Land sourcing is the specialist end of the UK property sourcing industry: identifying plots and sites with development potential, assessing their planning prospects, and connecting them to housebuilders, developers or investors before they reach the open market. It sits alongside, but is meaningfully different from, standard property sourcing, which deals in finished or nearly-finished residential stock rather than raw or semi-developed land.

This guide sets out how land sourcing actually works in the UK in 2025 and 2026: the data sources and software sourcers use, who buys the land they find, what they typically earn, and the legal and compliance obligations that apply whether you are sourcing a half-acre infill plot or a 40-acre strategic land parcel. It is written for two audiences: people considering land sourcing as a business, and investors or small developers trying to work out whether a land sourcer is worth paying.

Executive Summary

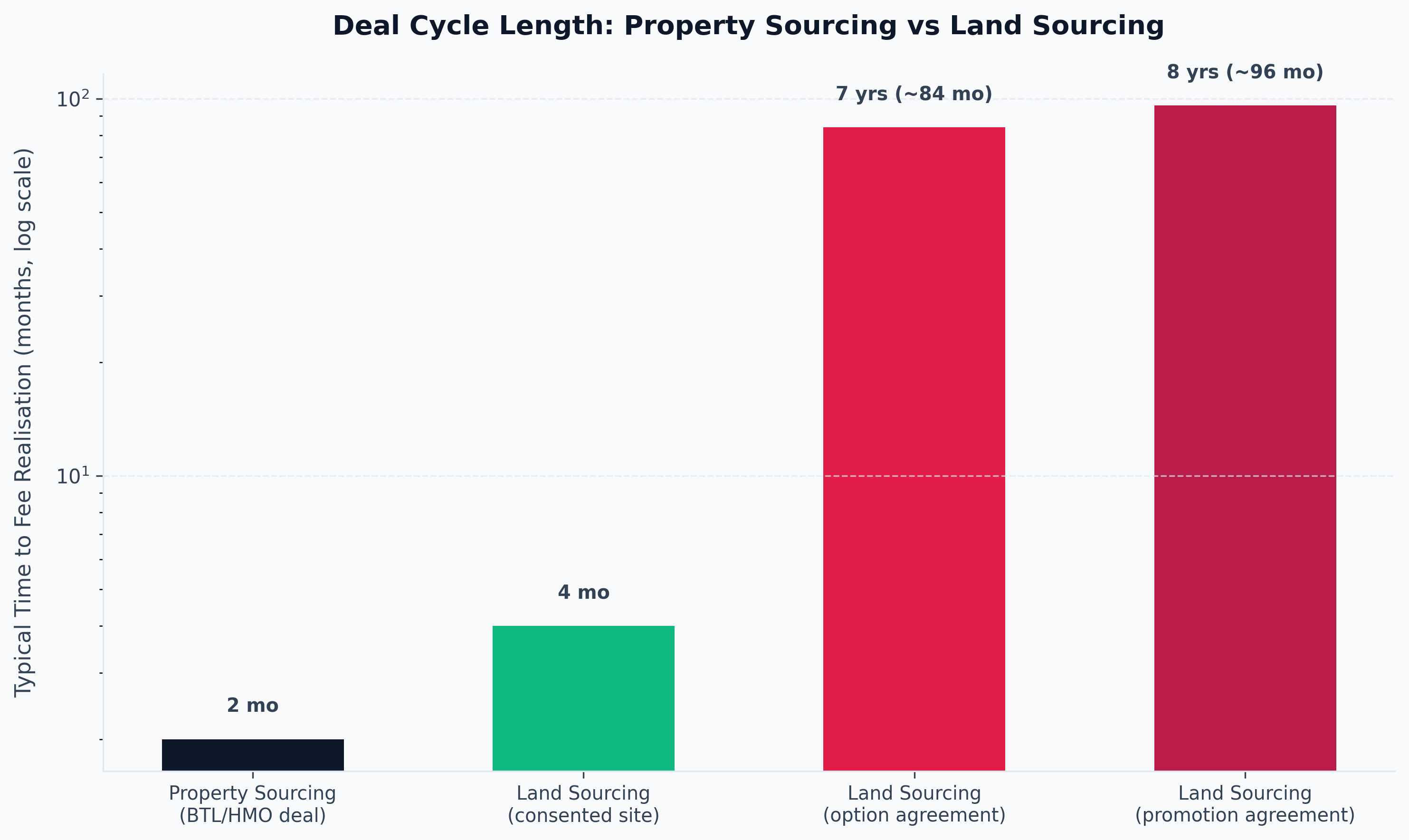

- Land sourcing differs from property sourcing in asset type, buyer, timescale and risk. Property sourcers move BTL flats and HMOs in weeks to months; land sourcers often work option agreements that run for years before a fee is realised.

- Sourcers find sites through HM Land Registry data, local authority brownfield and self-build registers, planning application monitoring, direct-to-landowner letter campaigns, and specialist software such as Searchland, LandInsight and Landstack.

- Buyers are overwhelmingly professional: volume housebuilders, SME regional builders (62% of whom cite land availability as their single biggest constraint), strategic land promoters, and self-build plot buyers.

- Fees for land deals run higher than residential sourcing, typically 1-5% of the eventual purchase or uplift value, with development-site sourcing fees commonly quoted around 2% and an £8,000 minimum.

- Compliance is non-negotiable: HMRC anti-money laundering supervision, a redress scheme (TPO or PRS), ICO registration and professional indemnity insurance apply to land sourcers exactly as they do to residential sourcers, and enforcement has stepped up sharply.

- Planning permission is the single biggest value driver. Agricultural land trading at roughly £8,000-£15,000 per acre can be worth many multiples of that once outline or full planning consent is attached, which is why sourcing accuracy on planning probability matters more than sourcing volume.

What Land Sourcing Actually Means

Land sourcing is the process of identifying, assessing and introducing undeveloped or under-developed land to a party who wants to build on it. That could be a strip of paddock behind a cul-de-sac with obvious infill potential, a disused commercial yard eligible for a brownfield residential scheme, or a greenfield parcel adjacent to a settlement boundary that might come forward through the local plan.

The sourcer's role typically covers three things. First, finding the site, often before it is marketed. Second, forming a view on planning probability, because raw land value and land-with-consent value can differ by an order of magnitude. Third, structuring the introduction, whether that is a straightforward fee-for-introduction arrangement, an option agreement, or a promotion agreement negotiated on the landowner's behalf.

This is a different discipline to sourcing a three-bed semi for a buy-to-let investor. It requires planning literacy, comfort with multi-year timescales, and the ability to read title plans, local plan allocations and constraint layers rather than just comparable sold prices.

Land Sourcing vs Property Sourcing: A Side-by-Side Comparison

The two disciplines overlap in name and sometimes in personnel, but the economics and skill sets diverge substantially.

| Factor | Land Sourcing | Property Sourcing |

|---|---|---|

| Asset type | Raw land, brownfield sites, agricultural parcels, options over land | Existing residential property (BTL, HMO, BRRR, serviced accommodation) |

| Primary buyer | Housebuilders, SME builders, land promoters, self-builders | Individual buy-to-let and portfolio investors |

| Core skill | Planning policy literacy, title and constraint analysis | Comparable evidence, refurbishment costing, yield analysis |

| Typical timescale | Months to years (option periods commonly 3-10 years) | Weeks to a few months from introduction to completion |

| Fee structure | 1-5% of price or uplift, or a share of planning gain via option/promotion agreement | 1-3% or £2,000-£6,000 flat fee, usually paid on completion |

| Payment trigger | Often contingent on planning permission being granted, which may never happen | Usually contingent only on legal completion of the purchase |

| Regulatory status | Same as property sourcing: AML, redress scheme, ICO, PI insurance all apply | AML, redress scheme, ICO, PI insurance all apply |

| Key risk | Planning refusal, prolonged option periods with no fee, title or access defects | Survey down-valuation, vendor withdrawal, chain collapse |

The practical implication is that land sourcing rewards patience and planning judgement over transaction volume. A property sourcer who completes two deals a month has a repeatable, cash-generative model. A land sourcer might work a single option agreement for four years before it converts into a fee, which is why many land sourcers run a hybrid book that includes some faster residential deals to keep income flowing. Our guide to deal sourcing property in the UK covers that residential side in detail.

