"I want to make money in property."

That is not a business plan. That is a wish.

In 2026, the "accidental landlord" is an endangered species. With mortgage rates hovering around 5%, Section 24 taxes eating profits, and regulation tightening, the days of buying a random house and hoping for the best are over.

If you want to survive—and thrive—you need to treat property like what it is: a business. And every serious business needs a plan.

Whether you are seeking £100k angel investment or just trying to convince your spouse to remortgage the family home, this guide will help you build a bulletproof Property Investment Business Plan.

Why You Need a Plan (The "Why")

You wouldn't start a tech company without a plan. Why treat a £200,000 asset differently?

1. Verification for Lenders

Commercial lenders (especially for Ltd Company mortgages) want to see that you are a serious operator. A solid business plan can be the difference between a "Yes" and a "No," or even secure you a better rate.

2. Attracting Joint Venture (JV) Partners

Trying to raise private finance? An investor will not give you £50,000 based on a handshake. They want to see your strategy, your numbers, and your exit plan. A professional document screams competence.

3. Avoiding "Shiny Object Syndrome"

Property is full of distractions. One minute you're looking at HMOs in Stoke, the next you're tempted by a Serviced Accommodation course in Dubai. Your plan is your anchor. If a deal doesn't fit the plan, you don't do it.

Section 1: The Executive Summary

Write this last, but put it first.

This is your elevator pitch. It should be one page maximum.

What to include:

- Mission: e.g., "To build a portfolio of high-yielding HMOs in the North West for long-term cash flow."

- The "Why": e.g., "To replace my £50k corporate salary within 36 months."

- The Goal: e.g., "Acquire 5 properties in 3 years with a total GdV (Gross Development Value) of £1m and net cash flow of £3,500/month."

Section 2: Core Strategy (The "What")

Pick a lane. You cannot be an expert in everything.

1. Vanilla Buy-to-Let (BTL)

- Focus: Single lets (houses/flats).

- Pros: Passive, easy to finance, easy to exit.

- Cons: Low cash flow (£200-£300/month per unit).

- Best For: Wealth preservation / Retirement planning.

2. HMOs (Houses in Multiple Occupation)

- Focus: Renting by the room (Students/Professionals).

- Pros: High cash flow (£800+/month per unit).

- Cons: High effort, strict regulation (licensing/Article 4), higher utility bills.

- Best For: Income replacement.

3. BRRR (Buy, Refurbish, Refinance, Rent)

- Focus: Buying dilapidated property, adding value, pulling cash out.

- Pros: Infinite ROI potential (recycling your deposit).

- Cons: High risk, high stress, requires reliable builders.

- Best For: Aggressive portfolio growth.

Decision Matrix: Be honest with yourself. If you have a demanding full-time job, BRRR might break you. If you have no cash, vanilla BTL won't scale.

Section 3: Market Analysis (The "Where")

Don't just say "The North." You need to be specific. Pick a "Goldmine Area."

My Target Area: [Insert Town/City] e.g., Stoke-on-Trent (ST4 Postcode)

Why this area?

- Yield: Average yields are 7% (vs 3.5% national average).

- Demand: Home to Staffordshire University (15,000 students) and Royal Stoke Hospital (largest local employer).

- Regeneration: £40m "Levelling Up" fund secured for town centre improvements.

Tenant Profile

- Who is your customer? e.g., "Medical professionals and mature students."

- Does your product match them? e.g., "We will provide high-end, ensuite rooms with strong WiFi and desks."

Section 4: The Financial Plan (The "How")

This is the section that matters most.

1. Startup Costs

List everything you need to get the first deal done.

- Deposit: £25k (25% of £100k house)

- Stamp Duty: £3k (3% surcharge included)

- Legal Fees: £1.5k

- Sourcing Fee: £3k (if applicable)

- Refurbishment: £10k

Total Initial Investment: £42.5k

2. Operating Costs (The Stress Test)

Can you survive if rates go up?

- Mortgage: Stress test at 6% interest (not the current 4.5%).

- Maintenance: Allow 10% of gross rent.

- Voids: Allow 1 month per year (8%).

- Management: Allow 12% + VAT for a letting agent.

Net Profit Calculation:

- Gross Rent: £12,000/year (4 rooms @ £250/m)

- Minus Expenses: £6,000 (Mortgage + Costs)

- Net Profit: £6,000/year (£500/month)

3. Exit Strategy

Always know how you get out.

- Plan A: Hold for 20 years for pension income.

- Plan B: Sell to another investor as a turnkey investment if capital is needed.

- Plan C: Refinance in 5 years to release equity.

Section 5: The Power Team (The "Who")

You are the CEO. You need staff (even if they are outsourced).

- Mortgage Broker: Whole-of-market specialist (not your bank manager).

