Target Keyword: property sourcing agreement UK

A single poorly worded clause in a property sourcing agreement UK can cost you tens of thousands of pounds — or worse, leave you legally exposed with no recourse. Yet most investors sign these contracts after nothing more than a ten-minute phone call and a PDF attachment. That stops today.

Whether you are an investor hiring a sourcer for the first time, or a deal packager drafting your own deal sourcing contract, understanding exactly what belongs in this document — and what should trigger an immediate walkaway — is not optional. It is the difference between a profitable, protected portfolio and a catastrophic financial dispute.

This guide breaks down every critical clause, maps out the compliance landscape as it stands in 2026, explains fee payment timing and escrow best practices, and provides a practical structure you can adapt or use to interrogate any agreement placed in front of you.

What Is a Property Sourcing Agreement?

A property sourcing agreement is a legally binding contract between a property sourcer (also called a deal packager or property finder) and an investor. It sets out the terms under which the sourcer will identify, negotiate, and present investment opportunities in exchange for a fee.

This is not a handshake arrangement. Under English contract law, a valid sourcing agreement creates enforceable obligations on both parties. If the sourcer fails to deliver properties meeting the agreed criteria, the investor may have grounds for a claim. Conversely, if the investor circumvents the sourcer and transacts directly with a vendor introduced through the sourcer's network, the sourcer retains a legitimate claim for their fee.

The agreement sits at the intersection of several regulatory frameworks:

- Estate Agency Act 1979 — If the sourcer's activities constitute "estate agency work" (introducing a buyer to a seller for the purpose of effecting a sale), they must comply with this Act, including registration with a redress scheme.

- Consumer Rights Act 2015 — Terms must be transparent, fair, and not create a significant imbalance to the detriment of the consumer.

- Anti-Money Laundering (AML) Regulations — Sourcers handling client money must be registered with HMRC for AML supervision.

- The Property Ombudsman (TPO) / Property Redress Scheme (PRS) — Membership of a recognised redress scheme is mandatory for anyone carrying out estate agency work.

A property sourcing agreement UK that ignores these frameworks is not just unprofessional — it is potentially unlawful.