How Land Sourcers Actually Find Sites

There is no single database that shows every developable plot in the UK. Sourcers stitch together public data, paid software and old-fashioned relationship-building.

HM Land Registry Data

HM Land Registry holds title records covering land and property worth more than £8 trillion across England and Wales, and it is the foundation layer almost every other tool builds on. A title register costs around £7 to download through the official portal and tells you the registered legal owner, any charges (mortgages) against the land, and any restrictive covenants or easements that affect development potential.

Beyond individual title lookups, HM Land Registry publishes open data sets including Price Paid Data (every registered residential sale since 1995), INSPIRE Index Polygons showing the approximate boundary of every registered freehold title, and a dataset listing UK companies that own land or property in England and Wales. Sourcers use the company-ownership data in particular to identify land banks held by dormant or semi-active development vehicles that might be persuaded to sell.

Planning Portals and Application Monitoring

Every live and historic planning application in England is searchable through individual local authority planning portals, and several third-party tools aggregate these into a single national feed. Monitoring applications reveals which sites are already being promoted by other parties, which areas a given council is approving development in, and where a refusal on a neighbouring plot might signal wider policy resistance.

The Planning Portal (the national government-run reference site) is useful for understanding process and permitted development classes, but it is not itself a site-sourcing tool. Serious land sourcers instead track applications through data platforms that index thousands of applications and flag emerging patterns, such as a council granting consent on the third resubmission of a similar scheme after two refusals.

Brownfield and Self-Build Registers

Local planning authorities are legally required to maintain a Brownfield Land Register under the Town and Country Planning (Brownfield Land Register) Regulations 2017. To qualify, a site must be previously developed land at least 0.25 hectares in size, or capable of supporting at least five dwellings. Registers are published in two parts: Part 1 lists all qualifying brownfield sites, and Part 2 lists sites the council has additionally granted "permission in principle," a lighter-touch route to outline consent.

Separately, under the Self-build and Custom Housebuilding Act 2015, every local authority must maintain and publicise a register of individuals seeking land to build their own home, reviewed at least annually. Land sourcers working the self-build and small-plot end of the market monitor both registers, since brownfield register listings are a rare example of a council publicly signalling where it wants development to happen.

Land Sourcing Software

Manually cross-referencing Land Registry data, planning history, flood risk, ownership and constraint layers does not scale, which is why a small cluster of specialist platforms now dominates UK land sourcing. The table below summarises the main options as of 2026; our companion piece on property sourcing tools and software covers the wider residential sourcing stack.

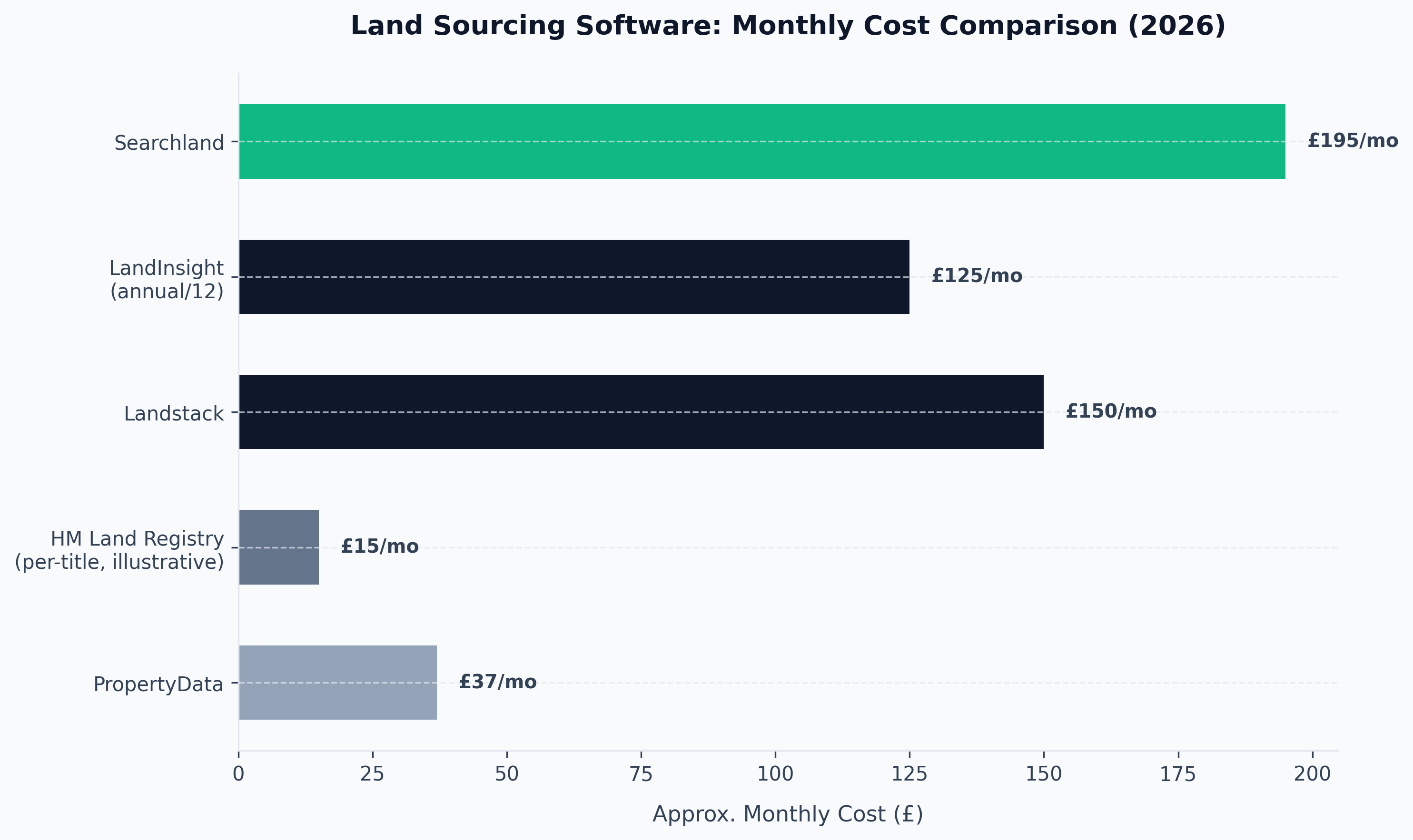

| Tool | Best For | Typical Cost | Notes |

|---|---|---|---|

| Searchland | Off-market site sourcing, planning and ownership overlays | From around £195/licence/month (annual billing) | Combines title, planning, local plan policy, constraints and comparables; added an AI/MCP connector in 2026 for natural-language site queries |

| LandInsight (LandTech) | Institutional and developer-grade site appraisal | Enterprise pricing, often £1,500+/year | Long-established "industry standard"; strong on ownership and EPC data layering |

| Landstack | Standardised planning and development data across Great Britain | Subscription, quote-based | Strong on planning applications, local plan allocations, and Biodiversity Net Gain data |

| PropertyData | Comparable evidence and yield mapping, less land-specific | £14-£60/month | Useful for the residential comps side of a mixed sourcing book, not a dedicated land tool |

| HM Land Registry (official portal) | Ground-truth ownership and title checks | £7 per title register | The base layer every other tool ultimately draws on |

Pricing and feature sets change quickly in this space, so treat the figures above as a starting point for comparison rather than a locked-in quote, and confirm current terms directly with each provider before committing to an annual licence.

Off-Market and Direct-to-Landowner Approaches

Writing directly to landowners remains one of the oldest and still most effective land sourcing tactics, precisely because it bypasses agents and the open market entirely. Effective campaigns are targeted rather than blanket: sourcers identify a shortlist using ownership and planning data, address the letter to the actual registered owner, reference the specific site, and focus on opening a conversation rather than making an immediate offer.

Response rates are modest. Sourcers running structured mail-merge campaigns commonly report somewhere between 5 and 15 replies per 100 letters sent, heavily dependent on list quality, the specificity of the letter, and whether the landowner has already been approached by other sourcers. A landowner who is not actively looking to sell today may still be worth cultivating for a future option agreement once their circumstances change, such as retirement or inheritance planning.

