest rate environments, investors must approach multi-let finance with precision and robust financial planning. This comprehensive guide details the strategies, criteria, and nuances of securing the optimal commercial mortgage or HMO mortgage for your portfolio.

Understanding the Multi-Let Landscape in 2026

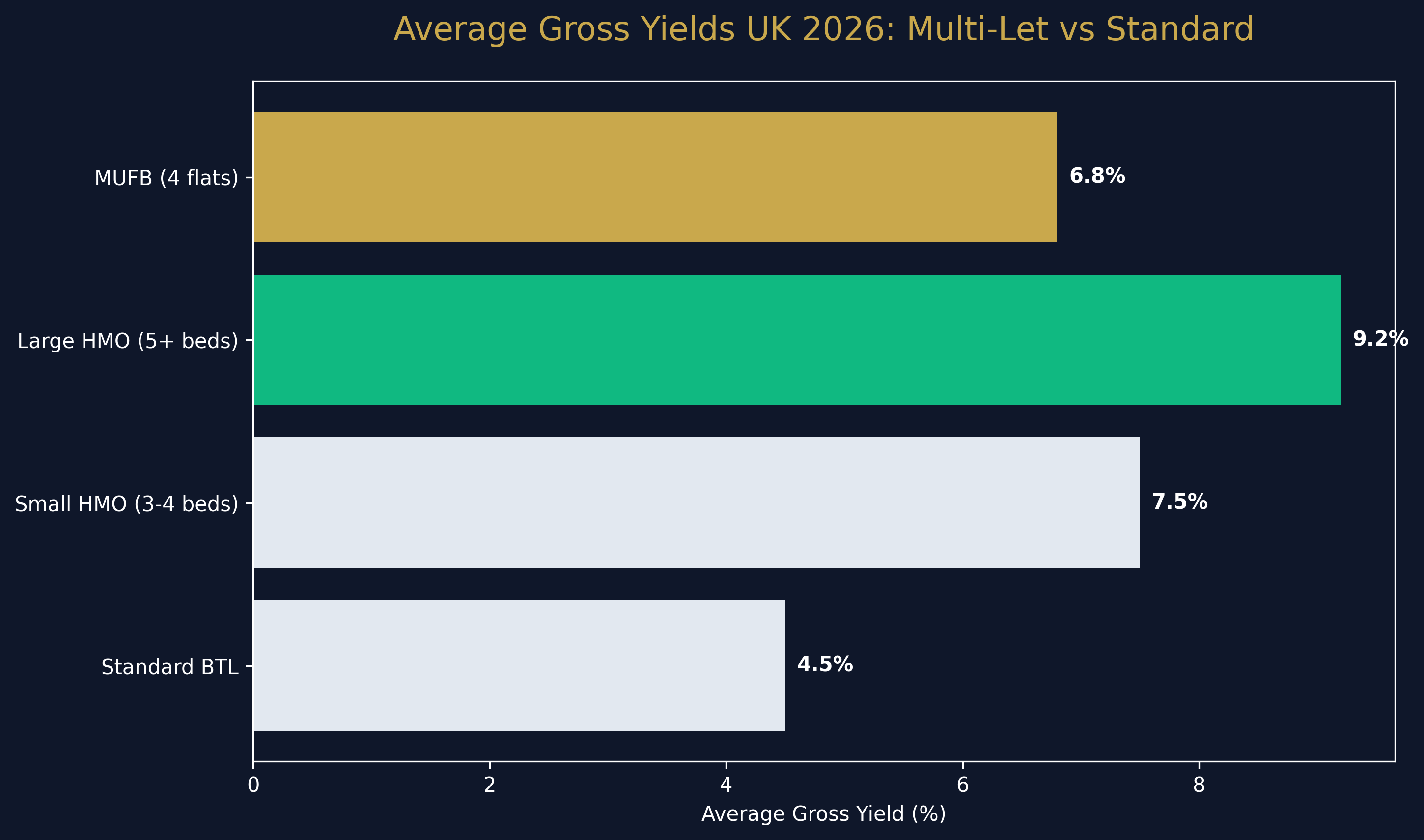

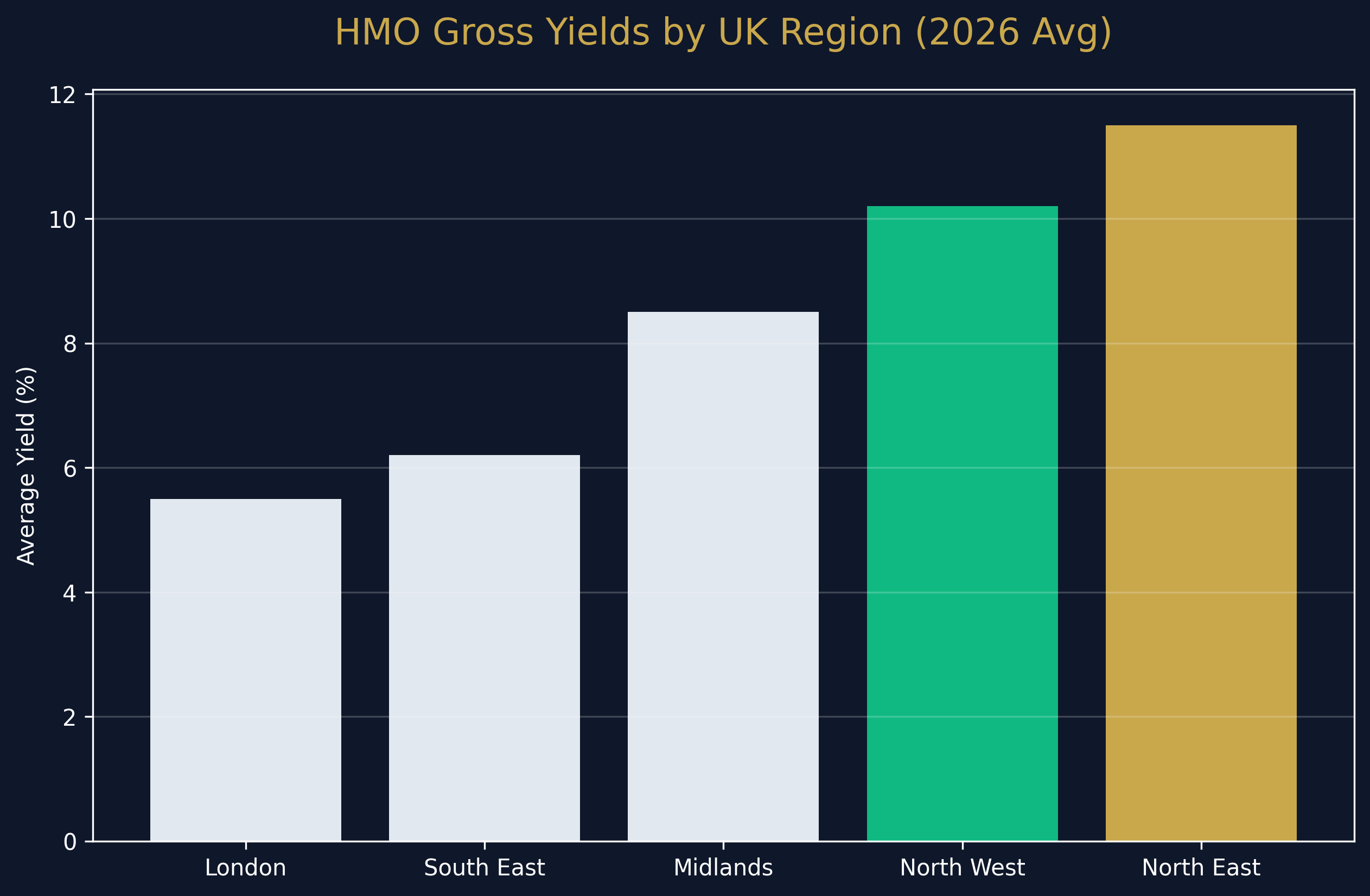

The appeal of multi-let properties lies primarily in their potential for higher gross yields compared to standard buy-to-let (BTL) investments. By renting out individual rooms or self-contained units, investors can mitigate void periods and maximize cash flow. However, lenders view these assets through a different risk prism.

The two primary categories of multi-let properties are:

- HMOs (Houses in Multiple Occupation): Properties rented by at least three unrelated tenants sharing facilities. These often require specific local authority licensing.

- MUFBs (Multi-Unit Freehold Blocks): Single freehold properties divided into multiple self-contained units, such as a block of flats.

The financing structures for these two asset classes, while similar in some underwriting principles, diverge significantly in application and lender appetite. A commercial mortgage may be required for larger MUFBs or mixed-use properties, while specialist HMO mortgages dominate the shared living space.

The Core Financing Options

When constructing your capital stack for a multi-let acquisition or refinancing, you generally have access to several specialized products. Unlike residential mortgages, these products emphasize the asset's income-generating capability, usually scrutinized through the Interest Coverage Ratio (ICR).