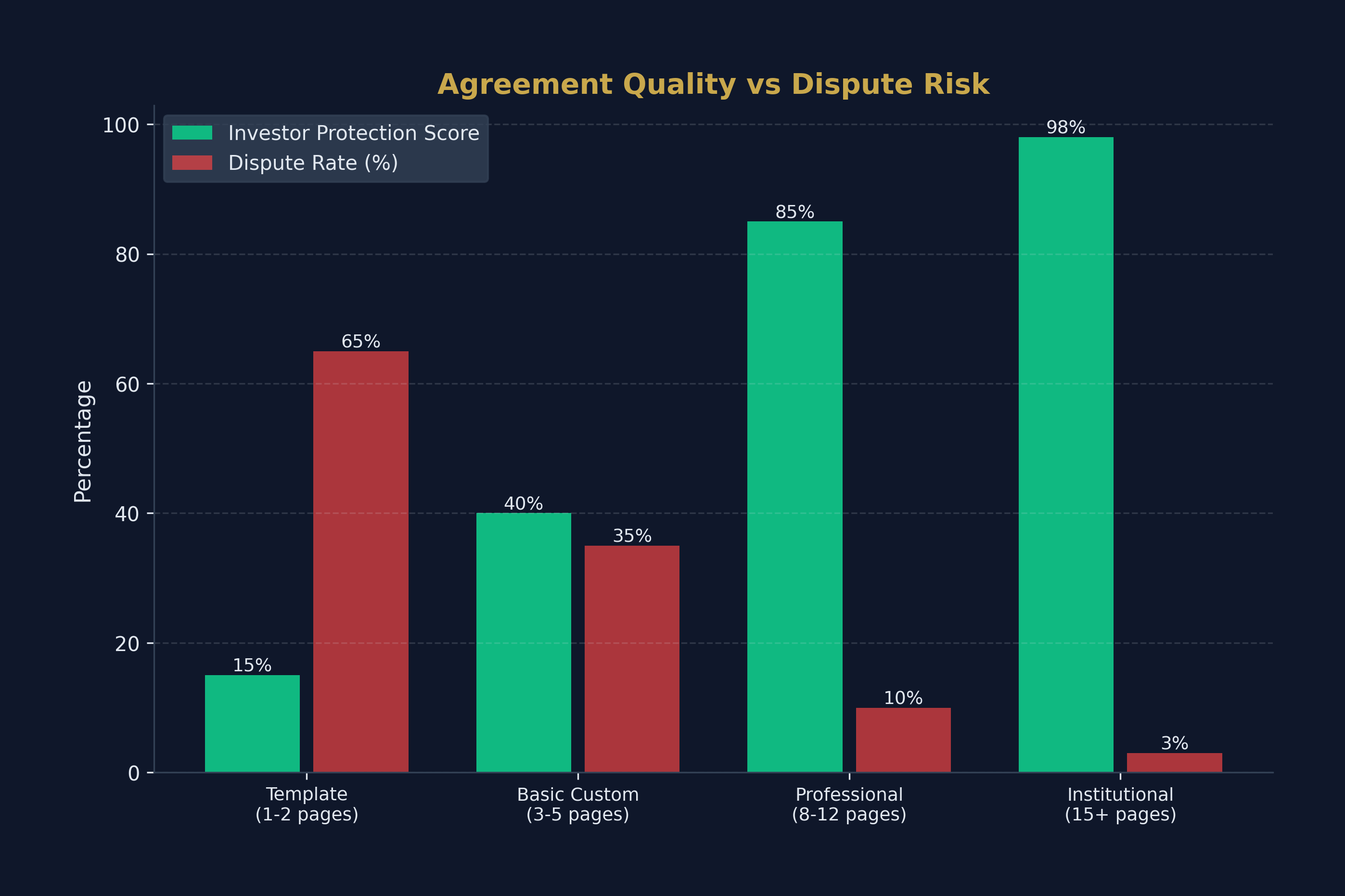

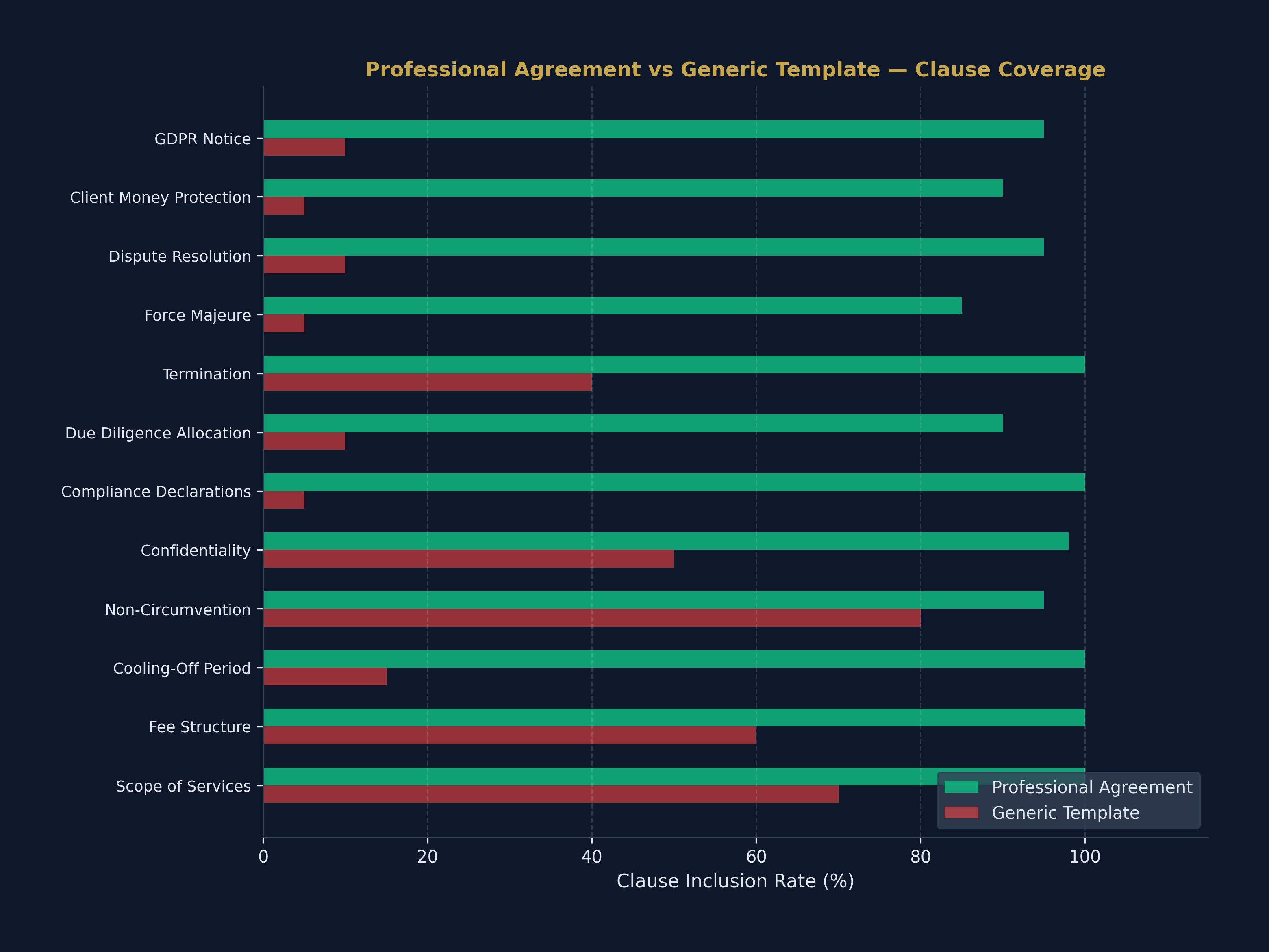

Why You Cannot Rely on a Generic Template

The internet is littered with one-page sourcing agreement templates. Most are dangerously inadequate. NAPSA (the National Association of Property Sourcing Agents) has stated explicitly that a well-constructed sourcing agreement template should exceed ten pages. Anything shorter is almost certainly missing critical protections.

Generic templates typically fail in three ways:

- No compliance framework. They omit references to the Estate Agency Act, AML obligations, and redress scheme membership — meaning the sourcer may be operating unlawfully and the investor has no escalation path.

- Ambiguous fee triggers. Phrases like "fee payable upon completion" sound clear but create disputes when deals fall through after exchange, when refinance valuations disappoint, or when the investor pulls out citing due diligence concerns.

- No limitation of liability. Without a Force Majeure clause and a cap on the sourcer's liability, the investor is exposed to unlimited claims, and the sourcer is exposed to disproportionate risk relative to their fee.

If you are a sourcer, investing in a professionally drafted property sourcing terms of business is not an overhead — it is your single most important business asset. If you are an investor, reading every line of the agreement before signing is not paranoia — it is basic due diligence.

The 12 Essential Clauses in a Property Sourcing Agreement

1. Scope of Services

This clause defines precisely what the sourcer will deliver. Vague language like "we will find you properties" is worthless. A robust scope clause specifies:

- Type of sourcing: Below-market-value (BMV) deals, HMO conversions, commercial-to-residential, auction lots, off-plan, or specific strategies like BRRR or rent-to-rent.

- Geographic parameters: Named towns, postcodes, or local authority areas.

- Investment criteria: Minimum yield, maximum purchase price, target refurbishment budget, or required rental income.

- Level of service: Some sourcers provide an end-to-end service (sourcing through to completion), while others deliver a deal pack and leave the investor to manage conveyancing, surveys, and mortgages independently.

If the scope is unclear, every subsequent dispute becomes a "he said, she said" argument. Insist on specificity.