Agricultural Land and Rural Sourcing

Agricultural land sits at the raw end of the land sourcing spectrum. Most farmland trades for its agricultural use value, but a meaningful minority of parcels sit adjacent to settlement boundaries, along transport corridors, or within areas a council has flagged for future growth, all of which make them candidates for promotion or option agreements rather than a straight sale.

Sourcers working this segment need a working knowledge of the local plan process: which sites a council has already allocated for housing, which are being promoted through the "call for sites" process ahead of a plan review, and where the sequential test for development (brownfield first, then lower-grade green belt land, known as "grey belt," then green belt only where necessary) is likely to bring land forward. This is genuinely specialist territory and overlaps heavily with strategic land promotion rather than conventional deal sourcing.

Networking With Agents, Planning Consultants and Developers

A significant share of land deal flow never touches a portal or a register search. Rural chartered surveyors, planning consultants, and regional housebuilders' land buyers all hear about opportunities early through professional relationships, and sourcers who build genuine standing with these contacts get first sight of sites long before any formal marketing begins.

Who Buys Sourced Land

Understanding the buyer side shapes what makes a site worth sourcing in the first place.

Volume housebuilders buy large strategic sites, typically 50 to several hundred units, and prefer land with a clear route through the local plan rather than speculative applications with no policy support. They work with in-house land teams and established agents, so a sourcer's edge here is usually an early lead on an unallocated site rather than access to sites already on the market.

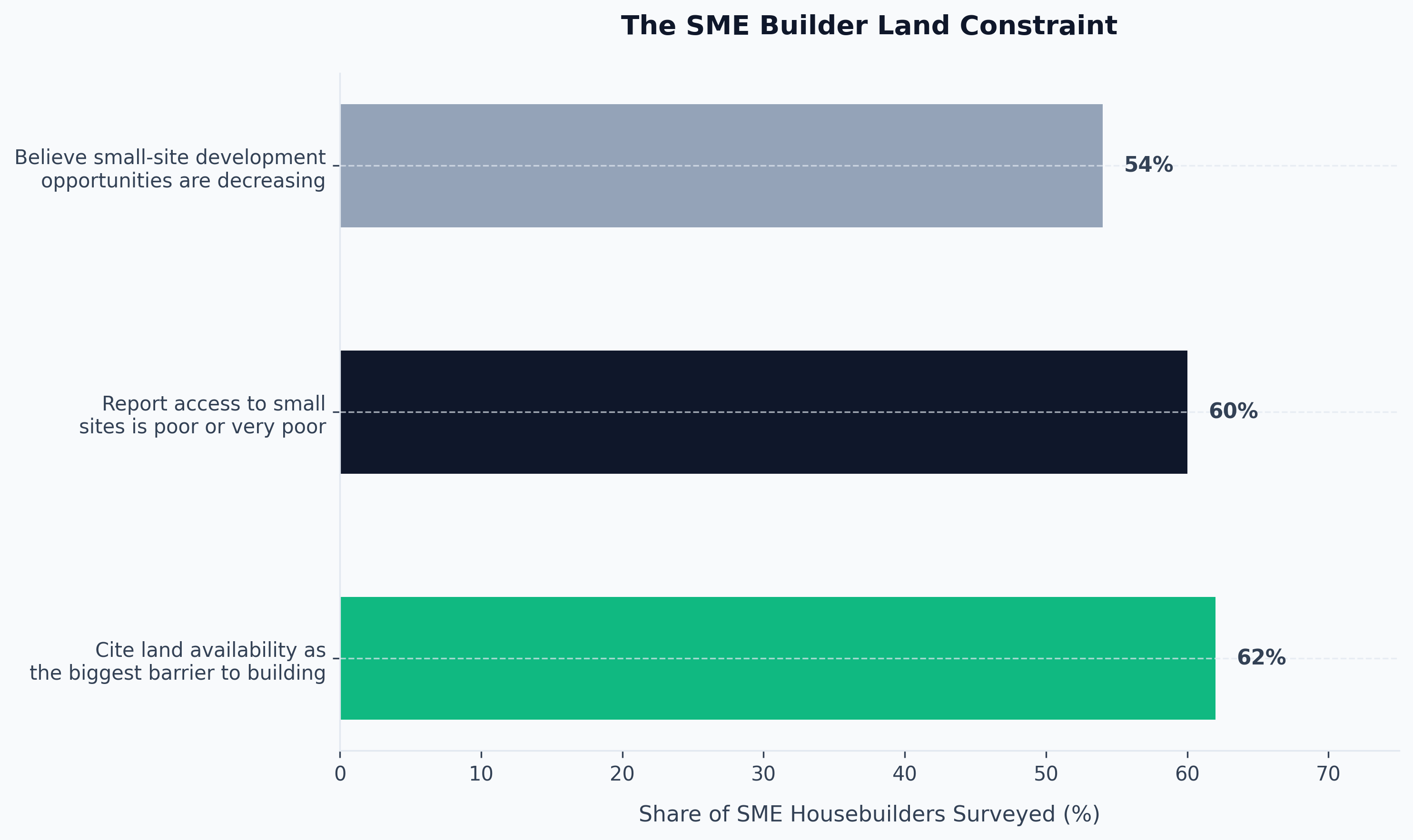

SME and regional builders are, by their own trade body's data, chronically constrained by land access: 62% of small housebuilders identify finding suitable land as the single biggest barrier they face, and 60% describe access to small sites as poor or very poor. This is a structural gap a land sourcer can fill, since SME builders typically want 5 to 30-unit sites that are too small to interest volume housebuilders but too complex for an individual investor to assess alone.

Strategic land promoters buy or option raw land with no immediate planning prospects, fund the multi-year process of getting it allocated in the local plan, and then sell it on (usually via a promotion agreement, covered below) once consent is realistic. This is capital-intensive and typically the preserve of specialist promotion companies rather than solo sourcers, though sourcers can broker the initial introduction.

Self-builders and small plot buyers purchase single plots, often sourced from brownfield or self-build registers, and are a lower-value but faster-moving segment of the market. Commercial and mixed-use developers round out the buyer pool, particularly for brownfield sites eligible for commercial-to-residential conversion under permitted development routes.

Government policy is actively trying to widen this buyer pool further. Homes England has committed to making certain land parcels exclusively available to smaller builders, and a £1.2 million PropTech Innovation Fund has been earmarked to improve data and certainty on infrastructure capacity for SME housebuilders, both of which point to growing institutional demand for exactly the kind of small and mid-sized sites land sourcers specialise in finding.

Land Sourcing Fees and Economics

Land sourcing fees are structured differently from residential sourcing fees, reflecting the longer timescales, higher stakes, and planning risk involved.