- Solicitor: Property specialist (not the guy who did your divorce).

- Builder/Handyman: Reliable, vetted, and available.

- Letting Agent: ARLA regulated, local expert.

- Accountant: Property tax specialist (knows Section 24 inside out).

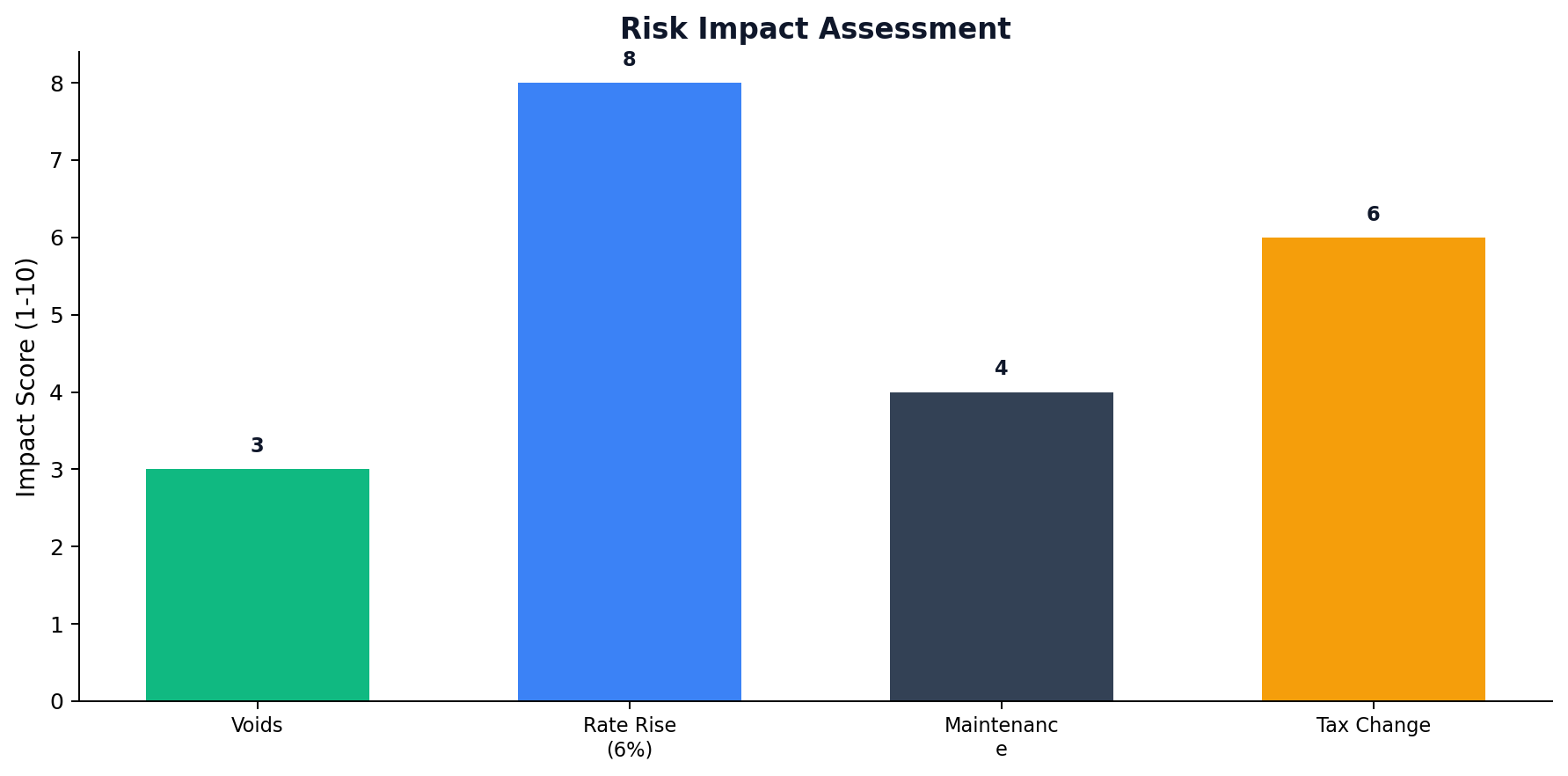

Section 6: SWOT Analysis (Honesty Time)

Strengths:

- I have £50k cash savings ready to deploy.

- I have a good credit score (excellent mortgage eligibility).

Weaknesses:

- I have zero refurbishment experience.

- I work 9-5 and cannot manage renovations myself.

Opportunities:

- Market uncertainty is creating distressed sellers (motivated to sell quickly).

- Rents are rising faster than inflation in my target area.

Threats:

- Interest rates could rise to 6%+, squeezing cash flow.