1. Dedicated HMO Mortgages

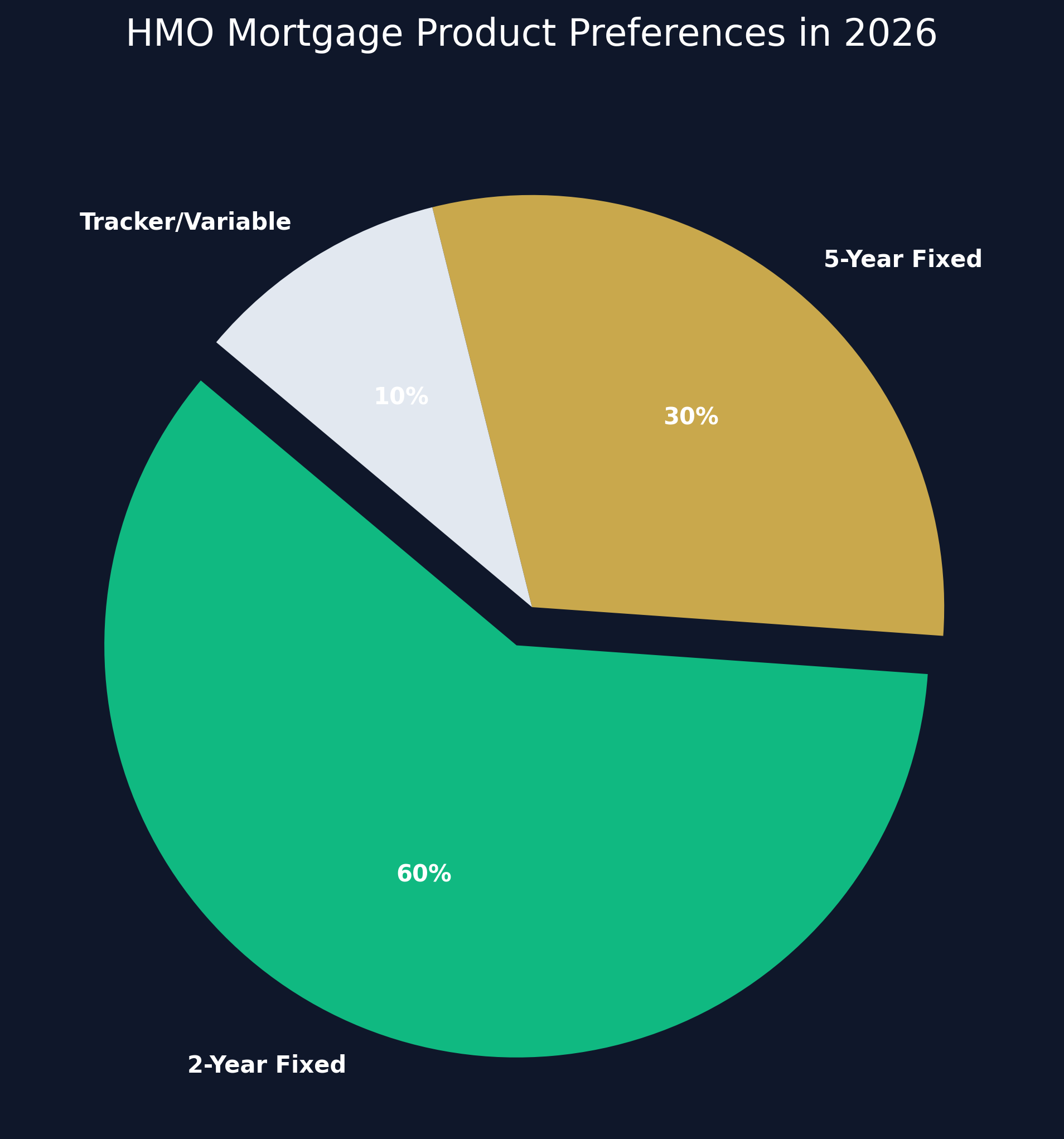

An HMO mortgage is bespoke to the shared-living model. Given the higher turnover of tenants and increased management intensity, lenders price these products slightly higher than standard BTLs—typically 0.1% to 1.5% above standard rates.

In 2026, we are seeing 2-year fixed rates starting around 4.5% at 75% LTV, depending on the borrower's profile and the property's energy performance (EPC). Lenders will heavily scrutinize the property's compliance with local licensing laws and fire safety regulations.

2. Multi-Unit Freehold Block (MUFB) Mortgages

MUFB mortgages are designed for investors holding multiple self-contained flats under a single freehold. Because the risk of total void is lower (if one tenant leaves, the others still pay rent), the risk profile is different.