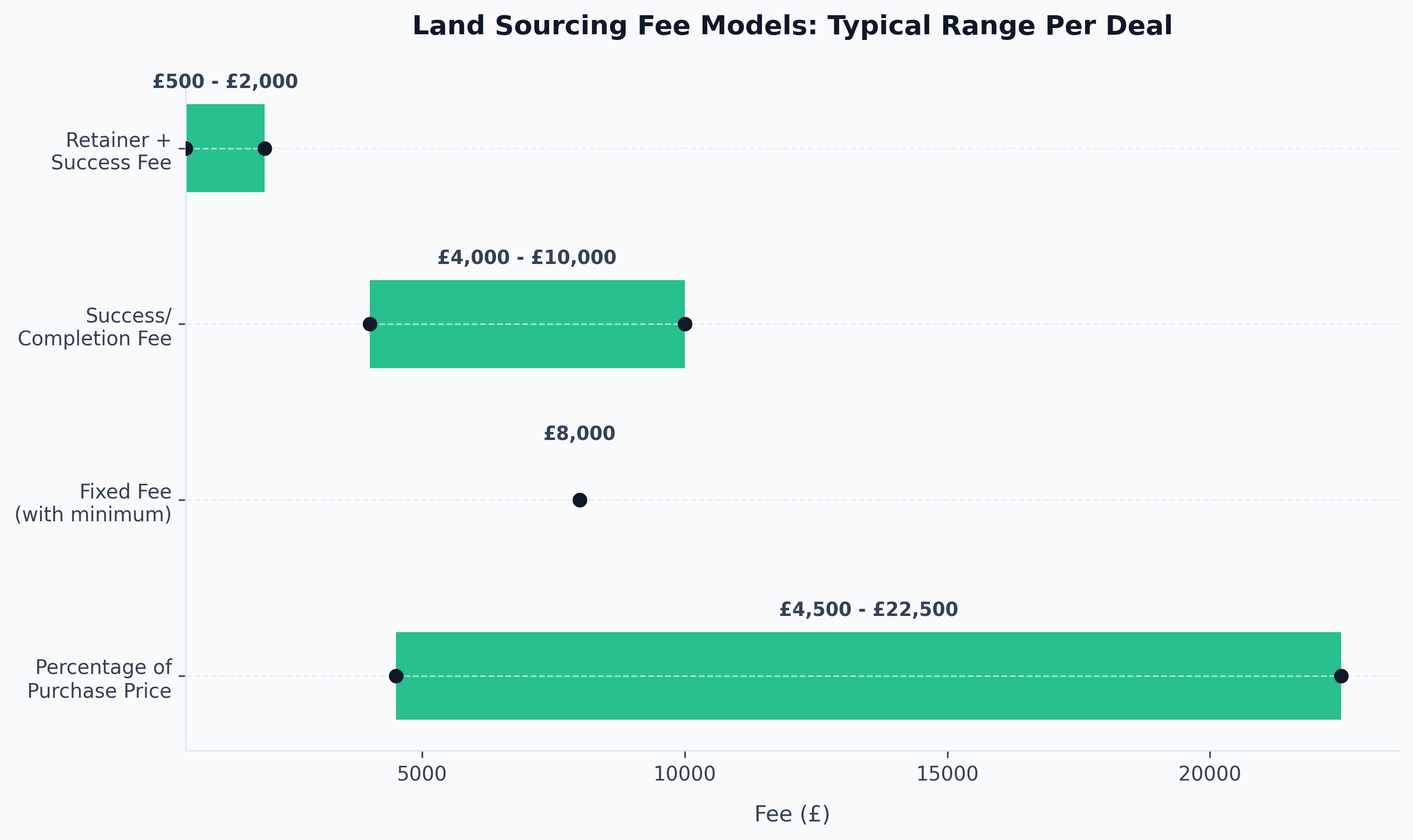

Fee Structures in Land Sourcing

| Fee Model | Typical Range | When It Applies | Key Risk |

|---|---|---|---|

| Percentage of purchase price | 1-3% (residential-scale sites), rising toward 5% on complex or strategic land | Most common structure for introducing a developable site to a builder or developer | Percentage alone does not reward planning risk taken on by the sourcer |

| Fixed fee with minimum | Often around 2% of price with an £8,000 minimum on development sites | Sites where a straight percentage would undervalue the due diligence required | Minimum fee can make small sites uneconomic to source |

| Success/completion fee | £4,000-£10,000+ per deal, tens of thousands on larger land parcels | Sourcer introduces the opportunity; fee paid only on legal completion | No income during long option or planning periods |

| Option/promotion share | A negotiated share of the uplift or sale proceeds, realised only on planning consent or sale | Strategic land and promotion agreements | Fee may never materialise if planning permission is refused |

| Retainer plus success fee | £500-£2,000/month retainer plus a completion fee | Ongoing search mandates for developers with a standing land requirement | Retainer rarely covers the sourcer's real time cost alone |

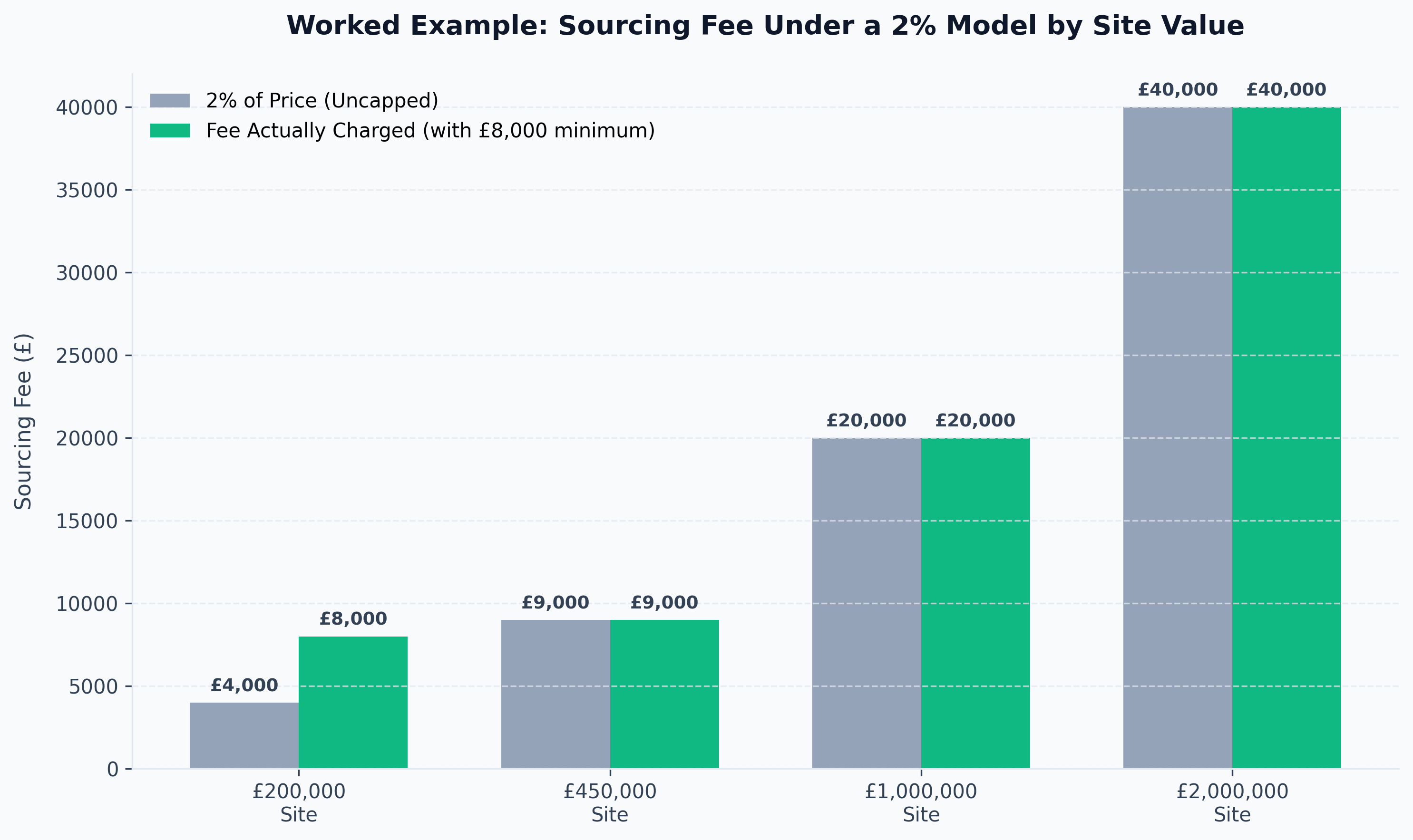

A Worked Example

Consider a 1.5-acre brownfield yard bought for £450,000 by an SME builder acting on a sourcer's introduction, sourced under a 2% fee with an £8,000 minimum. Two per cent of £450,000 is £9,000, so the percentage model applies rather than the minimum, and the sourcer earns £9,000 on completion. If the same sourcer had instead structured the deal as a promotion agreement and waited three years for outline planning consent before the land was sold on, their share of the resulting uplift could be substantially larger, but only if consent was actually granted.

Realistic Earnings

Land and development deal fees are meaningfully higher per transaction than standard residential sourcing fees, commonly £4,000-£10,000 on straightforward introductions and considerably more on larger sites or portfolios, where percentage-based commissions of 1-5% apply. The trade-off is volume and speed: a residential sourcer completing two deals a month can build a predictable £10,000-a-month income, whereas a land sourcer might close two or three land deals a year, with option-based work paying nothing at all until consent is secured, if it ever is.