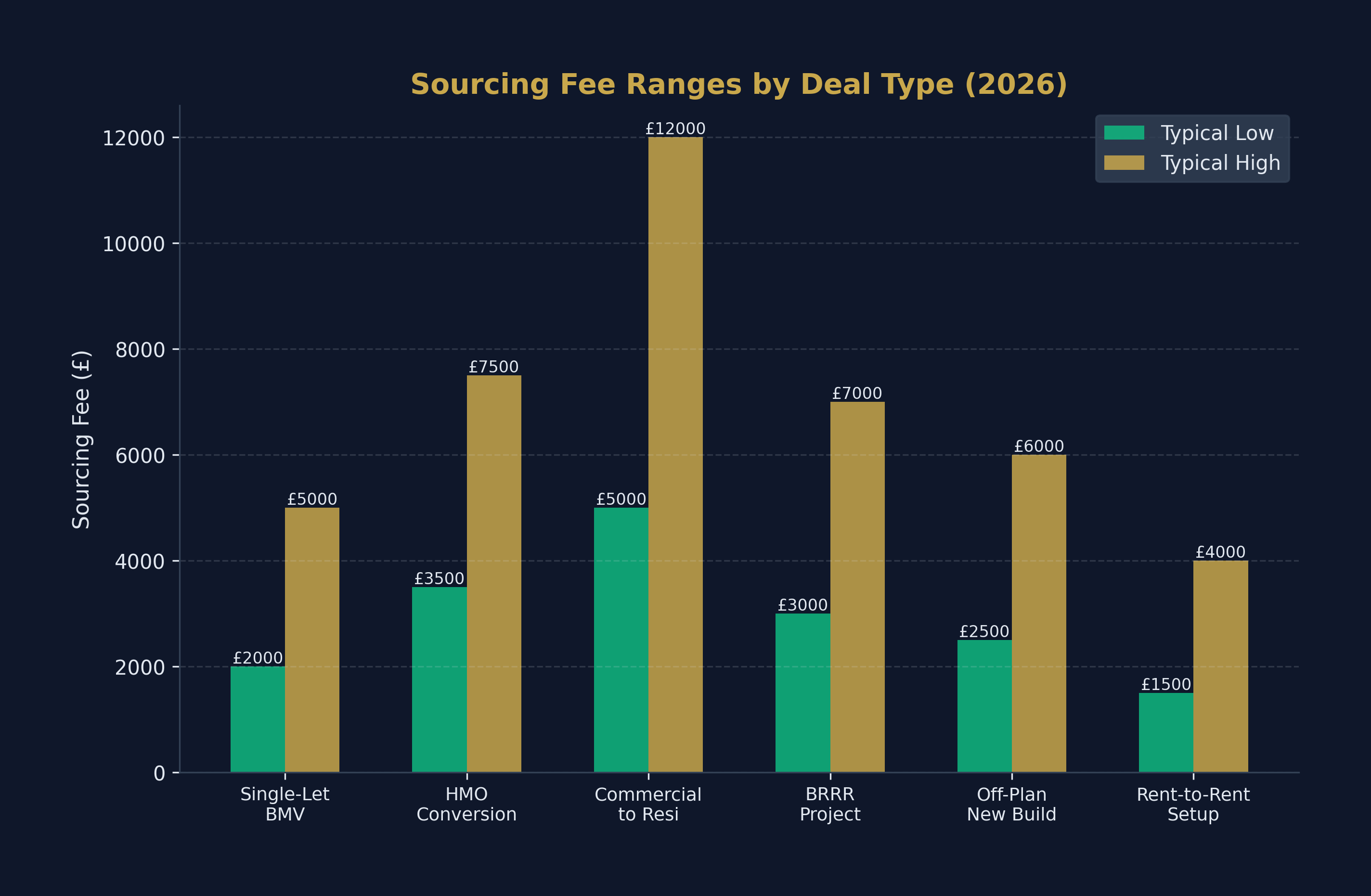

2. Fee Structure and Payment Terms

This is where most disputes originate. A transparent fee agreement property clause must address:

- Fee type: Flat fee (e.g., £3,000–£7,000 per deal), percentage of purchase price (typically 1%–5%), or a hybrid.

- Payment triggers: When exactly is the fee due? Common structures include:

- Reservation fee (£500–£2,000) payable upon accepting a deal pack, typically non-refundable.

- Completion fee (the balance) payable upon legal completion of the purchase.

- Upfront fee — some sourcers charge the full fee before any deal is presented. This is a significant red flag unless protected by a cooling-off period and escrow arrangement.

- Refund policy: Under what circumstances is the investor entitled to a full or partial refund? The Consumer Contracts Regulations 2013 grant a 14-day cooling-off period for distance contracts (agreements signed online or over the phone without face-to-face contact).

A sourcer who refuses to put their fee structure in writing, or who demands full payment before presenting any opportunities, is either inexperienced or operating outside industry norms.

3. Cooling-Off Period

Under the Consumer Contracts (Information, Cancellation and Additional Charges) Regulations 2013, if the agreement is entered into at a distance (online, by phone, by email), the investor has a statutory right to cancel within 14 days of the commencement date without penalty.

This right cannot be contracted away. Any clause purporting to waive the cooling-off period is unenforceable and should be treated as a red flag. NAPSA-compliant agreements explicitly reference this right and outline the refund procedure.

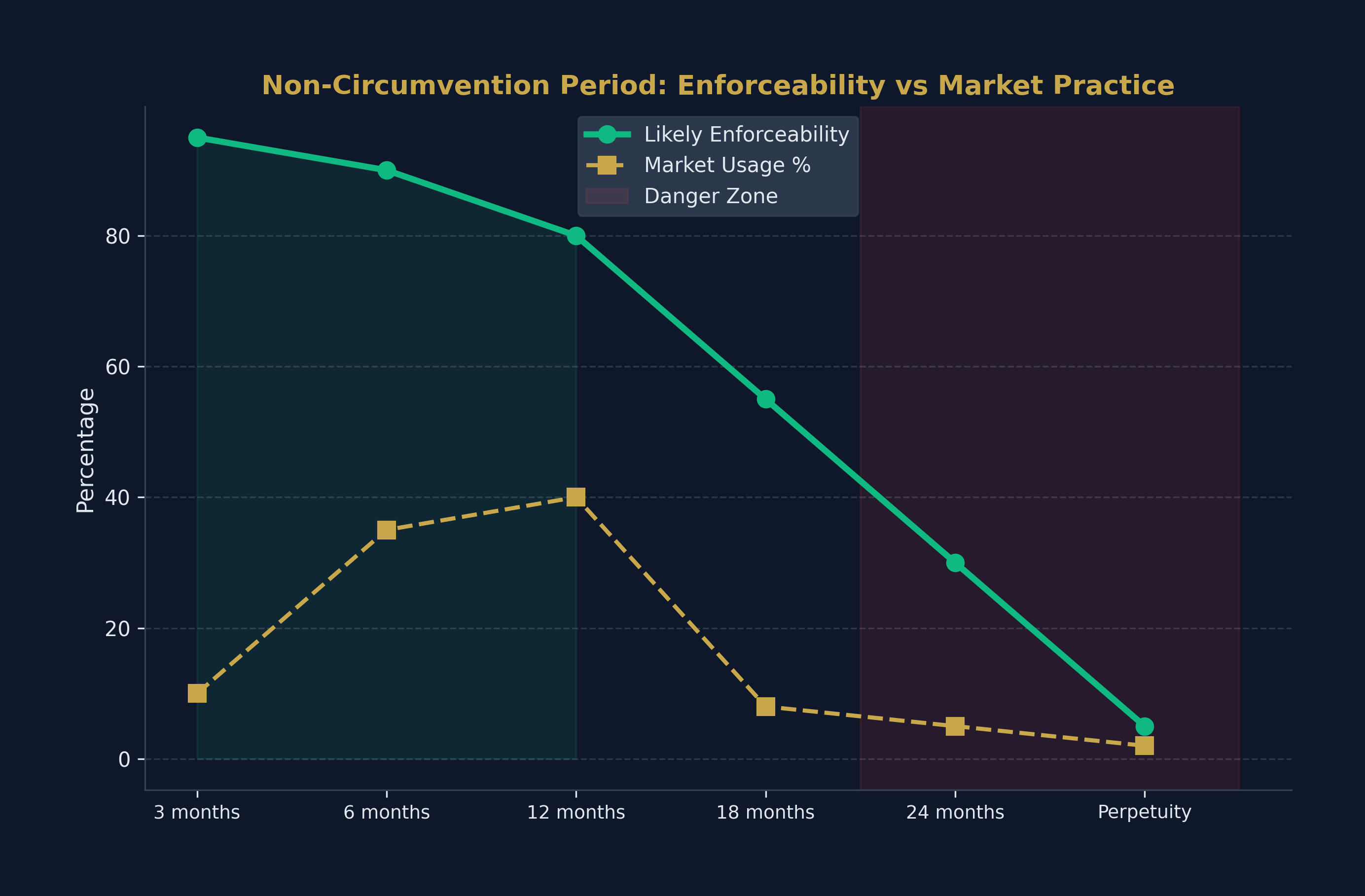

4. Exclusivity and Non-Circumvention

A non-circumvention clause prevents the investor from bypassing the sourcer and dealing directly with a vendor or agent introduced through the sourcer's efforts. This is legitimate and standard — sourcers invest significant time and money building relationships with estate agents, auction houses, and motivated vendors.

However, watch for overreach:

- Excessive duration: A non-circumvention period of 6–12 months post-introduction is reasonable. Clauses extending to 24 months or "in perpetuity" are aggressive and potentially unenforceable.

- Overly broad scope: The clause should apply only to specific properties introduced by the sourcer, not to entire postcodes or agent relationships the investor may already have.

- No defined introduction mechanism: A proper clause specifies how an "introduction" is documented (e.g., a written deal pack sent via email with a timestamp).

5. Confidentiality Obligations

Sourcing agreements typically contain confidentiality clauses preventing the investor from sharing deal details, vendor information, or the sourcer's proprietary methods with third parties.