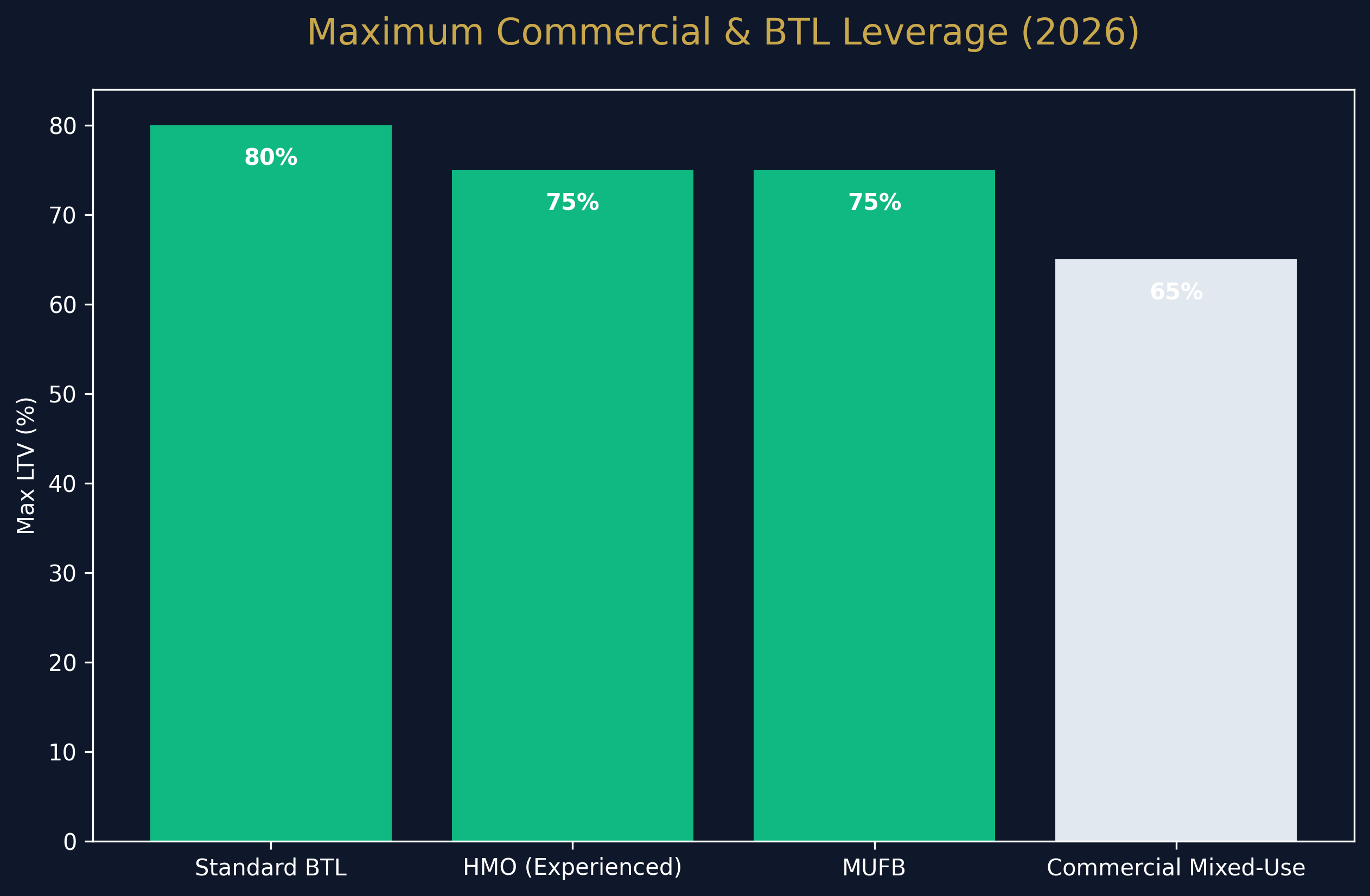

These mortgages are characterized by slightly more expensive rates than single-unit BTLs but offer the convenience of financing an entire block under one facility. A 25% deposit is standard, though experienced portfolio landlords might access up to 80% LTV under certain conditions.

3. Commercial Mortgages

For properties exceeding typical residential lender limits (e.g., MUFBs with more than 6 to 10 units, or properties with ground-floor commercial space), a true commercial mortgage is necessary. Commercial mortgages are underwritten on the strength of the asset, the borrower's track record, and the broader economic viability of the location.

Yield and Debt Service Coverage Ratio (DSCR) become the paramount metrics here, moving away from standard residential affordability models.

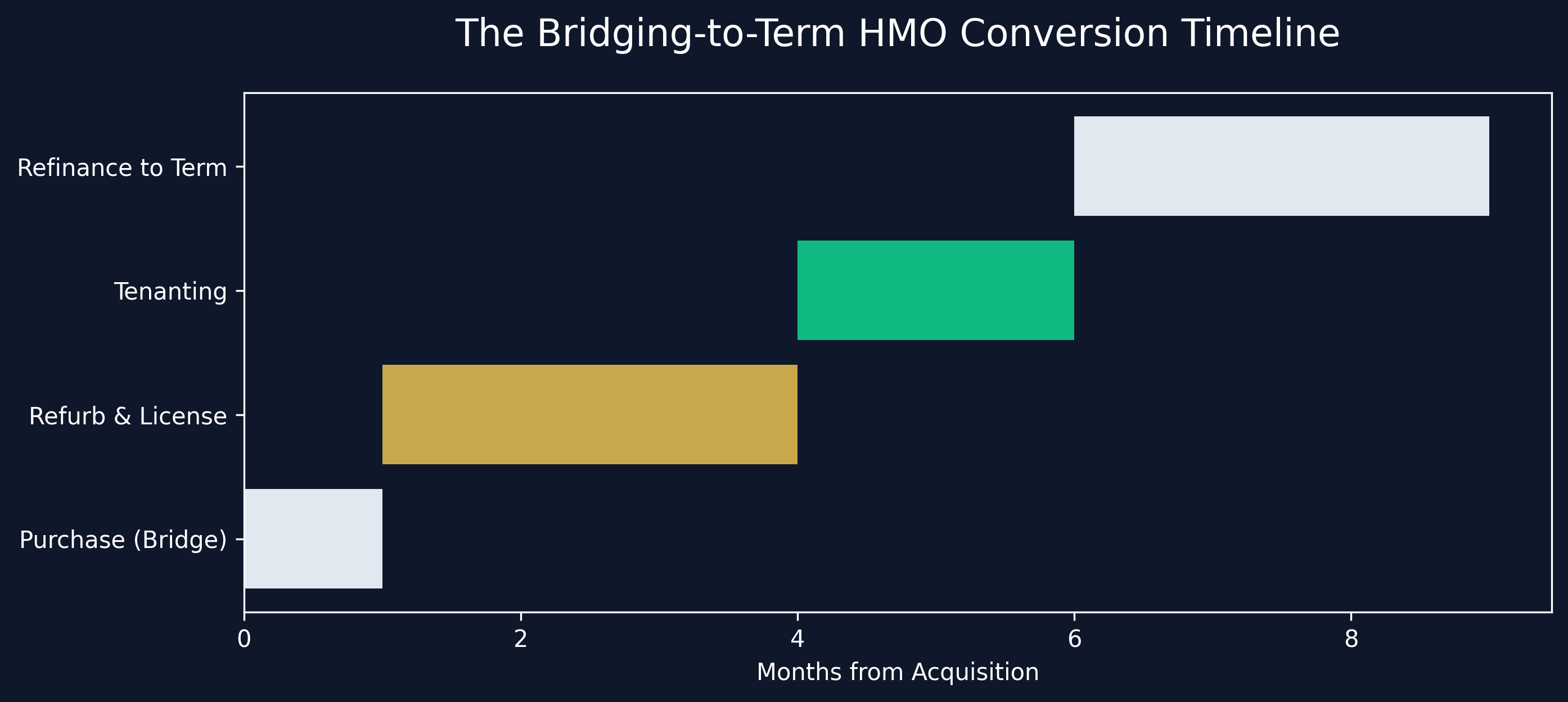

4. Bridging Finance for Conversion

If you are purchasing a standard family home (C3 use class) to convert into an HMO (C4 or Sui Generis), standard mortgage lenders will not lend on the property in its unconverted state if you intend to gut it.

Bridging finance provides short-term capital (typically 6 to 18 months) to purchase and develop the asset. Once the property is converted, licensed, and tenanted, you can refinance onto a long-term HMO mortgage based on the new, higher commercial valuation.

Navigating Lender Criteria in 2026

The lending environment in 2026 is defined by stringent underwriting, heavily influenced by the new Renters' Rights Bill. Lenders are more focused than ever on the durability of rental income.