Anecdotal reports from UK property forums are consistent on this point: land and development sourcing fees can look large on paper, but the effort and holding period required to earn them is substantially higher than sourcing a standard buy-to-let flat, and deals are genuinely scarcer than course providers and marketing material often suggest.

The Legal Side: Sourcing Agreements, Option Agreements and Promotion Agreements

Land transactions typically involve two distinct layers of legal documentation: the agreement between the sourcer and whoever is paying their fee, and the agreement between the landowner and the eventual developer or promoter.

The Sourcing or Fee Agreement

This is the contract between the sourcer and their client, whether that client is an individual investor, an SME builder, or a developer with a standing search mandate. It should specify the fee structure and trigger for payment, the scope of the sourcer's obligations (introduction only, versus ongoing due diligence support), exclusivity terms, and what happens if the deal falls through for reasons outside either party's control. Our detailed breakdown of property sourcing agreements covers the clauses that matter most, and the same principles apply directly to land sourcing agreements.

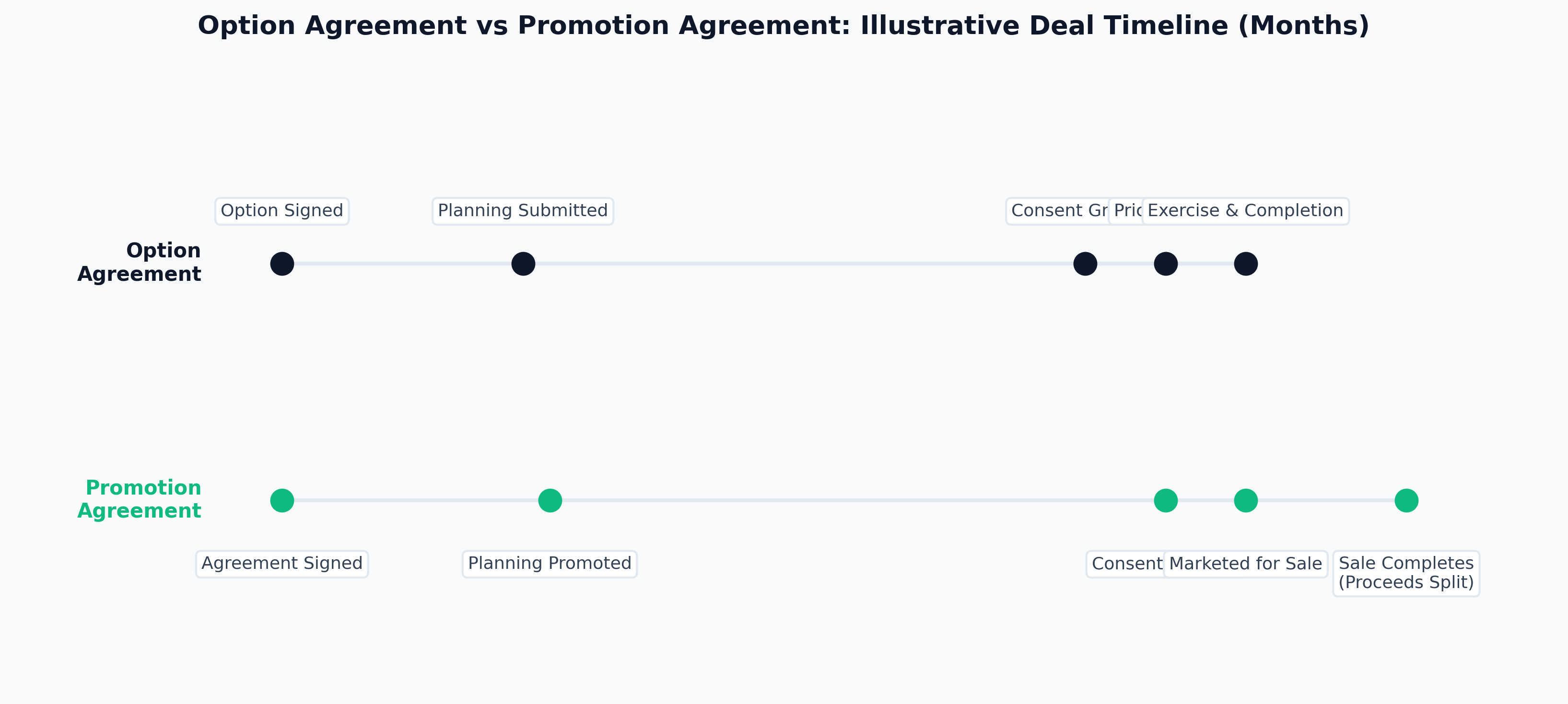

Option Agreements

Under an option agreement, a landowner grants a developer (or land sourcer acting for one) the right, but not the obligation, to buy the land within a defined period, commonly 5 to 10 years, sometimes longer. In return, the developer usually funds and manages the planning process at their own cost. If planning permission is achieved, the developer serves a Price Notice, the purchase price is agreed (typically at a discount to open market value, after deducting the option fee and planning promotion costs already spent), and an Exercise Notice completes the purchase.

Promotion Agreements

A promotion agreement works differently. Rather than the promoter buying the land themselves, they fund the planning process on the landowner's behalf and then market the land openly, usually via a competitive bidding process, once consent is secured. Proceeds are split between the landowner and the promoter after the promoter's costs are reimbursed. Because the eventual sale happens on the open market, promotion agreements are often considered more landowner-friendly than option agreements, since both parties are incentivised to maximise the final sale price rather than lock in a fixed discount in advance.

Option vs Promotion Agreement: Quick Comparison

| Feature | Option Agreement | Promotion Agreement |

|---|---|---|

| Who buys the land | The option holder (usually the developer) | A third party via open market sale |

| Price mechanism | Pre-agreed discount to market value at exercise | Competitive market sale, proceeds split after costs |

| Who funds planning | Developer/option holder | Promoter |

| Typical duration | 5-10+ years | Similar, often tied to plan review cycles |

| Landowner risk | Locked into a pre-agreed pricing formula | More exposed to market timing, but shares upside |

Compliance Checklist for Land Sourcers

The regulatory framework covering land sourcing is identical to the one covering residential property sourcing, because HMRC and the courts treat anyone brokering the introduction of land or property for financial gain as carrying out estate agency work, regardless of whether the asset has a roof on it.