NAPSA has cautioned against substituting a standalone NDA (Non-Disclosure Agreement) for a proper Terms of Business Agreement. An NDA protects information but does not define scope, fees, or obligations. It is a supplement, not a replacement.

Standard confidentiality periods run for five years post-termination of the agreement.

6. Compliance and Regulatory Declarations

A compliant property sourcing agreement UK should contain explicit declarations from the sourcer confirming:

- Registration with a property redress scheme (TPO or PRS).

- HMRC registration for Anti-Money Laundering supervision.

- Professional indemnity insurance coverage.

- ICO (Information Commissioner's Office) registration for data protection.

If these declarations are absent, the investor should request evidence before signing. A sourcer who cannot produce these documents is likely non-compliant, which creates risk for the investor — particularly if a transaction goes wrong and there is no formal complaints escalation path.

7. Property Due Diligence Responsibilities

This clause allocates responsibility for verifying the investment opportunity. Critical questions include:

- Who commissions the survey? The sourcer may provide a basic investment appraisal, but the investor should always commission their own RICS survey.

- Who verifies title? The investor's solicitor handles this, but the sourcer should flag any known issues (restrictive covenants, planning conditions, leasehold complications).

- Who is responsible if the deal numbers are wrong? Most sourcing agreements include a disclaimer stating that projections are estimates, not guarantees. This is reasonable — but the sourcer should be liable if they knowingly misrepresent material facts (e.g., fabricating rental comparables or concealing structural issues they were aware of).

8. Termination Clause

Both parties should have a clear exit route. A well-drafted termination clause covers:

- Investor termination: The investor can terminate with written notice (typically 14–30 days), subject to any fees already earned for deals in progress.

- Sourcer termination: The sourcer can terminate if the investor fails to respond within a reasonable timeframe, provides inaccurate investment criteria, or engages in abusive behaviour.

- Automatic termination: The agreement expires after a defined period (e.g., 12 months) unless renewed in writing.

- Post-termination obligations: Fees for deals introduced before termination but completing after it remain payable.

9. Force Majeure

This clause excuses performance failures caused by events beyond either party's reasonable control — pandemic restrictions, legislative changes, banking system failures, or natural disasters.

Without a Force Majeure clause, a sourcer who cannot deliver due to a market-wide event (such as the stamp duty surcharge introduced at short notice) remains technically in breach. Similarly, an investor who cannot complete because their mortgage offer is withdrawn due to regulatory changes would still owe the completion fee.

10. Dispute Resolution

Litigation is expensive and slow. A well-drafted agreement should specify a dispute resolution escalation:

- Informal negotiation — 14 days for the parties to resolve directly.

- Mediation — Through a recognised body such as CEDR (Centre for Effective Dispute Resolution).

- Complaint to redress scheme — If the sourcer is TPO or PRS registered, the investor can escalate for free.

- Arbitration or court proceedings — As a last resort, governed by English and Welsh law.

11. Client Money Protection

If the sourcer holds deposits, reservation fees, or any other investor funds, the agreement must specify:

- Funds are held in a separate designated client account, ring-fenced from the sourcer's operational funds.

- The sourcer has client money protection insurance or membership of a client money protection scheme.

- The conditions under which funds are released to the sourcer (typically only upon a defined trigger, such as legal completion).

This is non-negotiable. A sourcer who commingles client funds with their own bank account is breaching regulatory requirements and creating a direct risk that the investor's money is lost if the sourcer becomes insolvent.

12. Data Protection and GDPR

The agreement should include a privacy notice explaining how the investor's personal data will be processed, stored, and shared. Under UK GDPR, the sourcer is a data controller and must:

- Identify the lawful basis for processing (typically "legitimate interest" or "performance of a contract").

- Specify data retention periods.

- Outline the investor's rights (access, rectification, erasure, portability).

The Option Agreement: A Sourcer's Secret Weapon

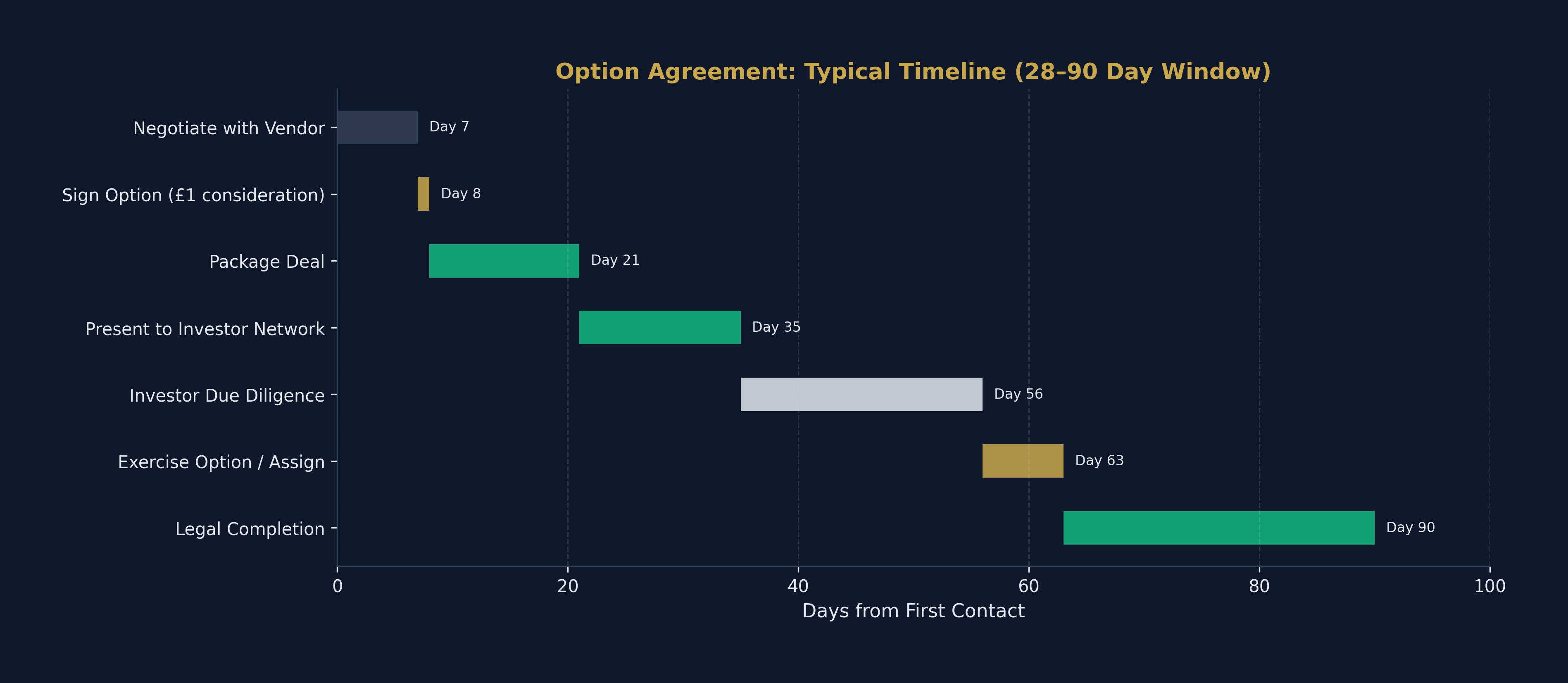

An option agreement property sourcing arrangement is a distinct but related contract used by sophisticated sourcers who deal directly with vendors.