Experience Requirements

The majority of specialist lenders require a proven track record. For HMO mortgages, a minimum of 12 months' experience as a standard BTL landlord is often a prerequisite. However, the market has seen some lenders relax this for "first-time HMO landlords" provided they utilize a professional, ARLA-registered letting agent to manage the property.

For MUFBs, experience is almost universally required, given the complexities of block management and potential freehold/leasehold dynamics.

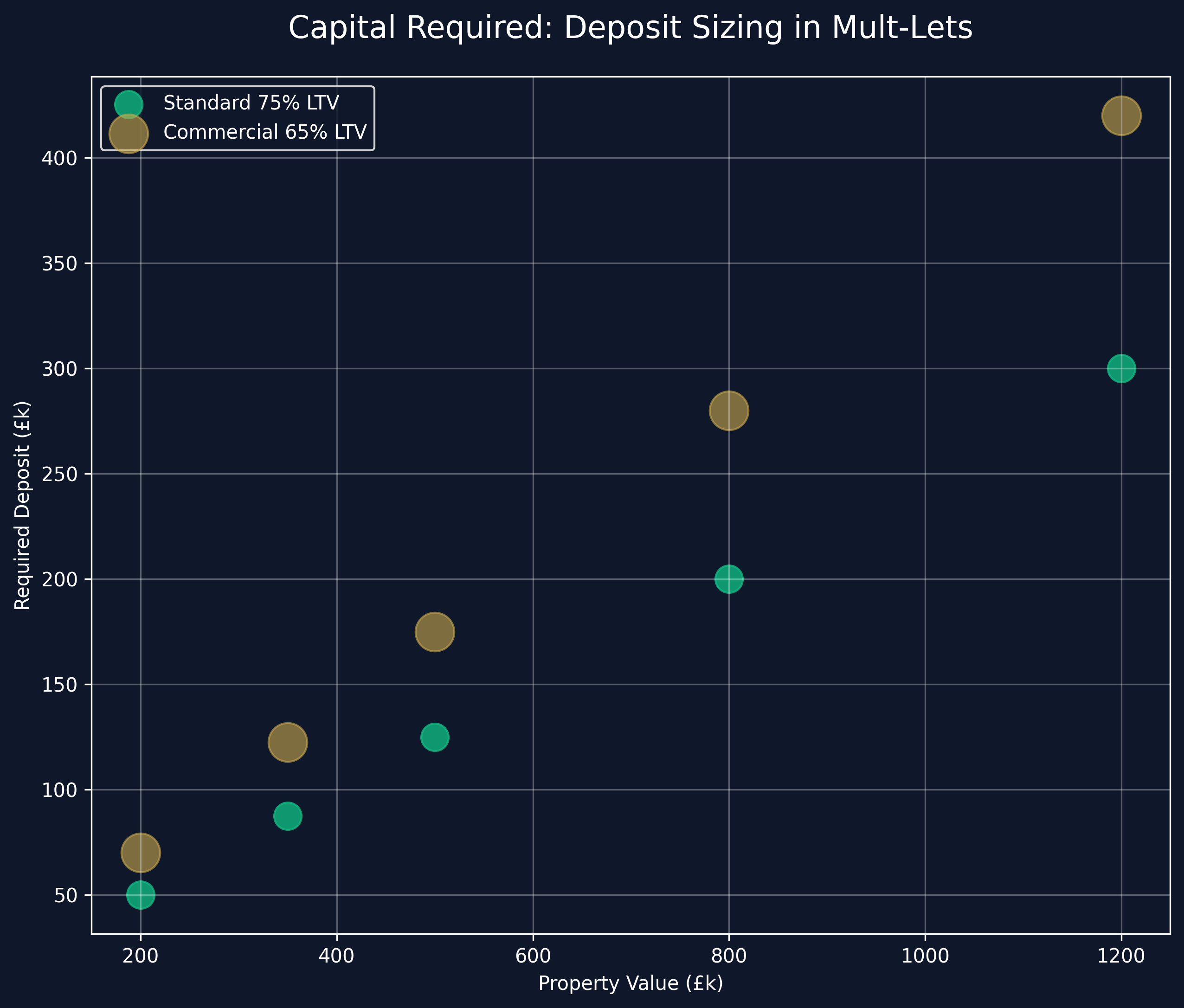

Deposit Requirements and LTV

Leverage is the double-edged sword of property investment. For multi-let properties, expect to put down a minimum deposit of 25% (a 75% LTV). While 80% LTV products exist, they usually come with punitive interest rates and are reserved for prime assets in top-tier locations.

When converting a property into an HMO using bridging finance, lenders might offer 70-75% Loan-to-Gross-Development-Value (LTGDV), ensuring your capital is appropriately deployed against the end asset value.