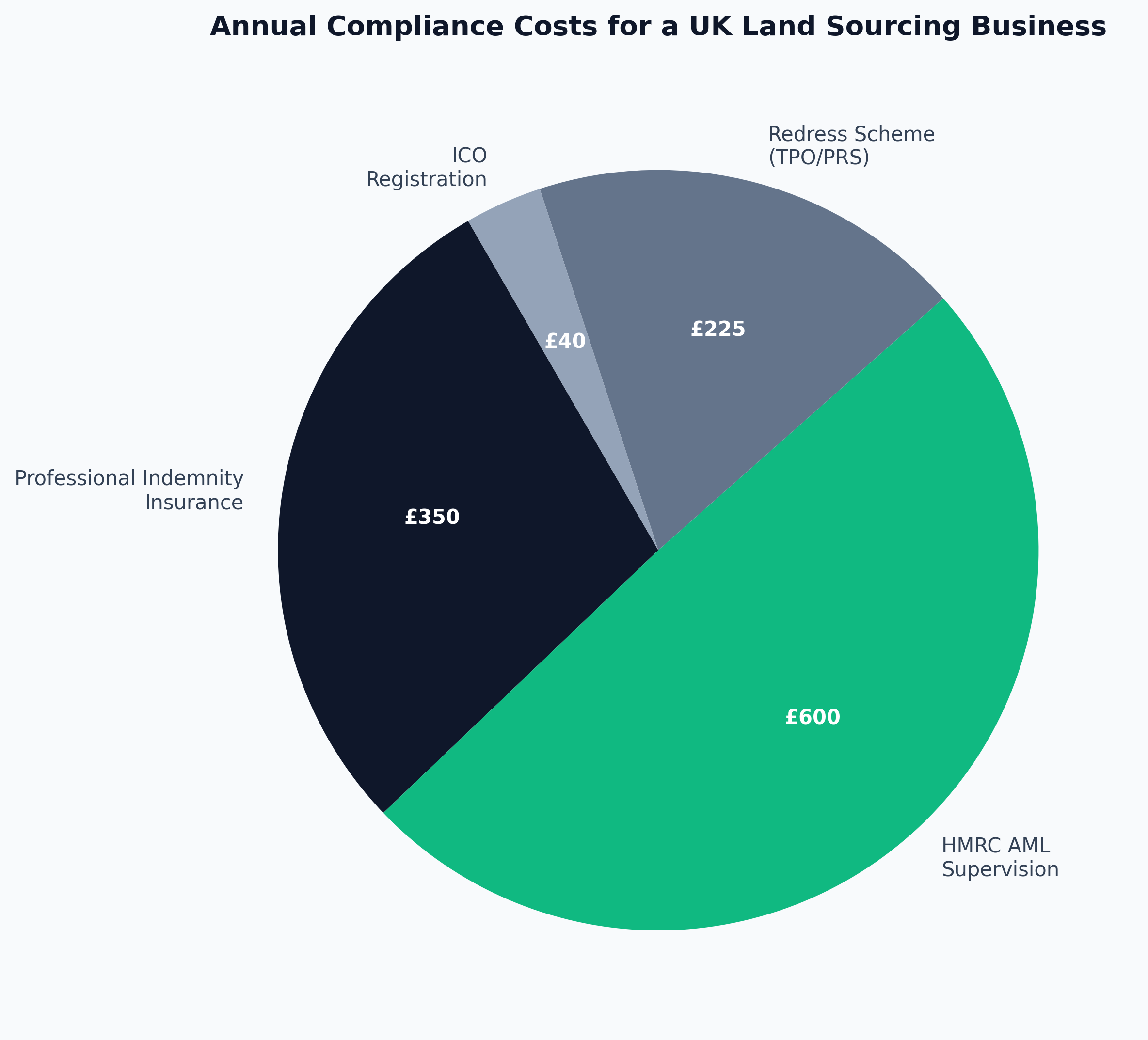

- HMRC Anti-Money Laundering (AML) supervision. Property and land sourcing businesses fall under the Money Laundering Regulations 2017 and must register with HMRC, appoint a nominated officer, and carry out identity and source-of-funds checks on clients.

- Property redress scheme membership. Registration with either The Property Ombudsman (TPO) or the Property Redress Scheme (PRS) is a legal requirement under the Consumers, Estate Agents and Redress Act 2007, with fixed penalties of up to £5,000 for non-compliance.

- ICO registration. Any sourcer handling personal data (identity documents, financial information, landowner contact details) must register with the Information Commissioner's Office under UK GDPR, at a modest annual cost.

- Professional indemnity insurance. Not always a statutory requirement, but a practical prerequisite for redress scheme membership and standard practice across the industry, typically covering £100,000 to £1 million in claims.

- Written sourcing and option/promotion agreements for every deal, setting out fee triggers, exclusivity, and what happens on planning refusal.

- Companies House due diligence on any landowner or developer counterparty, checking for dormant filings, strike-off actions, and director history.

Enforcement in this space has intensified. Industry research covering 500 UK property-sourcing businesses found that roughly 90% failed even a surface-level compliance check, and separate reporting identified 136 sourcing firms fined a combined total of more than £1.1 million by HMRC for failing to register for AML supervision. Land sourcers working with larger sums and longer timescales carry correspondingly larger exposure if these obligations are ignored.

Planning Permission Basics That Affect Land Value

Planning status is the single largest driver of land value, and understanding the mechanics is essential to sourcing land credibly rather than optimistically.

Outline vs Full Planning Permission

Outline planning permission establishes the principle of development on a site, agreeing broad matters such as land use and quantum while leaving detailed design ("reserved matters") to a later application. Full planning permission approves the complete detailed scheme in one step. Outline consent is faster and cheaper to obtain and is often what a land sourcer or promoter targets first, since it de-risks the site enough to attract a developer while leaving the detailed design (and its cost) to whoever buys the site next.

Permitted Development Rights

Permitted development (PD) rights allow certain categories of development, notably some commercial-to-residential conversions, without a full planning application. The Town and Country Planning (General Permitted Development etc.) (England) (Amendment) Order 2026 came into force on 9 April 2026, though its changes were largely technical rather than a wholesale expansion of PD rights. Wider proposals, such as increasing rear extension depths and scrapping curtilage limits, remain under consultation rather than enacted law, and the Planning and Infrastructure Act 2025 left householder PD rights unchanged. Sourcers should treat PD potential as a valuable but narrow tool, applicable to specific building types and use classes rather than a general shortcut around planning risk.

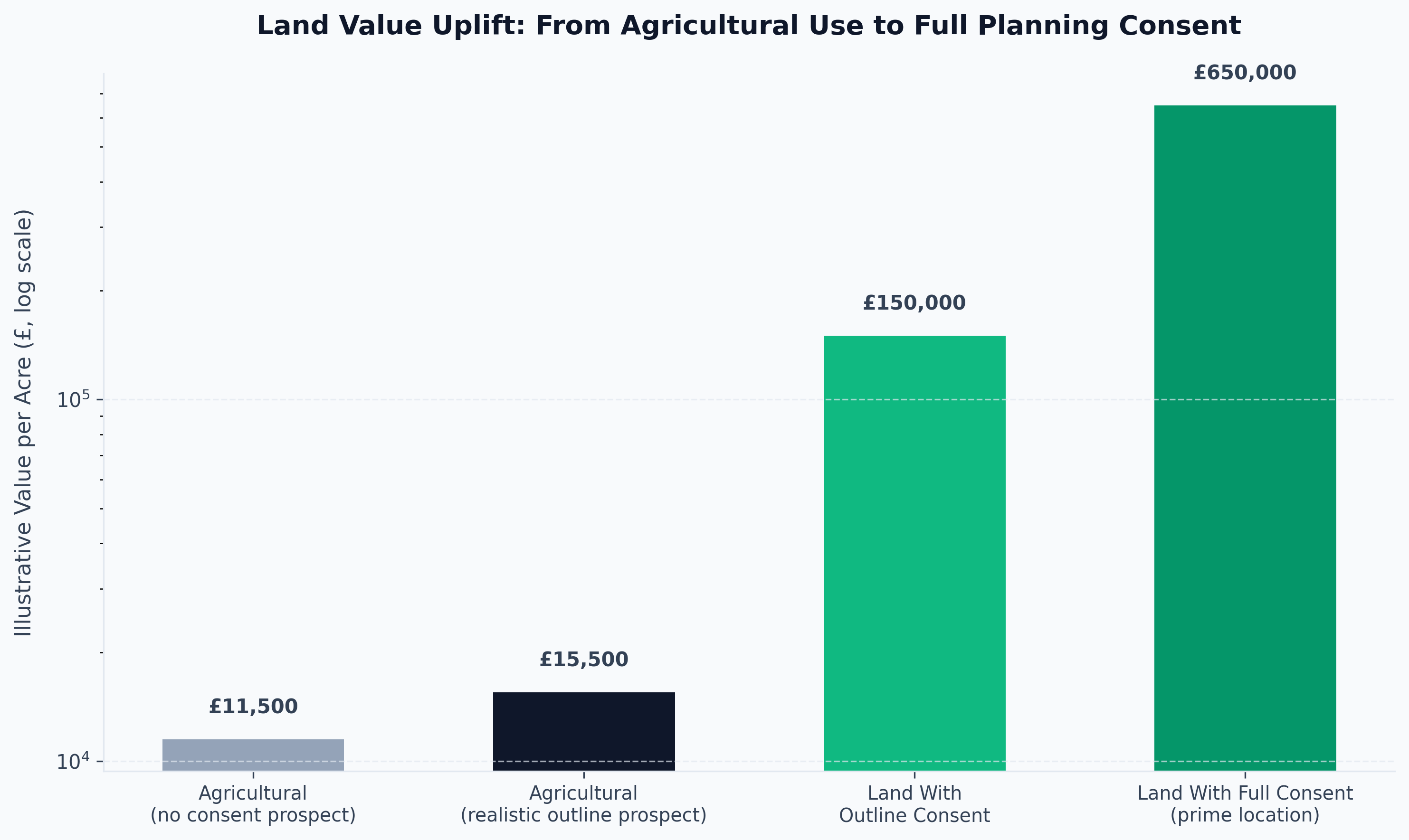

The Land Value Uplift

The gap between undeveloped and consented land value is the entire economic rationale for land sourcing and promotion.