- Labour government could introduce rent controls or tougher EPC rules.

Call to Action: Start Your Plan Today

Don't overcomplicate it. A 2-page plan executed well is better than a 50-page plan that sits in a drawer.

Action Steps:

- Define your goal (Cash flow or Capital Growth?).

- Pick your area (Where do the numbers stack?).

- Run the numbers (Stress test at 6%).

- Build your team (Find a broker first).

Your property business starts the moment you write this plan. Good luck.

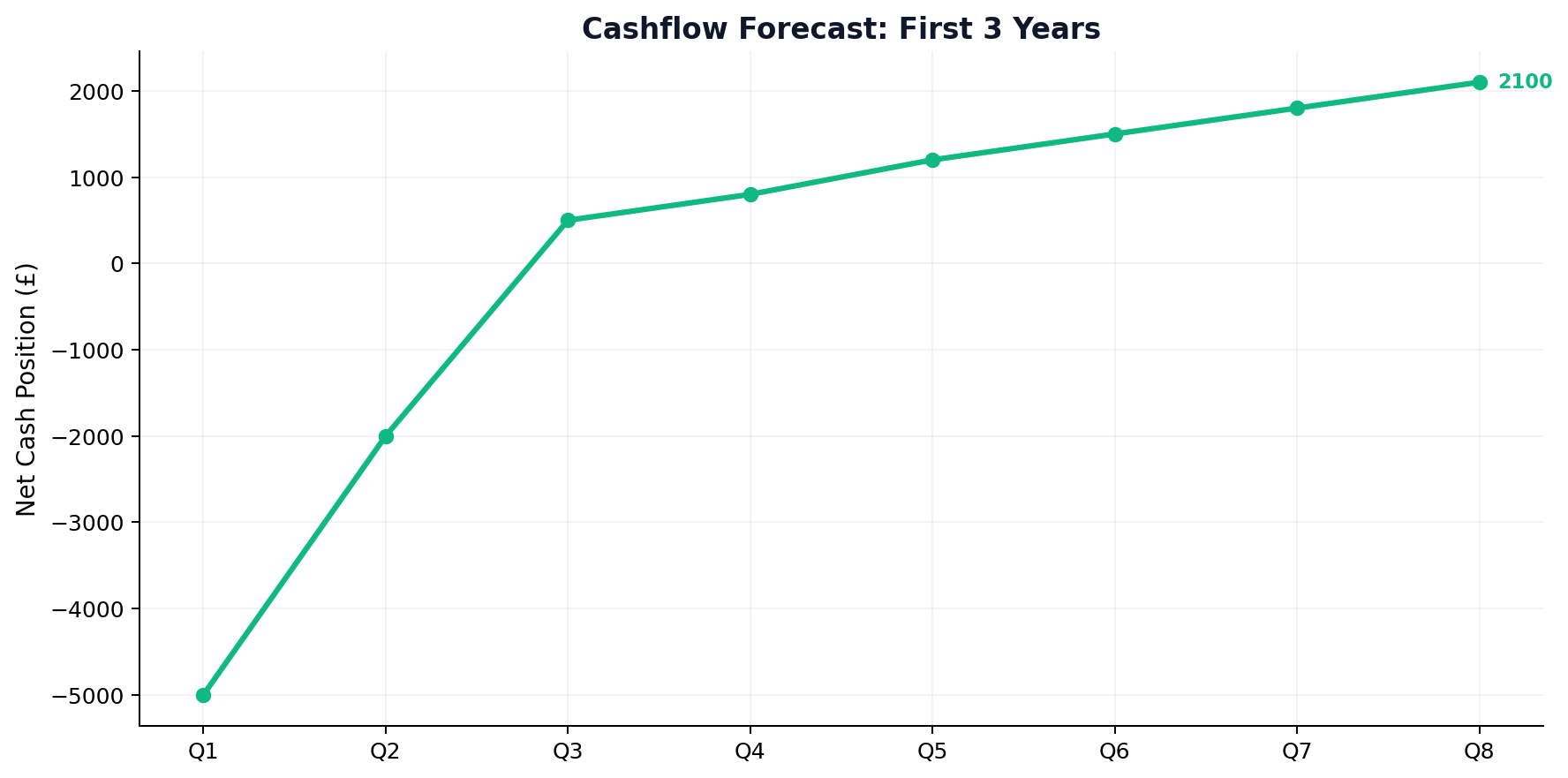

Figure: Cashflow Forecast 3 Years

Figure: Cashflow Forecast 3 Years

Figure: Risk Impact Assessment

Figure: Risk Impact Assessment

Stop being a landlord. Start being an investor.

Shaded Canvas introduces serious capital to vetted UK property opportunities — targeting 12–16% net returns.

Start Investing →