Here is how it works: the sourcer negotiates a purchase price with a motivated seller and pays a nominal consideration (often just £1) to secure an option to purchase (or to assign the right to purchase) within a defined period — typically 28 to 90 days. The sourcer then packages the deal and presents it to their investor network. If an investor proceeds, the sourcer assigns the option or directs the purchase, earning their fee from the margin between the option price and the investor's purchase price, or through a separate sourcing fee.

Key clauses in an option agreement:

- Option period: The window during which the sourcer can exercise or assign the option.

- Consideration: The nominal amount paid to the vendor to secure the option. This must be genuine consideration to create a binding contract.

- Assignment rights: The sourcer must have explicit permission to assign the option to a third party (the investor). Without this, the option is personal to the sourcer and cannot be transferred.

- Vendor warranties: The vendor warrants they have legal title, the property is free from undisclosed encumbrances, and they will not market the property elsewhere during the option period.

Option agreements are powerful but carry risk. If the sourcer fails to find an investor within the option period, the consideration is lost (though typically minimal). If the vendor breaches the option by selling to someone else, the sourcer's remedy is typically limited to the return of their consideration plus damages — which can be difficult to quantify.

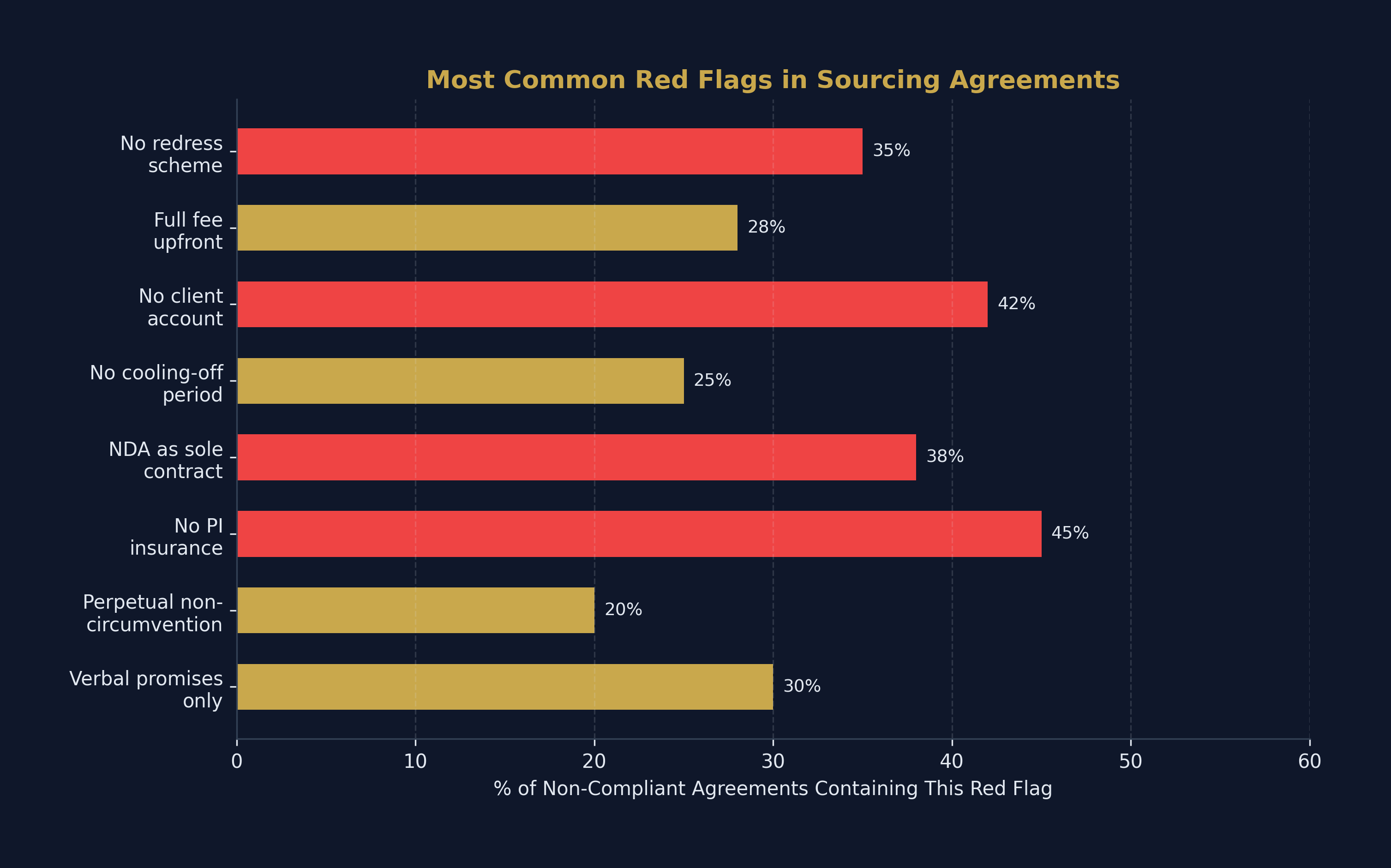

Red Flags: When to Walk Away

Not every sourcer is compliant, competent, or honest. Here are the red flags that should trigger an immediate pause — or a permanent walkaway:

Financial Red Flags

- Full fee demanded upfront with no cooling-off period or escrow protection.

- No separate client account — fees paid directly into the sourcer's personal or trading account.

- Fee significantly above market rate (more than 5% of purchase price for a standard single-let deal) without justifiable added value.

- No written refund policy or a policy that effectively makes all fees non-refundable under any circumstances.

Compliance Red Flags

- No redress scheme membership — if they are not TPO or PRS registered, they may be operating unlawfully.

- No AML registration — ask for their HMRC AML supervision number.

- No professional indemnity insurance — if the deal goes wrong due to sourcer negligence, there is no insurance to claim against.

- Refusal to provide compliance documentation when asked directly.

Contractual Red Flags

- NDA presented as the entire agreement — an NDA is not a Terms of Business. If a sourcer asks you to sign only an NDA before presenting deals, they likely do not have proper contracts in place.

- No termination clause or a clause requiring 12+ months' notice.

- Perpetual non-circumvention — enforceable clauses have a reasonable time limit.

- No Force Majeure clause — leaving both parties exposed to events beyond their control.

- Verbal promises not reflected in writing — if the sourcer says "we guarantee 20% BMV" on a call but the agreement says "estimates only", the written terms prevail.

Behavioural Red Flags

- Pressure to sign immediately — "this deal won't last" or "we need your reservation fee today." A legitimate sourcer allows time for review.

- Reluctance to allow legal review — any sourcer who discourages you from having a solicitor review the agreement is protecting themselves, not you.

- No track record or references — ask for case studies, completed deal examples, and investor testimonials. Verify independently.