| Land Status | Typical Value (Illustrative) | Notes |

|---|---|---|

| Agricultural (no consent prospect) | £8,000-£15,000 per acre | Reflects farming use value only |

| Agricultural with realistic outline prospect | Uplift of roughly 20-50% over raw value | Reflects planning risk, not certainty |

| Land with outline consent | Substantially above agricultural value, site and region dependent | Value now reflects unit numbers and GDV, discounted for remaining risk |

| Land with full/detailed consent, prime location | £300,000-£1,000,000+ per acre; £2 million+ in parts of the South East Green Belt | Reflects buildable unit density and location premium |

These figures are illustrative and vary enormously by region, unit density, and local market conditions, so they should be treated as a framework for understanding scale rather than a valuation tool for any specific site. Independent professional valuation advice is essential before any transaction.

Planning Reform Context

The revised National Planning Policy Framework raised the mandatory national housing target from 300,000 to 370,000 homes a year and introduced the concept of "grey belt" land: lower-quality green belt parcels, including previously developed land and sites like disused car parks or petrol stations, which now sit ahead of general green belt land in the sequential test for release. Development on green belt or grey belt land is subject to "golden rules" requiring higher levels of affordable housing and supporting infrastructure. For sourcers, this matters directly: land on the edge of settlements that was previously considered unpromotable green belt may now have a realistic route to consent, while genuinely high-quality green belt remains heavily protected.