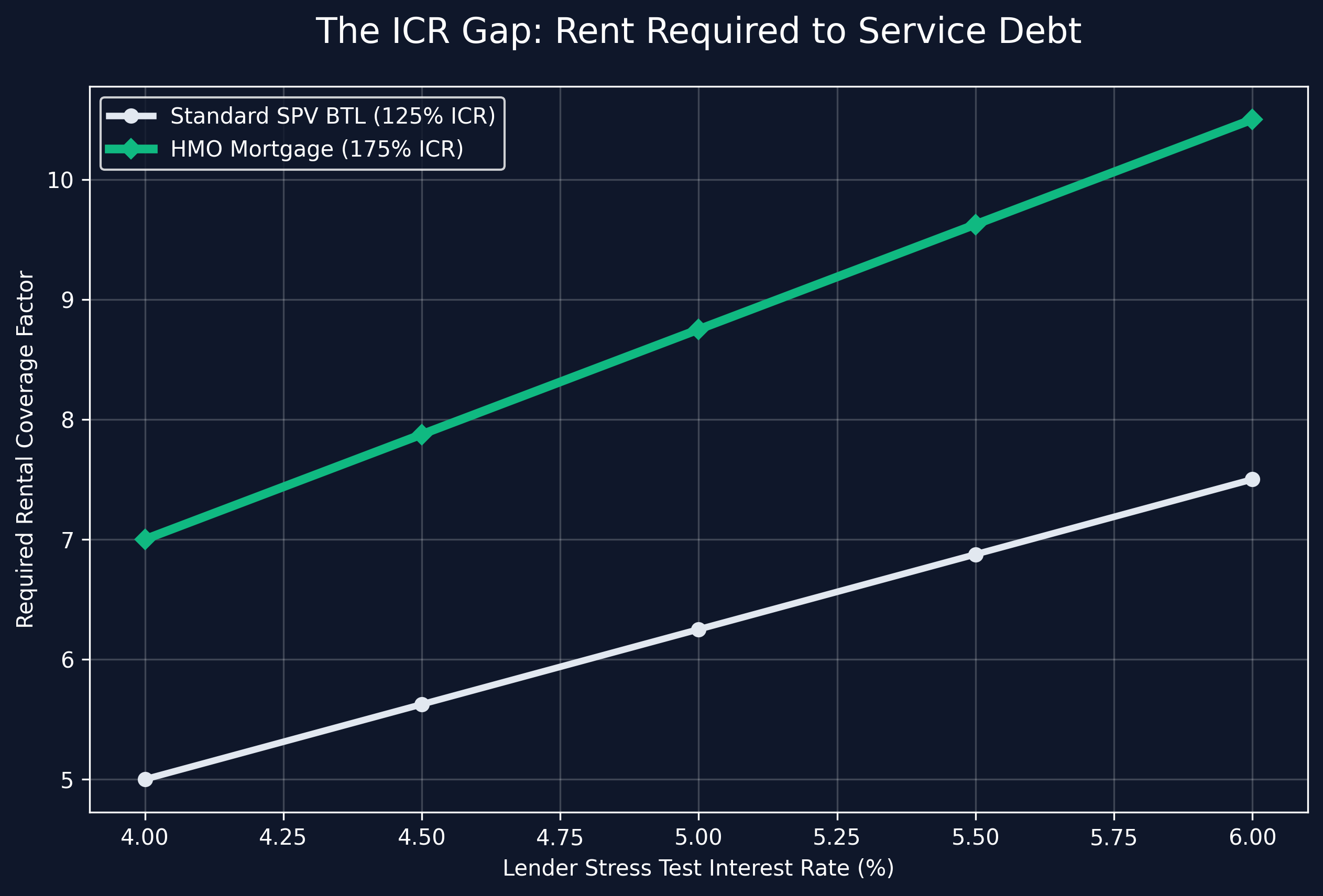

The Role of Yield and ICR

The Interest Coverage Ratio (ICR) is the ultimate gatekeeper in multi-let finance. Lenders mandate that the rental income must comfortably cover the mortgage interest, stressed at a hypothetical higher rate.

For standard BTLs, an ICR of 125% to 145% is common. For HMOs, lenders routinely apply a 170% to 175% ICR. This means your gross rental income must be at least 175% of your mortgage interest payment, calculated at the stress rate (often 5.5% or higher). This strict ICR calculation is precisely why the high yield of a multi-let is necessary; a standard single-let property would fail this stress test on a high LTV.