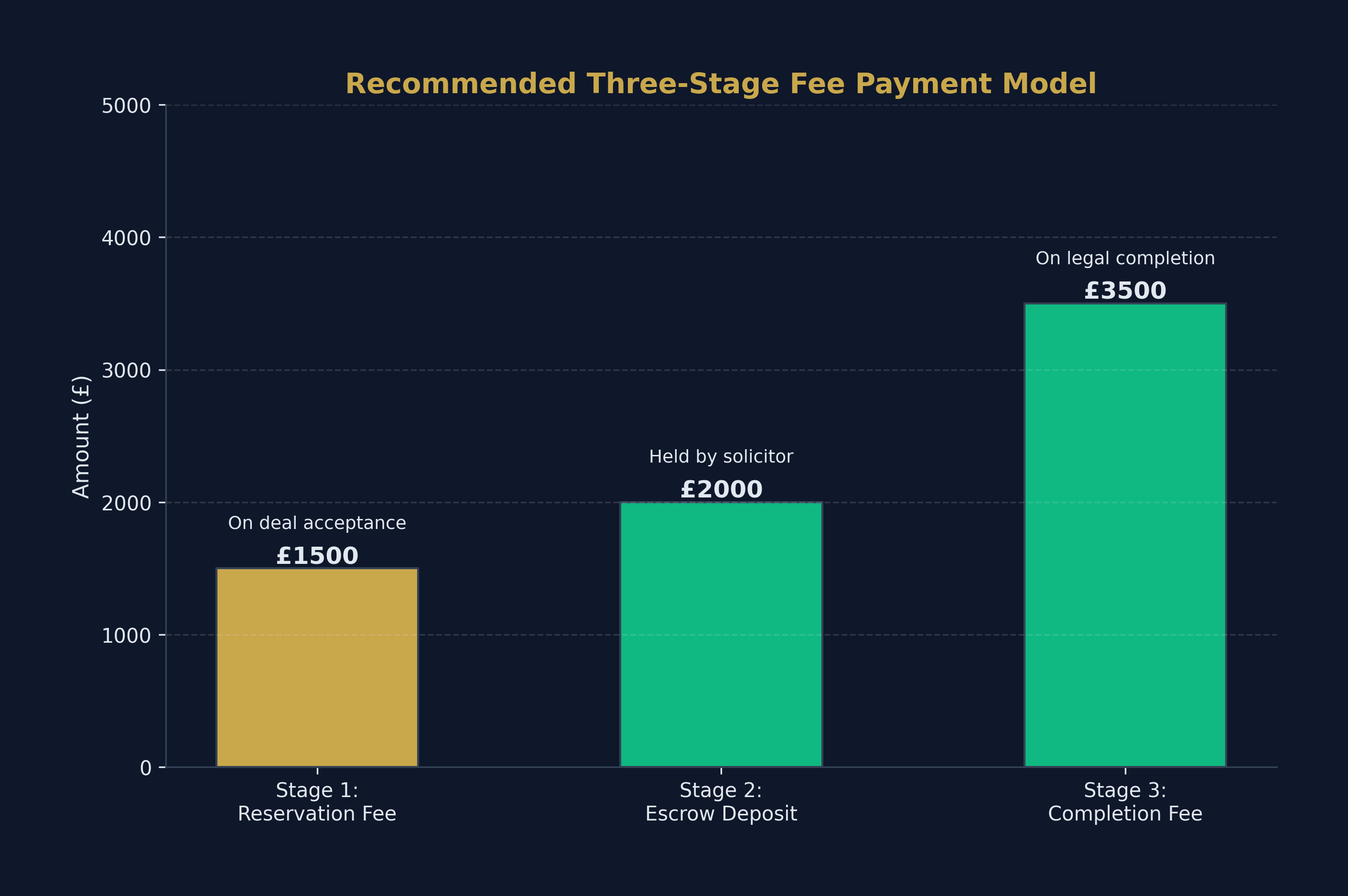

Fee Payment Timing: Getting It Right

The timing of fee payments is one of the most contentious areas in property sourcing. Here is the structure that best protects both parties:

The Three-Stage Payment Model

Stage 1: Reservation Fee (£500–£2,000) Paid when the investor formally accepts a deal and the sourcer takes the property off their list for other investors. This fee compensates the sourcer for their time and opportunity cost. It is typically non-refundable if the investor withdraws without legitimate cause, but refundable if the deal falls through due to factors outside the investor's control (e.g., failed survey, title issues, mortgage declined).

Stage 2: Exchange Deposit (Held in Escrow) If the sourcer requires a larger payment before completion, this should be held in a regulated escrow account or the investor's solicitor's client account — never in the sourcer's own account. Release conditions must be explicit in the agreement.

Stage 3: Completion Fee (Balance) The remaining fee is payable upon legal completion of the property purchase. This is the safest trigger for the bulk of the fee because it aligns incentives — the sourcer only receives the majority of their payment when the investor actually acquires the asset.

Escrow Best Practices

Escrow provides a critical layer of protection, particularly for larger fees or when dealing with a sourcer for the first time:

- Use a regulated escrow provider or hold funds with the investor's solicitor.

- Define explicit release conditions in writing — "funds released upon legal completion" is clearer than "funds released upon deal conclusion."

- Specify what happens in a dispute scenario — if the parties disagree on whether the release conditions are met, who decides? The escrow agreement should nominate an independent adjudicator.

- Factor in AML checks — regulated escrow agents will require ID verification and source of funds documentation. Plan for this to avoid delays on fast-moving deals.

Sample Agreement Structure

Below is a practical structure for a compliant property sourcing agreement UK. This is not legal advice — always have your agreement reviewed by a qualified solicitor — but it provides a benchmark against which to evaluate any contract presented to you.

| Section | Content |

|---|---|

| 1. Parties | Full legal names, registered addresses, company numbers (if applicable) |

| 2. Definitions | Key terms: "Property," "Deal Pack," "Completion," "Introduction," "Fee" |

| 3. Scope of Services | Detailed description of what the sourcer will deliver |

| 4. Investment Criteria | Investor's requirements (type, location, budget, yield target) |

| 5. Fees and Payment | Fee structure, payment triggers, VAT treatment |

| 6. Cooling-Off Period | 14-day statutory right for distance contracts |

| 7. Client Money Protection | Separate client account details, release conditions |

| 8. Exclusivity & Non-Circumvention | Duration, scope, introduction mechanism |

| 9. Confidentiality | Obligations, duration, exceptions |

| 10. Due Diligence Responsibilities | Allocation between sourcer and investor |

| 11. Compliance Declarations | Redress scheme, AML, PI insurance, ICO |

| 12. Limitation of Liability | Cap on liability, exclusion of consequential losses |

| 13. Force Majeure | Defined events, notice requirements, consequences |

| 14. Termination | Grounds, notice period, post-termination obligations |

| 15. Dispute Resolution | Escalation procedure (negotiation → mediation → redress → court) |