Planning Timescales in Practice

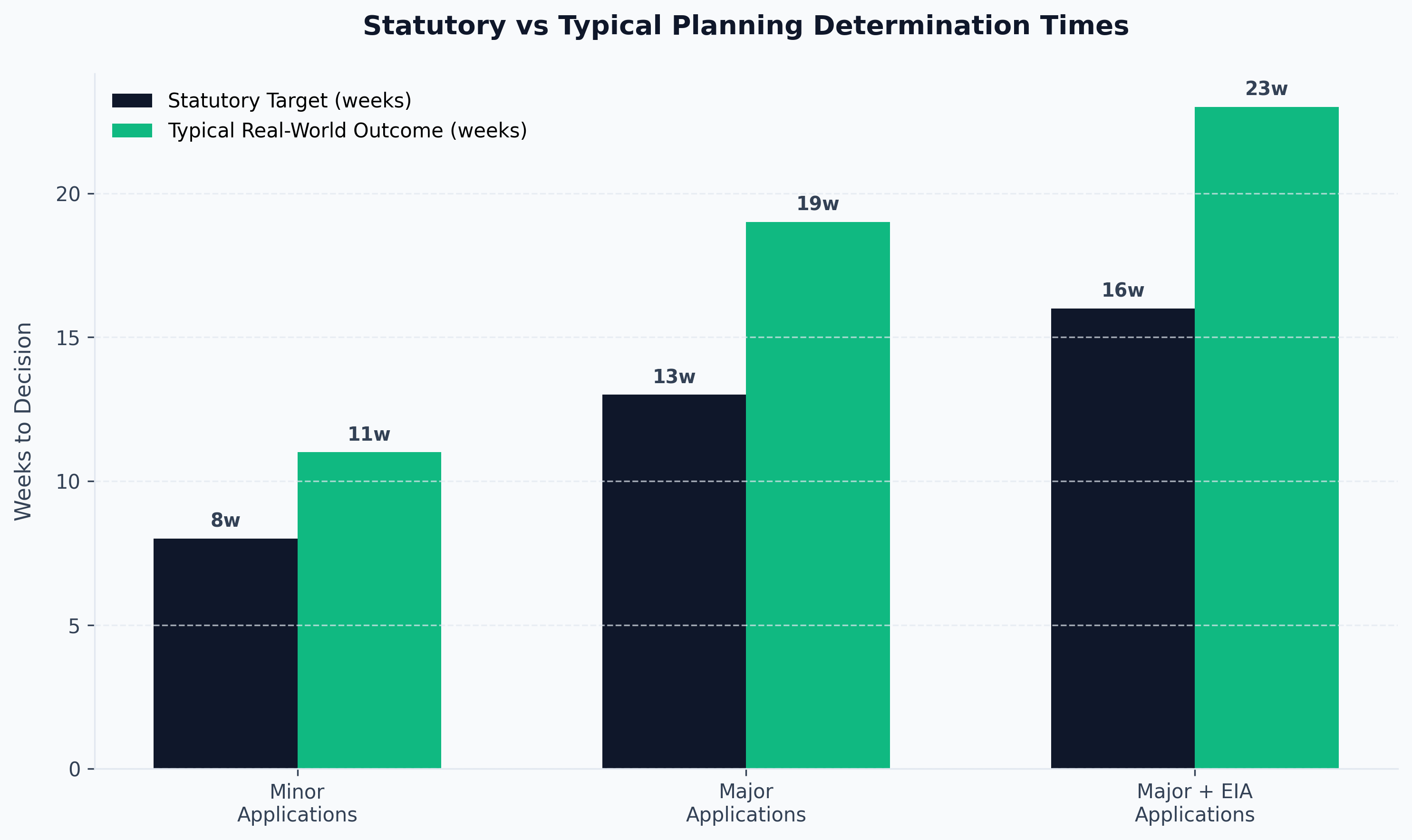

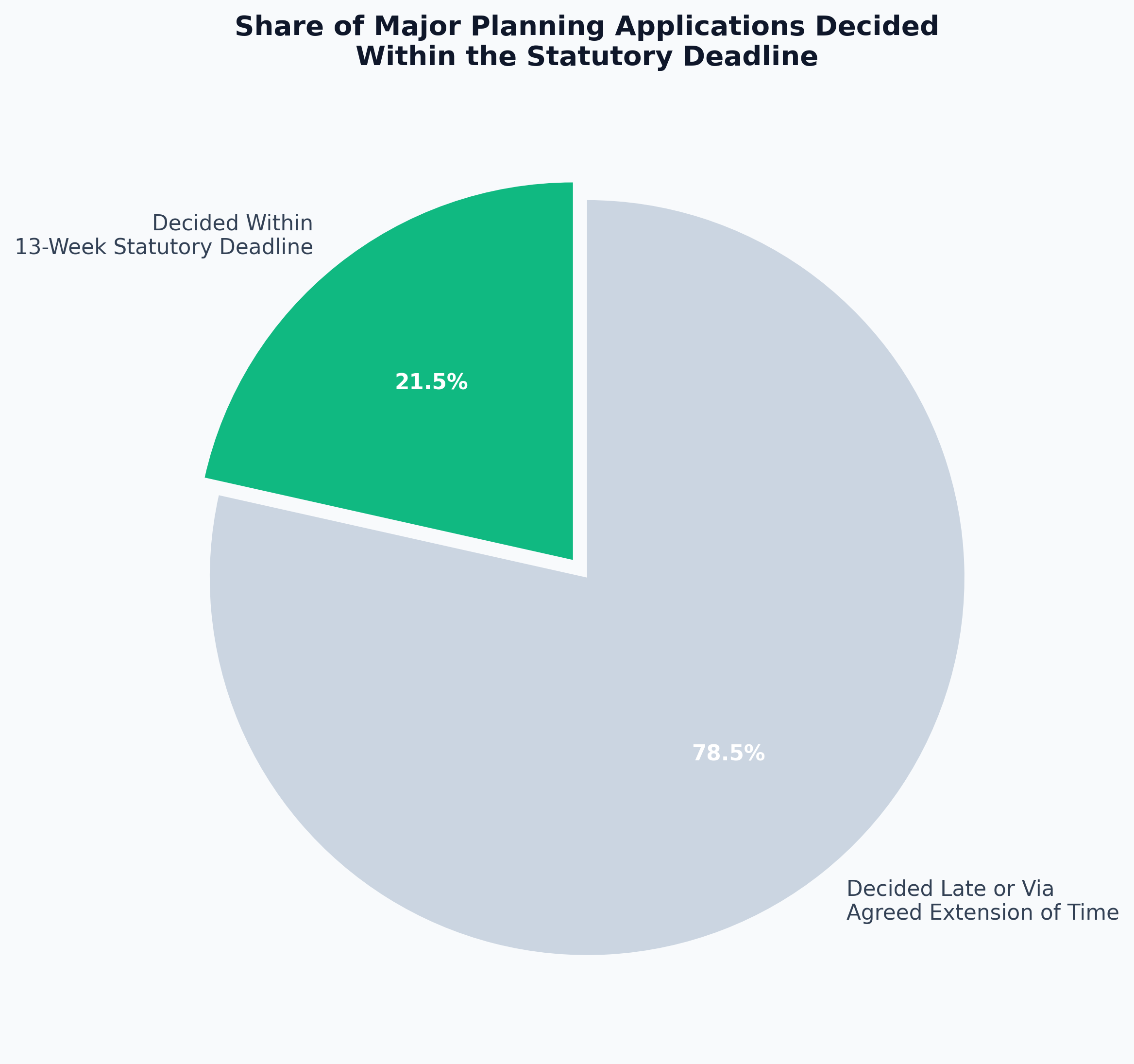

Statutory determination periods are 8 weeks for most applications, 13 weeks for major development, and 16 weeks where an Environmental Impact Assessment applies. In practice, only around 20-23% of major applications are decided within the 13-week statutory window without an agreed extension of time, and the validation stage alone averages around 17 days before a case officer even begins assessing an application. Sourcers and the developers they work with should budget for planning timescales well beyond the statutory minimums, particularly on anything classed as major development or requiring committee referral.

Risk Assessment: What Can Go Wrong in Land Sourcing

Land sourcing carries a materially different risk profile to residential property sourcing, and every risk below should be disclosed clearly to any client or investor relying on a sourced opportunity.

Planning refusal risk. The single largest risk in the sector. A site that looked highly promotable can be refused, appealed, and refused again, with years of holding cost and professional fees sunk before a final answer arrives.

Extended option periods with no income. Option and promotion agreements can run five to ten years or longer. A sourcer or investor relying on that fee has no guaranteed income until planning consent (if it comes) triggers a sale.

Title, access and covenant defects. Land without direct highway access, subject to ransom strips, or burdened by restrictive covenants can be effectively unbuildable regardless of planning status, and these issues are easy to miss without a proper title review.

Environmental and physical constraints. Flood risk, contamination history, protected species, and tree preservation orders can all sink a scheme that otherwise looks policy-compliant, and full assessment usually requires paid specialist surveys.

Market and regulatory volatility. Housing targets, green belt and grey belt policy, and viability guidance have all shifted materially in the past two years, and a site that looked promotable under one policy framework can lose that status under the next.

Unregulated market and counterparty risk. The land and property sourcing sector has a low barrier to entry, and industry compliance research suggests the large majority of sourcing businesses fail basic regulatory checks. UK property forums carry consistent accounts of sourcing fees paid for deals that were already public knowledge, or sourcers who become unresponsive after taking an upfront fee, so counterparty due diligence is not optional.

Land Sourcing Tools and Platforms: What to Prioritise

Given the cost of a full land sourcing software stack, most independent sourcers prioritise in a specific order: an HM Land Registry account for ground-truth title checks first, a mid-tier planning and ownership platform such as Searchland or Landstack second, and a dedicated appraisal tool like LandInsight only once deal volume justifies the enterprise-level cost. Our full breakdown of the property sourcing tools and software landscape covers the residential-focused end of this stack in more detail, including CRM and direct mail platforms that apply equally to a land sourcing pipeline.

How to Get Started in Land Sourcing

Land sourcing is not typically a first step into property sourcing. Most sourcers who move into land have already built residential sourcing experience, developed relationships with local builders and agents, and become comfortable reading title plans and planning documents. Our guide on how to become a property sourcer in the UK covers the foundational route in, and our deal packaging guide explains how to present a sourced opportunity credibly once you have one, both of which apply directly to land deals as well as residential ones.

Investors who would rather deploy capital into vetted opportunities than build a sourcing operation from scratch can review live opportunities directly at shadedcanvas.co.uk/invest.

Actionable Next Steps

- Register for compliance before taking a single fee. Confirm HMRC AML supervision, join a redress scheme (TPO or PRS), register with the ICO, and secure professional indemnity insurance covering land sourcing activity specifically.

- Set up a Land Registry account and a mid-tier sourcing platform. Start with official title checks and a single paid tool such as Searchland or Landstack rather than subscribing to the full enterprise stack immediately.

- Build a target list using brownfield and self-build registers first. These are the only data sources where a local authority is actively signalling where it wants development to happen.

- Run a small, targeted direct-to-landowner letter campaign rather than a mass mailout, and track response rates so you can refine list quality over time.

- Draft a standard sourcing agreement and understand option versus promotion structures before approaching your first landowner or developer client, and take independent legal advice on the specific wording.

- Budget for planning timescales beyond the statutory minimums, and disclose planning risk explicitly to any client or investor relying on a site you have sourced.

- Treat land sourcing as a longer-cycle complement to residential sourcing, not a replacement for it, particularly in the first two to three years while a track record and pipeline are being built.

FAQ

What is the difference between land sourcing and property sourcing? Land sourcing deals in raw or under-developed land destined for future construction, typically sold to housebuilders, developers or promoters, while property sourcing deals in existing residential stock sold to individual buy-to-let investors. Land sourcing timescales are longer, fees are structured differently, and planning risk plays a much larger role.

Do I need to be a chartered surveyor or planning consultant to source land? No, but you do need working knowledge of planning policy, title documents and local plan processes to source credibly. Many successful land sourcers build relationships with chartered surveyors and planning consultants rather than replicating their qualifications, using professional advice to validate planning judgement rather than relying on it alone.

How much can a land sourcer expect to earn per deal? Fees on straightforward introductions commonly range from £4,000 to £10,000, with percentage-based structures (typically 1-5%) applying to larger or more complex sites, and development-site sourcing often quoted around 2% with an £8,000 minimum. Deal volume is lower than residential sourcing, so annual income depends heavily on pipeline size and how many deals convert.

Is an option agreement or a promotion agreement better for a landowner? Promotion agreements are generally considered more landowner-friendly because the land is sold on the open market after planning consent, exposing both parties to competitive bidding rather than a pre-agreed discount formula. Option agreements suit developers who want certainty over the eventual purchase price and are willing to fund planning costs directly in exchange for that certainty.

Is land sourcing legal without HMRC AML registration and redress scheme membership? No. Anyone brokering the introduction of land or property for financial gain is treated as carrying out estate agency work under UK law, which triggers mandatory HMRC anti-money laundering supervision and redress scheme membership (TPO or PRS), regardless of whether the asset is land or a finished building. Non-compliance carries fines and, in AML cases, potential criminal liability.

What is "grey belt" land and why does it matter for sourcing? Grey belt is a category introduced in the revised National Planning Policy Framework covering lower-quality green belt land, including previously developed sites, that now sits ahead of general green belt land in the sequential test for release. It matters because it identifies a specific, policy-defined category of edge-of-settlement land where planning consent has become more realistic than it was under the previous framework, making it a priority area for land sourcers to research.

How long does it realistically take to complete a land sourcing deal? Straightforward introductions of land that already has consent, or is being bought subject to planning, can complete within the normal conveyancing timescale of a few months. Option and promotion agreements tied to securing planning permission from scratch typically run several years, and in some cases can extend well beyond the original option period if applications are refused and resubmitted.

Stop being a landlord. Start being an investor.

Shaded Canvas introduces serious capital to vetted UK property opportunities — targeting 12–16% net returns.

Start Investing →