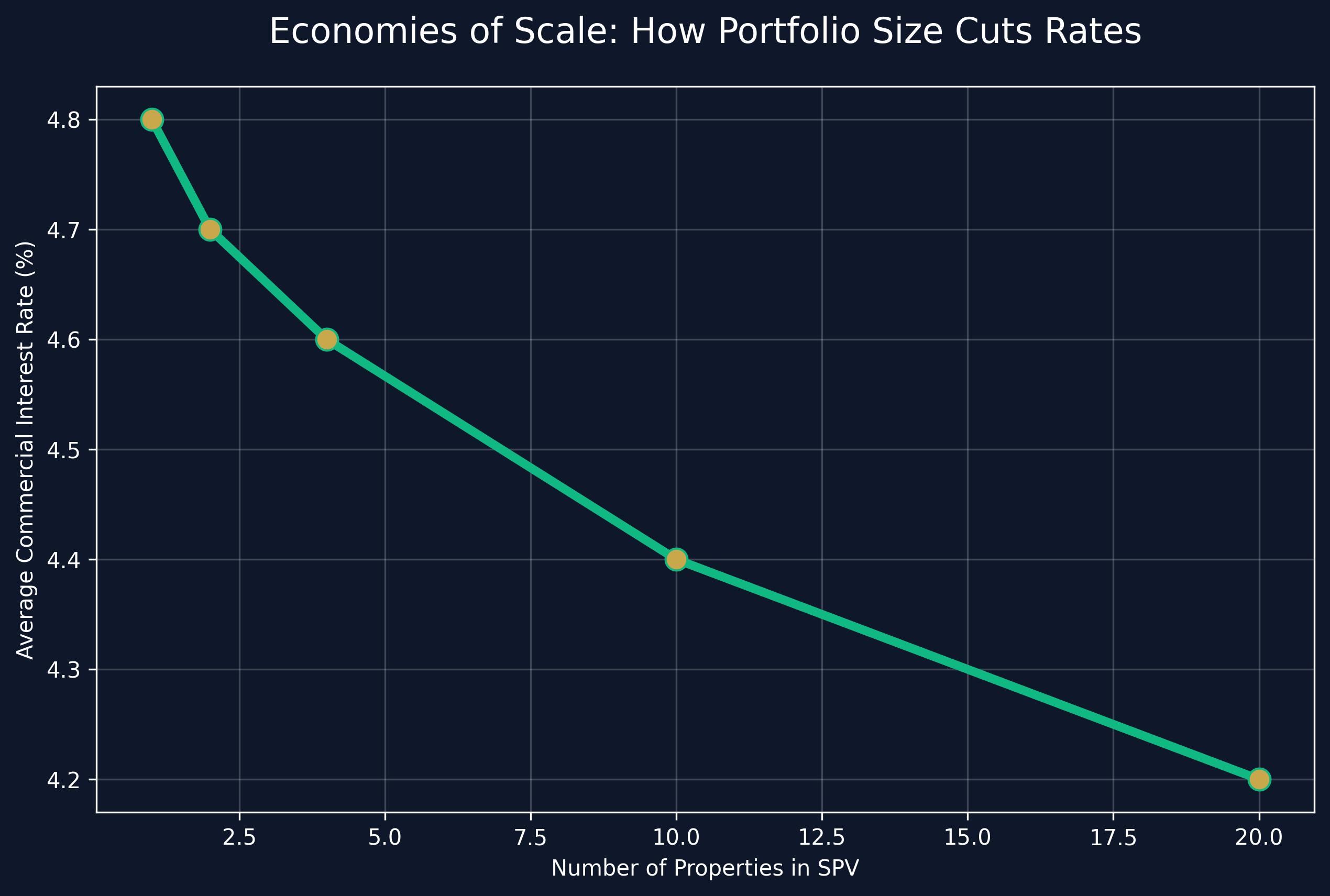

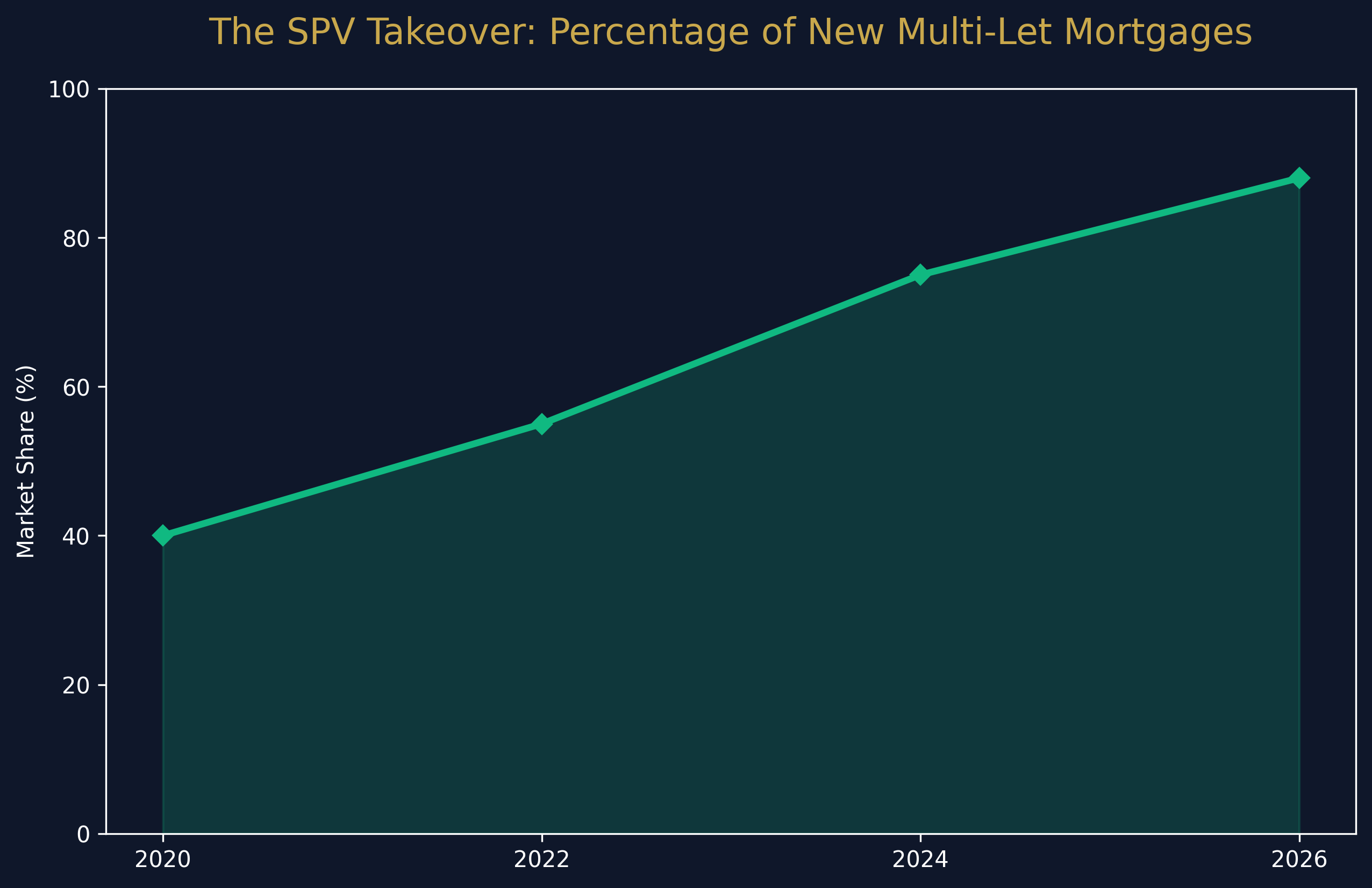

The Impact of Corporate Structures

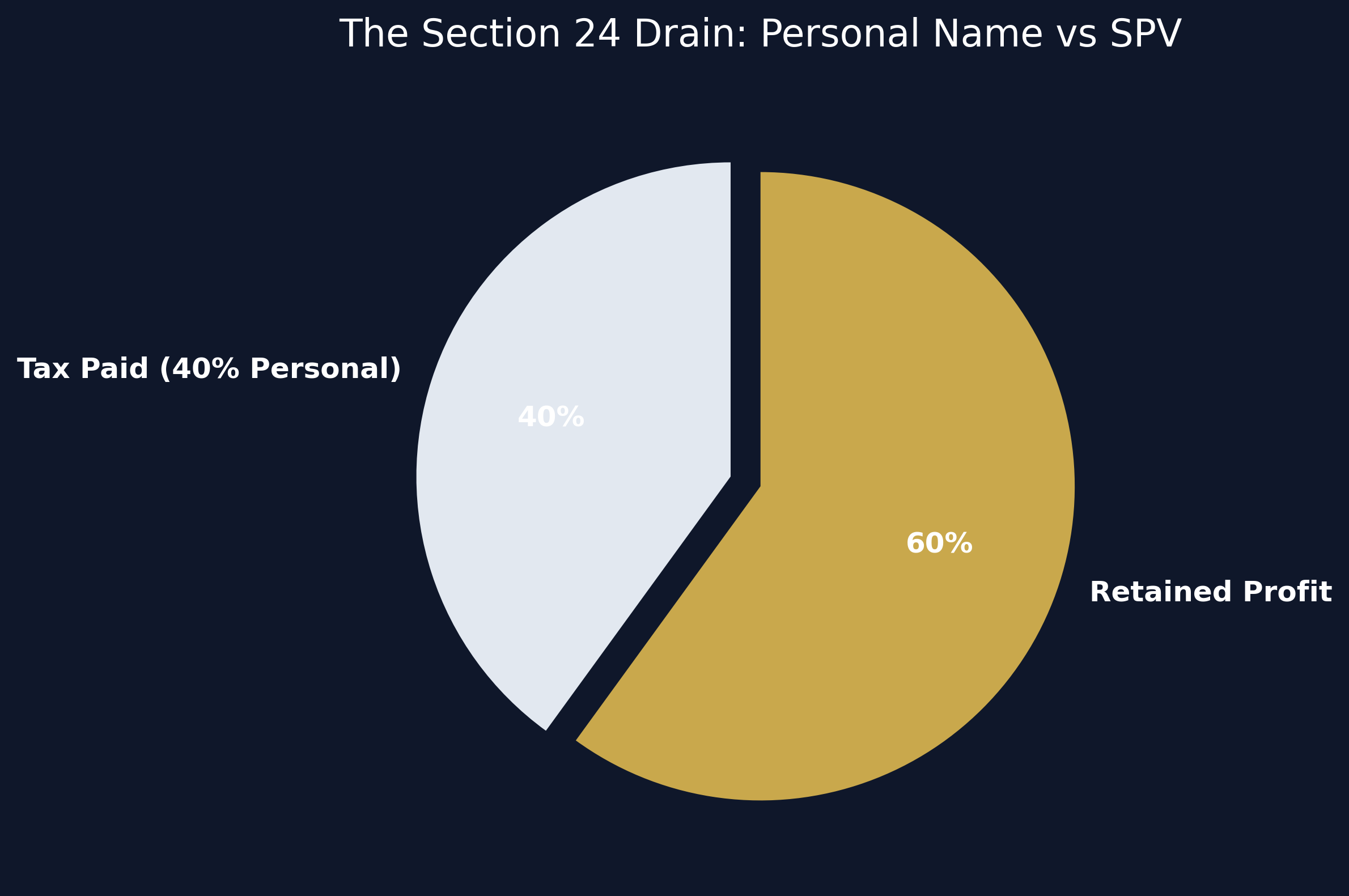

A definitive trend in 2026 is the dominance of Limited Company (Special Purpose Vehicle - SPV) borrowing. Section 24 of the Finance Act effectively eliminated mortgage interest tax relief for higher-rate taxpayers owning property in their personal names.

By financing a multi-let property through an SPV, investors can offset 100% of their mortgage interest against Corporation Tax (currently 19% to 25%, depending on profits).

Lenders are exceptionally comfortable with SPV lending. However, directors will universally be required to sign personal guarantees (PGs), meaning your personal assets remain on the line should the SPV default. Furthermore, the ICR stress tests are often slightly more lenient for SPVs (e.g., 125% instead of 145%), recognizing the tax efficiency of the structure.

Summary Checklist for Financing a Multi-Let

- Define the Asset: Are you buying an operational HMO, a MUFB, or an unencumbered house for conversion?

- Assess Your Experience: Ensure your landlord CV meets the 12-month requisite for specialist lenders.

- Calculate the ICR: Run rigorous stress tests at 5.5% interest and 175% ICR to ensure the property qualifies for the required leverage.

- Incorporate an SPV: Consult with a tax advisor to establish a Limited Company for the acquisition.

- Engage a Specialist Broker: The high street is rarely the place for multi-let finance. Utilize a broker with direct access to the specialist commercial and HMO lending panels.

By understanding these mechanisms, investors can effectively leverage capital, maximize their yield, and build a robust, cash-flowing portfolio in the complex but rewarding 2026 UK property market.

Stop being a landlord. Start being an investor.

Shaded Canvas introduces serious capital to vetted UK property opportunities — targeting 12–16% net returns.

Start Investing →