| 16. Data Protection | GDPR privacy notice, lawful basis, retention periods |

| 17. Governing Law | Laws of England and Wales |

| 18. Signatures | Dated signatures of both parties |

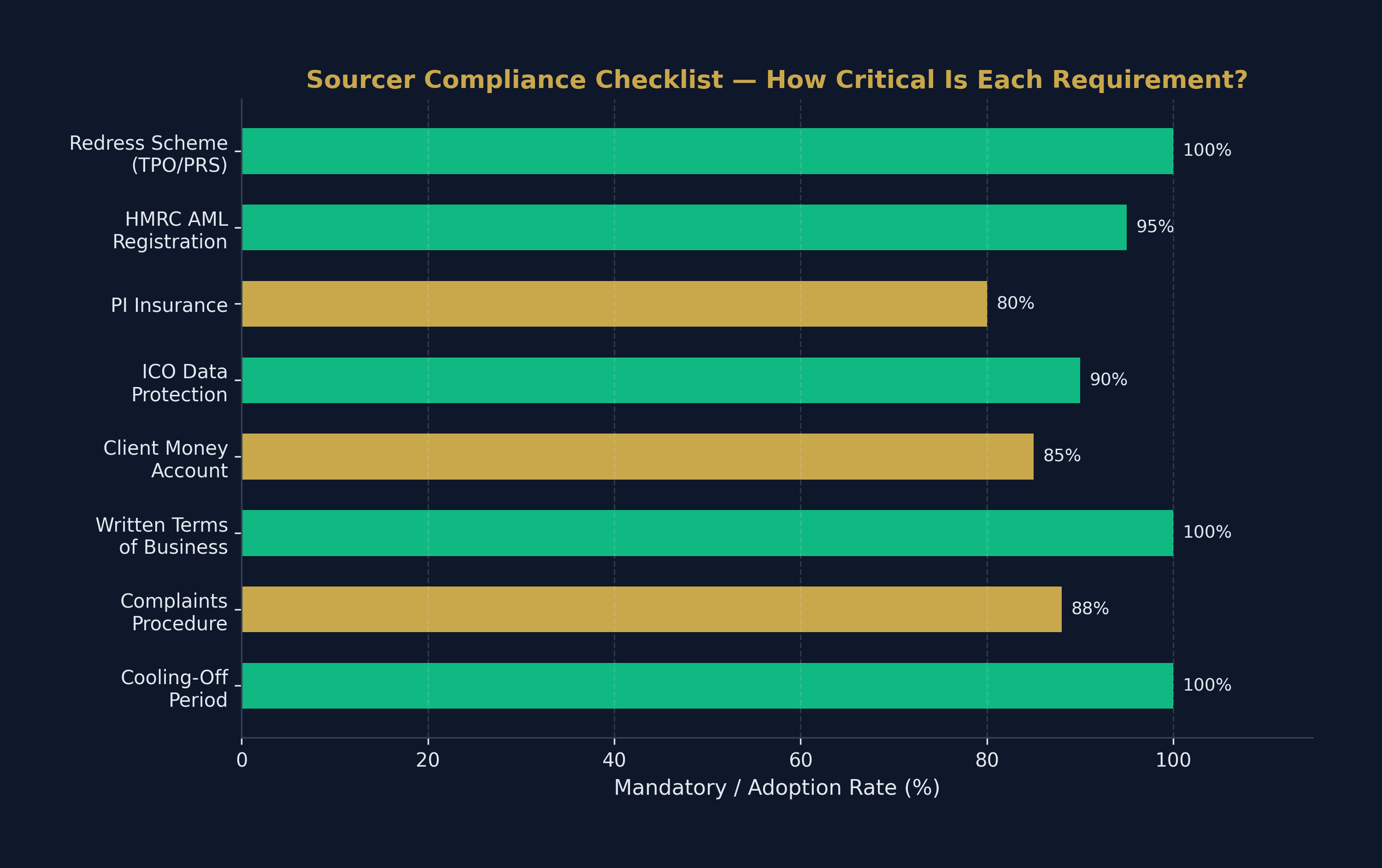

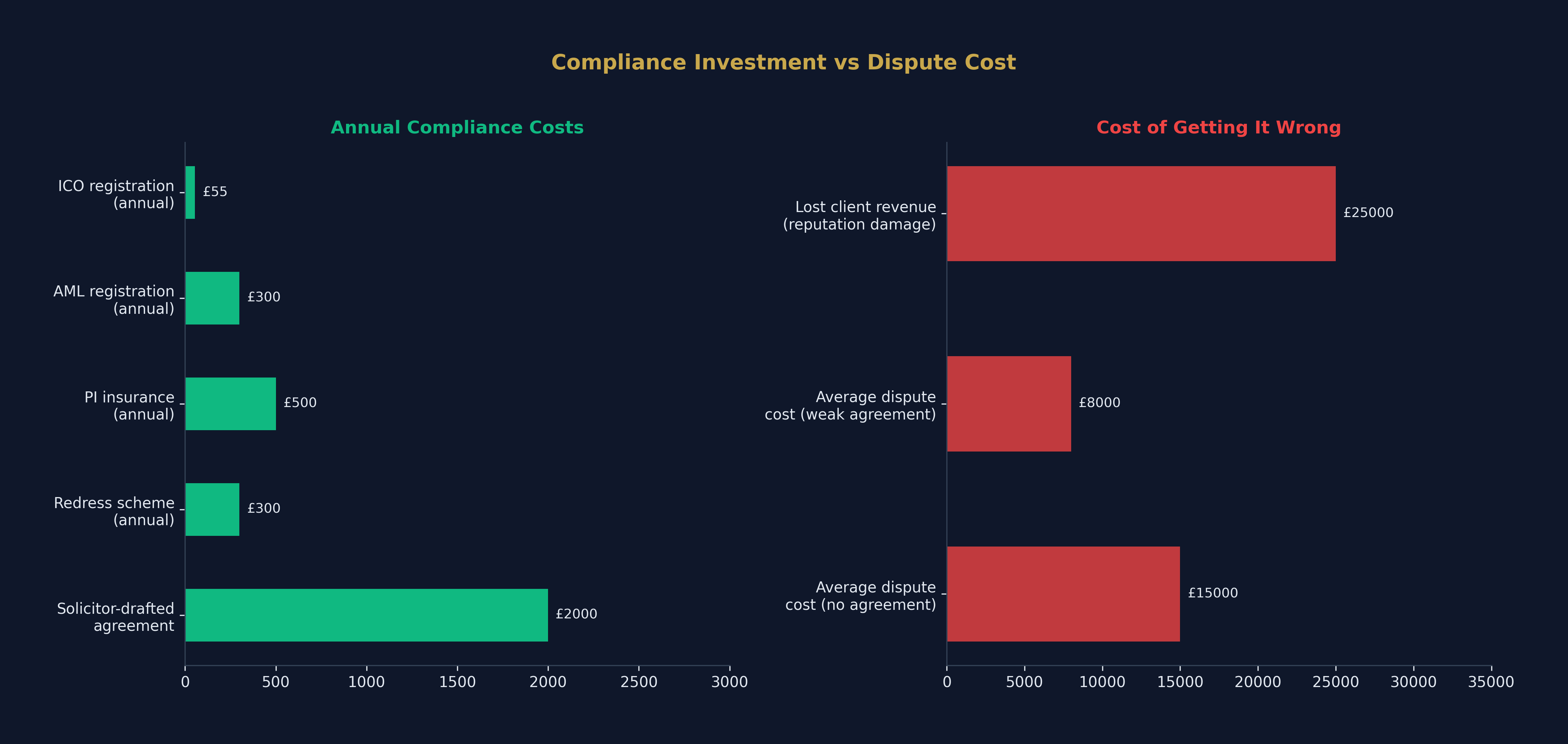

Sourcer Compliance Checklist for 2026

If you are setting up or reviewing a property sourcing business, this is the minimum compliance baseline as of April 2026:

| Requirement | Status Needed |

|---|---|

| Property Redress Scheme Membership (TPO or PRS) | Mandatory |

| HMRC Anti-Money Laundering Registration | Mandatory if handling client funds |

| Professional Indemnity Insurance | Strongly recommended (effectively mandatory for NAPSA members) |

| ICO Data Protection Registration | Mandatory |

| Separate Client Money Account | Mandatory if holding investor funds |

| Written Terms of Business / Sourcing Agreement | Mandatory under Estate Agency Act |

| Complaints Handling Procedure | Mandatory under redress scheme rules |

| Consumer Contracts Regulations compliance (cooling-off period) | Mandatory for distance contracts |

NAPSA members undergo in-depth compliance checks against these national minimum standards. While NAPSA membership is not a legal requirement, it provides a credible signal to investors that the sourcer operates within recognised professional boundaries.

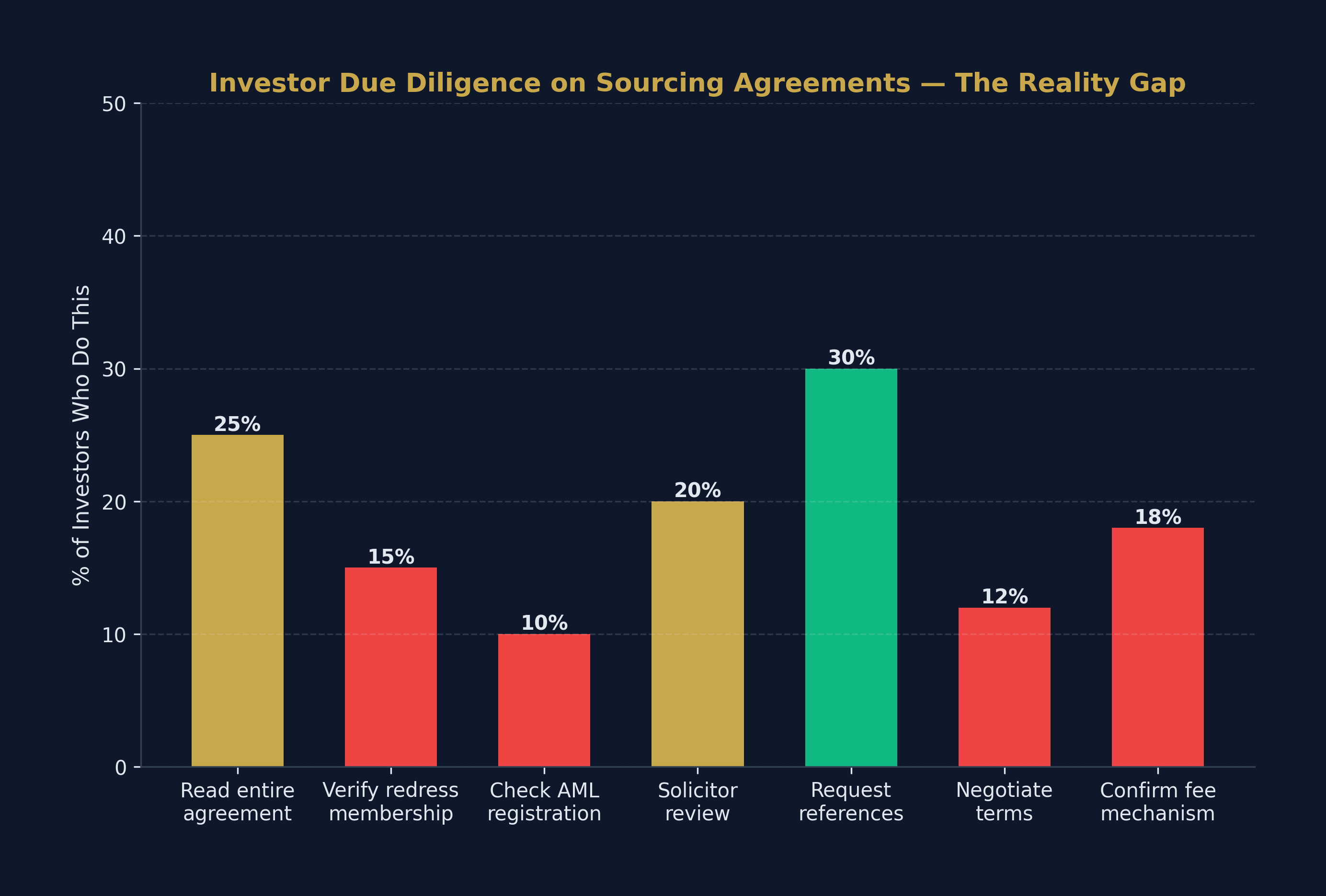

What Investors Should Do Before Signing

- Read the entire agreement. Not a skim — a line-by-line read. Flag anything you do not understand.

- Verify compliance credentials. Check TPO/PRS membership online. Ask for the HMRC AML supervision number. Request a copy of the PI insurance certificate.

- Have a solicitor review the agreement. A one-hour review costing £200–£400 can save you thousands in disputes.

- Ask for references. Speak to at least two previous investors. Verify that deals completed, timelines were met, and fees matched what was agreed.

- Negotiate. Sourcing agreements are not take-it-or-leave-it documents. Fee structures, non-circumvention periods, and service scope are all negotiable.

- Confirm the fee payment mechanism. Understand exactly when money leaves your account and where it goes. If it is not going into a client account or escrow, reconsider.

- Keep a paper trail. Every communication (email, WhatsApp, call notes) relating to the deal should be saved. If a verbal promise is not in the agreement, ask for it to be added.

What Sourcers Should Do to Protect Their Business

- Invest in a professionally drafted Terms of Business. This is your commercial backbone. A solicitor specialising in property or consumer law can draft a robust agreement for £1,000–£2,500 — a fraction of what a single dispute will cost.

- Register with a redress scheme. TPO and PRS both accept property sourcing agents. Non-registration exposes you to enforcement action and makes your contracts less enforceable.

- Document every introduction. Timestamp deal packs, use read receipts, and maintain a CRM log. If a non-circumvention dispute arises, your evidence must be watertight.

- Separate your accounts. Open a dedicated client money account on day one. Commingling funds is the fastest route to regulatory trouble and investor distrust.

- Get insured. Professional indemnity insurance covers you if an investor suffers a loss due to your negligence or error. Premiums for property sourcers typically start at £300–£600 per year.

- Join a professional body. NAPSA membership signals credibility and provides access to compliant templates, training, and a network of vetted professionals.

The Brutal Truth About Property Sourcing Agreements

The property sourcing industry in the UK operates in a regulatory grey zone. It is legal, but it is under-regulated compared to estate agency, financial advice, or conveyancing. This means the quality of sourcing agreements varies wildly — from institutional-grade contracts backed by compliance teams, to single-page PDFs knocked together in Canva.

As an investor, your property sourcing agreement is the only document standing between your capital and a sourcer's promises. If that document is weak, ambiguous, or non-compliant, you have no protection when things go wrong. And in property, things go wrong regularly — vendors pull out, valuations disappoint, mortgage offers collapse, and refurbishment budgets overrun.

As a sourcer, your agreement is simultaneously your revenue protection, your liability shield, and your professional credibility. Every clause you omit is a vulnerability. Every red flag you ignore is a dispute waiting to happen.

Get the agreement right, and property sourcing is one of the most efficient routes into UK property investment. Get it wrong, and it is an expensive lesson in why contracts matter.

Stop being a landlord. Start being an investor.

Shaded Canvas introduces serious capital to vetted UK property opportunities — targeting 12–16% net returns.

Start Investing →